Rajesh, a Pune-based manufacturer, watched helplessly as his opportunity to supply critical parts for an order slipped away. Despite his best efforts, he couldn’t get a loan of USD 23,000 (INR 20 lacs) to upgrade his equipment.

With purchase orders in hand, Rajesh approached his bank with confidence. What followed was a labyrinthine process that is familiar to India’s MSME sector. First came the demand for documentation, business registration certificates, three years of financial statements, tax returns, and property documents. Days turned into weeks as bank officials requested more paperwork, such as GST returns, bank statements, project reports, vendor agreements, and compliance certificates, sometimes contradicting earlier requirements. Follow-ups yielded vague responses about “processing timelines.” Meanwhile, his client lost patience and awarded the contract to a competitor with ready capacity.

This scenario repeats daily across India’s MSME landscape, where a significant credit gap persists.

India’s digital revolution, anchored by the JAM Trinity, transformed financial inclusion. The Pradhan Mantri Jan Dhan Yojana added 550 million accounts by April’2025, while UPI processed INR 23.94 trillion across 17.8 billion transactions, connecting 660 banks into its network and revolutionizing digital payments acceptance for small businesses. Despite these achievements, MSMEs face an INR 80 trillion credit gap, with nearly 50% MSME credit demand going unmet. Among 64 million MSMEs, 14% have access to formal credit.

This credit gap stems from structural barriers. Many MSMEs lack comprehensive financial records and don’t have collateral to support the scale of financing they require. The conventional lending process remains characterized by paperwork and waiting periods, particularly for new-to-credit (NTC) borrowers. In contrast, urban enterprises and large corporations secure credit within days through streamlined digital processes and relationship banking, highlighting the disparity in financial access. This gap threatens India’s ambitious economic goals to become the world’s third-largest economy by FY2028.

The primary obstacle lies in fragmented data architecture. Financial institutions, particularly smaller lenders, operate on legacy systems that cannot easily integrate with newer platforms. This creates isolated data pockets, preventing a holistic view of potential borrowers and causing unintentional exclusion. Regional rural banks and cooperatives, the first point of contact for rural borrowers, struggle most with these technological limitations.

Compounding this challenge is the scattered nature of data essential to underwriting loans. Land records remain with state governments, GST data with tax authorities, and banking information within individual institutions. Each data source requires separate integration efforts, creating prohibitive costs for smaller lenders. The consequences are tangible. Loan processing that should take days stretches into weeks as lenders manually collect and verify documents. Small businesses have large opportunity costs when capital isn’t available at critical junctures, leading to the exclusion of “thin-file” and “no-file” borrowers.

Unlike bilateral API banking arrangements or the Account Aggregator frameworks, ULI functions as a centralized technology platform that connects lenders with multiple data sources, whether financial or non-financial, through standardized APIs. This plug-and-play architecture eliminates the need for individual integrations that smaller lenders cannot afford. By consolidating financial data (GST returns, income tax filings) and non-financial information (land records, utility payments) into a unified framework, ULI transforms fragmented data repositories into actionable lending insights. For users, ULI simplifies the borrowing experience. Think of it as the digital equivalent of a marketplace where, instead of comparing different brands of products, borrowers can compare credit offers from multiple financial institutions on a single platform. Users provide basic details and financing requirements, and ULI instantly displays tailored credit options, with details on approved amounts, interest rates, and tenure. Borrowers can select the most suitable offer based on their preferences and receive funds directly into their accounts. This eliminates multiple bank visits, downloading numerous apps, or managing stacks of paperwork, transforming a weeks-long process into a streamlined digital experience.

Its key strength lies in the ability to automate documentation processes. Through digital verification channels including eKYC, and eSign capabilities, ULI can reduce loan processing times from weeks to hours. This efficiency addresses the opportunity costs that borrowers face when capital isn’t available at critical business junctures. ULI enables alternative credit assessment by incorporating diverse data points beyond traditional banking records.

The platform’s interoperability with other DPIs, like the Open Credit Enablement Network and Open Network for Digital Commerce, creates a more robust ecosystem for credit delivery. Smaller lending institutions gain access to sophisticated credit assessment tools previously available only to larger banks. Borrowers receive faster credit decisions based on more comprehensive data. As ULI evolves, its potential to close India’s credit gap will be essential to achieving the country’s economic growth targets and ensuring inclusive financial development.

India’s digital highways are built. Now, we must connect them so that no potential borrower is excluded. By bridging our data silos and streamlining credit access, we can unlock the true potential of India’s entrepreneurial spirit and ensure that our digital revolution truly serves all.

