MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

In this podcast, Nicholas Mungai, a financial inclusion expert at MSC, and Albert Bundi, an SME expert at MSC, have an insightful conversation about ways to address youth’s financial needs and overcome barriers to access finance for the youth.

“I am comfortable with basic tech, but when it comes to complex financial platforms, I think many youth still get overwhelmed.”—Maya, a university student

“I do not think so. For me, technology is a tool to find the best deals and opportunities. I use it frequently to manage my business finances and explore financial products that offer value.”—Rizky, a young entrepreneur

A brief discussion with two friends we met during the field study uncovers the varying experiences and levels of ease of many Indonesian youth who navigate technology. Youth is one of Indonesia’s largest and most influential groups. As per the BPS-Statistics Indonesia (Badan Pusat Statistik), Indonesia had 65.81 million people aged between 15-29 years in 2022. This represents 23.9% of the country’s population and 23.7% of the labor force.

Indonesia’s youth landscape offers a fascinating contrast that challenges our assumptions. Some may imagine a generation seamlessly navigating e-wallets, stock investments, crypto assets, and an array of digital financial services (DFS), but the truth is far more complex. Indonesia has an estimated 92% mobile phone ownership and 84% internet penetration among youth. As per the Financial Inclusion Insight Indonesia (2020), youth aged between 18-35 years reported higher use of digital financial services (45.5%) than others between 36-50 years (9.8%).

Yet, MSC’s study found that youth faced demand-side and supply-side constraints in their access to finances. These constraints included limited experience with formal financial services, lack of adequate collateral, and being perceived as a higher-risk borrower due to the absence of collateral security.

Indonesia’s digital gambling and crypto challenge

As per recent reports from Indonesia’s Financial Transaction Reports and Analysis Center (Pusat Pelaporan dan Analisis Transaksi Keuangan (PPATK)), online gamblers lost IDR 200 trillion (USD 12.5 billion) between 2017 and 2022. 78% of the 2.7 million online gamblers identified by the PPATK belong to the low-income group. They include youth who struggle to make ends meet on less than IDR 100,000 (USD 6.5) daily.

On the other side, Indonesia’s Commodity Futures Trading Regulatory Agency (Badan Pengawas Perdagangan Berjangka Komoditi or Bappebti) reported that 17 million Indonesians invested in cryptocurrency, a high-risk investment instrument of digital coins. Around 48% of crypto users are people aged between 18 to 35. While cryptocurrency has promised wealth, it has also brought some adverse outcomes and revealed that even young people who are good with technology can get caught up in systems that lead to adverse outcomes. OJK reported that the losses incurred by the public due to cryptocurrency-related scams and illegal robo-trading practices reached IDR 6.5 trillion (USD 400 million) in 2021.

Diversity beneath the surface

The Indonesian government introduced the “one student, one bank account policy” (KEJAR) specifically for young students to ensure access to a bank account. OJK also designed two products, Simpanan Pelajar (SIMPEL) and Tabungan mahasiswa dan pemuda (SiMuda), for providers to implement this policy. Financial literacy and readiness vary among youth. This, coupled with different levels of technological proficiency, hinders some youth when they attempt to open and operate a bank account.

One end of the spectrum has a group of youth who are not entirely tech-savvy. These individuals mostly rely on physical cash transactions, are unsure about digital platforms, and may even invest in traditional assets, such as livestock. They find comfort in the familiarity of physical currency and approach digital platforms cautiously. Conversely, Indonesia also has a group of digitally adept youth who embrace advanced financial practices. Our study testifies to this gap. Youth in Java prefer debit cards (48%) and electronic money (35%) transactions, the highest level across all islands. On the other hand, 93% of Sulawesi youth still prefer to transact in cash.

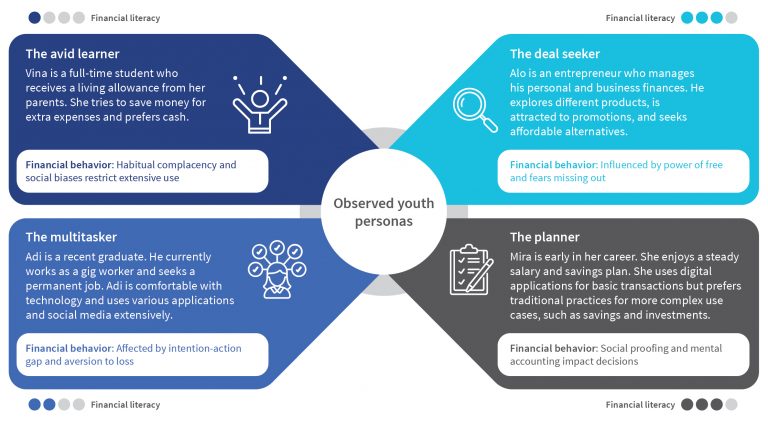

Exploring youth: Meet the four personas

We identified four different personas after in-depth discussions with more than 100 youth in six locations across island groups. Each persona had a unique approach to how they manage finances and embrace digital advancements. These personas embody the diverse characteristics and knowledge that define Indonesian youth.

