Women-owned micro, small, and medium enterprises (MSMEs), persons with disabilities, and green entrepreneurs continue to face barriers in accessing financial services in Indonesia. Many of these businesses are still assessed through conventional credit criteria, which may not fully reflect their business potential, risk profile, or contribution to inclusive and sustainable growth.

This user guide is developed under the FinClude Green program, a collaboration between Terala Foundation and MSC (MicroSave Consulting) with support from KINETIK. This guide addresses this gap by providing a practical approach for financial ecosystem actors to conduct more inclusive initial loan assessments. It is also designed as a hands-on reference for institutions that seek to integrate gender equality, disability, and social inclusion (GEDSI), and green considerations into their financing practices.

The guide presents an integrated GEDSI and green credit assessment approach that helps financial institutions better understand underserved customer segments and apply more context-sensitive lending decisions. It includes practical tools, checklists, and references to standard operating procedures. Together, these resources help institutions review their existing portfolios, identify customer needs, and assess loan applications through a more inclusive lens.

The user guide combines GEDSI perspectives with green criteria. It helps financial institutions look beyond standard credit requirements and consider the broader conditions, needs, and opportunities of women-owned MSMEs, persons with disabilities, and green entrepreneurs. The guide offers a starting point to strengthen inclusive credit assessment practices. It also supports fairer, more accurate, and more sustainable financing decisions for underserved entrepreneurs in Indonesia.

At a landing site on Lake Victoria, the day begins before sunrise. Boats return. Buyers gather. A quiet negotiation begins before the fish changes hands. Adhiambo, a teenage girl, stands at the edge. She waits for a trader who controls whether she can get fish to sell and earn enough to take food home. The rule stays unspoken yet understood. Access to fish depends on access to her body. Everyone present knows how the system works.

This is the second blog in a two-part series.Blog 1examined the structural drivers of safeguarding failure in fisheries communities. This blog outlines what programs must do differently.

The vulnerability that development programs encounter in fisheries communities is embedded in market structures, community infrastructure, and the life cycles of the people those programs serve.

Genuine safeguarding must, therefore, begin earlier, reach deeper into communities, and connect directly to program design rather than remain a compliance exercise.

Interventions must begin in schools rather than in workshops

The single highest-leverage safeguarding investment a fisheries program can make is to keep girls in school and to influence what boys learn while they are there.

Research in Siaya County, Kenya, has established a direct relationship between fishing activity and school dropout rates among girls. Once a girl leaves school, economic and sexual vulnerabilities increase rapidly. Programs should establish or contribute to scholarship pipelines that target children, particularly girls, in their areas of operation. This is safeguarding infrastructure and should be treated as core program design.

Beyond retention, programs should partner with local schools to integrate age-appropriate education on body autonomy, consent, and healthy relationships into curricula. Programs must be codesigned with teachers and community leaders. Girls need to learn early that jaboya is not a market law but a power imbalance that can be named and refused. Boys must learn that exploiting a woman’s economic desperation constitutes abuse and not entitlement or negotiation.

Diversify economic options to reduce dependency and risk

Jaboya does not persist because women lack awareness. It persists because, for many, the alternative is no fish and no income. When fishing is the only visible livelihood, fish scarcity becomes a total crisis, which deepens safeguarding risks.

Programs can expose young people to realistic, lower-barrier alternatives through career talks and livelihood showcases. Sector-adjacent options, such as fish processing, cold-chain logistics, and boat repair, reduce dependency on the daily catch without abandoning the community’s economic identity.

Digital opportunities deserve a place as well. Content creation and mobile commerce are accessible to any young person with a smartphone. MSC’s analysis of youth entrepreneurship consistently shows that combining economic opportunity with skills, mentorship, and market linkages is far more durable than access to finance alone. The goal is to keep communities in fishing while ensuring that it remains a safe choice rather than becoming a trap.

Build physical infrastructure as a core safeguarding feature

Blog 1documented the WASH deficit at most landing sites. For women and girls, this entails a daily risk of protection rather than mere inconvenience.

Organizations should treat investment in gender-segregated, lockable sanitation and bathing facilities as a core safeguarding expenditure. Where budgets do not allow direct investment, organizations should advocate with county governments, water authorities, and infrastructure donors to secure these facilities. Programs cannot credibly claim to protect women while leaving them exposed to menstruation without privacy. The physical environment forms part of the protection framework.

Build community-led protection systems that outlast the project

Formal reporting mechanisms, such as hotlines, safeguarding officers, and written complaint processes, frequently fail at landing sites. They are distant, often unknown, and mistrusted by communities with long experience of institutions that do not follow through.

Programs should invest in community safeguarding champions. Trusted local individuals can receive concerns, provide first-line support, and escalate cases appropriately. Jaboya is sustained by demand, and efforts to change that demand must engage men and youth as community champions.

Peer mentorship is equally important. Evidence from MSC’s gender-inclusive aquaculture work in India and from Nyamware Beach on Lake Victoria confirms this finding. When women gain control over productive assets, such as boats, savings groups, and processing infrastructure, they shift power dynamics more durably than training alone. A protection system succeeds only if it remains after the program team leaves.

Integrate psychosocial support to address existing harm and future risk

Safeguarding frameworks must address existing harm as well as future risk. Frameworks that fail to do both remain incomplete by design.

MSC’s work on meaningful financial inclusion for women has consistently shown that the physical, social, and psychological barriers women face cannot be addressed by economic programming alone. Psychosocial dimensions must be embedded into program design.

Communities experience high levels of trauma where jaboya is normalized, housing offers no privacy, and economic precarity is constant.

HEDSO’s mental health programming directly links the jaboya system to depression, anxiety, substance abuse, and suicidal tendencies among young women. A UNICEF-commissioned report by ODI and LVCT Health found that one in three adolescent girls aged 15 to 19 in Homa Bay County are mothers or pregnant, which is nearly twice the national average.

Implementing organizations must identify available services and establish referral pathways before implementation begins.

For instance, LVCT Health runs a toll-free youth counseling hotline that is available 24/7. HEDSO delivers community-based mental health support across the lake region, and Farm Africa’s YISA program targets jaboya prevention through women’s asset ownership and cage aquaculture.

Mapping these services is necessary but insufficient, since most remain concentrated in county towns far from landing sites where risk is highest.

