This report examines financial fraud vulnerabilities among low- to moderate-income (LMI) individuals in Bangladesh, India, and Kenya. With 55% of respondents receiving fake calls or SMS, scams like impersonation and PIN compromise disproportionately impact urban women and the underserved. Over 60% of the victims are unaware of grievance mechanisms, leading to unresolved complaints. The report proposes regulatory reforms, awareness campaigns, and technology-driven solutions to improve fraud prevention, grievance redressal, and consumer protection frameworks.

This report has been revised as of 26th March 2025. Please refer to this updated version and discard any previous versions.

Explore the key insights and strategies Akhand Tiwari, Partner at MSC, shared during a workshop he hosted at the NetHope Summit 2024 in Washington, DC. This presentation, “Empowering Low- to Moderate-Income (LMI) Consumers in the Digital Era: Building Trust and Capacity for Sustained Use,” delves into the challenges LMI customers face when they use digital financial services (DFS). It highlights critical barriers, such as deceptive designs, poor grievance mechanisms, and low trust. The presentation offers actionable solutions and emphasizes transparency, user-friendliness, relevance, timely service, and security to build trust and empower LMI users to adopt DFS.

Population aging is a global trend, with the number of people aged 60 and above increasing rapidly worldwide. India is also experiencing significant growth in its elderly population, a declining fertility rate (below 2.0), and rising life expectancy (over 70 years). Individuals aged 60 and above comprise just over 10 per cent of India’s population, around 104 million people. This figure will rise to 19.5 per cent of the total population by 2050.

The senior care system faces significant challenges due to the lack of a comprehensive, integrated policy for elderly care and support1. Key issues include inadequate infrastructure and capacity for elderly health and welfare, insufficient evidence-based resources for managing geriatric illnesses, and a fragmented social support system. Additionally, physical infrastructure is often inaccessible, and research and development are scarce. The rise of nuclear families has diminished traditional family support, while financial insecurity and vulnerability to financial abuse remain critical concerns. Digital inequalities, exacerbated by the COVID-19 pandemic, further complicate access to services. Moreover, there is limited awareness among seniors and caregivers about available welfare services. Currently, senior care primarily focuses on facility-based medical care, neglecting nonmedical and home-based care options.

The Ayushman Bharat story and how it impacts elderly care in India

The Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY) has recently expanded its coverage to include all senior citizens aged 70 and above, regardless of their income. This significant policy change aims to enhance healthcare access for the elderly population in India, which is increasingly vulnerable due to age-related health issues.

The expanded scheme will provide annual free health insurance coverage of up to Rs 5 lakh per family for senior citizens aged 70 and above. This includes approximately six crore individuals from about 4.5 crore families. The coverage is designed to be utilized on a family basis, meaning that if there are multiple elderly beneficiaries in a household, the Rs 5 lakh limit will be shared among them.

Notably, nearly one-fourth (23.76 per cent) of all hospital admissions under the AB-PMJAY since its inception in 2018 have been for patients aged 60 or older.2 Out of the approximately six crore elderly individuals (70+ years) in India targeted for coverage under the Scheme, individuals aged 60+ years account for about 14 per cent of the total 350 million Ayushman cardholders.

However, health insurance coverage remains low among the elderly population in India compared to their Southeast Asian and European counterparts due to significant disparities in access, affordability, and comprehensiveness of healthcare services.

Ayushman Bharat Health and Wellness Centers (ABHWCs) cater to the healthcare needs of India’s elderly population by providing comprehensive primary care services, including preventive, promotive, curative, and rehabilitative interventions, with a focus on community-based care, regular health assessments, geriatric-specific training for healthcare providers, and smooth referrals to higher level facilities. These centers now rechristened as Ayushman Aarogya Mandirs (AAM), are also tasked with promoting health literacy, immunisation drives, and cost-effective services, particularly in rural areas, but face challenges in terms of limited awareness among seniors, infrastructure gaps3, and a need to prioritise outpatient care for chronic disease management in addition to hospitalisation.

