Women in low-income communities may choose a channel based on the most economical choice that suits their life best, given their acute burden of unpaid care work and time poverty. It is critical to decode gendered aspects that lead women to choose their selected channel to help build their financial resilience.

MSC’s DEBIT framework helps us understand which channel the individual chooses and why. Comparing the DEBIT scores helps us identify actions that stakeholders like governments and financial service providers can undertake to help women have a wider range of channels to choose from.

Financial inclusion for women in India still has a long way to go. While more women appear to be financially included, the use of these accounts remains limited across the country, especially among low- and moderate-income (LMI) women. Women’s ownership of bank accounts has improved over the years. The increase is primarily due to the PMJDY mission, which was crucial to reducing the gender gap in bank account ownership—from 19.8% in 2014 to 6.4% in 2017. Findex 2017 reported that 77% of Indian women owned a bank account against 43% in 2014 and 26% in 2011. Yet it also shows that the estimated gender gap in account ownership and usage remains significant.

Women face relatively higher barriers to using financial services at the bank or agent point due to their limited mobility and adverse gender-based norms. Although pivotal to accelerating the usage of bank accounts, digital financial services continues to be under-utilized, especially among women in India.

Key drivers of the gender gap

Women’s low utilization of bank accounts mainly stems from operational factors and limitations placed by social-cultural norms. On the supply side, a lack of focus on women’s needs and financial behavior remains a crucial driver to their low utilization of financial services. Banking products and services do not recognize that women and men have different financial behaviors deeply influenced by gendered social norms. For example, women prioritize privacy and savings. They have horizontal social networks, smaller economic geographies preferring to transact closer to home due to less free time available, and constraints on safe mobility. They also have varied lifecycle needs as they experience more transitions like marriage, maternity, and childbirth.

The promise of DFS in addressing the gender gap

DFS can help women overcome these barriers by offering solutions that they can access remotely, safely, and cost-effectively. Such solutions could be designed to enhance privacy and women’s control over their money. It could address women’s time poverty and mobility constraints by allowing them to transact at their preferred time and location. The solutions could also help them cope better with emergencies by making it easier for women to send and collect funds from different sources. Effective digital savings tools could help women with managing risk better and enhancing their financial asset base. A digital footprint of women’s transactions can also help make their creditworthiness more visible to banks and financial service providers.

Suffice to say, DFS could be a strong catalyst for women’s economic empowerment.

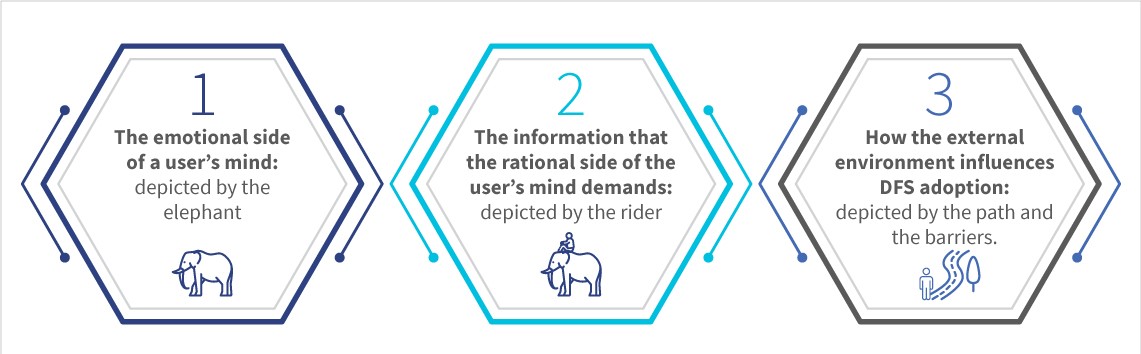

Inspired by the “Elephant, Path, Rider” framework by psychologist Jonathan Haidt, an examination of the journey of using DFS for the first time by men and women shows the interplay of the emotional and the rational mind for each step within the journey. The customized framework highlights three essential contributors to changing a user’s perspective to DFS and their interaction with it. These are:

