Africa has emerged as a melting pot for female entrepreneurship in light of the recent surge in attention to entrepreneurship. The continent has the highest rate of female entrepreneurship, at 24%, ahead of South-East Asia Pacific (11%) and Europe (9%). Moreover, female entrepreneurship in Africa contributes between 7% and 9% of its GDP, or some 150 to 200 billion dollars.

Yet, despite the dynamism that can be attributed to women’s entrepreneurship in context of these rather glowing figures, women face numerous barriers when they attempt to develop their businesses. Access to finance is one of the major issues. What are the possible solutions to this challenge?

Causes of the financing gap

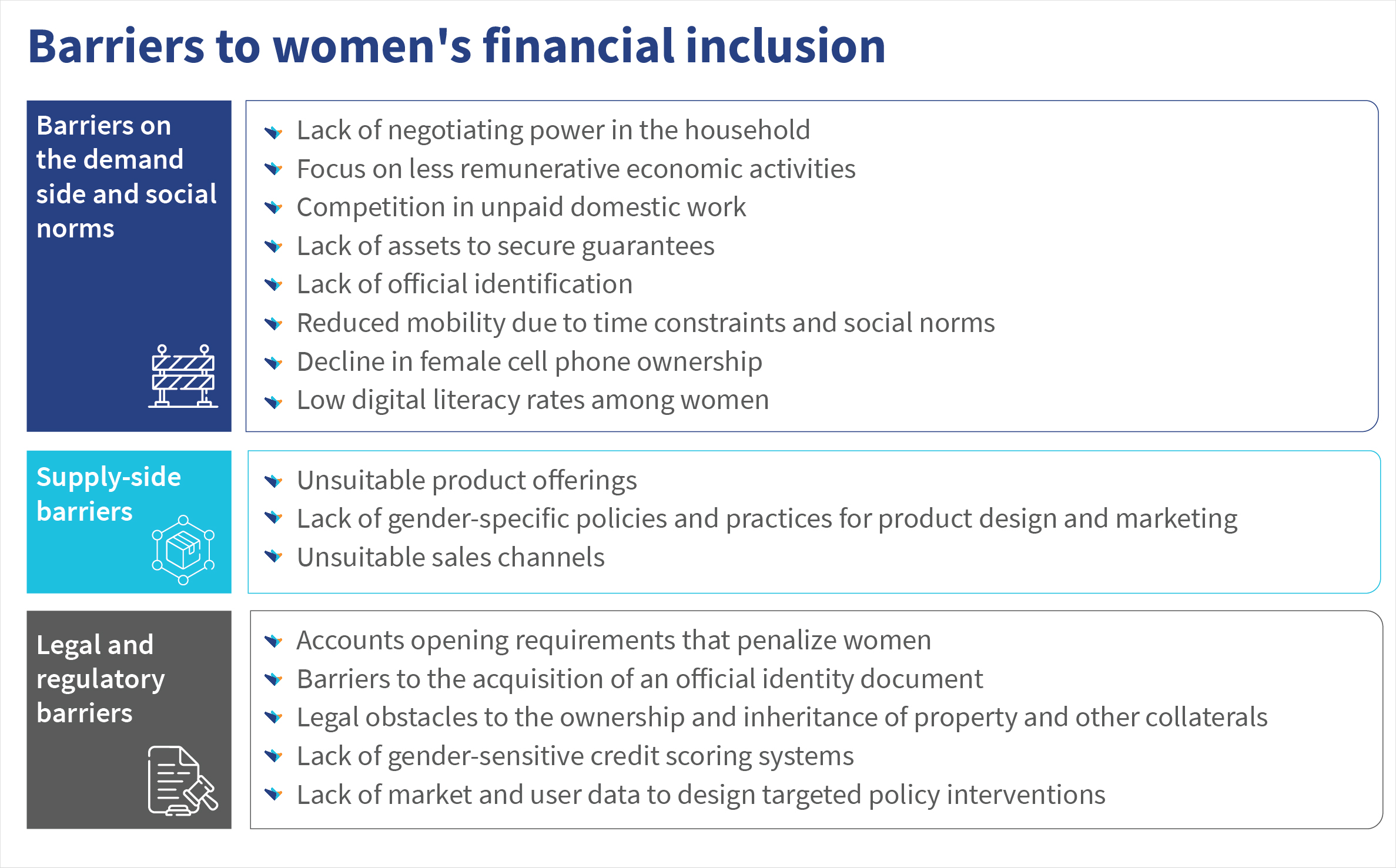

Worldwide, women’s access to finance remains disproportionately low. The situation is far more alarming in Africa, which starts with unequal access to bank accounts.

In Sub-Saharan Africa, only 37% of women possess a bank account, compared to 48% of men, a gap that has been widening for several years. Women frequently have little capital to start their businesses and are less likely to benefit from private investment or venture capital. “I sell clothes to support my family. I wanted to increase my capital to develop my business. Yet the bank denied me a loan, because, according to them, I do not have strong collateral,” said Karidja Bakayoko, a clothing retailer in Daloa City, Côte d’Ivoire.

Banks require collaterals that women cannot often provide. Men usually own valuable assets, such as land titles or vehicles, which they can provide as collateral to support some women. Notably, 45% of women in low-income countries have no official identity documents, compared to 30% of men. In addition, women are usually risk-averse, with little financial culture and a fear of failure, which often prevents them from requesting loans. They also have to contend with a lack of family support and a lack of training to develop the skills needed to run a business effectively. Other barriers include personal constraints, such as family projects, spouses’ professional projects, and family responsibilities, alongside women’s poor integration into business networks, and the lack of suitable financial products. In addition, banks’ lack of understanding of women-owned businesses and women’s lack of financial education are barriers to financial inclusion, as shown in the table below.

All these challenges have a negative impact on access to finance for African women entrepreneurs.

However, when financing and markets are available, women can contribute significantly to their families’ well-being. They can then mobilize savings to prioritize their children’s education. They also contribute to their country’s economic development by setting up businesses that create jobs and wealth.

Initiatives to boost access to finance for women entrepreneurs

Concrete actions are needed to promote women’s access to finance. Governments should introduce financial inclusion policies and regulations that favor women. To this end, several initiatives have already been developed across Africa, such as the Affirmative Finance Action for Women in Africa (AFAWA) program.AFAWA is an African Development Bank (AfDB) initiative that seeks to bridge the estimated USD 42 billion financing gap that affects women in Africa. The initiative is in early discussions with financial institutions in West Africa. AFAWAis also a USD 12.5 million anchor investor in Alitheia IDF Managers (AIM), the first private equity fund of its kind, led by experienced women fund managers that invests in high-growth SMEs owned and run by women in Africa. In 2018, AFAWA provided technical assistance to several banks. AFAWA trained 1,000 women entrepreneurs across the African continent in business model development and financial planning in collaboration with the Entreprenarium Foundation. The aim is to give them the resources they need to access financing easily.

