Throughout April and into May 2024, extreme record-breaking heat led to severe impacts across most of Asia. A severe heatwave in north India during the last week of May led to deaths and cases of heatstroke. Several studies (here, and here) have shown that extreme heat in South Asia during the pre-monsoon period has grown more frequent and is strongly influenced by climate change. Extreme heat disproportionately impacts the lives and livelihoods of vulnerable people, particularly women and those who live in informal settlements in urban areas of the developing world.

MSC conducted a study on the impact of extreme heat on micro, small, and medium enterprises (MSMEs) and their workers in India’s National Capital Region, which comprises New Delhi and surrounding areas. Here are the five things we learned from our research.

1) Extreme heat already affects workers’ health severely

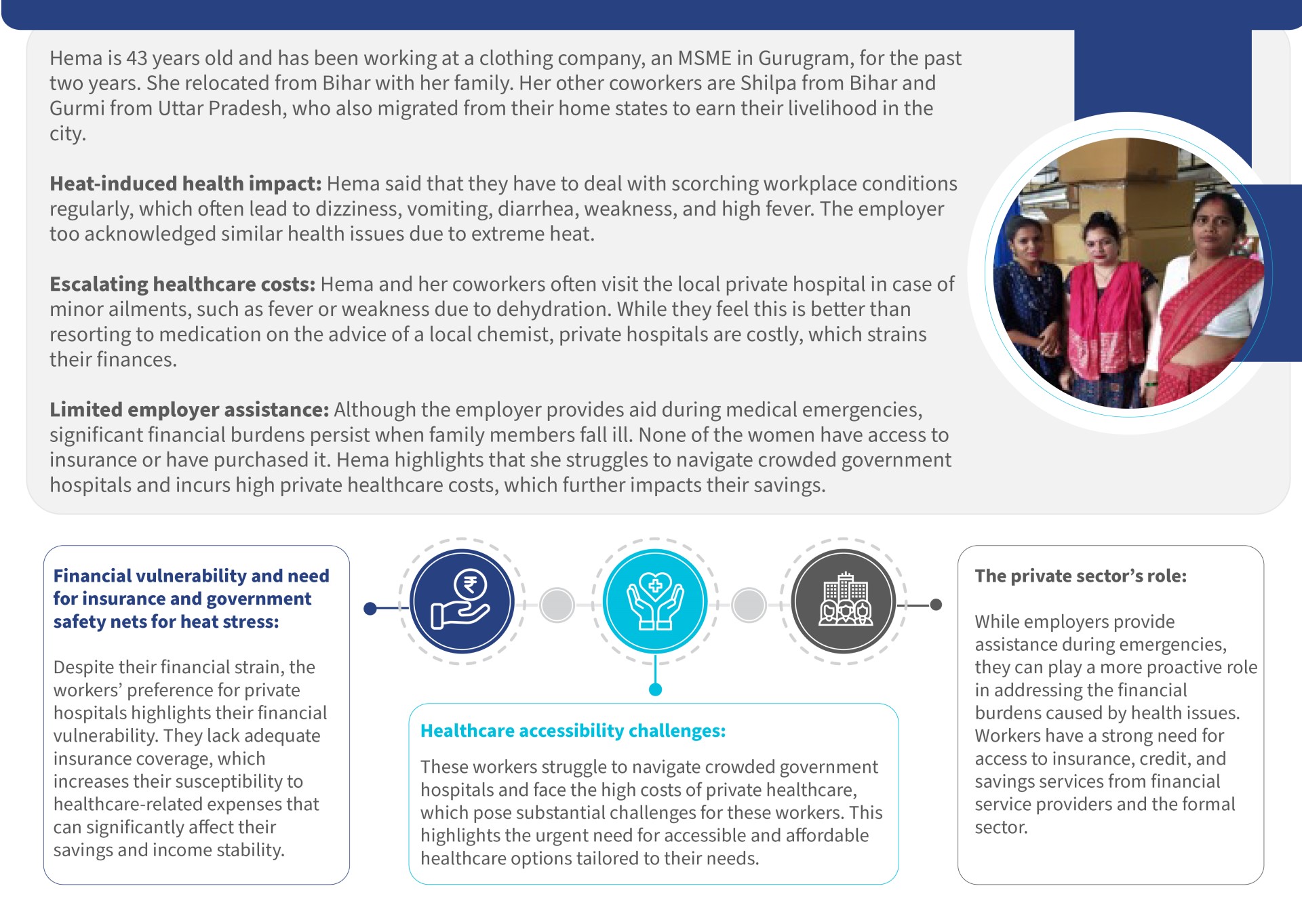

Extreme heat poses a significant health risk to MSME workers and their families. Heatwaves can lead to increases in heat-related illnesses, such as heat exhaustion, heatstroke, and dehydration, and worsen preexisting conditions, such as respiratory and cardiovascular diseases. Vulnerable groups, such as older adults, infants, pregnant women, and outdoor workers, are particularly at risk.