The oped was first published on Hindustan Times on 4th July, 2025

Ade, a 23-year-old woman with visual impairments from Indonesia, has been struggling to replace her expired debit card at a bank branch. The bank has no Braille documents and lacks procedures to support independent access for people with disabilities (PwDs). The bank staff asks her to come back to the bank with someone she trusts, which she finds difficult. Instead of adequately accommodating or addressing the accessibility gap, the banks fail to include PwDs like her in the financial system.

In this blog, we explore how the intersection of disability and poverty creates layered barriers to financial inclusion. It draws on field insights from a disability inclusion study conducted by MicroSave Consulting (MSC), in collaboration with Opportunity International Australia (OIA). The study was a joint initiative funded by the Department of Foreign Affairs and Trade (DFAT) and the Australian NGO Cooperation Program (ANCP).

How do non-inclusive services drive dependency?

Non-inclusive services present a significant barrier for PwDs who attempt to access financial products and services. Most financial institutions have failed to meet their needs around communication, physical, or digital access. As a result, basic activities, such as opening an account or replacing a card, require aid from family or friends. The story of 23-year-old Ade tells the challenges PwDs face in financial inclusion. Eventually, she had to reapply for an expired debit card and now avoids going to the bank altogether.

Often, PwDs are afterthoughts in Indonesia’s financial inclusion system, even when they make up 1.4 % of Indonesia’s population, or around 4 million people. Whether it is access to simple financial services, regular usage, or the quality of financial services, PwDs face persistent exclusion. Only 24.3% of PwDs in Indonesia have a bank account, compared to 47% of those without disabilities. Usage of digital financial services is even lower for PwDs, as only 1.1% of them have used the Internet to access financial services.

Such exclusion has a direct correlation to income disparities, as 55% of PwDs belong to low-income backgrounds. In Indonesia, they earn an average of just IDR 1.3 million (~USD 80.25) per month, and 69% work in the informal sector. The vulnerabilities PwDs face increase during times of crisis. As an example, during the COVID-19 pandemic, about 41% were classified as vulnerable to falling deeper into poverty. A 30-80% income drop was identified compared to their pre-pandemic incomes, below IDR 1 million (~USD 61.73).

How are digital finance services not yet universally inclusive?

While digital financial services may have reduced Ade’s visits to physical bank branches, such services are not inclusively designed. She faces other barriers when she tries to complete the electronic know your customer (e-KYC) process. The live detection feature, which requires users to move their head in specific directions or blink on command, was difficult for her due to her visual impairment. She had to repeat the process multiple times before she completed it.

People with intellectual disabilities or low literacy levels face even greater barriers when they use digital financial services. Complex steps like e-KYC can be confusing without simple instructions, clear language, or intuitive navigation. Features, such as voice guides, screen readers, or alt text for buttons, can make these services more accessible for people with disabilities.

Limited education and communication create dependency

Access to financial services is even more difficult for people with disabilities from low-income backgrounds, many of whom have had limited educational opportunities. They are often never enrolled in special education programs, where they could have learned sign language or Braille. This limits how well they can interact with formal systems or navigate them.

The challenges are even more acute for individuals who developed disabilities later in life due to aging. While age-related impairments are common across income levels, older adults from low-income households face greater barriers. With limited education, they struggle to adapt to new conditions or learn assistive tools and systems that would help them access financial services. As a result, many low-income PwDs, especially older adults, often must rely on others when using financial services.

In Bogor Regency, Macih, a 64-year-old homemaker with visual impairments, participates in a group lending arrangement provided by a formal microfinance institution (MFIs). Based on the Grameen model, small groups of women meet weekly at a member’s home. During these meetings, a field officer facilitates savings deposits, withdrawals, loan applications, and repayments. Macih relies on her husband to manage the paperwork involved in financial transactions. He reads the documents to her and helps her sign them, as she had completed only elementary school and never had the opportunity to learn Braille.

Another participant in the same lending group arrangement is 66-year-old Iroh, an agricultural worker who relies on others for support. Her hearing impairment developed due to old age, and she never learned Bisindo, the Indonesian sign language. She sees little point in doing so now, as no one around her uses it. She struggles to learn at her age and relies on a fellow group member to communicate with the field officer.

Assistive tools fail to be prioritized, especially for women

Access to assistive tools, such as hearing aids, walking sticks, or wheelchairs, is also a challenge for many low-income PwDs. These tools are often too expensive, and when daily survival is at stake, they are not prioritized. This especially applies to women, who put family needs above their own.

Hana, a 56-year-old nasi uduk seller, has had difficulty walking since childhood. In recent years, she has only received a prosthetic leg through a government aid program. When asked if she would have taken a loan to buy it, she shared that she preferred to support her small business and daily needs. However, day-to-day life stays difficult without such tools, which include seemingly simple tasks, such as a visit to an ATM.