Investment funds dedicated to women akin to Janngo, a venture capital fund run by women that invests 50% of its revenues in start-ups founded, co-founded or benefiting women, should increase even more. In Côte d’Ivoire, the government set up a fund in 2017 to promote SMEs and women’s entrepreneurship with a budget of 5 billion XAF. This fund seeks to facilitate access to bank credit for women entrepreneurs, including startups, across all business sectors. The initiative will provide a tangible boost to financing for women and help advance financial inclusion.

Financial institutions should not stay aloof from these initiatives. They could consider creating women-friendly banking procedures, such as waivers on minimum balances, reductions in collateral requirements, and inclusion of other forms of collateral that are more accessible to women. In addition, financial institutions would benefit if they develop products and services dedicated entirely to women that take their needs into account. They should consider important aspects, such as product simplicity or reliability, when they design these products and services, which are likely to guarantee their frequent use.

We must, however, note that the design of financial services should be accompanied by financial education programs that will enable women entrepreneurs to develop suitable financial skills and behaviors. In short, the goal is to improve women’s understanding of financial services while raising their awareness of the risks involved so that they can make autonomous and responsible financial decisions. It is with this in mind that the Digital Finance Hub has been created to offer everyone the tools they need to develop their business.

Worryingly, a customer base in excess of 1 billion women remain disconnected from financial services and predominantly underserved. To change this situation, FSPs must study women’s customer journeys and use this knowledge to design tailored financial product offerings. The dual benefit will be to transform women’s lives and offer commercial value to financial institutions. Financial institutions would be able to create new products and reach out to women, who are usually not funded. With a tailored offering, the financial institutions can grow their clientele—and their income.

South Asia is generally very hot, and people have built coping mechanisms to deal with the heat. However, climate change is set to push temperatures higher and increase heatwaves in the near future. Up to 75% of India’s workforce, or 380 million people, depend on heat-exposed labor and at times work in potentially life-threatening temperatures.

MSME workers who work in workshops with heavy machinery, outdoors, or are engaged as gig workers are at a higher risk of heat-related injuries and extreme symptoms. This study seeks to understand the vulnerabilities and challenges informal workers and MSMEs face with regard to extreme heat.

The Findex 2021 survey reported that 76% of adults had an account at a bank or regulated institution, such as a credit union, microfinance institution (MFI), or a mobile money service provider. In developing countries, 13% of these accounts were inactive, even when we use the conservative measure that the respondent “did not use their account at all in the previous year.” Given that governments were making payments to support post-COVID-19 recovery in the year before the enumerators conducted the survey, this figure probably understates the underlying inactivity significantly.

The reasons for this exclusion are well known. They include geographical barriers, since limited distance and poor infrastructure in remote areas restrict access to services. This is compounded by economic vulnerability, as poor communities often lack the income or documentation needed to use traditional financial services. Gender disparities further impede women’s inclusion, and a lack of financial capability limits broader participation. Policy and regulatory constraints, such as restrictive policies and high compliance costs, also hinder service expansion.

These excluded people are also often stranded on the wrong side of the digital divide as a result of the lack of access to mobile phones, poor internet connectivity, and low digital literacy compounded by unsuitable user interfaces. They are also most likely to be vulnerable to climate change and have the greatest need for information and financial services to cope with climate events, recover from them, and adapt to build their resilience.

FSPs have not been willing or able to support these excluded people on commercial terms. This is unlikely to change without de-risking, and in some cases subsidies, for them to do so.

Could climate funds be a catalyst?

UNEP estimates that the climate change adaptation costs for developing countries will increase to USD 160–340 billion annually by 2030 and USD 315–565 billion by 2050, which is five to seven times higher than the USD 49 billion of global adaptation flows in 2019-2020.

