This report evaluates the digital public infrastructure readiness of revenue authorities across Nigeria’s 36 states and the FCT using the Intelligent Revenue Authority (IRA) framework. It analyzes maturity across person-to-government, business-to-government, and government-to-government payment systems, highlighting significant variation in digital adoption. While some states demonstrate advanced integration, automation, and data use, many rely on manual processes and fragmented systems. The report proposes phased, state-specific roadmaps to strengthen interoperability, automation, digital governance, and human capacity, aiming to improve revenue mobilisation and service delivery.

Blog

Timely Wages, Trusted Payments: Smart Payments for Urban Livelihoods

Urban livelihoods in India are predominantly informal, leaving workers vulnerable to insecure employment and limited social protection. This vulnerability was starkly exposed during the COVID-19 pandemic, when millions of migrant and low-income urban workers faced sudden income losses. The Housing and Urban Development Department (H&UDD) of the Government of Odisha responded to this crisis by working with existing community networks to create mass employment opportunities for the urban poor, informal, and migrant laborers. While MUKTA provided a critical safety net, its effectiveness was undermined by severe delays in wage payments to beneficiaries. These challenges undermined the intended outcomes of MUKTA. They not only strained workers’ livelihoods but also resulted in weak fiscal accountability at the urban local body (ULB) and state levels.

To address these challenges, MSC, in partnership with the state government, designed and implemented a scalable Smart Payments Solution (SPS). The solution combined a digital program management platform, MUKTASoft, with a just-in-time funding system. MUKTASoft digitized every stage of scheme implementation using a rule-based smart payments engine. The JIT funding mechanism ensured that funds were released directly from the state treasury to beneficiaries’ bank accounts.

The pilot implementation of SPS delivered substantial results. Wage delays were reduced, approval times fell sharply, utilization certificate pendency dropped to zero, and overall fund management efficiency improved. Women SHG members also reported faster receipt of payments, reduced administrative burden, and greater financial independence. The success of the pilot led to the statewide rollout of SPS across all ULBs in Odisha. This case study demonstrates how smart payments, grounded in sound public financial management principles, can improve welfare delivery systems, and strengthen livelihood outcomes for urban informal workers at scale.

Performance over assets in Bangladesh’s credit reform

In this three-part series, we scrutinized the shift toward multiple credit bureaus for financial service providers (FSPs) in Bangladesh. The first part discussed the implications of the framework for multiple credit bureaus, while the second part focused on regulators and development partners (DPs). In this final part, we examine market incentives and global lessons that show how a multi-bureau system can drive financial inclusion on a large scale.

The multi-bureau reform enables Bangladesh to shift from a collateral- and relationship-based credit identity to a performance-based one. This change creates opportunities for MSMEs, informal workers, and new borrowers who previously struggled in the formal financial system.

Private credit bureaus can expand the basis to assess creditworthiness for these segments of borrowers, as they primarily assist borrowers without formal income documentation or collateral. While many low-income households and informal workers repay their debts reliably, their financial discipline remains hidden within single lenders.

Alternative data, such as mobile money transactions and utility payments, holds immense potential to serve such thin-file borrowers. However, the near-term priority for the regulator and the market must remain on standardizing and ensuring full-file reporting of traditional credit data from banks, MFIs, and cooperatives. Alternative data can only strengthen scoring after this core foundation becomes robust and reliable, which means its full utility is a second-stage integration.

When bureaus participate in the credit ecosystem, they make repayment history portable across the financial sector. This portability allows lenders to evaluate borrowers based on their repayment track record rather than their physical assets. The transition enables gradual increases in loan size over time. Eventually, as borrowers build their credit profiles, they can then move from microfinance products to formal enterprise loans. This progression represents a fundamental shift in how financial institutions view the creditworthiness of customers in emerging markets.

Most lenders globally treat bureau scores as only a first-level filter in their decision process. This initial screening may restrict credit access for borrowers with limited credit histories and thin credit files for lenders to assess their creditworthiness accurately. Still, borrowers typically can access more credit over time, as their data becomes richer and more comprehensive. The challenge lies in how consistently the market applies these scores and filters rather than rely solely on credit scores.

