MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

Digital technologies’ impact on women’s financial inclusion

byMicroSave Consulting

This podcast brings together Brenda Oyugi (Manager, Digital Transformation) and Scholastica Kaaria (Gender Specialist) from MSC. They share their insights on the role of digital technology in women’s financial inclusion.

Artificial intelligence (AI) is no longer in the future but is very much here and now. ChatGPT’s recent arrival has sparked discussions worldwide, including among The Alliance of Digital Finance Associations and MSC.

ChatGPT-4, launched on 14 March 2023, has 100 trillion parameters, compared to GPT-3’s 175 billion parameters, making it substantially more powerful, and we can even speculate on the brilliance of ChatGPT-5 and beyond.

AI chatbots already prevail in the financial services industry and have been used for many years. One of the first chatbots to launch was Ongair in Kenya in 2014, with Africa as a specific focus. Other examples include Zuri from Safaricom in Kenya, which helps customers access usage statements, top-up airtime, and check M-PESA and airtime balances; and Kudi in Nigeria, which allows users to transfer money, track account details, buy airtime, and pay recurrent bills, such as DSTV.

Another interesting deployment is Proto AICX, a multilingual chatbot deployed by the Bank of Ghana. This automated consumer protection solution collects and categorizes complaints across multiple channels and all financial institutions. Consumers can use the chatbot in English or Twi, which is the most spoken language in Ghana. Meanwhile, Standard Bank South Africa launched a WhatsApp-based chatbot that keeps its customers updated with its services and offers debt relief offerings. The chatbot also provided other important, relevant information during the COVID-19 pandemic.

Compared to other LLMs, ChatGPT stands out for its realistic approach to users, requiring them to type questions conversationally. This allows it to improve customer engagement significantly, streamline operations, and enhance overall customer experience. Customers are the lifeblood of any company. Hence, maintaining good relations with them is crucial to gaining loyalty and repeat business, ultimately leading to sustained growth and profitability.

In addition, ChatGPT’s multilingual support could help businesses provide customers with answers and information in various languages. It would help the business grow clientele, provide customer service to a global customer base, and even enter new markets. The multilingual support can also potentially attract new customers who were excluded earlier due to language barriers.

For consumers, particularly the underserved

The benefits are not limited to businesses alone. Consumers can also benefit from being able to access advice and information in a timely and efficient manner.

ChatGPT-powered chatbots can be available on various platforms, such as websites, mobile apps, and messaging applications. This accessibility enables individuals with limited access to traditional banking channels, such as physical branches, to engage with financial institutions conveniently and access essential services with ease.

ChatGPT can serve as an educational resource that provides users with information on budgeting, saving, and other financial topics. By delivering accessible financial education, ChatGPT helps individuals acquire essential knowledge and skills and promotes their financial well-being and inclusion.

