In Indonesia, large-scale social restrictions, falling consumer demand, and massive layoffs have affected all sectors of the economy. For the 64 million MSMEs operating in the country, this has caused severe disruptions in the supply chain and a drastic reduction in revenues.

Our report highlights the impact of COVID-19 on the MSME sector in Indonesia, particularly on micro-enterprises. We also provide policy recommendations to support the recovery of this sector.

* 0:00 – 2:30 – Graham Wright – Welcome Note, Introductions of the esteemed panelists, and introduction to the agenda – Role of digital financial infrastructure in situations like the COVID and beyond

* 2:30 – 3:30 – Graham Wright – Highlighted India’s achievements on its digital financial infrastructure by stating 3 recent achievements and introduced Topic 1: Role of digital financial infrastructure in situations such as COVID-19 pandemic

* 3:30 – 4:00 – Question 1 for Mr. Rakesh Ranjan NITI Aayog – We understand that payments under the relief package for COVID -19 were made to the beneficiary’s accounts April 1 onwards. Given the scale, how was the cash transfer to over 200 million women managed using Jan Dhan accounts?

* 9:42 – 10:10 – Graham Wright – Introduction to Topic 2:Establishing India’s digital infrastructure

* 12:20 – 12:40 – Question 2 for Mr. Rakesh Ranjan – Most countries want to develop a robust digital financial infrastructure – but (as we know) this is not an easy task. What allowed India to pull this off?

* 17:30 – 18:25 – Question 3 for Mr. Dilip Asbe NPCI – NPCI’s journey has been a hectic and very successful one. What were the key enablers and the key milestones?

* 23:30 – 24:55 – Question 4 for Mr. Rajnish Kumar – SBI is the largest bank implements policies of the government, has integrated with a range of payment systems, and has developed a huge agent network. What did it take at SBI to ensure these happened and what was the most challenging?

* 34:05 – 34:40 – Graham Wright – Introduced topic 3: Practical insights from rolling out the (emergency) cash support transfers, covering both CICO agents and payment infrastructure * 34.44 – 35.20 – Question 5 for Mr. Amitabh Kant – The payments were made to beneficiaries in April and May, and this is in progress right now as we speak for June. What are some of the challenges that the government faced?

* 41:00 – 41:50 – Graham Wright – Significant increase in the agent network and their roles

* 41:51 – 41:42 – Question 6 for Mr. Rajnish Kumar – How has SBI managed these cash transfers? Did you also see a regional variation? How did SBI support its remote branches and its agents during this time?

* 47:10 – 47:30 – Question 7 for Ms. Greta Bull from The World Bank For emergency cash support transfers, which you have seen in other countries as well, what are the lessons/best practices that governments could learn? In particular, how can governments extend these payments into rural areas?

* 55:11 – 56:34 – Graham Wright – Topic 4: What might other countries learn from India?

* 56:35 – 57:10 – Question 8 for Mr. Hari Menon from Bill and Melinda Gates Foundation What according to you are the key points that make the digital infrastructure in India, unique? What can other countries learn for both during the pandemic and more sanguine times?

* 1:04:46 – 1:05:19 – Question 9 for Ms. Greta Bull from The World Bank – How would you compare India’s journey with others? What are the key lessons that other countries can take away?

* 1:09:00 – 1:09:25 – Question 10 for Ms. Greta Bull from The World Bank – India’s journey has been long and it is still underway. While we understand a solution of this scale will take some time to shape up, what might governments do to quicken this pace? Any quick wins that they can take in the journey to digitize G2P transfers?

* 01:12:26 – 1:12:50 – Graham Wright – Introduction to Topic 5: How can countries build digital infrastructure amid the Covid-19 crisis?

* 1:12:55 – 1:13:07 – Question 11 for Mr. Dilip Asbe NPC – How has COVID 19 has challenged the digital infrastructure and what will change after this emergency?

* 1:18:06 – 1:18:33 – Question 12 for Mr. Amitabh Kant – How can India support other developing nations?

* 1:23:36 – 1:24:40– Question 13 for Mr. Hari Menon – What are key elements that can drive the digital financial infrastructure, other than scalability as pointed out? What initiatives are the BMGF supporting to help governments roll out digital financial infrastructure?

* 1:29:30 – 1:29:50 – Question 14 for Mr. Rakesh Ranjan – The digital divide is really important and in the Indian subcontinent, the exclusion of women is often a problem. What is India doing to ensure that women are also included in the digital infrastructure?