Program mapping may reveal that the nearest gender-based violence (GBV) counseling service is 45 km from a primary landing site. Such findings indicate systemic gaps in service provision rather than isolated safeguarding challenges. Programs should document these gaps and use the evidence to inform donor reporting, engage county governments, and shape policy discussions. Program learning should support system-level change and should not remain confined to safeguarding documentation.

Programs must also simultaneously advocate for decentralized outreach models, co-fund mobile or community-based psychosocial services where possible, and build first-aid psychosocial capacity into community champions. This ensures that some support exists at the landing site while longer referral chains are strengthened.

A framework for practitioners

The five interventions above extend beyond the scope of most safeguarding frameworks. Safeguarding and program design are not separate workstreams. The conditions that keep women and children safe in fisheries communities also enable economic empowerment programs to succeed. If safeguarding is to remain meaningful, it must address the conditions that make them vulnerable in the first place.

Before we finalize any safeguarding plan, we must ask:

Does our risk assessment name jaboya or equivalent transactional sex dynamics?

Does our community mapping include children under 18 who are already active in the fisheries economy?

Have we assessed WASH and housing infrastructure at our target landing sites, and do we have a response?

Are any school partnerships and scholarship commitments written into program design?

Do community champions include men and youth, and are they resourced to continue after project closure?

Are psychosocial referral pathways identified and functional before implementation begins?

Any negative answer indicates a need to redesign the program.

Samaki hukunjwa angali mbichi. If the fish must be folded while fresh, safeguarding must begin while the fish is still fresh, in schools, in communities, and in the design rooms where programs are built. It is at these entry points that risk can be reduced before it hardens into harm, and risks the lives of Adhiambo and many like her.

MSC works across financial inclusion, agriculture, fisheries, gender equality, and youth economic empowerment in more than 65 countries. Visit our library at www.microsave.net/library to explore fisheries finance work across Asia and Africa. The insights in this series are based on on-the-ground work with fishing communities.

Safeguarding has become a standard practice in development programming. Funders require it, implementing partners train on it, and reports refer to it daily. Safeguarding has meaningfully reduced harm when well-designed and contextually grounded. It has protected beneficiaries, staff, and communities from abuse and exploitation. But for fishing communities around Lake Victoria, safeguarding frameworks often feel as if they belong to a different world. Here, children learn to cast nets before they learn to read. Entire families share a single iron-sheet room. The lake serves as a kitchen, bathroom, and workplace.

There is a significant, often unacknowledged gap between safeguarding policy and safeguarding reality in fisheries communities across Sub-Saharan Africa. This blog examines the structural drivers of that gap. A second blog in this series will outline what fit-for-purpose safeguarding and program design should look like.

What safeguarding is and why fisheries are different

Safeguarding refers to measures designed to protect program participants from abuse, exploitation, neglect, and harm. It includes reporting mechanisms, codes of conduct, accountability structures, and protections against physical, psychological, sexual, and economic abuse.

Most frameworks assume that participants are adults with clear boundaries between home and work, and that vulnerability can be identified and contained. In urban financial inclusion or enterprise development programs, these assumptions generally hold.

In fisheries communities built around inland lakes in East and Central Africa, three structural realities consistently challenge these assumptions. The age at which people enter the economy, the exploitation embedded in the market system, and the physical infrastructure, or the lack of it, shape daily life.

MSC’s Gender, Equality, Diversity, and Social Inclusion (GESI) practice explicitly recognizes gender-based violence as a barrier to economic empowerment. Its impact on women’s mobility, agency, and participation in livelihoods cannot be separated from financial inclusion programs. MSC treats the safeguarding gaps outlined in the following sections as organizational concerns rather than donor compliance requirements.

The under-18 problem, when livelihoods begin before adulthood

MSC’s analysis of youth unemployment and economic participation in Sub-Saharan Africa finds that social, cultural, and structural barriers push young people into economic activity earlier than formal eligibility criteria allow. Gender and geography intensify this pattern, particularly for women and rural youth. In fishing communities, the pattern is more pronounced. The entry point is not eighteen.

Global Sisters Report has documented children as young as five working at landing sites. Along Lake Victoria, the boundary between childhood recreation and adult livelihood is almost nonexistent. By their early teens, many children catch, sort, sell, and reinvest in the fish trade. They are fully embedded in the fisheries value chain years before any development program would consider them eligible for support.

Most development programs define “youth” as individuals aged 18 to 35, in line with donor requirements and national legal frameworks. This definition leaves a 15-year-old exposed to an unregulated market, in which they face predatory actors and economic pressure outside the safeguarding framework. That reflects a structural blind spot with real consequences. Safeguarding design must catch up.

Jaboya: When the market demands the body

MSC’s work on meaningful financial inclusion for women finds that economic programming frequently reaches women without addressing the power dynamics that govern their participation in markets, leaving the structural conditions of exploitation intact while claiming inclusion. In fisheries, the starkest expression of that gap is jaboya, a sex-for-fish exchange documented across communities on Lake Victoria in Kenya, Uganda, and Tanzania. Similar practices appear in fishing economies across the Democratic Republic of Congo, Zambia, and coastal West Africa.

Women dominate fish processing and retail but rarely own boats or nets. When catches are low and competition is high, access to fish often becomes contingent on sexual favors, where fishermen hold the power to choose their buyers. This arrangement remains transactional and normalized in many landing-site economies. Sexual exploitation sits within the market structure that development programs enter when they work in fisheries.

A girl entering this economy at 12 or 13 learns its rules long before any safeguarding workshop reaches her. By the time that workshop reaches her, at 19, 25, or 30, she has spent a decade inside a system that teaches practices that conflict with the training.

The effects of these norms begin long before formal adulthood. As the Swahili saying goes, samaki hukunjwa ungali mbichi. The fish is folded while it is still fresh. If the shaping happens early, so must the intervention. This blog series examines this challenge.

Infrastructure and the architecture of vulnerability

The challenge extends beyond economic systems. It is also visible in the physical environments where people live and work. A phrase used among Luo communities around Lake Victoria captures the norm: “People of the lake do not fear one another’s bodies, because they have always shared the water.”

Communal bathing at the lakeside and the absence of physical privacy are not evidence of moral permissiveness.Scholars who study these communities consistently link these practices to generations of economic marginalization, limited infrastructure, and constrained living conditions. Safeguarding frameworks that ignore these realities risk misreading the context they seek to address.

The infrastructure deficit at most landing sites is severe.