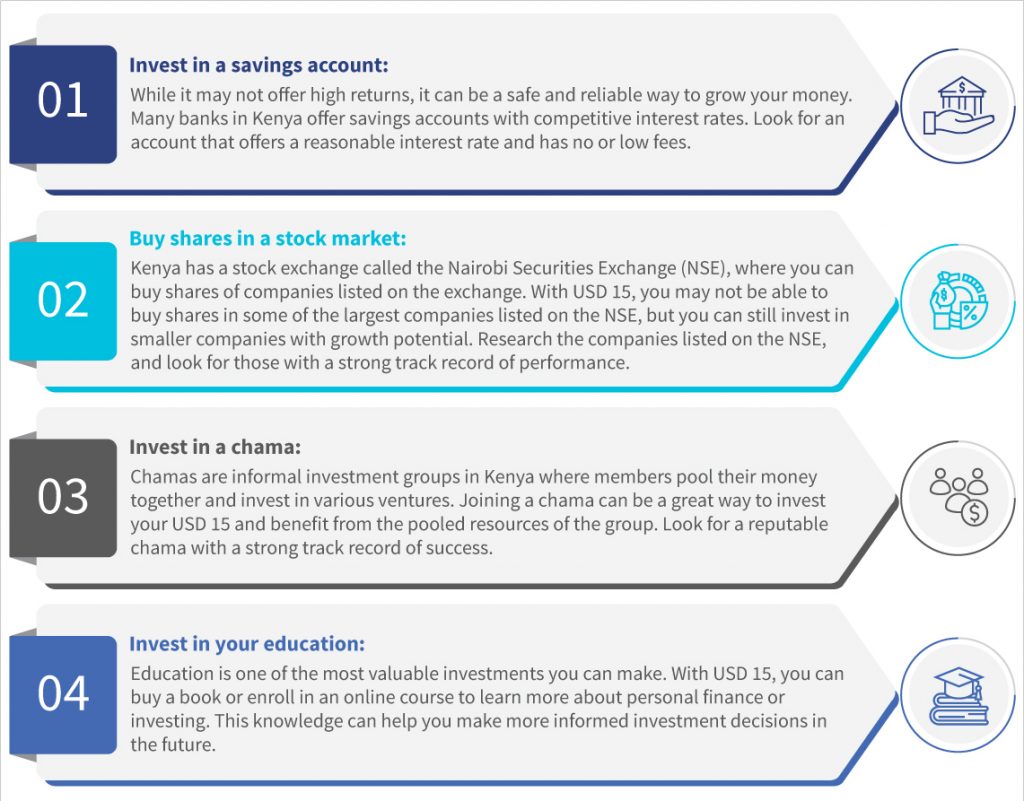

We gave ChatGPT a second test to understand what further benefits it could bring to an individual. We wrote to ChatGPT from the perspective of an MSC consultant based in Kenya and asked for financial advice on investing USD 15 in Kenya. This was ChatGPT’s response based on data available as of September 2021:

Investing in Kenya with just USD 15 might be challenging, but there are still some options available to you. Here are a few tips to help you invest your USD 15 wisely in Kenya:

Similarly, ChatGPT’s usage in advanced economies has stayed strong. As per a publication by Forbes, The Impact Of ChatGPT And Open Banking Cannot Be Underestimated. Mike Kelly, an entrepreneur, and a FinTech enthusiast, has built a plug-in to link ChatGPT to his bank account using the UK’s open banking APIs. The plug-in, called “BankGPT,” can show you your balance, find transactions, discuss your budgeting, and even make payments.

Concerns and ethical considerations

We have highlighted some of ChatGPT’s potential use cases, but what are some challenges and concerns in its use?

ChatGPT will also need training, and its output would need to be edited to ensure that the messages fit the company’s tone and voice, and, of course, be accurate. Without time and human intervention, it cannot be plugged in and output results immediately.

Regulations are minimal on the use of chatbots, and they certainly will not account for some of ChatGPT’s power and scope. Still, legislations, such as data protection and human rights laws, must be updated to cover obligations when developing and using AI to protect the customer and their data and avoid discrimination and bias. Some countries with no or outdated policies must incorporate or update them to protect consumers.

In the developing world, financial service providers and regulators have limited capacity to understand AI’s potential and its dangers fully. AI is often closed-source and for-profit, so its usage to support an agenda for inclusion will likely be limited. Many countries and financial service providers would find it prohibitive to purchase, train, and launch AI and then experiment with and use it.

AI could widen the digital divide if funding and capacity within the profession remain constrained. The open-source nature of ChatGPT, however, stands to deepen access further if it is adopted as a digital public good.

The advancement of ChatGPT and other tools to accurately generate realistic conversations will transform how we work, how businesses operate, and how customers experience services. Before we can confidently say that ChatGPT will enhance financial inclusion, we need to see the challenges around funding, capacity, and, particularly, regulations being tackled to realize its potential to support improved customer experiences and offer services that could enhance greater inclusion and informed customer choice.

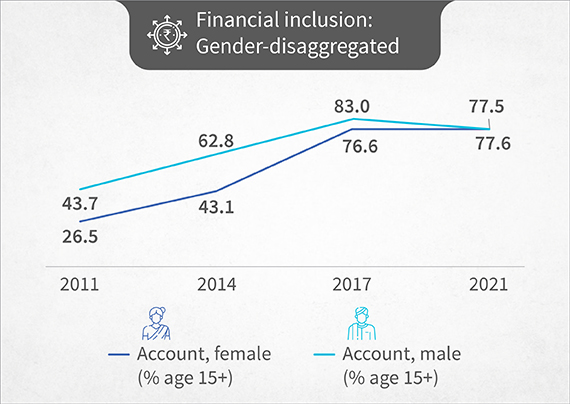

The road to achieving digital financial inclusion for women is long. Yet we must acknowledge that we are (slowly) moving in the right direction. The status of women in the financial inclusion ecosystem looks bright. The Global Findex data 2021 highlights that the gender gap among bank account holders has narrowed due to increased account ownership among women. Financial activity among women has risen as more women borrow from financial institutions and save in them.