Low earnings keep formal finance out of reach

Around 69% of PwDs are engaged in the informal sector and earn just enough to meet daily needs. As a result, financial products that may seem affordable to non-disabled people can still be out of reach for low-income people with disabilities. For instance, opening or maintaining a savings account is difficult, as it typically requires a minimum of IDR 20,000 to open and IDR 10,000 (~ USD 1.23 to ~ USD 0.61) to deposit. For these people, formal financial services can be entirely inaccessible when combined with transportation costs, physical effort, and the fear of being turned away or needing assistance.

The way forward

The layered challenges that PwDs face when they seek access to financial services make the design of inclusive financial products more complex. Inclusive solutions must be genuinely expanded, not merely provided as a formality. They must address the real barriers that PwDs, especially those from low-income backgrounds, face every day.

Assistive technologies should be easy to use and accessible to low-income users with disabilities. They should be included early in the design of products and services so their real needs align with what is offered. In the long term, efforts should expand affordable access to tools and training that help people with disabilities use financial services independently.

At its core, financial inclusion is to ensure everyone can access and use financial products and services. PwDs, especially those from low-income communities, have been left out of the financial inclusion landscape for too long. To fully achieve true financial inclusion, the layered challenges they face must be recognized and responded to. Only then can financial products and services become truly inclusive for all.

This article was first published on Inside Indonesia platform on August 1st, 2025

This report dives deep into the overlooked potential and pressing challenges of Indonesia’s blue food economy. With the world’s second-longest coastline and millions relying on fish for food and income, blue food is not just an economic opportunity, but a lifeline.

By spotlighting small-scale fisheries, aquaculture, and the often invisible role of women, the report unpacks the structural gaps holding the sector back from limited market access to climate vulnerability and food loss. It lays out six critical pillars nutrition, environment, justice, productivity, value creation, and waste to understand what’s broken and how to fix it.

Through community voices, field research, and policy insights, the report calls for urgent action: smarter investments, inclusive policies, and stronger support for local actors. The goal? A thriving blue food economy that feeds, empowers, and sustains fairly and sustainably.

“Street foods have traditionally been an integral part of Indian society… They represent the rich local traditional cuisines,” notes a government release. From the chaat stalls of Delhi to the idli vendors of Chennai, street food plays an integral role in India’s urban food environment. It provides convenient, low-cost meals to millions of people and serves as a primary source of income for a significant share of the country’s informal workforce—estimated at around 10 million street vendors and about INR 8000 crore (USD 960 million) daily. The affordability and accessibility of street food make it a daily reliance for working-class consumers, especially those in urban areas with limited time, income, or kitchen access.

Street vendors also have the potential to support nutrition security, particularly when fresh produce or traditional recipes are used. Seasonal offerings—such as sprouted moong salads, roasted peanuts, or fruit carts—can provide essential micronutrients. This potential is often undermined when vendors prioritise cost-cutting over quality, using substandard or adulterated ingredients.

The sector is also associated with environmental and climate-related challenges. The widespread use of single-use plastics, unsafe food packaging, and poor waste disposal practices contributes to urban pollution and environmental degradation.

Another challenge is that while the government has made significant strides in recognizing street food vendors the sector is still largely informal, under-regulated, and often disconnected from food business policy ecosystem. Until recently, most policy conversations for street food have centered around hygiene and food safety in the context of foodborne illness, an equally important challenge emerging is: the poor nutritional quality of most of India’s street food. Vendors often use substandard or adulterated ingredients, reused oils, and nutrient-poor recipes. These practices expose consumers to long-term health risks, including diet-related non-communicable diseases, and undermine efforts toward ensuring nutrition security in urban India.

The evolving challenge: from food safety to nutrition security

Nutrition security goes beyond ensuring food is safe from contamination—it requires that food is also nutrient-dense and dietarily adequate. While affordable and filling, many street foods lack the required nutrition. A large proportion of street foods fall into the high-fat, sugar, and salt (HFSS) category made with refined flour, reused cooking oils, and added sugars are calorie-dense but offer limited amounts of essential nutrients such as high-quality protein, dietary fibre, vitamins, and minerals.

This pattern of consumption contributes to the dual burden of malnutrition—with undernutrition persisting in the form of micronutrient deficiencies (“hidden hunger”), alongside a growing incidence of non-communicable diseases such as obesity, type 2 diabetes, and hypertension. These risks are particularly pronounced in urban areas where dietary diversity is constrained by affordability and access.

