“Agent Lifecycle Playbook” is a comprehensive guide to ensure high-performing, resilient, and inclusive agent networks. This playbook is based on global insights, which outline effective practices across the full agent lifecycle. These include recruitment, onboarding agents, strengthening capability, liquidity, safety, and long-term viability. This playbook integrates a strong gender lens that offers strategies to support and scale women agents. It equips providers, policymakers, and ecosystem actors with actionable tools to enhance agent productivity and improve last-mile financial service delivery.

This playbook is developed as part of the project, “Scaling agent viability and quality,” funded by the Gates Foundation from 2023 to 2025.

Climate change is reshaping financial risk, yet conventional credit models too often penalize the very populations most in need of support. Farmers, small businesses, and low-income households in climate-vulnerable regions face higher costs, stricter terms, or outright exclusion — even when they invest in adaptation.

This article makes the case for climate-responsive finance with retooling risk models; scaling adaptive products; and aligning regulators, financial institutions, and development partners to build resilience. Ultimately, financing resilience is not just a social good — it is the strongest safeguard for the financial systems themselves.

Increasing Global Warming Means Increasing Financial Risk

Our world is on track for a 2.7°C rise by 2100. Over the past 50 years, the planet has faced an average of one disaster every day or two, linked to weather, climate, or water hazards, according to the World Meteorological Organisation (WMO). The number of such events has increased fivefold over this period, with 11,778 disasters recorded between 1970 and 2021. The economic toll has also mounted — with estimated losses of USD 4.3 trillion suffered over this period, with costs rising each decade.

The World Bank’s Findex 2025 report confirms what we at MSC have witnessed firsthand: Climate shocks have become routine for low-income communities. In low-income countries, 35% of adults reported experiencing a natural disaster or weather shock in the last three years. Two-thirds lost income or assets, and the poorest 40% were one-third more likely to be affected than others.

The cost of climate change is very much a financial one, as the developing countries, already vulnerable, are staring down future losses of USD 1–1.8 trillion annually by 2050 due to escalating physical climate risks.

As economies face the strain, financial institutions — especially banks — face it too. The growing physical risks impair the solvency of borrowers and reduce the value of collateral, increase default correlations, and create more systemic credit risk. To manage this risk, the Bank of International Settlements (BIS) suggests incorporating physical climate risks into banks’ credit risk models. This integration of physical climate risks into credit risk frameworks is designed to improve how banks evaluate loan performance in climate-affected geographies and sectors, and thereby reduce their exposure to underpriced climate risk.

But there is a catch. Existing models classify vulnerable borrowers — farmers, small firms, informal workers, low-income households — as inherently riskier. If adopted blindly, this suggestion from BIS could entrench this exclusion.

Banks respond to this classification with higher rates, tougher covenants, or outright loan denial, often ignoring borrowers’ adaptation efforts. Vulnerable populations are then locked in cycles of using high-cost informal debt to finance recovery, having insufficient resources to further adapt, and stagnation. This happens because high interest rates trap them in debt cycles, diverting income from productive uses. With no savings or credit buffers, they remain unable to invest in adaptation or upward mobility, perpetuating stagnation. At the macroeconomic level, this not only hurts climate adaptation but also a country’s economic growth.

Financial Products Need to Evolve to Take Account of Adaptation

Financial institutions often do not have climate-change-responsive products for climate vulnerable populations. For many customers, climate change has become a barrier to economic growth, as financial institutions often avoid serving them or lack appropriate products tailored to their needs. We found evidence of this in Bangladesh, where customer savings withdrawal increased and credit decreased following climate events.

This means that climate-vulnerable customers, often least responsible for climate change, face a triple financial hit:

Losses from climate events;

Limited access to financial services or access at higher costs (e.g., higher insurance premiums or underinsurance); and

At a macroeconomic level, public bailouts of distressed financial institutions placing an unnecessary burden on taxpayers and eroding customer trust in the formal financial system.

Many borrowers acknowledge their climate risks and even invest in resilience measures such as building flood defenses, raising homesteads and vegetable plots, or responding to drought with boreholes and water tanks. Yet, when they approach financial institutions, either for working capital after making such investments, or for credit to finance these resilience measures in the first place, they often face higher interest rates or outright refusals, since financial institutions rarely see such activities as directly income-generating.

In contrast, “climate-safe” borrowers, those in resilient geographies or with access to existing adaptive infrastructure, may enjoy lower rates, preferential loan terms, and access to green finance.

Over time, this bifurcation of risk-based lending will concentrate capital in resilient geographies and/or among resilient borrowers while starving high-risk areas of the financial resources needed to adapt. If credit risk models only account for climate risks without requiring a plan to address borrowers’ vulnerabilities or considering their adaptation plans, it will worsen their challenges. This underscores the urgent need for adaptive, flexible financial products that (i) respond to shocks, and (ii) balance the risk protection of both borrowers and lenders with affordable credit.