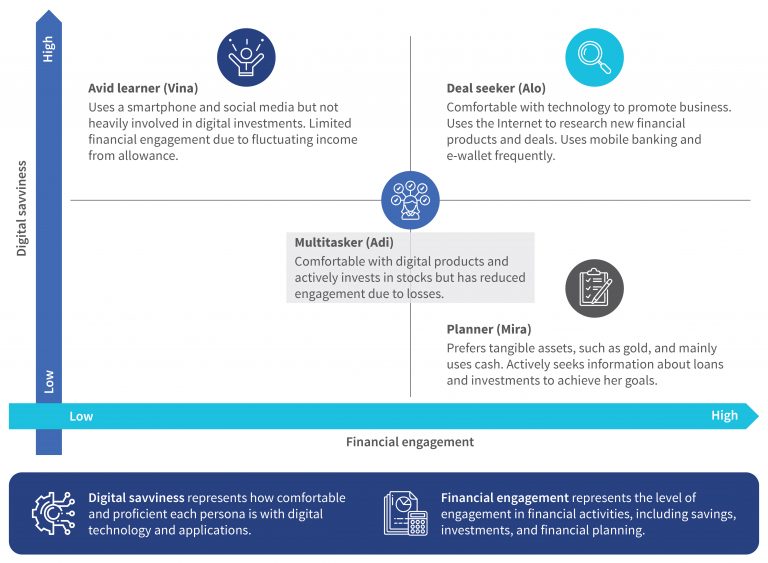

Let us examine where each persona falls within our digital savviness and financial engagement matrix. This matrix helps us understand how comfortable they are with technology and their involvement level in financial activities.

Translating personas into effective policies

Our exploration into the diverse youth personas reveals the complex financial landscape of Indonesian youth. These insights are valuable for policymakers to establish comprehensive policies and interventions based on the personas. The following recommendations can help policymakers serve all youth personas effectively:

Develop comprehensive digital financial literacy programs tailored to Indonesian youth. Despite increased investment among youth, 78% lack fundamental financial and investment services knowledge, which highlights the necessity for comprehensive financial education. As part of this initiative, policymakers and stakeholders should establish robust monitoring and evaluation mechanisms to track financial literacy progress. MSC underscores the importance of the shift from limited-impact traditional methods to a product-centric learning approach that uses experiential and peer learning delivered in “teachable moments.” Furthermore, we can also use influencers to deliver small financial lessons to youth. Each persona could get tailored features to increase engagement:

The planner: Develop simplified digital financial education materials that align with traditional practices. Offer personalized financial literacy sessions that focus on tangible asset investments, such as gold. Provide user-friendly digital platforms with easy access to key product information;

The deal seeker: Create interactive and gamified digital financial literacy content to engage this persona. Offer budgeting and financial planning apps with customization features to cater to their fluctuating income patterns. Collaborate with influencers to promote financial education on social media platforms;

The avid learner: Establish online courses and webinars that cater to educational goals. Provide youth-centric financial education content on platforms they commonly use. Emphasize the importance of goal-oriented savings and investments in their learning journey;

The multitasker: Partner with popular tech platforms to deliver bite-sized financial literacy content. Offer educational content through apps they frequently use. Implement referral programs that encourage them to share financial knowledge with peers. Ensure that financial information is easily accessible via digital channels they prefer.

Strengthen data protection regulations and ensure transparent communication in financial interactions. MSC emphasizes strong data protection to build trust and safeguard personal and financial data. This will benefit all personas who use digital financial services.

Encourage the use of e-KYC to streamline onboarding processes for youth. Policymakers can tailor this policy for each persona. For example, Mira, the planner who values simplicity and traditional practices, should receive e-KYC through a trusted financial institution with physical branches. Meanwhile, Adi, the multitasker, can benefit from e-KYC integrated into the platform he already uses, such as ride-sharing or delivery apps, to complement his fast-paced lifestyle.