Despite sitting on the shores of major water bodies, most landing sites have little or no sanitation infrastructure. Toilets, where they exist, are shared, unlit, and unsafe, particularly for women after dark. The UN Economic Commission for Africa has noted that women and girls manage menstruation, bathing, and personal hygiene in public or semi-public spaces. This creates continuous, daily exposure to harassment and assault, regardless of what any program’s safeguarding policy states on paper.

Programs that work in these communities must catalyze investment in gender-segregated, lockable sanitation and bathing facilities at landing sites. This is safeguarding infrastructure, which programs must include in protection frameworks, budgets, and advocacy agendas from the outset.

Housing conditions compound the problem. At many landing sites, entire families live in single iron-sheet rooms renting for the equivalent of a few dollars a month. Children are immersed in adult economic and social realities from an early age, often without protection or alternatives.

The gap reveals a structural problem

These three realities of economic entry, market-based sexual exploitation, and infrastructure deficits are the more prevalent problems as per the case argued in this blog, revealing a safeguarding gap that no code of conduct can close. The vulnerability that fisheries programs encounter is systemic. It is embedded into the market structure, the physical environment, and the lifecycle of the communities that programs serve.

Programs that carry only a policy document, without attention to these realities, arrive too late and are underequipped to address the structural drivers of vulnerability in fisheries communities.

These realities demand a broader view of safeguarding. We should look beyond reporting mechanisms and compliance requirements to address the environments, markets, and social systems that shape risk.

In the second blogof this series, we present what fit-for-purpose safeguarding looks like in fisheries communities. The approaches include early school-based intervention, scholarship pipelines, community-led protection systems, livelihood diversification, and psychosocial support. Programs must be designed with design choices that carry the safeguarding burden, rather than policy alone.

MSC works across financial inclusion, agriculture, fisheries, gender equality, and youth economic empowerment in more than 65 countries. Visit our library at www.microsave.net/libraryto explore MSC’s fisheries finance work across Africa and Asia. The insights in this series are based on field experience with fishing communities.

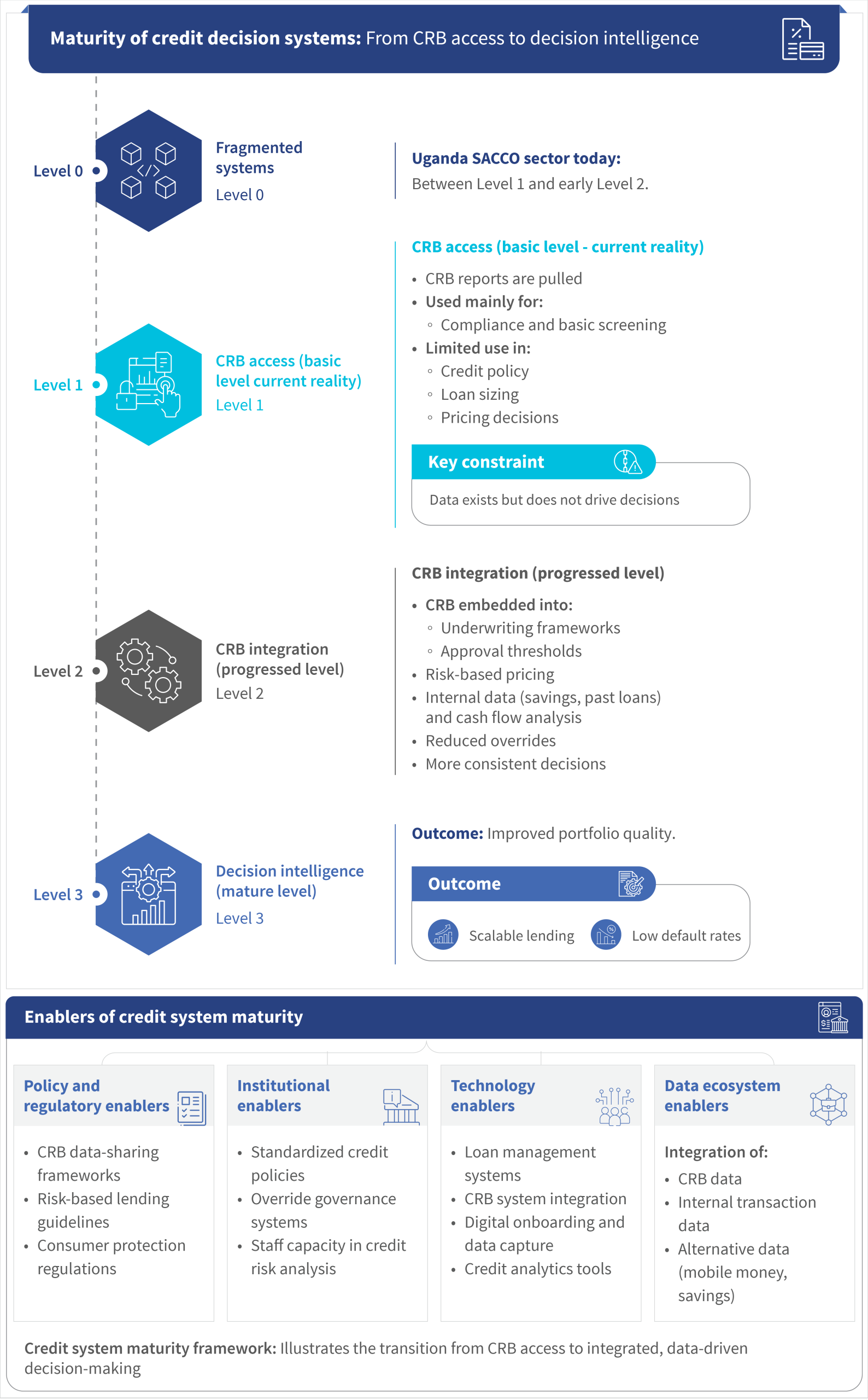

Uganda enters a new phase of formalization of its credit market. Recent data from the Bank of Ugandashows that the number of borrowers captured in the Credit Reference Bureau (CRB) systems increased from 2.9 million to 4.1 million between 2024 and 2025. During the same period, the credit inquiries rose by 28.4%, from 653,400 to 838,700. These trends reflect the growing use of credit data and risk-based lending across banks, savings and credit cooperative organizations (SACCOs), microfinance institutions (MFIs), and digital lenders.

At face value, this is a success story. Greater access to credit information should support better lending decisions and stronger repayment performance. However, emerging evidence suggests a more nuanced reality. While CRB use is associated with better performance, it does not guarantee stronger repayment outcomes.

