What role can blended finance and digital technologies play?

Climate change is one of the most pressing issues of our time. It impacts millions around the world, particularly the most vulnerable communities. We must adapt and build resilience to the changing environment to navigate this complex challenge.

Crucially, adaptation is not a one-size-fits-all solution. It requires local leadership, community involvement, and innovative approaches. This means local government agencies need to work hand-in-hand with affected communities to develop adaptation strategies. Moreover, adequate and accessible financing and technology are essential to support these actions.

We are celebrating MSC’s 25th anniversary with the tagline “International vision, local precision, for real impact.” These are not empty words. More than 99% of our 300 staff are from the countries where we operate. They understand the language, the political economy, the social norms, and the markets we serve. And they are recruited for their understanding of MSC’s mission and commitment to it. This is essential because so much of MSC’s comparative advantage lies in our ability to sit with, understand, and empathize with those who are too often simply “the target market.” Our ability to derive deep insights into the needs, aspirations, perceptions, and behaviors of poor people and vulnerable communities allows MSC to enhance the reach of communications, the uptake and usage of products and services, and their impact.

MSC consistently puts end-users at the center of the work we do. Even when we address supply-side challenges, we believe the initial work should focus on the customers first. For example, when we work on process improvement, we start with the customer journey to understand how the people who matter most experience the process. After all, market-led services are the most successful and impactful. This is particularly important in responding to the climate crisis, where we have a clear consensus that localized solutions are essential.

MSC delivers training and skill transfer as an integral part of our commitment to empower local capability and develop local talent wherever possible. Doing so allows local public and private sector institutions to break free from their dependence on external consultants and to develop and drive their own agendas with the knowledge and tools they acquire by working alongside MSC staff on a project. Inevitably, this depends on our clients’ willingness to take this approach and invest in capacity building. At the turn of the millennium, this was a priority for donors but seems to have become less important in recent times. Given the localization agenda, this decreasing emphasis on hands-on experiential learning to build indigenous capabilities seems shortsighted.

MSC prides itself on its commitment to, and history of, asking tough questions in the face of consensus or groupthink and taking the lead to shift paradigms within what is often a somewhat incestuous industry. We are always ready and willing to challenge norms or received wisdom. Our deep in-the-field approach to our work makes us particularly well suited to this role.

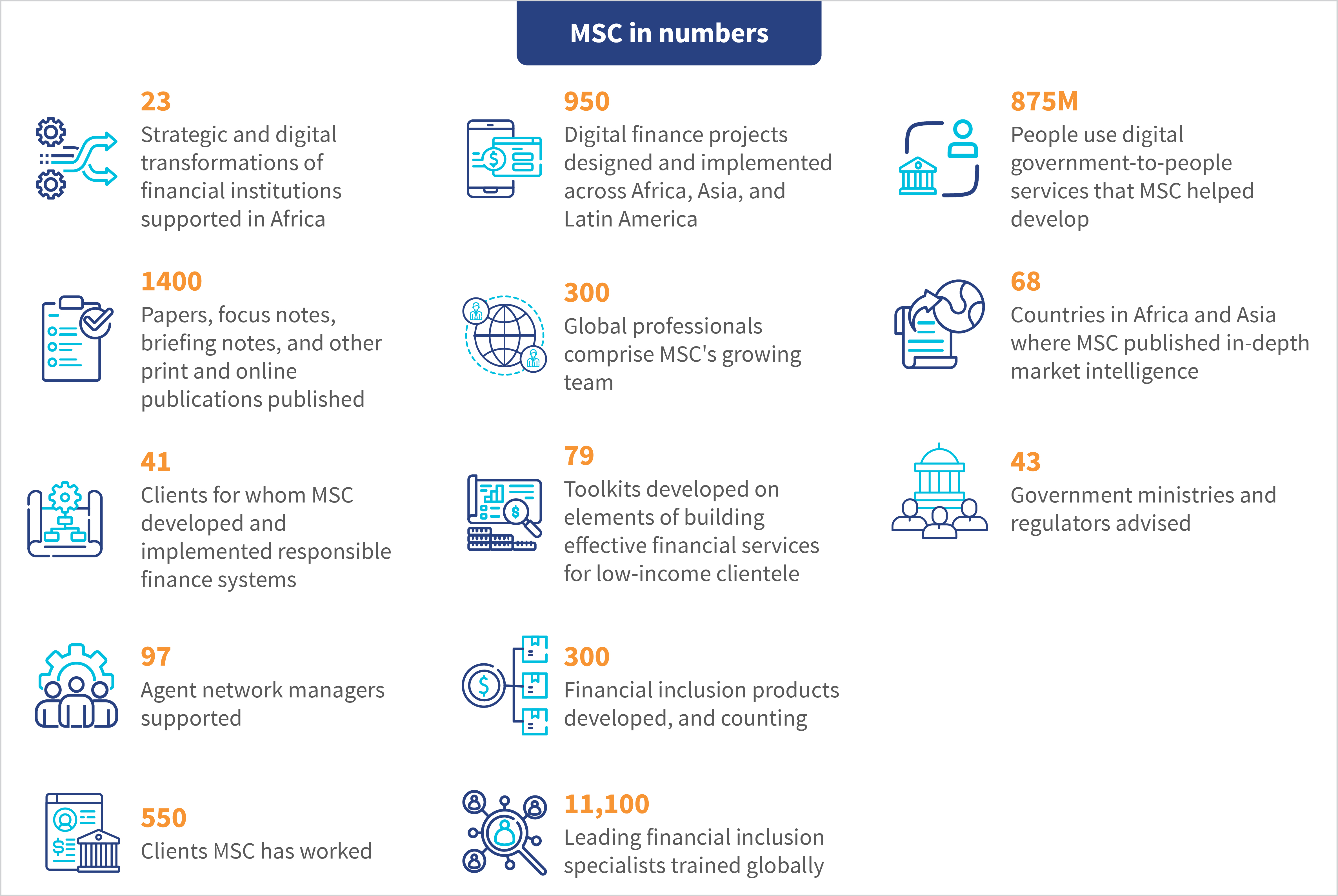

In 1998, we began to use qualitative research techniques that blended focus group discussions with participatory rapid appraisal tools to derive deep insights to build client-responsive products and services for poor people. This approach preceded the use of human-centered design for financial services by more than a decade. Indeed, industry leaders repeatedly told us to use quantitative research methods. Nonetheless, MSC’s “Market Research for Microfinance,” now Market Insights for Innovation and Design, rapidly became the go-to resource and source of training for practitioners across the globe. Today, more than 875 million people across the globe use products and services designed or refined by MSC with the use of these qualitative techniques.

Soon after MSC set up an office in India in 2006, it was clear that MFIs were expanding faster than their processes and systems could control to pursue “meaningless growth.” Furthermore, it was clear that many government-led financial inclusion programs , particularly the self-help groups (SHGs), were being challenged by the larger loan sizes and the more stringent delinquency management of these joint liability group-based MFIs. MSC foresaw and predicted a significant problem for microfinance in India as most commentators celebrated the arrival of private equity funds and the proposed IPOs of MFIs. The prediction was not difficult given the three dress rehearsals for the main event of the Andhra crisis, but we were largely a lone voice of caution in the chorus of approval that supported the commercialization and rapid growth of MFIs.

Despite the demonstrable impact on trust, fraud and consumer protection in digital financial services did not receive serious attention until more than a decade after M-Pesa’s takeoff. MSC tried to flag the challenges of fraud and consumer protection for many years, particularly for women. However, only relatively recently have these issues shed their “inconvenient truth” status and started to receive the attention they deserve.