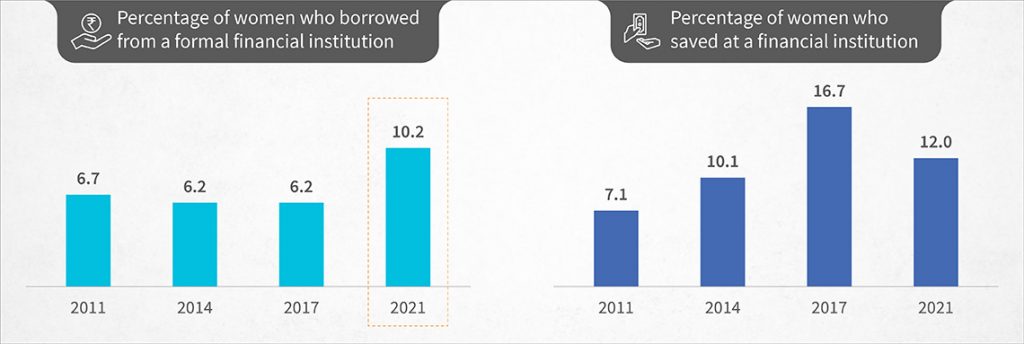

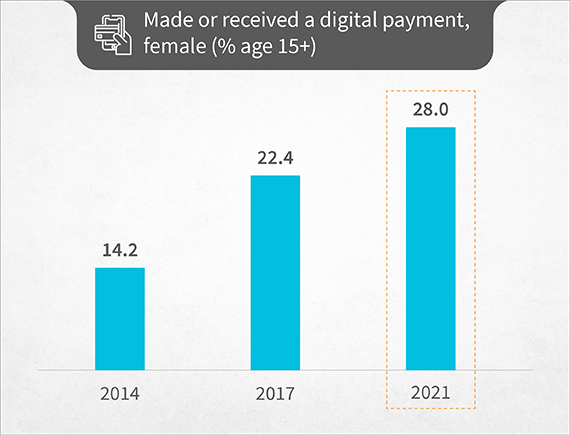

Moreover, DFS-related activity has also seen growth. The ownership of debit and credit cards among women has also increased notably. Women who make or receive digital payments have almost doubled since 2014.

Figure 1: Account ownership among women increased to 77.6% in 2021, reducing the gender disparity in financial inclusion to 0.1%

Figure 2: Percentage of women who borrowed from or saved at a financial institution

Figure 3: Percentage of women who made or received a digital payment

Despite the increasing ownership of financial accounts, the adoption and use of digital financial services are yet to take off fully among women. Increased risks around customer protection and data privacy in the digital finance ecosystem have emerged as a significant deterrent to the uptake of DFS among women. Women often do not trust digital channels when they try to access financial services. For instance, MSC’s research with female recipients of G2P programs in Bangladesh highlights that fear of fraud is a key reason why women hesitate to use digital modes of payments beyond cash-outs.

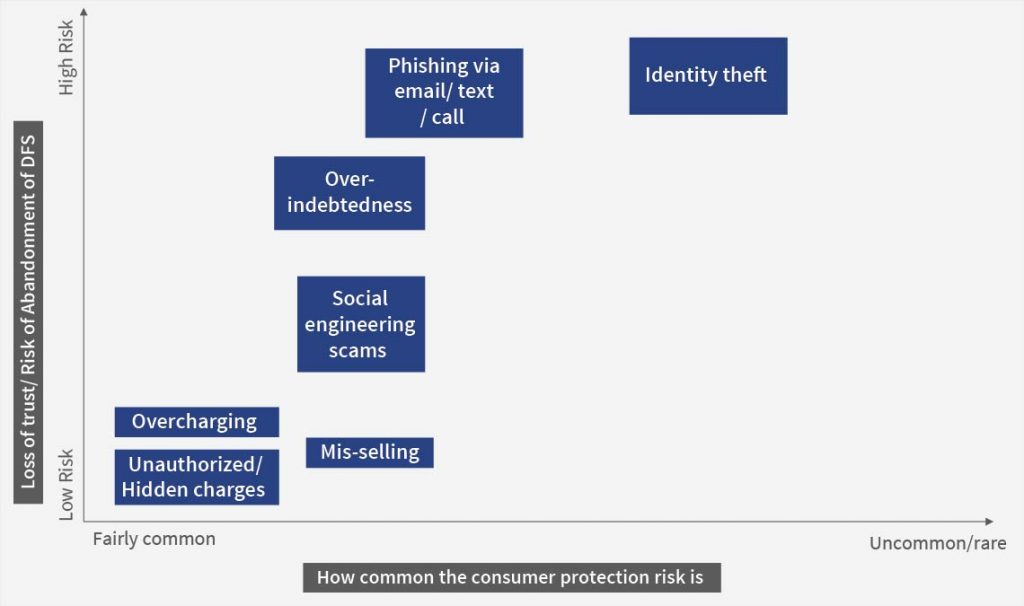

Unfortunately, as CGAP reports, women, specifically rural women, are more vulnerable to experiencing DFS-related risks. DFS-related risks are constantly evolving. They reduce confidence in using DFS, decrease active usage, and, if unaddressed, may even compel users to abandon DFS completely. Below, we have mapped[1] the most common DFS-related consumer risks to their impact on a woman’s trust in DFS or risk of abandonment of DFS by women.