It is vital to examine how lenders use CRBs in loan screening and how that shapes borrower behavior over time to understand the outcomes.

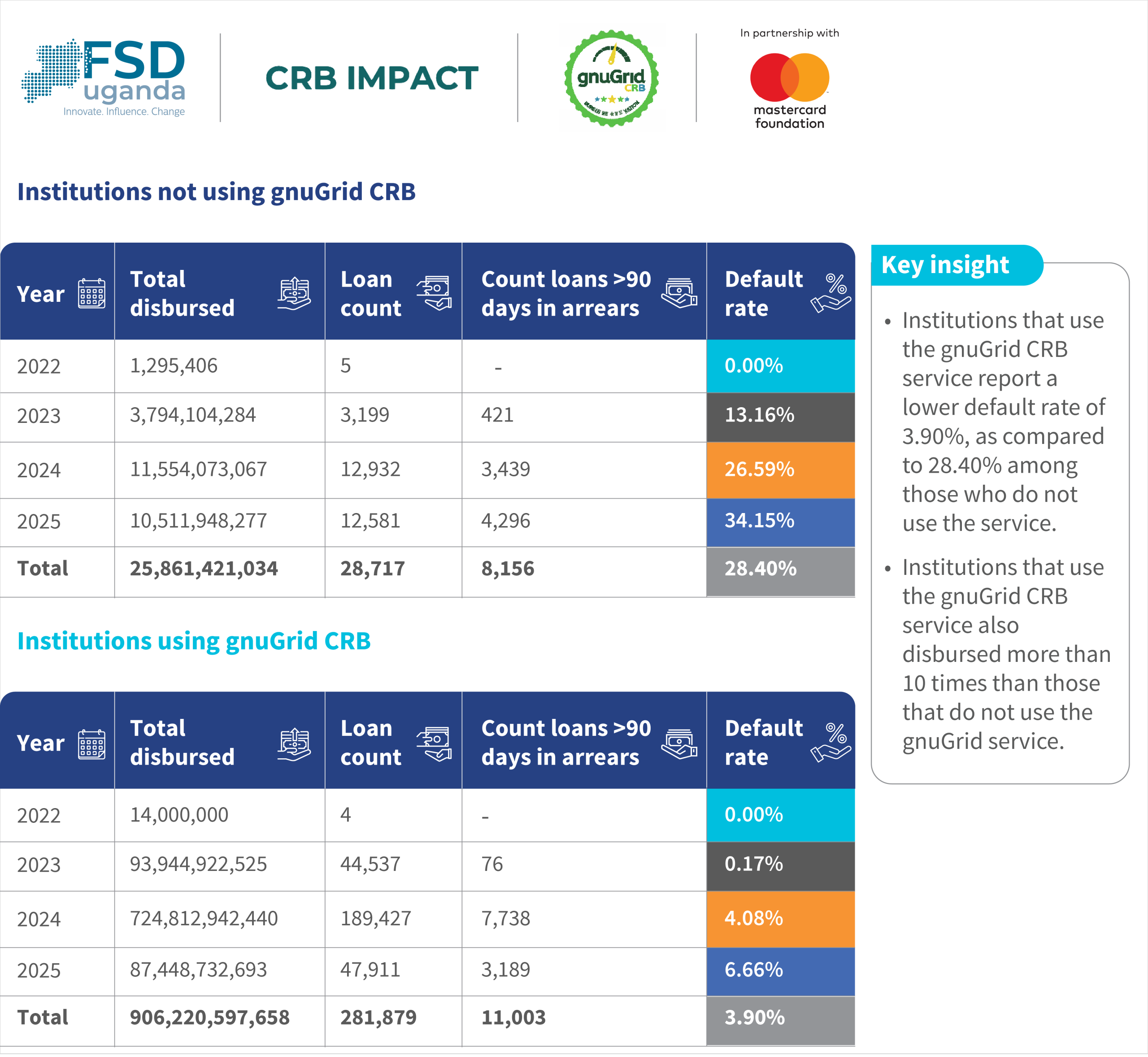

Data from Uganda’s credit market indicates higher performance among institutions that use CRB systems. Evidence from portfolios supported under the MSERF reinforces these findings. Institutions that use CRB systems report significantly lower default rates of around 3.9% compared to 28.4% among non-users.

Figure 1. Source: gnuGrid CRB

However, the relationship between CRB use and portfolio performance is more complex than it first appears. Between 2022 and 2025, MSERF disbursed UGX 99.34 billion (~USD 26.7 million) to 22 participating financial institutions. The facility reachedmore than 334,000 borrowers and generateda loan volume of UGX 381.24 billion (~USD 102.5 million). Despite this scale and widespread CRB access, portfolio performance remains uneven. Default rates among CRB users have increased over time, and outcomes vary significantly across institutions, even among those using the same CRB systems.The difference is not access to data, but how institutions use it.

The primary role of CRB data is to improve borrower selection.CRBs enable more informed credit decisionsby providing visibility into repayment history, outstanding obligations, and exposure levels.

Figure 2. How loan officers evaluate credit reports

However, in many institutions, CRB reports remain a procedural step. Staff pulls and reviews the reports, but they do not incorporate them into structured decision frameworks. Lending decisions continue to rely on personal judgment or informal criteria.

By contrast, high-performing institutions translate CRB signals into clear decision rules, such as score thresholds, rejection criteria, and risk-based loan structuring. These rules lead to more consistent borrower selection and better portfolio outcomes.

Evidence from the MSERF risk-based pricing (RBP) pilot illustrates how this transition plays out in practice. Analysis of matched loan portfolio data from the gnuGrid platform shows that, over time, structured SACCO scoring increasingly influenced pre-disbursement decisions, particularly between May and December 2025.

During this period, clearer differentiation appeared across risk bands. The CCC and DDD received the largest average loan sizes, approximately UGX 9.26 million (~USD 2,452.97) and UGX 11.45 million (~USD 3,033), respectively. Despite this higher exposure, these segments recorded the lowest levels of current delinquency by value. In contrast, weaker segments underperformed despite lower exposure. The EEE showed weaker repayment outcomes, and III exhibited the highest PAR30, PAR60, and PAR90 levels.

These patterns suggest that the scoring model effectively ranks borrower risk, and that value is realized when scores are actively used in pre-disbursement decisioning. When this occurs, scoring results in improved risk differentiation and more efficient credit allocation.

However, the effectiveness of such systems depends on use and on how scoring models are designed. Emerging evidence highlights several constraints that affect accuracy and fairness.

