The Self-Help Group (SHG) Model in India has been instrumental in improving the financial health of households. It also empowers women to participate actively in household financial decisions. However, most SHG members have limited digital and financial literacy. Therefore, they do not qualify for the parameters defined by the government for SHGs to avail of loans. MSC studied the SHG solution, Money Purse, developed by Anniyam Payment Solutions, to digitize the SHG value chain.

GoGullak- Making personal finance management easier

This blog looks at a startup called GoGullak, part of the Financial Inclusion Lab accelerator program, which is supported by some of the largest philanthropic organizations across the world—Bill & Melinda Gates Foundation, J.P. Morgan, Michael & Susan Dell Foundation, MetLife Foundation, and Omidyar Network.

India is home to ~450 million blue-collar workers, most of whom earn a decent income but struggle to save adequately due to lack of appropriate tools. Piyush is one of them. He works in a factory in Delhi and earns INR 20,000-30,000 (USD 244-365) monthly, depending on the incentives he receives. He often struggles to manage his finances and resorts to personal loans for exigencies. Once he pays off his EMI and other necessary expenses, such as school fees and rent, he struggles to manage his remaining expenses.

Piyush knows that budgeting and tracking his expenses would help, but he finds it challenging to follow through every month. He tried a few ledger-keeping applications, but these did not suit his needs as they all worked after expenses had been incurred and did not help in decision-making when making payments. He continued to struggle to pay monthly EMI or save and invest to build an emergency fund.

Millions like Piyush face fail to manage their finances due to a lack of knowledge about financial planning and limited access to appropriate tools through which they can plan. This struck a chord with former engineers Avinash, Yashraj, and Yash —the co-founders of GoGullak.

Since their college days, the trio has been passionate about building a scalable product that could create real social impact. Initially, they worked on a financial education solution for investing in stock markets but quickly realized that financial management is a bigger cause of concern among India’s middle-income investors. Most users used several ledger-keeping apps to manage their finances but struggled to save enough money for investments. This led them to conceptualize GoGullak in February 2022, christening their venture based on the Hindi word for traditional earthenware coin boxes children use to save small change: “gullak.”

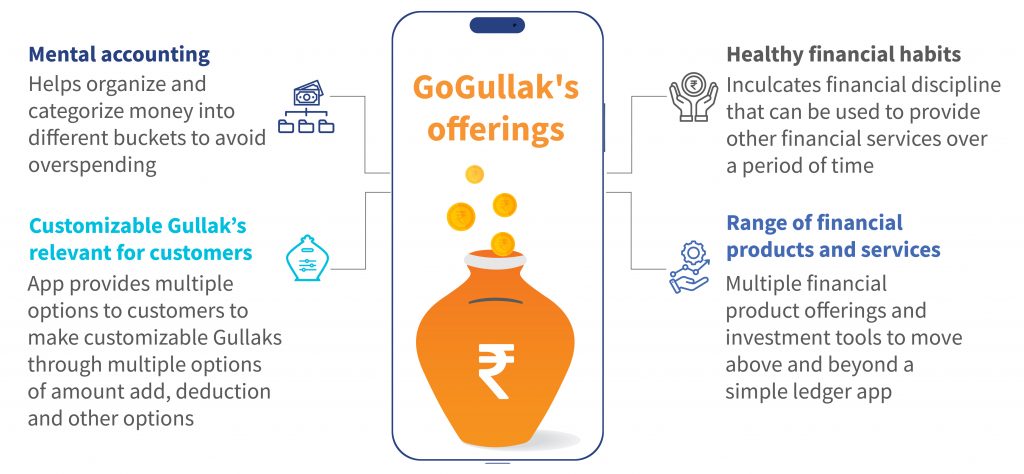

The GoGullak pitch: Building better financial habits through the concept of mental accounting

GoGullak is an aspiring neo-banking platform that helps users align their financial goals through real-time budgeting like an orchestrated finance platform that makes financial management as easy as arranging files on a computer. GoGullak uses the principles of mental accounting, popularized by behavioral scientist and Nobel laureate Richard Thaler as a way people organize and categorize money as per its intended purpose. This helps users better understand their spending habits and make more informed financial decisions. Users can park their money for specific purposes in separate micro-containers in their accounts, just like physical Gullaks.

A major problem that users like Piyush face is the inability to control their spending when all of their money looks the same in a single digital account, even though each rupee may have a different purpose.

To solve this problem, GoGullak allows users to save money for different categories, such as rent, bike expenses, subscriptions, food, and EMIs on the app. Unlike a typical savings account in a bank, GoGullak helps users to create labeled micro-containers, with each gullak acting as a sub-account on top of a single bank account. This allows users to budget their monthly expenses for each category on the app. The users pay through the gullaks created for each category on the app instead of conducting a post-facto analysis of the expenses incurred in the month. Users can club similar spending categories or earnings and manage them individually through these gullaks.

GoGullak offers complete customization of each gullak to each individual’s needs and offers them the flexibility to budget, track, and pay conveniently through a single platform.