Similarly, financial service providers must use a systematic approach to develop products for youth. MSC had previously identified six aspects of youth-targeted product development. Based on this research that focuses on behaviors and personas, they can also develop tailored products for each persona:

The planner: Recognize their inclination toward traditional practices and easy product access even for complex financial requirements. This suggests the need for streamlined, user-friendly interfaces in digital platforms. Offer concise “key fact statements” on products to appeal to this group and align with their preference for simplicity. Products, such as gold savings, also resonate better with this youth segment.

The deal seeker: This group’s pursuit of affordability and value indicates a prime opportunity for financial institutions to provide flexible solutions that cater to fluctuating income patterns. Develop products with features that allow customization to resonate well with this segment, such as adjustable savings goals or repayment schedules.

The avid learner: Address their preference for goal-oriented savings products. This can involve the development of platforms that allow youth to categorize their savings and visualize progress toward their objectives. Emphasize clear communication through “key fact statements” for engagement with this group.

The multitasker: Given their comfort with technology, suggest the potential for partnerships with different apps and platforms. Collaborations between financial service providers and popular tech platforms can enhance accessibility and reach, which aligns with this persona’s habits. Referrals and timely introduction to products and services through the right behavioral nudges will also increase uptake and use.

The planner, deal seeker, avid learner, and multitasker personas are not just demographic segments. They provide critical information about Indonesian youth’s varied aspirations and challenges. The right behavioral nudges will help increase product usage and promote financial health among Indonesian youth.

MSC has a dedicated team and strategy to continuously engage with stakeholders who serve the youth sector. This blog bases its findings and recommendations on Youth Finsights 2.0, a survey of 2,182 Indonesian youth aged 15-29. MSC and the financial inclusion youth ambassadors of DOKA conducted this survey for the National Strategy for Financial Inclusion (SNKI), with support from the Asian Development Bank. Here is the final report.

Various studies have acknowledged the increasing effects of climate change on the livelihoods of smallholders worldwide. Despite this acknowledgment, only a few studies have quantified the extent of resilience among smallholders.

MSC’s study represents an effort to assess smallholders’ climate resilience with the use of cost-effective survey tools. We anticipate that MSC’s frugal approach will motivate development agencies and private sector entities that work with smallholders to consistently gauge the smallholders’ resilience levels in the face of climate change.

Radha is a 28-year-old homemaker in rural Uttar Pradesh, India. She opened a bank account three years ago based on her husband’s suggestion. Yet she later discovered unexplained deductions. Her account was enrolled in government insurance programs without her knowledge. She stopped using her account as she felt she had little control over her hard-earned money.

Many people like Radha are unaware of financial products and associated terms. This is especially true for low- and moderate-income customers with limited literacy, who are largely “oral” and rely more on word of mouth. Some financial products may seem attractive upfront, but hidden costs in the fine print can erode trust and hinder informed financial choices.

Consumers struggle to compare options and assess financial products’ true value. They are often enticed by low initial fees and left in the dark about hidden costs. This limited knowledge can lead to hasty and uninformed financial choices by customers. As a result, their long-term financial health suffers.

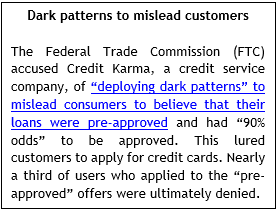

Deceptive designs and hidden pricing techniques commonly used by some financial service providers include:

1. Bundled products and services with the bank account: Most banks bundle insurance programs, such as Pradhan Mantri Suraksha Bima Yojana (PMSBY) and Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) with accounts. This is done without the customers’ awareness of product features or their consent to bundle the services. The LMI customers usually realize it later when they see unexplained deductions from their bank accounts. Most people do not claim benefits as they do not know enough about the product, even when they are eligible and genuinely need them. Since the inception of the PMJJBY and PMSBY programs, only around 0.7 million families out of the 500 million or so enrolled have claimed benefits. Since customers are charged the program’s annual premiums without their informed consent, their trust in the digital financial services ecosystem declines.

2. Account maintenance fees: Banks often advertise free or low-cost savings accounts that may have hidden maintenance fees triggered by factors, such as minimum balance requirements, transaction limits, or inactivity. In India, public and private banks’ average minimum balance requirements range from USD 6 to USD 60 (INR 500-5,000). An account maintenance charge or minimum balance requirement is not inherently wrong, even if it is almost universally unpopular. Yet, banks must ensure that every customer is informed about these policies during the account opening process.