* 1:32:50 – 1:38:33 – All the panelists Concluding thoughts and comments

This blog is about a startup under the Financial Inclusion Lab accelerator program, which is supported by some of the largest philanthropic organizations across the world – Bill & Melinda Gates Foundation, J.P. Morgan, Michael & Susan Dell Foundation, MetLife Foundation and Omidyar Network.

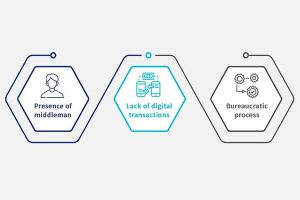

Around the world, small and marginal farmers get a meager share of the overall value created in the agriculture supply chain. This is mainly due to three critical inefficiencies, as highlighted in Figure 1. PayAgri is a platform for farmers that works to overcome them and optimize returns for the farmers.

The founders of PayAgri, Rajeev J. Kaimal and Rajkumar KVM started their venture based on a strong need for a holistic solution that could improve the economic condition of farmers. They felt that piecemeal solutions are unlikely to create a desired and sustainable impact.

Figure 2: Rajeev J Kaimal and Rajkumar KVM, the founders of PayAgri

Rajkumar is an investment banker who comes from an agricultural family in Theni, Tamil Nadu. Rajeev G. Kaimal worked in the rural banking and financial services space for over 18 years. In 2014, Rajeev became the founding member ofSamunnati, a finance company that worked in the dairy value chain. Rajkumar joined later as a consultant to help build products and set up the company’s trading division. They saw the plight of small farmers in India as a problem that needed a solution—one they sought in the agricultural space.

Their shared interest and common passion in agriculture prompted them to conceptualize PayAgri in February, 2017. Its objective is to use technology to create an inclusive economy that takes care of the aspirations of every player in the agriculture value chain without compromising on the interest of farmers.

Connecting farmers to lucrative markets

At present, small and marginal farmers take the smallest share of the consumer’s rupee in the entire value chain—under 30%. A large part of that goes to various intermediaries and is absorbed in market (mandi) fees and commissions of the Agricultural Produce Market Committee (APMC) markets (Figure 3). While intermediaries perform a critical role in the value chain, some optimization is necessary to help small and marginal farmers get a larger share of the overall pie.

Typically, the farmers get fair prices for their grade A produce easily through retail vegetable vendors. Yet they struggle to find a market for grade B and grade C produce. Other factors like delay in payments by traders, non-transparent pricing, and limited technology go against the interest of small and marginal farmers.

Figure 3: Local supply chain

Rajeev and Rajkumar realized that they could support farmers in terms of both market and financial linkages. Of the two, market linkage has been their current focus as it is easier to achieve and provides immediate relief to farmers. The FI lab supported PayAgri and its registered farmers to help farmers get a better price for their produce. This support also strengthened PayAgri’s forward linkages by:

Scoping out the existing purchase practices of vegetable vendors and small hotel owners in and around Chennai;

Expanding markets for the farmers and providing a better pricing structure for their grade B and grade C produce;

Identifying market avenues for their produce in smaller hotels, roadside eating-outlets, and restaurants and by developing a suitable pricing strategy.

Further, PayAgri constructed a warehouse near the consumption hub to store farmers’ produce. Through these strategic steps, they were able to eliminate a few intermediaries and ensure better price realization for the farmers.

In the next round of technical assistance, the FI lab helped PayAgri conduct a baseline assessment to identify potential intervention areas and ascertain the priority to digitalize the Agri value chain in the Nilgiris district of Tamil Nadu. The findings of this study helped PayAgri assess the efficacy of its intervention to help the community to get higher returns on investment from the value chain of root vegetables. The program also initiated a pilot diagnostic study that supported PayAgri to build an impactful medium-term strategy on digitalization.

The impact on small and marginal farmers

Based on the digitalization strategy, most of the interventions from PayAgri fall under different types of linkages, such as:

Input linkage (directly with input manufacturers)

Financial linkage (access to finance through banks or NBFCs)

Market linkage (directly with institutional buyers)

Risk mitigation through insurance and

Technical support

The immediate requirement for small and marginal farmers is to facilitate market linkages and to help them to grade, sort, and package their produce. With its agri-hub model running in a few cities, PayAgri has been able to support the farmers in all these areas, resulting in better prices to farmers for their produce.