An ecosystem approach to build the business model

The founders understood that if they could create value for users when they sought to plan, store their money, and pay through GoGullak, they could uncover an opportunity to monetize the platform. They could provide users with suitable products, such as mutual funds, insurance, white and electronic goods with save now, buy later (SNBL- where customers can save in installments to buy products in future) while offering them good consumer brand deals. In the process, the founders want to create an ecosystem where consumer brands and financial institutions can use transaction data to offer GoGullak customers tailored offerings.

GoGullak’s ecosystem will help users plan, save, invest, and purchase transparently while promoting good financial behavior. “I am focused on building long-term sustainability for the user and GoGullak. Anything bad for users in the short term, even if it is good for GoGullak’s revenue, is not sustainable. GoGullak’s analytics will nudge users to adopt sustainable financial practices and spending through the platform for the long-term,” notes Yash, GoGullak’s co-founder.

GoGullak’s vision is to ensure that users enjoy financial freedom and bring financial discipline back into their lives. This vision resonated with leading financial institutions in the country and has encouraged them to tie up with GoGullak to offer its solution to their customers. GoGullak is currently a part of the Fincluvation program with the India Post Payments Bank (IPPB). Under this IPPB willl leverage GoGullak’s solution for its customers.

Challenges for GoGullak

Automated personal finance management lies at the core of GoGullak’s value proposition. While this is valuable and holds appeal across different customer segments, GoGullak’s product roadmap and promotion will have to ensure that the initial hook of financial management translates into adopting other products like investment, insurance, financial analytics, and SNBL, as these are key revenue sources. In this process, another challenge for GoGullak is to make an intuitive user interface so that users can navigate through various products and features with the least possible friction. Besides these, system integration with banks and other financial institutions to provide a smoother user experience has been a constant challenge for the team.

Support from FI Lab

Under the FI Lab program, MSC helped GoGullak identify its target segments, understand their behavior, and help the founders identify gaps in the app’s UI/UX journey. The research with salaried classes and micro-entrepreneurs revealed pain points in managing their personal finances. It helped identify the key focus areas for GoGullak to build loyalty and retention. The insights helped the startup refocus and target its efforts towards a particular range of income and occupation segments. GoGullak’s proposition resonated the most with these segments and helps them address their pain points efficiently.

The MSC team also helped GoGullak build a B2C and B2B2C GTM strategy and created an implementation roadmap post its launch.

Building financial discipline and a digital future

GoGullak plans to boost its customer reach and performance. As it grows, it will focus on big data and artificial intelligence to build services that will make personal finance management easier for its users. With the vision to make GoGullak universally accessible and helpful, it expects to create an impact on the low- and middle-income segments. In addition, the team is working on creating a voice-based chatbot in the native languages of India to improve the usability of its app for even low-tech savvy persons. “Ultimately, we want to give everyone their financial assistant, which will act as their second brain for personal finance,” says Avinash, the co-founder of GoGullak.

The co-founders believe that by making financial planning and management more accessible and useful to everyone, they can empower people to take control of their financial future and achieve their financial goals.

This blog post is part of a series that covers promising FinTechs that have been making a difference in underserved communities. These startups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative and is co-powered by MSC. #TechForAll, #BuildingForBharat

Kaarigar Mandi: Preserving India’s traditional handmade footwear

Introduction

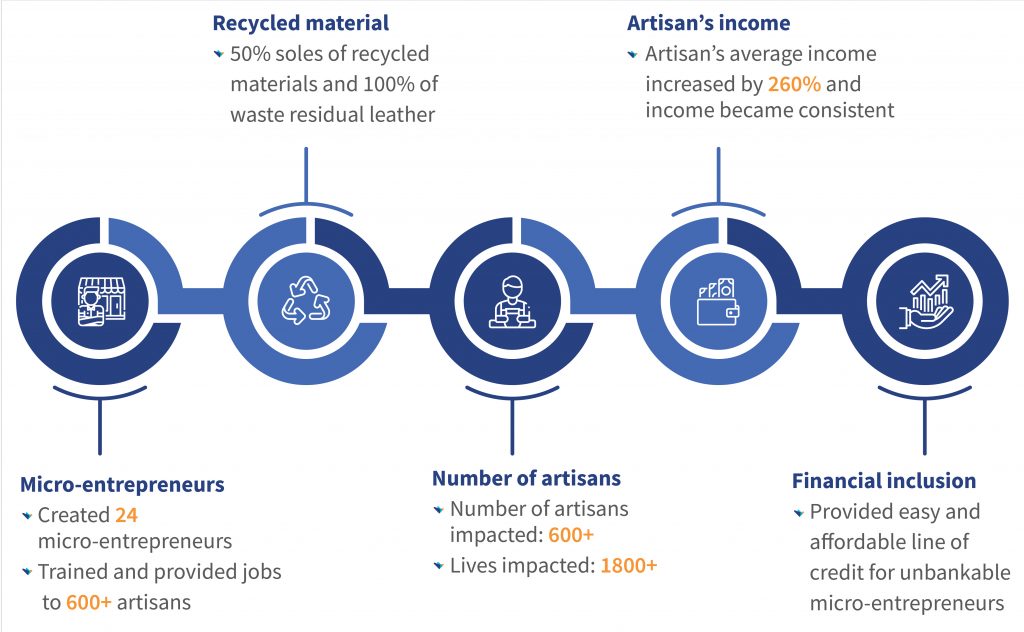

The Indian footwear market employs more than two million footwear artisans and was valued at USD 24 billion in 2022, with an annual growth rate of 6.7%. Approximately 20% of its employees are from Agra, Uttar Pradesh. Agra caters to 65% of the domestic footwear demand of India. However, during COVID-19, almost 70% of the footwear manufacturers shut shop due to inadequate business. This blog looks at Kaarigar Mandi, a footwear startup in Agra, and its effort to preserve traditional handmade footwear manufacturing while securing the livelihood of the footwear artisans.