For Bangladesh, consistency has emerged as a more critical issue as the country moves forward with its reforms. The Bangladesh Bank issued letters of intent (LoI) to five companies to form credit bureaus: Creditinfobd, TransUnion, bKash Credit, First National Credit, and City Credit. Later, TransUnion and bKash announced that they would establish a joint company, which reduced the number of credit bureaus to four. These four private bureaus will now enter the market with different methodologies.

Consistency will be paramount for the market to trust this multi-bureau system. This depends on three core elements:

- Data definitions: The exact borrower attributes being captured and reported, such as loan type, repayment status, and delinquency buckets;

- Weighting logic: How different variables, such as repayment behavior, outstanding exposure, and frequency of defaults, are weighted within the score;

- Score calibration: How raw risk estimates are translated into standardized score ranges so that scores are comparable and predictive.

If the scoring models diverge significantly, lenders may over-rely on the most conservative scores available. They may also avoid bureau insights altogether and return to traditional assessment methods, which include requiring collateral, relying solely on fixed income in the form of pay stubs, or using manual relationship-based assessments. This outcome would limit the benefits for low-income and MSME borrowers who need these new pathways the most.

The Bangladesh Bank maintains direct oversight over the scoring process to prevent this fragmentation. These regulatory safeguards are central to consistency and consumer trust:

- Mandatory model approval: The central bank requires mandatory model approval for all credit bureau scoring methodologies.

- Non-discriminatory scoring: Guidelines explicitly prohibit the collection of sensitive attributes, such as political affiliation or religious beliefs, to prevent bias.

- Score as a filter: A critical protection mandates that lenders cannot rely solely on a bureau’s score; it must be used as only one structured input among others in the credit decision process.

The impact of this bureau reform also depends on the digital readiness of lenders across the market. Smaller FSPs with manual data workflows struggle with consistency and timeliness. Borrowers cannot fully use their reputation capital when technical limitations obscure credit history. The infrastructure must support seamless data exchange to realize the reform’s full potential.

True inclusion requires the definition of creditworthiness to expand beyond formal loan repayment data. The system must incorporate behavioral indicators, such as mobile money patterns, utility payments, and savings behavior. These indicators accurately reflect financial reliability in informal settings where traditional credit histories are absent. The challenge lies in how bureaus translate diverse data sources into robust models that lenders will trust.

Pakistan offers relevant examples through platforms, such as Jumo and JazzCash, which use mobile money transaction patterns to determine internal credit scores. Bangladesh can adopt similar approaches where bureaus recognize financial progress through non-traditional indicators.

