The digital savings and payments channels carry the immense potential to increase access to basic banking services. The changes in the payments landscape due to the pandemic have altered people’s outlook in Vietnam. Digital payments solutions, such as mobile, QR, and card payments, saw an upward trend in Vietnam as people preferred the convenience of saving and paying digitally.

The “Innovate, Implement, Impact” or “i3” program, supported by the MetLife Foundation, uses digital technology to provide better opportunities for people to plan, save, borrow, and spend safely. Further, the video explores the digital journey of Vietnam during the pandemic.

Usage of smartphones appears to increase household income and consumption. Both quality (relatively) cheap smartphones and 3G+ coverage are increasingly available throughout Africa. But the majority of households have very limited disposable income both to buy a smartphone, but in particular to purchase data. The prohibitive cost of data stops many using the internet/apps and those that do “sip” rather than “surf”. The result is a significant and persistent usage gap, even as the coverage gap reduces. Orality and lack of digital capability mean that icon- and IVR-driven interfaces will be essential to build self-initiated usage. But much of the shift to internet/app usage must be assisted and mentored by agents. Agents offer a range of real advantages but also a wide variety of risks/consumer protection concerns which will require attention.

Bangladesh sanctioned and launched agent banking in 2013 to provide alternative and accessible banking services to its underserved and underprivileged population. As of 2021, 13,591 banking agents opened 11 million bank accounts through 18,314 banking outlets. However, due to the COVID-19 outbreak, Bangladesh imposed lockdowns and stay-at-home orders that prevented businesses, including banking agents, from generating income. Despite the hard barriers, like many other agents, 60% of Bank Asia agents did not stop operating even when the commercial branches were closed. They borrowed money from friends and family members to continue their banking operation and supported the government by disbursing assistance funds to vulnerable people.

The biases of the LMI segment and product development lessons for providers

Our previous blog showed that Bangladesh and Vietnam have some macroeconomic similarities yet differences. This blog examines the similarities, and even differences, in biases through the lives of two low-and moderate-income LMI segment protagonists, Morium from Bangladesh and Hoang from Vietnam.

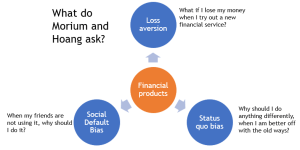

Our work suggests three distinct behavioral biases drive people’s decision-making from the LMI segments while using digital financial services (DFS)—loss aversion, status quo bias, and social default bias. There are several other biases, but financial service providers (FSP) seeking to serve LMI people with DFS will always face these three key ones.

What do they face?

Morium works in a readymade garment (RMG) factory on the outskirts of Dhaka. During the pandemic, she received her salary in her mobile financial services (MFS) wallet but still primarily uses cash for day-to-day transactions. Hoang hails from the north-central coastal district of Quỳnh Lưu in Vietnam. She has been running a grocery store for the past five years and is relatively tech-savvy.

How should FSPs factor in these biases when designing products for the LMI segment? Understanding and responding to these biases is key to effective product design.

Loss aversion

Loss aversion is best encapsulated by “losses loom larger than gains.” Morium lives on a salary that is just about sufficient to make her ends meet. Hence, she wants to make low-risk choices and avoid losses from incorrect financial decisions. She wishes to save money cautiously for the future. She, therefore, invests in the Deposit Pension Scheme (DPS), a formal recurring deposit instrument used by millions of LMI people. On the other hand, Hoang does not trust banks and chooses savings options that she believes carry a lower risk. She prefers to keep cash at home and with informal associations and clubs comprising people she knows and trusts.

When she sends money home through mobile money, Morium depends on agent-assisted transactions, as she fears sending money to the wrong account.

Status quo bias

Status quo bias is seen in people who persist with their current practices and resist any new behavior. People tend to continue with the old system unless they find a strong enough reason to change.

After COVID-19 hit, the Government of Bangladesh mandated all RMG factories to transfer salaries to workers’ MFS wallets. Morium received her salary in her bKash wallet for the first time. Prior to this, she has always used cash to buy her daily needs from grocers and merchants. Due to this status quo behavior, even now, she withdraws her salary (at an MFS agent point) and spends in cash rather than using her MFS wallet to pay digitally for her purchases. Morium exhibits status quo bias because had she not withdrawn money in cash, she would have saved on the 1.85% cash-out fee she has to pay the agent – about BDT 185 (USD 2.15) for her BDT 10,000 (USD 116) salary. bKash P2P charges are BDT 5 (USD 0.058) for transactions of less than BDT 25,000 (USD 290) (for that month), so she would have to do 37 of these before cashing out became a rational economic decision. Status quo behavior can be expensive!