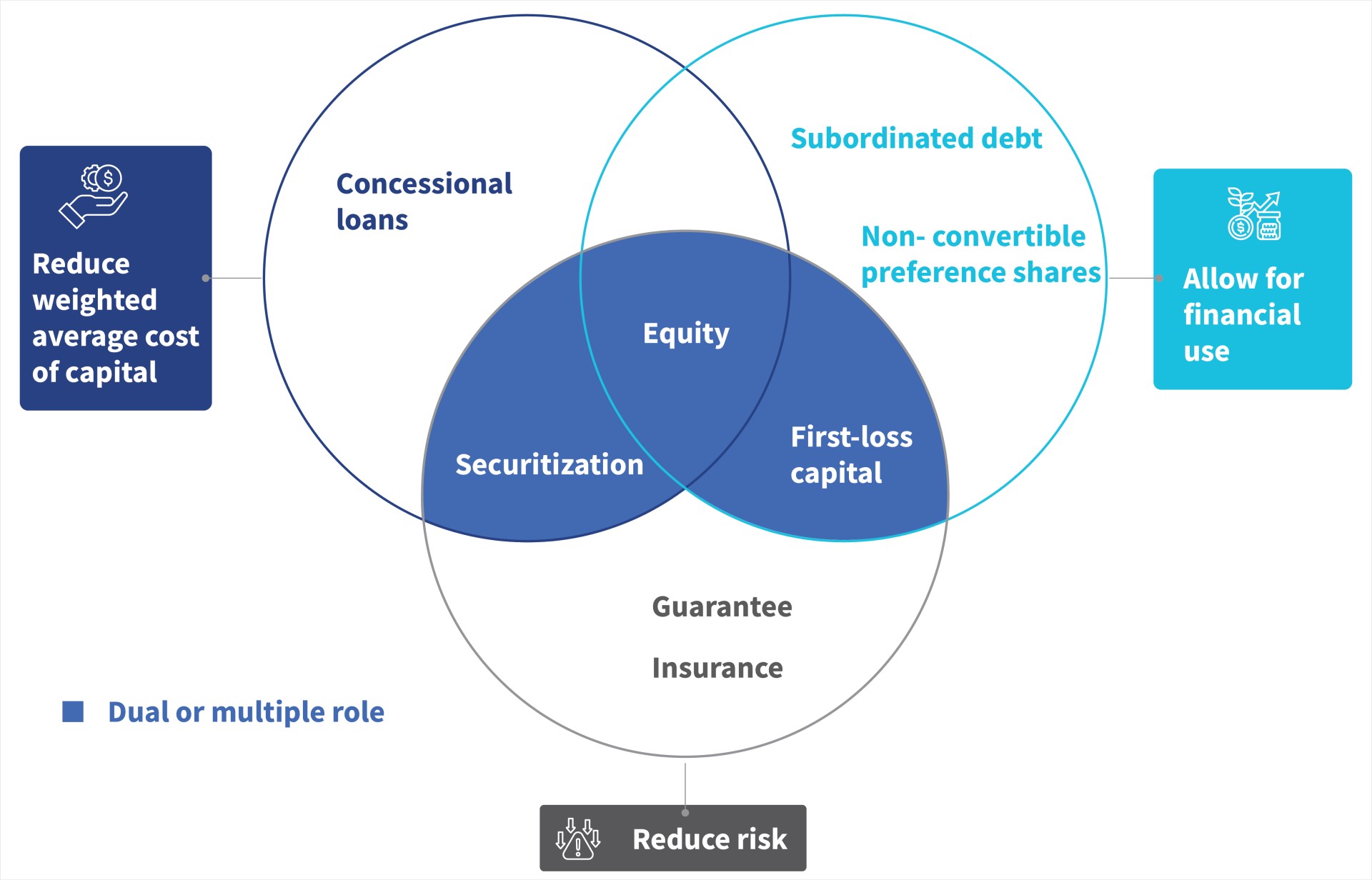

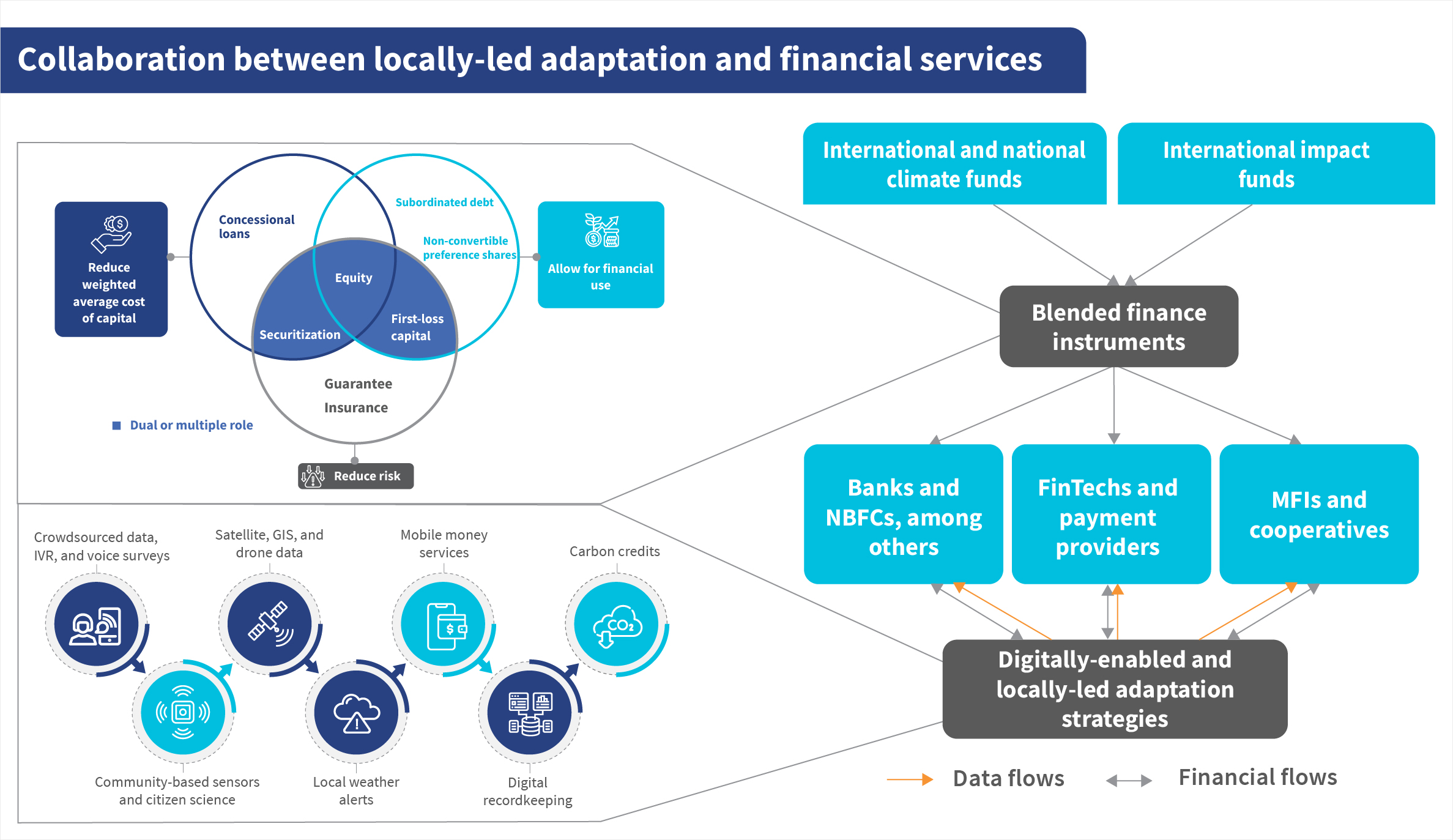

International and national funds, alongside impact funds, could use blended finance instruments to unlock public and private sector capital to address this chasm between the need for finance and its availability. Blended finance instruments can be used to reduce risk, permit capital leverage, and reduce the average weighted cost of capital. Using these instruments in preference to, or alongside, the grants that are most commonly used by many of the climate funds at present, could stretch precious adaptation funds and help bridge the chasm.

What role should blended-finance play?

Can digitally enabled locally-led adaptation turbocharge locally-led adaptation strategies?

Digitally enabled locally-led adaptation (LLA) is essential to scale and optimize locally-led adaptation strategies. It also offers the opportunity to create digital profiles and thus conduct risk analyses of these populations and their livelihoods.