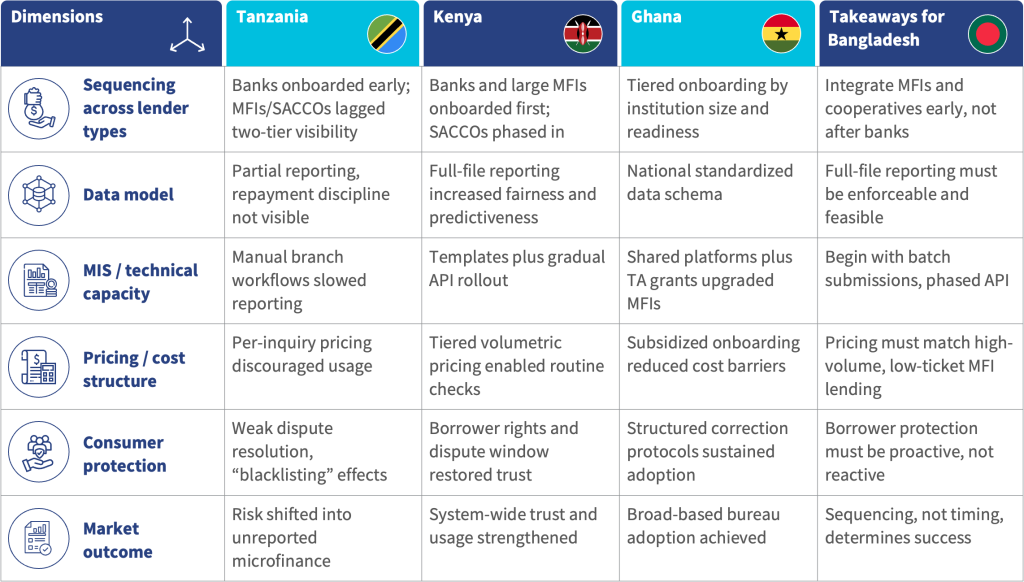

Similarly, Africa offers valuable lessons from credit bureau transitions. If participation remains uneven, a “two-speed” credit market emerges. Global lessons, particularly from Tanzania and Kenya, demonstrate that when reporting is mandatory only for banks and not fully integrated by MFIs, credit discipline improves in the formal sector. However, this change merely shifts over-indebtedness to the segments that remain unreported. This is the key risk for Bangladesh in terms of financial stability.

If MFIs and cooperatives lag in both reporting and the use of bureau data, credit risk migrates into unregulated segments. Bangladesh must address this immediately to ensure the reform strengthens the financial sector.

Tanzania and Kenya saw banks adopt bureaus early, but microfinance institutions (MFIs) and savings and credit cooperative organizations (SACCOs) lagged significantly. This gap shifted over-indebtedness problems to unreported segments. Meanwhile, Ghana shows that broad visibility across all lender types is achievable. The country sequenced onboarding by institutional capacity and provided smaller lenders with dedicated technical support.

Bangladesh must integrate MFIs and cooperatives early in the implementation process to prevent a two-tier system where only formal banks benefit from shared data. The integration should follow a phased approach that starts with standardized batch submissions. The system can transition to real-time API checks as capacity improves.

Comparative lessons from the implementation of credit bureaus in Africa

Source: Created by MSC with inputs from Maxwell Investment Group and Zeeh

Credit bureau pricing structures must support high-volume, small-ticket transactions that characterize MSME and microfinance markets. Per-inquiry fees discourage routine use by MFIs and merchant lenders, which operate on thin margins. Volume-based or institutional flat-rate models support regular bureau checks without prohibitive cost barriers.

Beyond access fees, bureaus must provide decision-ready intelligence over raw data dumps. They should deliver standardized scorecards and risk dashboards that help lenders apply bureau information meaningfully in their underwriting processes. Many smaller lenders lack the technical capacity to build proprietary models from scratch.

Regulatory authorities and governments must establish consumer protection frameworks alongside technical infrastructure. Kenya’s experience shows that negative-only systems can entrench exclusion rapidly when borrowers cannot recover from mistakes. Borrowers must have clear rights to access, dispute, and correct their records. Improved data infrastructure alone will not automatically change credit decisions in the market. FSPs must treat bureau information as a primary input that actively influences loan amounts, interest rates, and repayment terms.

A major tension in the transition is between regulatory enforcement (reporting data) and voluntary participation (using data). Specifically for MFIs and high-volume digital lenders, cost and workflow friction often drive this tension. If bureau access is priced per inquiry or per user, institutions may report data to comply with regulations but limit bureau checks in practice, which would render the bureau a passive repository rather than a live decision-making tool.

Regulators must, therefore, establish a supportive pricing model, such as volume-based or institutional pricing, which makes high-frequency, low-cost access viable for all lender segments to ensure lenders use the bureau in underwriting.

Regulators, DPs, and FSPs must prioritize three critical elements in their execution:

- Ensure broad participation across all lender types from the start;

- Establish strong data standardization that creates consistency across bureaus;

- Enforce proactive consumer protection measures to build trust in the system.

The success of Bangladesh’s multi-bureau system depends on operational choices and specific implementation plans, rather than broad policy goals. The sequence of implementation matters more than the speed of rollout. If made sensibly, these coordinated efforts will unlock the full potential of Bangladesh’s credit bureau reform and carve pathways to financial inclusion for people who have been excluded for far too long.