MSC’s decentralized approach, local capabilities, and finger on the pulse of markets across Africa and Asia have positioned it well to both catalyze significant change for good and be a dissenting voice amid the clamor of consensus and groupthink. MSC’s significant achievements and contribution to the rapid evolution of financial inclusion, and now in digital governance, agriculture, climate change, gender equality, and health and nutrition, are inspiring. I hope you will forgive me for being a tiny bit proud of the outstanding teams, past and present, which have worked so hard to deliver on our inspiration, “A world in which all people have access to high-quality, affordable, market-led financial, economic, and social services in the digital age.”

As we mark 25 years of driving positive change, MicroSave Consulting (MSC) reflects on a transformative journey from 1998 to 2023. MSC has evolved into a powerhouse of impact-oriented business consulting, from pioneering projects to fostering global partnerships. Our success is a testament to our team’s dedication, clients’ trust, and partners’ collaborative spirit. We thank everyone who has been a part of MSC’s story and contributed to our growth and impact. Here is to the next 25 years of making a positive impact on the world!

Twenty-five years since its inception as “MicroSave,” MSC has made remarkable progress. Yet, we continue to contend with two powerful forces—technology and climate change. Both these forces can potentially create substantial change worldwide. However, while technology and climate change present many opportunities, they also pose significant existential risks.

We need to think creatively outside the norms and silos that constrain us. The clock is at one minute to midnight. We must act before it is too late.

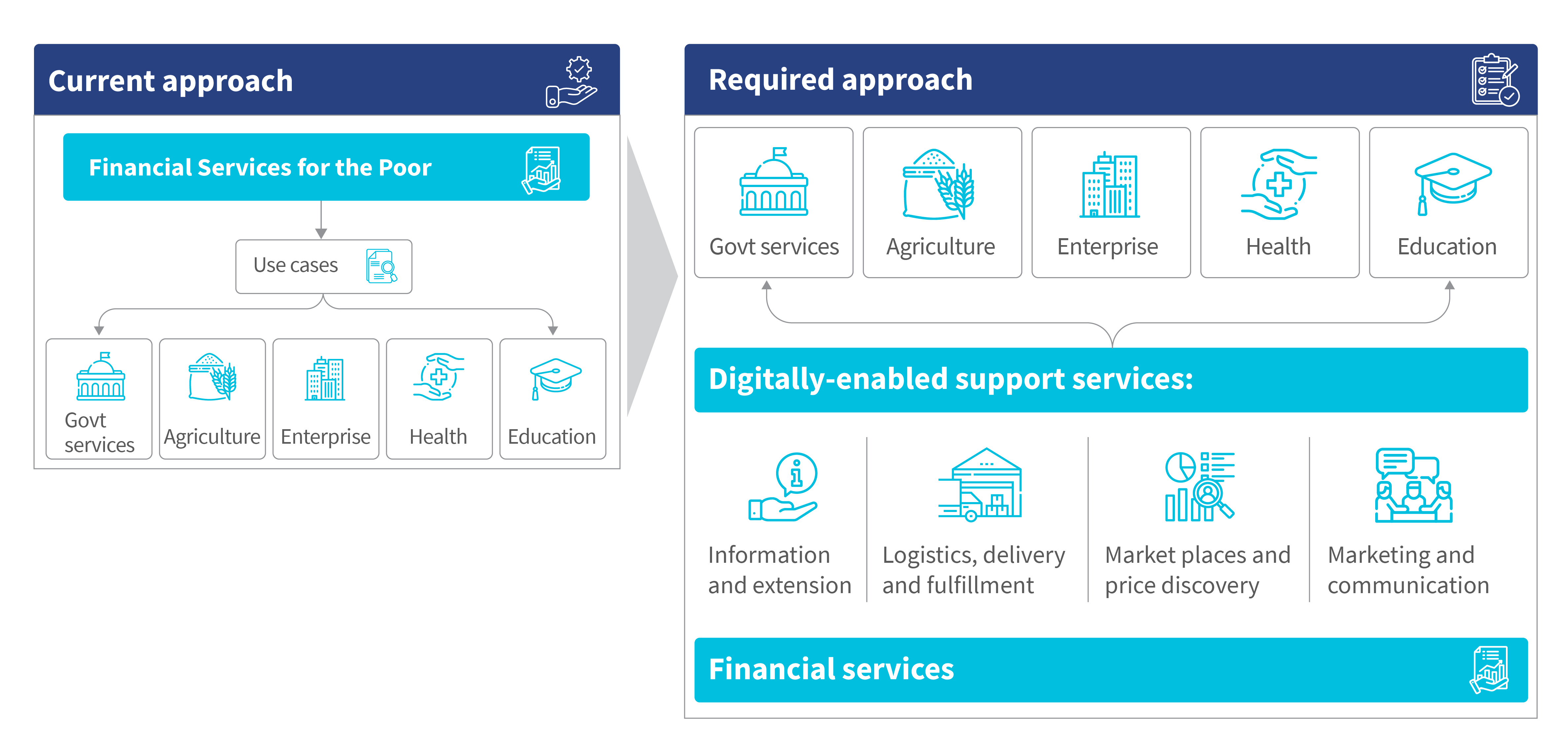

The technological revolution has allowed MSC to broaden its work to answer the long-ignored, elephant-in-the-room question: “Financial inclusion for what?” Access to a bank account is not useful by itself, particularly if the customer does not fully trust the formal or digital financial system. We must design and deliver financial services that poor people want and can use to manage their money better. We must use FinTech front ends to offer financial services in a way that corresponds to their mental models and aligns with them. Moreover, these financial services must integrate with the real economy and facilitate participation in it, so that people are not just financially – but also socially and economically – included.

The digital revolution provides the opportunity to do this. This means that instead of viewing inclusive financial services for the poor as a vertical, we need to view them as an enabler. Financial services are a small but important cross-cutting support component of larger, digitally-enabled, real-world economy activities if viewed this way. Thus, financial services become an enabling ancillary function driven by real needs that arise from the real economy—for which digitally enabled support services play an increasingly important role.

This approach also allows us to deliver real value to poor and vulnerable communities who face profound changes in their livelihoods due to the climate crisis. MSC’s recent work with CGAP, Decodis, and FSD-Africa examined climate change’s impact on poor farmers in Bangladesh, India, and Nigeria. The findings were shocking. Droughts and flooding are increasing in frequency and intensity, often within the same cropping season. Slow-onset desertification and salination are inescapable. Smallholder farmers are facing a relentless erosion of their income and asset base, and lack the resources to adapt to increase their resilience to these changes.