From Risk Avoidance to Resilience Building

A pivot from exclusionary risk models to financing adaptive measures and supporting high-risk borrowers, rather than sidelining them, will help reduce the huge, estimated, financial impact. For example, the U.K.’s Institute and Faculty of Actuaries project Global GDP losses of up to 50% between 2070 and 2090. Practical tools like the Climate Vulnerability Index can help unlock this capital, as can integrating climate risks into lifetime customer value, credit scores, and loan appraisals. Financial institutions should use climate risk models not just to redirect capital but to segment customers more effectively. With geolocation and sectoral data, banks can target vulnerable groups, farmers, small firms, and urban informal workers; and offer financial products that adjust to their circumstances, including flexible repayment schedules, weather-indexed credit, and microinsurance.

To better serve low-income communities, lenders can combine community-based lending models with digital data (such as mobile payments and satellite imagery) to assess creditworthiness beyond collateral. Public guarantees and blended finance can lower risk and attract private capital. Climate-smart credit lines, linked to adaptation actions (like water harvesting or crop diversification), can incentivize resilience. For this, institutions do not need to overhaul their product suites. Many providers can strengthen climate relevance simply by refining how existing products are positioned, structured, and supported. For instance, MSC’s 3R Strategy offers one practical pathway to do this. Institutions can repurpose existing products toward climate use cases; rejig them with flexible, season-aligned structures and early-warning protocols; and reinvent purpose-built offerings like disaster loans, emergency savings, and climate-smart agriculture loans. Finally, embedding financial literacy and insurance bundling within such products ensures sustainability and long-term inclusion.

This shift can be accelerated through blended finance and carbon finance, both critical tools to strengthen climate resilience, which are undergoing reform to improve how they perform. Blended finance, which uses a mix of public and private financing, while designed to de-risk climate investments, has been hampered by inefficiencies in multilateral climate funds. Carbon finance — instruments that channel funds toward emission reduction or carbon offset projects — was meant to add a revenue stream, but lost credibility after weak standards led to a race to the bottom, and is now being restructured to restore trust and effectiveness. Both mechanisms, despite their current deficiencies, hold significant potential if their governance frameworks, use cases, and applicability are diversified to better align with local contexts, emerging technologies, and adaptive financing models.

Alongside these, regulators can leverage RegTech (regulatory technology) to help financial institutions meet climate-related regulatory requirements efficiently, and SupTech (supervisory technology) to harness data and analytics for early warning, monitoring, and supervision of climate risks. Together, these tools enable the integration of borrower-level climate data into early warning systems, detecting emerging distress early, and ensuring lending frameworks foster equitable and resilient outcomes.

Parting Thoughts

Financing low-income communities and their adaptation requires not just loans based on a better understanding of their characteristics and needs; it also involves changes in other parts of the financial system. Scaling resilience requires guarantee funds, supportive regulation, and post-disaster mechanisms like moratoriums or loan restructuring. A promising innovation is the use of pre-approved disaster loans, released automatically in anticipation of extreme events, triggered by predictive models such as Google Flood Hub.

Governments, development partners, climate scientists, and civil society must coordinate to deliver affordable credit, insurance, and advisory services for low-income communities, reinforced by digital tools, capacity building, and policy incentives. In the end, though, customer resilience is the strongest safeguard for financial systems.

Akhand Jyoti Tiwari is a Senior Partner at MSC, with two decades of experience at the intersection of strategy, innovation, climate action, and inclusive development. His leadership has enabled MSC to forge high-impact partnerships, unlock new business opportunities, and expand its footprint across Asia, Africa, and the Pacific. A trusted advisor to governments, development partners, and private sector leaders, Akhand guides organizations in navigating complex transitions toward sustainability, inclusion, and resilience.

Ayushi Misra is a Sector Lead at MSC and manages work on financial policy, regulation, and inclusive service delivery. She focuses on advancing financial inclusion for low- and middle-income segments through inclusive product and policy design, impact investing, SME finance, and financial sector strategy. Ayushi has contributed to developing climate lending frameworks, sustainable credit lines, and risk-sharing mechanisms for green and inclusive growth.

This was first published on GARP on November 27, 2025.

India stands at a pivotal moment in its development journey, with the largest-ever cohort of educated, digitally savvy, and financially aware young women — many single, ambitious, and ready to lead. For the first time, they’re entering the economy with real access to banking and digital tools. But access alone isn’t autonomy. True empowerment begins when financial inclusion evolves into asset ownership, enabling women to shape their futures and achieve financial independence.

This shift from access to ownership is still a work in progress — but the Sukanya Samriddhi Yojana (SSY), launched in 2015, offers valuable lessons in how gender-intelligent design can accelerate asset creation, drive behavioural change, and scale inclusion.