Opportunities for total value unlock of AB-PMJAY

Despite the country’s expansion of PMJAY to the elderly population, there are several opportunities for unlocking the full value of the PMJAY scheme among the target beneficiaries. Awareness of the benefits of PMJAY among the elderly population remains a significant barrier. Access to mass media and digital platforms can be challenging for older adults, further complicating efforts to inform them about available health insurance options.

The existing healthcare infrastructure may struggle to accommodate the increased demand from an expanded beneficiary base. Smaller hospitals often operate on tight margins, and the influx of elderly patients requiring more intensive care could strain their resources. Ensuring adequate reimbursement rates that reflect actual costs incurred by healthcare providers is crucial for maintaining service quality.

Currently, the PMJAY primarily covers hospitalisation expenses but lacks provisions for outpatient care. Many elderly individuals require regular outpatient services for chronic conditions, which are not adequately addressed under the scheme. Expanding coverage to include outpatient services is essential for comprehensive geriatric care. The financial implications of expanding coverage to a larger population must be carefully considered. While the government has allocated funds for this initiative, ensuring timely payments to healthcare providers is vital to prevent disruptions in service delivery.

Most geriatric services are currently available at tertiary care hospitals, with limited outreach to rural areas where a significant proportion of the elderly reside. Training community health workers and enhancing primary healthcare services will be critical in addressing this gap.

While the expansion of PMJAY to include elderly citizens marks a significant step forward, several challenges must be addressed to unlock its full potential. Increasing awareness among low-income households, expanding outpatient coverage, ensuring adequate reimbursement rates, and timely claim settlements are essential for sustainable healthcare delivery. Additionally, strengthening geriatric care infrastructure, particularly in rural areas, and enhancing the training of healthcare professionals will be key to meeting the growing needs of India’s aging population.

References

1. Senior Care Reforms in India: Reimagining the Senior Care Paradigm, a Position Paper by NITI Aayog

2. Calculated from NHA AB PMJAY Dashboard

3. AB HWC Assessment Report 2022, MoHFW

This article was first published in Express Healthcare on 8th December 2024.

In 2023, scammers stole more than $1 trillion from victims worldwide, with Asia emerging as a hotspot for financial fraud. The Indian Cybercrime Coordination Centre (I4C) found that Indians suffered cumulative losses worth approximately $214 million (INR 1,776 crore) from January to April 2024 as a result of cyber frauds.

While digitization has revolutionized the delivery of government benefits, expanded access and minimized exclusion, it has also amplified fraud. Fraudsters have started to target government program recipients through fake messages and calls, often posing as government agencies or officials. They prey on vulnerable individuals, particularly those with low literacy levels who rely heavily on digitally disbursed government support, to trick them into giving money or revealing personal information.

MSC’s recent research with banking customers indicates a rising vulnerability among beneficiaries who receive government payments digitally into bank accounts or mobile wallets. The study uncovered a surge in fraud cases following government announcements on fund disbursement or notifications that require citizen action to continue accessing government services. These challenges pose a significant threat to the effectiveness and integrity of digital benefit delivery.

Accounts of defrauded government program beneficiaries

Case 1: Manju from Rajasthan, India, received a call from a scammer posing as a central government official, who informed her that her application for the PM Awas Yojana, a credit-linked subsidy program for affordable housing, had been selected. The fraudster asked her to submit a registration fee of $600 (INR 50,000) to finalize her residence allotment. Elated, Manju made the payment. Later, when she received no confirmation or house, she realized she had been defrauded.

Case 2: Aftab, a 70-year-old veteran daily wage worker in Dhaka, Bangladesh, benefits from the government’s old age allowance. One day, a fraudster posed as an official from the Department of Social Services and informed him that his account had been inactive and he would not receive the next payment. The scammer asked Aftab to share a code sent to him via message to reactivate his account. The fraudster then used this code to access his bank account and robbed him of all the money in his wallet account.

