Tag: Savings services to the poor

Graham Wright and Leonard Mutesasira

The relative risks to the savings of poor people

In view of the highly risky nature of saving in the informal sector, it is...

Jul 16, 2018

Anurodh Giri, Nishant Kumar, Sakib Mehraj and Ritika Srivastava

Relative risk to the savings of the poor in Uttar...

In order to understand how poor people save and the relative risks involved, MicroSave conducted...

Jan 6, 2011

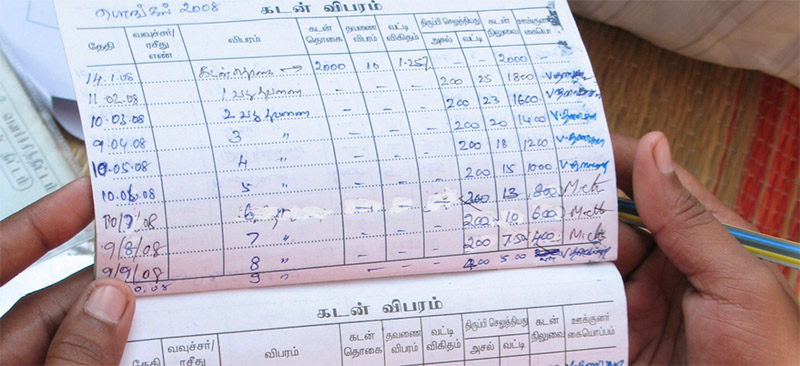

Savings Booklet

The Savings is the third publication under the OPE Series. This Booklet brings together a...

Mar 12, 2010

- 1

- 2