Why women?

Women’s higher susceptibility to DFS-related risks is certainly not shocking. While the drive from governments and DFS providers to financially include women is admirable, their frequently low digital capability limits their understanding of the potential risks and vulnerabilities associated with DFS. This makes them easier targets for fraudsters.

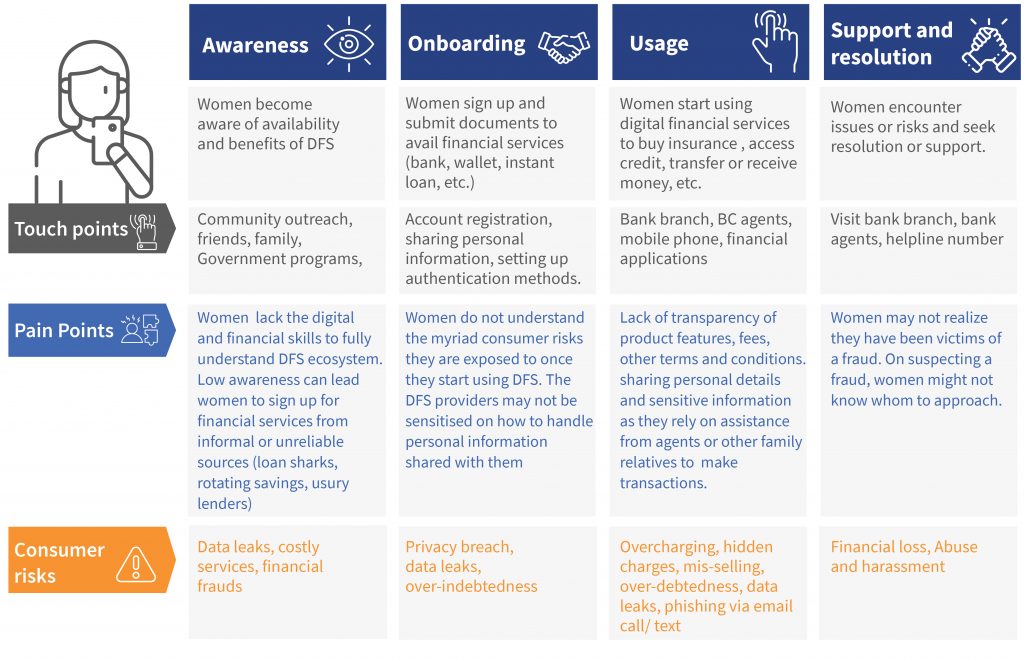

Many women are essentially DFS proxy users or agent-dependent users. They rely on family members or assistance from agents to access financial services and conduct transactions. Women may face unique social challenges as others manipulate their relationships or exploit power dynamics to gain unauthorized access to their financial accounts or sensitive information.

Figure 5: Tracing a woman’s journey as she accesses financial services to map DFS consumer risks she is exposed to disproportionately

So, what can DFS providers do?

Controlling evolving consumer risks is crucial to ensure sustained DFS usage among women. This can be done through the creation of an action-oriented, gender-intentional approach to monitor and safeguard DFS users against consumer risks. Devising solutions that reduce DFS consumer risks for women will require DFS providers to:

1. Collect and analyze gender-disaggregated data: DFS providers should collect gender-disaggregated data for digital financial services and products. The gender-disaggregated data should be collected for account ownership, usage, and user grievances. This will help identify early on the most common issues concerning women. An analysis of gender-disaggregated data for a grievance resolution mechanism (GRM) can help DFS providers improve their products and offer women customized solutions. Moreover, this data can be used to design financial education collaterals that target specific needs highlighted by women.

2. Design robust and responsible grievance resolution mechanisms: DFS providers should build GRM systems that have a simple user interface and easy-to-navigate user experience designs. MSC’s research in Uganda highlights that most customers do not use GRM systems because they lack trust in the systems or struggle to navigate complex interfaces. Fraudsters impersonate customer care executives and deceive them in the name of resolving issues, which leads them to lose money. Since women are more susceptible to such fraud, DFS providers should ensure they build responsible GRM systems that are well-communicated and have a quick response time.

3. Design responsive channels and content to spread awareness about DFS consumer risks: The likelihood of DFS users being defrauded would be lower if they knew more about fraud and the fraudsters’ behavior. An interactive chatbot can be preinstalled on mobile phones with in-built features that include information on types of financial fraud, new trends, and patterns fraudsters use, and the best practices users should follow while making digital financial transactions. For feature phones, IVRS can be used to sensitize female DFS users to make them more vigilant while using digital channels.

