A significant gender disparity persists in Indonesia’s labor market. The country’s informal sector employs 64% of women. The diverse sector encompasses own-account workers, casual laborers, microenterprises, and street vendors. Yet the rapid digitization of informal work in Indonesia and its impact on women’s employment remain inadequately understood.

MSC conducted a comprehensive study in collaboration with the Ministry of Women Empowerment and Child Protection of Indonesia to address this gap. It sought to assess female informal workers’ accessibility and experiences in the evolving digital economy. The research was designed to capture these women’s multifaceted experiences and explore how digital trends transform their work in five key areas:

Women’s day-to-day realities and challenges in informal work and their experiences in informal employment;

Female informal workers’ access to digital financial services and their usage ;

The impact of societal norms and caregiving duties on women’s work;

Opportunities for business growth and skill enhancement available for women;

The availability and effectiveness of social protection measures and childcare services for informal workers.

The report is based on a survey of 400 female workers across nine Indonesian provinces. It presents actionable recommendations for government ministries, civil society organizations, and public and private sector entities.

The report analyzes barriers women face throughout their employment lifecycle. Female informal workers can fully engage in the job market and benefit from it if they overcome these barriers. This would foster a more equitable labor market and, in turn, enhance female labor force participation rates in Indonesia.

Here are the links to the reports:

1) Click here to download the full report in English.

2) Click here to download the report’s summary in Bahasa Indonesia.

We organized a webinar titled “Sathi Network: A Pathway to Women’s Economic Empowerment through Financial Inclusion,” which was held on 20th May 2024. The discussion featured a panel of experts from leading FinTechs, banks, regulators, and philanthropic organizations worldwide . Their conversation focused on the following:

Ideas to reduce the gender gap in financial inclusion,

How agent networks can accelerate financial inclusion, and

The role of DPI in women’s economic empowerment

Panelists:

Dr. Md. Habibur Rahman, Deputy Governor, Bangladesh Bank

Arisha Salman, Financial Sector Specialist, CGAP

Syed Abdul Momen, Deputy Managing Director & Head of SME Banking, Brac Bank PLC

Sasidhar N. Thumuluri, Managing Director & Chief Executive Officer, Sub-K Impact Solutions

Arjun Venkatraman, Program Officer, Digital, the Bill & Melinda Gates Foundation

Martin and Joseph are nano-entrepreneurs in Nairobi. They are actively engaged in the transport sector. Martin ferries individuals and cargo on his boda for a living. A local financial institution finances his boda, which runs on a traditional internal combustion engine. He decided against an e-boda (electric motorcycle) due to his counterparts’ negative experiences with the first-generation e-bodas. His business was brisk until 2020, when COVID-19 shutdowns led to reduced demand for nano-entrepreneurs.

As time went on, the war in Ukraine and other macroeconomic factors further challenged Martin’s situation. Today, the prevailing inflation, high interest rates, and rapid currency devaluation in Kenya make it difficult for Martin to operate. He struggles to make timely repayments against his loan and run his motorbike due to fluctuating fuel prices. He also cannot upgrade his aging boda due to higher financing and replacement costs.

In contrast, Joseph entered the transport business in late 2023 and bought an e-boda from a leading e-mobility provider. His transition was smooth. He could save USD 6 daily on fuel costs—more than 50% of his earnings. Moreover, the superior quality of the current fleets made his maintenance costs negligible. His transition immediately increased his daily profit and boosted his resilience after the period of economic turbulence.

Today, Joseph travels about 80 kilometers on a fully charged battery and pays USD 1.42 to swap out his battery at charging stations. These stations have been rapidly growing across the city. Joseph is an ardent supporter of e-bodas. He has persuaded others within his chama to transition despite challenges, such as high upfront costs, costly credit terms, limited charging stations, and persistent fears around the perceived unreliability of e-bodas.

Martin is among Africa’s 27 million boda operators—a sector poised to grow by 50% by 2050. This growth would result in increased traffic congestion and more traffic accidents, such as injuries and fatalities. The sub-sector with the exception of e-bodas would also contribute to higher emissions and poor air quality. In comparison to the globe, the growth of Africa’s global electric vehicle (EV) market share has been slow. EVs are expected to contribute less than 2% of the global market by 2029. Despite the small market share occupied by Africa, there has been recommendable growth within each country. For instance, around 40 e-boda startups have emerged in Kenya and raised USD 52 million—a first for the continent. Each e-boda provider offers unique products, distribution, and payment models to capture the internal combustion engine market. Yet e-mobility adoption remaings slow despite interventions focused on awareness, quality, finance, technology, infrastructure, and policies, as revealed in MSC’s interviews with industry players. Our teams spoke to representatives from organizations, such as ARC Ride, Auto Truck East Africa Limited, Knights Energy, and KIRI EV.