First, data source gaps can introduce structural bias. For example, when Mobile Network Operator (MNO) data is used only partially, borrowers on one network may receive an implicit advantage, while others are penalized despite similar behavior. In such cases, scores reflect data availability rather than true risk.

Second, static representations of risk, such as lifetime maximum arrears, can misrepresent borrower behavior. Borrowers who experienced temporary shocks, such as during COVID-19, may continue to be penalized even as their repayments improve. This weakens incentives for recovery and misaligns with the goals of programs, such as the MSERF, which aim to support resilience.

Third, the weighting of risk variables can unintentionally reinforce exclusion. For example, reliance on collateral as a primary risk determinant may disadvantage women, whose repayment performance is often strong, but asset ownership is limited. While SACCOs often mitigate this through guarantorship, these mechanisms are not always reflected in scoring models, creating a disconnect between actual risk mitigation and model outputs. These issues highlight that the value of CRB data is shaped by institutional use, model integrity, and contextual relevance.

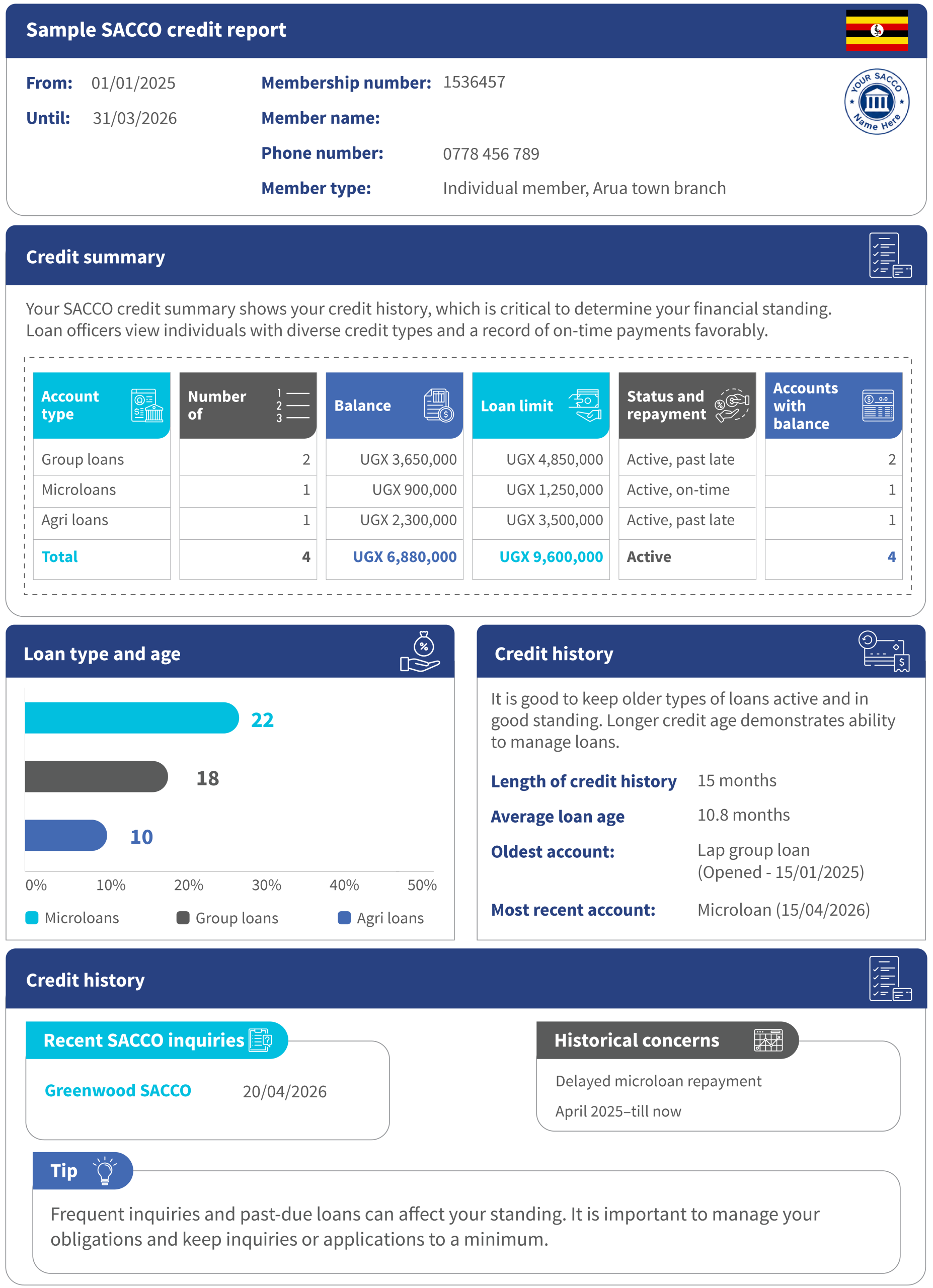

Figure 3: Sample SACCO credit report

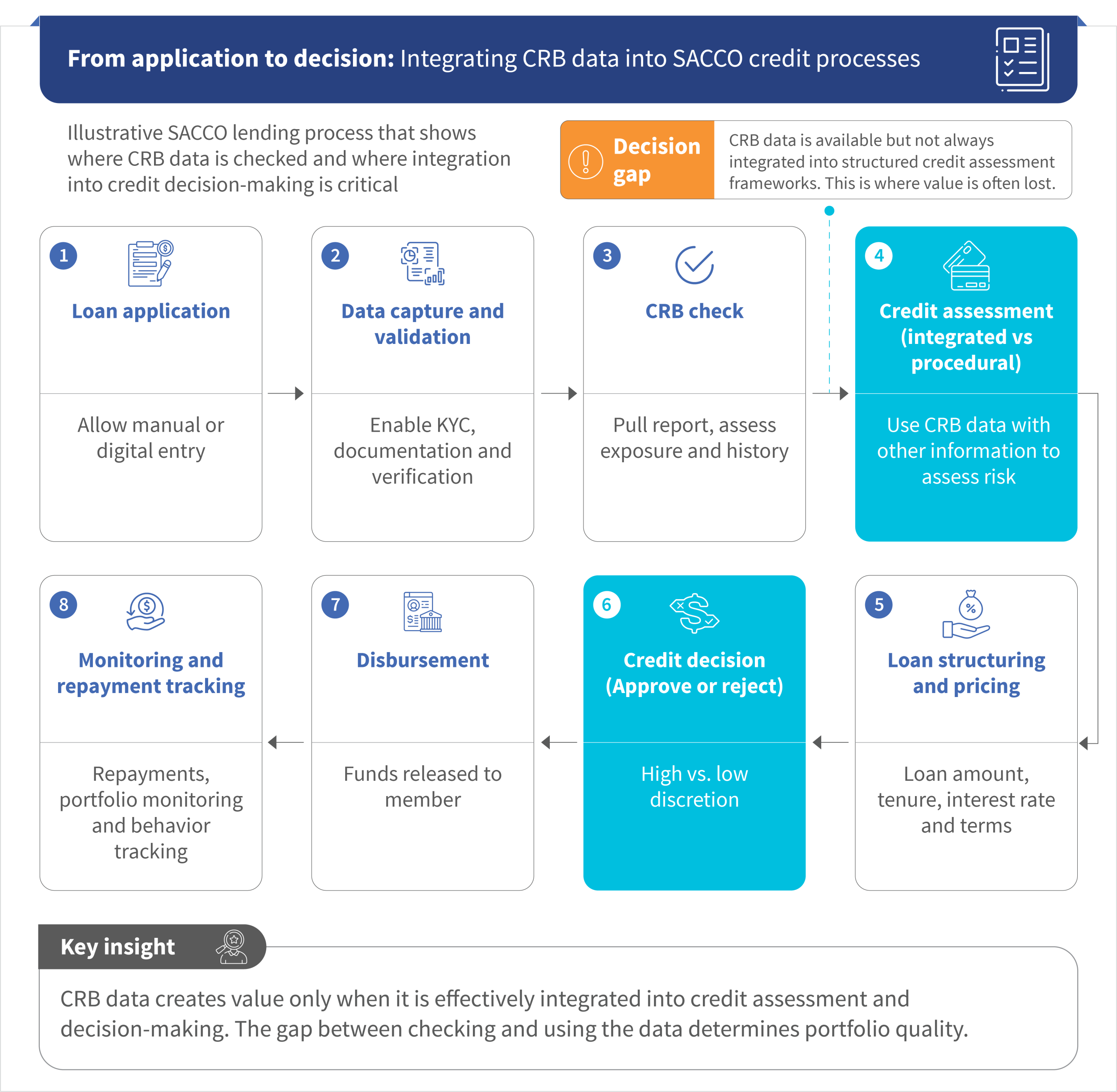

The gap between CRB access and effective use is most visible among SACCOs.In practice, this gap lies not in data availability but in how CRB data is used within the lending process.

Figure 4: A typical SACCO lending process flow with CRB data

Despite their central role in financial inclusion, many SACCOs lack the systems and capacity needed to translate CRB data into consistent lending decisions. A primary constraint is limited digitization. Many SACCOs rely on manual processes and fragmented systems, which make it difficult to integrate CRB data into workflows or generate consistent assessments.

Governance and capacity challenges further weaken credit decision quality. Weak governance leads to inconsistent application of credit policies, while high override rates undermine discipline. Limited staff capacity to interpret CRB data reduces its effective use.

Data ecosystem gaps also persist. CRB data primarily captures formal credit histories, but many SACCO clients operate informally with limited documentation. Without complementary data, such as cash flow or behavioral indicators, risk assessment remains incomplete.

SACCOs also face a persistent tension between inclusion and risk management. Without strong systems and segmentation frameworks, this often results in either a rise in defaults or overly conservative lending.

In addition to these operational constraints, SACCOs face emerging challenges related to scoring model design. These models rely on incomplete data sources, static risk measures, and heavily weighted collateral variables; their outputs may not reflect borrower realities. This is particularly important in SACCO contexts, where informal income, guarantor-based lending, and recovery trajectories shape repayment behavior. Without continuous calibration, scoring models risk reinforcing bias instead of improving decision quality. CRB systems influence lender decisions and borrower behavior.

