Aadhaar, India’s unique identification system, has become essential for identity verification and service delivery, significantly impacting the lives of over 1.4 billion people since its inception in 2009. It is crucial in social welfare, financial inclusion, and digital governance. Aadhaar’s biometric authentication, including fingerprint, iris, and face recognition, ensures uniqueness, reduces fraud, and improves service delivery.

Initially, Aadhaar used fingerprint authentication, which proved cost-effective and widely accessible. However, environmental factors, age, and manual labor sometimes affected its reliability, leading to the introduction of iris authentication. Iris scans provided high accuracy and were particularly useful for individuals with hard-to-capture fingerprints, though they required specialized handling.

In 2018, the UIDAI introduced face authentication, which enhanced inclusivity, particularly for the elderly and disabled. With an accuracy rate of 84%, face authentication quickly gained popularity due to its contactless nature and ease of use via smartphones. Today, it supports over 55 million transactions monthly and is used for KYC processes, improving the customer experience across sectors, including banking, government services, and travel.

This playbook is a reference guide that will help introduce audiences to face authentication as a modality and provide an overview of its adoption along with prevalent use cases.

Kishan, a farmer from northern India, met with an insurance agent and purchased an endowment plan – a type of life insurance policy that pays the full sum assured to beneficiaries if the insured dies during the policy term, or provides the sum assured upon maturity if the policyholder survives the term. The insurance agent talked up the potential returns and assured Kishan that the premium payments would be manageable within his budget. Kishan trusted the agent and signed the insurance form without fully understanding the implications of the premium payments. Over time, he struggled to meet the premiums. After three years, he finally surrendered the policy, hoping to salvage some value. To his dismay, he discovered that he could not recover even half of what he had paid in premiums.

Kishan’s case highlights systemic issues of information asymmetry and mis-selling in insurance, where sellers misrepresent crucial details, leaving vulnerable individuals financially exploited.

Widespread mis-selling of insurance plans

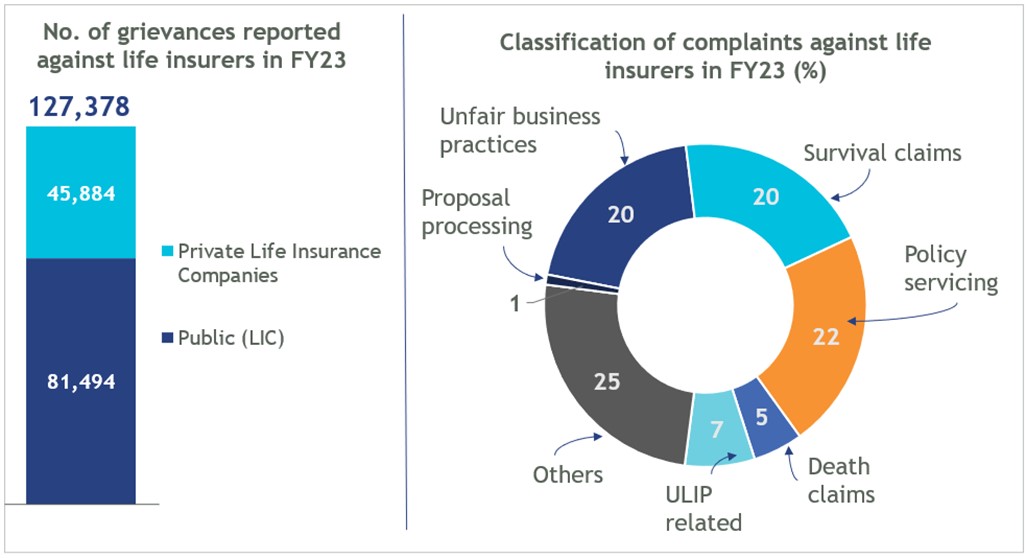

Insurance-related mis-selling is rampant in India and, we suspect, in many other developing countries as well. As per the Council for Insurance Ombudsmen’s Annual Report 2022-23, mis-selling-related grievances for life insurance accounted for 58% of the total entertainable complaints of the year. Further, in 2022-23, the Insurance Regulatory and Development Authority of India (IRDAI) received around 124,000 complaints against life insurance providers, with 20% related to unfair business practices.

Sales agents often employ pressure tactics and push life insurance plans that offer poor returns and inadequate insurance coverage despite high premiums. They tend to make this push without a thorough understanding of the customer’s needs. To make matters worse, opaque policy terms and complex fine print from insurers, along with misrepresentation or omission of critical information by insurance agents, create confusion and potential pitfalls for customers.

Agent incentives don’t match customer needs

Higher commissions lure some agents into such tactics. Commission levels are set by insurance companies, within the IRDAI regulatory framework, as a percentage of the premium paid by policyholders. Therefore, agents often try to sell endowment policies with higher premium rates in order to get the higher commissions. Additionally, agents receive significantly higher commissions from the first-year premium compared to subsequent years. To maximize their earnings, some agents encourage policyholders to prematurely surrender existing policies and sign up for new ones, thus earning another first-year commission. This practice, known as churning, burdens customers with surrender costs they are often unaware of.