We spoke to a footwear maker from Agra to understand the problem better. Saurabh is a footwear master artisan who employs six other artisans from his community. He has been struggling ever since several shop owners who sold footwear refused to buy from him. He worked with a bulk footwear buyer. But lately, the buyer has not placed any orders with him. He rued, “Buyers say they do not know me, so they cannot trust me.” The lack of buyers forced Saurabh to explore others to sustain his business. Saurabh is now worried about getting work for himself and the artisans working under him, as no new buyers have been entertaining him.

The graphic below describes different problems Saurabh and other master artisans like him face due to an uncertain business environment.

Kaarigar Mandi is a startup that works with such master artisans. It helps them standardize their production through quality checks, capacity building, and greater transparency in the footwear manufacturing process. This standardization helps them match the needs of bulk footwear buyers. The startup aspires to build an aggregator platform between the artisan community and bulk footwear buyers. It seeks to support the artisan community through raw materials, job stability, timely payments, and linkage to a formal credit ecosystem.

The light bulb moment

Kaarigar Mandi was founded in 2019 Ankit Kumar, Gagan Mukhi, and Dr. Hifza Afaq. Before Kaarigar Mandi, Ankit used to work as an e-commerce consultant for domestic footwear brands in Agra. He met various footwear artisans in the factories during his stint. These artisans owned small handmade footwear manufacturing units. But rapid industrialization in the sector led them to lose their clients and business. During conversations with these artisans, Ankit realized that their footwear craft was high quality. Yet sub-par raw materials and lack of standardization led to low-quality end products.

Kaarigar Mandi was founded in 2019 Ankit Kumar, Gagan Mukhi, and Dr. Hifza Afaq. Before Kaarigar Mandi, Ankit used to work as an e-commerce consultant for domestic footwear brands in Agra. He met various footwear artisans in the factories during his stint. These artisans owned small handmade footwear manufacturing units. But rapid industrialization in the sector led them to lose their clients and business. During conversations with these artisans, Ankit realized that their footwear craft was high quality. Yet sub-par raw materials and lack of standardization led to low-quality end products.

Ankit recognized this fading craft’s potential as a lucrative business venture and founded Kaarigar Mandi as an end-to-end footwear supply chain platform. He changed his focus to offer high-quality products to the artisans to enable them to create superior-quality footwear. He also introduced technology and professionalism to footwear manufacturing in the supply chain. The technology increases standardization and transparency in the supply chain to enable the sale of handmade footwear to bulk buyers and consumer brands.

Ankit brought in his friend Gagan, who had footwear manufacturing experience, as a cofounder. Gagan started to handle the operations and artisans’ relationship with Kaarigar Mandi. Later, his wife, Dr. Hifza, joined the founding team as the technology founder.

Kaarigar Mandi’s milestones so far

The unique pitch

- Kaarigar Mandi facilitates financial support to artisans and connects them with lenders. These lenders can provide easy, low-cost credit to manage the artisans’ capital requirements. One such platform is Credochain, part of the Financial Inclusion (FI) Lab’s earlier cohort.

- Kaarigar Mandi conducts multi-level quality checks to deliver footwear with less than a 1% rejection rate for bulk footwear buyers. Thus, it builds trust among its customers.

Impact on artisans

Kaarigar Mandi works with more than 600 footwear artisans in Agra. These artisans aspire to grow their microenterprises with the startup’s support. They are keen to learn how to manage their businesses efficiently. MSC’s field research highlights how the artisans’ engagement with Kaarigar Mandi has helped them get a steady income and upgrade their skills to make better footwear. Kaarigar Mandi has also partnered with NGOs, such as Ek Pahel in Agra, to train female artisans to make quality footwear and provide them with work to earn additional household income households.

The empathy, affection, and respect Kaarigar Mandi extends to its artisans is the key differentiating factor of its engagement. “My husband is a footwear artisan and was the only breadwinner for the family. Two years back, he got severely ill. My son and I struggled to survive when we met Gagan bhaiya from Kaarigar Mandi. He gave us an instant loan to care for my husband’s illness, trained me to manufacture footwear, and employed my 16-year-old son as an admin support in their office. He has changed our lives and treats us with respect—just like a younger brother,” smiles Shanta, a female footwear artisan.

Roadblocks ahead

Kaarigar Mandi faces two critical roadblocks in its growth journey:

- First, it struggles to retain skilled artisans who often leave the handmade footwear industry when they do not have steady work and seek other roles, such as factory workers or street vendors. As a result, it has to spend more time and money to recruit and train new artisans. Sometimes, it even pays them in advance to cover their weekly or monthly salary before they start work.