Preventive inclusion pays dividends: Initiating girls’ financial inclusion during childhood helps preempt structural barriers for women and reduces the long-term costs of corrective policy interventions.

Design drives behaviour: Gender-intelligent products can reshape household saving patterns, directing resources towards girls and fostering sustained financial commitment to their futures.

Scalability within existing systems: SSY shows that gender-intelligent design is both feasible and scalable within mainstream institutions, creating opportunities to better serve underserved women.

While most policies for women begin in adulthood, like credit, cash transfers, or pensions, meaningful inclusion requires early lifecycle intervention. Early interventions allow time for accumulation and the magic of compounding to kick in, not just in numbers but also in terms of financial behaviour change.

SSY exemplifies a successful early lifecycle intervention. Accounts are opened for girls aged 0–10, with deposits continuing through adolescence (10–18) and maturing in early adulthood (18–25), aligning with education and marriage milestones. Partial withdrawals at 18 can fund higher education, while balances left beyond 21 continue earning interest. Since its introduction, the returns have consistently exceeded 7.6%, making it an attractive long-term savings option for parents. SSY has grown from 42 lakh accounts and ₹123 crore in deposits in 2014–15 to 3.5 crore accounts and over ₹3 lakh crore in 2024–25 with the national average deposit per account at ₹63,402. To put that in perspective, this corpus rivals the annual budgets of several Indian states.

Regional studies show that SSY has improved education equity and financial security for girls; and, parents’ preparedness for future needs. It changed aspirations from marriage-focused saving to investing in higher education. This behavioural shift mirrors global child-focused financial products like Singapore’s Child Development Account and UK’s Junior ISA. However, SSY is among the few globally to direct financial assets explicitly in the name of girls, correcting a historic gender gap in asset ownership.

The success of SSY also hinges on institutional participation. Post offices and banks have played a pivotal role in scaling the scheme and building trust. This is critical in a country like India, where gaps in women’s financial inclusion and asset ownership are particularly pronounced, underlining the need for banks to deploy and scale more gender intelligent products. Women remain the most unbanked and underbanked segment in India. IFC estimates credit demand among women-owned very small enterprises alone is ₹83,600 crore (approx. $11.4 billion). Demand for savings, investment, insurance, and pension products also remains underserved. SSY has helped post offices and banks attract substantial deposits for the government treasury, while earning commissions and making it a win-win for both financial institutions and women.

Post Offices manage about 68% of all 3.07 crore SSY accounts, thus leveraging their historic trust and large network. This demonstrates that gender-intelligent design can scale through established financial channels, integrating equity-oriented products into mainstream banking without need for parallel structures.

As SSY approaches its tenth anniversary, it presents a pivotal moment to expand its reach in lower participation states and evolve to meet the financial aspirations of today’s families. Enhancing the scheme by raising the investment cap and extending the 15-year deposit window can further strengthen its returns and long-term impact.

SSY is more than a savings scheme, it’s a blueprint for inclusive growth. It shows that policy can shift household behaviour. The next challenge is for financial institutions to sustain this momentum by creating gender-intelligent products that build trust, deliver long-term value, and make inclusion measurable and accountable for girls.

For policymakers, this means embedding gender intelligence into every layer of financial inclusion. For markets, it means women as mainstream economic drivers and designing solutions that truly serve their financial needs.

SSY 2.0 can continue to be a powerful instrument for gender intelligent financial inclusion transforming early savings into lifelong security for millions of girls.

This was first published on Hindustan Times on Nov 28, 2025.

Our new report looks at how digital platforms are reshaping microenterprises in Bangladesh across the retail, transportation, and social commerce sectors. These platforms emerged as major income sources for transporters and social sellers, while retailers relied on them most during the pandemic. Retailers prioritize buy-now-pay-later options; transporters depend on auto companies, while social sellers increasingly use platforms to establish connections with formal credit. Convenience features, such as doorstep delivery, return-trip support, analytics, and fair policies, strengthen loyalty. We explore these dynamics in more detail in the full report.

Conventional systems of crop survey, which include Girdwari, rely on manual record-keeping methods. This system faces multiple challenges, such as approximations, memory lapses, and damaged paperwork. The Village Revenue Officials (VROs) conduct Girdawari. They record crop details, reviews, and update land records, which include ownership information and revenue assessment. Additionally, as part of the crop survey, they follow a sampling method based on grid selection by the statistics department, with grids varying based on irrigated and non-irrigated areas.

While Girdwari remains essential for administrative purposes, it has significant limitations in terms of accuracy, timeliness, and standardization. Digital records of seasonal crop sowing in agricultural plots across the country are necessary to overcome these limitations. The crop sown registry under AgriStack provides a continuous recording system that records information at different stages of cultivation. The registry maintains a historical, plot-level record of key details, such as when, where, and what crops are planted in each cropping season. It creates a detailed record of plot-level agricultural activity.