Under current IRDAI regulations, a policyholder who surrenders a policy early receives a surrender value much lower than the total premiums paid. For example, if a policyholder surrenders in the second year, she receives only 30% of the premiums paid up to that year, bearing a surrender cost of 70%.

Unethical practices like churning, concealing surrender costs and pushing high-premium, low-return plans, stem from agents’ incentives tied to the high first-year commissions. The gain for the agents contrasts with the loss to the policyholders, who are at a disadvantage due to lack of transparency around surrender values and costs.

Diminishing consumer trust in insurance agents

Individuals like Kishan buy insurance expecting financial protection. Rural customers tend to trust sales agents and rely on them as the primary channel for purchasing insurance. However, this reliance can be concerning when combined with a low level of awareness of consumer risks in insurance. Most low-income customers are unable to discern unfair sales and marketing tactics used by agents, exacerbating their vulnerability. Without clear information about costs, premiums and surrender policies, these clients face increased financial risks, diminishing their trust in insurance and driving negative word-of-mouth publicity for the entire insurance industry.

“It is better to invest money in a fixed deposit than to purchase insurance,” said Kishan, when he cited his experience of low returns and poor customer support from a private insurance company.

Call to action

Regulators and providers must enhance customer protection in the insurance industry. Transparent practices, ethical sales tactics and responsive customer support are essential to build trust, protect customers and sustain the insurance industry’s growth. Here are some strategies that can be implemented:

1) Enhance monitoring and auditing: Customers are overreliant on agents when they purchase insurance, so regulators and providers should ensure regular audits and compliance checks to ensure adherence to regulatory standards. Although the IRDAI has established a code of conduct for insurance agents and intermediaries, its compliance should be monitored. Insurers should be mandated to monitor sales patterns, analyze complaints and detect mis-selling. The regulator will need to take corrective action against insurers found violating norms.

2) Standardize policy information: Policy documents are complex, lengthy and filled with jargon, making them difficult for people to understand. This leads to widespread information asymmetry. Insurance companies should share key information on premiums, surrender values, exclusions, claim rates, customer support and more in standardized, user-friendly templates. These should accomodate language preferences, communication modes and intuitive design for clarity and accessibility.

The infographic below illustrates a comprehensive insurance policy document’s key features alongside a standardized insurance policy summary template. This template is designed to simplify and clarify the key components of an insurance product. It includes section headers per the Insurance Distribution Directive’s recommendation and color-coded icons for easy navigation.

3) Balance customer interests: Most Indian life insurance companies opposed a 2023 draft proposal which would have set a limit on policy surrender charges. The IRDAI’s recent decision to scrap this proposal benefits the insurance companies but not the customers. High surrender charges can be perceived as a tactic to lock in policyholders, eroding public trust in the insurance industry. Therefore, the regulator must allow some flexibility to balance the interests of both insurers and policyholders.

4) Promote customer support and grievance resolution channels: Although the IRDAI has developed an integrated grievance management system (IGMS) to handle and resolve complaints efficiently, customer awareness of this system remains limited. Customers rely on their agents to register grievances, thus depending on the very people who may have mis-sold policies in the first place. This process delays resolution. Therefore, the IRDAI should widely promote IGMS and push insurers to speed up claim resolution and response times.

5) Enhance customer understanding of insurance through gamification:Gamification can simplify complex subjects, and makes learning about insurance policies, policy types, benefits and conditions engaging by integrating quizzes, story-based adventures, role-playing and virtual simulations. This approach helps customer retain information better, ultimately empowering them to make informed decisions while enjoying the process.

Insurance providers can incorporate gamification into their mobile apps, enabling customers with smartphones to learn independently. For low-income customers without smartphones, internet access or technical proficiency, insurance agents can guide them through gamified modules and offline resources during in-person consultations. Additionally, SMS can be used to deliver quizzes, tips and educational content.

Protecting insurance customers is increasingly important as risks and complaints are rising. These steps will lead to better financial outcomes, reduced distress, and a more responsive, competitive insurance industry. We can empower consumers to make educated decisions with robust regulatory standards and transparency.

The blog was first published on the FinDev Gateway website on 23rd August 2024.

Mary is a small trader in Nairobi who aspires to own a home one day. She earns a consistent income, yet the barriers to homeownership are daunting as the costs are high and her financing options are limited. Her modest income is sufficient to cover her daily needs but not enough to buy a home in Nairobi’s skyrocketing property market. MSC’s recent research commissioned by Habitat for Humanity International highlights that Mary’s situation is far from unique.

Like Mary, many Kenyans face hurdles when they seek access to affordable finance tailored to their needs and income levels to construct, improve, or expand their existing house. Lack of collaterals and proof of consistent income, high interest rates, upfront contribution fees, and the stringent requirement to access financing have demolished her dream of owning a home, either in Nairobi or in her rural village.

This blog addresses the challenge of designing affordable housing products for low- and moderate-income earners in Kenya, where rapid urbanization has outpaced the housing supply. Innovative financial solutions that focus on affordability and build the capacity of financial institutions are essential to serve this segment effectively. We explore new strategies to highlight how institutions can create sustainable housing products that meet the real needs of people from this segment and deliver tailored solutions to them.

