Yeredeme Group (GYD), which means “self-help groups” (SHG) in Bambara, is an innovative methodology for rural women’s empowerment based on self-management and peer-learning activities. Its implementation was possible thanks to a technical partnership between an Indian NGO, the Manjari Foundation, and the Malian NGO, CAMIDE. The model integrates livelihood activities development, financial intermediation, women’s empowerment, and community development.

With the Yeredeme methodology, more than 2,500 women from 19 villages in the Logo municipality in Mali have been organized into 189 SHGs. These women were granted microcredits regularly in the SHGs. In addition, they also benefited from larger refinancing loans disbursed by Benso Jamanu, the financial branch of CAMIDE.

SCBF, the Swiss Capacity Building Facility, is an organization that provides technical assistance to financial services providers to help them build the expertise needed to develop client-centric financial products. With SCBF’s support, Benso et CAMIDE has extended the Yeredeme methodology in two additional rural municipalities (Sero Diamanou and Liberte Dembaya).

The goal is to reach 5,000 women (households) with the Yeredeme groups methodology by creating the following grassroots women’s institutions: 320 SHGs in 40 village organizations and two federations. As Yeredeme groups are rooted in self-management, peer-learning activities will focus on building the capacity of women whose role will be to support the setup, management, and development of 60 CRPs (community resource persons), 320 Sebennikela (group accounting secretaries) and 40 control officers.

The SCBF commissioned this study to understand the Yeredeme methodology’s effects on clients.

India’s farmers have had a long history of struggle. For decades, they have battled a multitude of agricultural challenges, such as fragmented landholding, numerous intermediaries, and low value addition. In response, the country has actively promoted farmer producer organizations (FPOs) as a solution. FPOs intend to address these serious issues through the aggregation of demand for high-quality inputs, credit, and technologies and the aggregation of outputs to improve smallholder farmers’ market access.

Yet despite these efforts, major processors and output purchasing companies hesitate to engage directly with FPOs. This blog explains the options available for FPOs to trade with institutional buyers and the on-ground issues FPOs must overcome to establish better market linkages. We limit the discussion to cereals and grains, which constitute most of India’s agricultural production.

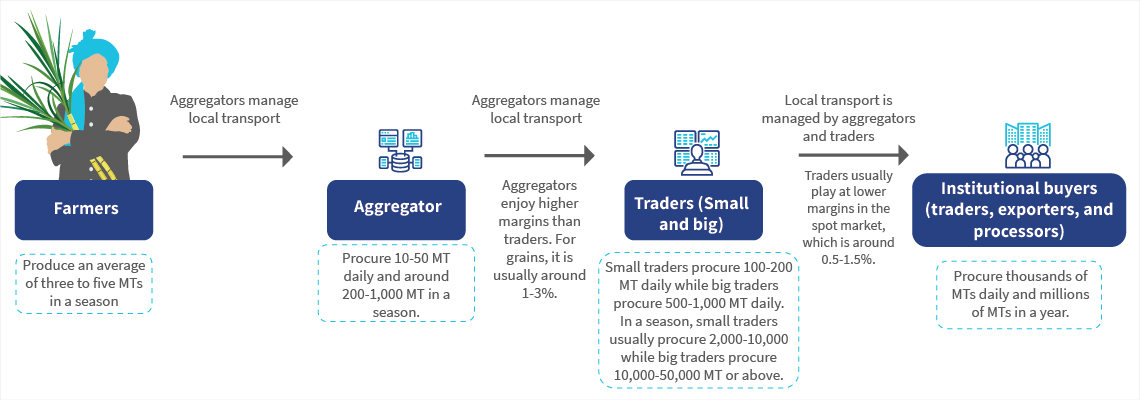

The intermediaries, such as aggregators and traders, are critical in the conversion of small amounts of 2 to 5 MTs into hundreds of thousands of MTs as required by the large buyers within a short period of 30-45 days. Throughout this process, the material is graded into different qualities, which allows the buyer to buy the desired grade. The following provides a generalized representation of participants in the commodity value chain.

Figure 1: Agriculture commodity value chain—from farmer to institutional buyer

What avenues do FPOs have to engage with large institutional buyers?