Interoperability in Bangladesh: The Stakes, the setbacks, and the way ahead

Despite regulatory readiness and technical infrastructure, key providers remain hesitant to adopt interoperability. Addressing commercial, operational, and governance gaps now is essential for nationwide uptake

Interoperability is widely acknowledged as one of the most powerful enablers of digital finance. When customers can send, receive, and use money across various providers—such as banks, payment system providers, wallets, and cards—the payments ecosystem becomes faster, more convenient, and potentially cheaper.

The World Bank and CPMI’s Principles for Financial Inclusion (PAFI) emphasise that interoperability increases competition, reduces fixed infrastructure costs, enables economies of scale, and significantly enhances customer convenience.

Globally, interoperable systems—from India’s UPI to Tanzania’s mobile-money rails—have demonstrated that shared infrastructure significantly increases transaction volumes, lowers marginal costs, and fosters innovation. Interoperability also strengthens merchant acceptance and makes digital ecosystems “sticky”, reducing customer dropout, increasing digital uptake, and improving trust.

Yet Bangladesh did not have interoperability for years, and relied on bilateral arrangements

Despite having one of the world’s most dynamic mobile-money sectors, Bangladesh operated without true interoperability for more than a decade. Before 2019, the market relied heavily on bilateral arrangements such as bank-to-wallet transfers through individualised agreements (e.g. BRAC–Rocket partnerships), card-to-wallet top-ups using specific bilateral integrations (e.g. bKash–Mastercard), and wallet-to-wallet transactions between select partner providers, rather than across the whole ecosystem.

This bilateral approach had three consequences:

a) high integration costs for each new partnership;

b) no uniform pricing, leading to market distortion;

c) digital silos, where each large provider captured its own customer base and ecosystem.

Given the dominance of leading MFS providers such as bKash, Nagad and Rocket—and the associated float income, agent-network investments, and branding advantages—there was little commercial incentive for them to open up to competitors voluntarily.

How things have changed

To address these structural barriers, the UK-funded Business Finance for the Poor in Bangladesh (BFP-B) programme undertook extensive technical work on interoperability from 2017 to 2020.

BFP-B concluded that Bangladesh could unlock enormous value if it shifted from bilateral, provider-led integrations to a switch-based, rules-driven interoperable ecosystem under Bangladesh Bank.

Under the BFP-B programme, MSC developed a comprehensive framework to support the Bangladesh Bank in the rollout of interoperable digital financial services. The operational guidelines defined key use cases including wallet-to-wallet, bank-to-wallet, card-to-wallet, PSP-to-wallet, and merchant payments and outlined a phased, switch-based implementation sequence with real-time settlement through the National Payment Switch Bangladesh (NPSB).

These guidelines were comprehensive, detailed, and technically robust—yet adoption was limited at the time for various reasons, including a lack of provider participation.

After more than five years, Bangladesh Bank has enabled interoperability through NPSB

Recently, Bangladesh Bank formally enabled account-to-account interoperability through NPSB, updating the regulatory framework to include banks, mobile financial services, microfinance institutions, and payment service operators. The switch now supports real-time clearing and multi-party settlement. This marks a significant regulatory commitment as NPSB rules are upgraded, settlement processes standardised, and technical processes established for providers to follow.

Despite regulatory readiness, the adoption of interoperability through NPSB has lagged. Providers question the commercial benefits as they face high integration and transition costs. They also argue that current interchange and fee structures do not offset lost float income and ongoing agent commissions, particularly for high-volume players with large agent networks. Many still doubt NPSB’s uptime, message integrity, fraud controls, and real-time-payments performance, and may hesitate to integrate until reliability at scale is demonstrated. Integrating with the central switch also requires significant technological upgrades, testing, and reconciliation changes, which weigh heavily on smaller or legacy institutions. Unresolved questions on SLAs, liability, AML/CFT, and interoperable pricing can further delay decisions and the onboarding of providers onto NPSB.

What can now be done to resolve concerns and bring large providers on board?

For successful uptake of interoperability, four specific actions—based on our experience—are necessary:

Reset the commercial model through a structured, transparent interchange framework: A well-designed pricing structure is key to successful interoperability. It must incentivise players to cover the costs of managing payment infrastructure, fraud prevention, and customer management and servicing. In Bangladesh, major players will also consider the impact on float income, transactional revenues, and distribution expenses before fully embracing interoperability.