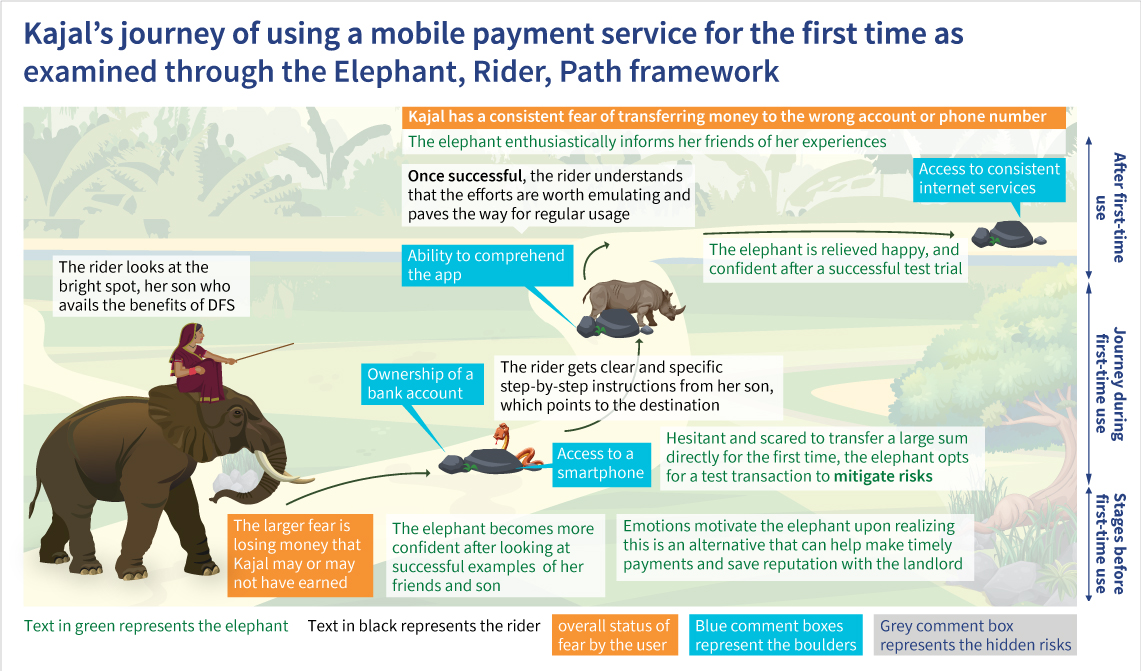

The below is a snapshot of Kajal’s (a volunteer at Odisha Livelihoods Mission) journey of using a mobile payment service for the first time. Despite a positive experience, she hesitates to use DFS the next time due to her risk-averse nature and the limited availability of customer service to help with any errors she may make.

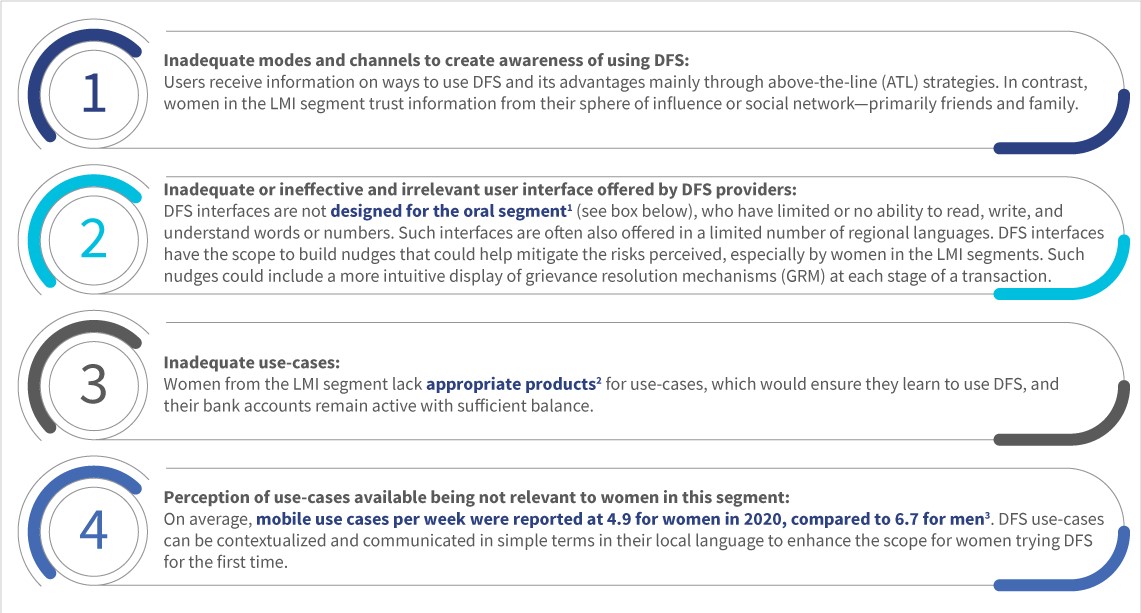

This examination has helped identify the following critical factors that contribute to limiting the uptake of DFS, especially among women:

The government’s response

Government departments have undertaken several initiatives to enhance the use of financial services, including DFS. These initiatives include efforts undertaken by the Department of Financial Services, the Ministry of Rural Development, and NITI Aayog. They focus on enhancing access to financial services among women and ensuring account ownership at the last mile.