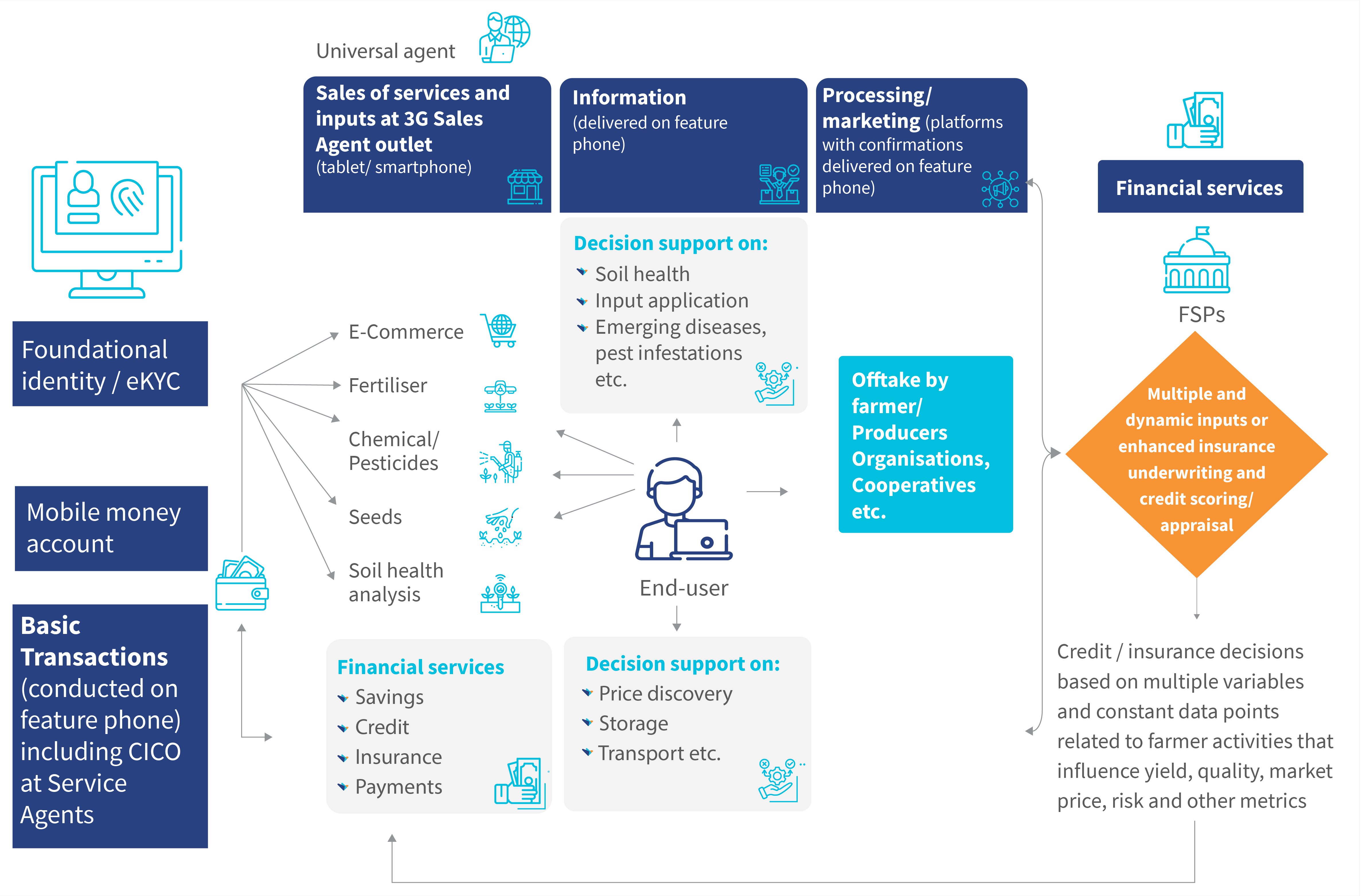

Technology and financial services must be accessible, suitable, and affordable for marginalized farmers located in remote areas often untouched by the technological revolution to successfully transform agri-food systems. We must not exclude these communities from the fourth industrial revolution. “Universal” or sales agents and “transaction” or service agents must combine forces to ensure this. While sales agents will help vulnerable and excluded communities access technology-based products and services, service agents will allow them to use these services daily.

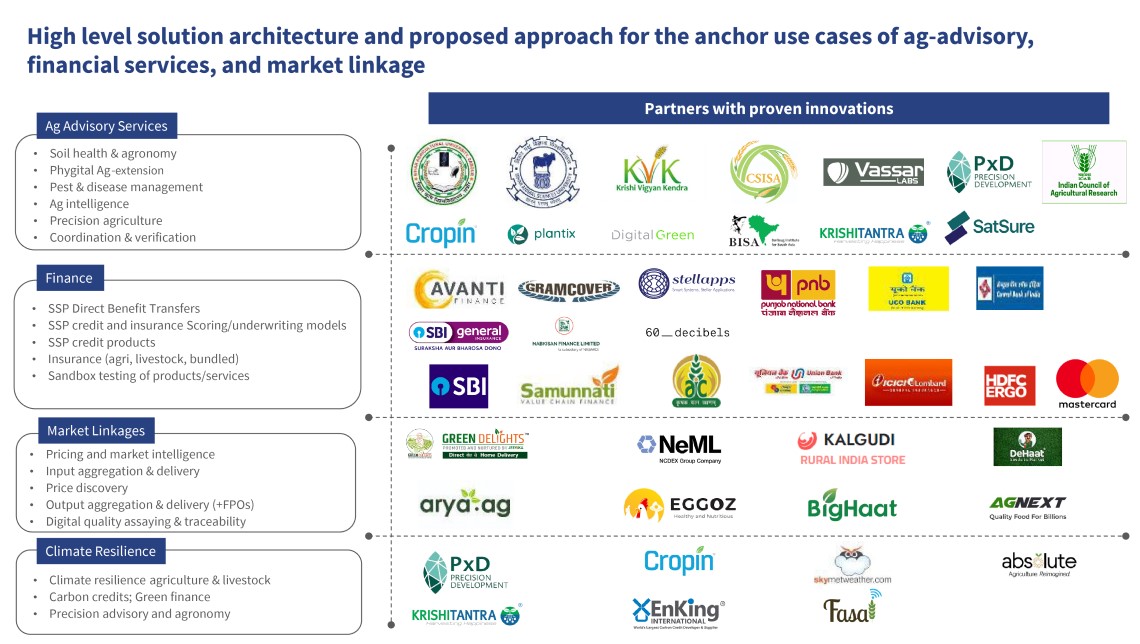

This type of approach depends on effective digital public infrastructure. Foundational digital identity allows a digital “agri stack” to track farmers’ land holding or rental, soil health, and crops, livestock, or both. Based on this, it can provide a range of farmer-specific information to support input and output processing, marketing, and alerts on emerging pests, diseases, and more, as well as how to best respond to these. This type of integrated stack can then provide data to financial service providers and help farmers access the credit, insurance, payments, and savings services they need.

Although it seems easy, it is not. Farmers are notoriously, and understandably, risk-averse and often unwilling to change. However, it is not entirely impossible. MSC has been working with the Federal Ministry of Agriculture and Farmers’ Welfare in India to implement Agri Stack. We have also been working with the Government of Bihar to design and implement the Digital Farmer Services (DFS) platform. The DFS will integrate and diffuse innovations, use and build on shared data and complementary services, create a digital public infrastructure, and use open architecture.

India has a remarkable digital ecosystem that gives it a head start to transform agri-food systems to help farmers. Many core digital technologies and biotechnologies are already available to help farmers increase productivity and adapt to climate change. However, the real challenge lies in the diffusion of these innovations – how we enable and drive their uptake and usage – which will require a deep understanding of farmers’ needs, aspirations, perceptions, and behaviors.

However, the climate crisis will also require farmers to adapt. We will need a localized and participatory approach to ensure that planned and autonomous adaptation strategies complement rather than conflict and bring truly beneficial and transformative change. Household-level autonomous adaptation will require investments that poor households typically cannot afford. Even when smallholder farmers have access to credit, it is usually short-term and limited in value. Thus, such credit is unsuitable and inadequate to finance significant adaptation that will result in long-term resilience.