The second challenge for Kaarigar Mandi is that the footwear industry in India comprises traditional and close-knit businesses. Large institutions as well as small-scale footwear buyers usually have long-standing relationships with their preferred vendors. These vendors can meet the buyers’ specific needs. Kaarigar Mandi faces resistance as a new entrant in the footwear business.

It had to invest more time and effort to build trust among bulk footwear buyers. In response, Kaarigar Mandi manufactures small batches of footwear in various designs to be used as samples for various institutional buyers. However, while such small-batch manufacturing is essential to create a market for Kaarigar Mandi, the approach negates economies of scale. It is thus not sustainable in the long term.

Support from MSC’s FI Lab

MSC’s FI Lab’s support to Kaarigar Mandi has been strategic in backward and forward linkages to address these roadblocks.

- MSC collaborated with Kaarigar Mandi to identify artisans’ problems and assess ways to support them. The team interacted with the artisans directly and collected field insights to enhance their relationship with Kaarigar Mandi. MSC suggested several mitigation initiatives. These included upgrading artisans to take work from various firms, including Kaarigar Mandi, capacity building on business and inventory management, and standardization of quality checks. Better quality checks would allow Kaarigar Mandi to establish strong ties with the artisan community and become their preferred partner for footwear production.

- The MSC team explored the emerging opportunity to supply footwear to D2C (direct-to-consumer) brands to generate more business. The team helped Kaarigar Mandi reposition itself as a quality supplier to generate business from the D2C footwear companies. MSC’s assistance will allow Kaarigar Mandi to create more business and provide its artisans with a consistent line of work. In the first month of Kaarigar Mandi’s repositioning through a social media campaign, MSC helped it get more than 60 leads from footwear D2C brands.

MSC designed these two interventions to address the two key, interrelated challenges of artisan churn and limited buyers for products. D2C footwear is a growing segment, and if Kaarigar Mandi can position itself well, the artisans will stand to gain the most. MSC’s support continues to generate online leads through extensive social media marketing to position Kaarigar Mandi as a reliable, high-quality brand among D2C players.

Way forward

Alongside its business goals, the startup also wants to preserve the traditional art of footwear manufacturing, arrest migration, and build the local economy. It plans to expand its artisan network to 5,000 in two to three years. It also seeks to provide them with continuous work and increased engagement throughout the year. Thanks to Kaarigar Mandi’s efforts, artisans like Saurabh can now look forward to preserving their skills and aspire toward a brighter future.

Finequs: Democratizing the lead generation of financial products to increase access

Introduction

The Pradhan Mantri Jan Dhan Yojna (PMJDY) in India increased access to formal financial accounts to 78%, providing significant benefits to low- and moderate-income (LMI) segments. However, the usage of these accounts among the LMI segment in access to financial products remains limited.

This blog highlights the journey of the FinTech startup Finequs. The startup works to deepen access to financial products, such as loans, credit cards, and other financial products, to increase account usage by the target segment. It seeks to democratize the lead generation process for financial products through merchant channels. In this blog, you will discover how Finequs strengthens this merchant channel and motivates them to add financial services to their offerings.

Finequs is part of the Financial Inclusion (FI) Lab’s sixth cohort. The Lab has supported 50 startups focused on the LMI segment as part of CIIE.CO’s Bharat Inclusion Initiative, with technical assistance from MSC. The Lab receives support from some of the largest philanthropic organizations worldwide—the Bill & Melinda Gates Foundation, J.P. Morgan, Michael & Susan Dell Foundation, Omidyar Network, and MetLife Foundation.

Credit is a chronic need in India. However, only 11.8% of adults could borrow funds from formal financial institutions. Several studies, including MSC field analysis and Global Findex, highlight that lack of trust and access to financial products or distance from financial institutions results in low activity in financial accounts.

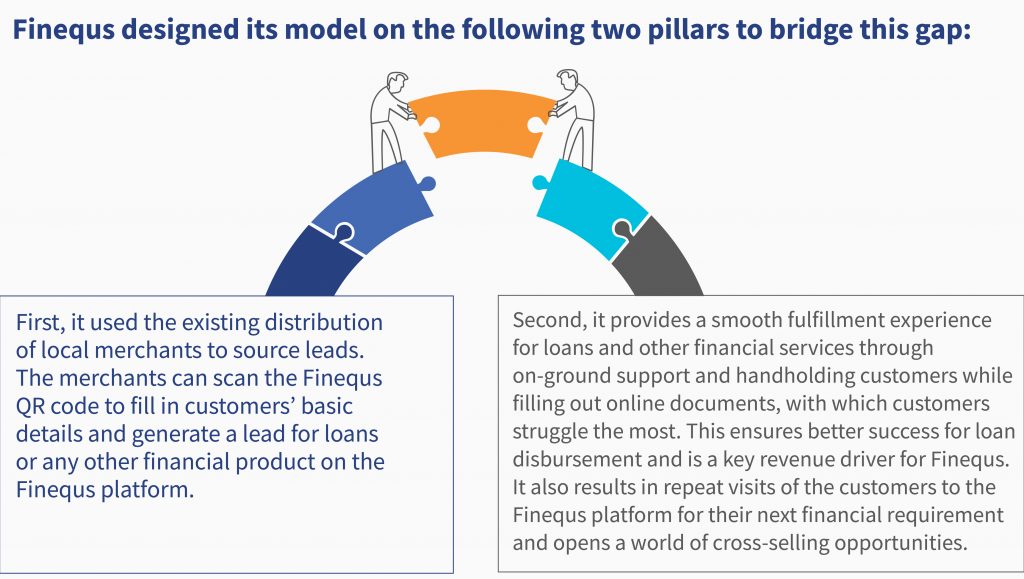

Finequs is on this journey to make access to financial products similar to going to the local market for grocery shopping—simple and convenient. It uses the retail merchant channel to generate leads for financial products on behalf of formal financial institutions.