This registry serves as a national database of all crops grown in the country. It lists their scientific and regional names and assigns each a unique crop ID. At present, crop data collected by states often differ in terminology and classification. For example, the same variety of paddy or maize may be known by several local names across districts, a variation that is reflected in state-level records as well.

The Crop Registry addresses this issue through a standardized taxonomy that ensures consistent and accurate crop records. Beyond standardization, the registry supports the discovery of new varieties and hybrids. New crops that emerge through local innovation or research can be added to the database with relevant metadata. This database ensures that India’s agricultural data ecosystem remains current and inclusive.

Once these crop taxonomies are standardized, the system can improve production forecasting, crop insurance pricing, and credit access. It also enables early warning systems for crop failure. Together, these improvements enhance interoperability across digital platforms and support better coordination among stakeholders.

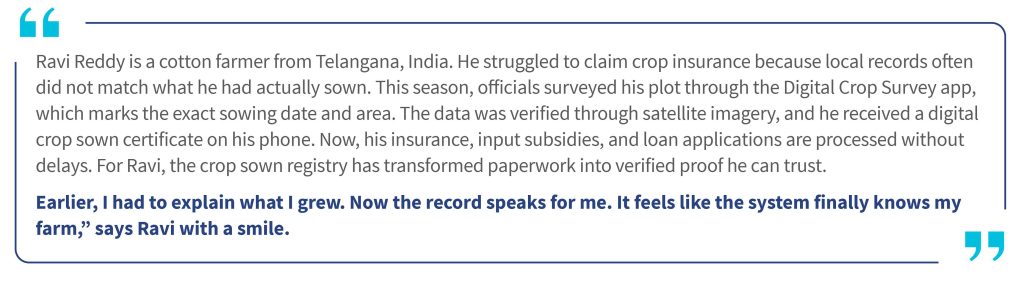

Built on this foundation, the Digital Crop Survey (DCS) application established the crop sown registry. The objective of the DCS is to obtain an accurate view of all crops grown on all land parcels nationwide. The application uses geofencing and AI-based image processing technology to ensure the legitimacy and reliability of data collected. This approach reshapes how farmers, government agencies, and businesses interact with agricultural data. The crop sown registry offers greater flexibility than earlier registries.

The registry also updates every crop season cycle based on the crops sown by the farmers on their plots. For every surveyed farm plot, it captures details, such as farmer ID, farm ID, village local governance code (LGD), year, cropping season, crop ID, sown area, date of sowing, and geotags.

The Government of India has developed a central reference application to conduct the DCS. States can either use the reference application or modify their existing applications to meet the technical requirements. The DCS application uses farmer and farmland data from the revenue records, along with geo-referenced village maps, to generate maps of owner plots and record crop sown information at the plot level. The village maps and farmland plot information are integrated directly into the crop survey system before each season. Once integrated with the farmer registry and the geo-referenced village map registry, it retrieves farmer details, farmland data, and geo-coordinates directly.