Hoang wants to borrow formally but hesitates to visit banks due to the hassles of providing collaterals and navigating complex documentation requirements. She is more comfortable maintaining the status quo by borrowing from informal sources. Even though she knows of the risks, she shuns buying insurance cover. She perceives it as an expensive product for the rich. She maintains status quo bias by depending on informal support groups. The idea of saving now and reaping benefits later does not appeal to them.

Social default bias

Individuals exhibit this bias when they can or do not make informed decisions and copy others’ choices. Morium tends to follow the “leaders” in her factory who influence major financial decisions. Despite owning a mobile phone and an MFS wallet, Morium follows her friends and exhibits social default bias by making P2P transfers with the help of an agent. Stories of DFS-related fraud, instances of siphoning value out from wallets, sending money to the wrong customers, and cautionary media news weighs heavily on her mind and pushes her to display this bias. Even when it comes to savings, Morium saves in DPS, just like her friends.

Address bias through smart product design

FSPs can create a strategy that takes these biases into account by scrutinizing the requirement of customers using the eight Ps of the marketing framework—product, price, place, promotion, people, process, physical evidence, and positioning. Doing so will help them overcome the barriers that often prevent LMI people from accessing DFS.

Product:

Morium and Hoang are attached to their current ways of managing their finances. People will buy your product only if it offers an easier experience than their current one. Break status quo bias with product features such as zero savings balance, high liquidity and easy access, quicker turnaround times, and no penalties.

Stop trying to attract customers with high return rates alone. A combination of liquidity, safety and return (in that order of priority) may address loss aversion better.

Mimicking the features of informal financial systems familiar to LMI users helps overcome status quo bias. For example, MSC supported the FinTech Kosh to mimic microfinance digitally.

Use the power data to offer need-based products. MSC supported the FinTechs Finarkein and Numer8 to optimize the power of data for product design.

Price:

Hoang worries about the high price of products. Keeping costs low and affordable for LMI people, who often run on a tight budget, can help address loss aversion and social default bias. Many FinTechs offer affordable savings using this principle.

Help them to start small and build habits. Fintech Lakshya helps people save as low as INR 5 (USD 0.07) and build a habit.

Build sachet products (like insurance). MSC helped one provider in Vietnam to roll out a small premium product to insure against COVID-19.

Ensure that pricing is clear and transparent—build trust to undermine status quo bias and, eventually, enable social default bias in favor of your product.

Place:

Morium fears stepping into banks to access financial products. Offer her products in surroundings familiar and comfortable to her. FSPs can partner with aggregators, mom and pop stores, agent outlets, post office outlets, and community centers. MSC is working with several FSPs in Bangladesh to offer financial products through some of these outlets.

If you build digital marketplaces or platforms, make sure they are in a local language, with colloquial terms, are easy to navigate, and have less clutter. And remember that many people are oral, so intuitive interfaces are key.

Promotion:

Build marketing strategies that appeal to the needs of LMI people using local language and cultural context. MSC has helped many FinTechs build this in India—Bridge2Capital, myPaisa, Navana tech.

Communicate the benefits of products straightforwardly using words that people from the LMI segments use. Train your staff and cut the jargon!

Ensure that human customer touchpoints are easy to reach, knowledgeable about the product, and sensitive to the needs of LMI customers. This comfort breaks the status quo behavior of the likes of Morium. Learn from Bangladesh’s microfinance!

Enable and support agents to build trust. Remember that the bank security guard is probably the preferred touchpoint for LMI people coming to your bank branches.

Shorten forms, reduce paperwork, and limit data fields. This allows people to sign-up quickly and try something new by reducing status quo bias.

Think of ways to mimic the features of informal financial systems familiar to LMI users. These have great simplicity. Hoang is comfortable with informal clubs; can your financial product give her the same comfort and ease?

Use a combination of technology and in-person support to break status quo bias. BRAC Bank in Bangladesh banks on technology and agents through its bKash network to reach the last mile.

The status quo springs from a fear of the unknown. Create a physical environment that is welcoming, familiar, and helpful with clear and concise signage in the customers’ language. When MSC first worked with Equity Bank, we saw farmers leaving their shoes at the door of the bank’s polished marble branches.