Finance as a driver of uptake

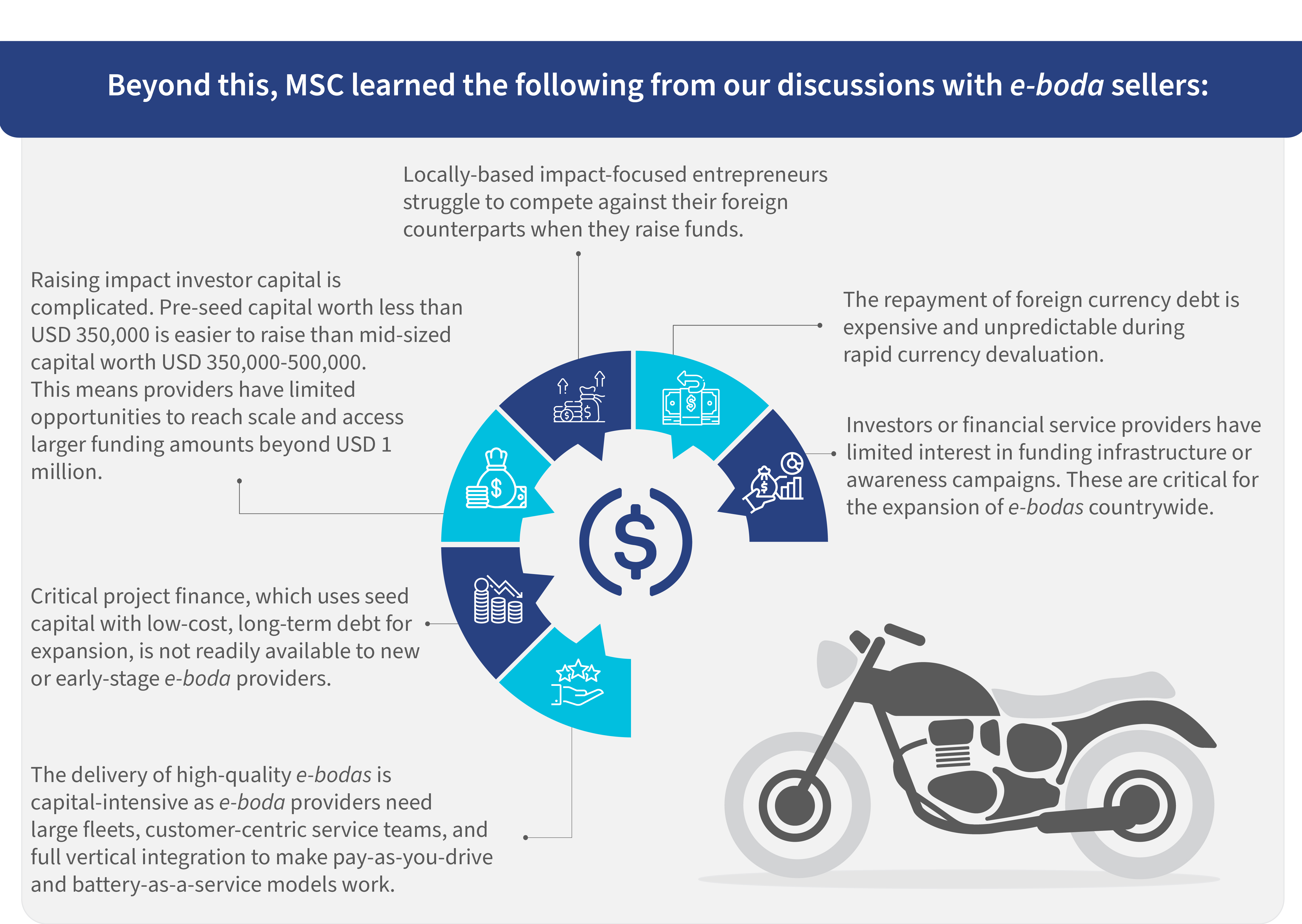

Improvement in access to finance on both the demand and supply sides is pivotal to drive e-bodas’ uptake. Until recently, financial service providers were unwilling to finance the purchase of e-bodas due to their unfamiliarity with the segment and the unproven nature of the solutions. However, this has been changing due to the emergence of quality solutions, tracking, and lock-out technology.

M-KOPA, Mogo, Watu, and Fortune Credit are public examples of organizations that lead the charge with innovative business-to-business (B2B) and business-to-consumer (B2C) payment and financing models. Yet the cost of financing remains elevated despite these efforts. In February 2024, the Central Bank of Kenya reported that commercial interest rates were as high as 15.88%—the highest in the past five years.

Beyond this, MSC learned the following from our discussions with e-boda sellers:

MSC’s recommendations to address financing challenges

Based on our assessment of the financing challenges, MSC recommends the following solutions to unlock financing constraints:

1. Use blended financing solutions. These solutions can crowd in funds from state and non-state resources at cheaper rates to reduce adopters’ borrowing costs. These solutions also increase working capital facilities for credit providers, minimize risks associated with foreign currency volatility, and inject liquidity into providers’ operations.

SDG-focused patient capital providers, such as international investors or donors, can be involved to provide this cheaper capital to local financing entities. MSC worked on the EVOLVE RSP Project, which provided partial credit guarantees and concessional loans to promote two- and three-wheelers in India. Africa can replicate this approach.

2. Use green financing instruments to build infrastructure and help popularize e-bodas countrywide. The Kenya Green Bond Programme and the county green finance assessment program by FSD Kenya exemplify how debt instruments can support real economic growth in a climate-responsive manner.

Moreover, funds from these instruments can meet the growth needs of mid-sized e-boda providers, promote quality assurance, and enhance market awareness. These can also drive industry innovation, support technology advancements, and offer results-based incentives to spur growth and promote inclusivity in a male-dominated sector that has barred women’s participation due to cultural and safety concerns.

3. Develop digital solutions that support credit appraisal, disbursement, and repayments. These solutions can also support product tracking, reverse logistics, and lock-out technologies in case of default. Digital products can drive accessibility, affordability, and convenience among nano-entrepreneurs while they incentivize climate-smart behavior adoption if combined with innovative climate financing solutions, such as carbon credits.

A telematics device in each vehicle can reduce finance risks when asset finance instruments are used. These devices track performance, calculate carbon credits, and estimate potential revenues generated.

Despite challenges, Kenya’s e-boda subsector is poised to take off rapidly. This subsector provides significant opportunities for economic growth and environmental benefits as it reduces greenhouse gas emissions. However, the subsector’s success hinges on the availability of innovative financial instruments.

Joseph’s experience showcases the progress made in the delivery of demand-side financing solutions and the economic benefits that accrue to nano-entrepreneurs. The critical role of innovative financing cannot be overstated. Solutions, such as blended finance, green finance, and digital solutions, are vital to lower entry costs, enhance e-boda businesses’ viability, and provide sustainable mobility. This is critical if Kenya intends to successfully introduce more than 1 million e-bodas by 2030.

External contributors include the following industry experts:

MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

In this podcast, Mandira Sharma and Jeanne Ng’ang’a from MSC discuss trends in Kenya's electric motorcycles (e-mobility) sector. They cover challenges hindering e-mobility adoption, the crucial role of local manufacturing, and available financing options for individuals and businesses transitioning to e-mobility.

“I wanted to buy two sewing machines for my tailoring business and reached out to my nearest bank branch for a loan. The bank officials gave me a list of documents I must submit to initiate the loan process. However, I did not understand the listed documents and where to obtain them. I tried to contact bank officials but did not receive adequate support. I am unsure what to do next,” sighs Pragna, a 32-year-old woman entrepreneur from Hyderabad, India who runs a tailoring business.

Fig 1: Pragna’s desire versus the current ordeal

Pragna’s story is not an isolated case. It highlights the importance of mentorship support for the 8 million women-led businesses (WLBs) in India, which can help them overcome such challenges. Mentorship support implies access to professional industry networks, hyperlocal peers, and experienced mentors for handholding and guidance. MSC’s recent study reveals that mentorship support is crucial for WLBs’ growth. A study by the Reserve Bank Innovation Hub suggests that WLBs that receive mentorship support show a higher level of business acumen and willingness to seek external funding.

(Source: Qualitative interviews with 150 WLBs in India and MSC’s analysis on the importance of mentorship support for WLBs)