While food safety efforts have made headway in addressing hygiene and microbial contamination, the nutritional risks associated with low-quality ingredients and poor formulations remain inadequately addressed. The continued reliance on adulterated inputs, excessive frying, and nutritionally imbalanced preparations compromises the safety and the dietary value of meals widely consumed in India’s urban food environments. Addressing these issues is essential to making street food a reliable part of India’s nutrition security landscape.

Vendor realities: barriers to safer, nutritious street food

While the discussed issues underscore the persistent risks associated with street food, they also reflect the economic and operational realities faced by vendors. To sustain their livelihoods, many vendors prioritise low-cost preparation and mass appeal, often at the expense of food quality and nutrition.

Improving food safety and nutrition in this sector requires more than regulation—it demands a grounded understanding of vendors’ day-to-day constraints. Most operate with minimal infrastructure, limited access to clean water, refrigeration, or waste management, and little formal training in food safety or nutrition. Financial limitations often lead to the use of low-quality or adulterated ingredients, reused oils, plastic packaging, and unsafe storage practices. These challenges are further compounded by long working hours, exposure to heat stress, and growing climate-related vulnerabilities, all of which affect both vendor well-being and the consistency of food safety practices.

Government efforts and public initiatives

The Government of India has taken important steps to address both demand- and supply-side challenges in the informal food sector, with a particular focus on food safety. Through the Food Safety and Standards Authority of India (FSSAI), several key initiatives over the past five years have aimed to formalise, regulate, and build the capacities of street vendors—with an emphasis on improving hygiene and quality standards and promoting safer food handling practices across urban settings.

FSSAI’s Clean Street Food Hub initiative aims to certify clusters of 50 or more vendors based on hygiene, sanitation, infrastructure, and food handling practices. The initiative is a collaboration of the Ministry of Health and, the Ministry of Housing and Urban affairs, underscoring the commitment of the government to recognize the value of safe street foods. Iconic street food markets in some cities such as Kankariya in Ahmedabad, Chappan Dukaan in Indore, Girgaon Chowpatty in Mumbai, etc. have already received this certification after undergoing structured improvements, including infrastructure upgrades, vendor training, and third-party audits. These hubs demonstrate that street food can be both affordable and safe, provided adequate support and oversight are in place.

The broader Eat Right India campaign promotes safe, healthy, and sustainable diets and includes street food vendors as a key constituency. Through the Food Safety Training and Certification (FoSTaC) programme, vendors are being trained in safe food handling, personal hygiene, and basic nutrition. FSSAI has worked with municipal corporations in many cities to make training and certification mandatory for vendor registration, using incentives such as visibility, branding, and inclusion in government-supported vendor lists.

Recognizing the risks of reused cooking oil, FSSAI introduced the Repurpose Used Cooking Oil (RUCO) framework, which sets limits for total polar compounds (TPC) in frying oils and promotes the collection of used oil for biodiesel conversion. Total Polar Compounds are formed on repeated frying. The toxicity of these compounds is associated with several diseases such as hypertension, atherosclerosis, Alzheimer’s disease, liver diseases. While initially targeted at larger food businesses, the initiative has encouraged public dialogue on safe oil use and has been piloted in some municipal vendor clusters through awareness drives and mobile testing labs.

4) Credit, registration, and infrastructure through convergence

While public initiatives have laid the foundation, there is a significant opportunity for the private sector—particularly food manufacturers, ingredient suppliers, and digital platforms—to fill existing gaps and co-create solutions.

1. Improving access to quality ingredients:

Private sector actors—particularly food manufacturers, distributors, and aggregators—can play a critical role in improving the quality of inputs used by street vendors. This includes:

Stable, low-trans-fat oils packaged in smaller quantities for daily use

Verified dairy products, such as milk and paneer, sourced from regulated suppliers

Fortified ingredients, like iodised salt, iron-rich flours, or spice blends with added micronutrients

Bulk procurement models, vendor cooperatives, or branded supply chains targeting street food clusters could make these products more accessible. This could be tied to incentive schemes where vendors who use verified products are eligible for recognition or partnerships.

2. Vendor training and certification partnerships:

Food companies and CSR programmes have demonstrated that hygiene and food safety training can be scaled through private engagement. Examples include Nestlé India’s collaboration with NASVI and Swiggy’s onboarding of street vendors under the PM SVANidhi scheme. These efforts can be expanded to include nutrition modules, with simple guidance on using fresh ingredients, reducing oil reuse, adding vegetables, and reformulating popular items.

Private labs and startups can also provide low-cost food testing services, mobile diagnostics for oil degradation, and self-certification toolkits, enabling vendors to monitor their practices in real time.