Positioning:

FSPs should build customer protection in their solutions. Toll-free phone numbers that work, empathetic agents, responsive and supportive grievance redress systems will build customer trust.

If you feel that building a brand will take time, partner with a known brand to which LMI people can relate to address the status quo and social default bias. Customers value the safety and security of products—so use this to address loss aversion bias. Fintechs that offer savings and investment products partner with well-known banks and mutual fund houses.

Focus on emotional appeals that resonate with LMI customers. Our i3 program partner in Bangladesh, Apon Wellbeing, stresses “workers wellbeing” in its pitch. It stresses the importance of health, hygiene, and nutrition in its product offering, which helps people shun the status quo bias.

Conclusion

Biases are not specific to LMI segments. These are inherent human behaviors and are challenging to overcome. But what FSPs can definitely do is create products that appeal to this population and nudge these users into using these products. Thinking about the 8 Ps should at least help them offer an antidote to some biases. However, it will be a trial and error path with no successes guaranteed.

Microenterprises in Vietnam account for more than 98% of the business, 40% of the GDP, and 50% of the total employment. The COVID-19-induced lockdown restrictions prompted many merchants to go digital by selling foods and drinks online through super apps. The “Innovate, Implement, Impact” or i3 Program, supported by the MetLife Foundation, creates opportunities for nano and microenterprises to go digital and “cashless.”

Watch our video for more updates on the i3 program in Vietnam.

“We see the potential volume, but do we design profitable products for low-and moderate-income (LMI) people?”. MSC faces this question repeatedly in discussions with our clients across Asia and Africa – including our partners in Bangladesh and Vietnam under the MetLife Foundation-funded i3 program.

In these two blogs, we answer this question – Irrespective of the country you are in, these are key behavioral biases to keep in mind to create compelling, engaging, and profitable products for the mass market.

Worldwide, behavioral biases shape the needs, aspirations, and behaviors of people from low- and moderate-income (LMI) segments. These biases play a vital role in how people from these segments perceive, accept, and use financial products and services. This two-blog series covers Bangladesh and Vietnam. The first part highlights the macroeconomic and demographic differences and remarkable similarities between the two countries. The second part delves into the behavioral biases of the LMI segments which financial service providers (FSPs) need to keep in mind when designing products for them. Even though there are macro-level differences between these countries, their LMI segments show deep commonalities in behavioral biases toward financial services.

As part of the i3 program, MSC supports different stakeholders, including banks, FinTechs, microfinance institutions, wallet providers, and government departments in Bangladesh and Vietnam. MSC’s support helps these stakeholders understand and serve the needs and aspirations of the LMI segments and move them toward better financial health.

Let us start with the macro-economic and demographic data of these countries, highlighted in the graphs below.

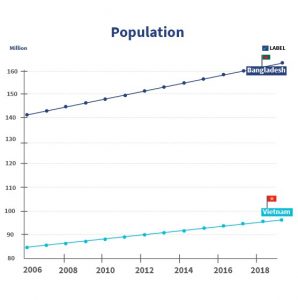

With 165 million people, Bangladesh is around 70% more populous than Vietnam. In Bangladesh, the population density is five times that of Vietnam. However, close to 60% of their population lives in rural areas. Most of the migration to the cities happens because of unemployment and education.

Both the countries fare equally well on life expectancy—Bangladesh has a life expectancy of 73.6 years. In contrast, Vietnam has a life expectancy of 75.8 years. Bangladesh is a slightly younger country, with a median age of about 27 years compared to 32 years in Vietnam. While leading economies like Europe, the US, South Korea, and Japan are aging, Bangladesh and Vietnam have the advantage of a young working population. This demographic dividend offers a distinctive edge for the GDP of these countries in the future.

Fifty percent of the population of both countries comprises women, many of whom who want to work. For example, Bangladesh’s readymade garment (RMG) sector employs nearly 4 million people, mainly from the LMI segment, 60% of whom are women. Also, see this webinar on “Successful cash support payments to the most vulnerable: Lessons from Bangladesh” for an overview of the RMG sector’s contribution.

