This white paper outlines a strategic roadmap for advancing bancassurance as a scalable and inclusive insurance distribution model in Bangladesh. It highlights the regulatory, institutional, and technological enablers needed to strengthen consumer trust, drive innovation, and expand outreach, particularly in rural and underserved areas. The paper also emphasizes the role of bancassurance in building climate resilience through digital delivery, parametric products, and ecosystem collaboration, and outlines actionable pathways for regulators, banks, and insurers. It also showcases MSC’s role in providing policy support, product innovation, and capacity building to create an equitable, climate- smart insurance ecosystem

Unlocking financial resilience: How MFIs can solve the climate disaster in Bangladesh’s farm economy

Around 60 million smallholder farmers produce nearly 60% of Bangladesh’s food. However, most lack adequate tools to adapt to the dangerous risks climate change brings. Every year, these farmers face threats, such as floods, droughts, cyclones, salinity intrusion, river erosion, and pest outbreaks. The scale and frequency of these disasters continue to grow, with deadly results.

In 2024, monsoon floods destroyed 1.1 million metric tons of rice, while Cyclone Remal damaged crops across 50 districts, and a record-breaking April heatwave scorched rice and fruit harvests. In coastal Khulna, salinity intrusion and drought wiped out more than 18,800 hectares of paddy and vegetables. In November 2023, Cyclone Midhili flooded farmlands and affected more than 160,000 farmers. For families who already live on the edge, one bad season can push them back into poverty. This forces them to make painful trade-offs between food, education, and healthcare.

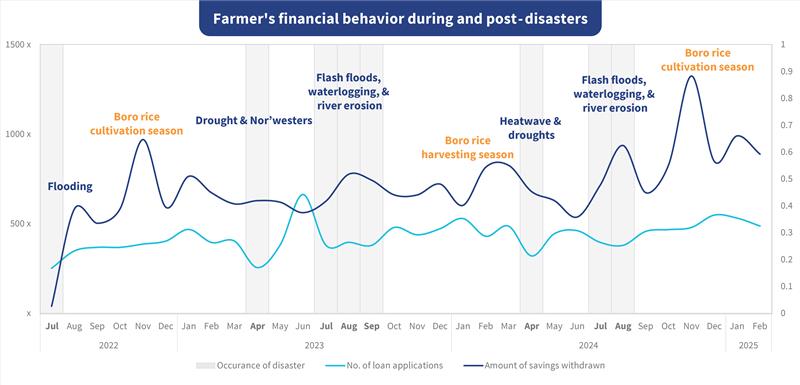

MSC recently conducted a study on agri-allied customers in some of Bangladesh’s most climate-vulnerable regions. We found that when a climate shock hits, farmers react with urgency. They withdraw any savings or sell off assets to buy food, repair homes, replace lost livestock, and cover other important expenses. The need for capital surges once the immediate crisis has passed, as farmers must replant crops, rebuild structures, and replace equipment. This drives up the demand for loans. However, they hesitate to take on new debt as income sources become uncertain. MSC’s primary study also reveals a similar trend, as shown in the graph.

In these moments of urgency, farmers resort to System 1 Thinking, which is hasty, instinctive, and often desperate. Many smallholder farmers borrow from multiple sources and must sometimes turn to informal moneylenders who charge steep interest rates. What starts as survival borrowing can spiral into a vicious debt cycle, as they scramble to repay one loan by taking on more debt that eats into their already fragile incomes. Their lives are so precarious that a single failed farming season can trap a household in chronic financial distress without any safety net.

Credit and savings have expanded significantly in rural Bangladesh due to microfinance institutions (MFIs). However, these tools alone are not enough during and after climate disasters. This is where products, such as asset-based microinsurance, can cushion when disaster strikes. Unfortunately, insurance coverage in rural Bangladesh remains negligible. Less than approximately 1% of older farmers have any form of comprehensive agricultural insurance.

Farmers often view insurance with suspicion. Many hear stories of delayed payouts, unclear policy terms, or agents who disappear after they collect premiums. Others consider insurance a bad omen. Insurers have limited rural reach on the supply side. They have a thin distribution channel and slow administrative processes. The insurers are less digitally connected and do not understand claim mechanisms well. The result is a trust gap, and farmers who could benefit the most from insurance are the least likely to buy it.

From the insurers’ perspective, rural markets are hard to reach profitably. Yet, if they partner with MFIs, they can unlock high-volume, low-cost distribution. MFIs already have the network, client trust, and collection systems in place that can lower acquisition costs and improve premium collection rates.

For decades, MFIs have built deep, trusted relationships with rural clients. Farmers see MFI staff regularly to disburse loans, collect them, and for financial advice and support. This trust and accessibility give MFIs an advantage most insurers lack. MFIs can embed microinsurance into current loans or savings products and make them easy to adopt. They can collect premiums and loan instalments at the same time, which would remove the need for separate payments and reduce administrative hurdles. MFI staff can act as facilitators between farmers and the insurers when claims are needed by the farmers. This would help farmers file claims and ensure timely and transparent payouts.

From the insurers’ perspective, rural markets are hard to reach profitably. Insurers can partner with MFIs to unlock high-volume and low-cost distribution. MFIs already have the network, client trust, and collection systems that lower acquisition costs and improve premium collection rates. A partnership between MFIs and insurers can go beyond social impact and serve as a business opportunity for insurers. Therefore, insurers can work with MFIs to expand their customer base, diversify risk pools, and build long-term revenue streams from millions of small but consistent premiums.

