The water, sanitation, and hygiene (WASH) sector has no shortage of need but lacks proof. Until investors can clearly see where their capital goes, how it performs, and the outcomes it delivers, private finance will remain far below the scale needed to close the global WASH gap. And this gap today is massive. As per the WHO–UNICEF Joint Monitoring Program (2025), 2.1 billion people still lack access to safe drinking water. Another 3.4 billion lack basic sanitation, while 1.7 billion lack basic hygiene. Closing these gaps by 2030 will require almost three times the current investment. Public budgets cannot provide the additional USD 100 billion each year.

The funding shortfall is structural. Developing countries spend nearly USD 165 billion each year on water infrastructure. Public finance accounts for 91% of this amount, while private investment accounts for less than 2%. Tariffs, taxes, transfers, and official development aid provide the rest. Governments cannot increase public spending due to competing fiscal priorities, high debt, and the long payback periods of WASH investments. WASH also receives limited climate finance.

Of the USD 1.9 trillion tracked in 2023, only USD 49 billion was allocated to water and wastewater management. Private capital has therefore become essential. Mobilizing private capital is therefore a necessity, not a convenience.

The sector has reached an inflection point. Impact investment in WASH grew by 33% between 2015 and 2019, which made it the fastest-growing sector tracked by the Global Impact Investing Network (GIIN). Development finance institutions, such as the International Finance Corporation (IFC), FMO-Entrepreneurial Development Bank, and DEG, now co-invest with private partners across Asia and Africa. Yet, capital flows remain modest. The constraint is not in appetite but in the evidence generated.

How fragmented reporting holds back WASH investments

Credible impact measurement is essential to attract private capital to WASH. Investors and development finance institutions rely on standardized metrics to assess portfolio performance, compare investments, and show results to stakeholders.

The lack of a harmonized measurement framework creates fragmented reporting requirements. Financial service providers (FSPs) must satisfy multiple reporting standards. This duplication increases reporting fatigue and limits comparability across portfolios and geographies. Existing WASH frameworks measure service access and public expenditure well. However, they do not meet investor needs or assess investment performance effectively. A review of existing monitoring tools identified four major gaps that continue to constrain private capital in the WASH sector:

- The tools track service-level and policy indicators but capture limited data on private finance flows and loan performance to be useful for capital allocation decisions.

- They require FSPs to track and report on indicators that sit outside their existing management information systems (MIS), which creates a reporting burden.

- They measure outputs at the institutional or portfolio level, but lack the granularity to attribute health, income, or service outcomes to individual clients or loans.

- They allow each investor or framework to define their own indicators and methodology, which leaves no common measurement language to compare investments across portfolios and sectors.

Other sectors demonstrate the value of harmonized reporting. The Green Bond Principles helped expand the green finance market from less than USD 1 billion in 2012 to more than USD 500 billion annually within a decade. Standardized reporting also accelerated microfinance growth. WASH now needs the same foundation. A common measurement language can give investors the confidence to commit capital at scale.

Closing the evidence gap through the e-MFP WASH action group impact indicator framework

The European Microfinance Platform (e-MFP) WASH Action Group impact indicator framework was developed to address the gaps identified above. It provides a practical method aligned with global standards for institutions that work in resource-constrained environments. The framework has three goals:

- Reduce reporting burdens on FSPs;

- Improve data comparability across portfolios;

- Strengthen the link between finance deployed and outcomes generated.

The framework draws on internationally recognized standards, including the WHO–UNICEF Joint Monitoring Program, UNICEF’s Global Framework for Urban Water, Sanitation, and Hygiene, and WHO’s guidance on water, sanitation, and hygiene. It provides a consistent basis for measuring WASH investments across geographies.

The framework includes 11 core indicators across four dimensions: Financial, social, climate, and service levels. Financial indicators show how capital performs. The remaining dimensions measure the changes that investment creates on the ground. Together, they provide the evidence base that responsible investors need.

Each core indicator includes sub-indicators that allow disaggregation by borrower segment, enterprise size, gender, geography, WASH subsector, loan characteristics, climate contribution, and service levels. This level of detail helps financial institutions understand how much capital they should deploy, who receives it, how it performs, and what outcomes it achieves.