If we cannot use technology and the long-promised-but-rarely-delivered international climate adaptation funds to deliver higher value and longer-term finance, farmers will only be able to afford limited measures. Many of these limited measures will prove to be maladaptive. They will provide some short-term alleviation but compound the long-term problem. We must reimagine financial services to take a systems perspective that encompasses all four major elements found in most economies: (i) the formal financial sector; (ii) embedded finance; (iii) informal or community-based finance, and; (iv) state finance, which includes international funds.

Technology and climate change will not only affect agriculture. Similar challenges and opportunities already exist for enterprise, health, education, and government services. The key to addressing these challenges will be to understand and involve local communities as they define the problems and potential solutions.

And MSC is responding accordingly. We have been investing significant resources to build our internal capability and add value in this rapidly transforming landscape. We have been deepening our partnerships in response to the complexity of climate change and its potential impact on vulnerable communities. We have been adapting our acclaimed Mi4iD tools to incorporate the perspectives of vulnerable communities, and to support localized, participatory responses to the emerging and rapidly evolving realities they face. We have been scaling up our Center for Responsible Technologies team. This team is specifically focused on the role of artificial intelligence (AI)—both to deliver AI-enhanced value to our clients and projects and to improve the quality and speed of our internal processes to deliver first-class reports and client delight.

It is a very interesting time to be alive… to all the possibilities.

Everyone claims “thought-leadership and impact,” so I sympathize as you roll your eyes. But give me a few minutes of your precious time to “explain my claim.”

Twenty five years ago, MicroSave-Africa was established to help African microcredit providers diversify their mono-offerings to include savings products. The clue was in the brand. However, in 1998, East African microcredit organizations suffered primarily from enormous client churn. This was because their products were unsuitable and expensive for their target market. MicroSave’s mission quickly changed to helping financial service providers understand and address the low-income market.

Catalyzing a market-led approach for the industry

Initially, we focused on the demand side and tailored the approach I had used in Asia—participatory rapid appraisal tools set in focus groups—to derive deep insights into the needs, aspirations, perceptions, and behaviors of poor people. We codified this into the acclaimed “Market Research for MicroFinance” toolkit, which was later used by hundreds of MFIs and consultants worldwide. Indeed, a competitor design company described it as “the grandfather of human-centered design.” To this day, I am not sure if that was a compliment or a slight!

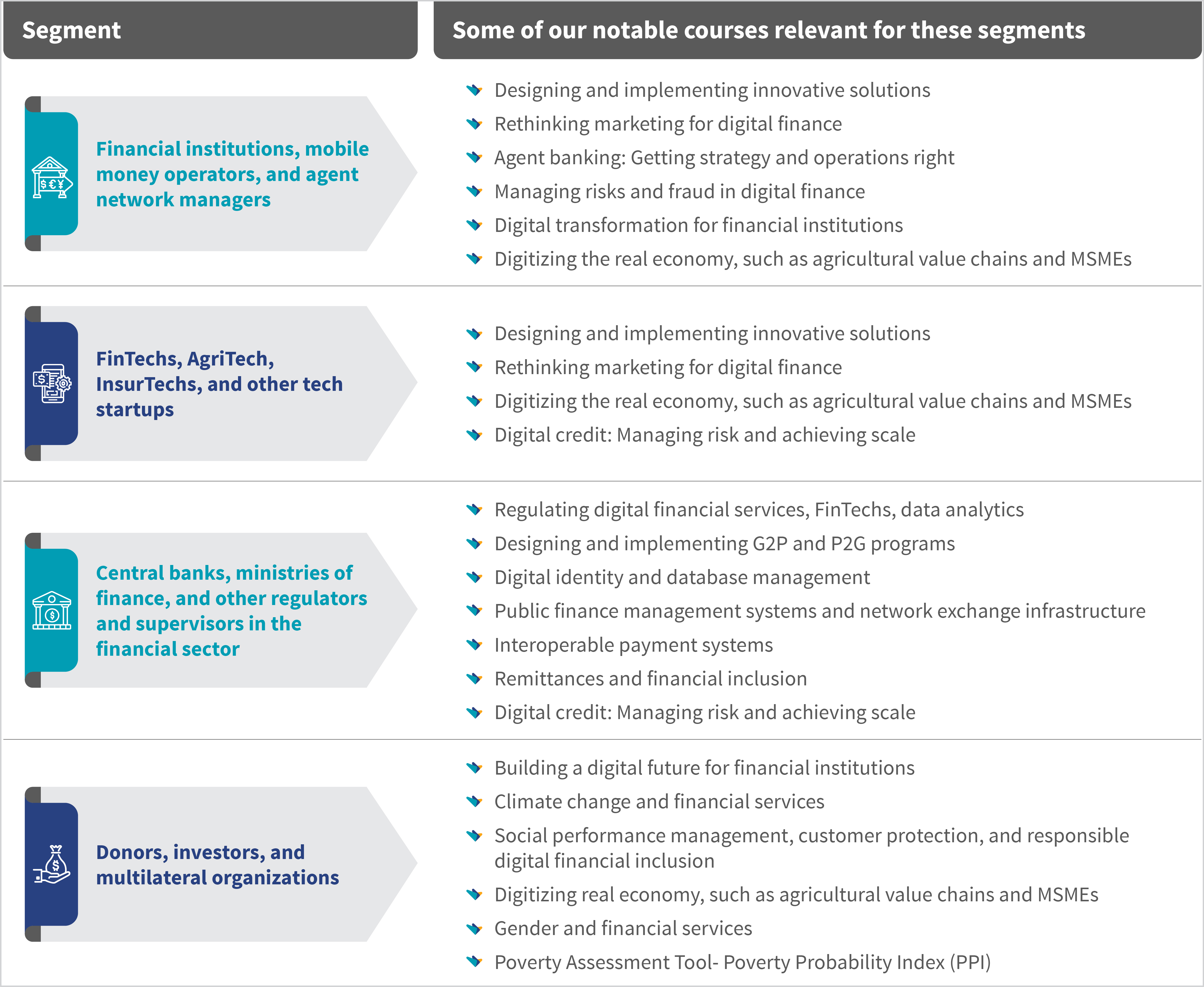

But of course, addressing the demand side alone is not enough. We needed to reengineer the supply side as well to be truly client-responsive. We collaborated with leading experts to build, test, and disseminate a range of toolkits on almost every aspect of a market-led organization. This included strategic business planning, process analysis, product marketing, and staff incentives. These toolkits are updated continuously to reflect the rapidly evolving market. They remain a core part of MSC’s internal and external training programs through what is now The Helix Institute at MSC (see table below).

