For well over a decade, MSC (MicroSave Consulting) has assessed and analyzed a broad range of government payment programs across Asia and Africa. Government welfare programs often suffer from the intention-impact gap—largely a consequence of poorly planned or executed communication. As a result, crucial information either becomes distorted or fails to reach recipient families.

This blog explores the intricacies of government communication using case studies and best practices from welfare delivery programs across various countries.

Live and learn: Case studies

The Pradhan Mantri Ujjwala Yojana (PMUY) is a widely promoted welfare program in India that provides low-cost and subsidized liquefied petroleum gas (LPG) cylinder connections to more than 80 million beneficiaries. The program offers beneficiaries LPG connections and equipment kits, including a stove and pipe, at a 50% subsidy. Beneficiaries could pay the remaining 50% either upfront or in installments. However, if the beneficiary opts to pay in installments, they would not be provided the promised subsidy on the purchase of LPG refills until they finish paying the installments to settle the full amount.

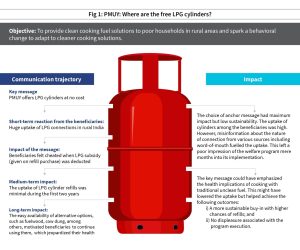

The government had promoted the program heavily through both print and electronic media, including advertisements using public hoardings and TV commercials. However, publicity at the local level through “word of mouth” erroneously declared the connection free of cost. As a result, most beneficiaries felt cheated when their subsidies on the purchase of LPG refills were deducted. The identification of local influencers and clear definition of the offering—clean and subsidized but not free cooking fuel, would have kept the message on track and set correct expectations. Figure 1 unpacks some of the avoidable hiccups in the promotion of PMUY.

The government had promoted the program heavily through both print and electronic media, including advertisements using public hoardings and TV commercials. However, publicity at the local level through “word of mouth” erroneously declared the connection free of cost. As a result, most beneficiaries felt cheated when their subsidies on the purchase of LPG refills were deducted. The identification of local influencers and clear definition of the offering—clean and subsidized but not free cooking fuel, would have kept the message on track and set correct expectations. Figure 1 unpacks some of the avoidable hiccups in the promotion of PMUY.

Under the successful “Give It Up campaign” of 2016, the government appealed to affluent LPG consumers capable of paying the market price to surrender their LPG subsidies voluntarily. The program inspired 10 million well-to-do households to surrender their LPG subsidies, which can then be channeled to poorer households. The withdrawal of subsidy is a tricky issue that governments in the past have failed to address. Then why did it succeed this time?

The “Give It Up” campaign was primarily successful due to two factors. Firstly, the target audience was presented with a clear picture of the problem and the proposed solution. Secondly, the citizens who gave up their subsidies received individual recognition in the scroll of honor. Unlike transient promotional content on mass media, individuals had a proud proof of their contribution, which sparked mass philanthropy. The voluntary nature lent the mantle of a good samaritan to the citizens and inspired better engagement. Figure 2 depicts the objectives of the campaign and the behavioral levers it used to succeed.

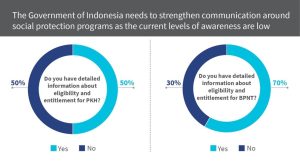

MSC’s assessment of G2P programs in Indonesia highlights the need to optimize communication for social protection programs. For instance, our study of the Program Keluarga Harapan (PKH), a conditional cash transfer that targets poor households, revealed that poor communication limited its success. 50% of respondents did not know the exact details of their entitlements and the withdrawal process. Even frontline workers lacked adequate program information as they encouraged beneficiaries to withdraw their benefits as soon as possible. This led to a misconception that the government would take the money back if any balance remained in the accounts of beneficiaries.

Similarly, beneficiaries of the Bantuan Pangan Non-Tunai (BPNT), a food assistance program for the poor in Indonesia, also highlighted communication gaps related to entitlement and eligibility. The government developed targeted communication and training material for frontline workers and field facilitators. However, it could not promote these well, as many frontline workers reported no awareness about the information material.

The case studies mentioned above suggest that poor communication impedes program and system-level functions despite intensified efforts to strengthen welfare delivery programs across the globe. At the program level, communication and outreach need to be robust to disseminate information related to targeting, benefit delivery, payment methods, monitoring, evaluation, and grievance resolution. At the system level, the focus must be on synchronizing the efforts of various stakeholders to reduce information gaps and overlaps.

A structured approach: Recommendations

A structured approach: Recommendations

Well Made Strategy has outlined six steps to strategic communication that can be used as a clear checklist to reduce communication gaps in the welfare delivery programs.