When repayment histories are recorded and shared, borrowers have stronger incentives to maintain discipline. Timely repayment becomes valuable, as it builds a credit history and improves future access to credit. This is reflected in stronger performance among institutions that actively use CRB data.

However, this effect depends on system credibility and visibility. Many SACCO borrowers remain partially outside the formal credit systems, which reduces the immediate consequences of default. As a result, incentives to maintain strong repayment behavior are weaker.

Rising default rates among CRB users, as depicted in Figure 1, reinforce this point. CRB data improves initial screening but does not guarantee sustained repayment performance as lending expands into new or higher-risk segments. Stronger outcomes occur where CRB data is embedded within broader systems that combine multiple data sources, continuously monitor borrower performance, and adapt lending decisions accordingly.

This is particularly important for underserved segments, such as youth borrowers, whose thin credit histories require complementary indicators to support both inclusion and repayment.

Uganda’s credit ecosystem is at an inflection point. Access to borrower data has expanded, but the next phase depends on how that data is used. The key shift is from data access to decision intelligence. This requires embedding CRB data into credit policies and decision frameworks, the combination of CRB data with internal and behavioral data, the strengthening of governance, the reduction of discretionary overrides, and investment in digitization to enable consistent, scalable decision-making. For funders, this means moving beyond capital toward capability-building. For financial institutions, it requires rethinking how credit decisions are structured and executed.

Uganda’s credit ecosystem has moved from data scarcity to data availability but has not reached decision-level integration.

Figure 5. Financial infrastructure maturity framework that illustrates the transition from basic functionality to fully integrated and interoperable systems

For MSERF 2.0 and similar initiatives, this requires a shift in focus to support SACCO digitization, pairing capital with technical assistance to strengthen credit risk management, data use, and institutional governance, and tracking decision quality alongside loan volumes.

Uganda’s experience shows that CRB systems improve transparency, but their impact depends on how effectively they are integrated into decision-making and how accurately scoring models reflect borrower realities. Poorly calibrated models can introduce bias, misrepresent risk, and weaken incentives for positive repayment behavior.

The focus has shifted from CRB adoption to effective CRB use for SACCOs and financial institutions. The key question is how to turn CRB data into better decisions, and ultimately, better outcomes.