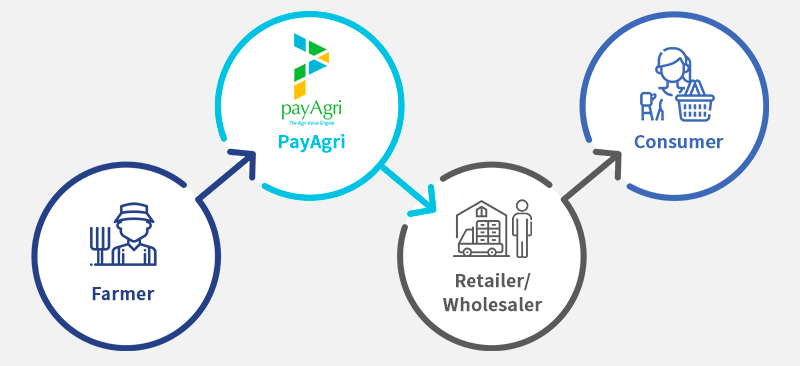

With farm-gate procurement followed by grading and sorting, PayAgri offers 10-30% more to farmers, depending on the crop—zucchini, capsicum, carrot, coconut, grains, and fruit, among others. This has been a result of the elimination of intermediaries from the value chain and partnerships with last-mile corporates and other retailers (Figure 4). Until 2019, PayAgri had an impact on over 2,000 farmers in terms of better incomes, through its platform with transaction values totaling over INR 60 million (USD 790K).

Figure 4: Tech-enabled supply chain

Besides driving market linkages, PayAgri has influenced farmers to improve the soil quality by sourcing organic inputs, which will help the farmers in the long run. PayAgri’s plan to provide holistic support and digitalize the entire Agri value chain for such small and marginal farmers will not only bring about reforms and efficiencies into the value chain but also help these small farmers build digital footprints. These digital records will make them creditworthy for the formal lending or banking institutions to lend against.

Roadblocks

“Working at the ground level is not an easy task”, says Rajeev, while speaking of the many hurdles that they encountered in the process. Although the current impact is a good start, PayAgri seeks to scale its operations and make the impact sustainable. Some of the major challenges that PayAgri faced or still faces are:

Convincing the farmers and Farmer Producer Companies (FPC) to work together;

Extensive reliance on cash transaction through the entire value chain, with no recordkeeping;

Lack of digitized records of farmers that otherwise would have helped them get better access to financial services;

Gaining the farmers’ trust to share data remains just as elusive as getting them working capital from formal institutions at reasonable rates of interest.

COVID-19, the unlikely catalyst to PayAgri’s success

Due to the current pandemic situation, PayAgri has delayed implementing its long term strategy. However, in general, the pandemic has been a blessing in disguise for the start-up and for the farmers and clients it serves.

PayAgri has been able to find a product-market fit for itself. Since the lockdowns started, the government has permitted the delivery of essential goods and services alone. PayAgri has been quick to respond to this situation, as highlighted in Figure 5, by aligning its logistics and distribution infrastructures to procure essential goods, such as food items. It has obtained licenses to transport and deliver the goods to its customers through its warehouses in Chennai and Theni, Tamil Nadu.

PayAgri has validated its business model by earning sustainable margins and becoming a strong enabler in the agri-supply chain . PayAgri’s customers are mostly retail or institutional buyers of farmer produce. They have shortened their pay cycles to PayAgri from a week to a day as they value PayAgri’s timely and quality assured deliveries of goods. This has led to improved cash flows for the start-up, which has, in turn, utilized these gains to maintain prompt payment to farmers and mitigated the risk to the farmers’ financials. Overall, PayAgri’s business model translates to gains for both the supply and demand sides.

Figure 5: PayAgri successfully delivered 12 trucks of rice and pulses to six cities in seven days, serving the farmers and the community

PayAgri has been experimenting with the farm-to-home model and has been piloting deliveries of its warehouse inventory directly to homes while cutting out the intermediaries.

PayAgri has also been trying to scale up. It has started to pilot a franchisee model in Coimbatore, Tamil Nadu. In this model, while PayAgri links the relevant FPOs to the Coimbatore franchisee, the franchisee is responsible for taking care of logistics to procure from FPOs and sell to PayAgri’s customers. The franchisee pays a fixed fee to PayAgri per year. Through this franchise model, PayAgri will offload the CAPEX costs to its franchisees and become profitable and scalable in a short span of time.