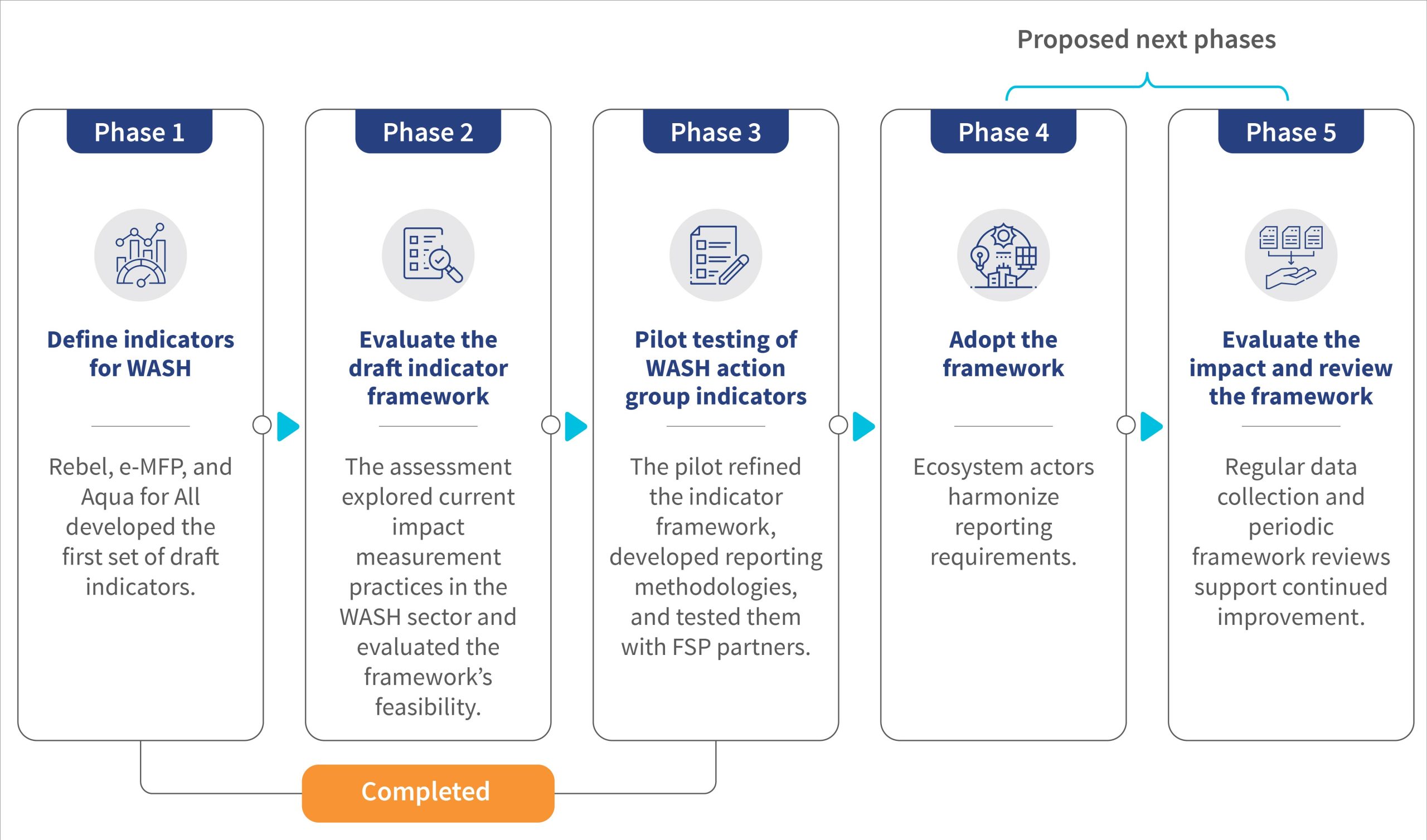

From design to reality

The framework evolved through three phases. During Phase 1 (2022-2023), e-MFP and Aqua for All commissioned the financial advisory firm Rebel to develop the WASH handbook and a draft indicator framework. This work established the conceptual foundation for standardized WASH impact measurement. During Phase 2 (2024), MSC (MicroSave Consulting) evaluated the draft with asset managers, financial institutions, and WASH SMEs. The assessment examined its practicality and alignment with existing measurement practices.

Phase 3 refined and operationalized the framework. FSPs across Asia and Africa, along with data platforms, tested the framework. The pilot assessed whether institutions could embed it within existing systems without creating an unsustainable reporting burden. The exercise mapped institutional data, reviewed MIS systems, and assessed data granularity. It also identified gaps in reporting capacity and in WASH-related information.

Rather than introducing parallel reporting systems, the pilot incorporated missing data fields into existing MIS wherever possible. Where FSPs lacked WASH or climate classifications, the pilot introduced tagging mechanisms and targeted system modifications that institutions could integrate into routine reporting.