Macroeconomic indicators

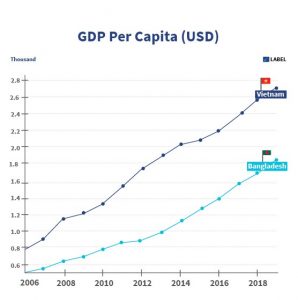

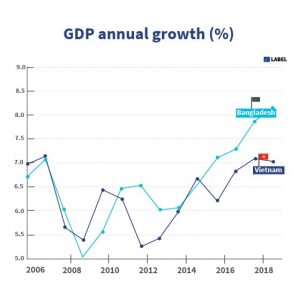

Both the countries have grown at a healthy GDP rate of greater than 5% over the past 10 years. However, the GDP per capita of Vietnam (at USD 2,785) is about 50% more than that of Bangladesh (at USD 1,961). High population and low GDP per capita translate into more people living below the poverty line in Bangladesh. The poverty headcount ratio at USD 1.90 a day (2011 PPP) as a percentage of the population in Bangladesh is 14.5% compared to Vietnam, which is at 1.9% as per 2016 data. Over the past decade, poverty in Bangladesh has been relatively higher than that in Vietnam.

Both countries have a large population from the LMI category (83% in Vietnam and 61% in Bangladesh), earning about USD 2–10 per day. The public and private sectors understand the potential of this segment, which is evident from the success stories of the likes of bKash and MoMo.

Unemployment continues to persist in both countries. The unemployed labor force in Bangladesh is about twice that of Vietnam. As of 2019, Bangladesh’s unemployment rate was 4.19%, while Vietnam’s was 2.04%.

Here, the role of micro, small, and medium enterprises (MSMEs) is essential. Bangladesh has about 6.9 million micro-enterprises, while Vietnam has about 5.5 million micro-enterprises. These smaller enterprises are job-creating engines. They employ 1–3 people each in both countries, providing employment opportunities. When we focus on small and medium enterprises (SMEs), Bangladesh has 900,000 SMEs, which is considerably more than 124,680 SMEs in Vietnam. These SMEs are the backbone of the economies of Bangladesh and Vietnam.

Lately, innovation around serving these micro-enterprises has increased. Startups offer exciting solutions that benefit these micro-enterprises around credit, e-commerce, SaaS, book-keeping, skilling, providing market linkages, etc. These solutions are expected to increase the revenues of the micro-enterprises and help them create more jobs.

Digital financial services

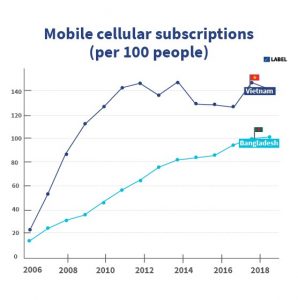

Mobile phone ownership in both countries is relatively high—141 in Vietnam and 101 in Bangladesh (per 100 people). However, smartphone penetration (of 2020) in Vietnam at 63.1% is way ahead of Bangladesh at 32.4%.

As of 2020, the percentage of internet users in Vietnam (77.4%) is higher than in Bangladesh (70.5%). This internet penetration is equal or better compared to the world population (65.9%).

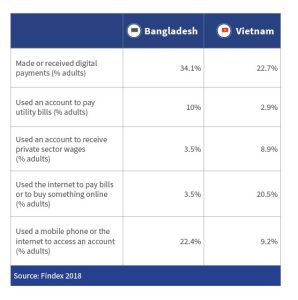

The table shows comparative data on digital payments in both countries. While Vietnam uses the internet for payments, P2P payments are most common in Bangladesh. In part because of a history of over-the-counter transactions, prominent players in Bangladesh, such as bKash, struggle to diversify from traditional use-cases of CICO (cash-in and cash-out) or P2P. In contrast, wallets such as MoMo have successfully convinced consumers to adopt more use-cases in Vietnam, though there is still scope to increase the volume, value and diverity of digital payments.

The governments of both countries continue to take the proactive steps, as so these Findex numbers are expected to rise in the coming years. For example, Bangladesh’s government has been working on transformational initiatives, such as the Parichoy e-KYC platform, BNDA interoperability project, and Startup Bangladesh. Vietnam’s government has set a goal to create firm foundations for a comprehensive digital transformation in 2021–2030. In June 2020, Vietnam approved the National Digital Transformation Program by 2025 to create a digital government, digital economy, and digital society while establishing competitive digital businesses globally. The Vietnamese government also approved a regulatory sandbox for FinTechs in September 2021 to foster innovation.

Both countries have been innovative in their drive for digital financial inclusion. But, as with most other countries around the world, they have a long journey ahead to make their LMI citizens financially healthy. However, with all these differences, the needs, aspirations and behavioral biases of LMI people are very similar in both countries.

Please tune in for our next blog, where we explain the key biases that complicate and facilitate the design of financial services in Bangladesh, in Vietnam and across the globe.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.