3. ATM subscription and usage fees: Per the RBI guidelines, most banks offer five free withdrawals at their ATMs and three free withdrawals at an out-of-network ATM every month. Any usage beyond these permissible limits is chargeable. After these free withdrawals, the big brick-and-mortar banks charge customers an average of INR 25 (USD 0.25) per transaction for withdrawals from a non-network ATM. However, many customers do not know of such limits and pay fees for ATM withdrawals. All major Indian banks also charge an annual fee to use debit or ATM cards. Yet, customers are not always informed upfront about subscription fees and other processing charges. While the bank websites include information about ATM withdrawal charges in their FAQs, customers often lack a detailed explanation of these terms and conditions, especially when they open their accounts online.

4. Fine print and terms: Financial products, such as loans, insurance, and credit cards, often come with lengthy terms and conditions that contain hidden pricing. For instance, credit card companies offer attractive introductory rates, which increase significantly after the introductory period. Similarly, loans may have hidden fees for early repayment or penalties for late payments. Around two-thirds of banking customers do not fully understand their DFS’s terms and conditions.

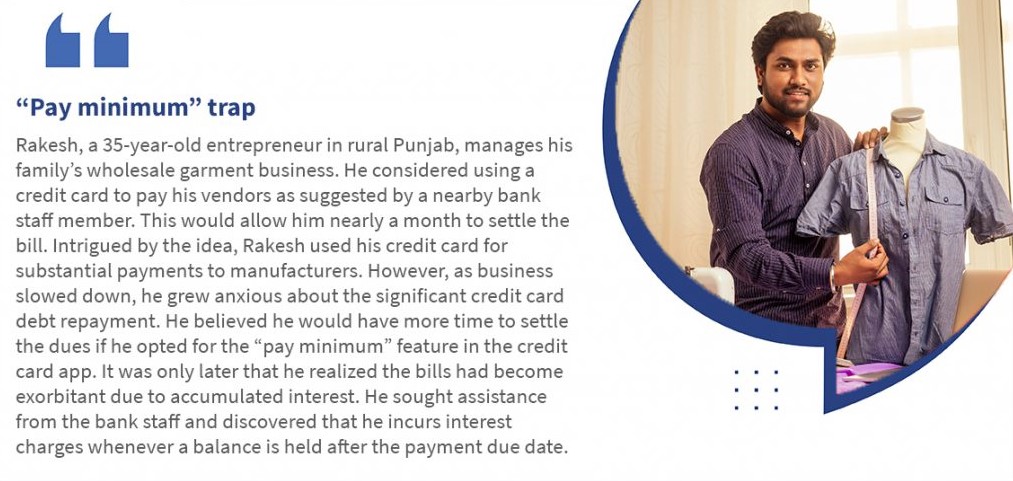

5. Credit options being pushed to customers: MSC’s work in the field has revealed that agents and company representatives push credit cards to customers that initially have zero fees. However, they later charge customers subscription fees. These agents do not provide customers with the important terms and conditions transparently, as most of the information centers around loyalty points and benefits. This lack of information can have serious implications. For instance, if an individual misses the minimum payment due date for a credit card, they may face repercussions depending on the duration of the missed payment. These repercussions could range from interest on the overdue balance and loss of the grace period to a drop in their credit score.

Similarly, “buy now, pay later” (BNPL) extends credit to many consumers who lack access to credit cards. Such payment options incur a higher cost, from 2-6% of the total transaction value, and lead to consumer debt. It often pushes people to buy more items than they can afford, although most consumers see BNPL as a consumer-friendly financial solution. An additional concern is that customers may not grasp the BNPL terms. This may lead to overlooked or delayed payments. A study found that 30% of BNPL users struggled with missed payments, which led to late fees, strained their finances, and harmed their credit scores.

Many others, such as Radha and Rakesh, have fallen prey to hidden pricing associated with digital financial services. This has gradually eroded customers’ trust in the financial ecosystem.

Protecting consumers—a clarion call for policymakers, regulators, and financial service providers: Consumer protection is crucial to ensure transparency and fairness. Policymakers or regulators must implement the following measures to ensure consumers are well-informed before they make financial decisions:

a. Responsible selling through adherence to regulations and compliance: Governments and regulators should mandate financial service providers to summarize essential product details, such as pricing, fees, and terms, in a clear, transparent, and client-friendly manner. They should provide customers with comprehensive information on risks and costs associated with the product. Financial service providers must dedicate a section of their website to customer rights and compensation processes for monetary or non-monetary loss due to implicit consent and ambiguous terms and conditions.