The housing landscape

Kenya faces a significant housing deficit, with an annual demand of 250,000 units and a supply of only 50,000, among which 49,000 units target the upper-middle and high-end market segments. This shortfall has led to the growth of informal settlements and overcrowding in urban areas like Nairobi. High construction costs, limited access to affordable financing, and outdated building codes further complicate the situation. The Bottom-Up Economic Transformation Agenda seeks to address these challenges by prioritizing affordable housing as a key pillar. The plan intends to build 250,000 new housing units annually through government investments worth KES 50 billion (USD 386 million) and an additional KES 200 billion (USD 1.56 billion) from private investors. The goal is to increase affordable homes from 2% to 50% of total housing, expand the mortgage market from 30,000 to 1 million through low-cost mortgages, and, in turn, create jobs and boost economic growth.

However, this plan faces significant pitfalls, including the controversial housing levy that has met with public resistance, as many citizens feel overburdened by mandatory contributions. Moreover, the initiative may fail to deliver long-term solutions unless it addresses structural issues, such as land ownership challenges, outdated building codes, and high construction costs. While the plan may boost short-term construction jobs, it risks not solving the underlying housing affordability problem if financing remains inaccessible for most low- and moderate-income earners in the long run. The initiative’s success hinges on overcoming these barriers and ensuring that the financial mechanisms are truly accessible to those who need them most.

Supply-side challenges for financial institutions in housing finance

Financial institutions in Kenya face substantial hurdles when they seek to develop housing products for low- and moderate-income earners. A significant challenge is the perception that lending to this segment is risky. About 83% of Kenyans work in the informal sector. They earn irregular incomes and lack formal credit history and collateral. As a result, these informal sector workers often do not qualify for traditional mortgage products, severely limiting their access to housing finance.

According to the Central Bank of Kenya, the mortgage market faces difficulties, with a 12.5% non-performing loan (NPL) rate for mortgages. These NPLs primarily result from borrowers who, despite having formal loans, struggle to meet their repayment obligations due to various economic pressures. Housing finance remains inaccessible to many, as average mortgage interest rates range between 12% and 14%. SACCOs, which offer slightly lower rates of around 10-12%, provide some relief but struggle due to limited access to long-term capital.

High construction costs make up 50-60% of housing prices. These costs constrain financial institutions and limit them from offering affordable mortgages. Strict compliance under the Banking Act raises costs for financial institutions and holds back innovation in housing finance. In rural areas, limited digitization makes credit risk assessment difficult, while SACCOs struggle to secure long-term financing. These barriers limit their ability to offer sustainable housing loans for low-income earners.

Key strategies for affordable housing design for financial institutions

In the section below, we outline three key strategies and innovative approaches that can help financial institutions develop effective housing finance solutions:

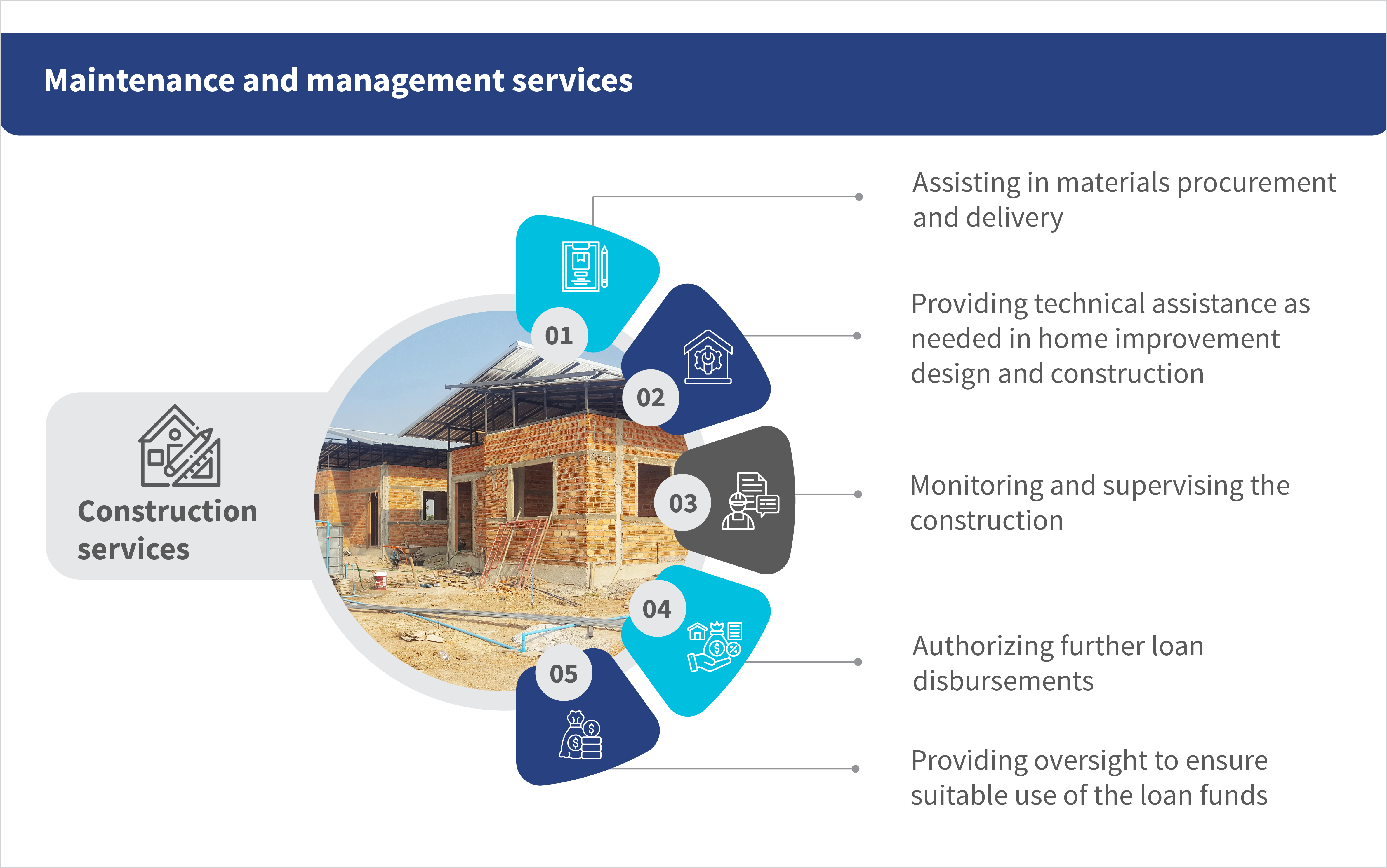

Integration of housing support services: Housing support services should be at the forefront of efforts to enable low- and moderate-income earners to access and sustain affordable housing. These services offer crucial assistance, including construction oversight, guidance on material procurement, and supervision of loan disbursements to ensure effective fund use. This comprehensive approach helps mitigate risks for financial institutions, builds trust with borrowers, and ensures housing projects remain sustainable in the long term.

Tailored financial products and innovative design approaches: Financial institutions must develop flexible housing finance products, such as micro-mortgages, income-based repayment plans, and incremental housing loans to cater to the specific needs of low- and moderate-income earners, particularly those with irregular incomes. An example is the Nyumba Smart Loan of the Kenya Women Microfinance Bank (KWFT), which has successfully expanded access to affordable housing, particularly for underserved populations and women. Incremental housing loans like the Nyumba Smart Loan allow borrowers to build homes in stages as they disburse smaller, flexible loans for each phase of construction. This phased approach reduces financial strain, aligns with cash flow, and makes homeownership more achievable for underserved groups. Alongside innovative, cost-effective housing designs, these products provide sustainable solutions that expand access to affordable housing without compromising quality or essential services.

Risk-sharing facilities (RSFs): RSFs reduce risk for borrowers through guarantees or cover potential losses, which help financial institutions lend to low- and moderate-income earners. In Kenya, the Kenya Mortgage Refinance Company (KMRC) uses RSFs to help lenders offer affordable mortgages to informal sector workers with irregular incomes, which helps reduce the cost of loans and makes them more accessible.In West Africa, the Caisse Régionale de Refinancement Hypothécaire (CRRH) provides liquidity to banks that allows them to offer lower-cost mortgages to low-income households. Loan uptake increases as a result. However, these initiatives still need more technical assistance and resources to reach a wider group of low-income earners. Currently, the Tanzania Mortgage Refinancing Company (TMRC) has partnered with two financial institutions to develop affordable housing products with support from HFHI and MSC. After the pilot phase, the TMRC plans to offer refinancing solutions to these institutions to scale the products and make housing finance more accessible to low- and moderate-income borrowers. This approach demonstrates how RSFs can enhance lender confidence and expand affordable housing opportunities.

Conclusion and recommendations

The development of housing finance products requires time and resources, which makes partnerships essential. Collaborations between FSPs, MFIs, governments, and development organizations create scalable solutions for low-income earners. Examples include partnerships, such as TMRC with HFHI and KMRC with the World Bank and IFC, which work to expand affordable housing financing. These collaborations are vital to enhance financial inclusion and build a sustainable, accessible housing market for underserved communities.

Governments should play a leading role by establishing clear regulatory frameworks and offering targeted subsidies to break down barriers to affordable housing finance. Development partners must contribute funding and technical expertise to drive innovation and ensure financial products meet the needs of low- and moderate-income earners. The KMRC can play a crucial part to create tailored refinancing strategies that address this group’s unique challenges, such as irregular incomes and limited collateral. Financial institutions, governments, and development partners must collaborate urgently to bring real progress, transform these solutions, and close the housing finance gap. Now is the time to build a sustainable, affordable housing market that truly includes the underserved.

Can we build household resilience among the unhoused without accelerating climate change?

MSC supported Habitat for Humanity’srecentstudies. The findings revealed a substantial unmet demand for affordable housing across Africa. The research revealed a deficit of 2 million units in Kenya and more than 1.5 million units in Zambia. These numbers illustrate a continent-wide challenge. The growing impacts of climate change further exacerbate this issue. They lead to intensified poverty and increasingly unaffordable housing. Frequent climate-related shocks have damaged existing housing infrastructure, and the strategies that informal settlements have relied on have failed under environmental change pressures.