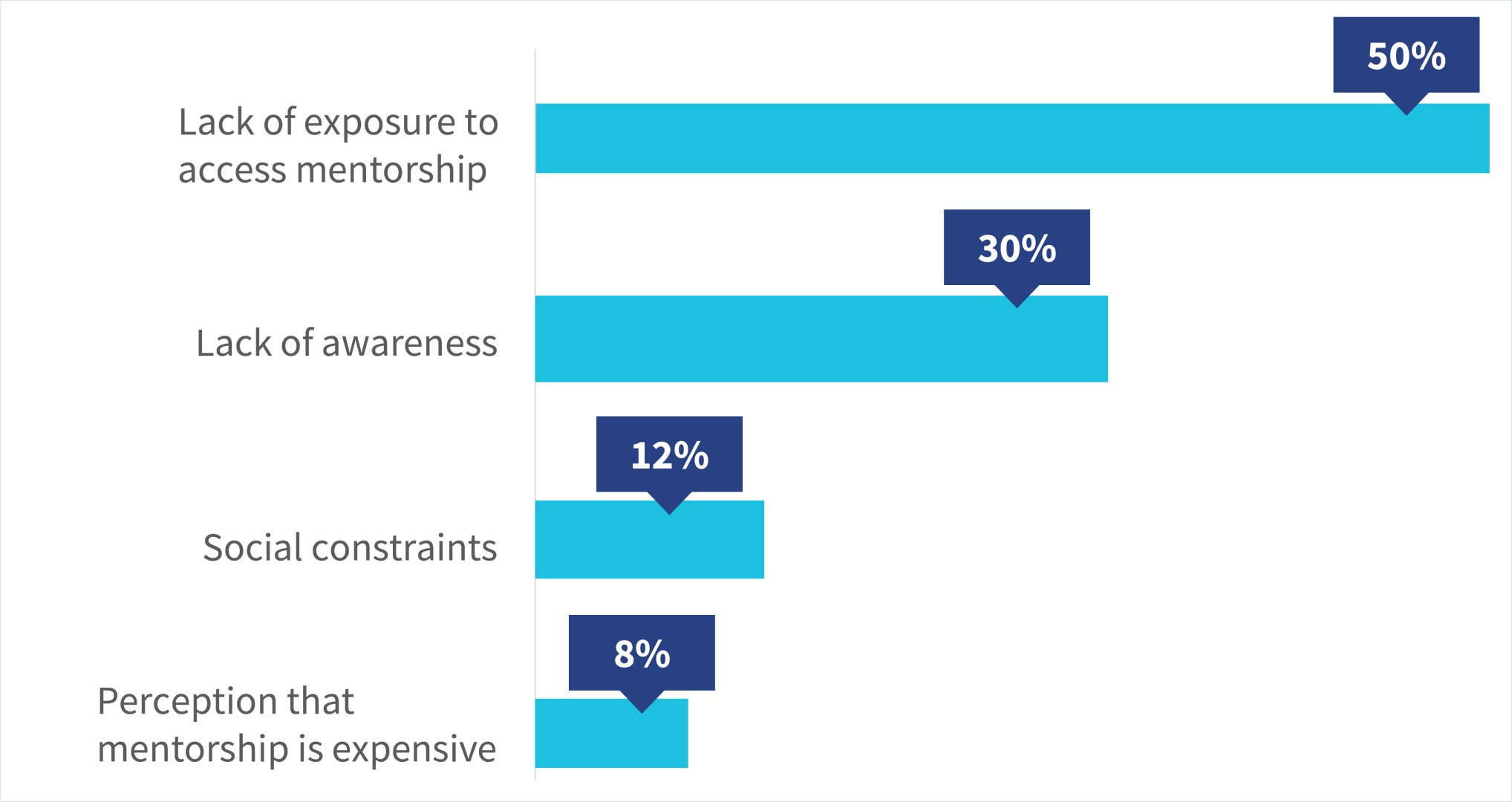

Further, a recent study by MSC and the Women Entrepreneurship Platform (WEP) found that a mere ~25% of surveyed women entrepreneurs have access to entrepreneurial mentorship and 64% are unaware of any mentorship programs for entrepreneurs. The concept of mentorship support for business growth remains nascent for women entrepreneurs, especially for those from Tier III and smaller geographies.

Role of specialized incubators to improve access to mentorship support

Overall, India has approximately 763 incubators and accelerators. However, most of them cater to the startup segment. Few incubation centers offer nuanced support to WLBs. In this blog, we delve into the role of one such incubator, WE Hub, which spearheads WLBs’ growth in India through mentorship support.

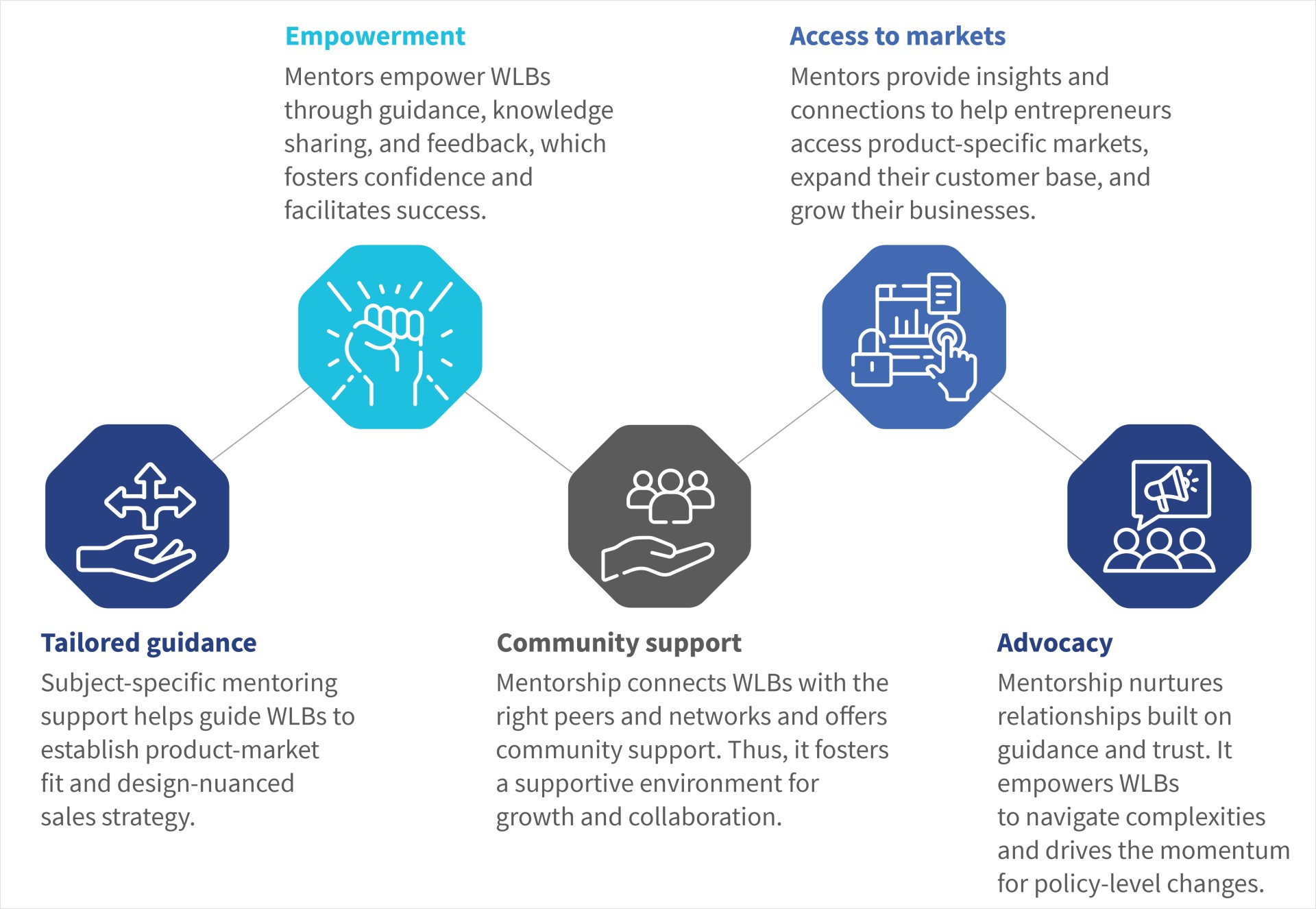

WE Hub is India’s first state-led incubation center in Telangana state that supports WLBs. The one-stop entity provides WLBs with entrepreneurship support across their business lifecycle. This includes access to capital, market linkages, training and capacity building, and networking opportunities. Mentorship and guidance across all these focus areas form the backbone of WE Hub’s work. Let us go back to Pragna’s case to understand this better.

Fig 4: Role of WE Hub across the entrepreneurial needs of Pragna

The WE Hub way: The use of peer groups to bridge the mentorship gap among WLBs

In the above image, we observed how guidance and mentorship play a key role in entrepreneurship. WE Hub’s method has been to provide “mentorship with the help of the community.” MSC designed a range of support areas to foster community engagement for WE Hub’s WLBs under the flagship project “ Women-led Business (WLB) program,” funded by the MetLife Foundation. These initiatives seek to create a network of mutual mentorship and empower women to support each other’s business growth collaboratively.