Conversely, customers generally expect little to no cost for digital payments, as cash is considered “free”.

To address this, Bangladesh Bank may consider:

- Publishing a long-term roadmap or vision, to be reviewed annually

- Establishing a high-powered steering group comprising major players as well as smaller players and think-tanks to determine the fee and incentive structure

- Allowing temporary transition incentives for providers with large distribution networks

This mirrors strategies from Brazil (PIX pricing standards) and Pakistan (regulated 1Link pricing).

Implement a formal phase-wise onboarding model with readiness audits

A five-phase rollout sequence is recommended to give providers adequate time to prepare and integrate their systems, ensuring a steady adoption of interoperability.

This phased approach is akin to building a payment highway: Phase 1 starts by connecting the two biggest cities (MFS wallets), where traffic is densest. Phase 2 connects these cities to the national rail network (banks), already established on the switch. Subsequent phases handle smaller connections (cards, PSPs) and specialised infrastructure (merchants/QR codes), ensuring the system prioritises high-volume traffic before being overwhelmed by complexity.

Bangladesh Bank can also adopt a readiness-audit model similar to Kenya’s PesaLink, ensuring that each provider meets minimum requirements such as real-time-settlement capability, cybersecurity capacity, fraud-monitoring systems, system redundancy, and uptime before onboarding. These strict audits ensure providers are fully prepared before joining the “highway”.

Strengthen and enforce dispute-resolution and AML frameworks: Effective interoperability requires a robust, regulator-led dispute-resolution framework to manage the risk of errors, fraud, and customer harm that arise from cross-network transactions. Stakeholders expect Bangladesh Bank to establish fast, transparent processes—with clear turnaround times, dedicated monitoring teams, mandatory provider cooperation, and digital logbooks of disputes. Typical TATs vary: technical timeouts can be resolved within minutes, whereas cases involving the wrong recipient may take several working days. Providers must freeze disputed funds, act in good faith during reversals, and maintain teams capable of resolving issues quickly to safeguard customer trust.

Interoperability also increases AML/CFT and fraud-related vulnerabilities, demanding strict compliance and oversight. All participating entities must follow the Money Laundering Prevention Act, Anti-Terrorism Act and BFIU guidelines; ensure robust and regularly updated KYC practices; and report suspicious or fraudulent activity immediately. Strengthened internal controls, clear governance roles, and risk-mitigation protocols are essential to protect the ecosystem and maintain system integrity as digital financial services become increasingly interconnected.

Phased onboarding and regulatory concessions: Interoperability introduces significant integration and compliance costs, especially for newer or smaller providers who must upgrade systems, hire technical staff, and strengthen their capacity for real-time payments. Similar challenges were seen in Kenya, where smaller banks struggled with capital-intensive upgrades during the PesaLink rollout, underscoring the need for phased onboarding and regulatory support.

International experience shows that temporary regulatory concessions can accelerate adoption and create a more level playing field. For example, Jordan’s JOMOPAY waived all provider fees, and providers themselves agreed to forgo interchange for the first two years, allowing the ecosystem to stabilise before cost-recovery mechanisms were introduced. Drawing on these lessons, Bangladesh Bank can promote integration testing through the central sandbox and waive switch and interchange fees for a defined period.

To support providers and customers in adopting interoperability, Bangladesh Bank and the Government can explicitly support zero-switch fees during the early stages.

Conclusion

Interoperability aims to address a significant economic challenge, extending far beyond a technical project. The BFP-B programme outlined operational and pricing options; Mojaloop now provides the technical rails. What is required now is coordinated execution: regulators setting clear, fair rules and timelines; dominant providers accepting temporary concessions in the interests of long-term market expansion; smaller players committing to strong operational standards; and donors and partners financing transition costs and technical assistance.

When each stakeholder plays their part—regulators guaranteeing a level playing field, market leaders managing migration responsibly, and development partners de-risking initial costs—interoperability will move from pilots and conferences to everyday transactions that lower costs and broaden access for millions.