The building sector generates 37% of energy-related greenhouse gas emissions, a significant contribution largely due to conventional methods that rely heavily on fossil fuels. These conventional methods include the use of energy-intensive materials such as concrete and steel, inefficient heating and cooling systems, and poor insulation, which lead to excessive energy consumption and higher emissions. In many urban areas, especially in developing regions, substandard buildings are often constructed with inadequate materials, and poor design, which makes them vulnerable to climate impacts, such as extreme weather events and rising temperatures. The situation will worsen if we continue to address housing needs through conventional methods and increase the demand for energy as global temperatures rise. As we work toward the provision of affordable housing, we must recognize that conventional approaches will likely aggravate the climate crisis. Two things become clear: We must address the housing deficit and ensure it is sustainable and resilient against climate impacts.

Although green homes offer a solution, their construction is often expensive for most households. Additionally, the government will need to increase its spending on green homes. Thus, we must focus on innovative solutions that balance affordability with sustainability to address these challenges. Green financing presents a significant opportunity. It can make housing more affordable and provide governments with the funds needed to finance affordable housing initiatives.

The need for affordable, green housing

Africa’s housing crisis sees an estimated shortfall of 51 million housing units. Millions of people live in substandard conditions, particularly in countries like Nigeria, where the housing deficit is 28 million units. The Democratic Republic of the Congo and South Africa face deficits of 3.9 million and 3.7 million units, respectively. These figures are made worse by Africa’s rapid urbanization, which has outpaced both housing development and economic growth.

Africa is experiencing the fastest urbanization growth globally but has the least developed housing finance. Unlike other regions, Sub-Saharan Africa has not matched its urbanization with economic growth or housing investment. Over the next three decades, Africa will see 1.2 billion more urban residents. With the population growing at 4.1% annually, which is double the global rate, the situation will deteriorate further unless stakeholders take action.

Many households struggle with limited access to affordable housing finance when they try to secure decent homes. Traditional financial products often do not align with sustainable housing needs, as high interest rates and stringent qualification criteria create substantial obstacles. While financial challenges persist, the housing sector faces an additional burden—climate change’s ever-growing impact.

Climate change intensifies housing challenges in several ways. Firstly, it increases the frequency and severity of extreme weather events, such as storms, floods, and droughts. These events can cause significant damage to homes, particularly those built with inadequate materials and poor construction practices. Floods, for example, can destroy entire neighborhoods, displace thousands of people, and cause substantial economic losses. Secondly, rising temperatures increase the demand for energy to cool homes. This escalates energy costs and contributes to higher greenhouse gas emissions. This issue is particularly problematic in regions with already-strained energy infrastructure.

The convergence of these pressing challenges underscores an urgent call to action for innovative and comprehensive strategies, particularly to develop affordable and green housing solutions, reduce environmental impact, and provide safe and healthy living conditions. The path forward lies in the integration of sustainable construction practices with cutting-edge housing designs and pioneering financial solutions. The following section explores solutions to make this vision a reality.

Green housing finance mechanisms

Green mortgages are designed to incentivize energy efficiency and environmental sustainability in housing. Green mortgages are home loans for homeowners who plan to buy energy-efficient homes or retrofit existing homes to improve energy efficiency. These mortgages often come with lower interest rates and longer repayment terms, which makes them more accessible to low-income families. Homeowners can save on utility bills through reduced energy consumption, which can make housing more affordable in the long run. Green mortgage programs that encourage energy-efficient houses have been implemented, for instance, in the Philippines, Uzbekistan, and Peru.

Green bonds are debt securities issued to finance projects with positive environmental benefits. Governments and financial institutions can issue green bonds to raise funds for the construction of affordable green housing. These bonds attract investors who want to support sustainable development and provide a steady flow of capital for housing projects.

Construction and mortgage loan guarantees are government-backed programs to support housing development and expand access to mortgage finance, particularly for first-time buyers and those with smaller deposits. These guarantees incentivize local financial institutions (LFIs) to finance the construction and purchase of affordable, green homes. These guarantees reduce the risk for lenders and, thus, make it easier for developers to access financing and help low-income families obtain mortgages. This mechanism fosters a self-sustaining housing finance ecosystem. Examples include:

Construction support or guarantee: This guarantee provides construction lending and technical assistance to local developers, such as Peru’s Market Accelerator for Green Construction (MAGC) program. It includes construction guarantee facilities lending programs to developers and construction loans for innovative green home designs.

Mortgage support or guarantee: This guarantee provides technical assistance to LFIs to integrate alternative credit assessments and expand mortgage access. Mortgage guarantees encourage lenders to offer higher loan-to-value mortgages through government support and backing and, thus, expand access to mortgage finance.

Grants: These provide technical assistance for housing developers and LFIs to support increased housing supply, provide market research and feasibility study assistance, and offer training on sustainable building practices and energy efficiency.

Although we have an opportunity to shape green financing, we face the paradoxical challenge of the blame loop. The persistent demand-supply gap cycle leaves energy-efficient options underutilized as a market disconnect widens between the demand for energy-efficient homes and the supply of financing and construction options.

