COVID-19 has led to lockdowns and restrictions on social engagements, resulting in increased usage of digital technology and tools across the globe. Today, we cannot talk about the entrepreneurship ecosystem without first looking at the challenges entrepreneurs encounter due to these restrictions.

Digital skills will be essential for 50-55% of jobs in Kenya, 35-45% in Cote d’Ivoire, Nigeria, and Rwanda, and 20-25% in Mozambique by 2030. Foundation digital skills will garner about 70% of the demand, while non-ICT, intermediate-level digital skills will account for 23% of the demand.

Importance of digital skills in youth entrepreneurship

Youth entrepreneurs are vital to a country’s social and economic development. According to the African Development Bank, 10-12 million youth enter the workforce each year, but only 3 million secure wage-earning jobs. As a result, fostering entrepreneurship among young people is essential.

Kutzhanova et al. (2009) examined four main dimensions of skill for entrepreneurs:

- Technical skills needed to create the business’s product or service;

- Managerial skills essential to the day-to-day management and administration of an enterprise;

- Entrepreneurial skills to recognize economic opportunities and act effectively on them;

- Personal maturity skills include self-awareness, accountability, emotional skills, and creative skills.

Since the onset of COVID-19, the tone of entrepreneurship has changed. As technology expands to become an integral part of our everyday lives, young entrepreneurs need to build their digital skills.

