Bangladesh’s digital finance revolution is often praised for its scale. According to a Transparency International Bangladesh (TIB) report citing Bangladesh Bank, there are 237 million mobile money accounts and 1.83 million MFS agents nationwide as of December 2024.

This has built one of the largest and most active digital payment ecosystems in the world.

Yet beneath this achievement lies a structural flaw that deserves urgent attention: Historically fewer than 1% of MFS agents are women. This figure is not a gender statistic to be filed away; it is an economic warning sign.

In any modern service-driven economy where value is created through interaction, participation, and service exchange, women cannot remain only consumers of financial services. They must also be part of its delivery infrastructure. Otherwise, the math of inclusive growth simply does not hold. In today’s economy, excluding women from the delivery layer of finance means excluding them from the core engine of economic growth itself.

Half the users are women. Almost none of the providers are

According to a TIB analysis of Bangladesh Bank data, as of December 2024, women now hold around 42% of Bangladesh’s mobile financial services accounts.They use mobile money to receive remittances, manage household transactions, run small enterprises, and increasingly participate in e-commerce.

Yet the frontline that powers this system, MFS agents handling cash-in, cash-out, merchant payments, and G2P transfers, remains almost entirely male. Unlike agent banking, which has a 50% mandate for female agents, the MFS ecosystem has no such requirement and continues to replicate a male-dominated structure. The result is a digital economy where women are permitted to consume but are effectively excluded from producing and delivering financial services. An economy built on one-sided participation cannot be inclusive or efficient.

Digital finance is a missed employment engine for women

This exclusion matters because digital financial services represent one of the easiest labour-market entry points for women in Bangladesh. Becoming an MFS agent does not require high literacy, large capital, significant mobility, or formal employment conditions. It allows flexible, community-based work that is compatible with household responsibilities and can evolve into stable micro-entrepreneurship.

For millions of women, especially youth and home-based entrepreneurs, this role could offer a rare pathway to income generation and formal economic participation. Bangladesh is foregoing this economic opportunity not because women are unwilling, but because the system is not designed for them.