Community groups to lean in:

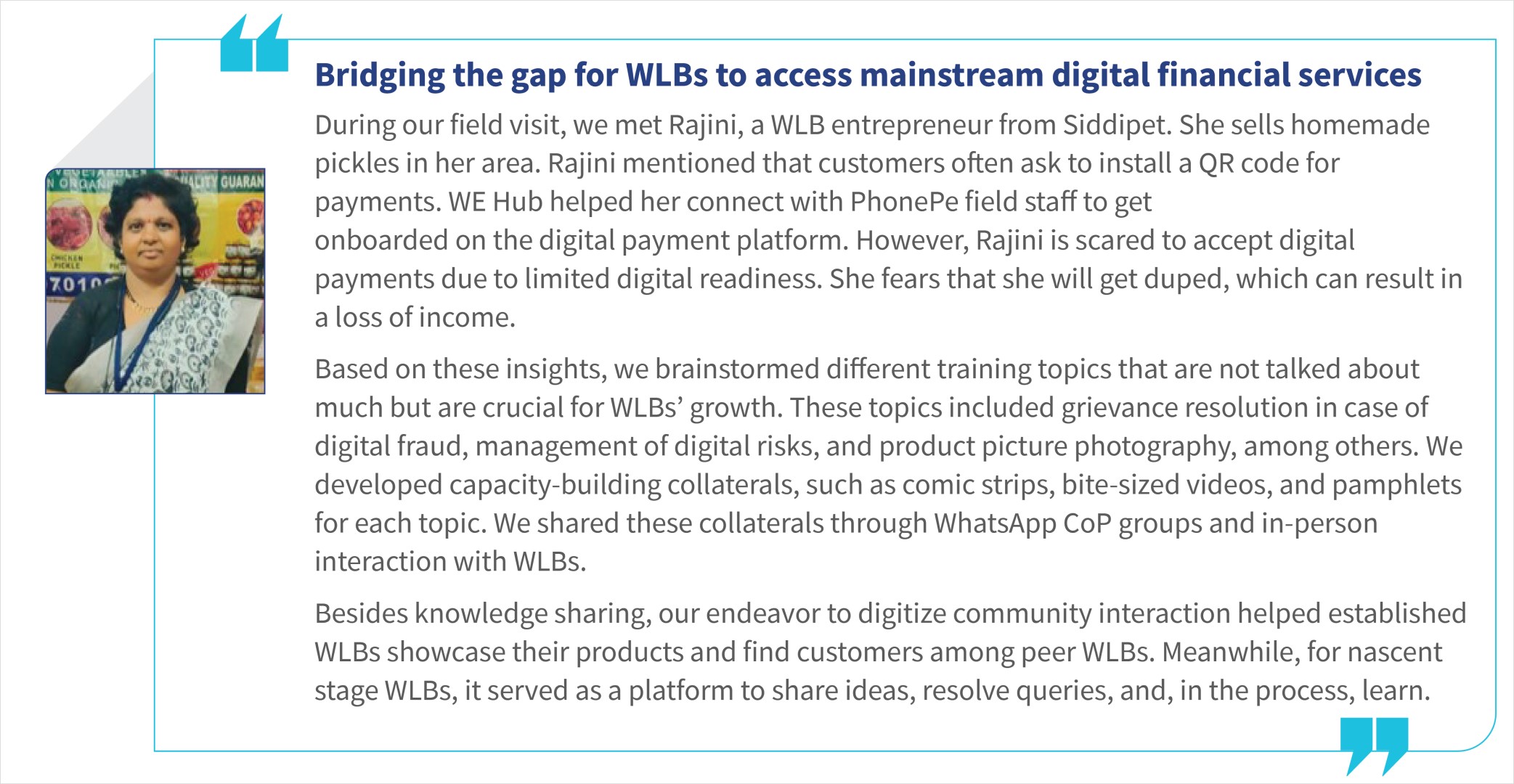

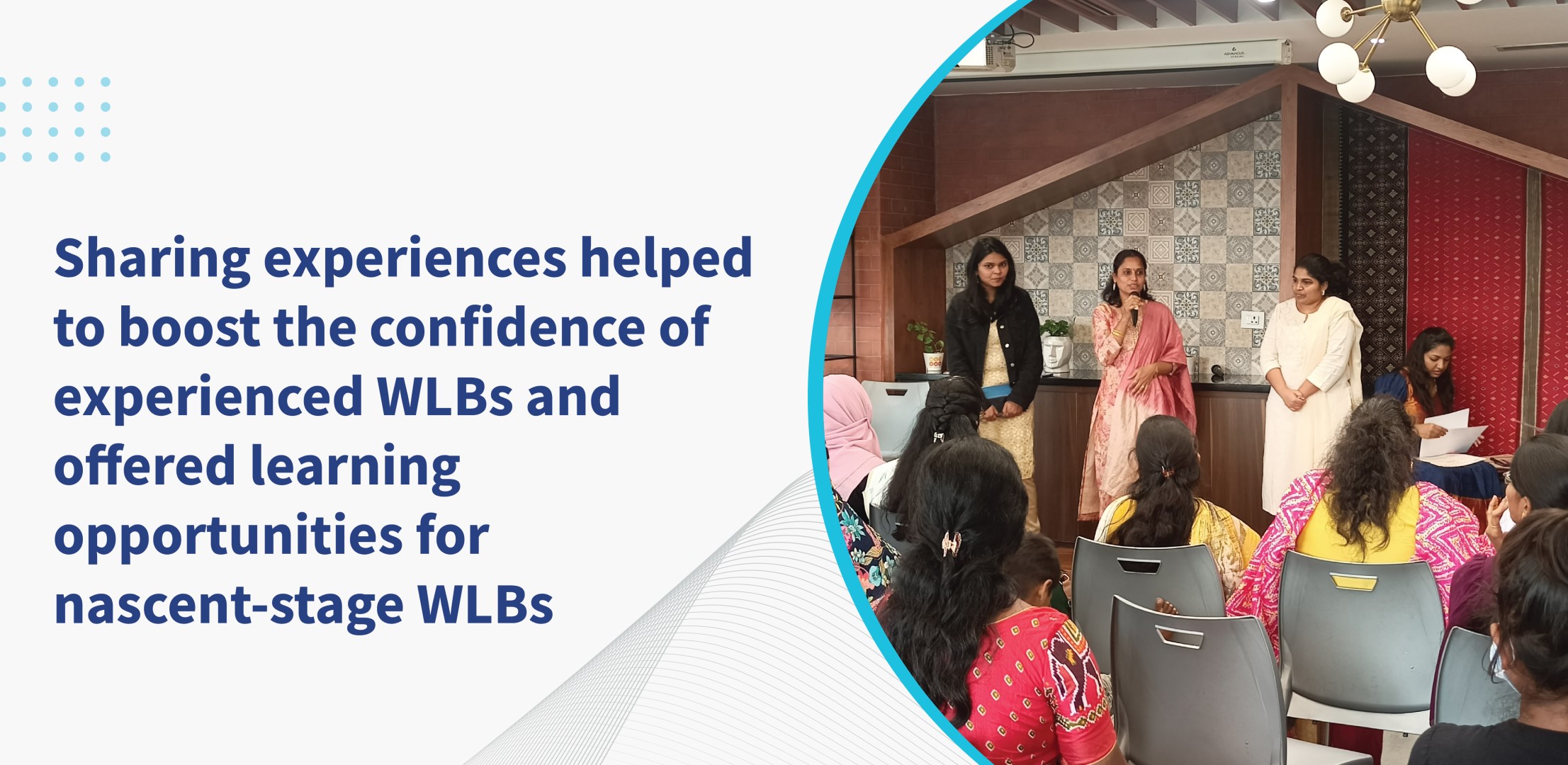

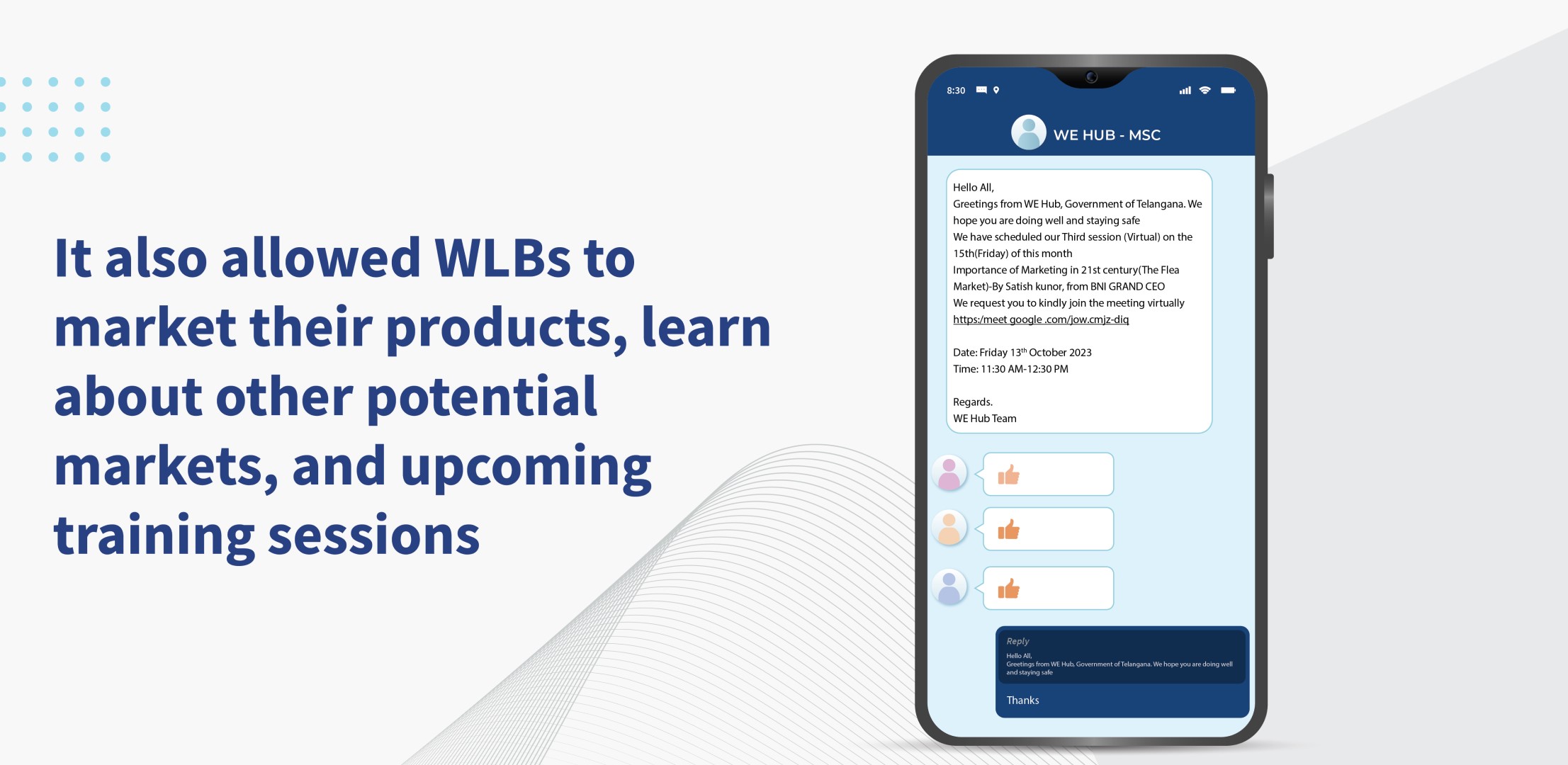

WE Hub regularly conducts in-person discussions with WLBs in similar businesses. However, those meetups primarily catered to training sessions or discussed physical marketing (fairs) events. MSC mobilized WLBs to come together and discuss the challenges around their business’s management with WLB’s support. The group was a good mix of mature and nascent business-stage WLBs.

Interactions with the peer community encouraged women to share their challenges freely and seek guidance from other WLBs. The suggestions from successful WLB entrepreneurs encouraged peer WLBs to continue to put effort into their businesses.

During our group interactions with WLBs, we observed that established WLBs had much to share about their journey. Most nascent stage WLBs were all ears to understand and learn more from each other. We asked ourselves, “Can we formalize and digitize this so that more WLBs can learn from each other?”