This blog post is part of a series that covers promising FinTechs that are making a difference to underserved communities. These start-ups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative and is co-powered by MSC. #TechForAll, #BuildingForBharat

MSC conducted a research to understand how the low- and middle-income (LMI) segments cope with the #COVID-19 pandemic. To examine how this pandemic has affected their lives, we spoke with 604 low- and moderate-income households across Bangladesh, India, Indonesia, Kenya, and Uganda. Our report offers a glimpse into their remarkable achievements, underlying challenges, shocking misery, and new opportunities in these trying times.

This blog is about a startup under the Financial Inclusion Lab accelerator program, which is supported by some of the largest philanthropic organizations across the world – Bill & Melinda Gates Foundation, J.P. Morgan, Michael & Susan Dell Foundation, MetLife Foundation and Omidyar Network.

Vijay Babu—a 45-year-old entrepreneur, Gowri—a 29-year-old house help, and Venkata Garu—a 57-year-old government employee, are residents of the same city. These individuals have another thing in common—they save through chit funds. An Indian “chit fund” is a traditional financial instrument that combines savings and borrowing. It has the perks of a personal loan, a beesi, and a recurring deposit all rolled into one. In a classic Indian chit fund, several people pool their money and the lowest bidder in the auction held amongst group members claims the amount.The rest of the amount gets distributed equally among the other members.

In India, chit funds come in three variants—those offered by the state governments, those started by registered companies, and those that are unregistered. The last variant is an informal chit fund that can be started between friends, families, and acquaintances. The first two are comparatively safer avenues for customers or subscribers to engage in. Chit funds allow bidders like Gowri to borrow any time during the chit period and set that off through regular monthly contributions until the end of the chit.

The light-bulb moment

However, chit funds have often been confused with Ponzi schemes and other scams such as the widely publicized Saradha and Rose Valley frauds that have colored the public perception of chit funds.

Also, since the chit funds run by state governments or registered companies have large groups, many group members do not know each other, leading to a trust deficit among them.

Most registered chit funds do not follow best practices and maintain sloppy, physical transaction records of the group. These records are difficult to audit by the regulators and so, the anomalies and corrupt practices of the chit fund companies often go undetected until the scams such as the ones mentioned earlier, come to light.

These factors above have led to a generally negative public perception about business operations of registered chit fund companies.

Founders of Chit Monks

Pavan, Malla, Sridhar, the founders of Chitmonks, and Praveen wanted to solve these problems and bring transparency and order to the chit fund industry by digitizing it. These four founders or “monks” left their regular jobs and used their experience in banking and information technology to devise solutions.

The unique pitch

Technology can lend transparency, which is what the chit fund sector needs to be more efficient and accountable in its operations. ChitMonks uses private commissioned blockchain technology across the entire life cycle of a registered chit fund to record the sequence of events immutably. The digitization starts from the registration of a chit fund company with the regulator and goes on to onboard and track the transactions of users subscribed to the chit fund. Besides, information on every event of the activities of the registered chit funds is visible to all related parties. This ensures transparency and integrity of the entire chit fund process on the blockchain. Since 2016, ChitMonks has used a smart contract-enabled blockchain platform to create solutions for the following three key issues that plague the sector:

Arbitrary guarantor requirements: To hedge against the risk of default in payments by the subscribers, chit fund companies insist on three to five guarantors instead of just one. This is to pressurize the subscribers into making timely payments. However, it makes the subscribers uncomfortable to join chit funds because they fear these companies will divulge their delinquencies to their guarantors and harm their reputation in the community.

Lack of transparency: The movement of funds at different stages is generally opaque in chit funds. This adversely affects the customers’ perception of chits. Despite the availability of flexi and quick loans, subscribers often wait for months to get the money they bid for.

Limited visibility for local regulators: State-level regulators have limited visibility in chit operations and therefore lack the ability to solve the grievances of subscribers.

ChitMonks is one of the few startups that attempts to solve these issues from a “regulatory-first” perspective.

The roadblocks

One of the key challenges for ChitMonks is to bring about behavioral changes in the way things have been done for decades. While its services have the potential to alter the course of the chit fund sector, ChitMonks faces several headwinds, mainly based on the traditional way of doing business. A few challenges are listed below:

Challenge faced by ChitMonks

The chit fund companies are largely family businesses that are reluctant to change their operating procedures. This attitude is common and hinders the end-to-end digitization of chit operations.