Equity Bank and digital transformation

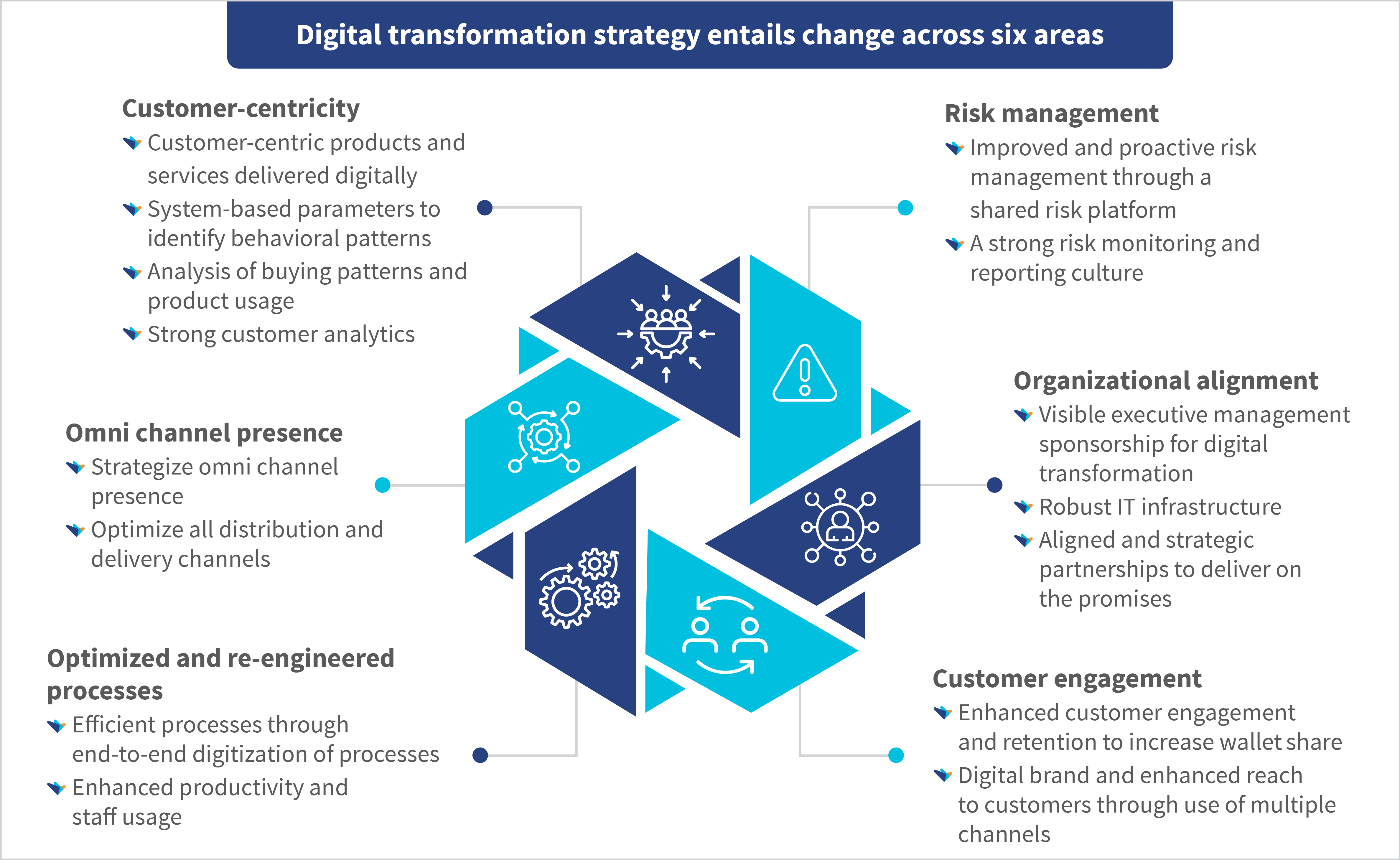

Equity Bank emerged as the poster child for MicroSave’s work to transform institutions—first on a market-led basis and then to be digitally led. When Equity Building Society first approached us in 2001, it had 109,000 customers. Today, it serves more than 15 million people in six countries, and 99% of its transactions in Kenya occur outside its branches. It was and continues to be a real privilege to work with Equity Bank and learn alongside it. The bank remains an inspiring beacon of how formal financial institutions can profitably serve the low- and moderate-income mass market if they use the digital revolution’s potential. Indeed, the lessons we learned working with Equity Bank form the basis for our extensive digital transformation practice. You can access a free introductory webinar on digital transformation here.

Therefore, it was perhaps reasonable that FSD-Kenya and CGAP’s final evaluation of the MicroSave-Africa project concluded: “MicroSave has made an undisputed contribution to the availability of better financial services for poor people across the globe. It has been good value for money, producing a wealth of outputs within the region and beyond.”

The acceleration and optimization of agent networks

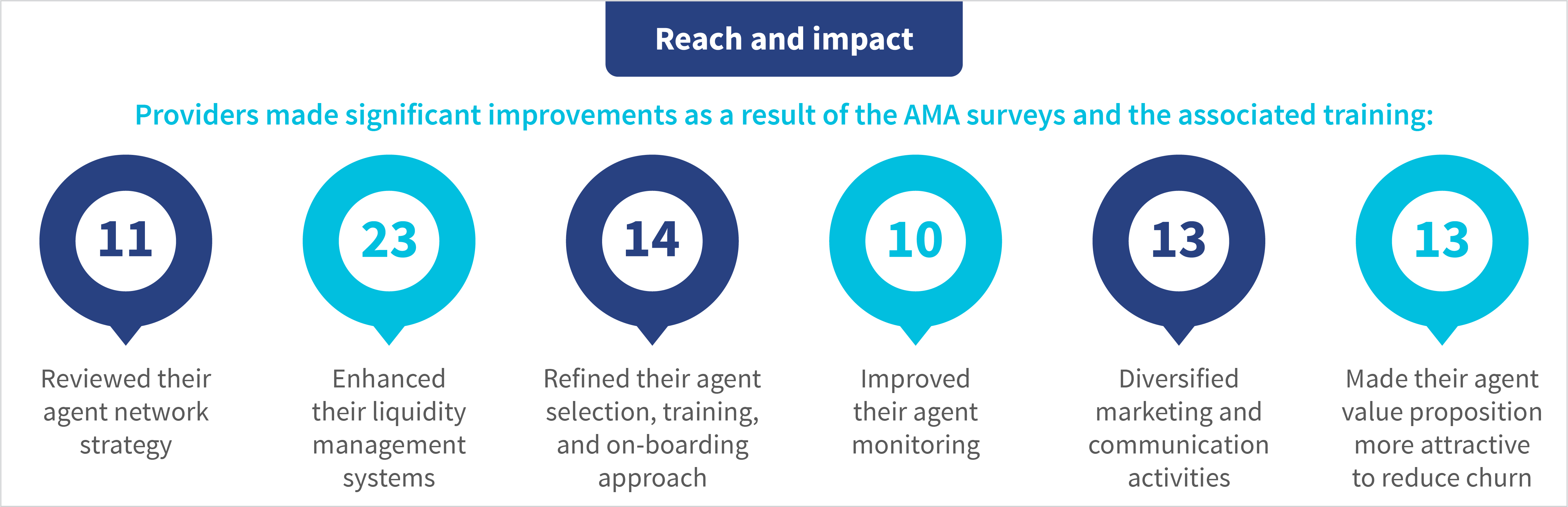

The creation or use of effective agent networks is a key part of digital transformation. MSC has worked with and trained leading mobile network operators, banks, and third-party agent network managers. These efforts have been groundbreaking.

It all started with M-PESA. MSC sat on the initial Steering Committee and conducted preliminary customer research as part of the pilot testing. It highlighted the importance of agent support and monitoring.

MSC collaborates with governments on public policy in various areas, such as food security, agriculture, health, energy, and financial inclusion. We have partnered with various countries to develop, evaluate, and implement vital digital public infrastructure and the programs they support. These countries include Bangladesh, Ethiopia, India, Indonesia, Malawi, and Zambia. Our efforts focused on the foundational infrastructure and the development and rollout of government-to-person (G2P) programs.

Driving policy and impact at real scale

1. Malawi and Zambia: We conducted digital readiness assessments and formulated detailed roadmaps for the countries’ transition to digital G2P payments.

2. India:

We contributed to PAHAL and Ujjwala LPG (cooking gas) initiatives. Our efforts helped eliminate 33 million fraudulent beneficiaries from the system;

We reviewed the National Food Security Act (NFSA) and provided recommendations to enhance nutritional outcomes for 800 million people;

We offered crucial insights for the Bantuan Pangan Non-Tunai (BPNT) food subsidy transfer program. It had 5 million beneficiaries in 2018, which has now increased to 20 million beneficiaries. It has been renamed to the Sembako program.