Studies suggest that by 2100, an estimated 1.5 million additional lives in India may be lost annually due to climate-driven extreme heat. This alarming projection underscores the urgent need for effective health interventions and policies to protect workers from the adverse effects of extreme heat. However, insufficient data hinders proper analysis of extreme heat’s impact on vulnerable populations. Additional investments are needed to uncover impact data.

2) Extreme heat leads to economic losses and reduced productivity

The economic impact of extreme heat on MSMEs is already significant. High temperatures lead to productivity losses, reduced working hours, and increased operational costs. A study estimates that India already loses around 101 billion hours of work annually due to heat, equivalent to the work done by approximately 35 million people, each working an eight-hour day in a year. This loss translates to a potential GDP reduction of up to 4.5%, or approximately USD 150-250 billion by 2030.

Women, in particular, face a more significant burden due to unpaid domestic labor. As a result of extreme heat, women lose 19% of their paid working hours, while more than two-thirds of heat-related productivity losses stem from unpaid domestic tasks. This additional workload worsens gender inequalities and highlights the need for gender-responsive policies to address the unique challenges women face in the workforce.

3) Poor Infrastructure and high energy demand worsen the impact of extreme heat

The infrastructure in many MSME sectors is ill-equipped to handle rising temperatures. Poorly constructed workplaces and homes, inadequate cooling systems, and frequent power cuts exacerbate the impact of extreme heat. Workers who live in informal settlements without access to passive or active cooling solutions are particularly vulnerable.

We found that air conditioning and other cooling technologies significantly increase MSMEs’ energy consumption during the summer months, which strains the already unstable electrical grids. This high energy demand can lead to power outages, further increase costs for MSMEs, and diminish the capacity of healthcare facilities and other critical infrastructure to cope with heat-related challenges.

Sahil, an MSME owner in Gurugram, told MSC that “running air conditioning in summer is costly due to frequent power cuts. Generators or additional fuel costs an average of 1.5 -2 lakh (USD 1,700 to 2,300) monthly, which increases my operating costs drastically.” The lack of proper urban planning and green spaces in rapidly urbanizing areas also contributes to the urban heat island effect, which makes cities significantly warmer than surrounding rural areas.