The light-bulb moment

Former banker Krishnan Vaidyanathan founded Finequs in 2019 in Chennai, India.

The ambition to make financial inclusion accessible, inclusive, and democratic

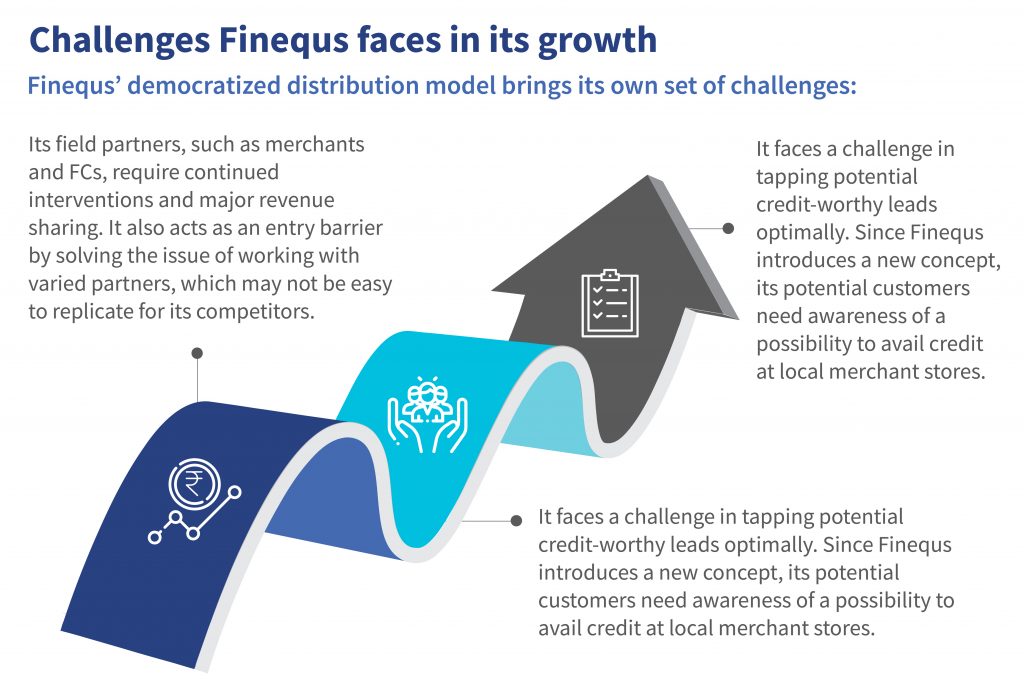

Krishnan used his rich and varied banking experience across premier private and multinational banks to understand the limitations of the traditional financial ecosystem to reach the underserved segments of society. Even the FinTechs operating for a considerable time cannot reach the masses. Gaps, such as trust in the digital medium and the savviness of users to avail digital loans of their own, limit the uptake of formal credit products. Finequs saw this opportunity and decided to operate at the intersection of technology and financial institutions to deepen access to financial products by improving their distribution.

Krishnan used his rich and varied banking experience across premier private and multinational banks to understand the limitations of the traditional financial ecosystem to reach the underserved segments of society. Even the FinTechs operating for a considerable time cannot reach the masses. Gaps, such as trust in the digital medium and the savviness of users to avail digital loans of their own, limit the uptake of formal credit products. Finequs saw this opportunity and decided to operate at the intersection of technology and financial institutions to deepen access to financial products by improving their distribution.

Finequs designed its system to serve customers with limited digital savviness. These customers may or may not own a smartphone and need assistance to complete a financial transaction digitally. A major gap persists between the complete digital journey desired by lenders and the customers’ capability and requirements.

Some of its target customers are new to credit or may have bad credit scores limiting their access to formal loans by partner lenders. To solve this issue, Finequs has also looped in services, such as gold loans and credit score repair, to bring these customers into the formal credit fold.

Finequs seeks to streamline these products among the underserved segments through its distribution channel, which primarily constitutes merchants. Merchants can add revenue for the lead generation efforts at practically no investment or stocking up of goods. Finequs confirms that merchants can add anywhere between USD 180 and USD 600 additional monthly income by associating with Finequs.

Merchants can increase user engagement by providing access to various financial services, such as instant loans, credit cards, and home loans. To date, merchants have disbursed loans amounting to approximately USD 7 million through collaboration with more than 50 formal lenders.

Finequs has also partnered with direct selling agents and other partners with on-field presence to serve as fulfillment centers. These fulfillment centers take the load of processing work from merchants and assist the customers in completing their forms and other documentation processes once they are registered in the Finequs platform as potential leads.