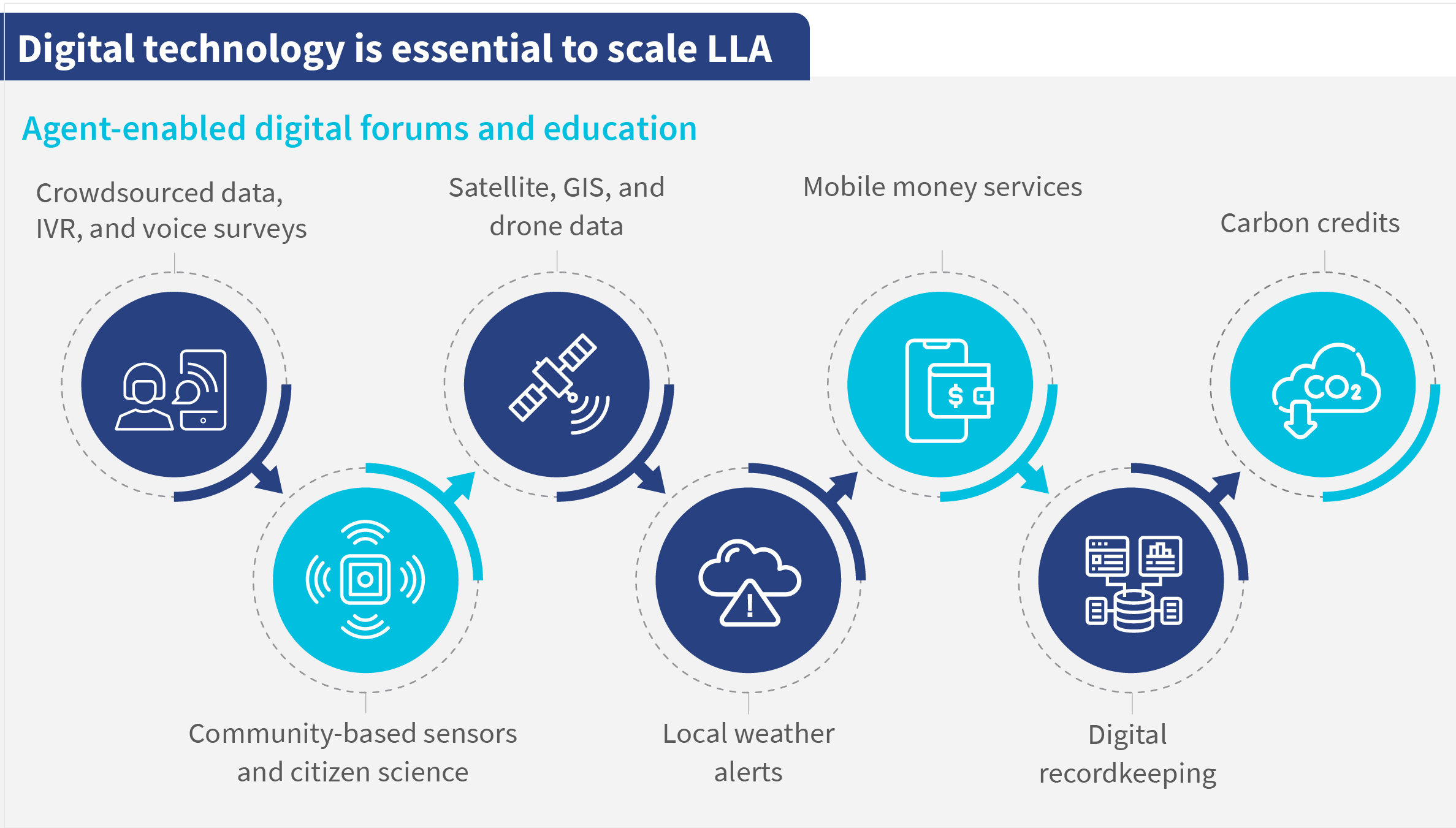

Digital technologies driven by satellites, crowd-sourcing, and AI, such as those used by CropIn, Ushahidi, and Amini, have great potential to support LLA planning and implementation. Community-based and operated sensors could collect localized climate data for analysis and planning and complement climate change predictions from GIS and machine learning models. As adaptation plans are implemented, local language weather apps, such as TomorrowNow, could provide communities with vital alerts about imminent weather changes to enable them to prepare and respond better.

These technologies can expedite and scale strategy development processes, support implementation, and enhance governance functions, such as monitoring, evaluation, and learning. Additionally, the carbon offsetting programs that could also provide some funds for adaptation often face challenges in the certification of carbon-offset activities and distribution of funds to the intended vulnerable communities. Digital platforms, such as CaVEx, present opportunities to overcome these obstacles and ensure more effective implementation and payment of benefits.

Communities can use community-based and operated sensors, satellite and drone services, and feedback platforms to report progress and challenges in real time. Mobile money services and digitally-enabled smart contracts could be used to ensure the transparent and efficient delivery of funds for adaptation projects against performance targets. Furthermore, digital payments and digital record-keeping could ensure the accountable use of resources and thus create important digital trails that facilitate credit risk appraisal and lending by formal financial service providers.

Findings from the Global Findex 2021 survey likewise reveal new opportunities to use digital payments for wages, government transfers, or the sale of agricultural goods, to drive financial inclusion and expand the use of financial services among those who already have accounts. Digitalizing some of these payments is a proven way to increase account ownership. In developing economies, 39% of adults—or 57% of those who had an account with a financial institution (excluding mobile money)—opened their first account specifically to receive a wage payment or receive money from the government.

Opportunities to facilitate locally-led adaptation strategies

Indeed, MFIs, credit unions, and other community-based FSPs and their agents are well-placed to facilitate digitally enabled LLA planning and strategy development alongside capacitated local government officials. Doing so would allow FSPs to deepen their understanding of the needs, aspirations, and behaviors of these climate-vulnerable communities, and learn how they mitigate the risks they face. This, in turn, would allow FSPs to use the funds and blended finance instruments offered by international and national climate funds and impact investors to provide financial services to these communities.

Bridging the digital divide

In addition, the use of digital technologies as part of the LLA process provides us a unique opportunity to get these populations used to digital devices and data and comfortable with them. These LLA-driven use cases provide opportunities to offer real value to these hard-to-reach communities, increase their resilience, and demonstrate the benefits of digital tools to them. Many of the most vulnerable communities comprise smallholder farmers who could benefit from digitally-enabled value chains and financial services.

Climate change, and the LLA response to it, could very well become an essential bridge across the digital divide for these farmers and others currently stranded in the analog world.

We have examined the causes and effects of the digital divide—where the most vulnerable members of society are stranded in an analog world—in the blog “Can AI help with locally-led adaptation? The challenges.” Despite efforts to close this gap through AI-powered modern technologies, the adoption and penetration of these technologies have fallen well short of expectations. We can summarize the problems as follows.