FPOs often act as substitutes for aggregators and small traders. A primary motivation behind FPOs’ formation is to bypass intermediaries and establish direct trading channels with food processors and other significant institutional firms. In this section, we have listed different trading approaches FPOs can take to deal with large buyers:

1. Daily supply based on daily prices: FPOs can engage in daily commodity trading if they receive prices every morning. Large institutional buyers typically have designated locations, such as warehouses, for delivery during the harvesting season. Under this method, the FPO receives daily prices from the buyer, factors in operational expenses, and determines the procurement price for the day. Interested farmers make deals with the FPO, which procures and delivers the produce to the buyer’s delivery center. This process minimizes FPOs’ price risk as it treats each day’s material as an independent trade. However, operational efficiency is crucial to maintain sufficient margins. For example, the FPO should plan the procurement quantity from farmers in a way that it can fill the trucks deployed. If the trucks’ space is not filled, the produce’s transport cost will increase and eat into the margins. Similarly, the quality should be good enough to ensure the trucks are accepted with no deductions at the buyers’ warehouse.

2. Large quantity trades with fixed terms (“sauda”): Another method involves the execution of large trades at a single price point within a limited delivery period, commonly referred to as “sauda.” Large institutional buyers widely adopt this method. It entails an agreed-upon quantity, price, and quality to be delivered within a fixed time. While this method allows for slightly better prices and provides a fixed price over a specific duration, it comes with risks. FPOs must meet their commitments to avoid fines or jeopardizing future trades, which makes operational maturity crucial.

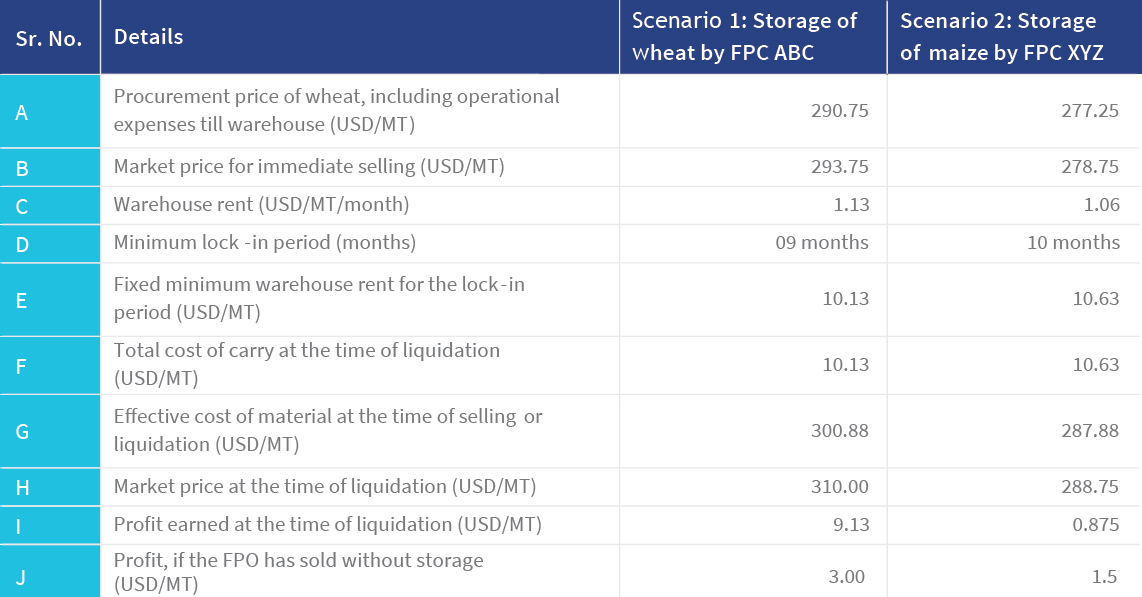

3. Storage of commodities to sell in the future: The usage of accredited warehouses for storage with the intention of future sales is often suggested to secure higher prices. However, our practical experience reveals that this approach is also the most precarious. Commodities’ storage introduces additional expenses, which include costs of carry or storage, susceptibility to market price volatility, shrinkage or storage losses, and heightened financing requirements. Professional warehouses always come with a mandatory minimum lock-in period, which significantly increases costs. This may result in FPOs achieving minimal profit margins despite price appreciation. Market price risks, influenced by global supply chains and external factors, further compound the challenges.

A comparative analysis in the table below illustrates two scenarios: In Scenario 1, FPO ABC stored wheat for nine months, and in Scenario 2, FPO XYZ stored maize for 10 months. While FPO ABC realized a profit of USD 3/MT, FPO XYZ’s profit was only USD 0.87/MT. Notably, despite the maize price appreciation, FPO XYZ experienced a reduction in profit margins due to associated storage costs. Both FPOs had internal financing. If external credit was involved, the interest rate during the storage period would have further eroded the FPOs’ profit margin.