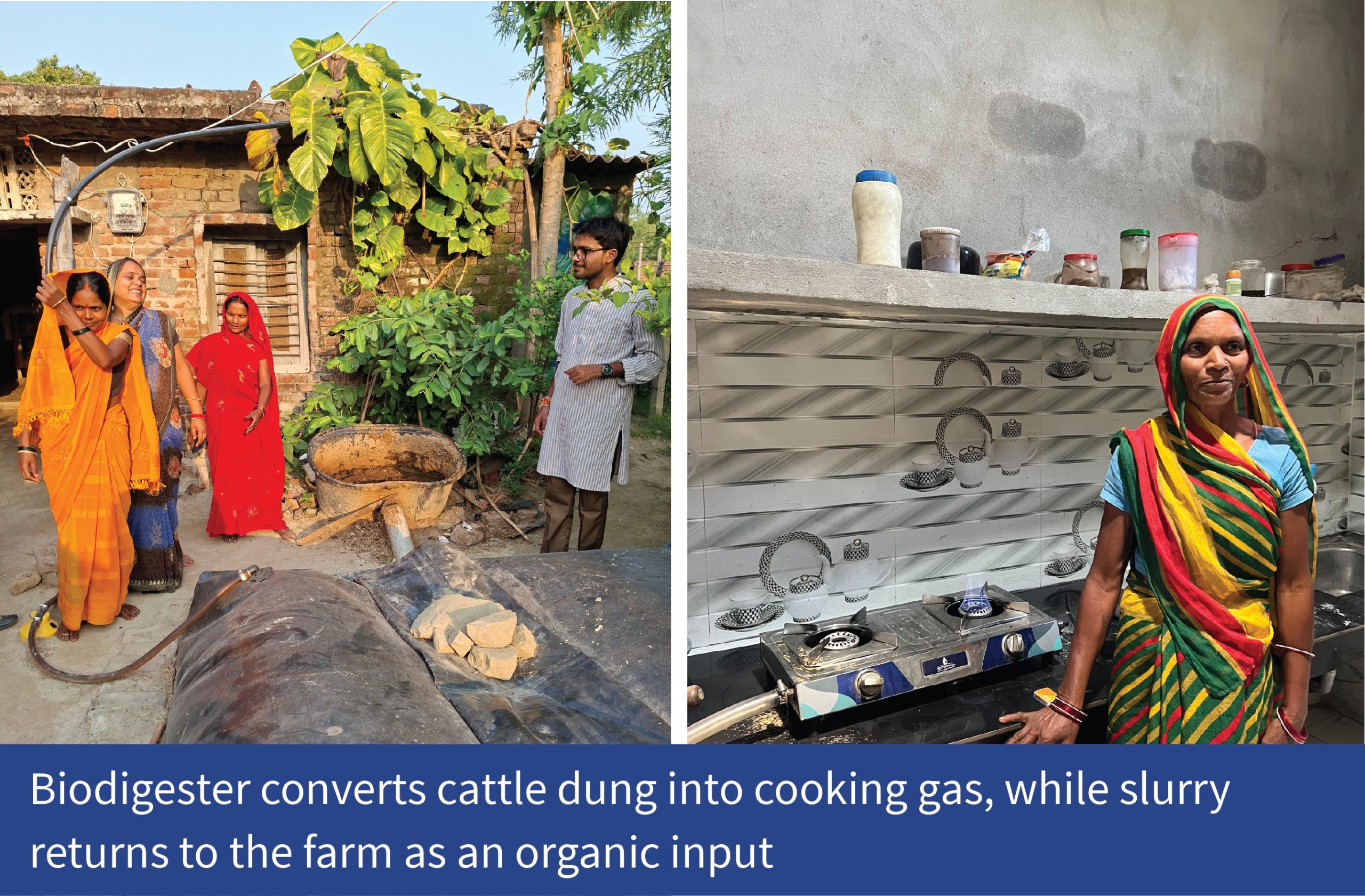

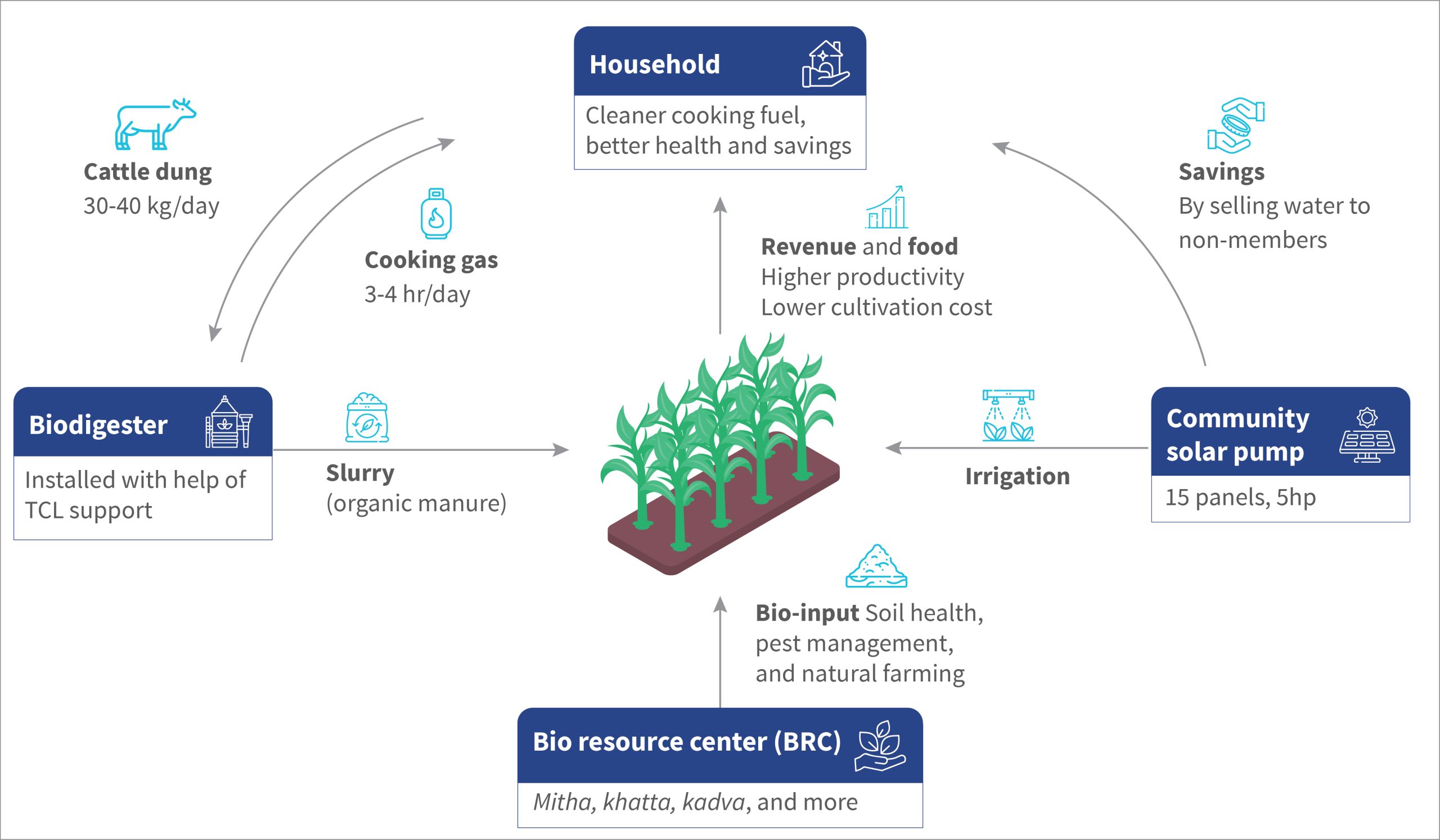

In Bahraich, Uttar Pradesh, a solar irrigation pump is doing more than lowering diesel use. Managed by the Ekta women’s group in Mohanpur Mafi, it helps farmers irrigate more reliably, cultivate across more seasons, and sell irrigation water to nearby farmers when local demand within the group falls. A household biodigester adds another layer to the rural economy. It converts cattle dung into cooking gas and returns slurry to farms as an organic input. At the bio resource center (BRC), women associated with the Udyami Mahila Producer Company Ltd. (UMPCL), a farmer producer company (FPC), produce bio-inputs that offer farmers a lower-cost pathway to soil health management, pest control, and natural farming, with institutional support from the Trust Community Livelihoods (TCL).

The TCL model works because it connects energy, water, soil, livestock waste, and women-led institutions within one livelihood system. For practitioners who work in decentralized renewable energy and regenerative agriculture, Bahraich raises an important question.How can rural livelihood assets across energy, water, and regenerative agriculture move beyond supported pilots and become locally governed service systems that create recurring value for farmers?

Many rural energy programs focus primarily on assets, such as pumps, biodigesters, solar panels, or clean cooking units. In Bahraich, the model builds an ecosystem around these assets to support local economic development in agriculture.

This blog examines three priority assets and how communities use, pay for, maintain, and convert them into recurring value.

1. Renewable energy as community-managed infrastructure

The solar irrigation system in Mohanpur Mafi offers a strong lesson in service delivery. The system includes 15 solar panels and a 5 horsepower (hp) pump. It currently irrigates about 12.5 acres and can potentially serve 20 acres, along with nearby farmers.

The women-led group manages water distribution, payment collection, recordkeeping, and group savings. As a result, the system functions as a community-managed service model,rather than a simple diesel replacement. The immediate gain is lower diesel dependence. The deeper benefit is a shift in cultivation practices. Reliable irrigation allows farmers to cultivate crops during the Kharif, Rabi, and Zaid seasons. These seasons correspond to the monsoon, winter, and short summer cropping periods.

Before the solar irrigation system, diesel costs and supply uncertainty made Zaid cultivation difficult for many farmers. The system changes the cropping calendar by providing water when farmers need it.

Group members pay a reported USD 0.026 or INR 2.5 per unit of water, while non-members pay a reported USD 0.031 or INR 3 per unit. The group deposits the revenue into its savings account. The pump supports crop production, generates local revenue, and strengthens community ownership.

The shift in this approach matters because the scale of decentralized renewable energy depends on ownership, pricing, maintenance, and recurring user value. During non-irrigation periods, communities can assess productive uses, such as flour milling or local processing. Any expansion, however, requires clear demand, load requirements, pricing, and maintenance arrangements.