3. Enhancing consumer trust and market linkages

Food delivery platforms, e-commerce apps, and local food discovery tools can support transparent vendor listings, hygiene scores, and traceability for consumers. Vendors meeting safety and nutrition criteria can be promoted through these platforms, creating market-based incentives for quality improvements.

Private players in food processing and logistics can partner with municipalities to develop shared kitchen infrastructure, cold chains, or clean cooking carts, helping bridge the infrastructure deficit that currently constrains street food safety.

Future direction and recommendations

To align India’s street food ecosystem more closely with public health and nutrition priorities, future interventions must move beyond hygiene compliance and explicitly address food quality, dietary adequacy, and vendor viability. This shift requires a balanced approach—one that protects consumer health while supporting vendors as key actors in the food system. The following areas offer actionable pathways to reframe street food safety through a nutrition-sensitive lens:

Integrate nutrition into food safety standards: FSSAI and state food authorities can incorporate nutritional benchmarks—such as limits on reused oil, inclusion of fortified ingredients, or minimum vegetable content—within vendor certification frameworks. This will help shift attention from contamination control alone to overall food quality.

Leverage PM SVANidhi and urban missions for food quality: Existing schemes supporting vendor credit, registration, and formalisation can be expanded to include nutrition training, input linkages, and quality assurance. This creates an integrated model where street vendors receive support not just to operate, but to improve the quality of their offerings.

Invest in vendor-centric digital tools: Mobile applications and simple tech solutions can offer vendors access to training modules, hygiene checklists, safe recipe guides, and supplier directories in local languages. These tools can help vendors make informed choices without incurring additional costs or regulatory burdens.

Protect vendors from external vulnerabilities: Interventions must account for heat stress, climate variability, and financial shocks that affect vendor livelihoods. Support measures—such as shaded carts, hydration points, health insurance linkages, and climate-resilient infrastructure—should be part of nutrition-sensitive urban planning.

Create a healthy street food certification or label: A voluntary nutrition-positive vendor recognition scheme, tied to improved recipes, verified sourcing, and responsible cooking practices, can help vendors differentiate themselves and attract more health-conscious consumers.

Raise consumer awareness and drive demand: Public campaigns can increase understanding of nutritional risks in commonly consumed street foods, while encouraging demand for safer and healthier alternatives. Consumer behaviour plays a powerful role in shaping vendor practices—greater awareness can accelerate the shift toward nutritious street food.

Conclusion

India’s efforts to improve street food safety through regulation, training, and infrastructure have laid critical groundwork. However, the focus must now expand to nutrition security, for these interventions to translate into long-term public health gains. Street food will remain a vital part of the urban food ecosystem, especially for low-income consumers. Ensuring that it contributes positively to diets—not just in taste and satiety, but also in nutritional value—requires aligning the interests of vendors, regulators, consumers, and private actors.

By working together to improve inputs, reformulate recipes, and create incentives for quality, stakeholders can transform India’s street food sector into a safe, nutritious, and trusted source of urban nourishment.

This blog was first published on the NUFFOODS Spectrum platform on 2nd June 2025.

Rahim runs a busy tea stall in Singair Upazila, Bangladesh. Every day, he serves steaming cups of cha to a steady stream of customers. Business is good, but cash payments are a headache. Customers get frustrated when he lacks change. Some walk away when he offers toffees instead of small change. By the end of the day, Rahim struggles to track his sales, and he wonders—is there a better way?

Rahim is not alone. In Bangladesh, 80% of transactions occur in cash, which creates inefficiencies and stalls business growth. The Bangladesh Bank introduced Bangla QR to reduce the burden of cash payments. Bangla QR is a universal QR-based payment system designed to simplify transactions and boost financial inclusion. Yet, cash remains king. What is stopping the shift?

Our research in Bangladesh reveals a critical gap: Local bank branch officials lack the necessary technology, skills, and insights to support digital payment processes. When merchants face challenges, they turn to these branches for help. However, branch officials often cannot assist them. As a result, merchants must seek support from the head office, frequently located far away, which leads to frustration and delays.

This lack of on-ground support erodes merchants’ trust in the banking system and discourages small merchants from adopting digital payments. At the same time, bank staff—who feel unprepared to address these issues—are less likely to promote solutions, such as Bangla QR. Ultimately, this weakens efforts to expand digital payment adoption.

Understanding Bangla QR-based digital payments

QR codes provide a contactless and efficient way for people to pay. They help bridge the gap between traditional banking and digital financial services. The integration with the National Payment Switch makes transactions seamless and allows users to pay easily across multiple platforms.