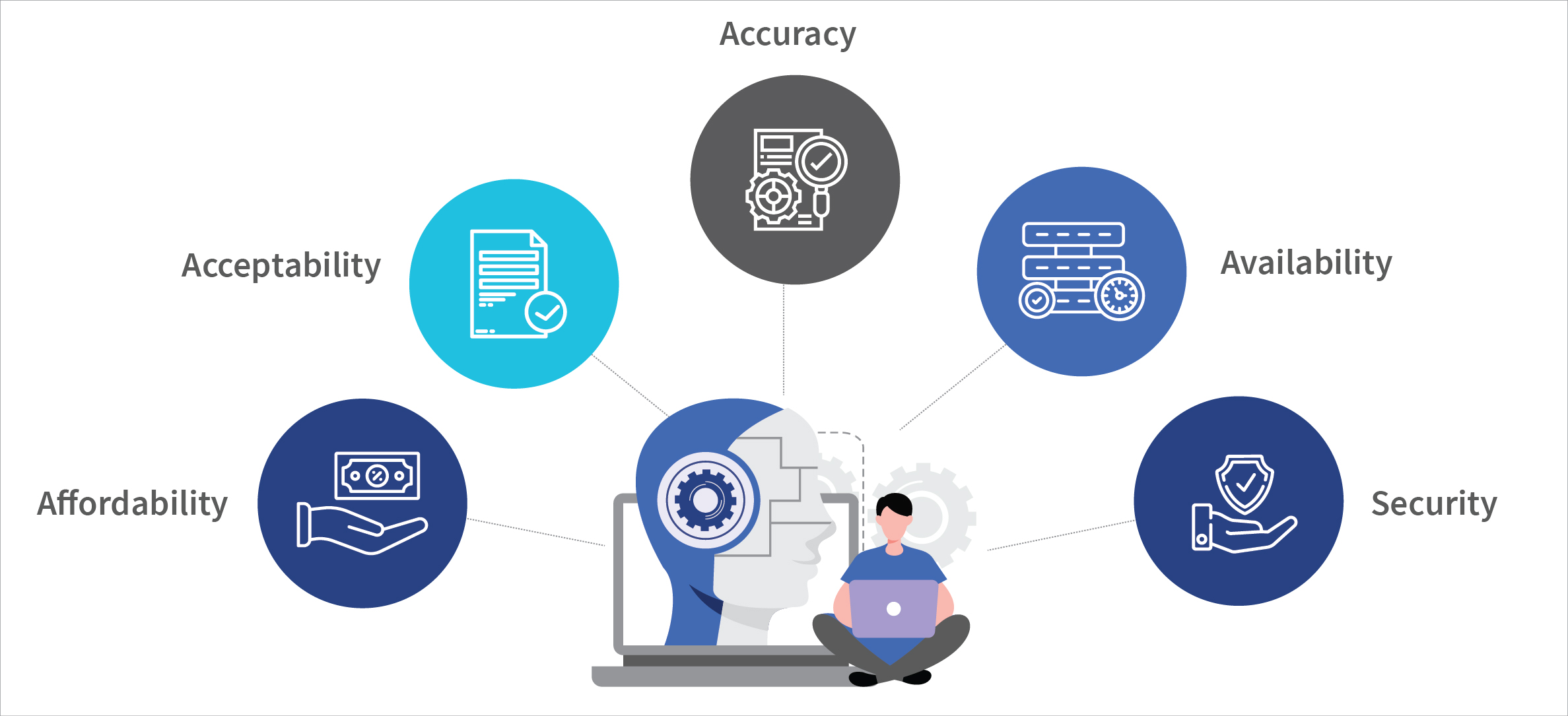

We need to address five aspects here:

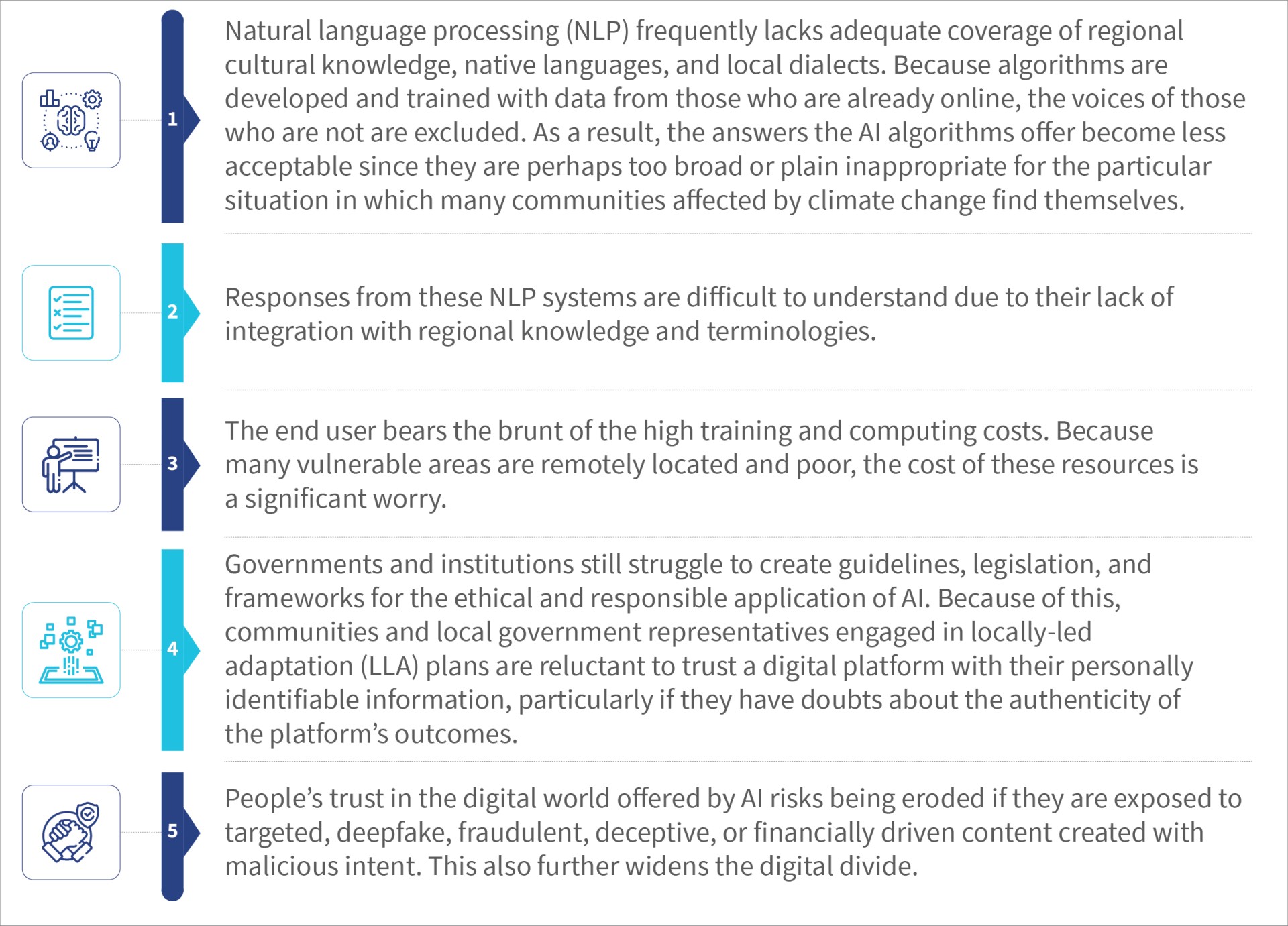

Data is the main source of dependency for any nation’s AI journey. Governments must create their frameworks, policies, and goals for AI and engage in its development. Affordability will be easier to achieve if the state invests to collect, preserve, process, and operationalize data. For example, India’s AIRAWAT AI supercomputer, which is among the world’s 100 most powerful systems, helps enable technology and AI for the welfare of common people and contributes to their socioeconomic growth.