Globally, MFI–insurer partnerships have proven effective. In the Philippines, the microinsurance mutual benefit associations (Mi-MBAs) bundle insurance with microloans, which insure more than a million clients. In Indonesia, PasarPolis partners with MFIs and digital platforms to sell affordable, simple insurance products alongside everyday transactions. In India, VimoSEWA combines insurance with social protection and livelihood support for women in the informal sector.

Bangladesh has started to see similar innovations. The Bangladesh Rural Advancement Committee (BRAC) has partnered with the Syngenta Foundation, the Green Delta Insurance Company, and the Sadharan Bima Corporation to offer crop insurance to its clients. MSC’s research revealed that when products are simple, affordable, and trusted, farmers are willing to pay the extra premium for their peace of mind. However, the scale remains small, and broader adoption requires MFIs to innovate products, simplify claims, and engage strongly with communities.

In recent years, climate risks have only intensified, while the gap between farmers’ needs and the tools available to manage those risks has widened. MFIs can uniquely bridge that gap to complete the financial protection package with embedded microinsurance alongside credit and savings. For farmers, this financial protection package means the difference between a fresh start after a disaster or years of debt. For MFIs, it can protect loan portfolios and strengthen client relationships. For insurers, it provides a way to access a profitable, underserved rural market at scale. Ultimately, this creates mutual benefits for all the involved stakeholders.

Microinsurance is the missing link in rural financial resilience that can emerge as the gateway to a transformative future for smallholder farmers. When we empower MFIs to deliver microinsurance, we can transform lived experiences from survival toward inclusivity and planned empowerment. It is time to equip Bangladesh’s farmers in Bangladesh with the tools they need to withstand and recover from climate disasters.

Microfinance for Climate Resilience- Voices from the Field

Design that works: The Mi4iD approach

We developed Mi4iD—our proprietary, multidisciplinary thinking process. Mi4iD blends behavioral science, rigorous research, and human-centered design, through which we solve complex challenges in social and economic development.

We use Mi4iD to keep empathy at the core of our research as we uncover why people do what they do, build solutions that drive change, and test them in the real world. Our teams cocreate with clients to prototype user-centric products and services that are desirable, feasible, and scalable.

Mi4iD brings structure to innovation through:

1) Grounded insights

2) Strategic ideation

3) Real-life testing

4) Scalable design blueprints

Discover more about Mi4iD, how it works, and how it transforms intent into impact at https://www.microsave.net/mi4id/

Collaborate with us and learn more about the Mi4iD process at info@microsave.net or mi4id@microsave.net.

Assessment of market systems for MSME digitalization and device financing for youth women-inclusive MSMEs in Uganda

The UN Capital Development Fund (UNCDF) commissioned this study by MSC under the 10X Program. In partnership with the Mastercard Foundation, the UNCDF implements the program with Outbox Uganda, Women in Technology Uganda (WITU), and Refactory Academy. The assessment examines digitalization of MSMEs and device financing in Uganda, with a focus on youth and women entrepreneurs, including refugees and persons with disabilities. It highlights key challenges, such as affordability, digital literacy, and access to financing. The study provides actionable recommendations to enhance digital adoption, strengthen access to finance, and support sustainable growth in Uganda’s MSME sector.

MSC supported BAPPENAS in launching the Blue Economy report: Strengthening the role of small-scale fisheries for Indonesia’s food security

The Ministry of National Development Planning (BAPPENAS) has officially launched a national report titled “Accelerating the Blue Economy in Indonesia” on August 6, 2025 in Jakarta. It is part of a larger strategy to enhance food security and promote sustainable development. The report is set against the context of a global crisis and the escalating impacts of climate change. Several partners, which include MSC (MicroSave Consulting), have contributed to the Blue Food Assessment through qualitative field research.

MSC participated in the launch event held in Jakarta as a technical partner. During the event, MSC emphasized the need to understand the conditions and priorities of small scale fisheries and aquaculture (SSFA). The SSFA community has long sustained the backbone of Indonesia’s aquatic food sector, but remains significantly under-supported.

“Gender dynamics play a pivotal role in how communities access natural resources,” said Grace Retnowati, Executive Director of MSC Southeast Asia. “When women’s contributions are overlooked, their ability to claim rights and benefit from resources is diminished. Add to that the territorial tensions between large and small-scale fishers, and we see how equity and sustainability must go hand in hand.”

The report adopted a qualitative approach and examined the four key provinces of East Java, East Nusa Tenggara, South Sulawesi, and Maluku. This approach engaged with more than 140 community stakeholders, local governments, and the private sector. Although SSFA actors account for 85% of the national fisheries sector, they still face many challenges. These include limited access to finance, inadequate post-harvest technology, high food loss rates, and constant pressure from climate change and environmental degradation.

The Ministry of National Development Planning (Bappenas), Rachmat Pambudy emphasized the strategic role of fisheries in national development. “Fish is our most efficient source of protein, rich in omega-3 and essential for nutrition,” he said. “It has long supported the livelihoods of coastal communities. As we pursue the Vision of Indonesia Emas 2045, the ocean must be safeguarded as a vital source of life and prosperity.”

He noted that Blue Food development will be prioritized over the next five years, in line with Asta Cita and Indonesia’s identity as the world’s largest archipelagic nation.

The report outlines a set of concrete recommendations. These include how to integrate aquatic foods into social protection schemes and promote nutrition literacy through behavior change communication. It also highlights how to apply eco-friendly technology innovations and expand social protection for small-scale fishers and aquaculture farmers.

The blue economy can potentially increase marine sector’s contribution to GDP by up to 15% by 2045. This events marks how the government is committed to place the blue economy as a cornerstone of Indonesia’s long-term development.