Bangladesh can finally achieve interoperable digital payments—unlocking enormous value across households, MSMEs, government services, and the broader digital economy.

This was first published on tbsnews on 10 December, 2025

How development partners can enable an inclusive multi-bureau future

In the first part of this three-part blog series, we examined the fundamental challenge of data quality that Bangladesh’s new multi-bureau credit system faces. We established that financial service providers (FSPs) must report complete and standardized information to ensure borrowers’ repayment histories serve as verifiable financial assets across the entire market. Only through this commitment can the system realize its promise of inclusion.

In this second part, we focus on the architects of the system. The Bangladesh Bank, government ministries, and global development partners (DPs) must recognize the critical truth that this reform extends beyond the licensure of new credit bureaus. The objective centers on financial inclusion at scale. The architects of the reform must actively execute the following three essential elements to drive this systemic change:

- Strong regulatory oversight;

- Sequenced implementation;

- Targeted technical assistance.

The Bangladesh Bank established a robust regulatory framework for the multi-bureau system. Comprehensive guidelines are now available, and the rules mandate full-file reports, shared data submission obligations, and reciprocity, which refers to the requirement that any institution accessing credit bureau data must also provide its own borrower data to the bureau. This ensures that all participating institutions contribute to and benefit from a comprehensive and transparent credit information system.

This framework is intentionally broad and includes all major lender segments, such as banks, nonbank financial institutions (NBFIs), microfinance institutions (MFIs), cooperatives, and digital lenders.

On paper, this foundation promotes broad market participation. In practice, however, the quality and coverage of data reporting depend heavily on the technical capabilities and existing incentives of individual lenders. While large commercial banks and leading MFIs operate centralized management information systems (MIS) that can integrate bureau reporting quickly and efficiently, this is not the case across the sector.

Many smaller MFIs and cooperatives rely on simple, branch-level systems. This infrastructure gap critically undermines how well they can deliver consistent, standardized, and timely reports. If these smaller institutions fail to report their client data, then the very clients they serve remain invisible to the new system. This would most significantly affect rural entrepreneurs, informal workers, and thin-file borrowers who have limited or no history in the formal banking system.

The introduction of private credit bureaus, therefore, will not automatically shift the system toward behavior-based assessment. Success depends entirely on the following three factors:

- Enforcement of the regulatory architecture;

- Consistent participation by lenders;

- Protections for borrowers to prevent unintended exclusion.

Global DPs become an indispensable force at this juncture. Institutions, such as the World Bank and development finance institutions (DFIs), must provide strategic support for the transition. They must offer a carefully sequenced strategy, effective enforcement mechanisms, and technical assistance across a diverse set of lenders. These partners should actively support the Bangladesh Bank to strengthen both the regulatory environment and supervisory capacity.

These partners can strengthen the ecosystem through the interventions below:

- Sequenced implementation: DPs should help the Bangladesh Bank segment lenders based on MIS maturity. The regulator can then define differentiated and time-bound minimum standards for each segment. Smaller institutions struggle with real-time systems. DPs can support the introduction of batch submissions as a practical interim solution.

- Strengthened oversight: DPs can enhance the supervisory capabilities of the Bangladesh Bank and the Microcredit Regulatory Authority (MRA). This enhancement includes the following two priorities:

- Harmonize data standards across all sectors: Disparities in data fields, definitions, and collection methods between the Bangladesh Bank-regulated banks and the MRA-regulated MFIs can lead to data fragmentation. DPs must support a unified approach to ensure that the bureaus effectively use and compare the information reported by all lenders.

- Improve model governance oversight: The shift to a multi-bureau system will introduce multiple, privately developed credit-scoring methodologies. Supervisors must ensure that bureau score models remain transparent, explainable, and non-discriminatory. Strong oversight is essential to prevent automated decision-making from unintentionally excluding or unfairly pricing loans for specific borrower segments. Development partners can provide technical support and draw on international best practices to help strengthen model governance, supervisory review, and audit frameworks.