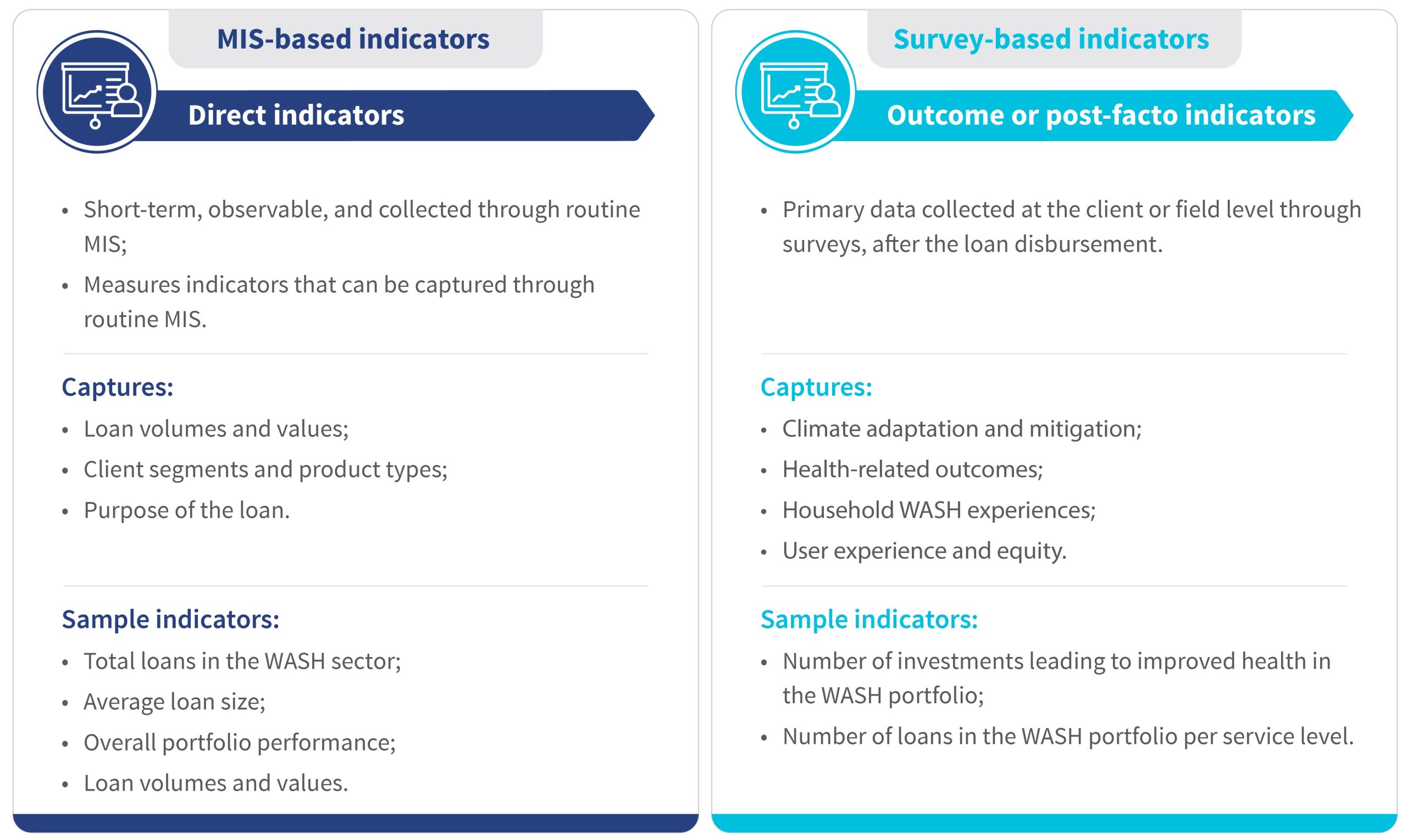

Figure 1: Classification of indicators by reporting effort and data collection method

The pilot also refined the original 16 indicators into 11 core indicators. It retained, redefined, merged, or removed indicators based on operational feasibility and analytical relevance. The project developed a suite of practical tools to support implementation. These include an operational manual with standardized indicator definitions and reporting guidance. They also include standardized MIS templates for portfolio and financial indicators, as well as structured survey instruments and digital data-collection tools for outcome indicators that MIS cannot capture.

The framework classifies indicators as MIS-based or survey-based. It also groups them by reporting effort: Low for MIS-derived indicators, moderate for survey-based indicators, and high for indicators that require retrospective classification. This approach supports phased adoption based on institutional readiness. Together, these tools help institutions integrate the framework into existing reporting systems and promote consistent and comparable WASH reporting.