Support from the FI Lab

FI Lab’s support to Finequs included customized solutions to address its demand- and supply-side challenges. The FI Lab provided technical assistance and field insights into merchant operations, their relationship with partner entities, and potential leads onboard onto the platform.

Our team split the technical assistance into two levels. First, we focused on the merchant channel and recommended ways to strengthen its relationship with Finequs. We also suggested merchant classifications and incentive structures that could motivate merchants to work for Finequs. Second, we analyzed FCs and validated the model for scale-up. We suggested ways in which Finequs could use FCs to increase the success rate for loan conversions and the best practices to follow.

Continued innovation

Gearing up for instant loan disbursement at the merchant centers: Finequs partnered with a few lenders to provide timely loans and created an instant loan disbursement plan for a smaller sum of approximately USD 123- USD 183. Finequs will provide real-time information to the lenders using their algorithms on this data to underwrite instant loans.

Enabling platforms to disburse loans: Another major innovation from Finequs includes creating suitable application programming interfaces (APIs), which third-party platforms, such as enterprise resource planning modules (ERPs) in hospitals and schools, can use to provide credit facilities to their customers. Finequs’ motto is to partner with offline and online stores to offer credit facilities.

Big data analysis to help generate qualified leads: Finequs invests in developing its data capability to complement its partner lenders’ efforts. Finequs logic engine can improve the lead quality for lenders by including customer data and local knowledge, such as major occupation and seasonality of income. Krishnan sounds confident about the future, “I need to know my customer better and help lenders make the right decision, which will significantly increase Finequs’ value—beyond just generating leads.”

MAKSPay: A bold bid to unlock the untapped potential of India’s street vending economy

At the end of yet another long day, Ventakesh dragged his pushcart piled with unsold flowers from the Gudimalkapur market near Telangana state’s capital, Hyderabad, back to his tiny home. He had been anxious about his future since the pandemic set in. Like many street vendors in the market, he wondered if he could restart his business and resume his livelihood in the post-pandemic months.

Venkatesh struggled to make ends meet during this challenging time with diminishing savings and a meager income. Applying for a personal loan crossed his mind, but the documentation-heavy process, usurious interest rates, and lack of mortgage, among others, dampened this aspiration. Ventakesh is among India’s 5 million street vendors whose businesses suffered from the pandemic. Many gave up their business, while others struggled to survive.

Several FinTechs have tried to solve the problems of this underserved segment. Among them is MAKSPay, a platform under the brand name PehchanPe, which works to revolutionize the borrowing experience of millions like Venkatesh.

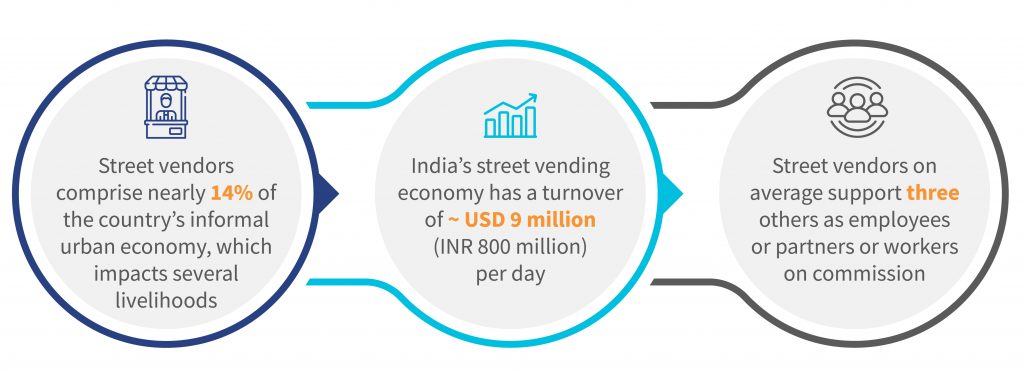

Street vendors form an indispensable part of the Indian economy. India’s street vendor economy is built upon micro-entrepreneurship and addresses several challenges, including unemployment. The infographic below charts the crucial role street vendors play.

Fig 1: The street vendor economy’s role in India; Source: The ISST

However, most street vendors live hand to mouth, earning less than USD 0.98 (INR 80) daily—way below the Minimum Wage Act. Every day, street vendors in India battle manifold challenges—access to finance is one.

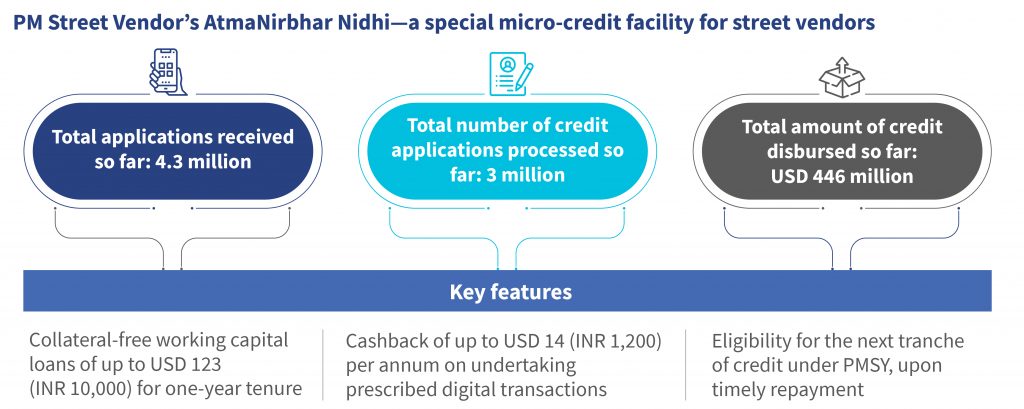

The government unveiled the PM Street Vendor’s Atma Nirbhar Nidhi (PMSY) program to revive and support street vendors. The graphic below mentions some of the program’s main features:

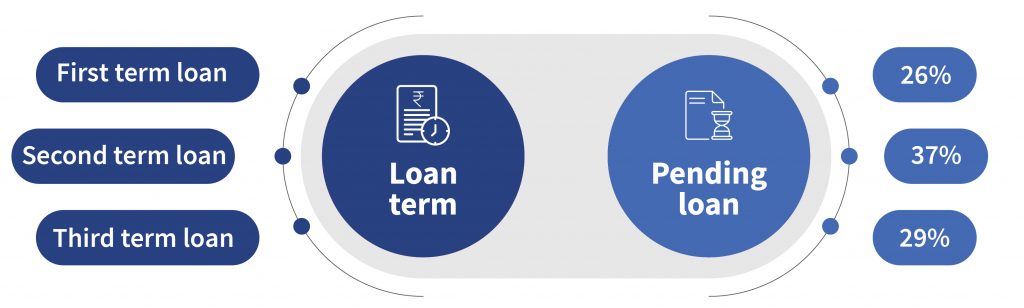

PMSY is a ground-breaking initiative, yet several factors constrain it from achieving its full potential. These include a complex loan application process, low-level awareness among street vendors, and over-dependence on urban local bodies to sanction loans. Moreover, lending institutions in India worry about non-performing assets (NPAs), currently at 12% for PMSY-disbursed loans, as seen in the figure below.

MAKSPay seeks to address these specific issues. This is its story.

The journey of MAKSPay founders

The journey of MAKSPay founders

Shiva and Kavitha, a couple from Hyderabad, saw an opportunity in crisis to support street vendors through MAKSPay. Shiva worked with leading consulting firms across Southeast Asia for years before he returned to India in 2009. Cofounder Kavitha doubles up as MAKSPay’s Chief Operating Officer and had worked in banking and credit underwriting with financial institutions in the UK.

They thought of combining their strength in tech and banking to build something meaningful for marginalized communities. Then the pandemic happened, which served as a watershed moment for them.

When the government launched PMSY during the subsequent lockdowns, the duo quickly identified gaps and mitigation strategies to act upon. They spoke to a few banking professionals and realized that financial institutions hesitated to lend to street vendors due to the costs involved for low-value loans and associated credit risks.

They spoke to street vendors through the National Association of Street Vendors of India (NASVI). A common understanding emerged—despite formal credit availability, most street vendors either did not know about the loans or hesitated to apply for loans due to the tedious processes involved. Shiva and Kavitha were confident they could use the PMSY program’s Jan Dhan bank account facility to improve the street vendor segment’s financial well-being. The duo set up MAKSPay in December 2020 to improve credit access for millions of street vendors, much like Ventakesh.

MAKSPay officially partnered with AU Small Finance Bank and started disbursing loans under PMSY with support from the Reserve Bank Innovation Hub (RBIH). MAKSPay integrated with the bank’s tech stack and digitized the loan disbursement and repayments process.

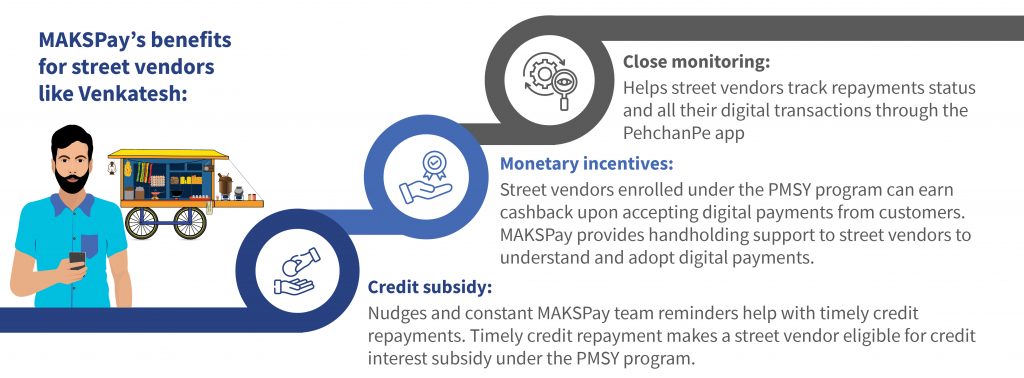

MAKSPay developed an app, PehchanPe, to improve the convenience for street vendors, who can use it to apply for loans easily.

MAKSPay’s key features

- Digital on-doorstep process: MAKSPay app uses digital public goods (DPG), such as DigiLocker, NSDL (for eSign), and facial biometrics, to offer an end-to-end digital lending experience to street vendors. Under the usual process, street vendors need to visit the bank branch for document verification to access credit. Thanks to MAKSPay, they longer need to leave their vending unit to get a loan under PMSY.