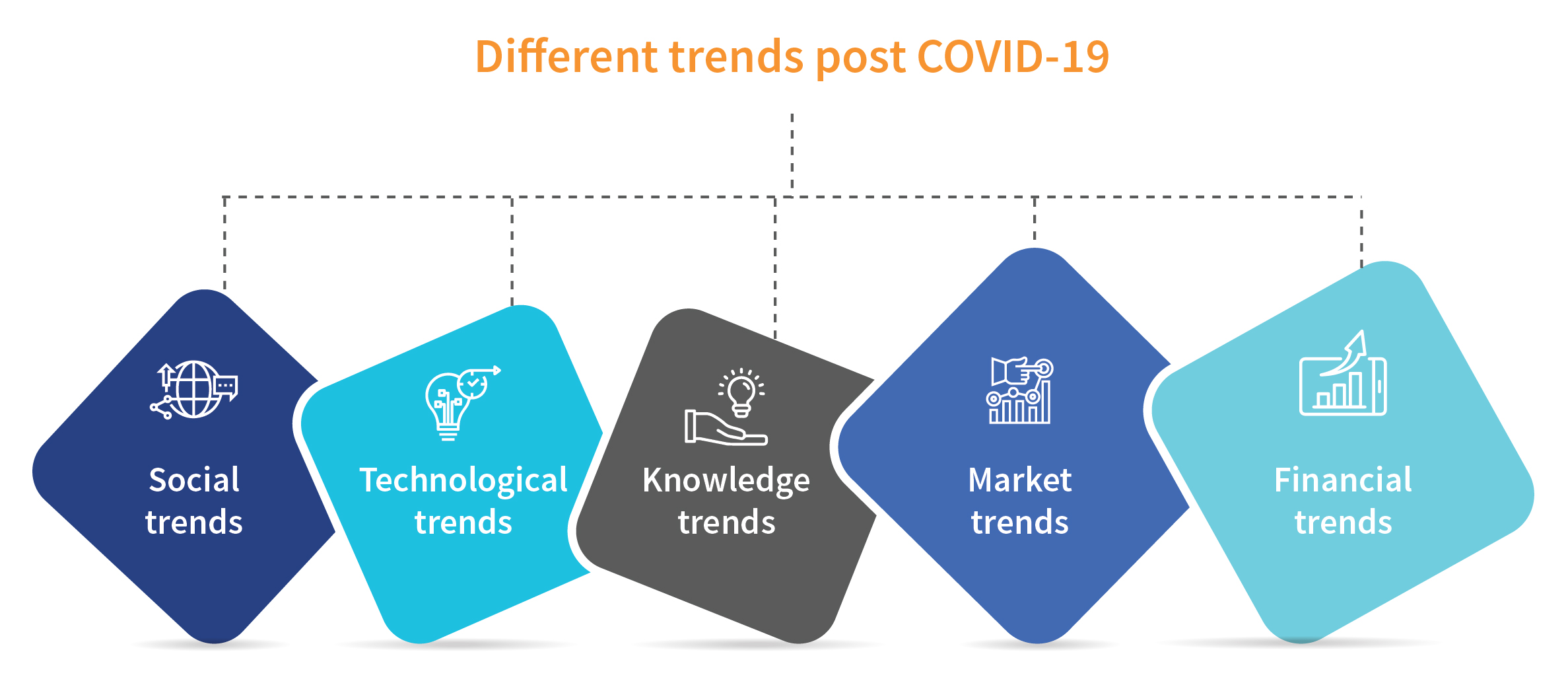

After the outbreak of COVID-19, we have witnessed different trends:

Figure 1 showing different trends observed after COVID-19 outbreak

- Social trends: Post COVID-19, the way people interact in society changed. DataReportal highlights that 4.7 billion people worldwide now use the internet, while 4.1 billion people have social media accounts. The user bases registered a growth of 7.4% and 12.3%, respectively, in 10 months from 2019 (as of October, 2020).

- Technological trends: Dependence on technology has increased, and COVID-19 has altered how we live and work. These changes have led to an explosion of new technologies and innovation, forcing businesses to adapt or disappear rapidly.

- Knowledge trends: Online delivery is often the preferred channel for education and training due to lockdowns.

- Market trends: E-commerce has revolutionized the way customers interact in the market. Some countries have achieved 7% growth in this sector, where the average growth rate is usually around 1%.

- Financial trends: A higher uptake of digital financial services (DFS) has eased access to financial products. A World Bank policy report finds that at least 58 developing countries have used digital payments for COVID-19 relief.

With these changing trends, young entrepreneurs must learn new skills to remain relevant.