How do scammers entice beneficiaries who receive social payments digitally?

Fraud perpetrators continuously evolve and adapt tactics to exploit vulnerable beneficiaries. They often promise assured receipt of government benefits or create a fear of halted payments to manipulate customers into sharing sensitive details. Low digital capability and literacy make many digital payment program account holders particularly vulnerable. Their need for benefits drives them, and they often overlook privacy protection and secure banking practices, increasing their susceptibility to scammers.

One key point of vulnerability is found in the enrollment process for government programs. Beneficiaries with low literacy levels tend to need assistance with the enrollment process, so they provide physical copies of their documents to government program representatives. The representatives may hold on to these documents to complete the beneficiary’s enrollment process later, increasing the risk of data theft. Many programs also involve lengthy documentation procedures, further exposing recipients to the risk of fraud and data leakage.

Program beneficiaries may also be unaware of or unable to access official information sources on aid disbursements, such as touchpoints, officials or websites. When sophisticated fraudsters can access sensitive information, such as ID details, bank account numbers and enrollment application numbers, their calls or requests seem legitimate and can convince unaware customers to fall for their schemes.

How can the government help beneficiaries avoid becoming victims of fraud?

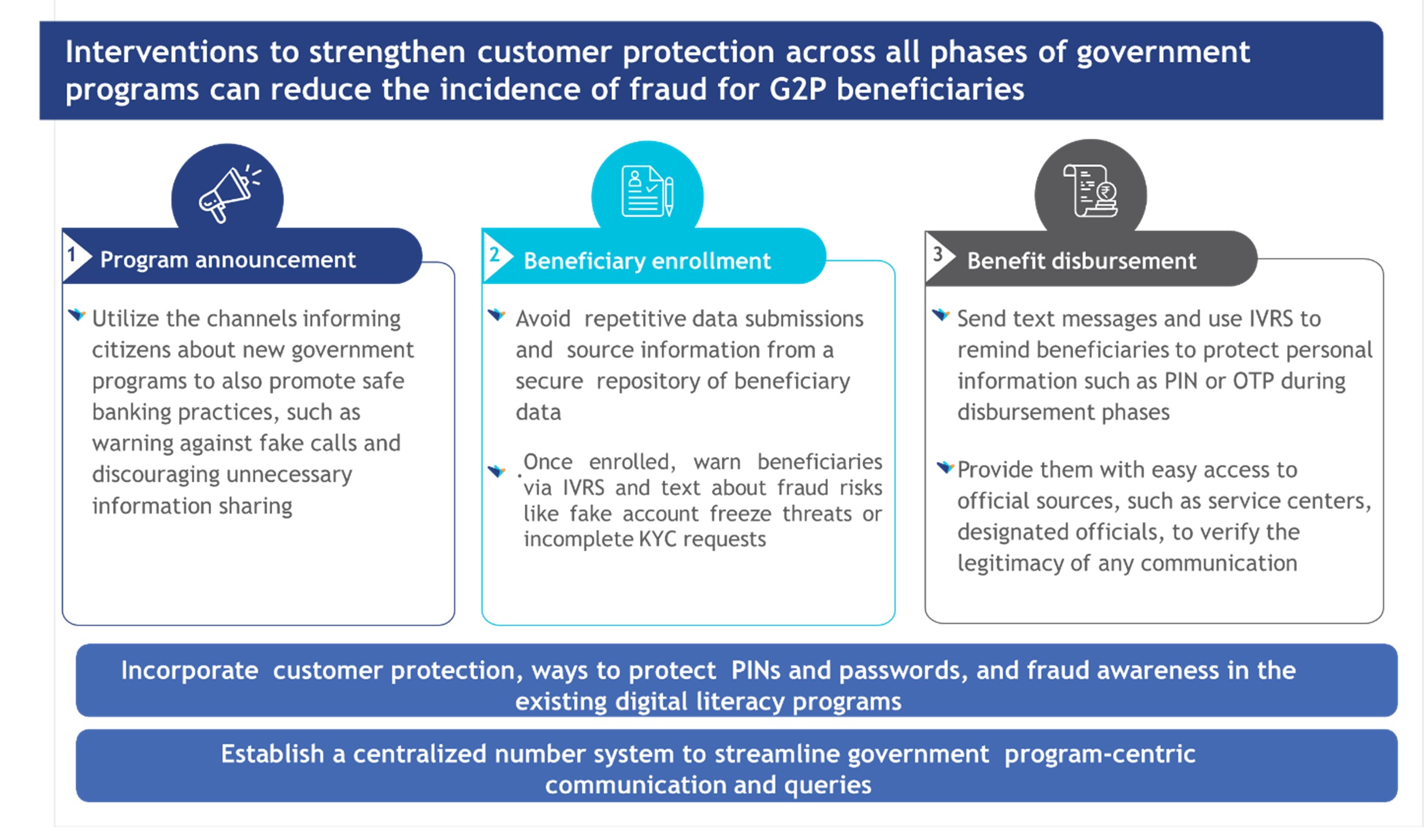

A customer protection-oriented approach is needed to decrease fraud among government program beneficiaries. There are a few clear steps that can be taken:

1. Education: Beneficiaries must be educated on safe banking practices. This can be done through channels already used for program-related awareness initiatives, such as websites, posters and community outreach programs. Existing digital literacy programs should incorporate a comprehensive customer protection component to enhance beneficiaries’ ability to navigate online platforms safely and securely.

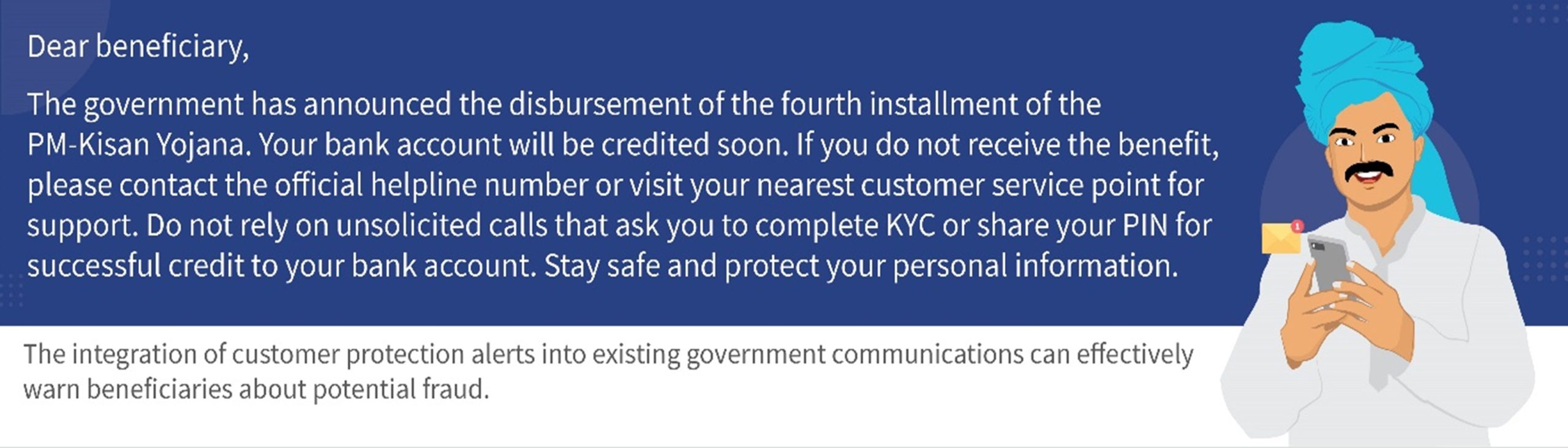

2. Communication: The government should establish a centralized contact number to provide information about all government programs. This number would serve as the sole communication channel from the government, so that beneficiaries can easily identify messages which come from the official source as opposed to fraudulent messages. The government should send text messages and use interactive voice response systems (IVRS) during program enrollment and disbursement phases to alert customers. These communications should inform beneficiaries about:

a) Prevalent fraudulent activities related to government programs.

b) The importance of protecting personal information.

c) Ways to recognize fraudulent activities.

d) Clear instructions on how and where beneficiaries can seek support if defrauded.