Our advisory role led to the formation of a strategy for the electronic know-your-customer (e-KYC) process. The strategy is expected to benefit 60 million unbanked individuals in Indonesia.

MSC uses deep market insights derived from our human-centered design and process analysis toolkits to devise innovative solutions, conduct preliminary tests, and solve complex challenges. We also provide monitoring and evaluation services that enable our clients to optimize their systems and operations.

Driving and scaling innovation

MSC’s leadership on digital inclusion, it is unsurprising that we have been involved as technical service providers to labs or accelerator programs in Bangladesh, India, Senegal, and Vietnam. These labs are differentiated by their resolute focus on nurturing startups. They have a clear and consistent commitment to serve the low- and moderate-income (LMI) segments. In India, the FILab has supported 50+ startups that have positively impacted the lives of 47.7+ million LMI people and raised USD 266.5 million in funding in just five years.

A center of excellence for professional development

As with all leading consulting firms, MSC experiences staff churn of 10-20% per annum. A few staff leave because of the pace of organizational growth and change, or the pressure of our commitment to excel in all that we do is too much. Several leave for higher studies and use their time and experience with us to gain enrollment for postgraduate studies in prestigious universities—typically in the US or the UK. Some leave to use their experience with us to set up their own startups—including the remarkable FarMart and Flow. But many leave to join other organizations—most commonly UNCDF, IFC, and GSMA. You can find a library of slides and videos of our alumni as they discuss their work and how their time at MSC helped them do it here.

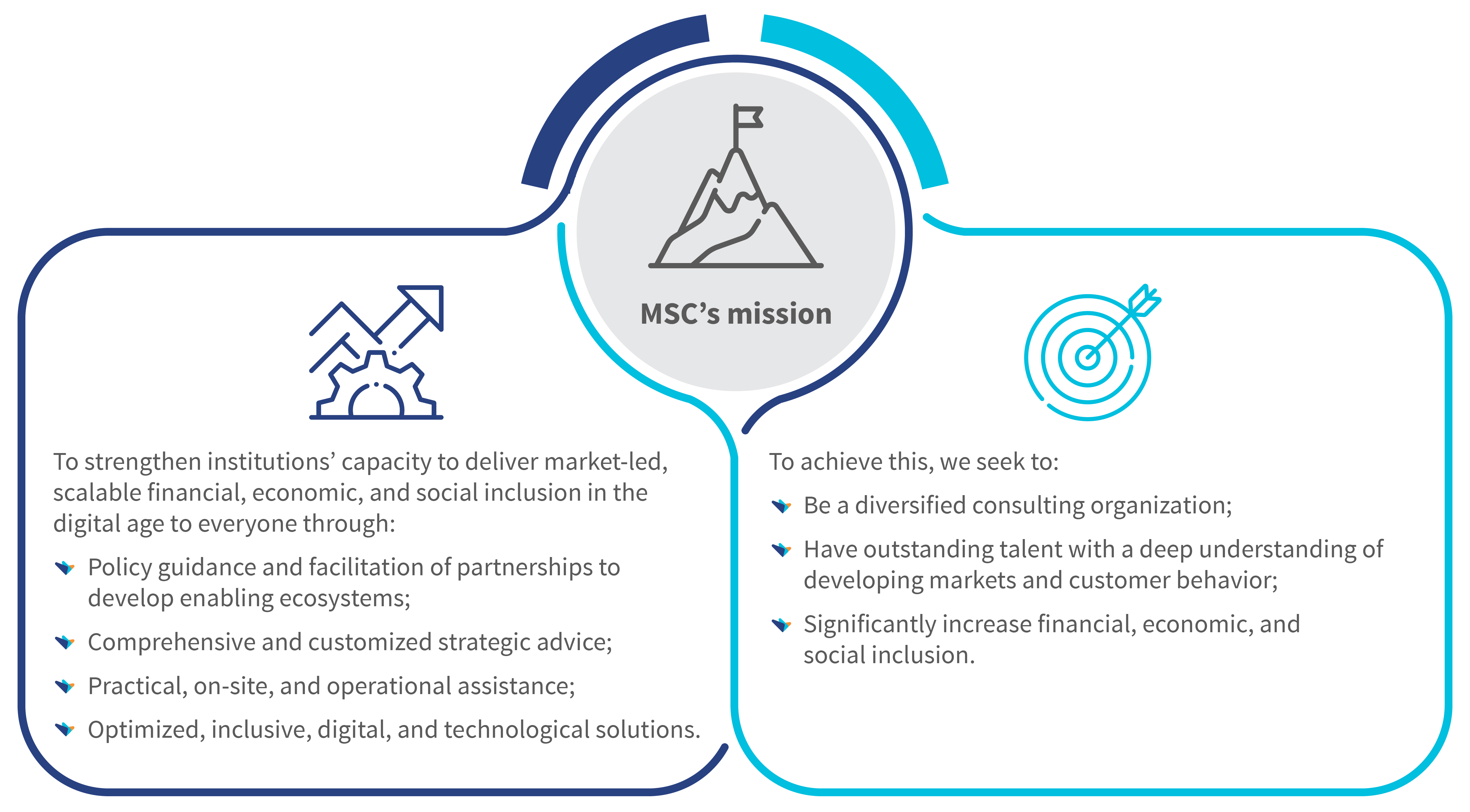

Initially, we found it disheartening to spend years building the knowledge, skills, and professionalism of bright young individuals, only to see them whisked away by international agencies that now largely operate as rival consulting companies with higher salary structures. We are a little more sanguine now. We have to view MSC as a respected and valued center of excellence for professional development with outstanding graduates who make important contributions to global development and our core mission: “To strengthen the capacity of institutions to deliver market-led, scalable financial, economic, and social inclusion in the digital age to all people.”