4. Creation of market monitoring mechanisms: Monitoring and analysis of GRM data for women can help DFS providers design better products for women and improve their access to finance. Furthermore, providers can seek regular feedback from women through surveys, analyze social media complaints, and review and track risk management practices to detect potential risks or vulnerabilities women who use DFS face.

In conclusion, DFS providers must recognize and address women’s heightened vulnerability to DFS-related risks. Providers can build a safer DFS ecosystem tailored to women’s needs by adopting these practices. Education initiatives that seek to raise awareness of customer protection hold immense potential to safeguard women’s financial well-being when coupled with robust mechanisms to mitigate fraud risks.

As women continue to drive revolutions through increased financial activity, DFS providers must create safeguards to protect them from potential risks in their financial engagement. If DFS providers place the security and empowerment of women front and center, they can carve a path for a transformative era in women’s financial inclusion—and in the process, a better future for all.

“Yet again, my loan application got rejected. These banks keep asking for an income certificate,” rued Mohan to his wife after another day at his garment shop. Mohan runs his small outlet in the Gorakhpur region of India’s Uttar Pradesh state. He has been looking for a business loan for about five months now. Mohan want to improve the stock at his shop to increase earnings to support his daughter’s education. He is short of capital and is tired of applying unsuccessfully for a loan at commercial banks.

Does he need to turn to the local moneylender again to fund his business? Will the system leave Mohan and countless others like him out of the formal lending ecosystem yet again? These are hard questions that a handful of FinTechs have tried to answer.

The FinTech market in India in 2022 was valued at USD 584 billion, of which the lending tech market was worth USD 270 billion. Digital lending is also expected to grow 4.75X by 2030, with a market size of USD 1.3 trillion. The top three lending SAAS platforms in India raised $58 million in total, while the FinTech SAAS platforms raised around $360 million. The availability of skilled talent, rapid adoption of digital solutions, and the enormous market potential of over 900 million smartphone users in India by 2025 have led to the growth of fintech companies. New-age FinTechs like Roopya can accelerate digital lending by using ubiquitous digital public infrastructure (DPI), India Stack.

Roopya’s foundation goes back to the founders’ early days

Raman and Sudipta found their entrepreneurial spirit in their early childhood days. Raman started earning in the eighth standard by renting out video games. Raman reminisces how those video games changed his future forever. On the other hand, Sudipta wrote software and did market research assignments to support his college fees. Raman and Sudipta are tech and data enthusiasts and realized early on that data could change the landscape of the lending industry.

In 2014, they acquired a startup called Roopya.com that worked as an institutional DSA and generated loan leads for their lending partners. Over time, in 2018, they realized that to serve more customers, Direct Selling Agents (DSAs) need a platform that can connect them and their customers to multiple lenders. Hence, with a vision to make instant loans a reality for the masses, they founded another company called Roopya. Money that works to connect all stakeholders in a lending ecosystem on a single platform.

Roopya as a catalyst in #LendingToTheNextbillion

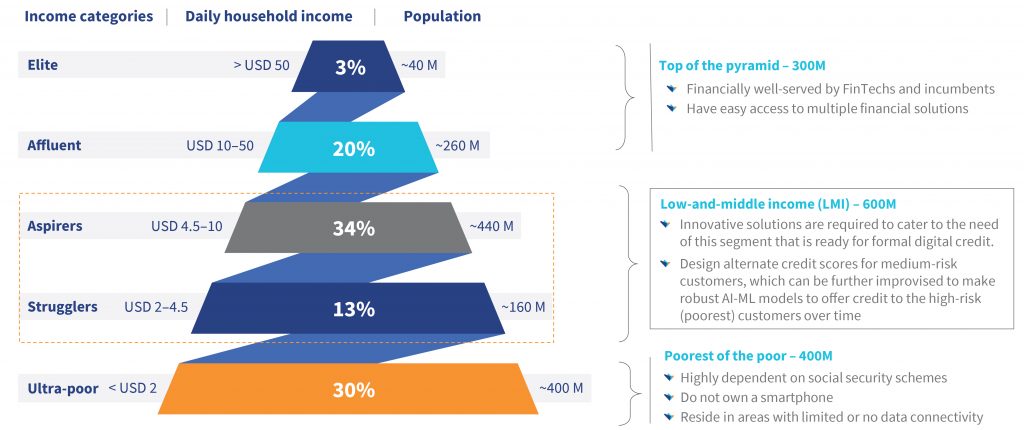

India has a diverse credit market, with a population of 1.4 billion people. We can categorize India’s population into five segments based on differentiated income levels (See diagram 1). As per an Experian report, while the elite and affluents have formal digital lending sources available, the aspirer and strugglers find it difficult to identify the right credit products, despite their readiness for formal digital credit. Our tailor, Mohan, who is from this segment, can approach the Roopya platform through their webpage on his own or through DSA to find a lender for his credit needs.