While these government initiatives are laudable, the complex range of physical, social, and psychological barriers mean that they are unlikely to be adequate, even if they achieve scale. If India intends to achieve real digital financial inclusion for all, it will need to expand the financial services space for millions of low-income women.

Expanding the financial services space would require creating convenient access, valuable use-cases, exposure, and trust-building—first through assisted access to DFS. Female BC agents at the last mile could be a critical channel to encourage exposure, build trust, and ensure a positive first experience of DFS for women users. These local agents are an integral part of the community and enjoy women’s trust. Ultimately, these agents could provide women with the skills, confidence, and trust to use digital tools to conduct self-initiated transactions—especially if they can get their hands on intuitive user interfaces.

The Jakarta Post first published this blog on 8th March, 2022.

Working from home: A choice for some but a circumstance for another

Work from home (WFH) has become associated with the pandemic for those who have the luxury to choose to work from home. Yet not everyone can have this option and still have sustainable income, decent working space, and secured social protection each month. “Other” work-from-home workers have been working from home much before the pandemic but under different working circumstances.

These others are home-based workers. According to the ILO/MAMPU project report, home-based workers (HBWs) are those “who are self-employed and/or subcontracted piece-rate workers (putting-out system), and most of them are women.” In Indonesia, the law on MSMEs also accommodates the concept of home-based workers, categorizing them as an informal sector.

The Implementation Guideline to Home Industry Development, published by the Indonesian Ministry of Women’s Empowerment and Child Protection (MoWECP), classifies home-based workers as a cottage industry. A cottage industry is a production system within which products are produced by creating additional value from raw materials, carried out in individual homes and not in a particular location (factory).

Yet these home-based workers, whether in the putting-out system, self-employed, or part of the cottage industry, remain vulnerable to shocks. The Indonesian Labor Law is yet to define HBWs. Indonesia has yet to ratify the ILO Convention No. 177 on homeworkers. In the absence of a law, HBWs remain predominantly informal workers. Informal workers lack formal contracts, stable income, high wages, health cover, workers’ insurance, and adequate working conditions. The absence of a law increases their vulnerability to unemployment, exploitation, and poverty.

A WIEGO 2021 Statistical Brief outlines that COVID-19 exacerbated the already-existing multiple vulnerabilities of HBWs. For those who do not use ICTs in their work, HBWs suffer the greatest loss of work and income. In Indonesia, despite the challenges, women in informal work have proven to be resilient, even though they are paid lower than men. A Jakarta Post article also mentioned that informal female workers, such as women HBWs, are expected to also take on the primary child-rearing responsibilities and housework, besides earning low wages.

Sense and workability: A facilitator’s remark on women home-based workers

In many social development programs, heroes in the field contribute to the success of a program. One such hero in this context is Zaenab Hafiezh. Zaenab is a local facilitator who supports the MoWECP’s program on women’s economic empowerment for female home-based workers in Rembang Regency (Central Java Province).

Zaenab, also an HBW, applied to be a facilitator in 2016 for MoWECP’s women home-based workers program in Rembang. The MoWECP was set to support the program for only two years, after which it would continue from the local regent office. While many of her fellow facilitators resumed their role, Zaenab was among the ones that continued her critical role as facilitator to several women HBWs in the neighborhood.

As a fellow HBW, Zaenab understands her peers’ situation, challenges, and needs in navigating livelihood strategies and securing basic everyday essentials. Zaenab facilitates women HBWs who are self-employed and in the putting-out system. Her task is to support the mobility level and empowerment of those she facilitates, according to the “implementing guideline on home-based workers” published by MoWECP.

This program was part of the ministry’s effort to achieve the 3ENDs, namely: (1) ending violence against women and children, (2) ending human trafficking, and (3) ending economic inequality between men and women.