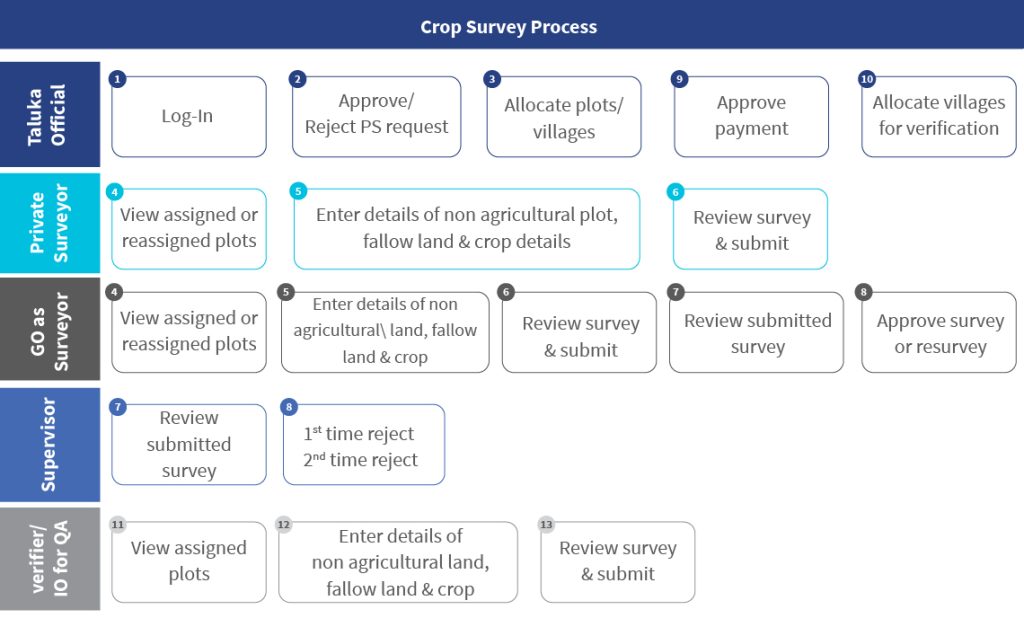

The DCS is a time-bound exercise, usually completed within 45 days of initiation. Surveyors collect and verify data in multiple stages, and supervisors review samples for quality assurance. Inspection officers also conduct mandatory checks on at least 20% of villages each season to ensure accuracy and consistency. This process ensures accuracy and consistency in the data collected. The central government or state governments will also appoint an inspection officer for quality assurance (QA). The inspection officers must perform QA checks on a minimum of 20% of the villages in each taluka every season. This layered review ensures data accuracy and consistency. This process ensures accuracy and consistency in the data collected. The central government or state governments will also appoint an inspection officer for quality assurance (QA). The inspection officers must perform QA checks on a minimum of 20% of the villages in each taluka every season. This layered review ensures data accuracy and consistency.

Despite its potential, the crop sown registry and the DCS implementation face multiple challenges that require careful planning and coordination. Some of the significant challenges are highlighted below:

Pan-India availability of digitized and geo-referenced maps:

The biggest challenge in the creation of a crop sown registry is inconsistent geo-referencing across states. Some have precise data at the plot level, while others only map at the village level, which affects accuracy. If major shifts in geo-referencing remain unaddressed, data will be recorded against incorrect plots. Standardized nationwide geo-referencing is crucial to track crops, yields, and trends effectively.

Complexity of land ownership issues:

One of the major issues with the digital crop survey is land ownership. There are situations where the land is in the name of a family member. Yet, the legal heir carries out cultivation. The subdivision may not reflect as a single plot on the map. Additionally, land possession often differs from the official owner listed in the record of rights. These land issues must be kept aside for crop recording. The government conducts surveys against the plot instead of the owner’s name, so in the owner’s name column, it appears like “owner of plot no. 10.”

Complexities in crop taxonomy:

Diverse crop varieties across regions present a significant challenge due to the presence of numerous sub-varieties and hybrids. Accurate documentation requires detailed data collection, agronomic expertise, and efficient processes. Streamlined data entry, proper training, and validation are essential for accuracy.

Integration of states with the existing DCS apps:

The integration of the DCS apps by states with existing digital survey systems, such as the MP Kisan app in Madhya Pradesh, the e-Pik Pahani in Maharashtra, or the Bele Darshak in Karnataka, poses a significant challenge. These states already have well-established and mature DCS applications, each with its unique platform, database schema, and architecture. The seamless integration of these diverse systems into a unified registry requires careful consideration and a clear migration strategy.

These challenges must be addressed to ensure reliable data for policymaking, effective resource allocation, and targeted support programs for farmers.

Overall, the DCS app provides farmers with digitally verified crop sown certificates, which serve as proof to avail services, such as credit, insurance, etc. These certificates also allow farmers to sell their harvest in advance at competitive procurement rates. Furthermore, the crop sown registry enables governments to estimate the market supply of various crops. This data supports decisions related to export and import as well as the allocation of food grain for industrial purposes, such as ethanol production. From a broader perspective, the system creates a win-win situation.

Over time, decisions that previously relied on estimates will be based on verified data. The crop sown registry will become a single source of truth for what India grows each season. Data consolidation and stakeholder alignment across the country pose significant challenges. Yet, the benefits of clear crop records justify the effort.