1. What is the desired change?

Clarity on the objectives of communication is imperative. Steps to achieve the same are as follows

2. Who is the target audience?

Identification of various stakeholders whose engagement will help fulfill the communication objectives is essential for the judicious use of resources. These stakeholders may include existing and potential program beneficiaries, frontline workers, local opinion leaders, and NGOs, etc.

The knowledge of their cultural specifics, socio-economic situation, and perception of the campaign objectives helps create a more effective reach. Customize the content and frequency of communication, based on the nature and involvement of stakeholders—direct stakeholders need to be informed more frequently due to their direct engagement with the last mile.

3. How can you best connect with the audience?

3. How can you best connect with the audience?

A study of the target audience, their life cycles, and typical aspirations for the program will help identify the messages and channels suitable for them.

4. What do you want them to know and do?

Messaging should be focused and not generic. The significant difference in demographics and socio-cultural situation of people in rural geographies and their urban counterparts are necessary to consider. Beneficiaries should have access to clear and concise information about their entitlements, eligibility, and other program-related nuances in the most simplified manner. The messages should be in the local language and designed to overcome exclusion factors, such as illiteracy, disability, etc.

5. What communication channels should you use?

Communication channels should be selected based on their reach, frequency, and credibility. The use of multiple communication channels can help target a variety of audiences across gender, age groups, literacy rates, and location—urban or rural.

6. How do you know whether you have influenced the audience?

6. How do you know whether you have influenced the audience?

The monitoring and evaluation of the impact of communication efforts are important. Collect feedback on the effectiveness of the communication aspects of G2P programs. This would help feed lessons and improve the overall outcomes of the program.

While the framework detailed above is an effective tool to craft a good communication strategy, its use is not limited to welfare delivery programs. Today, governments across the globe face the herculean task of managing the COVID-19 crisis. Keeping the citizens calm and informed about important details is one of the key goals. Since the onset of the pandemic, governments have taken several initiatives to make communication more clear, effective, and timely. We will analyze the highs and lows of their journey so far in the next blog of this series.

Though India is among the top crop-producing countries across the globe, it suffers from lower crop yields. The major reasons behind this are systemic issues and the lack of micronutrients in Indian soil.

This publication explores various natural and human-induced factors that affect the availability of micronutrients in Indian soil and factors that influence the improper use of micronutrients. It also provides policy-level recommendations to boost the government’s efforts to increase agricultural productivity and its aspiration to achieve the Sustainable Development Goal of “Zero Hunger.”

The Government of India undertook various reforms to improve the fertilizer subsidy distribution system, including the introduction of direct benefit transfers. Despite improvements in the distribution of fertilizers, it faces various challenges in the implementation of direct cash transfers (DCT) in fertilizers. This publication highlights these challenges and provides an approach for the government to resolve the barriers in a planned, stepwise manner before the national rollout of DCT in fertilizers.

The publication discusses lessons and insights from MSC’s comprehensive evaluation studies on major LPG subsidy programs including PAHAL (DBTL) and PMUY. It summarizes India’s reforms to streamline, digitize, and transform cooking gas subsidy from an in-kind to a cash transfer program. The publication also highlights key lessons for policymakers to reduce the government’s subsidy burden. It builds on the G2P digitization framework and expands on the importance of institutional and ecosystem readiness and the usage journey of recipients for successful reforms.

The COVID-19 pandemic has posed unprecedented challenges for governments and citizens around the world, straining health systems, economies and the very social fabric of nations. The risk associated with this crisis is especially high for those with limited access to resources due to their gender, geography, age and ethnicity.

Women comprise an overwhelming majority in this segment. Emerging evidence suggests that the pandemic is imposing a disproportionately higher socio-economic cost on women. As Melinda Gates, gender equality advocate and co-chair of the Bill & Melinda Gates Foundation put it, “COVID-19 is gender-blind, but not gender-neutral.” In this article, we discuss four potential types of fallout from COVID-19 that will have lasting socio-economic impacts on women in India and other low- and middle-income countries. These are based on multiple studies that MSC conducted between March and July of 2020.