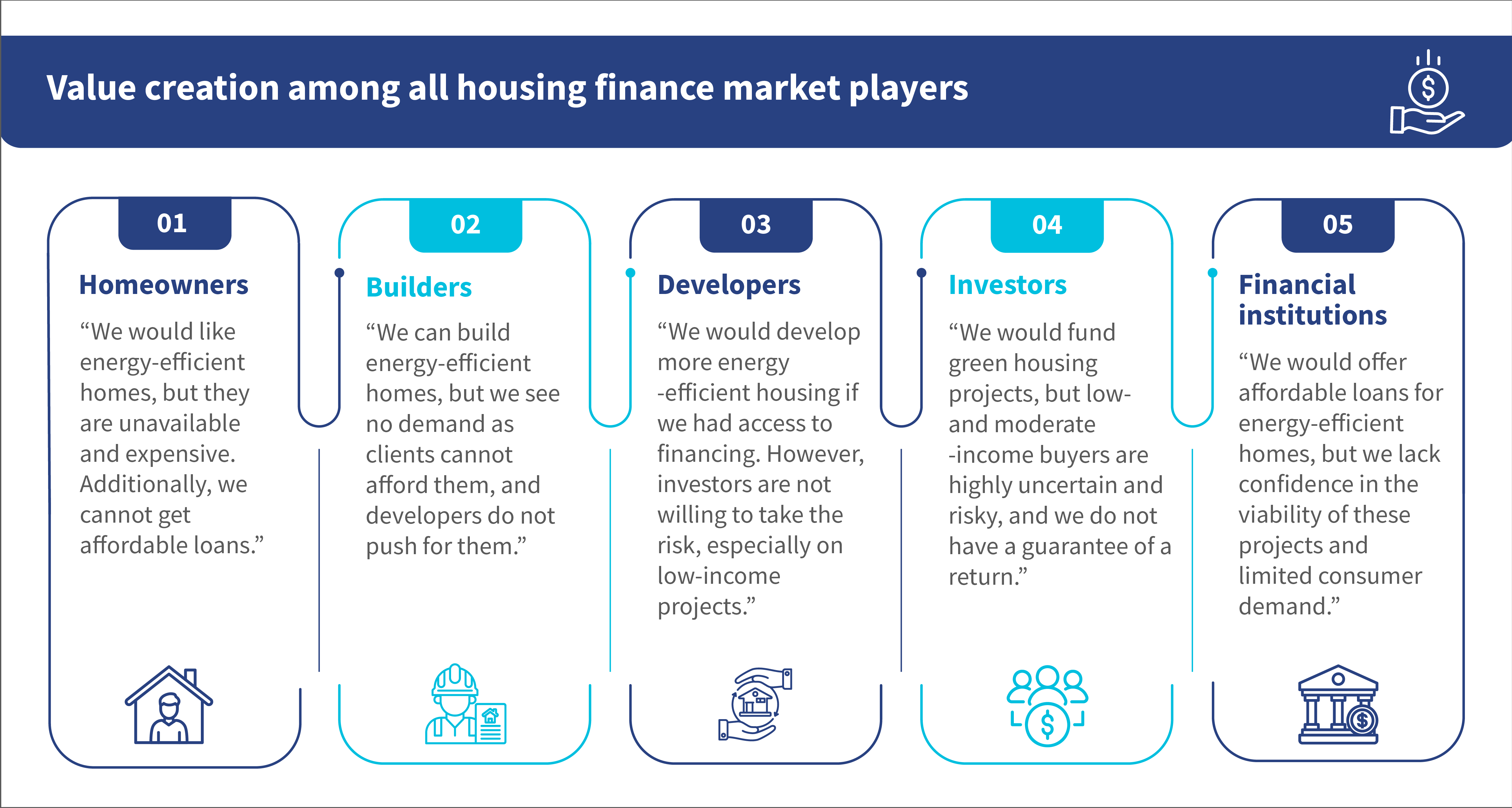

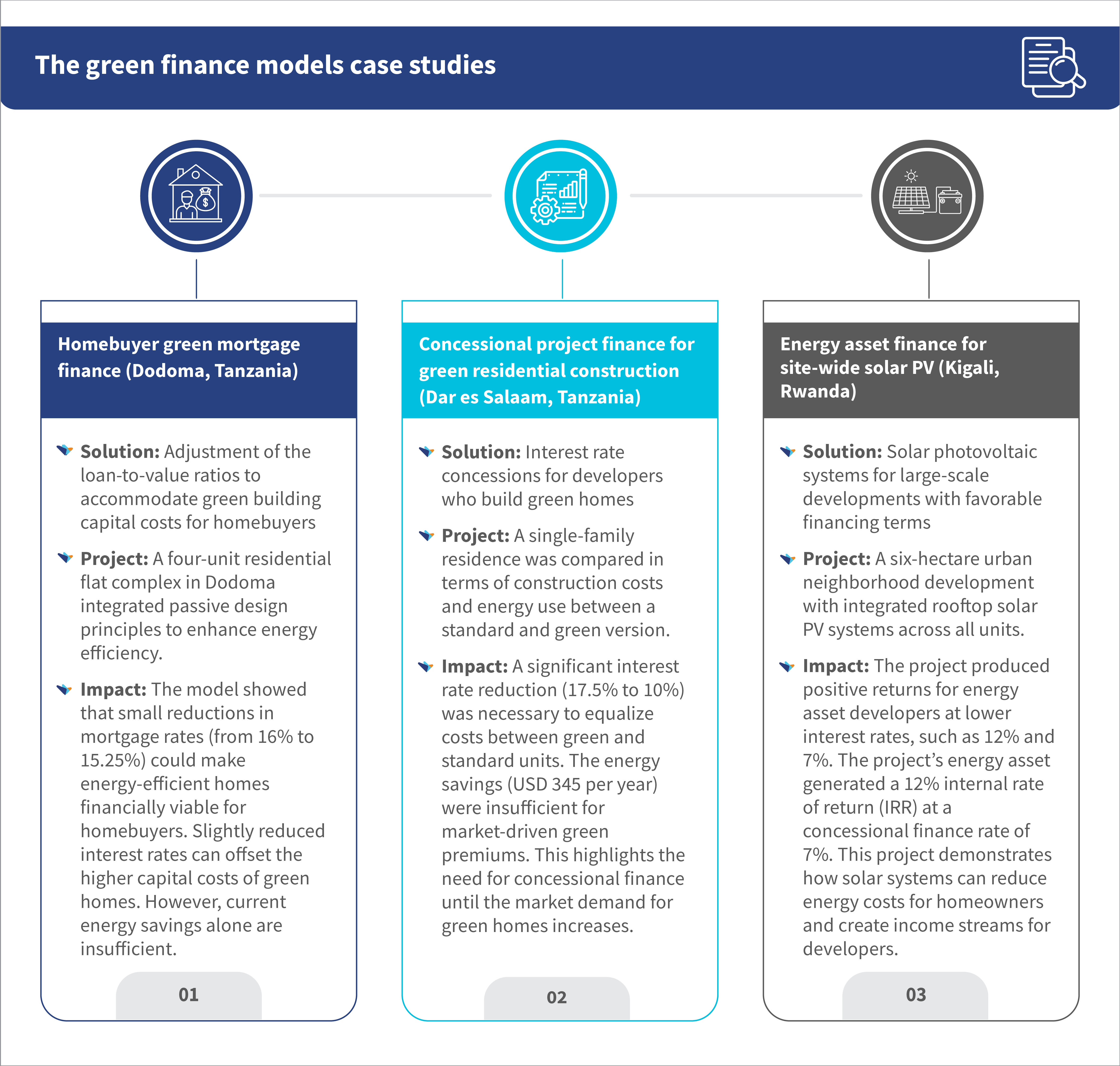

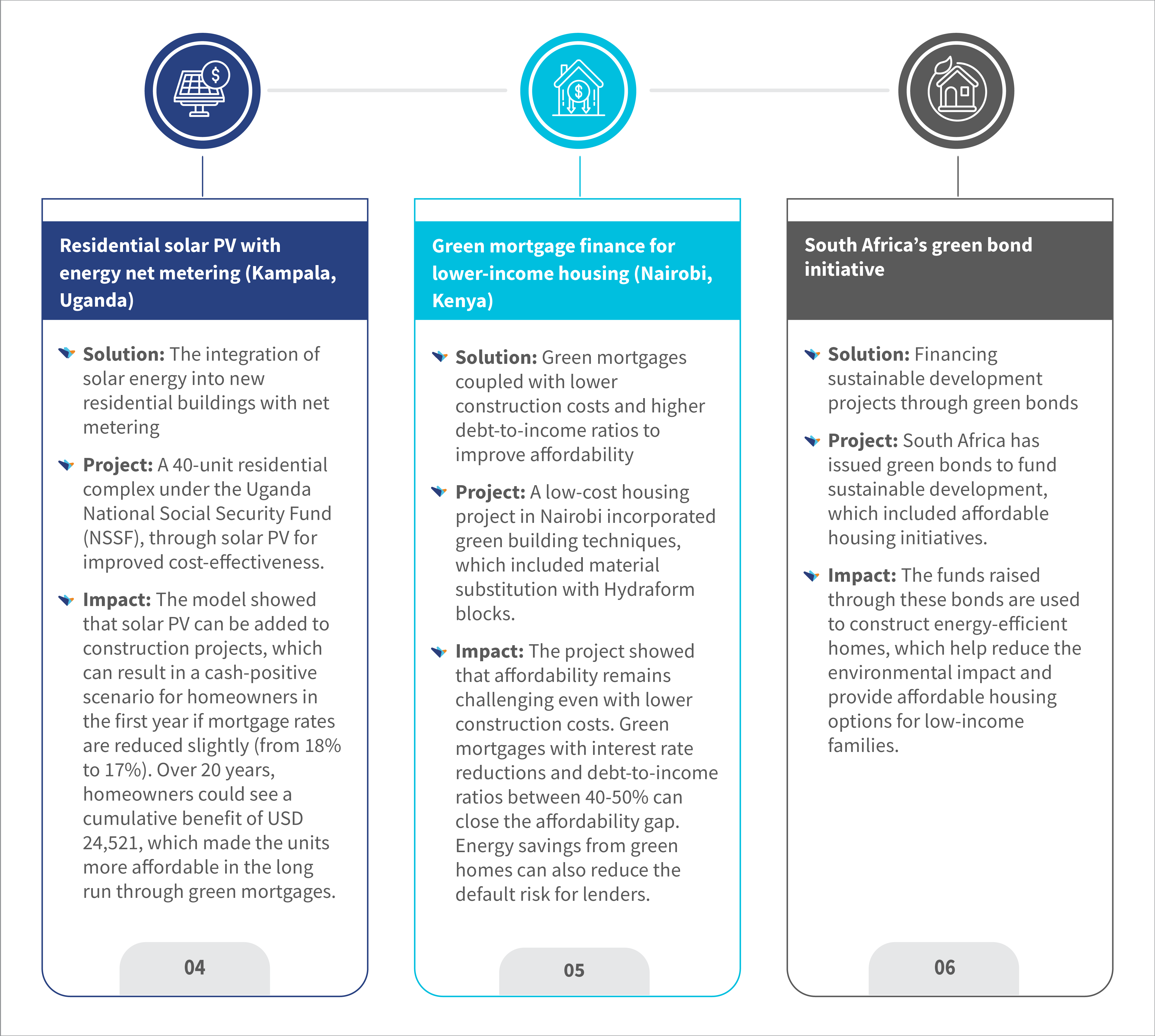

Case studies: Green finance models in Africa

The infographic below explores emerging practice case studies in Africa that evaluate the capacity of various finance products to reduce barriers to green building and enable value creation among all housing finance market players.

Affordable green housing finance can deploy decentralized credit enhancements to local financial institutions. It can, thus, catalyze, normalize, and scale private construction and mortgage lending. The mechanisms can be tailored to establish a self-sustaining ecosystem that supports the construction of affordable green homes and long-term homeownership.

Conclusion and recommendations

The development of affordable green housing in Africa presents a transformative opportunity. However, several significant challenges impede it. These include limited access to financing for both developers and potential homeowners, the high initial costs of green construction, and the lack of awareness and expertise in green building practices. Despite these obstacles, the need for affordable, climate-resilient housing continues to grow as urbanization accelerates across the continent.

We must take concrete action to bridge these gaps and use the potential of green housing finance. Our previous research, commissioned by Habitat for Humanity International (HFHI), HFH-Kenya, and HFH-Zambia, has laid the foundation for understanding affordable housing needs. The next step is to explore how green financing mechanisms can be adapted and scaled to meet the African housing market’s unique challenges.