Figure 2: Phases in the development of the WASH action group framework

The road from framework to ecosystem adoption

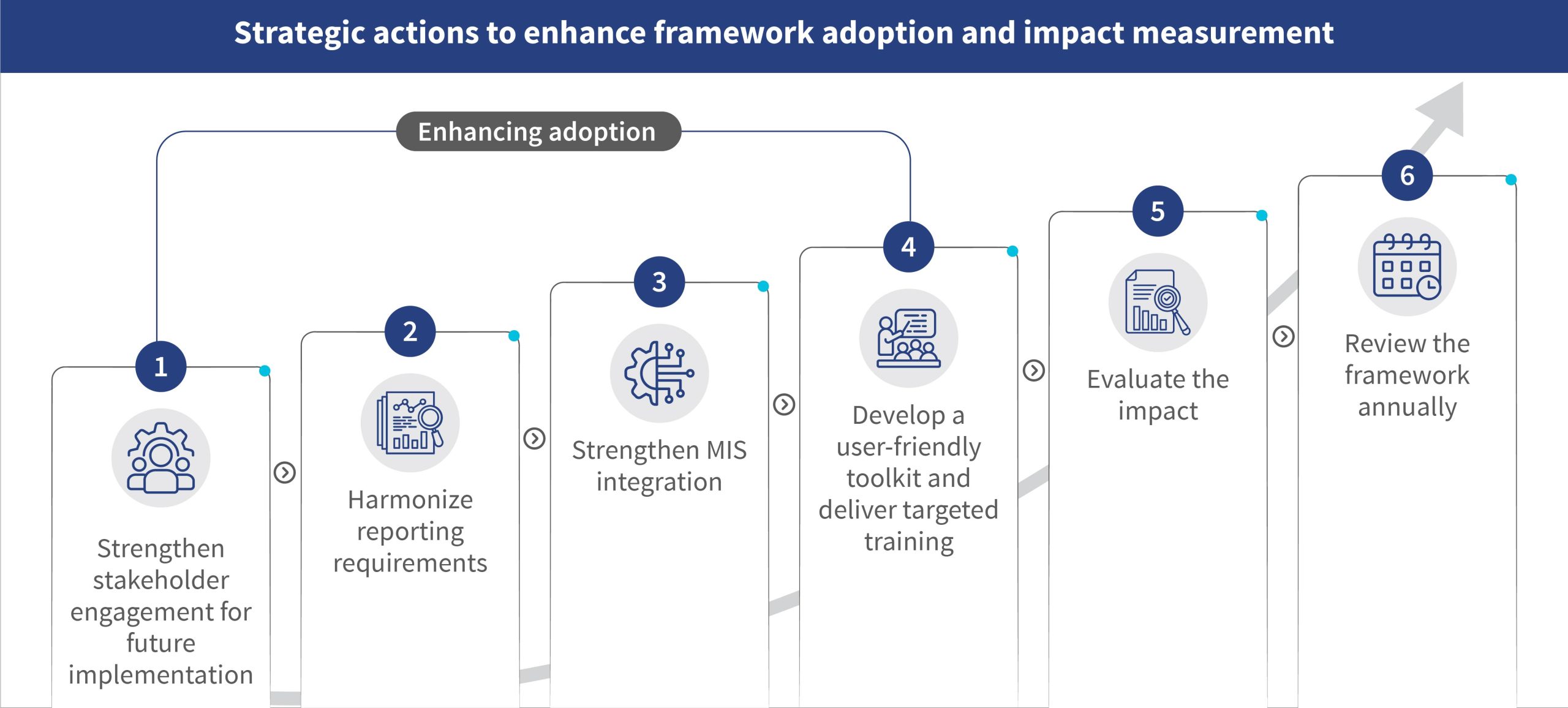

The e-MFP WASH Action Group has developed the data architecture, tools, and guidance needed for credible, comparable, and decision-useful WASH impact measurement. The pilot confirmed an important lesson: Impact measurement creates value only when investment decisions incorporate it from the outset. It should not become a compliance exercise.

Figure 3: Scaling adoption of the framework

The next step is ecosystem-wide adoption. Investors, FSPs, asset managers, and data platforms should converge around a common reporting approach. Institutions should adopt the framework in phases. They should first integrate indicators into existing MIS and later expand into survey-based outcome measurement. They should also establish baseline values for social, climate, and service-level indicators to support meaningful impact assessment over time. Regular evaluations and framework reviews can strengthen comparability, improve investment decisions, and mobilize more private capital for the WASH sector. The framework is ready. The sector now has an opportunity to adopt it collectively and put it into practice.

For the sanitation entrepreneur who seeks capital to serve more households, better impact measurement may seem far removed from day-to-day operations. Yet, it can determine whether investors have the confidence to commit capital in the first place. A common measurement language can help the sector show results more credibly, compare investments more consistently, and mobilize private capital at a scale that matches the challenge. Ultimately, unlocking capital for WASH is not only a financing challenge. It is an evidence challenge. The framework offers a path to address both.