To Zaenab, the 3ENDs goals reflect real concerns she learned from several experiences of her fellow HBWs. She also believes this women’s home-based economic empowerment program by MoWECP is a tactical approach to reducing violence, trafficking, and economic inequality in her hometown. Zaenab’s facilitation journey, though, was not smooth. She faced risks from husbands who rejected the program and blocked their wives from participating. Yet she saw other instances where this program could help survivors exit domestic violence situations. From her observation, women HBWs experience economic struggles alongside domestic violence. The burden does not stop there. Some of these women are the primary breadwinners for their families and struggle to make ends meet while caring for children and household chores.

Based on the lessons from Zaenab’s facilitation, the workability of women HBWs depends on the fulfillment of four critical needs. These are:

Assistance in strengthening leadership and confidence as women home-based workers, to enhance eligibility and mobility;

Support in capacity building on product development and marketing to increase the value of their work;

Facilitating a safe space to include men in the conversation, especially husbands of women HBWs, who are also vital to support their wives;

Commitment in policy and budgeting to recognizing and protecting home-based workers as acknowledged workers.

Zaenab notes that if the above needs are supported, the pathway to increasing female home-based workers’ mobility level, quality of employment, and economic empowerment is achievable and will help achieve the 3ENDs objectives.

The MoWECP stated that:

1. Strengthening women’s leadership and economic empowerment is part of its mandate under the gender mainstreaming unit and as part of their home-based workers’ programs. It has initiated a series of awareness campaign activities as part of this endeavor. This includes socialization on themes related to gender equality, gender-equality-based entrepreneurship, eliminating violence against women and children, and reproductive health.

The MoWECP also notes the importance of including men in conversation and awareness programs on women’s economic empowerment. It has already included partners to develop and execute more tailored programs as needed.

2. The MoWECP has also connected with some sub-national governments to promote local homeworkers’ products in local markets, through local and national crafts councils, and to affiliated companies and private sectors. The mentorship program will also serve as a platform to enhance product development and marketing capacity.

3. MoWECP supports the endeavor of several local governments that made local commitments through development planning and budget. It has also mandated its agencies on-site to be the activity focal point to support local initiatives.

Yet MoWECP realizes that it too will need collaborative support from allies to achieve the needs of women home-based workers comprehensively.

Friends, allies, and comrades

So, who are these allies of women home-based workers in Indonesia who can fulfill the said needs? Moreover, how can more players support their empowerment pathway?

The MoWECP has been a friend, ally, and comrade to women home-based workers by initiating the women’s home-based economic empowerment program since 2016. MoWECP has organized a pilot program in 21 regencies and cities. It is now is in the progress of replicating these efforts to other regencies and cities. The program’s success stories, such as those led by Zaenab, have become references of best practices to other sub-national governments to have the same commitment in strengthening women home-based workers in their area.

In MSC CPD Indonesia’s discussion with the Economic Assistant Deputy of MoWECP, Eni Widiyanti, she mentioned that MoWECP is committed to improving the conditions of women home-based workers. This commitment is also strengthened by connecting with like-minded organizations like MSC CPD Indonesia.

MSC CPD Indonesia also works on economic and financial inclusion, supporting MoWECP to strengthen women’s economic empowerment through economic inclusion and digital financial inclusion. MSC applies a gender-centrality framework to ensure its work on women’s economic and financial empowerment is inclusive and gender-responsive.

Other friends, allies, and comrades are the coalitions of civil society organizations, such as the Indonesian Homeworkers Network, the Indonesian Social Observer Foundation, and Homenet Indonesia. They have voiced and influenced the national and sub-national legislation on protecting home-based workers in Indonesia. The Ministerial Regulation on the Protection of Home-based Workers is not yet legislated. Yet at the sub-national level, local leaders have developed local regulations and policies that champion the narrative for an equal and inclusive working system for home-based workers. To name a few, local CSOs like TURC, Yasanti, and BITRA have been making progress on this advocacy in Java and Sumatra provinces.

CSOs play a significant role in connecting and networking on the issue with other strategic actors and organizations, which are potential allies in this campaign. Some conversations have also included local employment agencies, women’s empowerment agencies, and local development agencies.

MSC CPD Indonesia is also a friend, an ally, and a comrade to women home-based workers. MSC CPD Indonesia is currently developing a partnership with MoWECP to strengthen women’s economic empowerment through economic and digital financial inclusion.