Potential fallout #1: Women are more economically disadvantaged

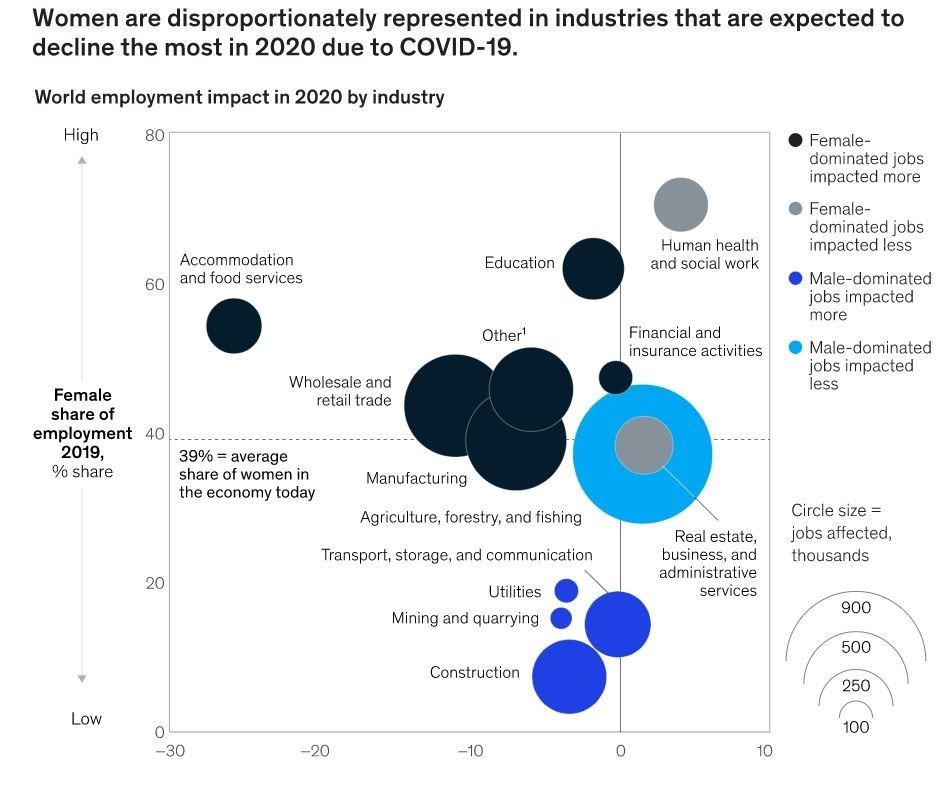

A research note from Citigroup estimates that of the 44 million workers in vulnerable sectors across the globe, 31 million women face potential job cuts, as compared to 13 million men. McKinsey reports that women’s jobs are more vulnerable to this crisis, with the job loss rate for women 1.8 times higher than that of men. Women make up 39% of global employment but account for 54% of overall job losses.

This disproportionate loss of women’s jobs seems to be a worldwide phenomenon. In Britain, mothers are 1.5 times as likely as fathers to have lost or quit their jobs during the lockdown. In the U.S., women accounted for 55% of job losses in April of this year, despite making up less than half of the workforce. This disparity is partly because women are overrepresented in sectors that the crisis has acutely affected, such as hospitality and tourism.

Even before the pandemic, more women than men in India were unemployed. The pandemic has only worsened this situation. MSC’s studies across Bangladesh, India, Indonesia, Kenya and Uganda find that women tend to be more worried about the lack of employment, food shortages and the financial crisis. These differences are particularly acute in India and Uganda. (For more details, please refer to this country-level comparison dashboard).

MSC’s recent research on the impact of the crisis on the low- and middle-income (LMI) segment and micro, small and medium enterprises (MSMEs) confirms that COVID-19 is widening the pre-existing socio-economic gender gap. In India, as many as 82% of women-owned MSMEs reported a decrease in their income, as compared to 72% of male-owned enterprises. Women-owned MSMEs face greater restrictions, decreasing demand, rising costs of inputs, inability to access markets and an increased burden of care work at home, among other factors that severely affect their incomes.

In addition, according to the World Economic Forum’s Global Gender Gap Report 2017, on average, 66% of women’s work in India is unpaid, compared to just 12% of men’s work. Mounting job losses and the economic slowdown will likely raise the household debt delinquency ratio and increase the proportion of women in unpaid work. MSC’s research on the LMI segments confirms that the burden of unpaid work has increased for women by 54% in Asia and 12% in Africa.

Potential fallout #2: COVID-19 will further restrict women’s mobility and increase the information gap on addressing health-related vulnerabilities

Through our studies focused on the LMI segment in Bangladesh, India, Indonesia, Kenya and Uganda, MSC has identified TV and radio as the main sources of information on COVID-19 for both men and women. However, women rely more on their social networks to obtain information on COVID-19, such as neighbors, local shops, friends, relatives and local government extension workers. Only 25% of men rely on their social networks to procure information, as compared to 40% of women.