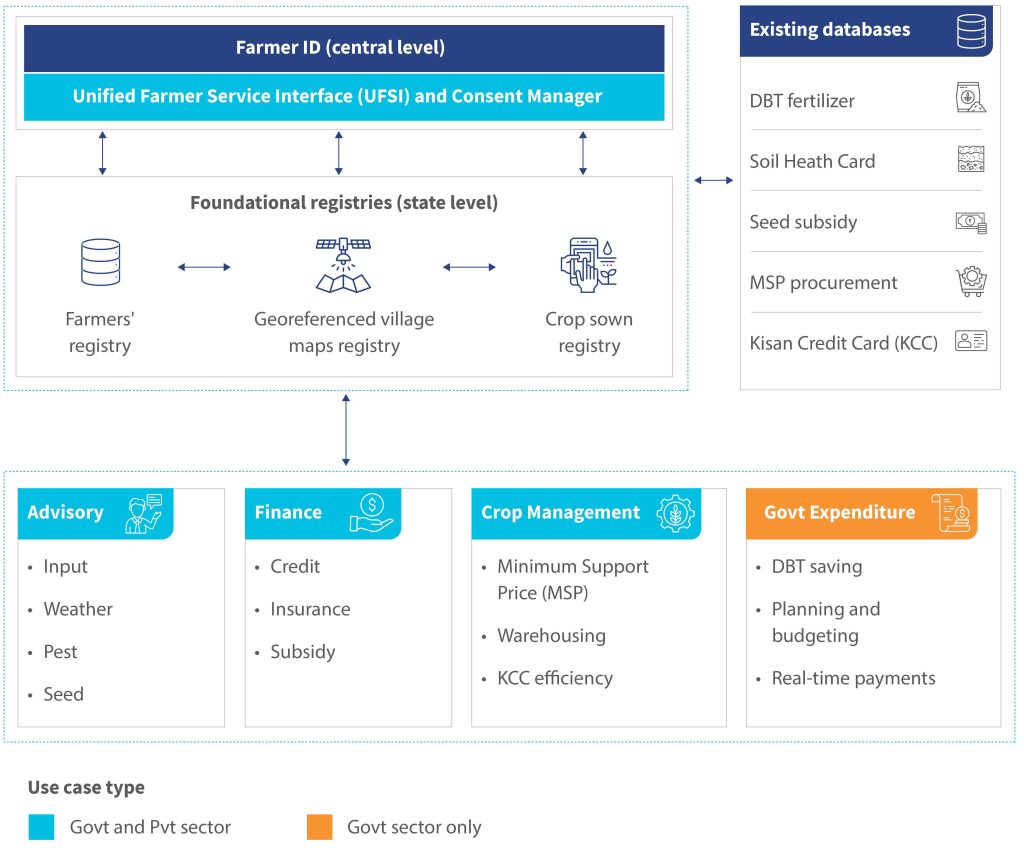

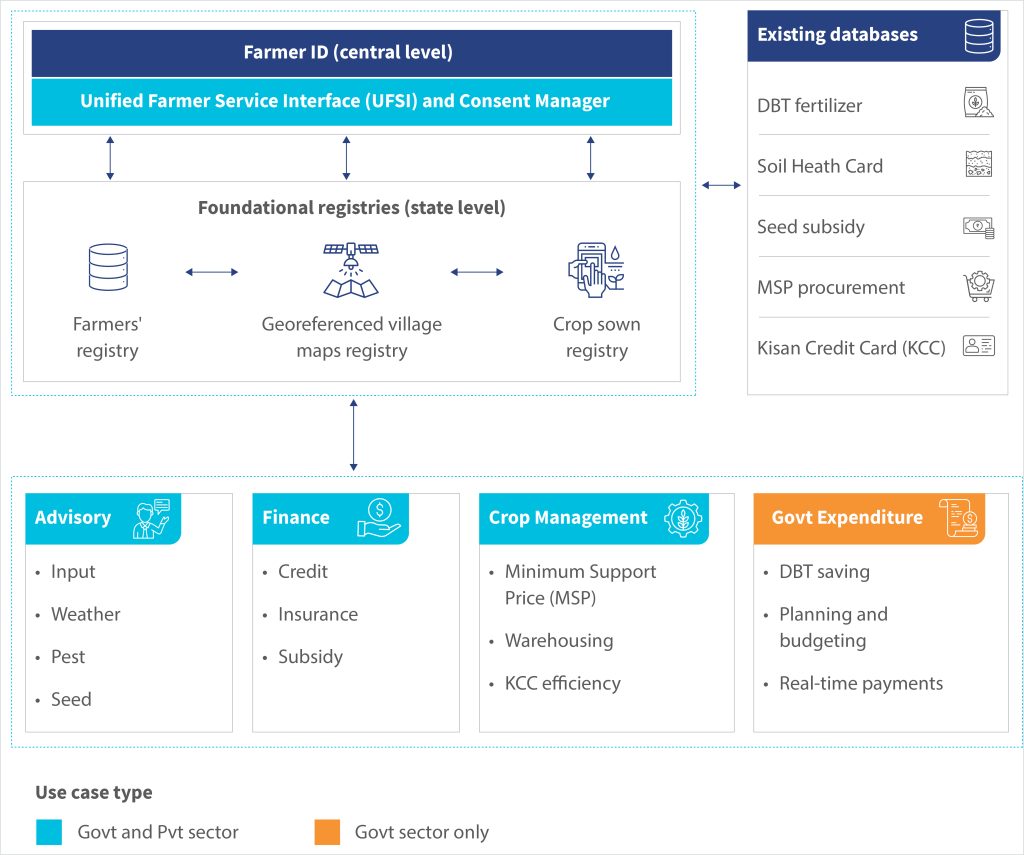

Together, the three foundational registries form the core of AgriStack. These registries interconnect to create a unified, reliable view of farmers, their land, and what they grow. When combined, they enable better planning, timely advisories, efficient delivery of benefits, and more transparent agricultural programs. The illustration below shows how these registries connect with existing databases and support a range of use cases across advisory, finance, crop management, and government expenditure.