3. Streamline and secure enrollment processes: A data minimization and proportionality approach is needed to streamline the enrollment processes for government programs and ensure beneficiaries are not asked to provide the same information repeatedly. A secure repository of beneficiary data can serve as a source for such details, ideally as part of a digitized end-to-end enrollment process.

The figure below maps out these recommendations across the phases of government programs:

A multifaceted approach must emerge to safeguard government program beneficiaries against fraud. Enhancing digital literacy, streamlining enrollment processes and ensuring effective communication can significantly reduce the risk of fraud and ensure that vulnerable individuals, such as Manju and Aftab, continue to receive the support they need without falling victim to deceit.

This article was first published in the FinDev Gateway on 29th October 2024.

As Indonesia continues to build its economic growth based on the foundation of its rich natural resources, a critical opportunity lurks within its waters in the form of fish and other aquatic foods. Often called “blue foods,” fish and aquatic foods are a dietary staple for millions across the archipelago. Fish plays an essential role in meeting the nutritional needs of Indonesians. Between 2017 and 2022, the country’s per capita fish consumption has climbed steadily from 47.34 kilograms to 57.27 kilograms, as per December 2023 data from Statistik Kementerian Kelautan dan Perikanan. This rise signals the increasing role of fish in the Indonesian diet. Yet despite this growth, malnutrition, particularly among children, persists alongside widespread micronutrient deficiencies.

This paradox—high fish consumption alongside malnutrition—points to significant gaps in dietary intake and highlights the urgent need for policies that promote nutrition-focused blue food systems. Take East Nusa Tenggara as an example. The province faces the highest case of stunting in Indonesia at 37.9%, way above the national average of 21.5%, despite a per-capita fish consumption of 53.06 kg, only slightly below the national average.

To understand the paradox, we must dive into the heart of the fish supply chain, which comprises the country’s small-scale fishers. More than 10 million people are involved in small-scale fisheries in Indonesia, around 5 million of whom engage in fishing mainly to feed their households. For these communities, fish serves as a source of sustenance and income, which leads to trade-offs that can limit the nutritional benefits they derive from their daily catch.

Research from MSC Indonesia and Bappenas reveals that many fishers struggle to consume nutritious seafood themselves despite their vital role in the fish supply chain. While fish is a staple in their diets, fishers often sell high-quality fish to earn a living and consume lower-value fish at home. During lean seasons, this challenge intensifies and forces many to turn to less nutritious options, such as instant noodles. When fishing yields are low, fishers often buy cheaper, lower-quality fish from local markets. Price, rather than nutritional value, drives fish selection in these households. This behavior reflects broader economic hardships and limited nutritional literacy in low-income coastal communities.

Fishers also widely practice traditional preservation methods, such as salting and drying, to ensure food security during off-seasons. However, these methods can reduce the nutritional value of the fish. Consequently, many fisher households rely on simple meals of fish, rice, and sambal (chili paste) with minimal use of vegetables or nutrient-dense foods. Although fish remains a dietary mainstay, the unchanging preparation and preservation techniques limit their intake of essential fatty acids, vitamins, and other vital nutrients. For young children and new mothers, the lack of dietary diversity hampers ability to achieve optimal nutrition, particularly in the crucial first 1,000 days of life, and contributes to stunting and other malnutrition linked growth and development delays.

The lack of nutritional knowledge also affects dietary choices among pregnant and lactating women, who can benefit greatly from nutrient-rich seafood if they are empowered to make informed dietary choices. Limited knowledge, access or affordability of their specific dietary needs can leave vulnerable populations, including children, women, and the elderly, with nutritionally inadequate diets.