b. Use of standardized templates for easy monitoring: Regulators should conduct audits and market studies and oversee compliance with disclosure rules and consumer protection regulations. They can create uniform templates for financial service providers to ensure the information presented is consistent and clear. These templates would also help in monitoring and evaluation. It would thus allow customers to compare different offerings and make informed choices. Regulators should analyze specific harms posed to vulnerable consumers through market monitoring tools and provide regulatory solutions to mitigate them. For instance, FSD Kenya and Princeton University collected and analyzed tweets relevant to consumer protection and directed toward 29 different financial institutions in Kenya. Otoritas Jasa Keuangan (OJK), Indonesia’s financial services authority, started an initiative to upgrade its consumer protection practices. OJK worked with MSC to develop a chatbot and a consumer protection portal, Aplikasi Portal Perlindungan Konsumen (APPK). Both enabled quick and automated registrations to process these complaints efficiently. The chatbot channel and email response system received an average of 51,000 complaints monthly.

c. Promote technology and innovation for customer education: Customers’ education on financial products, services, and associated costs is essential. Technology, such as financial apps and tools, can enhance customer awareness, help them monitor their financial activities, and facilitate recourse in case of discrepancies. Countries such as China, Colombia, and Singapore have created platforms to encourage data sharing under regulated conditions to help consumers monitor their financial activities and facilitate recourse if they feel deceived. In July 2020, Bangko Sentral ng Pilipinas (BSP) launched a consumer assistance chatbot, BSP Online Buddy. It allows consumers to file complaints against BSP-supervised financial institutions through simple chat messages. It provides a convenient and user-friendly platform for consumers to seek resolution.

d. Publish transparency reports: The International Monetary Fund (IMF) has crafted a Central Bank Transparency Code (CBTC). It emphasizes the need for heightened transparency and accountability to uphold public backing for central banks and their stakeholders. IMF successfully piloted the first evaluations through its CBTC and reported that some banks, such as the Bank of Canada and the Central Bank of Chile, have already changed their frameworks. This is crucial to preserve independence and bolster policy effectiveness. Similar efforts by regulators can enhance transparency among financial services. Regulators should mandate publishing transparency reports on hidden pricing and corresponding compensatory actions taken by financial service providers. These reports should have the number of complaints lodged in the bank’s system and with the ombudsperson and the bank’s comprehensive response to each registered complaint.

Such recommendations can protect consumers from financial products and services with unclear terms, such as hidden fees, to enhance consumer trust in the financial system.

A transformation is underway in rural Indonesia. Women’s cooperatives have entered the agent business, defied social norms, and paved the way for financial empowerment for cooperative members and the broader women’s community. MSC partnered with PEKKA and BRI to support the digital transformation of three women’s cooperative agents in Tangerang, Karawang, and Bantul through the Women Digital Ambassador (WDA) project.

This blog is the third under the WDA project. The first assessed whether women’s cooperatives are ready for digital transformation. The second blog analyzed the transactions women agents conducted and the income they derived. This blog uses a gender-focused approach to highlight ways to address women’s diverse challenges in the agent business and thus increase their client base and income. We also emphasize the significance of female agents as they improve their community’s reception toward banking services and suggest strategies to expand their presence in rural Indonesia.

An examination of female agents’ onboarding experience

Ibu Neng is a 39-year-old high school graduate. Her cooperative’s board entrusted her to operate the BRILink banking agent service in Tangerang’s Kemiri subdistrict. Her journey began with doubts about her ability to run an electronic data capture (EDC) machine and other digital devices. Now, she conducts more than 100 transactions each month. However, she struggles to predict cash flows and manage her liquidity. Her inability to ride a motorcycle also restricts her mobility when she needs to visit bank branches to rebalance her float.

Unlike Ibu Neng, Teh Niar is a 27-year-old tech-savvy woman who graduated from a vocational high school in Karawang district. She is confident in her role as a BRILink agent and often uses YouTube tutorials to learn how to handle various new transactions. Despite competition from a long-established agent in the locality who serves more walk-in customers, she still has a niche market. Niar uses her social networks and cooperative affiliation to serve a distinct set of customers beyond cooperative members. However, she has limited working capital and cannot accept higher-value transactions, which compels her to reject some high-potential customers.

Such stories highlight factors that shape female agents’ realities. These factors include education, social norms, awareness, and the ability and confidence to run an agent outlet. The question is: Will these factors prevent these two female agents from succeeding in their business?