Subscribers need a guarantor to claim the bid money as they will have to continue to pay into the chit for the remainder of its rounds even after they have won the bid prize. Agreeing to be a guarantor is based more on trust rather than the real willingness to pay in case of a default. Subscribers are hence wary of digitizing this aspect of chit funds, as they fear it will be relatively more difficult to convince a guarantor to sign on a permanent digital record.

Many state regulators are still paper-driven organizations. The blockchain implementation of chit fund processes is not just a digitization of existing processes but also a paradigm shift that involves a completely new suite of technologies. This is why most state regulatory bodies are reluctant to adapt to it.

The state governments procure new technologies through a bidding system based on request for proposals (RFP), which requires a minimum of three bidders to compete. Since it is one of the very few companies with such a technology and there are not sufficient number of bidders, the RFPs frequently get cancelled. Therefore, ChitMonks finds it difficult to secure the required government approvals to implement its solutions across India.

Support provided by the FI Lab

CIIE.CO and MSC organized boot camps, diagnostic sessions, and clinics to build robust strategies and identify challenges that ChitMonks needs to overcome in order to scale its business. Through consulting support, ChitMonks understood several pain points to help its customers and companies in the long run. These included the provision of customer e-KYC to reduce the time taken to claim the prize money, along with e-auctions to improve accessibility and serve the customers better. The companies stand to gain from the digital verification of guarantors to assess their authenticity and reliability. In the long term, ChitMonks realized that a credit report based on chit repayments can act as an alternate scorecard to potentially secure loans from the bank. It also understood how to analyze the commitments of subscribers across the registered chit funds to help companies gauge the risk quotient of a potential subscriber.

The program also extensively mentored the team to build its investment readiness and enhanced its profile through evangelizing efforts. The support provided by the lab also helped the team assess and plan the rollout of these services in a phased manner, as elaborated in the section below. Overall, the FI lab acted as an extended co-founding member of the ChitMonks team.

Supporting chit fund companies and subscribers in times of Covid-19

Realizing the new world order with a focus on social distancing, the Chitmonks team is in the final stage of building an appropriate B2B solution for its platform. They will roll out new feature within a month. It will:

Digitize the process for collections from subscribers

Automate and digitize the auction process. Chit funds can hold auction without any physical presence of either the subscribers or their representatives

For the subscribers, Chitmonks plan to roll out a mobile application which will:

Enable online Know-Your-Customer (KYC) through e-verification using Aadhaar

Integrate payment gateway(s) so that a subscriber can make presence-less payments to the chit fund companies

The long term goal

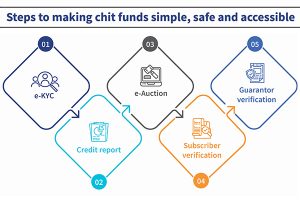

Steps to make chit fund simple, safe and accessible

Once the pandemic is over, based on the recommendations from the program, ChitMonks will offer five value-added services. They will roll out these services, as illustrated in the adjoining figure, in a phased manner based on ease of execution and stakeholder acceptability. The services will not only help chit fund companies make their day-to-day operations more efficient, but also serve to improve their public image.

The founders of ChitMonks are aware of the pitfalls of the sector as well as the opportunities it offers if the issues are addressed. The digital services of the firm can potentially put chit funds back on the map alongside favored products, such as mutual funds, credit cards, and recurring deposits. With the steady headway ChitMonks has made in re-engineering this veteran product, and its rapid entry in the states of Andhra Pradesh, Telangana, and Tamil Nadu, the face of chit funds is set to change for the better.

This blog post is part of a series that covers promising FinTechs that are making a difference to underserved communities. These start-ups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative and is co-powered by MSC. #TechForAll, #BuildingForBharat

The COVID-19 global health crisis is unprecedented. While it challenges health systems across the world and in Africa in particular, it also sheds light on opportunities linked to digital health.

The Ebola epidemic of 2014-16 highlighted many failings of the health systems in the continent. The coronavirus (COVID-19) outbreak is testing the region once again. The rapid and exponential spread of the virus has given rise to many initiatives that seek to overcome what some have termed a “healthcare war”. HealthTechs and other players in the ecosystem have increased efforts to stop the propagation of COVID-19. CcHub, the largest innovation incubator in Africa, for example, announced funding and technical support for technology projects that work to slow COVID-19 and mitigate its social and economic impact.