In Bangladesh, Bangla QR is a key example of this technology in action. It improves transaction efficiency and ensures security for users. Encrypted transactions protect sensitive data and build trust among merchants and consumers. Bangla QR is also cost-effective. It offers lower merchant discount rates (MDR) of 0.5% through bank apps and 0.8% through mobile financial services (MFS) wallets, which makes it more affordable than other DFS payment systems. This makes it a practical choice for small merchants who seek to accept digital payments.

When it comes to QR, local bank branches are in a bind

Our discussions with banks revealed that no local bank staff had the necessary technical knowledge about QR-based digital payments or the merchant onboarding process. Furthermore, they lacked access to the digital payment platform and its data, which limited their ability to assist merchants effectively. As trusted points of contact for local customers and merchants alike, these officials highlighted that the promotion of QR-based digital payments would be futile if customer grievances were not resolved effectively first.

Without proper grievance management, customers may lose faith in the system, which would lead to a decline in digital payments’ adoption. Bank officers believe that access to customer and merchant-related data related to QR-based transactions will revolutionize how effectively they can support customers and merchants. However, the officials highlight another challenge—budgetary and staffing limitations—due to which they struggle to onboard QR merchants and promote digital payments.

Adoption challenges trickle down from branches to merchants

As per MSC’s research in Singair, 64% of retail traders do not understand the value proposition and use cases of QR-based digital payments. This compels them to seek answers at bank branches, which delays adoption. Delays in fund settlements and variations in MDR across providers deter their uptake of QR payments. Bank branches also lack the infrastructure to support these transactions and provide customer support. Bank officials lack knowledge about QR-based payment systems and cannot resolve customer grievances, which erodes customer trust. Concerns over security and fraud are also significant barriers to broader adoption.

How can banks strengthen branch capacity to support local merchants with digital payments?

Banks can cover significant ground with these five easy solutions.

Comprehensive training for local bank staff on digital payments and customer support is essential. Banks can develop standardized training modules for the branches to ensure consistent merchant onboarding. This module should also be available to new or transferred bank officials to ensure smooth integration.

Streamlining merchant onboarding through digital means, such as personal retail accounts, can reduce the administrative burden and speed up merchant acquisition.

A standard operating procedure designed by a regulator or the central management of respective banks can also streamline the QR merchants’ onboarding process.

Banks can develop a dashboard to provide their branches with access to transaction data. Bank officers could resolve customer grievances at the local level with this tool. It would enhance trust and confidence in digital payments. Additionally, banks can provide incentives to local bank officials based on the number of QR merchants they onboard.

Finally, banks can increase funds to promote digital payments. Digitization can help the bottom-line of banks in the long term. For example, Kotak Mahindra Bank doubled its customer base in India from 8 million to 16 million after it launched its fully digital banking service, Kotak 811. The way ahead

Local banks must be empowered to accelerate the adoption of QR-based payments in Bangladesh. These branches are the first point of contact for merchants and customers. Their capacity must be strengthened through training, simplified and streamlined processes, and better access to transaction data. This can help rebuild trust, resolve grievances, and encourage the widespread use of Bangla QR.

The shift to a stronger digital payment system can benefit merchants and consumers alike to enable Bangladesh’s progress toward an inclusive digital economy. Only then would millions of microentrepreneurs, just like Rahim, serve up many more cups of refreshing ‘cha’ to his customers and, in the process, chart a better future for themselves and their families.

This op-ed was first published on The Daily Moon on 23rd February 2025

Millions of women across India rely on loans from microfinance institutions (MFIs) to support their livelihoods, manage small businesses, and fund essential household needs. While most MFIs have digitized loan disbursements, the vast majority of repayments—nearly 87% as of FY 2021-22—still occur in cash. This reliance on cash makes borrowers’ lives difficult every day.

Take Reena, for example. A factory worker in Bengal, Reena must carve time out of her hectic schedule to withdraw her banked salary to pay her loan for house repairs. Grocery store owner Seema’s story has a similar ring. Hailing from a small village in Bihar, Seema has an irregular income and often relies on her husband for financial support. However, even if she wishes to access her loan repayment details to update him, Seema must first deal with a cumbersome offline process.

Meanwhile, in the southern state of Kerala, fish vendor Asha uses a basic phone. She constantly worries about carrying cash to repay her business loan, which remains a common challenge among borrowers who lack access to digital EMI payments.

Across India, more than 83 million MFI borrowers have a similar story to tell. Despite the clear advantages of digital transactions and the efforts of MFIs to introduce solutions, the shift away from cash repayments is yet to pick up pace.