Digital skills and their applications

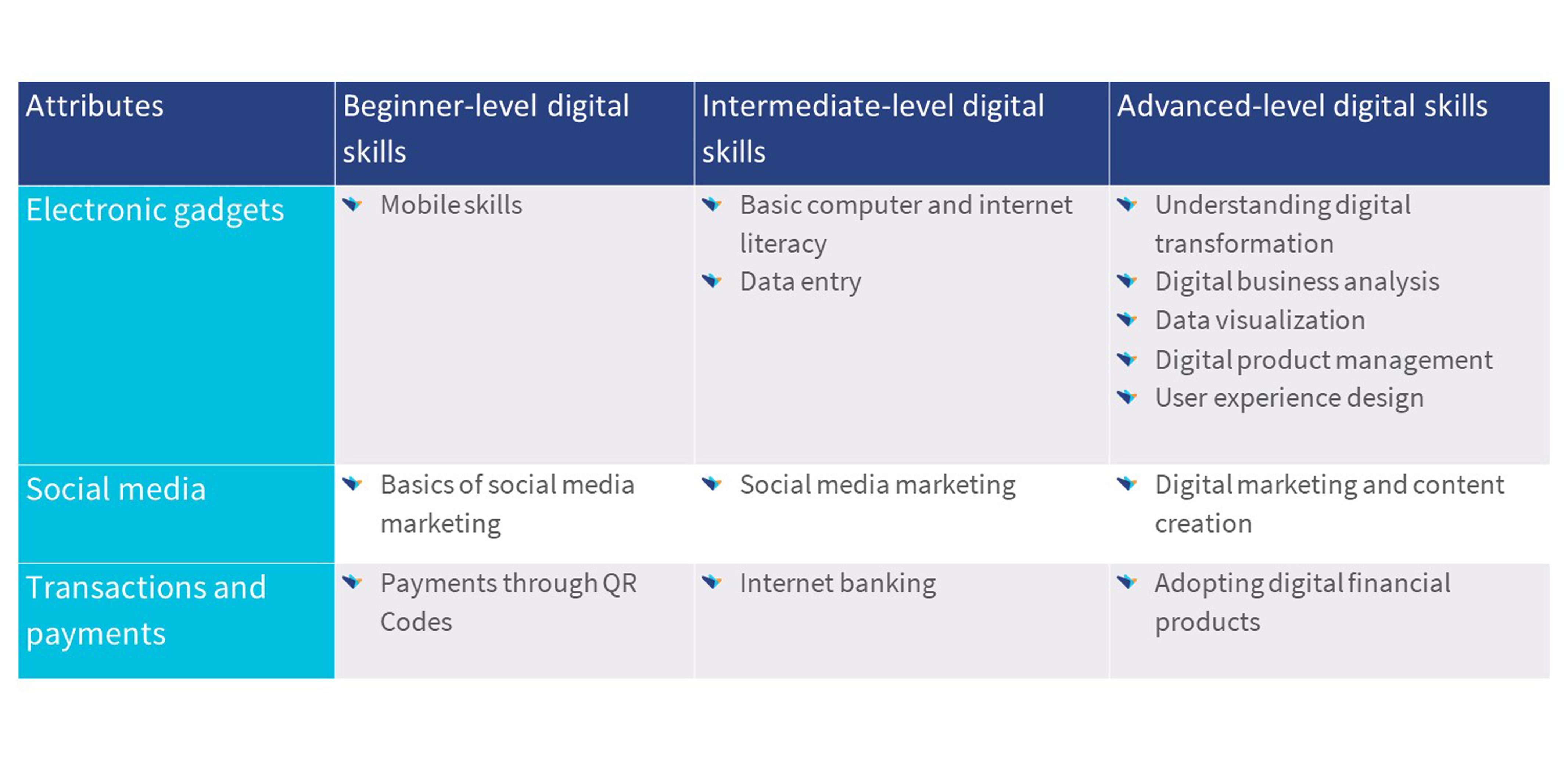

According to UNESCO, digital skills are abilities to use digital devices, communication applications, and networks to access and manage information. This means knowing digital skills and the ability to apply those skills in the digital world. Hence, young entrepreneurs need to learn digital skills and integrate them into their enterprise.

A recent ILO study suggests new technologies in enterprises enhance how well they can increase productivity, create employment, reduce poverty, and promote local development. We classify digital skill tools into beginner-, intermediate-, and advanced-level digital skills (see Table 1).

Table 1: Need for different digital skills for young entrepreneurs at various stages of evolution