Digital technology could present the beginning of a solution for African countries, given the region’s widespread lack of infrastructure, healthcare workers, and equipment. In African countries at the heart of the digital revolution, some start-ups that focus on social impact have developed digital financial platforms that offer loans to small enterprises. Others have designed digital products that offer mental health support to people in isolation, or open-source coding to develop affordable ventilators.

Digital technologies can provide invaluable support to the healthcare sector. They can help conduct remote monitoring and follow the spread of infectious diseases. People can use digital technologies to teach security measures through gamification and avoid contagion in the process. The balancing of public health protection and privacy rights is a challenge that encryption and anonymization technologies can resolve. “Harnessing the power of digital technologies is essential for achieving universal health coverage”, notes WHO Director-General, Dr. Tedros Adhanom Ghebreyesus. Back in 2005, the WHO adopted a resolution designed to establish a global eHealth strategy, which led to the creation of the Digital Health Atlas.

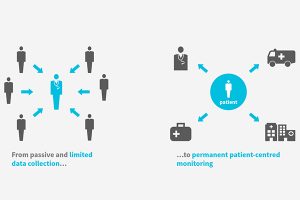

These technology innovations place the patient at the heart of processes, improve information flows, and allow for shorter timeframes than traditional approaches. The strength of HealthTechs lies in their creativity, their adaptability, and their speed of execution. They have an innate ability to understand client needs and design tailored products or services to meet such needs, with the flexibility to modify these products and services quickly to reflect market evolutions.

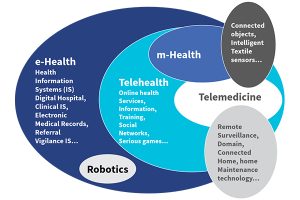

HealthTechs encompass a range of different services. They provide critical solutions to help respond to growing patient demands and relieve hospitals under pressure. Telemedicine, for example, which uses technology to provide remote healthcare services, contributes to filling in the gap when doctors are not available by offering remote consultations. This could provide effective solutions for isolated populations that usually lack access to these types of services.

Teledermatology helped care for 406 patients over a year and a half during its pilot phase in Bamako, Mali. Today, in Francophone Africa, over 4,000 people have access to healthcare services through the Bogou platform, which provides support in areas, such as obstetric emergencies, pediatrics, cardiology, and dermatology.

Source: WHO, Global diffusion of eHealth, 2016

mHealth uses mobile devices, such as smartphones, sensors, and tablets to allow patients to collect data on their own. In response to the COVID 19 crisis, Kemais Gomun developed his Apollo app in Côte d’Ivoire, in under two months. This free mobile application uses geo-location and self-diagnosis functions to help identify priority patients and improve patient care. Data collected through the app is sent to the National Public Hygiene Institute, which coordinates patient care in response to COVID 19.

eHealth offers solutions that range from prevention to treatment, as well as training for healthcare professionals. In Togo, for example, the government launched an official information portal in less than a week after the first cases were reported in the country, to provide reliable information on coronavirus. This includes information on symptoms and the spread of the virus across the country. The portal also offers information on where to seek medical help, health guidance, measures taken by the government to tackle the crisis, and links to useful media and other third-party resources.

However, although HealthTechs could contribute effectively to democratizing access to healthcare, they face several challenges. Connectivity and access to digital platforms are essential for the effective rollout of digital health solutions. Internet coverage remains limited and expensive in most sub-Saharan African countries, where only 22% of the population has an internet subscription. The continent also lacks visibility on the different players in the field of digital health and their initiatives.

MSC is currently working on mapping out the different players in the HealthTech sector in Francophone Africa. The objective of the project is to paint a picture of the tech start-up ecosystem in Francophone Africa and provide an opportunity to identify enterprises with a high potential for impact or growth. This will enable governments and West African businesses to collaborate with the start-ups they see as having direct value, provide a greater number of effective regulatory frameworks, and resolve current inefficiencies.

Francophone Africa has seen an exponential growth in start-ups that offer digital health solutions and is poised for the development of such solutions. The growing awareness of the opportunities digital technology presents for the healthcare sector is promising for HealthTechs. While some countries in the region are already well advanced in digital health, the success of these new models lies in the ability of HealthTechs to clarify their business models. It also lies ineffective public and private partnerships, which require the establishment of enabling and incentivizing regulatory frameworks.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.