The pandemic has also further limited women’s mobility, due to the lockdowns announced to curb its spread, limited or no availability of public transport, and stringent social distancing measures. This severely affects not only the lives of individual women but also the functioning of women’s collectives like self-help and joint liability groups. These groups are now unable to hold physical meetings and interactions, which limit women’s access to support systems and networks of information outside their homes.

Potential fallout #3: COVID-19 will suppress women’s voices and rights

Countries across the globe have reported an uptick in intimate partner violence associated with the lockdown. This is alarming, especially in light of data from the National Family Health Survey 2016 that suggests one in three women experience intimate partner violence in their lifetimes. A working paper published by the U.S. National Bureau of Economic Research compiled complaints registered with India’s National Commission for Women. It found an increase in the number of domestic violence complaints in red zone districts — those with strict restrictions on mobility. The average number of monthly complaints in these districts increased from below 1.5 before the lockdown in March to almost two during the lockdown in May. noticed an increase in incidences of domestic violence in their neighborhoods during the lockdown.

Meanwhile, on the global level, the United Nations Population Fund warns that the pandemic could undo almost a third of the progress made against gender-based violence.

Potential fallout #4: Women will be left behind in the race for digital adoption

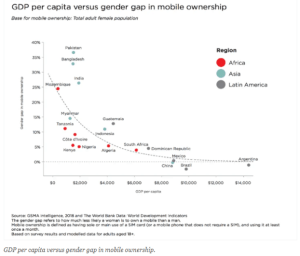

Women generally lose out on access to and adoption of technology, given the persistent digital gender gap. GSMA reports that women in low- and middle-income countries are 8% less likely than men to own a mobile phone and 20% less likely to use mobile internet. A . The gender gap in mobile ownership is particularly large in Bangladesh, India and Uganda. Growing evidence suggests that, for the short-term at least, global smartphone sales are plummeting. The MSC report also points to women’s increased reliance on cash in the current situation. It shows a gender gap in the time spent on phones for any activity, implying reduced scope for women to adopt digital financial services.

MSC’s previous research with garment factory workers in India found extremely low adoption of digital channels among women. Though 36% of female workers have a smartphone, just 3% of them use mobile banking services, compared to 22% of male workers. The trend is similar among other channels, such as mobile wallets and BHIM, India’s mobile payment application. The absence of a strong digital ecosystem is another factor behind this low uptake, as digital channels and products are not designed around the needs of women in this segment.

Several factors already work against women when it comes to the adoption of digital channels. These include reduced mobility, limited or no access to and control of phones, and a relative lack of their own to use during the transaction Additional obstacles include the absence of a strong digital ecosystem, a lack of women-focused products in the market–and more importantly, the fear of losing money in case of a failed transaction. Given these challenges, the prevailing gap in digital adoption may either remain unaltered or grow further during the pandemic.

Several factors already work against women when it comes to the adoption of digital channels. These include reduced mobility, limited or no access to and control of phones, and a relative lack of their own to use during the transaction Additional obstacles include the absence of a strong digital ecosystem, a lack of women-focused products in the market–and more importantly, the fear of losing money in case of a failed transaction. Given these challenges, the prevailing gap in digital adoption may either remain unaltered or grow further during the pandemic.

The signs of this widening gap are already present. MSC’s research with Indian MSMEs highlights that 33% of enterprises have started using social media for communication, while 10% have partnered with e-commerce players to mitigate risks to their businesses. However, these strategies were mainly confined to urban men. The research also indicates that India’s digital divide will further widen the education gap.

In conclusion, a gendered approach to planning for post-crisis recovery and reconstruction will help mitigate the larger-scale consequences of COVID-19 for girls and young women. If women’s unique needs and challenges are neglected, it may lead to greater gender disparity. Practitioners and policymakers both face an important test, as their actions will determine whether women are left behind in the post-COVID-19 world or not. The United Nations Secretary-General, Antonio Guterres has rightly called for the inclusion of women’s needs as part of the strategic response to COVID-19. Policymakers around the world are now responsible for crafting gender-responsive actions, and establishing gender justice and equality as a more prominent part of the mainstream pandemic response. The awareness of gender issues and the prioritization of gender rights and interests can not only get us through this pandemic faster, it can also help us move toward building an equal, inclusive and resilient society after the crisis has passed.

The blog was also published on Next Billion on 1st of October, 2020