Through MAKSPay, street vendors can complete the process digitally by themselves at the place of their choice. Further, MAKSPay’s field agents offer handholding support to street vendors who hesitate to use digital platforms independently. The digital process reduces the overall time for credit disbursement from 30 days to potentially under 30 mins.

- Flexible repayment: MAKSPay and its partner bank’s co-branded QR codes are installed at the street vendor’s vending unit, linked to their bank account. Street vendors are expected to install QR to accept payments from customers. The installment amount is debited automatically from the bank account linked to the QR.

- MAKSPay’s system helps financial institutions, such as banks and NBFCs, to enable quick loan disbursement. It will permit better control and transparency over the street vendors’ business and ability to repay loans.

Digital transactions through QR codes and their use for repayments help street vendors build credit discipline and motivate them to transact digitally. Timely repayment history and digital footprint make street vendors eligible for PMSY and other formal borrowing opportunities.

The FI Lab’s support

The FI Lab’s support

The Lab has offered a holistic support package to MAKSPay. This support ranged from mentor hours and grant capital to field studies led by financial inclusion experts who specialize in consumer and market insights.

MAKSPay intends to serve as a one-stop financial solution for street vendors. As an initial step, it plans to provide affordable customized insurance for street vendors, for which MSC conducted on-field research in Hyderabad and Lucknow.

MSC assessed the street vendors’ awareness of insurance products, willingness to pay, and expectations with the policy cover to design insurance products to fit their needs. We also identified suitable insurance firms that MAKSPay could partner with to offer insurance products.

The MAKSPay team was keen to streamline its technology offering and sought a nuanced understanding of the on-ground challenges in the lending process. MSC assessed its lending model to map the process alongside stakeholders and identify risks in Jaipur—one of the pilot locations. We suggested a suitable risk mitigation approach based on the risks identified.

Where is MAKSPay headed?

MAKSPay intends to emerge as the last-mile technology partner of choice for lenders for PMSY. MAKSPay continues to partner with partners, such as American India Foundation, to further improve its reach among street vendors.

MAKSPay is on track to scale its operations in the next few months with more banking and NBFC partners in the pipeline. MAKSPay will target and disburse loans to 100,000 street vendors across select pilot locations. It started with Rajasthan and Telangana, which has an overall base of around 800,000 street vendors. Based on the pilot’s success, MAKSPay plans to cover eight more cities and target approximately one million street vendors by the end of 2024.

Credit facilitation is just the tip of the iceberg. MAKSPay has also been working to use India’s digital public infrastructure (DPI) foundation-based Open Network for Digital Commerce (ONDC) to enable online selling for street vendors. In the coming days, MAKSPay is all set to improve the financial lives of millions of street vendors, such as Venkatesh, and empower them to be proud self-employed entrepreneurs.

Battles to win

MAKSPay partnered with several stakeholders in the pilot phase, such as banks, NBFCs, the NASVI, and payment aggregators. These collaborations call for a lot of coordination and swift iterations at the backend for seamless implementation.

Yet with its agile tech platform, MAKSPay can customize customer onboarding, loan disbursement, and repayment architecture as required by the financial institutions’ lending processes. Such customization aligns with the Reserve Bank of India’s digital lending guidelines.

Digital agriculture solutions for climate-resilient smallholder agriculture: Lessons from the GSMA

This session resulted from a collaboration between GSMA and MSC’s climate-resilient agriculture virtual club #CRAgVC. Our shared mission was to amplify knowledge sharing and disseminate findings from two groundbreaking reports from the GSMA AgriTech Programme.

The session explored the transformative potential of digital solutions to build climate resilience for smallholder farmers.

00:00 – 06:56 Welcome note and introduction of the webinar’s topic and guests by Willis Ogutu, Manager, Private Sector Development, MSC

Guests:

- Lisa Chassin: Insights Manager, GSMA AgriTech

- Jan Priebe: Senior Insights Manager, GSMA AgriTech

06:58- 24:38 Jan Priebe presented on “Digital agriculture solutions for climate-resilient smallholder agriculture.”

25:10 – 52:16 Lisa Chassin presented on “Developing and scaling digital services for climate resilience.”

53:08 – 1:05:18 The panelists responded to a round of questions from the audience.

Question 1) Do the rural landscapes of most developing countries have enough mobile towers to facilitate rainfall measurements reasonably, consistently, and accurately? And can local farming communities avail of the data freely and easily?

Question 2) Using the developer approach, can you identify the rainfall level in mm?

Question 3) How did the GMSA reconcile the need for credit risk assessment and loan repayment? How did it recognize that providing access to credit (easy-to-access, distribute, and collect payments) is critical for small-scale farmers to become climate-resilient and move toward sustainable farming livelihoods?

Question 4) Is the cost of SMS included in the service offering’s feasibility for telecommunication company partnerships to provide these advisory services? From experience, a third party would find it difficult to offer these services when it has to pay for SMS as a service.

Question 5) As cell technology evolves into 5G, 6G networks, and more, will commercial microwave links (CML) data continue to work in the same way?

1:06:15 – 1:07:06 The guests shared their concluding remarks.

1:07:06 – 1:08:01 Willis Ogutu of MSC presented the concluding remarks.