Roopya, with a specified user license, has made instant loans a reality

Roopya, with seven NBFC partners and 30+ DSA partners, has served as a catalyst to fulfill credit needs of more than 300,000 people like Mohan who often struggle to get a loan as they do not know lenders who offer a variety of credit products. The same is true for small lenders (Regional Rural Banks, Small Finance Banks, and Non-Banking Financial Companies) that intend to serve customers like Mohan but have limited avenues to reach and source these customers. Roopya made gross revenue of USD 194,000 in the financial year 2022-23.

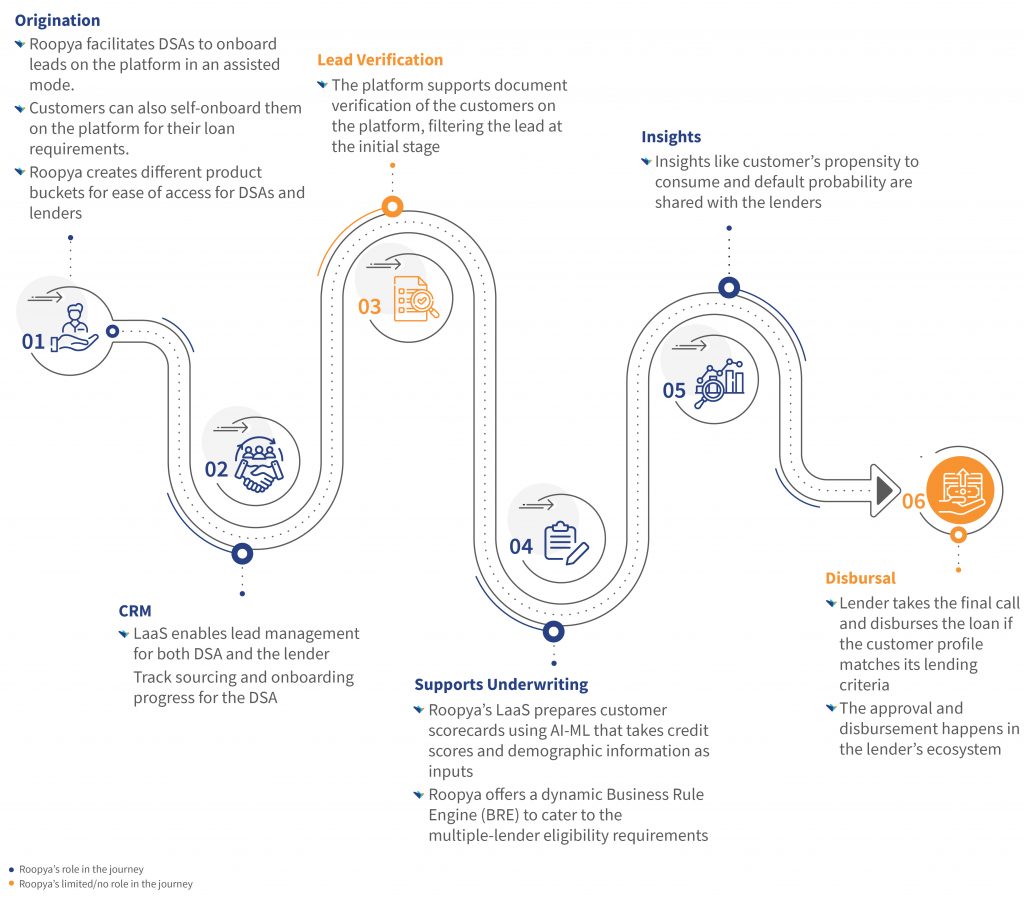

Roopya’s specified user license enables it to obtain the credit information of the borrowers from the credit bureaus registered on its platform. Roopya designed an AI/ML-based credit assessment tool that creates algorithms based on inputs such as credit scores and demographic variables to filter creditworthy individuals and share it with lenders. Lenders can then reach out to these borrowers and provide them with the desired loan. Roopya caters to the diverse credit requirements of customers by mapping them to portfolios offered by various lending platforms. The following diagram illustrates the role of Roopya’s LaaS platform in the digital credit journey of the customer.

What does Roopya offer to various stakeholders?