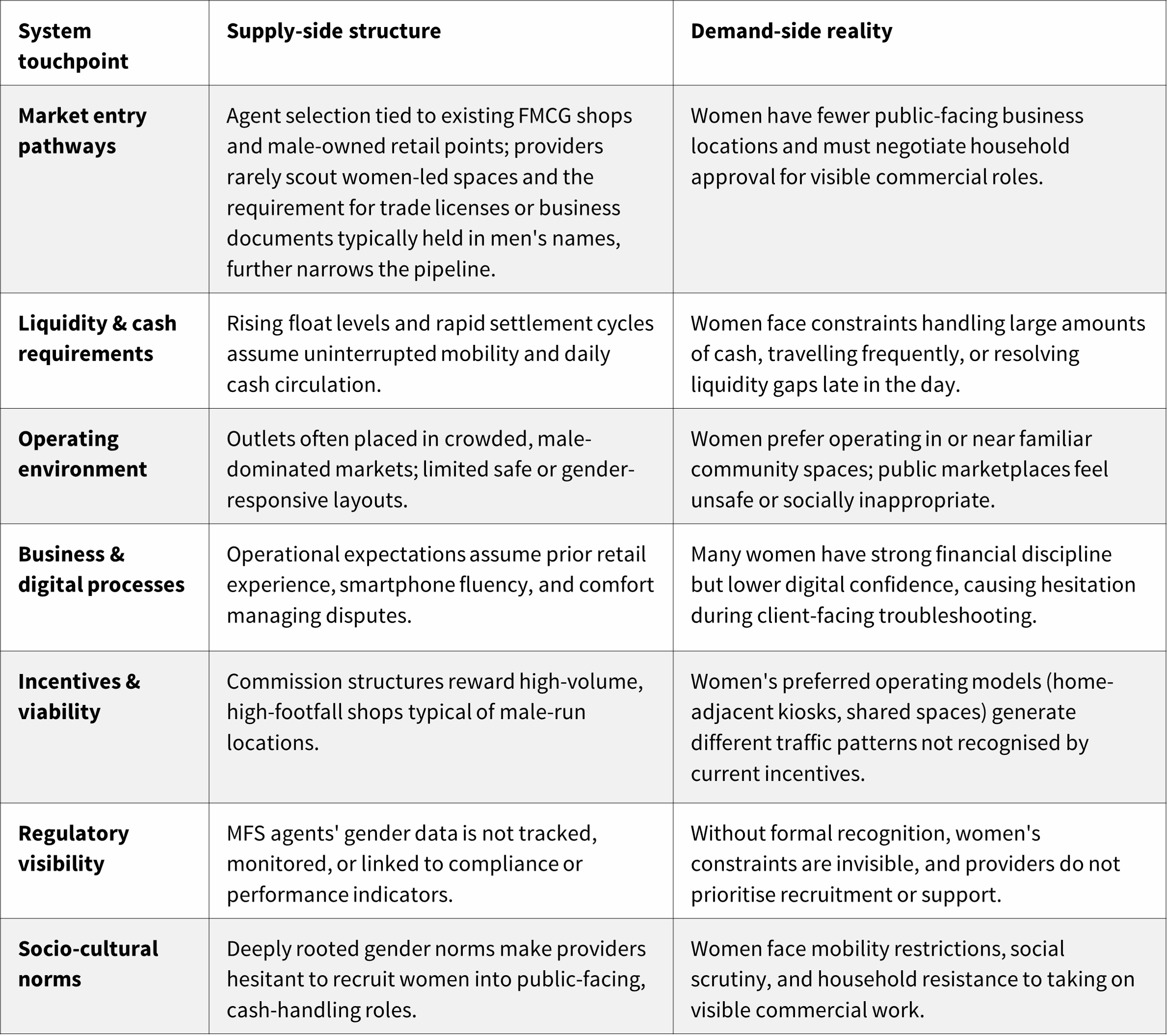

The problem is the system design

Providers often argue that “women do not apply” or that women struggle with liquidity, safety risks, or high-footfall business requirements.

But evidence from India, Nigeria, East Africa, and Bangladesh’s own women-led agent pilot tells a different story. CGAP experience from markets such as Kenya and Nigeria shows that when female agents are supported with appropriate liquidity mechanisms, safer operating environments, and proximity-based models, they perform on par with or better than their male counterparts, despite having less working capital and mobility.

When the operating model aligns with women’s realities, community-level locations, tailored liquidity support, safer training environments, and incentives not tied solely to high-footfall markets, women not only participate, they excel.

They build higher trust with customers, convert dormant accounts into active users, manage compliance more reliably, and reduce churn.

The real issue is that the current agent model in Bangladesh is built around social norms: Retail spaces owned by men, mobility-heavy cash cycles, long operating hours in male-dominated marketplaces, documentation and trade licenses in men’s names, and training formats that assume freedom of movement.

When these structural assumptions go unquestioned, women appear “unsuitable” when in reality the architecture itself excludes them. A system designed for one demographic will always reproduce that demographic.

Women agents make business sense

Countries that have invested in women-led agent networks have demonstrated clear commercial returns.

In specific market programs, female customers have been significantly more likely to transact with women agents. According to World Bank research, in the Democratic Republic of Congo, women customers were about 1.5 times more likely to use female agents, boosting transaction volumes. In Bangladesh, evidence from MicroSave Consulting’s SATHI Network evaluation report on women-led agent networks shows that female agents routinely handle 15-20 transactions per day across mobile financial services and agent banking, earn stable monthly commissions, and attract a disproportionately high share of women customers driven by trust and comfort at the point of service.

Female customers who hesitate to seek assistance from male agents show higher comfort levels with women agents, which increases transaction volume and reduces dependency on informal intermediaries. This creates positive network effects: More women agents lead to more active women users, which increases ecosystem liquidity and digital commerce. The benefits are economic, not symbolic.

Breaking the 1% barrier is an economic imperative

If Bangladesh is to build a more inclusive and dynamic digital economy, it must redesign who gets to participate in the delivery layer of financial services.

This requires a coordinated shift across policy, provider design, and ecosystem partnerships including gender-responsive MFS agent guidelines, simplified KYC and licensing pathways for women-run, home-adjacent outlets, recruitment through women-focused MFIs and community networks, and safer, community-centric operating models.

The economic case is straightforward. A digital economy where women account for nearly half of users but over 97% of providers are men is structurally unbalanced.

It suppresses participation, weakens trust, keeps millions of women dependent on intermediaries, and slows the expansion of digital commerce.

In an era where economic value is increasingly created through service delivery, human interaction, and digital participation, not just production, this imbalance is costly.

Women already drive a substantial share of Bangladesh’s digital financial activity. What remains unsettled is whether they can be empowered to shape, deliver, and fully benefit from the very systems they sustain.

Bangladesh’s next phase of inclusive growth will be determined not by how many women use digital finance, but by whether they are allowed to build it, lead it, and profit from it.

This was first published in “Dhaka Tribune” on 8th Jan, 2026.