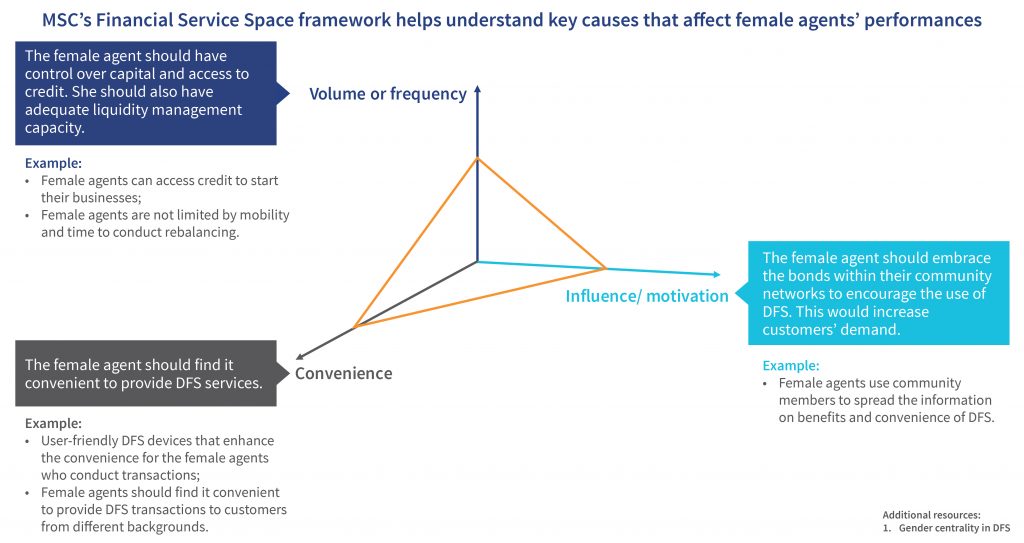

Gender centrality using MSC’s Financial Service Space (FSS) framework

The Financial Service Space (FSS) framework analyzes the environment in which an individual can conduct independent financial transactions. It considers factors, such as transaction volume or frequency, convenience, and influence or motivation. We used this framework to determine how these three aspects affect female agents’ performance.

Toward a path to profitability: How agents can overcome capital shortage and improve their liquidity management capabilities

The path to profitability is difficult for female cooperative agents, particularly since they have limited control over capital and liquidity management. They are expected to kickstart their ventures with modest initial capital. The capital usually starts small and increases gradually based on the cooperative’s financial stability. Their challenges are compounded by a lack of familiarity with the projection and management of the agent business’s variable cash flows and mobility-related difficulties in rebalancing.

Profitable digital financial service (DFS) transactions require higher working capital.

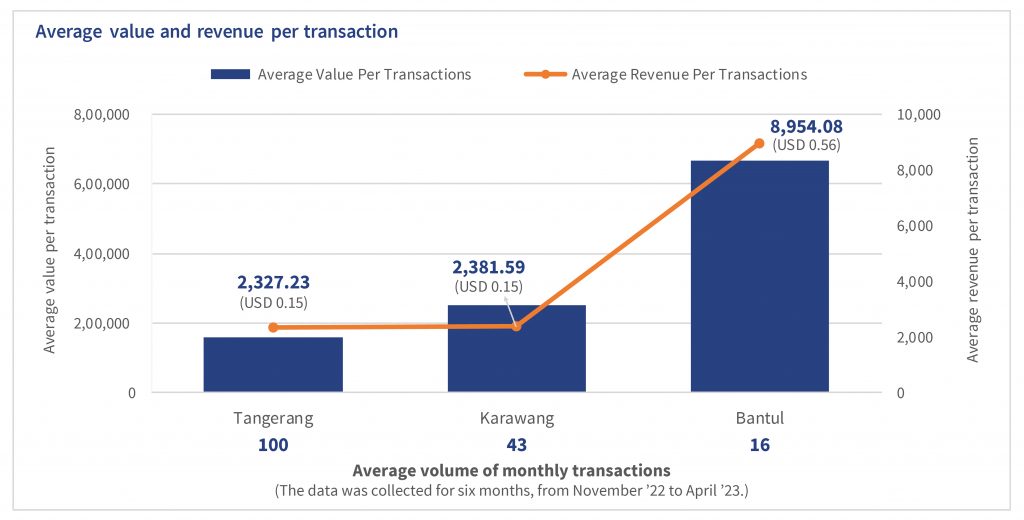

A comparison of the performance of three agents in Tangerang, Karawang, and Bantul reveals that Tangerang leads in transaction volumes, whereas Bantul excels in profitability per transaction. Conversely, despite lower monthly transaction values, Bantul stands out in profitability thanks to higher commissions per transaction. Bantul serves more inter-bank money transfers and cash withdrawals, which earn agents a higher gross commission, (IDR 15,000-20,000 or ~USD 1-1.5 per transaction) before a 50% deduction for bank fees.