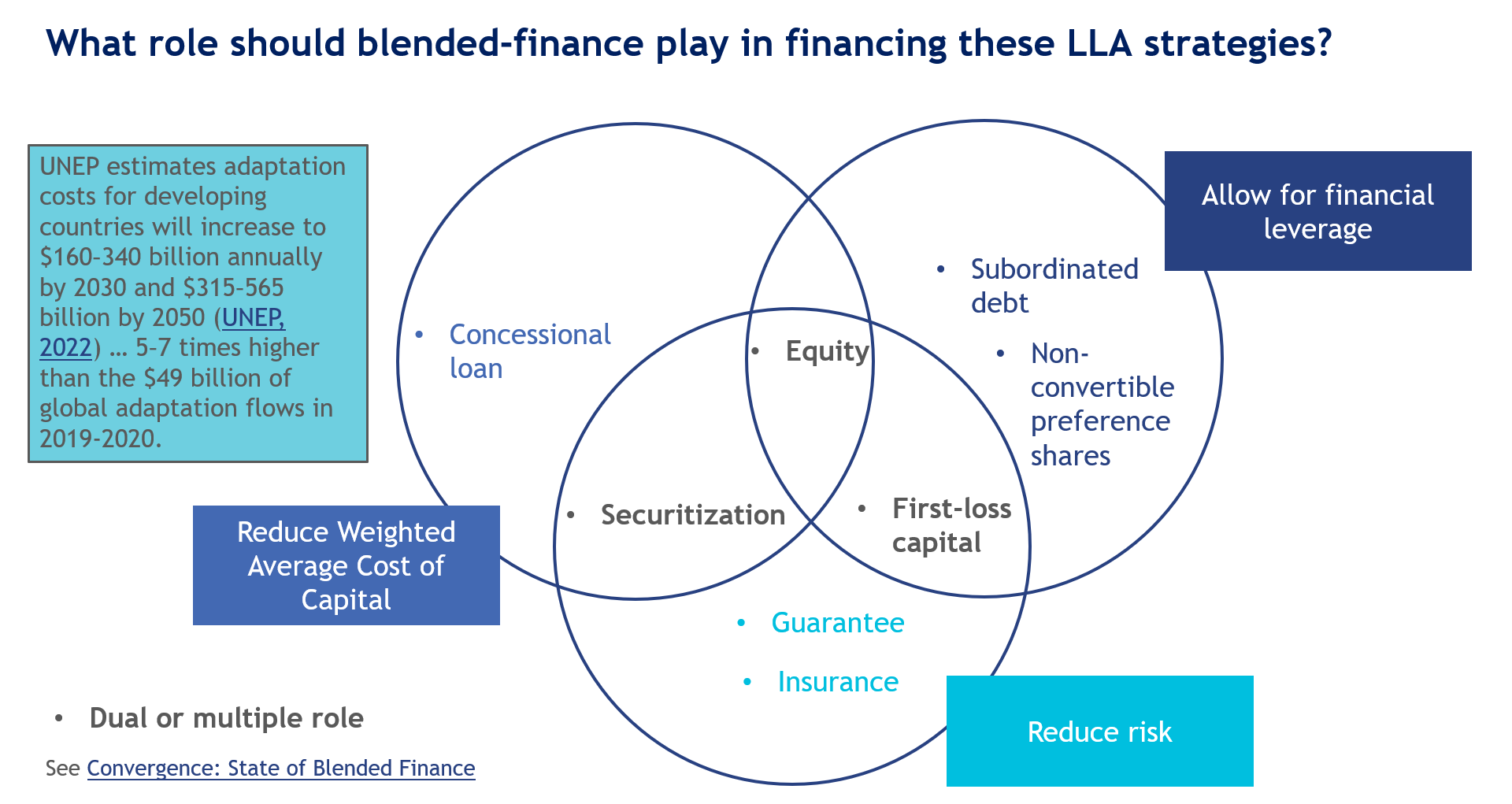

The global community spends just USD 30 billion annually on climate adaptation. However, when you put this figure into perspective, it represents a mere 10% of the projected USD 387 billion required each year (UNEP, 2023). Furthermore, a limited proportion of this funding actually reaches developing countries and finances locally-led initiatives.

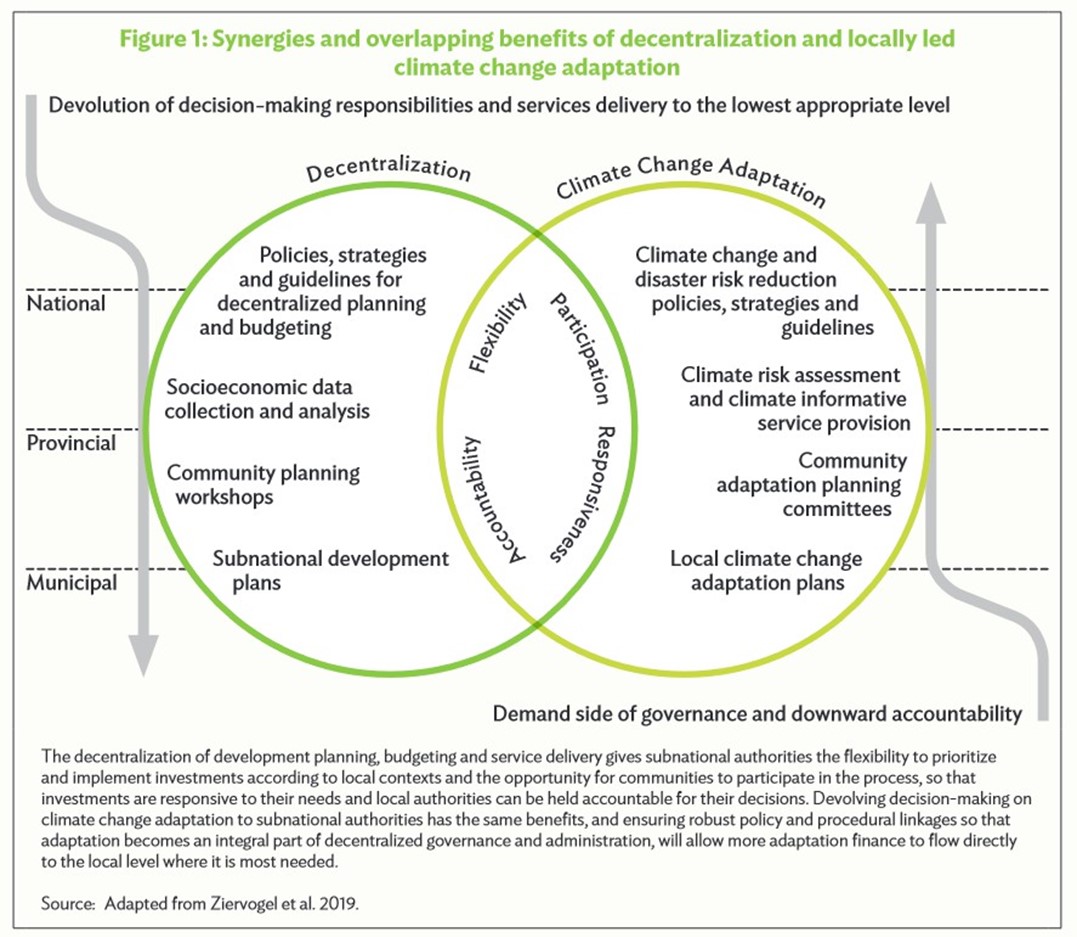

Locally-led adaptation is key. The most effective adaptation measures are those tailored to local needs, informed by community priorities, and implemented at the grassroots level. This localized approach not only responds to the immediacy of climate change impacts, but also ensures adaptation strategies resonate with the community’s lived experiences. However, as with all strategies, certain barriers can impede progress, such as ecological and physical constraints, limitations in knowledge and resources, and social dynamics. Yet, despite these challenges, several standout characteristics define successful adaptation initiatives: a commitment to addressing the foundational causes of vulnerability, a drive toward community-led innovations, a strong inclination toward decentralized governance, a relentless focus on overcoming social barriers, and devolved finance.

Devolved climate finance is a mechanism designed to redirect climate finance to where it is most impactful: the local level. When local entities have resources and decision-making authority, they are empowered to spearhead climate resilience and adaptation efforts. Countries, such as Kenya, Mali, and Senegal, are testaments to this approach’s efficacy, as they have incorporated decentralized finance mechanisms into their climate strategies. Central to the success of such mechanisms are principles, such as community-led planning, support to established institutions, emphasis on social inclusion, and a steady focus on public goods. Yet, several challenges persist, such as the fragmentation of funds, potential compromises in budget data quality, and issues of capacity and coordination.

The private sector is an often overlooked but critical player in adaptation financing. If enabled by international, philanthropic, and public sector funds, private finance’s vast potential could usher in a new era of progress towards sustainable development goals and impactful climate adaptation.

Blended finance, which combines public and private sector investments, offers a promising avenue to reduce risk and the weighted cost of capital, and to leverage capital to catalyze innovation and market transformation, at scale.