Homework on home-based workers

The Rembang Regency experience led by Zaenab revealed the ecosystem of work for women home-based workers, which remains challenging. Yet these challenges can gradually be overcome with coordination, collaboration, and most of all, commitment to the recognition and protection of home-based workers. Zaenab’s experience also indicates that capacity building on gender equality and social inclusion on HBW should not be limited to the HBW. Instead, it should expand to all relevant stakeholders and key figures in the ecosystem. These stakeholders include men in the family, local and national government officials, private companies, service providers, and public institutions. Almost all have a weak understanding of the issues that women HBWs face. Strengthened coordination and collaboration can support the recognition of HBWs as workers and speed up processes to advocate policies and regulations on their protection.

Recognizing the profiles and gaps of women HBW can be enhanced by improving national and sub-national gender equality and social inclusion disaggregated data on HBWs. Such recognition will ensure they are not invisible in data. It will also ensure informed and comprehensive decision-making based on the reality and needs of (women) HBWs can fill the void on policies and development toward a decent, recognizable, and sustainable working condition for them.

Supporting the ongoing work of local CSOs and advocacy for the empowerment and protection of home-based workers is also vital. These CSOs can be partners and tandems of decision-makers and providers to assist in mainstreaming a comprehensive design and implementation of empowerment programs and policy development for and on home-based workers.

And last but not least is the inclusion of those not included in prior conversations and decision-making processes. Making room for HBWs, facilitators, companies, and service providers in the campaign and awareness dialogue and program designs on HBWs would ensure balance, meet the needs, and reinforce equity to improve their lives.

Finance Minister Nirmala Sitharaman, in her budget speech 2022, mentioned some significant reforms towards government procurement that have happened over the past few months. These are welcome developments in a landscape marked by State’s weak budget execution capacities. However, there needs to be a stronger push towards adopting public finance management reforms to enable the government to manage its finances better.

Take for instance the nearly Rs 2000 crore of idle funds recently unearthed by the special task force set up by the Tamil Nadu government. State Finance Minister Dr. Palanivel Thiaga Rajan called it a “trailer” with the whole picture across thousands of bank accounts yet to be seen.

The issue of unspent funds or ‘idle float’ lying in government accounts is, of course, not a new revelation. Last September, the Comptroller and Auditor General (CAG) of India highlighted a whopping Rs.4.72 lakh crore remaining unspent in FY19, citing poor budget formulation as a leading cause. Former CAG Rajiv Mehrishi had also pointed to the problem of unsatisfactory monitoring of allocated budgets and suggested an “end-to-end enterprise-based IT system” to improve expenditure tracing.

Idle float is a symptom of inefficient use of public funds. The funds stuck in the bank accounts of various government agencies as float add to the public debt. This is ironical for a low middle income country like India, since government cannot meet it expenditure commitments from its own funds and has to borrow additional funds adding to the fiscal deficits and the challenges that come in its wake. Downstream macro-effects include lower credit availability for the private sector and eventually, slower economic growth.

It also has a huge opportunity cost in the form of scarcity for those Implementing agencies (IAs) that have spent their allocations and need funds urgently. These IAs then struggle with mounting arrears and unpaid dues to contractors. This even as funds are available aplenty with other IAs and programs. This paradox of simultaneous plenty and scarcity manifests on the ground as poor service delivery to citizens.

Issues galore, reorientation a must

How does public finance work in India? If visualized as a tree, the Centre or states are at the top and transfer funds to lower branches representing state, district, local governments and panchayats. For most Centrally Sponsored Schemes (CSS), there is a multi-layered fund release mechanism. Each step of fund flow requires documentation, usually utilization certificates (UCs), to prove previous payment tranches have been used up. When this is done, the relevant state-level department releases more funds.

A delay at one branch – say, at the district level – for any reason often hampers the smooth release of funds to the next one, i.e. the block or panchayat level. As a result, funds often get stuck for years. Furthermore, after tranches are transferred, they are often not spent within a stipulated time period either on account of work not being done on time or delays in reporting.

Importantly, the flow of information is no smoother, resulting in a lack of observability on expenditure status. In most cases, data at the primary unit of activity (e.g. teacher attendance or weight measurement of a child by an Anganwadi worker) is fed manually and gets digitized “manually” by an army of Data Entry Operators (DEOs) who enter program data in computers. This same data, often with compromised authenticity, moves from one IT system to another. This too is done through another round of manual entries, not automatically through data exchange protocols between interoperable systems.

Overall, the data that resides in the system is recorded away from the primary unit of activity, and through a series of manual processes between disconnected information systems. This leads to a gap in the reporting of physical and financial progress.