Agents can build a sustainable business if encouraged to achieve higher transaction volumes and conduct more profitable transactions. BRI’s recent policy change aligns with this principle as it has shifted from “number-of-transaction-based” to “commission-based” targets. However, this presents an ongoing challenge because these agents have limited capital, which requires them to rebalance more frequently—and thus travel to bank branches. This leads to additional operational expenses and opportunity costs for agents as they strive to meet customers’ demands.

Variable demand: A liquidity puzzle

Balancing cash and e-float is also a challenge because of unpredictable demand. Moreover, female agents struggle to understand transaction patterns and financial flows, which means they struggle to predict liquidity needs and are forced to undertake irregular rebalancing trips.

A better solution could address the liquidity challenges and improve sustainability for new agents. Besides the provision of rigorous training on liquidity management, an automated system that monitors and forecasts future demand would simplify rebalancing. Indonesian financial service providers may consider such a solution. Nevertheless, the country’s agents crucially need an accessible system that addresses the diverse barriers they encounter.

Convenience for both customers and agents

The integration of women’s cooperatives with agent banking services brings DFS closer to the community. Unlike the conventional agent setting, customers, that is, cooperative members, can access DFS anytime and anywhere by contacting these female agents via phone or WhatsApp. The female agents can collect cash and payments later on through group meetings or visits to neighbors. This fosters familiarity with DFS for rural women who have long relied on cash.

However, agents do not experience the same level of convenience as customers. Female agents often struggle as they adapt to operational, technological, and financial challenges when they start the agent business. While they encounter difficulties in DFS transactions, agents do not rely solely on bank field officers. Instead, agents prefer YouTube videos and WhatsApp BRILInk agent groups as their primary sources for quick solutions to technical challenges. They typically approach bank field officers for more complex technological issues related to the device. Despite occasional struggles, these experiences have bolstered their confidence as they handle a broader spectrum of financial transactions.

Community networks can influence people and spread the word far and wide.

Agents offer incentives to cooperative members who refer DFS to new customers to boost transaction demand and sustain the business. These cooperative members have become enthusiastic advocates for DFS. They actively promote the variety and advantages of DFS and strongly emphasize the convenience of using agent services. Consequently, they have grown into influential marketing agents whose advocacy reaches their families, friends, neighbors, and even those not part of the cooperative. These female cooperative agents play a pivotal role as they enhance financial literacy and foster digital confidence within their communities through established networks and trust.

The criteria for success among female agents’ should extend beyond revenue metrics. While they struggle to meet specific revenue targets, these agents possess a unique ability to influence customers to explore new products and services, which fosters customer loyalty. Research reveals that female customers exhibit distinctive decision-making behaviors when they consider a new product or service. They value peers’ opinions on financial products, which emphasizes the role community networks play to shape their choices.

The development of a gender-intentional financial ecosystem needs collective effort.

In conclusion, if stakeholders overlook women’s empowerment in financial inclusion, it will lead to a significant lost opportunity for both service providers and society. Only if we recognize and address the diverse challenges women encounter in the agent business can we pave the way for a more equitable and economically prosperous future.

FPCs and derivatives markets: Contrasting experiences from the field

In May 2022, Saharsa JEEViKA Mahila Producer Company entered into maize September futures for USD 306 per metric ton (MT) for 800 MTs of maize. It completed the transaction and earned a margin of 4% against a 0.5-1% margin it would have received in the spot market in May. The FPC had sufficient working capital to hold the produce till September and could continue its other business activities.

During the same period, FPC ABC of Begusarai and FPC XYZ of Muzaffarpur also wanted to sell their maize produce on the NCDEX platform. FPC ABC deposited its produce at the exchange-designated warehouse and waited to sell its products, as the platform had no buyers available. It did not get any buyers even after it waited 15 days, so it finally sold its products in the local market. This happened because the maize futures contract was still relatively illiquid. The exchange did not have enough buyers and sellers.

In contrast, FPC XYZ took a sell position when it deposited its maize at the warehouse. However, it failed quality control and was rejected. The FPC had to sell its maize in the local market, but it had to buy the same quantity on the exchange platform to leave its sell position. At the time of exit, the price had increased, which resulted in a loss for the FPC.