Over the past 25 years, a range of organizations, including MSC, have been instrumental in integrating local communities into the development, financing, and monitoring of projects. It is imperative to harness these accumulated insights to advance locally-led adaptation planning. A comprehensive approach should prioritize community involvement and incorporate existing regulatory, policy, climate science, and financial dimensions alongside the governance to monitor, evaluate, and learn from the implementation of locally-led adaptation plans.

We need a methodology that harmonizes national policies with local governance and future climate forecasts to provide a robust framework. A pivotal aspect of this strategy involves the diversification of financing mechanisms, which range from international climate funds to community-based organizations, and thus ensures an integrated approach to both planned and autonomous adaptation efforts.

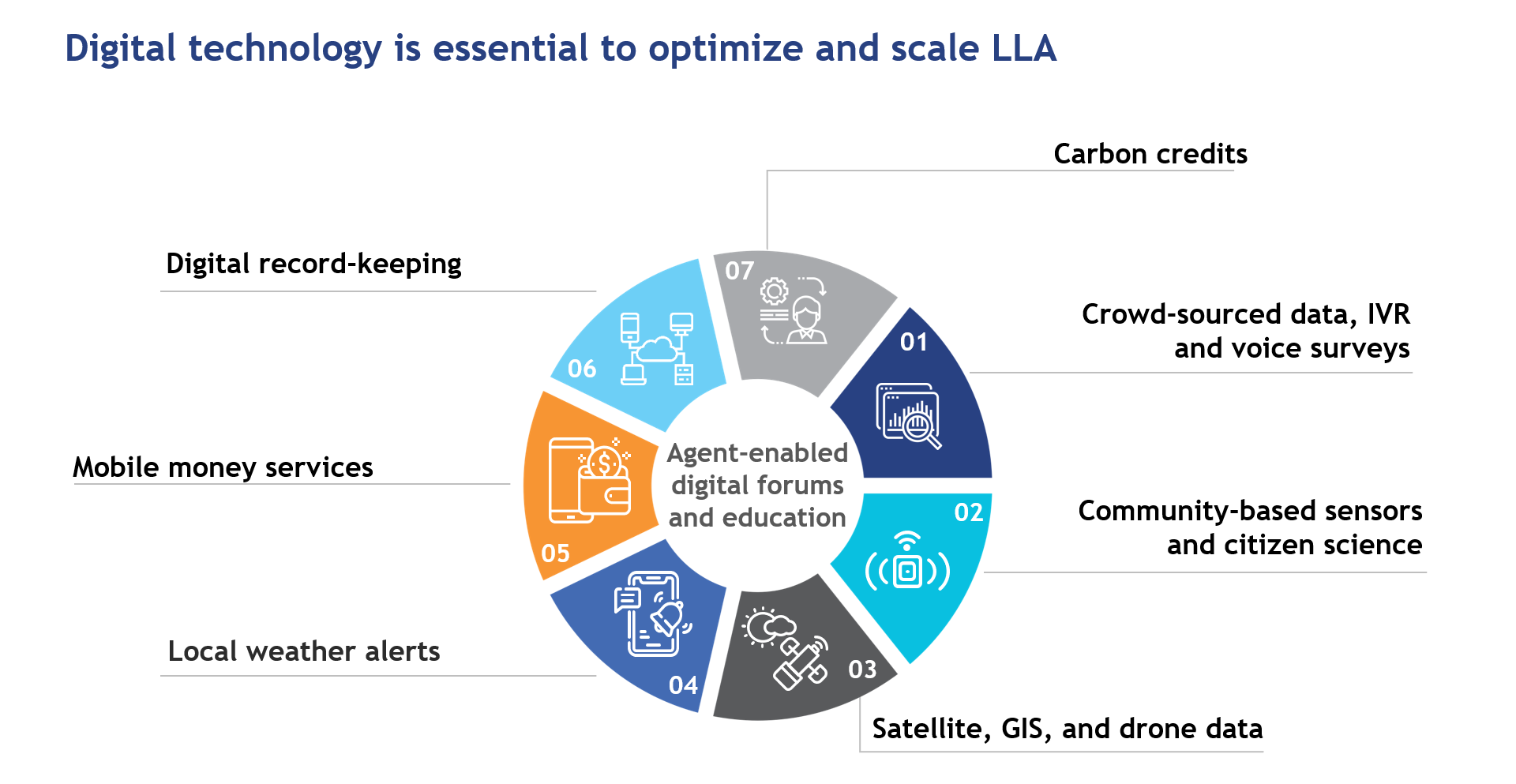

Digital technologies can potentially facilitate, accelerate, and mainstream locally-led adaptation planning and the governance functions of monitoring, evaluation, and learning, to refine and optimize adaptation initiatives. Cash-in cash-out mobile money agents, microfinance institution staff, or agricultural extension agents in climate change-vulnerable areas could become nodal points to help develop LLA plans. They can provide access to key data and insights for the participatory planning process, and then enable the management and governance of the implementation of those plans. Perhaps most importantly, they also often are embedded in the communities most impacted and therefore may have the trust and access to local communities that can subsequently inform appropriate solution design.

This approach to LLA would entail these agents acting as “catalysts of change” who use and facilitate access to a range of digital technologies. These technologies can be deployed to support and scale LLA planning and monitor the implementation of those plans for performance-based payments. AI-enabled online forums in local languages could offer opportunities for communities to share knowledge, discuss challenges, and co-create adaptation strategies. Mobile platforms could be used to deliver educational content on adaptation practices suitable for local conditions, as well as a range of financial services and payments against performance or for carbon offsets.

Community-based and operated weather sensors, satellites, drone services, and feedback platforms could be leveraged to develop community-led plans as well as provide a means to report on progress and challenges in real-time. These technologies can provide insights and recommendations to improve adaptation initiatives alongside local and national climate adaptation policies. Thus digital technologies could help with the development, monitoring, and governance of implementation of adaptation plans and enable smart contracts to reward the achievement of performance goals.

Digital technologies could complement the effectiveness of LLA strategies by providing increased accessibility for rural communities as well as for the MFI staff or CICO and agricultural agents that serve them. However, these digital tools must align with the local context, needs, and language to foster community participation, knowledge sharing, and sustainable adaptation practices.

Particular care must be taken to ensure that the poorest and most vulnerable have the opportunity to participate and/or lead in the planning and monitoring exercises (Jones, 2010).

We look forward to partnering with organizations that are prioritizing locally-led adaptation and identifying ways that digital technologies can support their impact.

We are celebrating MSC’s 25th anniversary with the tagline “International vision, local precision, for real impact.” These are not empty words. More than 99% of our 300 staff are from the countries where we operate. They understand the language, the political economy, the social norms, and the markets we serve. And they are recruited for their understanding of MSC’s mission and commitment to it. This is essential because so much of MSC’s comparative advantage lies in our ability to sit with, understand, and empathize with those who are too often simply “the target market.” Our ability to derive deep insights into the needs, aspirations, perceptions, and behaviors of poor people and vulnerable communities allows MSC to enhance the reach of communications, the uptake and usage of products and services, and their impact.

We are celebrating MSC’s 25th anniversary with the tagline “International vision, local precision, for real impact.” These are not empty words. More than 99% of our 300 staff are from the countries where we operate. They understand the language, the political economy, the social norms, and the markets we serve. And they are recruited for their understanding of MSC’s mission and commitment to it. This is essential because so much of MSC’s comparative advantage lies in our ability to sit with, understand, and empathize with those who are too often simply “the target market.” Our ability to derive deep insights into the needs, aspirations, perceptions, and behaviors of poor people and vulnerable communities allows MSC to enhance the reach of communications, the uptake and usage of products and services, and their impact.

We built on this to design and implement the

We built on this to design and implement the