As discussed in the previous blog, the state farmer registry will help identify all the farmers and the agricultural land parcels they own. Textual data on landownership is fetched digitally from the revenue records. This blog addresses the second question: Where are these agricultural land parcels located? The blog further explores the creation of a geo-referenced village map registry in India, and highlights the need to identify land locations and boundaries accurately.

Land has always been central to governance and taxation in India. The Mughals introduced early reforms, while the British later formalized systems, such as Zamindari, detailed land surveys, and revenue maps. At independence, India inherited these structures along with a reliance on manual records maintained by local revenue officials. Although these practices laid the foundation for land ownership and taxation, they also left behind fragmented and inconsistent records that continue to impact land management today.

After India’s independence, state revenue departments manually maintained land titles through local revenue officers called Patwaris. These revenue officers were responsible for managing all land rights tasks at the village level. They regularly updated the revenue records and cadastral maps after every change or “mutation”. Despite the manual maintenance of these records, the digitization of maps and records began only with the launch of the National Land Records Modernization Programme (NILRMP) in 2008.

The creation of a farm (geo-referenced village map) registry is essential to spatially identify and verify each land parcel boundary with geographic coordinates. This registry also supports digital crop surveys, precision advisory services, and evidence-based planning and research. For instance, in a digital crop survey, accuracy depends on the link between every land parcel in a village and its precise location on the map.This link ensures that surveyors record crop details for each plot through direct visits, rather than complete the entire survey from a single location that may even lie outside the village.

A geo-referenced village map registry enhances agricultural planning and service delivery when it links precise land boundaries with farmer and crop data. The combination of cadastral information with satellite imagery and ground truthing through GPS or drone-based surveys creates regularly updated, high-resolution spatial layers. This connection makes advisories more relevant, manages resources more efficiently, and delivers benefits to the right farmers. Key advantages include:

Improved agricultural advisories and farm management: Integration of geo-referenced maps with geographic information system (GIS), crop registry, and weather data enables real-time, location-specific agricultural advisories. This helps farmers increase yields and resilience and supports crop monitoring, early disease detection, and resource optimization.

Reliable land ownership information and effective land management: When digital maps are linked to the farmer registry, every land mutation or subdivision can be reflected spatially in near real time. This improves targeting, reduces disputes, and enhances transparency in land administration and the delivery of benefits.

Data-driven policy choices and market linkages: Geo-referenced maps and integrated land–crop data support better agricultural policies, crop diversification, and precision resource planning. They also strengthen market linkages that help farmers access nearby markets, track real-time prices, and reduce dependence on intermediaries, which ultimately improves profitability.

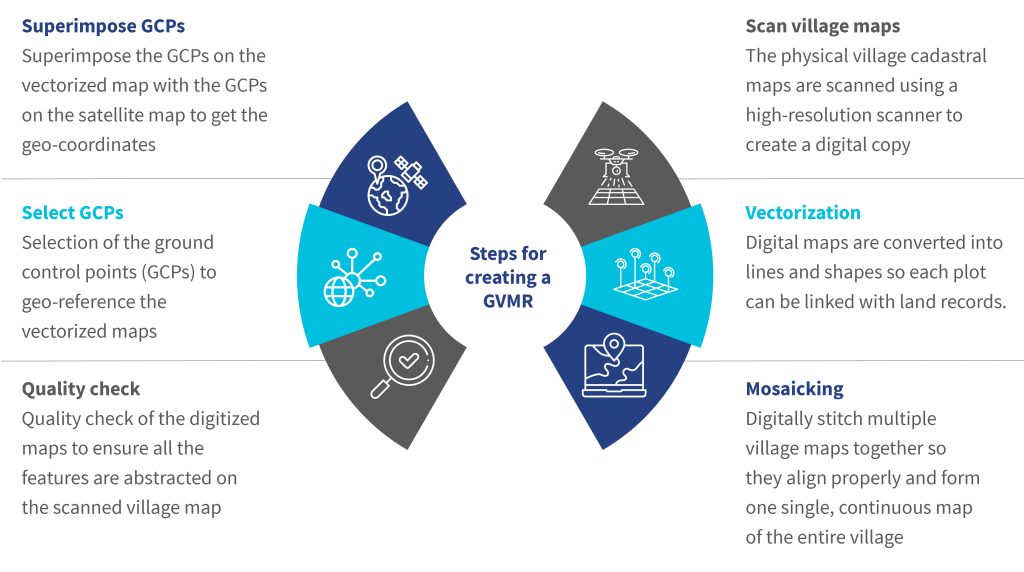

Creation of such a registry requires a series of technical and administrative steps. The ideal method is to capture fresh ground control points and physically map every individual land parcel that uses differential GPS or drone imagery. However, this is not always feasible due to costs, geographic terrain, data maturity constraints, and limited technical capacity. In such cases, states digitize the present cadastral maps and georeference them through satellite imagery. The process to digitize and georeference a village cadastral map can be broadly divided into six key steps, as outlined below:

Despite substantial government efforts, gaps persist in efforts to achieve complete digitization, integrate cadastral maps with ownership records, and update real-time geo-referenced data. It is crucial to bridge the following gaps to enhance data accuracy, interoperability, and service delivery to farmers:

Inaccurate physical maps: Many physical land records are old and not regularly updated. The government often fails to accurately reflect the actual situation on the ground due to delays in map revisions.