Several factors contribute to the persistence of cash. Many digital solutions fail to align with the varying technical capabilities and trust levels of a diverse borrower base. Additionally, several borrowers use basic phones or are new to digital platforms, which causes a potential mismatch between the borrowers’ requirements and the solutions’ design. Moreover, the integration of digital payment systems with the MFIs’ existing loan management infrastructure has proved . It involves multiple stakeholders, incompatible software that hinders easy integration across players, and high costs. It calls for substantial technical investment and efforts to achieve a suitable technology fit for the MFI’s systems.

The combination of such issues explains why borrowers continue to rely on traditional cash collections. Existing digital payment options frequently do not suit them. If MFIs wish to scale up digital payments, they must offer customized solutions that consider borrowers’ preferences, levels of digital readiness, and awareness.

The Microfinance Industry Network (MFIN) recognized these challenges alongside the need for tailored approaches and partnered with MSC in 2022. This partnership sought to address the barriers to the adoption of digital repayment solutions and digitize repayments at scale. As part of this initiative, MSC conducted an in-depth study with nine partner MFIs of the MFIN. The study sought to identify tailored digital repayment solutions aligned with each institution’s capabilities and their borrowers’ specific needs.

The study revealed critical insights. While smartphone ownership and internet connectivity are on the rise, borrowers’ ability and willingness to repay digitally vary widely based on awareness, skills, and comfort with technology. Although most borrowers know about digital methods, many lack the literacy to use them independently. Only 24% of borrowers reported using their phones for payments. Even those who use digital payments elsewhere strongly prefer cash. Safety concerns also further discourage borrowers with limited digital exposure.

MSC designed a framework to overcome these barriers that accounts for MFI readiness, cost implications, borrower access, ease of use, and safety. Based on this framework, we recommended tailored solutions and emphasized multitier training programs for MFI staff and borrowers. We share key insights from the study and highlight the solutions implemented across partner MFIs.