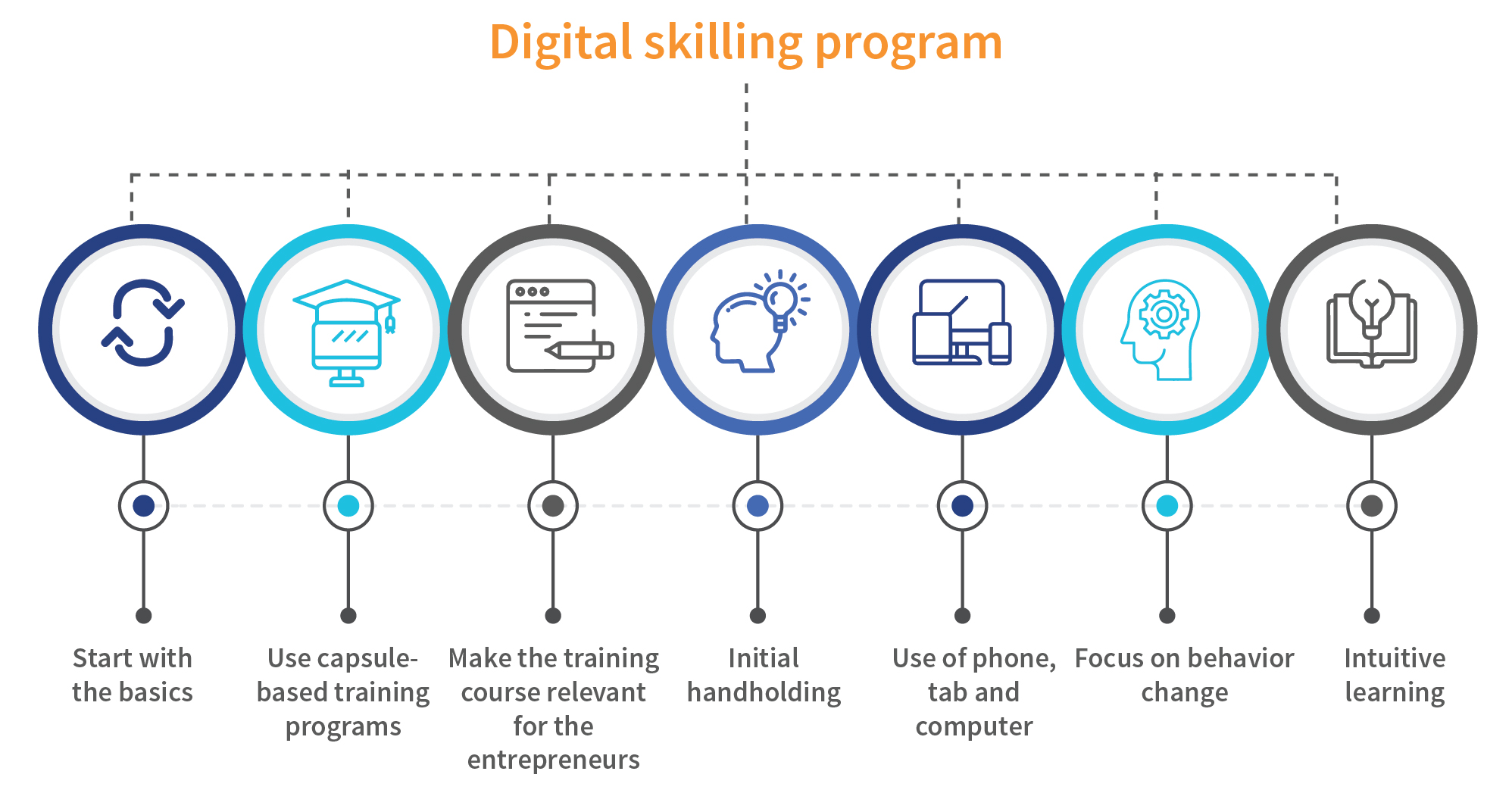

Critical lessons from MSC’s 15 years of experience in making digital skills training more effective

- Start with the basics: Start the training with the basics of digital skills and gradually move to intermediate and advanced skills based on the need of the enterprise

- Use capsule-based training programs: Starting or running an enterprise is time-consuming, so it is vital to understand that we divide a training module into tiny capsules to ensure better use of the entrepreneurs’ time. MSC through its training arm, the Helix Institute at MSC has developed a course in collaboration with the Mastercard Foundation, “Getting started in entrepreneurship.” We deliver this course in a self-paced mode on our learning management system (LMS).

- Make the training course relevant to the entrepreneurs: Use visualization tools to make the entrepreneurs understand the relevance of the digital skill training for their enterprise; use relevant and impactful images and local language to guide users through the interactive activities

- Deliver intuitive learning: Include elements of gamification and fun in interactive learning; gamify progression across modules, so the learners are motivated along the process; incentivize learners for certification, and mentorship opportunities

- Focus on behavior change: Anchor the design on the desired behavior and the pathway to move from the current behavior to entrepreneurial behavior.