Errors in manual maintenance of maps: During manual updates of land records and maps, human errors can occur. These errors result in incorrect information being displayed on the maps about the land parcel. For example, during mutation, manual updates to maps can result in errors, such as misplaced plot boundaries or incorrectly entered survey numbers.

Inconsistent land records: There are mismatches between the revenue records, field maps, and actual possession. These mismatches and land ownership disputes complicate land parcel ownership definition and the finalization of the digital village maps.

Errors in scanning and vectorization: Old paper maps may be damaged, faded, or poorly aligned, which can introduce distortions during the scanning process and compromise the precision of boundary markings. Additionally, low-resolution scans produce blurry lines and illegible text, which makes precise geographic information difficult to extract during the vectorization process.

Missing reference points in cadastral maps: Physical cadastral maps are difficult to match with actual locations since many rely on reference points. These include roads, trees, or landmarks that may have changed or vanished over time.

States across India have focused on efforts to digitize and geo-reference village cadastral maps through consistent mapping standards to address these challenges. This ensures spatial accuracy and interoperability across platforms. Some states have obtained high-resolution Cartosat-2 satellite images, while others have procured WorldView-2 satellite images for georeferencing.

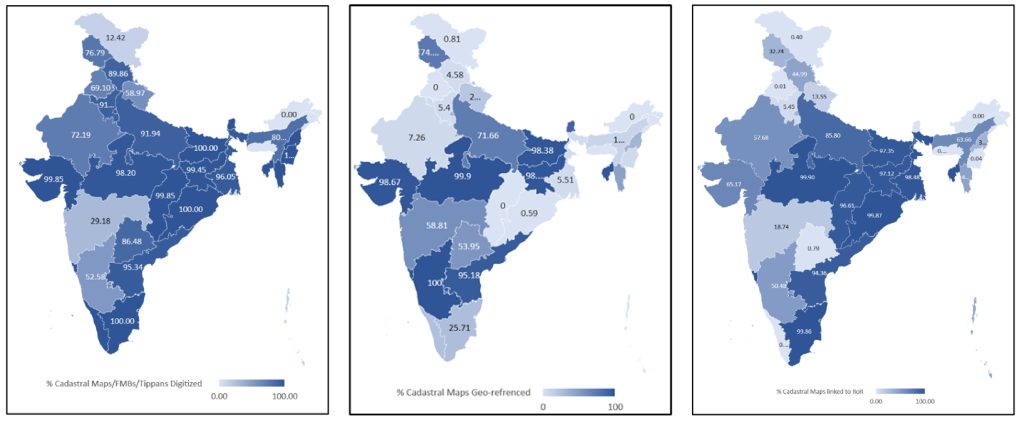

Several states have also used drone-based mapping to capture fine-scale ground details where satellite imagery is insufficient. At the same time, a few states also conduct a special survey and settlement process to accurately depict on-ground situations and geo-reference plots. As of now, more than a dozen states have completed the digitization of all village cadastral maps and are at various stages of geo-referencing.

The integration of digitized maps with the farmer registry will provide a comprehensive profile of a farmer’s land, as the ownership data and the geo-referenced boundaries of the land parcel will be mapped to it. As part of these initiatives, Indian states have started to digitize and geo-reference village cadastral maps.

Once these digitized maps are integrated with the state farmer registry, each farmer’s landholding will have a unified spatial-textual identity. This identity combines ownership data from the revenue records with the exact digital boundaries captured through the cadastral maps. This unified record will enable instant verification of land ownership, reduce duplication, and support spatial analysis for planning and governance. Accurate, digital land maps are essential to improve farmer-focused services, such as region-specific crop insurance, customized weather updates, and location-based crop advisories.

The georeferenced village maps registry along with farmer registry and crop sown registries, forms the foundation of AgriStack. Together, these foundational registries integrate spatial, ownership, and crop data to create a unified view of Indian agriculture. Once combined, these registries will support a wide range of use cases across advisory, finance, crop management, and government expenditure, which benefits public and private sector stakeholders.

The illustration below shows how the three foundational registries interact within the AgriStack ecosystem to drive this transformation.

In the next blog of this series, we will discuss the crop sown registry in more detail.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.