Bangladesh must embrace the responsible integration of alternative data. This action will open up the market for thin-file borrowers. Once the core credit system proves reliable, alternative data can substantially enrich bureau models. Data from mobile money transactions, merchant sales, and utility payments will all add value.

DPs should enable stakeholders to design standards for alternative data use. They must help develop interoperable data exchange formats that allow this non-traditional information to flow securely and efficiently.

Critically, DPs must help strengthen Bangladesh’s consumer protection framework. The system must embed the key borrower rights mentioned below to ensure trust and fairness:

- The right to access and correct credit data;

- Streamlined dispute resolution mechanisms;

- Notice before adverse action protocols.

Finally, DPs should support national efforts in financial literacy. Borrowers must understand how lenders use their credit histories and how to proactively manage their own credit reputation. This education empowers borrowers and reinforces the integrity of the system.

Bangladesh’s multi-bureau reform is emblematic of a critical moment. This reform goes beyond a technological upgrade and constitutes an institutional transformation. Regulators and DPs must commit fully to achieve inclusion and growth. Strong regulation and support will establish the foundation for systemic stability. While this groundwork is vital, the ultimate success of this reform depends on the effective use of this rich new data. Lenders must assess risk confidently for millions of informal workers. Micro, small, and medium enterprises (MSMEs) in Bangladesh currently face exclusion from formal finance. This system can change that.

In the third part of this series, we will examine market incentives and global lessons that drive creditworthiness assessment through alternative data. This analysis will show how the new multi-bureau system can serve as a mechanism for the nation to achieve financial inclusion at scale.

Part 2: Moving climate-displaced persons to financial self-reliance

In Part 1 of this two-part blog, we explored the harsh realities faced by internally displaced persons (IDPs) in Tanzania, such as Asha, whose lives are upended by climate disasters. We highlighted how the lack of identification, limited access to agents, and systemic trust issues keep IDPs excluded from financial systems, despite the country’s high overall inclusion rates.

In Part 2, we turn from challenges to solutions. How can financial services be redesigned to meet the unique needs of displaced populations? And what roles can regulators, financial service providers (FSPs), and development partners play to transform financial access into genuine economic empowerment?

Asha’s struggle underscores that financial services must be intentionally designed around their lived realities to serve displaced populations effectively. This calls for simpler onboarding processes, flexible and relevant product bundles, trusted grievance redressal mechanisms, and gender-sensitive financial literacy initiatives.

We must promote coordinated action across multiple sectors to create financial services that truly support the underserved. We can redesign financial inclusion strategies to reflect the realities of displacement, which can help Asha and many more turn hope into tangible economic empowerment.

Collaborative pathways toward financial empowerment

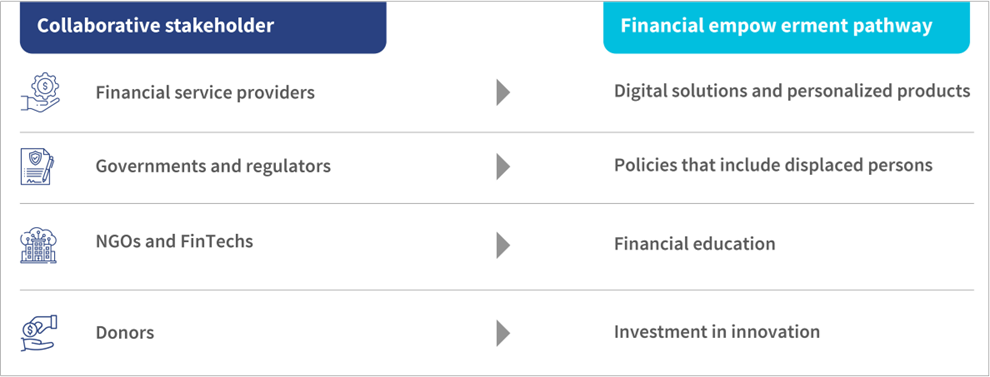

Global evidence shows that displaced persons can thrive when they are supported with the right financial tools within an inclusive financial system. Achieving this, however, requires coordinated action.

FSPs can design flexible, low-cost products customized to the realities of displaced populations, products that meet their immediate needs, and build pathways to long-term resilience.