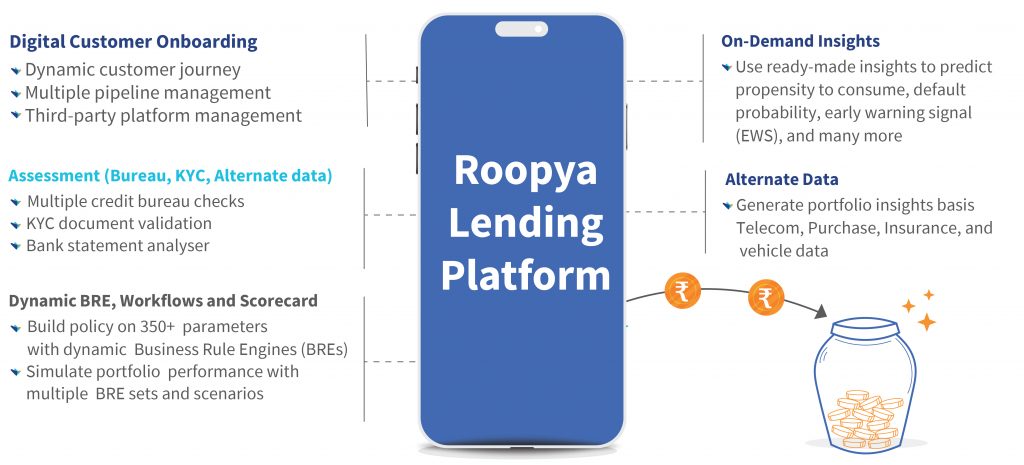

Roopya’s LaaS platform provides several benefits as follows to the DSAs and the lenders. The following figure illustrates how Roopya adds value for various stakeholders:

Primarily to lenders:

Loan origination and underwriting: The platform enables loan origination and underwriting support on a single platform combined with a workflow module, decision engine, and scorecard to manage millions of customers. Its advanced AI/ML can help lenders design early warning signals to assist loan disbursement decisions.

Monitoring tool: The platform provides agent monitoring tools to lenders and institutional DSAs.

Primarily for DSAs:

Automation: Roopya provides the digital infrastructure for agents to manage customer It automates the process through digital onboarding and processing customers’ documents. Consequently, the agents save time and effort as they no longer need to visit the customer’s location multiple times, earlier required for onboarding formalities.

Many-to-many network benefit: The platform also supports the agents by connecting them to multiple lenders.

Cost saving: Roopya can help DSAs cut down the opportunity costs associated with physical lending processes by more than 30%, thanks to its robust loan origination and AI metrics.

Challenges for Roopya

Roopya in its five years of operations, has grown to disburse loans with a cumulative value of USD 3.65 million. Roopya innovated to stay relevant in the challenging environment of economic shock and policy and regulatory changes that the digital lending industry has faced. The latter impacts their operations as they require more resources to build regulatory-compliant technology. In addition, it isn’t easy to convince traditional DSAs who operate within a closed credit ecosystem to use their platform. Hence, Roopya has to offer several customizations to cater to their varying needs to establish itself as a platform of choice.

Support provided by the Financial Inclusion (FI) Lab

The FI Lab’s technical support to Roopya capitalized on its strengths to position the startup as a preferred LaaS partners for lenders and institutional DSAs. The Lab helped Roopya to understand the needs of credit providers and enablers, such as lenders and DSAs, in the customer credit journey. The research with lenders and DSAs helped identify the pain points of these institutions and identify the stages in the journey where Roopya could support them. The insights helped Roopya identify the LaaS platform’s value proposition for different kinds of lenders and DSAs and thus design their partnership pitches accordingly.

MSC also supported Roopya in understanding various SaaS platforms used by banks in the loan process such as loan origination software (LOS), and loan process software (LPS). This helped Roopya identify the opportunities for value addition services that may be offered with the Roopya LaaS platform.