The National Strategy for Artificial Intelligence lays down the foundational roadmap to India’s AI journey. The work on the Indic language set allows content to be collected and delivered in Indian languages. With state backing to process vast amounts of data, private businesses can create last-mile solutions and delivery apps that are more cost-effective for the underprivileged population. These private institutions can then focus on educating the public on digital platforms. Here, too, the state’s capacity for broadcasting and information dissemination can be used to reduce the cost further.

Development organizations have also played a big role to bring down the affordability cost through their support of initiatives for multiple public use cases, such as healthcare to the doorstep, tele-consultancy, and medical interventions to detect symptoms, among others. For example, People+ai has been working on a strategic initiative Adbhut India (AI), which seeks to build ecosystem-level solutions actively across a spectrum of multiple projects in agriculture, healthcare, education, and governance. As more and more players participate in the ecosystem collectively and competitively, the quality of solutions will improve, and their costs will fall as per the market economics.

The acceptability of the solution for LLAs depends on the content’s localization and relevance. This means that the content should feature native terms and dialects wherever suitable. To help, the state or pertinent departments should create, oversee, and implement a local lexicon and glossary that can supplement the trained LLM models with techniques, such as retrieval-augmented generation (RAG). RAG is a method that uses information retrieved from external sources—in this case, the localized glossary—to improve the precision and dependability of generative AI models. For example, the armyworm pest has different names in India, such as “girni sena” or “fauji keeda.” In such cases, the RAG technique will supplement the LLM with a localized glossary of names. Similarly, OpenHathi by Sarvam AI has been developing an ecosystem with open models and datasets to encourage innovation in Indian language AI.

The local climate, soil, landscape, temperature range, and species, among other factors, should also augment the trained data to make the delivered content more accurate. Some data is available in government departments in silos, but its quality in terms of structure, relevance, and accuracy remains a big concern. Development organizations can play a vital role here to facilitate data collection by encouraging the use of digital technologies for LLA.

Availability is easy to achieve if all former aspects are in place. The design of the “last-mile” application should be intuitive for users and seek to reduce the digital divide through a suitable delivery mechanism. People who cannot read can be helped using audio or video content. Places with poor or no internet connectivity can be included through the use of state capacity of information broadcast and community service. Most of the LLAs are “employed” to render their service, and these organizations should also contribute through their corporate social responsibility. As discussed earlier, NLP trained in local dialects and languages is the key to success.

CICO agents, MFI staff, agricultural extension agents, and CBO or NGO staff can help those without smartphones access AI solutions. These agents can provide awareness, trust, and capacity building for AI solutions that require digital payments or transactions, such as e-commerce platforms, digital credit, or insurance products. The agents can enable people to invest in or adopt AI solutions for agriculture, such as smart irrigation systems, precision farming tools, or crop monitoring devices. Agricultural extension agents can also provide feedback and evaluation for AI solutions and facilitate the exchange of knowledge and best practices among farmers and other stakeholders. CBO or NGO staff can also advocate for the rights and interests of farmers, especially smallholders, and women, and ensure that AI solutions are ethical, responsible, and inclusive.

Securityand privacy are the most difficult aspects of all the concerns. Technology is just a tool, a weapon that can be used for both positive and negative outcomes. Any technology’s positive intent, promises, and capability have never been able to outrun the malicious intent to exploit loopholes, gaps, and back gates left unguarded due to a lack of strong foundational policies, laws, frameworks, checks, and measures. A coordinated and collaborative approach is required among multinational governments and private institutions to share, adapt, and enforce these countermeasures to keep bad elements at bay as far as possible.

Laws now need to go beyond border jurisdiction to spread the cover. Nations can no longer match the potential of AI in isolation if they want to ensure the safety and privacy of their citizens’ data and well-being. This is particularly important in the context of farmers, as discussed in the Climate Resilient Agriculture Virtual Club. Policymakers and regulators must develop farmer-centric data governance guidelines to implement fair and equitable data governance models that prioritize farmer participation even as they guard farmers against disadvantages and exploitation.

People hesitate to overcome the digital divide primarily because of a fear of fraud, cybercrimes, and misuse of personal information. Interestingly, advanced AI can analyze non-personal data over time to identify, for instance, farms and their owners, even without direct access to personal information. Digital literacy must be improved to address the hesitation. Governments and nonprofits must actively educate farmers on the digital skills needed for their development in rural areas. This education should also cover their rights and obligations in the digital world. Moreover, it is time for laws to recognize the “right to consent” as a basic right and integrate it into the educational curriculum for all citizens.

Conclusion

We must tackle the challenges of affordability, availability, acceptability, accuracy, and security to successfully integrate AI into development initiatives, particularly for people with low literacy. AI adoption depends on comprehensive data management and supportive government policies. Localization of solutions to align with cultural and linguistic needs is key to better acceptability and accuracy, while accessible design and community engagement are vital for broad availability. If security and privacy concerns are to be addressed, coordinated efforts will be needed across governments and institutions to establish protective measures and ethical standards.

A focused effort on technological innovation, digital literacy improvement, enactment of supportive legislation, and multi-sector collaboration is imperative. Such a holistic strategy will address immediate challenges and position AI as a powerful tool to foster inclusive LLA and, indeed, development in a broader way.

One reason behind the design flaw is women’s underrepresentation in digital designs and processes. This stems from various barriers, which include social norms, such as restrictions on mobility and access to assets that underpin all other barriers to digital participation. Women comprise only 30% of the tech workforce, with only 10% in leadership. This underrepresentation also results from socialization from an early age and stereotypes reflected in the entire digital ecosystem—from education to gendered digital marketing and video games.

A three-decade-long global analysis shows that 44.2% of 133 AI systems displayed gender bias, which reinforced harmful gender stereotypes. UNESCO’s report reveals that the development of AI and algorithms, a critical component of digital spaces, is often skewed toward male preferences and perspectives. The underrepresentation of women and their perspectives leads to biased results that do not effectively serve their needs. The results interpret the tech space as a gender-unintentional space where women are unwelcome.

This includes the Science, Technology, Engineering, and Mathematics (STEM) sector, which is highly male-centric and fails to consider these challenges. Social norms discourage women from careers in technology or other digital fields and limit their opportunities and confidence to develop digital skills and engage with digital technologies.

Digital spaces that lack female tech designers tend to reduce women’s visibility. This leads to a scarcity of use cases. For instance, when prompted to generate images of judges, an AI image software produced pictures of female judges in only 3% of cases. Such digital technologies reproduce these prejudices and exacerbate them. It, thus, makes tech sectors even less gender inclusive.