Digitizing the community interactions with human touch

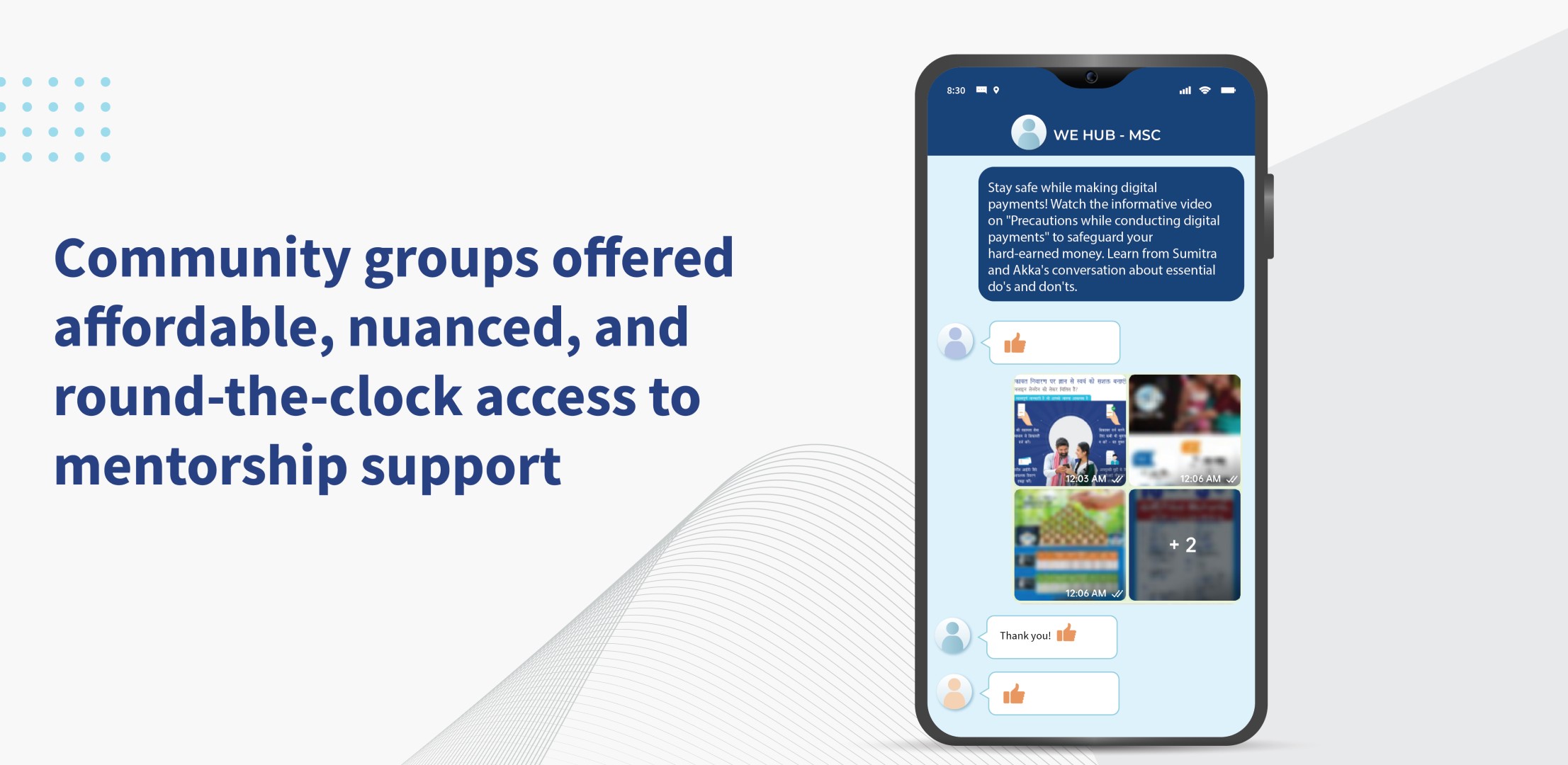

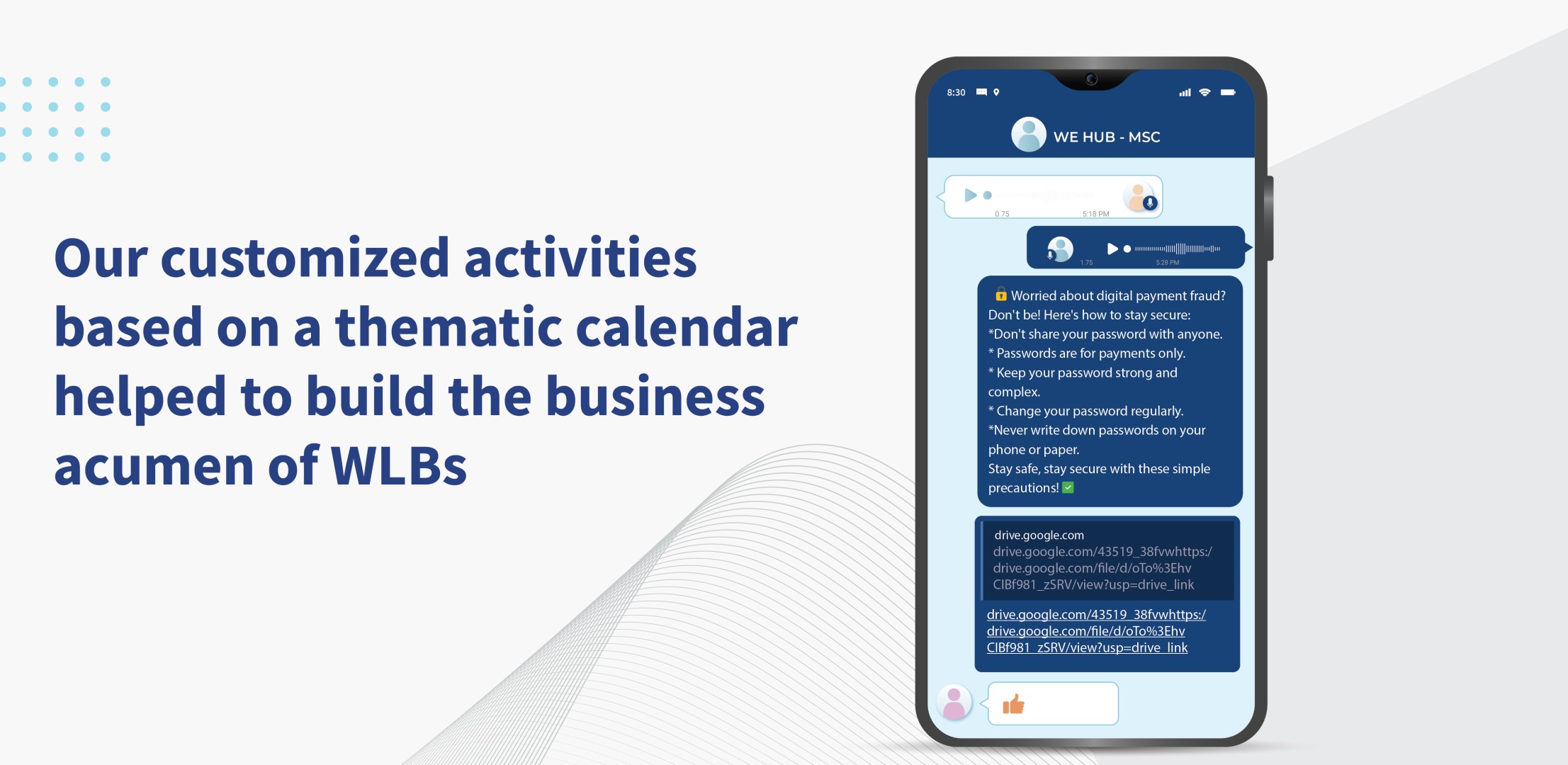

Most WLBs already used WhatsApp for communication. MSC used WLBs’ familiarity with WhatsApp for peer learning. We developed video collaterals that covered insurance, digital payments, business registration, marketing, and business management. We shared these videos with the WLBs in the learning groups we created on WhatsApp. This made the information easily accessible for WLBs.

MSC also identified other digital platforms to engage with these women, such as Google Meet, and used them to conduct group interactions. This was especially helpful for WLBs who could not participate in knowledge-sharing gatherings due to household responsibilities and long commutes. MSC included a good mix of in-person and digital learning sessions to ensure inclusivity, encourage peer learning, and forge the foundation for collaboration.

These initiatives helped WLBs engage meaningfully and learn the best business practices from each other. Ground-level insights determined most of MSC’s interventions and made them relevant and valuable for WLBs.

Use of technology for better engagement:

Our experience with WLBs suggests that they struggle to find relevant information related to business queries in simple and regional languages.

MSC used the WLB WhatsApp groups to integrate into the Sangini Konnect platform as part of the WE Hub project. Sangini Konnect is an artificial intelligence (AI) chatbot that allows WLBs to ask business-related queries and get detailed responses in the form of videos. All of this is in WLBs’ preferred regional language.

How did community-based interventions help WLBs?

WE Hub and MSC’s collaborative efforts to use the community for mentorship positively impacted 5,470 WLBs in Telangana. It encouraged 4,062 WLBs to try digital payments for business and learn about crucial financial resilience products, such as insurance. Community-based mentorship is scalable and affordable and helps WLBs navigate sociocultural norms. Studies suggest that WLBs can unlock India’s goal of becoming a USD 5 trillion economy. The lack of mentorship support is not limited to Telangana’s WLBs but also extends to India and the Global South markets.

We can bring millions of WLBs into the folds of the digital finance mainstream if we tailor the learning experience around community-based mentorship to align with the Global South market’s contextual and social setting. It can digitally empower millions of women like Pragna to run their businesses and become a role models for her peer WLBs in India and beyond.

The efficacy of transfers from higher to the lower tiers of any government depends on the underlying fund disbursement system. Sample this—the Government of India, as per the budget estimates of 2024-25, plans to transfer funds worth USD 266 billion or ~7% of India’s GDP, to states. This includes devolution of states’ share, grants or loans, and releases under Centrally Sponsored Schemes (CSS). The level of sophistication of these systems have a huge bearing on the nation’s ability to spend and spend well.