Way forward

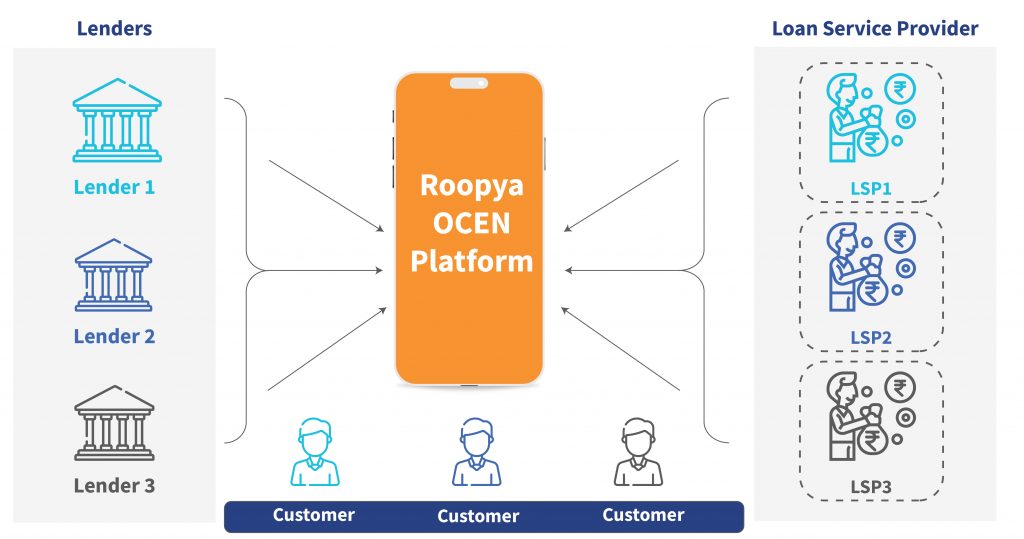

In conclusion, Roopya has significant tailwinds to become an important partner in the credit space for India’s LMI segment. Roopya can take advantage of the new Digital Public Infrastructure initiatives, such as Open Network for Digital Commerce (ONDC) and Open Credit Enablement Network (OCEN), that aim to create open and interoperable platforms for financial services. ONDC enables secure and consent-based data sharing among various entities, while the OCEN protocols allow lenders to connect with loan originators and service providers. Roopya can use these protocols to offer seamless and customized lending solutions to small enterprises and underserved individuals, the backbone of India’s economy. By doing so, Roopya can enhance its value proposition and contribute to the larger social and economic impact of financial inclusion.

The session included discussions around how catalytic financing can drive the supply of climate adaptation finance for the agriculture sector, especially for smallholder farmers who remain most vulnerable to climate change’s impacts.

The discussion intended to address the following questions:

Why do we need to mainstream climate adaptation finance for the agriculture sector?

How can catalytic finance help with the issue?

How is the impact investing community responding to this need?

Click on the timestamps from the webinar stream to hear specific segments.

Prasun Das elaborates on the need to finance climate adaptation finance for the agriculture sector. He highlights the necessity of knowledge collaboration, coherent policies, innovative financial instruments, and effective networks to overcome the barriers to green finance for smallholder farmers, who comprise most of the global agriculture sector.

Sandeep Bhattacharya, Advisor, Climate Change at GIZ, speaks about the initiative by Sustain Plus Energy Foundation and CINI to create farmer collectives called Production Hubs. He explains that these hubs use various technologies and practices to boost their income sustainably while facing challenges around maintenance, cost, scalability, and refinancing.

Krati Garg, Manager, Innovative Finance, KOIS, suggests that impact investors can help climate businesses attract commercial finance that balances impact and returns by using catalytic finance, standard impact measurement frameworks, and impact monetization.

Click on the timestamps below to watch the specific segments.

Chapters

04:29 – What is Lending SAAS? 08:30 – What was the trigger to start Roopya Money? 11:41 – Explain the business to a 5-year-old kid. 13:05 – How did you approach the building of the SAAS platform for the Indian lending industry? Given that the lending process is varied with such broad requirements, what were the underlying principles for you to design and build the product? 24:45 – Let’s talk business – what’s your model to earn? What is your cash cow? Other avenues that will open up. 29:19 – Are Indian lenders willing to open up for a lending SAAS? What are the underlying challenges you have faced? 36:10 – What’s your take on AI, especially with new-age generative AI impacting the financial technology industry? 39:06 – The RBI has recently given more clarity on the partnership between fintech and REs. FLDG has also received in-principle approval. Do you think REs may prefer to go with fintechs instead of investing to build their own stream of borrowers? 45:07 – India Stack is evolving – AA and OCEN and ONDC have become the buzzwords. How do you think Roopya can add value or gain from this ecosystem? 49:59 – How do you think India’s SAAS industry will shape up? What are the blind spots and opportunities? 52:11 – How does the acceleration by FI Lab help Roopya? How it can help scale the solutions. Any pearls of wisdom for both budding entrepreneurs and accelerators?

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.

Despite the increasing ownership of financial accounts, the adoption and use of digital financial services are yet to take off fully among women.

Despite the increasing ownership of financial accounts, the adoption and use of digital financial services are yet to take off fully among women.  Unfortunately, as

Unfortunately, as

Raman and Sudipta found their entrepreneurial spirit in their early childhood days. Raman started earning in the eighth standard by renting out video games. Raman reminisces how those video games changed his future forever. On the other hand, Sudipta wrote software and did market research assignments to support his college fees. Raman and Sudipta are tech and data enthusiasts and realized early on that data could change the landscape of the lending industry.

Raman and Sudipta found their entrepreneurial spirit in their early childhood days. Raman started earning in the eighth standard by renting out video games. Raman reminisces how those video games changed his future forever. On the other hand, Sudipta wrote software and did market research assignments to support his college fees. Raman and Sudipta are tech and data enthusiasts and realized early on that data could change the landscape of the lending industry.