Women in design: Bridging the gap

When women are actively involved in the design process, they bring diverse perspectives that help create use cases for a broader audience. Studies show that when tech designers seek to address development issues, as seen in the case of health, male designers tend to focus on conditions that exclusively affect men. In contrast, women-led teams often address a broader spectrum, which includes requirements that affect both genders.

An assessment of 200 companies under the Third Digital Inclusion Benchmark by the World Benchmarking Alliance (WBA) shows that consistent interventions and promoting gender-balanced representation is crucial for making a meaningful impact on women’s digital inclusion. McKinsey & Company’s report on diversity highlights that organizations with gender-diverse teams are 48% more likely to outperform their peers. This also applies to the tech industry, where more inclusive design teams create products and services that resonate with a broader user base.

A critical area where women’s high representation has significantly impacted use cases is the FemTech industry, which boasts more than 70% of companies with at least one female founder. FemTech companies, such as Maven Clinic, Peppy, Flo, and Clue, have been filling gaps that are yet to be addressed by pharmaceutical and HealthTech companies in maternal and menstrual health. They have improved care delivery and diagnosis by delivering culturally sensitive and tailored care, a clear link between women’s inclusion in digital design, improved outcomes for women, and more use cases of digital solutions.

HealthTech: Healthcare is a critical area where gender-responsive design is paramount. This is evident in menstrual tracking apps that initially lacked comprehensive features due to limited women’s input. Apple’s Health app, released in 2014, highlighted gender bias through the omission of menstrual cycle tracking despite its significance. This was likely influenced by a predominantly male workforce (70%). Healthcare apps have become more comprehensive with women as part of the design process. They offer insights into cycles, fertility, mood fluctuations, and personalized health recommendations. Health innovations must also be co-designed with women for greater uptake and enhanced use cases.

FinTech and AgriTech: Research on digital input loans reveals that limited data on women’s financial histories skews credit assessments toward men. This is ironic as extensive literature suggests that women are more likely to repay loans than men. Similarly, female farmers are less likely to apply for digital credit and thus receive lower amounts despite similar digital credit approval rates to men. The prioritization of gender intentionality in product design can promote gender equality in digital financial services and unlock an untapped market of underserved women. Also, an IMF paper finds that greater gender diversity in the executive board is associated with FinTech firms’ better performance.

EdTech: A notable example from the EdTech world is Coursera, which has a female founder motivated to make online education more accessible for underserved communities. Coursera now has more than 77 million registered students and partnerships with 200-plus institutions in 190 countries. Its global reach is constantly growing, with a valuation of almost USD 7 billion. Such women have established themselves as role models for other women to follow. Online education offers more flexibility in pace and schedule, which attracts many women. The insights gained from the EdTech sector can be applied to other areas where women are underrepresented to improve their participation and experience.

Men often design digital spaces for themselves by default. However, this blog shows the potential of women’s inclusion in design teams as the key to diverse and meaningful use cases. This comprises all the core and peripheral design elements: Product design, pricing, processes, people, place, physical evidence, promotion, and positioning. The examples in this blog show that the use cases for women have increased due to the right features in applications or better communication around digital products and services has enhanced the use cases for women.

Greater women’s representation in the digital design ecosystem can create more consumer-centric products and solutions that recognize and target women’s specific needs. Such products would lead to a less biased and more inclusive digital world, with improved digital opportunities for women and, meaning more use cases for them. We need higher representation of women in digital spaces and teams for this, which calls for more women in the STEM sector. By envisioning a future where women lead the design of digital innovations for the last mile, we can bridge the gender digital divide and promote digital inclusivity.

How far would a dollar go if it went straight to someone in need when they need it most?

With government-to-person (G2P) payments, governments increasingly disburse welfare benefits directly to individuals or households. These high-volume, low-ticket-size G2P transactions are vital to boost financial inclusion and empower vulnerable communities. Globally, programs such as Brazil’s Bolsa Familia and Zambia’s supporting women’s livelihoods (SWL) report cost savings, leak reduction, and timely payments for grant recipients through digital payments. In India, Jan Dhan bank accounts, Aadhaar for identity verification, and mobile payment applications enabled by the Aadhaar Enabled Payment System (AePS) and Unified Payments Interface (UPI) have boosted financial inclusion. These have allowed government programs to incorporate direct benefits transfers (DBT).

While promising, digital G2P payments remain in their early stages, and face challenges, such as friction in payments, information gaps, and contextual barriers. The MUKTA program in Odisha, India, is an example of a multi-stakeholder collaboration to reengineer digital systems and government policies and processes to operationalize digitally-enabled Smart Contracting and Just-in-Time funding systems (JiT-FS). It has enhanced program’s reach, improved observability, and provided a clear understanding of performance bottlenecks. Additionally, it has empowered stakeholders to refine and optimize the system continuously.

Admirable goal, administrative friction

MUKTA is a pioneering initiative designed to generate wage employment for vulnerable workers in urban Odisha during the COVID-19 pandemic. Rooted in community needs and responsive to local demands, MUKTA uses existing community-based organizations (CBOs) to execute public works projects that are sustainable and climate resilient. These CBOs enlist wage seekers to work on these projects and generate income for them.

Delayed payments to CBOs and wage seekers were a key challenge in program implementation. Beneficiaries faced lengthy wait times. Additionally, a baseline study across two pilot urban local bodies (ULBs) found that more than 50% of completed tasks were not processed for payment, and the rest encountered delays that exceeded one month. Wage seekers come from low-income households, and such delays undermine the program’s welfare objectives.

Such delays arise largely from cumbersome, paper-based compliances, billing, and verification processes. Every step—from attendance tracking and bill submission to verification, approvals, and payment instructions—relied on manual processes. It increased the administrative burden on local government personnel, who were overburdened already. These long-drawn processes also resulted in the underutilization of sanctioned funding as funds were parked idle in banks and had limited transparency.

Making processes and payments smarter

These challenges threatened to undermine MUKTA’s goals. It was clear that a transformative intervention was required. MUKTA embraced a three-phase “Smart Payments” approach to address these challenges:

Discovery: The identification of pivotal problems in program implementation

Extensive consultations with stakeholders at each government tier helped identify key requirements to complete payments under the MUKTA program and administrative inefficiencies that prevented timely completion. The tiers included the Finance Department (FD), Housing and Urban Development (H&UD) Department, local government officials, and CBO representatives.

Such programs require multi-entity coordination. Project definition, estimate creation, progress monitoring, and bill approval occur at the local government level. The state government sanctions overall fund tranches and executes electronic payments. The first step in the solution was to identify the information the state government would need to disburse payments and find a way to communicate it most efficiently. We used existing Integrated Financial Management System (IFMS) and Public Finance Management System (PFMS) data standards to develop functional requirement specifications. This further led to the development of a two-part solution: MUKTASoft, which streamlines processes and reporting through program implementers, and JiT-FS, which simplifies and speeds up fund disbursal.