- Digital solutions: Mobile money and digital wallets reduce the need for physical branches. In Jordan, refugees can register mobile wallets online, which proved vital during the COVID-19 pandemic. Uganda has allowed refugees to open bank accounts through their refugee IDs, which expands access quickly. MSC’s work in Uganda’s Bidibidi settlement under the Agent Network Accelerator (ANA) project highlighted how refugees use digital payments in practice. The study surfaced real-world challenges, such as registration bottlenecks, fraud, liquidity shortfalls, and weak agent networks. Insights from the study informed stronger digital payment strategies in humanitarian contexts.

- Tailored products: FSPs must develop accessible products with IDP-specific realities in mind. They must prioritize flexibility, affordability, and transparency. Small savings accounts with low minimum balances, microloans with flexible repayment terms and no collateral requirements, and insurance for climate or health risks are essential. Community finance groups, such as village savings and loan associations, continue to be a proven entry point, especially for women.

Governments and regulators should create supportive frameworks that address identification and access barriers, which enhance grassroots consumer protection.

- Policies that include displaced persons: National financial inclusion strategies must recognize IDPs as part of the population. Regulators can adopt flexible rules to make services accessible. For instance, policies need to accept refugee IDs or risk-based customer checks to be truly inclusive. MSC supported the Alliance for Financial Inclusion (AFI) in Tanzania to conduct a diagnostic study on the financial inclusion of climate-induced forcibly displaced persons (FDPs) and their host communities. The findings shaped a roadmap for the Bank of Tanzania to integrate FDPs into the National Financial Inclusion Framework (NFIF). This step brings displaced communities into the same financial system as everyone else. The roadmap suggested that government bodies should prioritize rapid, alternative identification methods, increase agent network density in areas affected by displacement, and strengthen consumer protection awareness at the community level. The roadmap suggested measures that ensure FSPs have effective complaint-handling and dispute resolution mechanisms.

NGOs and FinTechs are vital in order to promote trust, deliver effective localized financial education, and codesign community-centric and relevant financial solutions.

- Financial education: UNCDF’s financial education toolkit for refugees and host communities illustrates that training programs delivered through NGOs, local partners, or mobile platforms help people understand and use services effectively. Despite refugees’ and IDPs’ contextual differences, this toolkit, developed in collaboration with MSC, indicates that building financial literacy increases confidence and reduces exploitation. These training programs can include community-level financial literacy with a comprehensive curriculum that covers budgeting, saving, borrowing, and using digital financial services. These training programs have shown that we need to promote financial literacy initiatives to address systemic trust issues that resonate in local contexts. Simple, SMS-based educational modules and facilitated group training have bridged knowledge gaps, which promote greater confidence and proactive usage. Such efforts, though nascent, can possibly transform financial relationships from fearful transactions into empowered interactions.

Donors play a crucial role by funding pilots that innovate and test new solutions.

- Investment in innovation: 122 million people have already been forcibly displaced. These shocking numbers are expected to rise as climate events become more frequent and severe. Donors should invest strategically in innovative, displacement-focused financial inclusion initiatives. These initiatives include decentralized and locally led financing mechanisms that empower communities. Donors should also support green and inclusive financial policies that target vulnerable groups, and link funds to performance for transparency and impact on resilience.

Way forward

The challenge of financial displacement is urgent, but it can be solved. Governments can adopt inclusive policies and integrate displaced populations into national strategies, while regulators can allow alternative IDs and flexible risk assessments.

In turn, FSPs can design products that meet real needs, rather than focus solely on perceived risks. Technology providers can also extend digital solutions to remote areas and settlements.

Development partners can de-risk investments, fund digital infrastructure, and support blended finance mechanisms. Additionally, civil society can amplify the voices of displaced individuals, provide financial education, and serve as a bridge between communities and FSPs.

Financial displacement strips Asha and those many others of their agency and dignity. Financial inclusion can restore both. The choice is whether we continue with short-term aid or build systems that give displaced persons the tools to become self-reliant and contribute fully to their communities. The latter seems to be the most inclusive and empowers the path forward.