The current state of nutrition and dietary practices among fishers highlights a critical opportunity: Around 69% of Indonesia’s poor population lives in coastal areas, where many engage in fishing. Enhancing fishers’ access to nutritious blue foods could significantly benefit their health and well-being alongside that of the broader low-income coastal communities they represent.

Indonesia’s blue food economy has a unique opportunity to catalyze improved nutrition outcomes nationwide. Realizing this potential requires a holistic approach that enhances awareness, affordability, and accessibility and integrates blue foods into existing systems and practices.

First, the government and private sector should collaborate to improve the affordability and availability of nutrient-dense fish. Strategies, such as subsidies for farming high-value species, along with community-driven fisheries that prioritize local consumption can broaden access to these resources. In underserved areas, as demonstrated in India, initiatives to increase the availability of nutrient-rich fish can diversify diets and reduce the dependence on less nutritious alternatives.

One transformative approach lies in the incorporation of blue foods into national nutrition and social protection programs. Examples from other regions, such as the Philippines, show that integrating fish into social safety nets can yield significant health benefits. In Indonesia, integrating blue foods into social assistance initiatives, such as the Bantuan Pangan Non Tunai (BPNT) program, could help achieve this goal by providing essential foods to vulnerable families. The expansion of these programs in coastal areas would ensure that more nutritious seafood reaches households in need.

Likewise, promoting fish-based options for pregnant and breastfeeding women through the Program Keluarga Harapan (PKH) can help enhance the nutritional outcomes for vulnerable populations. Moreover, the anticipated launch of a national school meal program offers a valuable opportunity to incorporate fish-based meals in schools, especially in regions with high blue food production. This inclusion would enhance children’s nutrition and develop healthy eating habits early on.

Another crucial step is increasing nutrition literacy among fisher communities. Despite fish being a staple in their diet, many remain unaware of its specific health benefits, such as the role of omega-3 fatty acids, essential vitamins, and minerals in maintaining overall well-being. Community-based education programs delivered through local health clinics, schools, and fishing cooperatives can help these communities better understand the nutritional value of various fish species and the importance of nutrient-preserving preparation methods. Tailored information, education, and communication (IEC) materials, cooking demonstrations, and the training of community health workers can empower households to make healthier food choices. These initiatives can highlight the value of a balanced diet to help maximize the intake of essential macro and micronutrients.

Fostering dietary diversity through cultural and behavioral changes is equally important to complement education. Social and behavior change communication (SBCC) campaigns can encourage healthier cooking methods and promote the inclusion of locally available fruits and vegetables alongside fish. Moreover, Indonesia’s vibrant cultural festivals that celebrate fisheries—such as those featuring crabs or grouper—offer unique opportunities to engage communities. Nutrition experts can use these events to promote health literacy through recipe competitions, cooking demonstrations, and interactive sessions that underscore the importance of diverse and balanced diets.

The Indonesian government has already shown a strong commitment to advance blue foods and improve nutrition outcomes. Indonesia can unlock the full potential of its blue food economy if it combines education, economic support, and cultural engagement with strategic program integration. By doing so, the nation will be able to nourish its people and set a global example of how aquatic resources can drive sustainable and equitable health outcomes.

This article was first published in The Jakarta Post on 27th November 2024.

This fish recipe book, part of the JEEViKA Special Purpose Vehicle for Agriculture Transformation (JSPVAT) initiative, showcases traditional fish preparation methods across Bihar. Supported by the Bill & Melinda Gates Foundation, MSC, and WorldFish, it promotes the nutritional benefits of fish consumption, preserves cultural heritage, and empowers local communities through sustainable aquaculture. By encouraging healthy diets and fostering culinary skills, this initiative strengthens livelihoods and supports Bihar’s local economy.

Click here to download the Hindi version of the recipe book.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.