The above examples and MSC’s experience suggest that FPCs must address and mitigate key challenges to achieve widespread adoption. Let us discuss these challenges in detail.

1. Low awareness and technical knowledge of derivatives trading: FPC managers and board members should thoroughly understand the benefits and risks of derivatives trading. However, derivatives trading is complex and requires a sound understanding of its workings, each party’s expectations, and extensive documentation. NCDEX and SEBI conduct many programs to demystify derivatives trading for FPC management. However, more efforts are required. FPC-promoting institutions and nodal agencies, such as the Small Farmers Agri-business Consortium (SFAC) and National Rural Livelihoods Mission (NRLM), should make a concerted effort to scale up such awareness programs.

2. Inadequate working capital: Participation in the exchange platform requires significant working capital, as explained below:

a. Margin call and mark to market: Participants who want to engage in derivatives trading must deposit margin money, typically 10-12% of the total trade value. This amount remains blocked until the position is closed or settled with delivery. The other reason for the working capital requirement is the “mark to market” method to calculate the security’s fair value. Mark to Market (MTM) in a futures contract is the daily settlement of profit and losses that arise due to the change in the security’s market value until it is held.

The price movements of these contracts are monitored daily, and buyers and sellers pay or receive margins on their futures contracts, which the exchange executes. When the price of the futures drops, the exchange will withdraw the corresponding amount of money from the buyers’ margin account and deposit it in the sellers’ margin account to compensate for the price change. Similarly, when the futures contract price rises, the gains will be deposited into the buyer’s account, and the seller will lose this money in their account. So, FPCs must be ready to deposit money into their margin account to compensate for any price increases. This leads to additional working capital requirement from the FPC.

b. Capital for the duration of stock holding and logistics: The full delivery process of the material on the exchange takes at least 20 to 35 days. FPCs must crucially arrange sufficient working capital to buy materials and meet exchange and warehouse-level expenses. However, many FPCs lack the requisite working capital, which naturally discourages their participation in this ecosystem.

Only FPCs that meet these working capital requirements can engage in the derivatives markets. So, those with limited liquidity are excluded.

3. Stringent quality requirements: The exchange’s quality parameters are strict. FPCs risk rejection of produce at the exchange warehouse if their product does not meet the warehouse quality parameters. To prevent this, FPCs should develop internal capabilities to ensure high-quality procurement from its members and invest to educate members on quality parameters.

For example, JEEViKA FPCs have invested in training all their field team to use moisture meters. In fact, all the procurement teams and the Board of Directors (BoDs) have been given moisture meters during maize procurement. The FPCs also send advisories to farmers on simple post-harvest techniques, such as drying, storage, sorting, and grading, among others, to reduce issues of fungus and weevil-infested grains. Similarly, the FPCs conduct regular training for field teams and BoDs on measuring hector-liter.

4. High premium on options: The premium required to buy options contracts can be as high as 6-7% of the total trade value, higher than margins usually available in the spot market. The Securities and Exchange Board of India (SEBI) and some private sector players, such as Bayer Crop Science, have provided subsidies to encourage FPCs to participate. However, these subsidies are not permanent and available for a limited time. Policymakers play a role to subsidize the premium cost for FPCs to enable suitable price hedging. Suggestions have also emerged to replace the MSP (minimum support price) with put options for farmers. Philanthropic capital can also subsidize the premiums to buy options for qualified and well-functioning FPCs.

5. Liquidity of trades on the commodity exchanges: The futures market’s success is determined by liquidity—the frequency of trades in a specific commodity and the number of market participants trading in that commodity. FPCs or other market participants cannot enter or exit the market at will if the liquidity is low. Moreover, FPCs may also run the risk of market manipulation. Liquidity improvement will require government support to encourage derivatives trading across a slew of commodities and give confidence to market participants.

Conclusion

As highlighted in our previous blog, derivatives trading is an important tool for mature FPCs to de-risk themselves from price risks and ensure better market linkages. Systematic and structured capacity building of FPC management, subsidizing some transaction costs associated with trading, and consistent policy support could help increase the penetration of derivative trading among FPCs.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.

5. Credit options being pushed to customers: MSC’s work in the field has revealed that agents and company representatives push credit cards to customers that initially have zero fees. However, they later charge customers subscription fees. These agents do not provide customers with the important terms and conditions transparently, as most of the information centers around

5. Credit options being pushed to customers: MSC’s work in the field has revealed that agents and company representatives push credit cards to customers that initially have zero fees. However, they later charge customers subscription fees. These agents do not provide customers with the important terms and conditions transparently, as most of the information centers around