Donors and stakeholders can play a pivotal role here. We can answer key questions that remain by funding targeted research:

What innovative financial products can make green homes more accessible to low-income households?

How can we reduce the financial risks for developers and lenders in the green housing space?

What policy interventions would incentivize private sector investments in affordable, green housing?

How can large multilateral climate funds and blended finance instruments help catalyze private capital to scale affordable green housing initiatives?

Green financing must gain traction through systemic coordination, collaboration, and value creation across all market players. The answers to these questions will help us build a compelling case for green finance and ensure it becomes a cornerstone of Africa’s sustainable housing agenda.

The ‘Decoding the Financial Health of women-owned microbusinesses in India’ initiative was launched to address the unique vulnerabilities of women-led microenterprises, especially in the aftermath of economic shocks such as the pandemic. MSC, in collaboration with Sa-Dhan, conducted a pioneering study on the financial health of women-owned microbusinesses (wMBs) in India.

The project involved extensive research, including secondary analysis, expert consultations, and primary data collection, to develop a comprehensive financial health framework for wMBs. The framework defines key dimensions, parameters, and indicators that assess and improve financial health outcomes for women entrepreneurs.

MSC led the study’s design and execution to ensure a robust and evidence-based approach to financial health assessment for wMBs. The team conducted Key Informant Interviews (KIIs) with supply-side stakeholders, held brainstorming workshops with industry experts, and engaged Enterprise Support Organizations (ESOs) and government bodies to refine the framework. The study resulted in a structured methodology for measuring financial health, providing actionable insights for key ecosystem players.

The study delivered a first-of-its-kind financial health framework and checklist, offering practical financial and non-financial tools for stakeholders—including funders, financial institutions, ESOs, and policymakers—to assess and enhance the financial well-being of women-owned micro businesses. It also contributed to the broader financial health discourse in India by bridging research gaps and strengthening the understanding of how ecosystem actors perceive and influence wMB financial health.

J.P. Morgan Chase & Co. commissioned this project.

The Sathi Network, a women-led agent network, provides marginalized rural women in Bangladesh with access to financial services. Female agents build trust and empower unbanked women to engage in digital transactions confidently. They promote financial inclusion in a supportive environment. MSC carried out the impact evaluation of the Sathi Network for a2i one year after its intervention. Read the stories of Neela, Rahela, Fahmida, and Fahima. These women are working to overcome societal barriers, create sustainable businesses, and promote financial literacy among women in their communities.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.