The biodigester represents the household-level component of the model. It operates within the household economy and depends on livestock ownership, daily dung availability, cooking needs, and the household’s ability to use slurry on farms. The household that the authors visited during the field visit reported that the biodigester provides about three hours of cooking gas each day in normal conditions. The model requires two buffaloes or three cows, with a daily dung output of 30–40 kg.

Before adopting biogas, the household reportedly spent about USD 125 or INR 12,000 each year on liquefied petroleum gas (LPG). The family also relied on firewood and cow-dung cakes. The benefit is, therefore, reduced fuel dependence, rather than full replacement of all cooking fuel across all seasons.

Gas production declines during winter because lower temperatures slow digestion. Hence, households may require backup cooking options.

Veena Devi, a resident and user of the biodigester in Bhraich, reported that the biodigester reduced the need to make dung cakes and collect firewood. It also simplified cooking and kept utensils cleaner. The household applies slurry from the biodigester to fields, particularly during plowing. Farmers can also use the slurry to prepare bio-inputs.

The BRC anchors the regenerative agriculture componentof the model. Women produce bio-inputs, conduct demonstrations, and support producer structures that connect products with local demand. The center produces products that address practical farm needs. Mitha supports crop growth, khatta supports disease management, and kadva helps control pests. Farmers use these products on cereals, vegetables, spices, and high-value crops.

Field discussions suggest a significant cost advantage. Chemical inputs for a typical farm size of 0.2 acres may cost about USD 21 or INR 2,000. Bio-inputs from the BRC may cost approximately USD 2–3 or INR 200–300 for the same area, based on crop requirements and field conditions.

Adoption spreads through demonstrations, peer learning, TCL awareness sessions, and visible crop performance. The BRC therefore supports a local system in which women produce inputs, demonstrations build farmer confidence, and producer structures bring products closer to users. The center also connects directly to the decentralized renewable energy interventions. Solar irrigation improves water availability for more intensive cultivation. At the same time, BRC inputs help farmers manage soil health and input costs.

The key lesson from the TCL Bahraich model is that assets are only the starting point. The surrounding system turns energy, water, soil nutrients, and women-led institutions into recurring economic value. The TCL and MSC (MicroSave Consulting) now seek ways to translate this experience into an investable pathway for decentralized renewable energy, regenerative agriculture, and rural income growth.

This brief reframes financial education as a supporting component of financial capability infrastructure rather than a primary consumer protection tool. Global evidence and MSC’s experience across 50+ countries reveal that financial education delivers modest but durable results when targeted, behavior-linked, and delivered at teachable moments. Meaningful consumer outcomes depend on structural interventions, such as product design, disclosure standards, provider accountability, liability frameworks, and effective grievance redress mechanisms.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.