While the Public Financial Management System (PFMS), managed by the Controller General of Accounts (CGA), has certainly helped such flows become more traceable over time, the scale of the issue demands a mix of process and technology interventions.

So, what’s the solution?

There is an urgent need for these disparate systems to ‘talk to each other’. This will require an approach that integrates digital principles with public finance management (PFM) principles. These integrated ‘Digital PFM (DPFM) principles’ can transform the PFM ecosystem and improve governance and development outcomes. Two specific ones, Just-in-Time (JIT) and Single Source of Truth (SSOT), are starting points of the DPFM journey.

A JIT funding approach for centrally sponsored, central sector and state schemes will enable real-time funds transfers to the payee (contractor or individual) instead of it being parked in the bank account of implementing agencies (IAs). It would negate the need for pre-loading or funds transferred in advance.

It’s analogous to a bank issuing a credit card and defining a spending limit on that card. It authorizes an individual to spend up to a specific limit without transferring advance money into that individual’s bank account. Similarly, the Centre and state governments can define the spending limit of IAs for their respective schemes, without transferring money in advance. Money flows directly into the bank account of the contractor or beneficiary, only when the work is complete and the money is due. Modern technology allows this to work seamlessly with some tweaks in work practices. In fact, Rule 230(7) of the General Financial Rules, 2017, recommends JIT but unless it is implemented in principle and totality, the government and citizens cannot reap the technological benefits.

Similarly, pursuing an SSOT will enable aggregating scheme/program data at a single point that is accessible to a variety of public departments and agencies. This would foster higher systemic accountability and transparent reporting by individual departments and program heads. It will allow quick and, in some cases, algorithmic decisions. Such high-fidelity data is critical to the functioning of a JIT system.

Way forward

DPFM principles such as JIT and SSOT do not require an overhaul of current systems. They all have an associated technology play that just needs to be layered on current systems with tweaks in work practices. The PFMS is one part of the solution. It already tracks funds and expenditures. It can be re-factored a little, or a new module for JIT can be created to meet the requirements of real-time fund release and improve visibility.

Such enhancements will improve scheme monitoring and reduce float. If JIT can be integrated with the program MIS, it can help auto-trigger both payments from the Consolidated Fund of India or State to a department or program as well as to end beneficiaries. This would help administrators focus more keenly on service delivery than simply approving payments at respective branches. And one must not look far for inspiration. The Government of Odisha is implementing the Just-in-Time rule for various schemes such as the ‘Grant-in-Aid to Special Schools’ under Social Security & Empowerment of Persons with Disabilities Department (SSEPD) and the ‘Urban Wage Employment Scheme (MUKTA)’ under Housing and Urban Development department.

The Centre and States would do well to consider these smart solutions in their existing PFM architecture. The wins would not just be mutually beneficial; but have long-lasting positive impacts on state capacity, government savings, welfare planning, and service delivery.

This blog first appeared as an Op-ed in the Times of India, on March 9, 2022.

In collaboration with multiple partners across countries, MSC has collated inspiring stories of grassroots leaders. The booklet shares a snapshot of their journey, experiences, and insights and is a testimony to their grit and resilience. It also gives us a glimpse of the hardships women grapple with at the last mile.

MSC worked with the Reserve Bank Innovation Hub (RBIH) on a whitepaper on “Gender and Finance in India” for its स्व-नारी (Swanari) program. The paper discusses the landscape of gender and finance in India and highlights the main gaps in gender. Its premise is that applying a gender lens to financial inclusion is essential to understand barriers women face around equal access, usage, and quality of financial services offered. The paper analyzes public data on gender gaps in savings, credit, insurance, and pensions. Using inputs from experts and stakeholders, it attempts to understand key gender-based barriers. The whitepaper arrives at crucial problem statements around access, usage, and quality of financial services for the Swanari program. It also shares some promising innovations, good practices, and stories of female users and financial services providers. The paper ends with a call to move “toward gender-intelligent banking” and shares critical enablers that could catalyze women’s financial inclusion.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.

Financial inclusion for women in India still has a long way to go. While more women appear to be financially included, the use of these accounts remains limited across the country, especially among low- and moderate-income (LMI) women. Women’s ownership of bank accounts has improved over the years. The increase is primarily due to the

Financial inclusion for women in India still has a long way to go. While more women appear to be financially included, the use of these accounts remains limited across the country, especially among low- and moderate-income (LMI) women. Women’s ownership of bank accounts has improved over the years. The increase is primarily due to the