Design: Solution development and reform proposal

MUKTASoft is a workfare program management platform that streamlines project management and information flow among CBOs, local government bodies, H&UD, and FD. The expedited flow of standardized project information is key to reduce payment delays. MUKTASoft’s key operational components include project finalization, wage-seeker registration, digital attendance tracking, expense logging, and payment verification. All of these are streamlined through user-friendly interfaces for different users, such as CBO and ULB officials, among others.

MUKTASoft was designed to improve the overall efficiency of local and state government officials with consideration of the administrative burden-related challenges. This was done by:

The simplification of project progress tracking and wage payment approval. It sought to move from more than twelve steps, as identified in the baseline, to a simple three-step approach for each key document, which would involve the maker, checker, and approver;

The enhancement of the visibility of project progress or delays in payments. This ensured that the responsible authority or individual takes accountability for the problems. It also enabled them to take steps to resolve these problems;

Faster payments to wage seekers through Smart Payments through direct integration with the state IFMS.

The alignment of project management and program verifications set the stage to integrate Smart Payments and use digital technologies, such as JiT-FS, for pull-based release of funds once project milestones were achieved. Core PFM principles, such as “single source of truth” (to ensure data accuracy), “observability” (real-time tracking of performance), and “minimization of administrative burden” through smart contracts, have been woven into the design of both MUKTASoft and JiT-FS to strengthen transparency, accountability, and efficiency in the system.

Deployment: Orchestration of a seamless implementation

The implementation phase required multiple dependencies’ management. A fundamental challenge was to build trust and reliability in the solution to replace manual ways of working because of its high success rate. The deployment timeline faced disruptions, and development hurdles were common initially, as is typical when new systems are integrated for the first time. However, collaborative testing uncovered edge cases that affected transaction success rates, and a robust user testing phase helped validate various scenarios and user needs.

Checks and balances were introduced and implemented within MUKTASoft and the JiT module to address these emerging issues. For instance, at the project finalization stage, MUKTASoft checks for the availability of funds to cover the project’s expenses. This sanction validation establishes a spending ceiling before the approval of projects or payments. This was a key control that the State Finance Department must maintain. Similarly, when payments are directly transferred to wage-seekers’ bank accounts, each transaction’s success or failure must be checked, and corrective measures must be taken where payments fail.

Local governments, while initially hesitant, saw that MUKTASoft’s use for project creation, estimate approval, and work orders had tangible benefits. These included reduced administrative burden, fewer delays, faster payments, and enhanced accountability. With a clear demonstration of the value to all stakeholders, the adoption of the solution became universal.

Maximized impact: Outcomes of successful deployment

Reduced delays: The digitization of processes from attendance tracking to payment verification dramatically streamlined workflows, which facilitated the disbursement of payments to wage seekers and CBOs. Pilot data indicates around a 60% reduction in payment disbursement time for wage seekers. Under the new system, beneficiaries no longer have to wait months to get paid, as most bills are now processed in a matter of days.

Enhanced efficiency: Automation freed local government officials from administrative burdens. This allowed them to focus on project management and monitoring and led to improved project execution and resource use.

Transparency and data-driven decision-making: The integrated data platform enabled real-time tracking of project progress, expenditure, and beneficiary coverage, which enhanced transparency and accountability for all stakeholders. Insights from real-time data facilitated informed decision-making for administrators. This allowed quicker identification and resolution of bottlenecks and strategic allocation of constrained resources.

Empowering wage seekers: Timely wage payments and improved project execution under the Smart Payments system enhanced urban communities’ livelihood opportunities and overall well-being.

Lessons learned:

The system is being scaled to 25 ULBS out o 115 in Odisha after the pilot’s success in two ULBs. MUKTA’s journey offers valuable lessons for other G2P initiatives that seek to use technology for efficient PFM and inclusive development:

Existing infrastructure matters: Wage seekers’ enrolment is simplified through Aadhaar’s use for identity verification. Wage seekers’ mapping to bank accounts is already in place, with Aadhaar linked to Jan Dhan UPI’s widespread use addresses concerns around cash in and cash out. MUKTASoft and JiT-FS are a new wave of innovations that rely on the building blocks provided by India Stack and related reforms.

Process streamlining is a key lever for any tech-enabled reform: When workflows are digitized, with automation and minimized manual intervention, the time and effort users have to spend on administrative tasks decreases. They can focus on tasks that require human interaction or attention. At the same time, data’s reliability and timeliness improve, which enables administrators to manage performance better, and policymakers can develop data-driven plans and strategies.

Active and consistent collaboration: Strong partnerships between government, technology providers, and frontline users, which include grassroots organizations, are essential for successful implementation. The solution will be used when stakeholders feel ownership over it. For this, they should be involved throughout the process, with their needs being prioritized in the product design.

Data fragmentation undermines progress at all stages: All stakeholders must accept a “single source of truth.” which they contribute to by ensuring that all transactions take place through a single system of record. Although, it may require some transition period to achieve this goal, data should be updated promptly in the system of record, with appropriate verification or triangulation.

Adoption requires users to trust the new way of working: Adoption is not instant. Extensive training and support are essential to overcome initial resistance. As each set of stakeholders sees the new system’s benefits, they will be more likely to use it and advocate for it with their peers. This can also be used in periodic retraining as trained resources move and new resources join the department.

Adaptability is essential: Unforeseen challenges are inevitable. Flexibility and a willingness to find solutions are crucial for successful implementation.

Other G2P programs can unlock technology’s transformative potential to deliver effective social safety nets, empower vulnerable communities worldwide through these lessons, and build upon MUKTA’s success.

Smart Payments as a catalyst for inclusive development

The early success observed with Smart Payments for the MUKTA program underscores technology’s transformative potential in G2P transactions to reduce delays in service delivery and heighten public finance efficiency. It serves as a model for government agencies and prompts them to adopt smart payments as a catalyst for inclusive development.

Odisha’s journey is a model for an efficient and citizen-centric benefit delivery system, which emphasizes the need for adaptive strategies, collaborative partnerships, and a commitment to governance principles. Tailored to the local context, the solution can progress from basic Smart Payments, that encompasses digital recording of conditional payments and compliances, to a medium level incorporating workflow management systems and APIs. The ultimate moonshot solution integrates artificial intelligence or machine learning models, smart devices, and Internet-of-Things (IoT) to revolutionize the public finance landscape.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

All these challenges have a negative impact on access to finance for African women entrepreneurs.

All these challenges have a negative impact on access to finance for African women entrepreneurs.