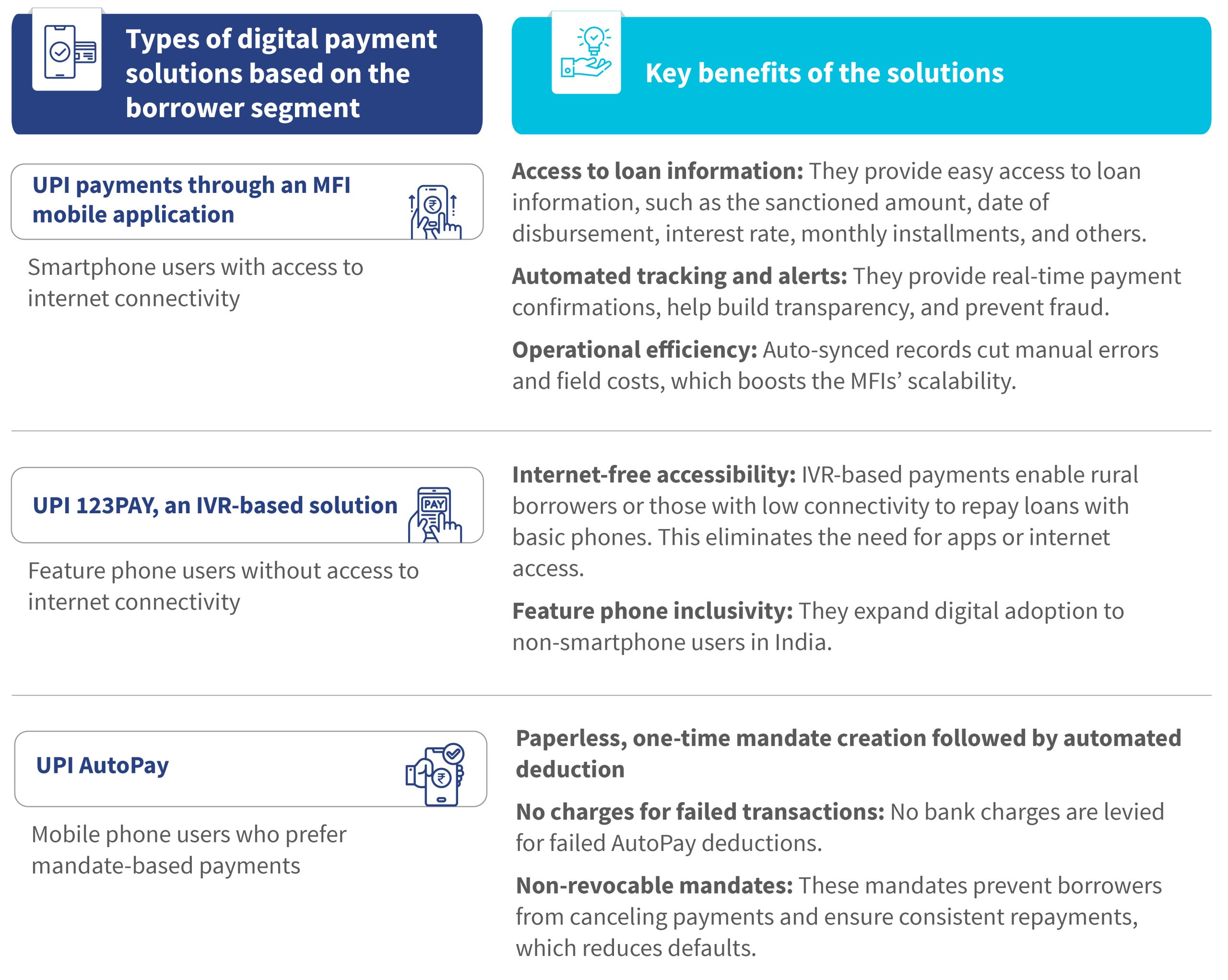

Based on the assessment and framework, the project focused on implementing key digital payment solutions tailored to borrowers’ varying needs. The partner MFIs implemented three leading solutions:

UPI payments via MFI mobile applications:Research showed that borrowers trust mobile apps developed by their own MFI. The MFIN sought to meet this preference and engaged FinTech partners to create customized mobile applications for each participating MFI.

UPI 123PAY IVR-based solution:MFIN recognized that 34% of borrowers use feature phones. It introduced a dedicated IVR number for each institution and integrated it with the MFI system to allow borrowers to repay digitally without a smartphone.

UPI AutoPay:Targeted to borrowers who seek convenience, this option allows automatic, recurring EMI deductions without manual initiation or PIN entry each time.

Such tailored solutions directly addressed the challenges of borrowers like Reena, Seema, and Asha. Thanks to UPI AutoPay, Reena no longer needs to take time off work to withdraw cash. Her EMI is automatically deducted from her savings bank account, which has freed up valuable time and effort. Seema benefited from the MFI’s mobile application, which gave her easy access to up-to-date loan repayment information. This allowed her husband to conveniently view her loan account details on the app and digitally pay the EMI as per the schedule. Meanwhile, basic phone user Asha used UPI 123PAY as a safe and accessible way to pay her loan installments digitally, which eliminated the risks associated with carrying cash for repayments.

The initiatives introduced through this project showed notable results. Digital repayments increased to 30% of all repayments across the pilot branches. Beyond individual impact, the adoption of digital payments streamlined MFIs’ collection processes as well, which freed up staff’s time and resources for loan sourcing and other services.

Such operational improvements are especially valuable given the way MFIs structure their lending. Typically, MFIs rely on joint liability groups—small groups of female borrowers who come together to access loans and support each other’s repayment efforts. These groups promote financial discipline, mutual accountability, and social support to help women build credit histories and strengthen their economic resilience.

Center meetings, which are regular gatherings of these groups, have shifted their focus away from cash transactions to build awareness and encourage the use of additional financial services. Digital repayments also create a transparent transaction history to benefit borrowers. They help borrowers track finances, demonstrate repayment capacity, and potentially uncover greater financial opportunities.

This initiative’s success offers several key lessons for the microfinance sector:

Custom solutions drive adoption: Digital tools tailored to MFI operations and local context lead to higher adoption.

Integration with existing systems is essential: Solutions are most effective when they fit seamlessly into staff routines and technology infrastructure, build trust, and save time.

Collaboration is vital to encourage digital adoption: Since the initial demand from borrowers may be low, MFIs must proactively build awareness among both staff and borrowers. A collaborative approach nurtures sustainable adoption.

While India’s microfinance sector moves toward digitization, the experiences of borrowers, such as Reena, Seema, and Asha, shine a harsh spotlight on the persistent challenges they face as they try to break free from their dependency on cash for repayments. While this project shows that tailored approaches and focused training can boost adoption, gaps in digital readiness remain a major barrier.

If MFIs are to overcome this hurdle, they must urgently prioritize the development of user-friendly and seamlessly integrated digital repayment tools. Stakeholders must invest substantially to build the digital capacity of staff and clients. Meanwhile, MFIs, FinTech partners, and policymakers must take intense collaborative action to address fundamental infrastructure and literacy barriers and ensure digital systems are both accessible and secure.

Only evidence-based, collective effort will allow the sector to revolutionize repayment processes, deepen financial inclusion, and unlock greater opportunities for the countless Reenas, Seemas, and Ashas across India. We look forward to sharing deeper insights from our ongoing engagement with MFIN to digitize MFI repayments. Watch this space for more details on our lessons and impact as the work progresses.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.