Table 1: Economics of storage of commodities and sales for two FPOs

Despite these risks, storage remains an important avenue for market linkage in regions without a significant presence of large buyers. This requires the produce to be transported to distant locations for sale to a large institutional buyer. FPOs must constantly check the arbitrage in prices available and the various costs associated with storage.

4. Delivery to distant locations or interstate transport: Large buyers often offer better rates closer to their processing units, which may be located far from the FPOs or in other states. FPOs must transport produce to these distant locations in such cases. The main risk involves quality checks at the designated delivery location. If the quality does not meet expectations, the price received may decrease, or the material could be rejected. This would lead to distress sales in unfamiliar geographies. A reliable network with transport agencies is crucial to tap into this opportunity.

What challenges must FPOs overcome to establish efficient market linkages?

Ensuring ruthless quality control: FPOs need to compete with aggregators and small traders through efficient procurement of the right quality at the right price. Educating farmer members in advance is crucial. Although the FPO belongs to them, it cannot compromise on the prevailing quality standards in the market. The price the FPO offers for a specific quality must align with market practices.

Identification of different buyers for different quality: As social organizations, FPOs are obligated to buy different grades from their member farmers. Therefore, FPOs must identify various buyers for different quality grades. The FPO, Aaranyak Agri-Producer Company Limited (AAPCL), Purnea, has built relationships with many maize buyers. These include poultry feed manufacturers, who require higher quality produce; starch manufacturers, who are fine with slightly lower quality maize; and local producers of industrial ethanol, who are not quality conscious.

Creation of suitable structures to scale: FPOs struggle to scale up as they face operational challenges, such as maintenance of procurement quality, arrangement of cost-effective logistics, and proper documentation for procurement and sales. Traditional field staff may not be a sufficient operational structure for scaling. JEEViKA-promoted FPOs have addressed this through a network of agriculture entrepreneurs (AEs). These AEs are educated youth in the villages and provide aggregation services to FPOs on a commission basis, which is linked to the quantity and quality of procurement. For example, Aaranyak FPC in Purnea collaborates with 12-14 AEs every season. This has helped the FPO increase annual maize procurement from 1,200 MT in 2020 to 4,150 MT in 2023. This approach has proven effective to enhance the FPO operations’ scale.

In conclusion, the complexities of market linkages for farmer producer organizations (FPOs) in India reveal both challenges and opportunities. We must appreciate and respect the current market structure and rules as the nation actively promotes FPOs to surmount structural issues in agriculture marketing. FPOs must overcome challenges, such as quality control, identification of diverse buyers, and creation of scalable structures, to thrive in the evolving agricultural landscape.

In the evolving landscape of AI for agriculture, the future lies in hyper-personalization and multimodal models. AI will increasingly use diverse data sources, which include images and videos, to offer personalized solutions. The focus is on enhancing localization, predicting trends, and addressing challenges, such as climate change and market fluctuations. As AI becomes more integrated, institutions should embrace its transformative potential to benefit smallholder farmers, ensure the services are tailored to their unique needs, and contribute to a more sustainable and resilient agriculture ecosystem.

Our recent work in Bihar highlighted climate change’s persistent impact, which led to disruptions from heat waves, droughts, and floods over the past decade. This has led to a significant increase in pest infestations for farmers. Bangladesh also observed similar challlenges where extreme heat and saline land from previous cyclones complicated land preparation. Erratic rainfall delayed and dried seeds, followed by torrential downpours that flooded and washed away crops. Cyclone Amphan further worsened conditions. It wiped out standing crops and introduced saline water, which made the soil less fertile. We worked with CGAP in Bangladesh and DECODIS in Nigeria on a macro scale and found climate change’s adverse effects on livelihood capitals. Now, in collaboration with the Government of India, Agristack, and the Government of Bihar, we intend to address these challenges by integrating a digital farmer services platform, which uses technology to enhance agricultural production, financing, and market linkages.

The first note in this series of notes—Insights note-Edition 1—covers aspects related to the business finances of informal enterprises (IEs) and how external factors affect them. It also unpacks informal enterprises’ adoption of digital technology and how they use it in business.

The note discusses examples from MSC’s Financial Diaries research on IEs to validate the findings. It also provides recommendations for policymakers and financial service providers to address IEs’ challenges.

This note uses data from surveys, daily diaries data, and qualitative interviews to unpack how female business owners in Bangladesh use digital platforms for business and examine their challenges. This note is a part of the ‘The Big Smalls of Bangladesh’ series under the Women’s Business Diaries project in Bangladesh.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.