- Provide initial handholding: Users initially need guidance but can quickly start taking the lessons forward. Hence, an initial handholding is vital to building a foundation for the skill training and confidence in it.

- Use a phone, tablet, or computer: The training needs to be delivered using a phone, tablet, or computer to maximize the adoption of these digital skills.

Figure 2 showing different elements that can make digital skills training effective

Figure 2 showing different elements that can make digital skills training effective

Our approach to delivering a digital skilling program

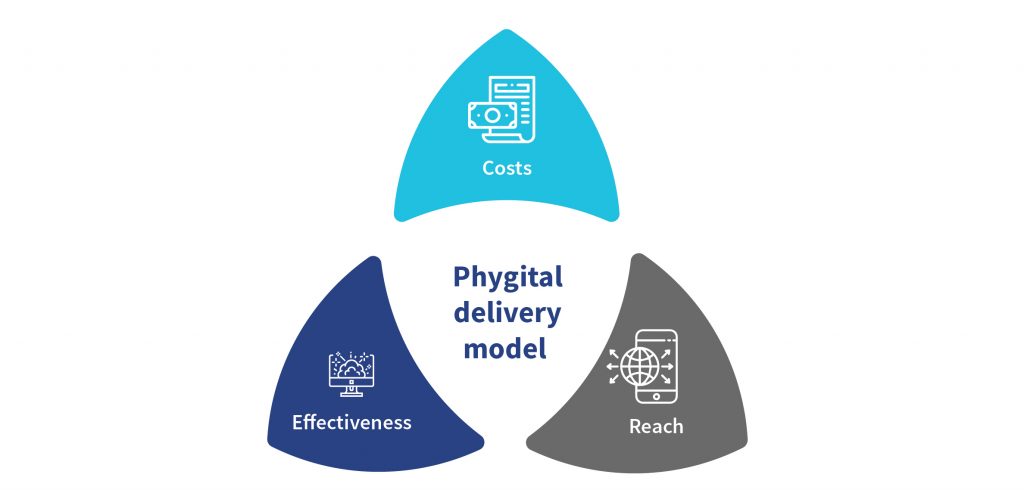

A critical step needed to foster digital skills among young entrepreneurs is to deliver the program effectively. Digital skilling programs can be delivered through different channels.

- Online skilling program: Online skilling programs use digital means to enhance the learners’ skills and capacities. This mode of delivery provides high value for money and is scalable; however, it offers limited interpersonal relationships. The effectiveness of online course delivery depends on the learner’s motivation level and appropriate course design and delivery tools.

- In-person skilling program: In-person skilling programs score high on effectiveness; however, the costs are comparatively high and not immensely scalable.

- Phygital model: Our approach is to design and deliver digital skilling programs that balance reach with effectiveness and cost of delivery. The phygital (physical+digital) skilling program combines in-person training to onboard people to digital means of learning. Our financial literacy program for refugees and the host community for UNCDF in Tanzania combined phygital approaches. The program covered mobile money and formal financial services, savings groups, and managing money. We suggest using a phygital model of delivery for such skilling programs to empower young entrepreneurs for sustainable learning.

Figure 3: Phygital delivery model

Young entrepreneurs must be supported to reduce digital skills gaps

Emerging economies require digitally savvy young entrepreneurs to build robust digital economies. By enhancing the digital skills of young entrepreneurs to transform their new and existing enterprises, we contribute to their increased productivity and employment opportunities. Government and funding agencies have an essential role in reducing the digital skill gaps among young entrepreneurs by introducing digital skill-building courses.

MSC worked with institutions like Expresso to improve the incubation approach in providing training and support to aspiring young entrepreneurs, allowing them to develop innovative solutions. In this partnership, we performed activities like mentor connect, The Hub for Digital Finance, coaching sessions, boot camps for startups and young people, and identification of customer segmentation. This program benefited almost 200 young people in Senegal. For more details on our work with young people, click here.