On 13th July 2023, the Department of Expenditure (DoE) issued a memorandum to implement the SNA-SPARSH mechanism to ensure the “just-in-time” (JIT) release of funds allocated to the CSS through the RBI’s e-Kuber platform. It builds upon the significant gains of the Scheme Nodal Agency (SNA) system’s implementation in July 2021. This blog post highlights the journey, challenges, and innovations in CSS funding. It focuses mainly on the SNA-SPARSH model and its implications for efficient fund release and payment processing.

SNA-SPARSH’s implementation in India represents a significant milestone in the government payments ecosystem, where the holy grail is to achieve JIT payments. As the name suggests, JIT payments would eliminate the gap between the actual physical event, that is, the work for which the payment is due, and the fiscal event. In this context, the fiscal event is the outward movement of money from the consolidated funds to the end beneficiary—a citizen, a business, or other government bodies.

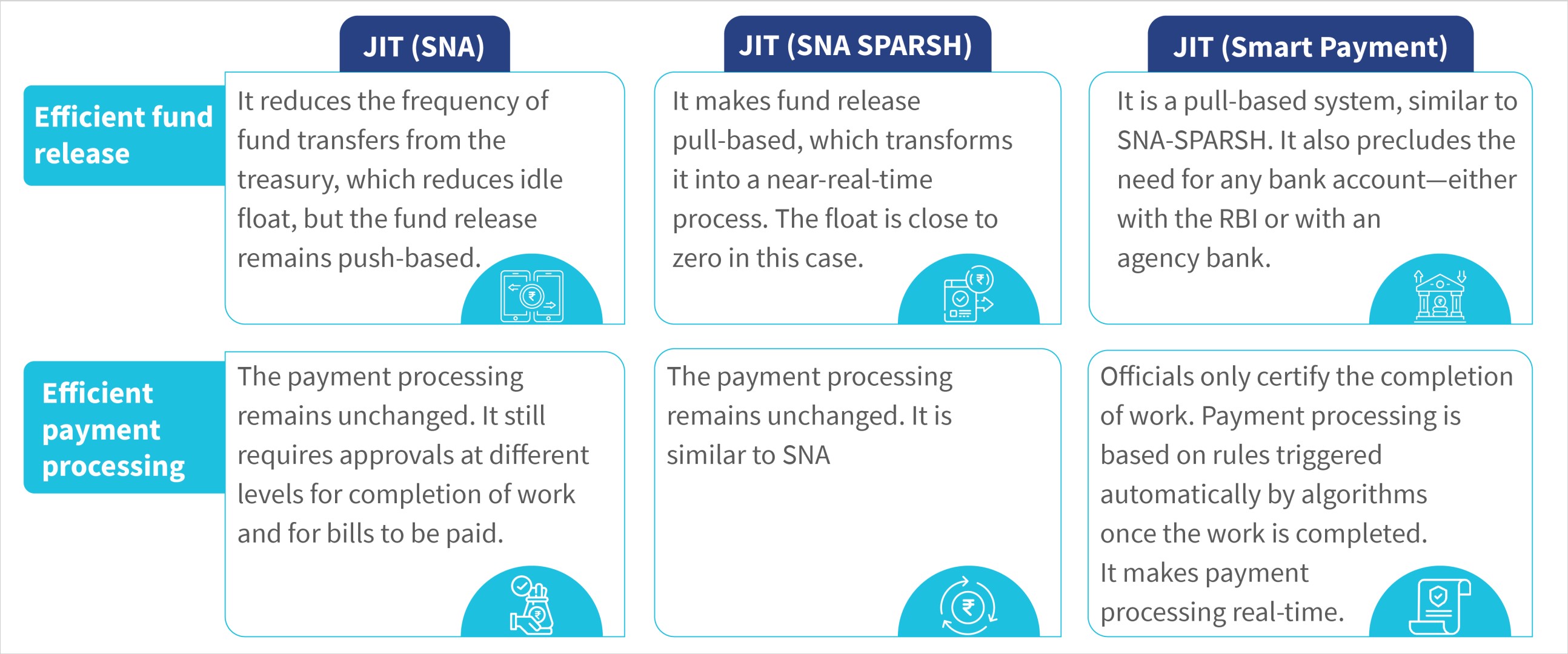

An implicit assumption in the government fund flow is that money will be pushed from one level to another, but SNA SPARSH inverts this assumption. It allows an agency that makes expenditures to pull funds up to the sanctioned limit when needed. With this, SNA SPARSH pushes the envelope toward smart payments, not just JIT. Operationally, the smart payment system will have two core attributes:

Efficient fund release: “pulling” funds from the treasury and passing them on directly to the beneficiary’s bank account;

Efficient payment processing: pulling funds in “real-time,” that is, just when payment for the work is due, based on rules triggered through algorithms.

The table below compares the three evolving versions of JIT on these two attributes.

At the root of this ambition for JIT payments is to enhance the state’s capacity to make expenditures effective and efficient. While the budgetary allocations to social sectors by the governments have slowly increased, available evidence suggests budgets remain unspent. Even with spent budgets, the achievement of outcomes remains low.

CSS accounts for a substantial portion of the central government’s budget, as per the interim budget for FY’25, at INR 5.02 lakh crores (~USD 60 billion), CSSs’ share is about 51% of the total transfers committed by the central government to the states. Thus, the deployment of JIT for CSS can potentially bring significant gains to optimize fund utilization and improve outcomes in the public sector.

A brief history of (just in) time

Over any given year, the CSS would be funded via a cascading fund transfer mechanism. Since the money moved from one agency to another, it led to funds in government bank accounts that sat idle for months or years before they needed to be spent.

The SNA was introduced to consolidate banking arrangements, reduce float, and enhance transparency in fund utilization. It has successfully integrated treasury systems across states and union territories, significantly reduced the number of government accounts, and provided real-time insights into fund releases and expenditures. It tackled challenges, such as unspent balances, cash shortages in some implementing agencies, and inefficient fund release strategies.

The quarterly release of funds and contingent additional releases based on utilization have helped reduce float and prevent the accumulation of unspent balances. India’s Finance Minister highlighted estimated annual savings of USD 1.2 billion from the SNA reforms. The SNA model successfully consolidated funds, improved transparency, and addressed various challenges in the fund release process.

SPARSH—the “pull” to complete the fund release

Under the SNA, the funds are still being “pushed,” albeit with fewer intermediate halts, in shorter bursts, and with a good view of where they are at any given time. The gap between the fiscal and physical events has also been reduced but not eliminated.

However, SPARSH marks a transition from a credit push (a-priori release of funds to various implementing agencies) to a debit pull-based fund transfer system in which a debit to the central pool is triggered only when implementing agencies issue payment instructions on the system. By design, SNA-SPARSH can “pull” funds in real time to the end beneficiary’s account, which takes it closer to a smart payment system. These design features are:

Integrated framework of PFMS, the state’s treasury or financial management system and the RBI’s e-Kuber platform that enables seamless flow of information across three systems;

Ability to onboard CSS, SNA, and implementing agencies on the platform—the last two via IFMS;

Creation of CSS-wise sanction orders for each state at the beginning of a financial year.

Under SPARSH, the eventual release of funds into the beneficiary’s bank account is triggered once the SNA or implementing agency generates the payment files. However, clarity is absent in the time gap between the generation of payment files and the physical event—the moment the work or the payment milestone is achieved in the field. When we revisit the holy grail of just-in-time payments, we find pulling of funds is not in “real time.” This does not qualify it as a just-in-time system since challenges in payment processing persist at the program implementation level.

Cometh the hour, cometh the smart payments

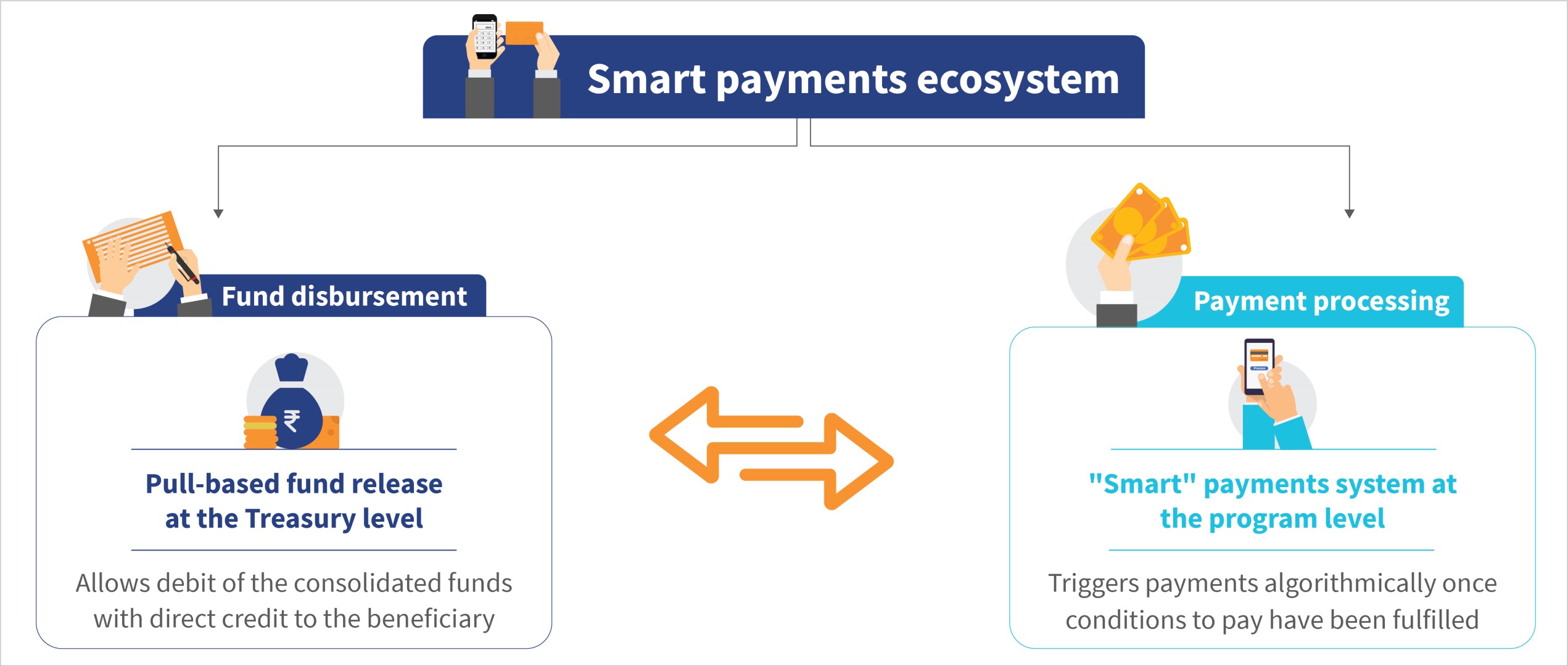

What is needed in this context is a payments processing system that can process payments, that is, generate payment orders automatically upon fulfillment of payment conditions for payees, such as vendors and citizens. Further, it should “talk” to the IFMS system to permit “straight-through processing” of invoices without manual intervention. In other words, we recommend a system that generates the payment files that SNA or implementing agencies can feed into the state IFMS.

When integrated with a pull-based fund transfer system like SPARSH, such a “smart” payments system creates a “smart payments ecosystem” that meets both the conditions of pull-based fund disbursement and the real-time processing of payments. The figure below shows this in detail. SPARSH’s pull-based fund transfer functionalities can be further improved by using a virtual treasury single account (VTSA), which would also eliminate the need to park funds it in any bank account—either with the RBI or an agency bank.

One such smart payments ecosystem is currently being implemented in Odisha. The Government of Odisha launched the MUKTA (MUkhyamantri Karma Tatpar Abhiyan) program to tackle job vulnerability that resulted from the COVID-19 pandemic. MUKTA encountered challenges, such as delays in claim settlement of wage-seekers and SHGs, idle parking of project funds, and ineffective project management.

MSC designed the “smart payments ecosystem” based on our work with the state’s Finance Department since early 2020. We designed a VTSA-based JIT funding system and a smart payments system, “MUKTASoft,” for the Housing & Urban Development Department.

The solution has enabled the transition from a “push-based” to a “pull-based” fund transfer system for beneficiaries, including wage-seekers, SHGs, and material vendors. Under it, the implementing agencies (urban local bodies in the case of MUKTA), pull funds from the state’s consolidated fund directly into the end beneficiary’s bank account in real time when a payment milestone is completed. The solution also incorporates autonomous rule-based processing of payments, which significantly streamlines the process and reduces the burden on officials.

The solution is being piloted in 23 of Odisha’s 149 Urban Local Bodies, and early results are encouraging. It has eliminated the float and reduced payment delays by 57% to the beneficiaries—wage seekers and SHGs. The smart payments system can potentially save the Exchequer as much as USD 50 million for a state like Odisha.

The way ahead

The journey toward an effective and efficient government payments ecosystem in India has seen significant progress with the SNA-SPARSH model. While challenges persist, ongoing experiments and successful pilots demonstrate the potential for transformative changes in how government funds are released and payments are processed. The Department of Expenditure can plan one more reform on SNA-SPARSH to make payment processing based on rules triggered automatically through algorithms upon completion of work certified by the executing agency. It would make payment processing real-time. The vision of JIT payments may soon become a reality to pave the way for improved governance and better outcomes.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

Martin and Joseph are nano-entrepreneurs in Nairobi. They are actively engaged in the transport sector. Martin ferries individuals and cargo on his boda for a living. A local financial institution finances his boda, which runs on a traditional internal combustion engine. He decided against an e-boda (electric motorcycle) due to his counterparts’ negative experiences with the first-generation e-bodas. His business was brisk until 2020, when COVID-19 shutdowns led to reduced demand for nano-entrepreneurs.

Martin and Joseph are nano-entrepreneurs in Nairobi. They are actively engaged in the transport sector. Martin ferries individuals and cargo on his boda for a living. A local financial institution finances his boda, which runs on a traditional internal combustion engine. He decided against an e-boda (electric motorcycle) due to his counterparts’ negative experiences with the first-generation e-bodas. His business was brisk until 2020, when COVID-19 shutdowns led to reduced demand for nano-entrepreneurs.

WE Hub regularly conducts in-person discussions with WLBs in similar businesses. However, those meetups primarily catered to training sessions or discussed physical marketing (fairs) events. MSC mobilized WLBs to come together and discuss the challenges around their business’s management with WLB’s support. The group was a good mix of mature and nascent business-stage WLBs.

WE Hub regularly conducts in-person discussions with WLBs in similar businesses. However, those meetups primarily catered to training sessions or discussed physical marketing (fairs) events. MSC mobilized WLBs to come together and discuss the challenges around their business’s management with WLB’s support. The group was a good mix of mature and nascent business-stage WLBs.