4) Current coping strategies are inadequate for future heat challenges

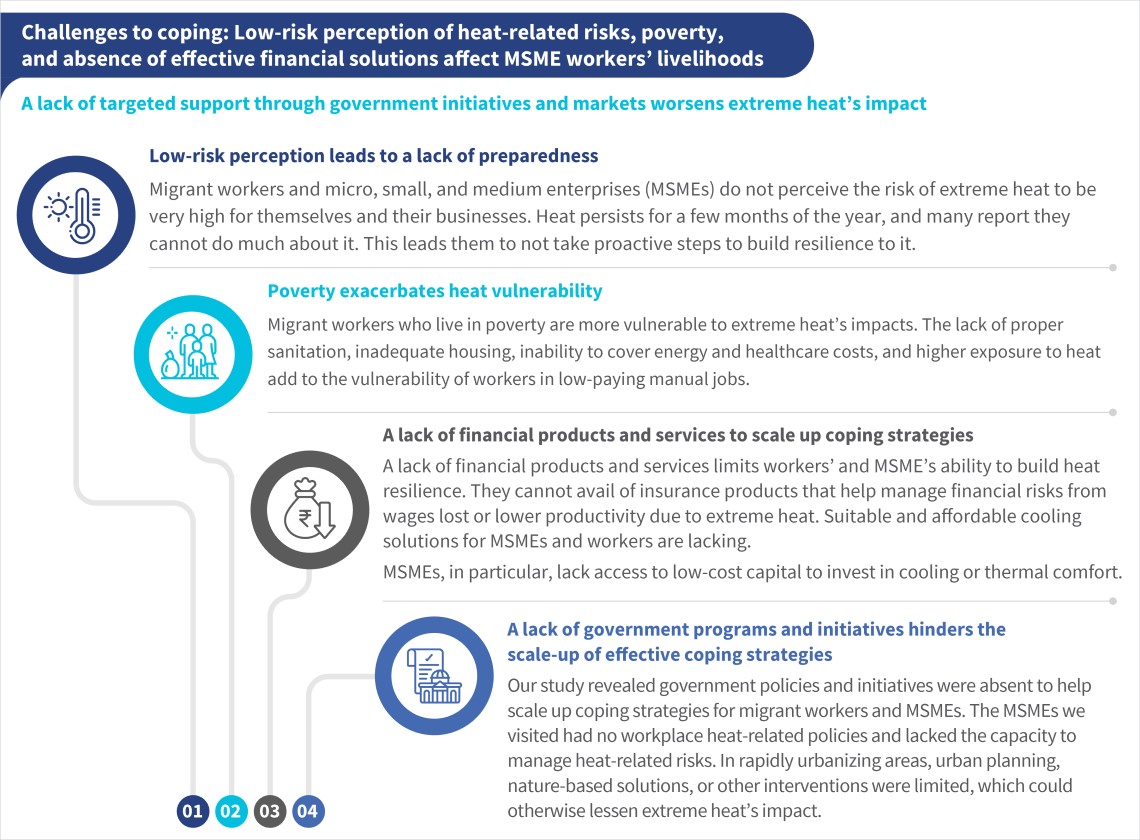

Current coping strategies employed by MSMEs and their workers are inadequate to meet the scale of future challenges posed by extreme heat. Workers often resort to basic measures to cope with the heat. They drink more water, wear light clothing, cover roofs with wet quilts, seek shade under flyovers and trees, and take frequent breaks. Residents cook food multiple times to prevent spoilage, often during the early hours of the day. However, these strategies are insufficient to address the severe and prolonged heat stress expected in the coming years.

Employers have also made incremental changes, but these measures will fail to build long-term resilience. They take steps, such as providing employees with fans, coolers, and cool drinking water but they are not enough to deal with the impacts of heat waves and extreme heat. Employers, therefore, need to develop affordable and sustainable cooling solutions, improve workplace safety, and enhance access to financial products and services to manage heat-related risks for their employees.

5) Despite progress, MSMEs and their workers need additional and targeted support to increase their resilience to extreme heat

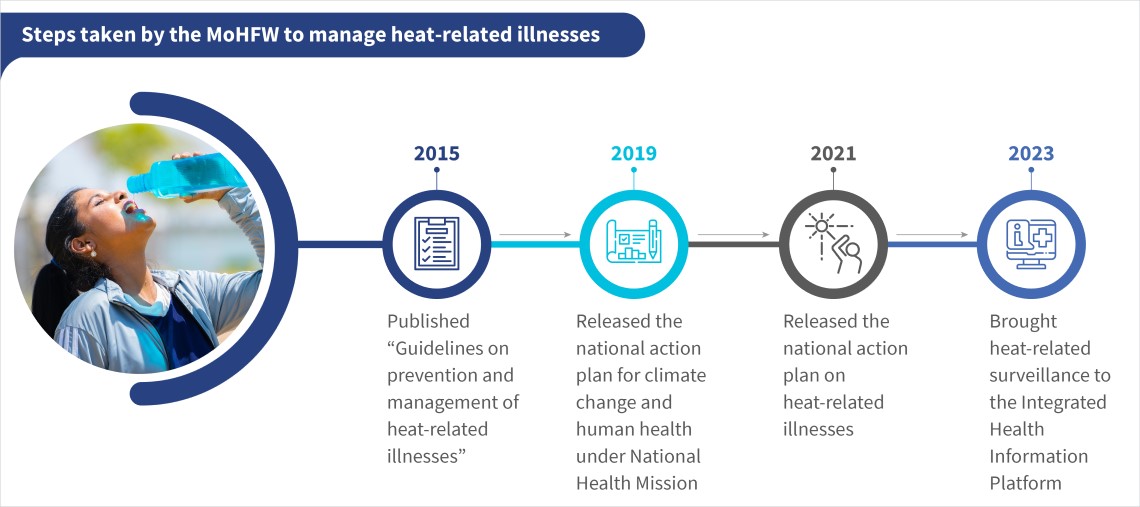

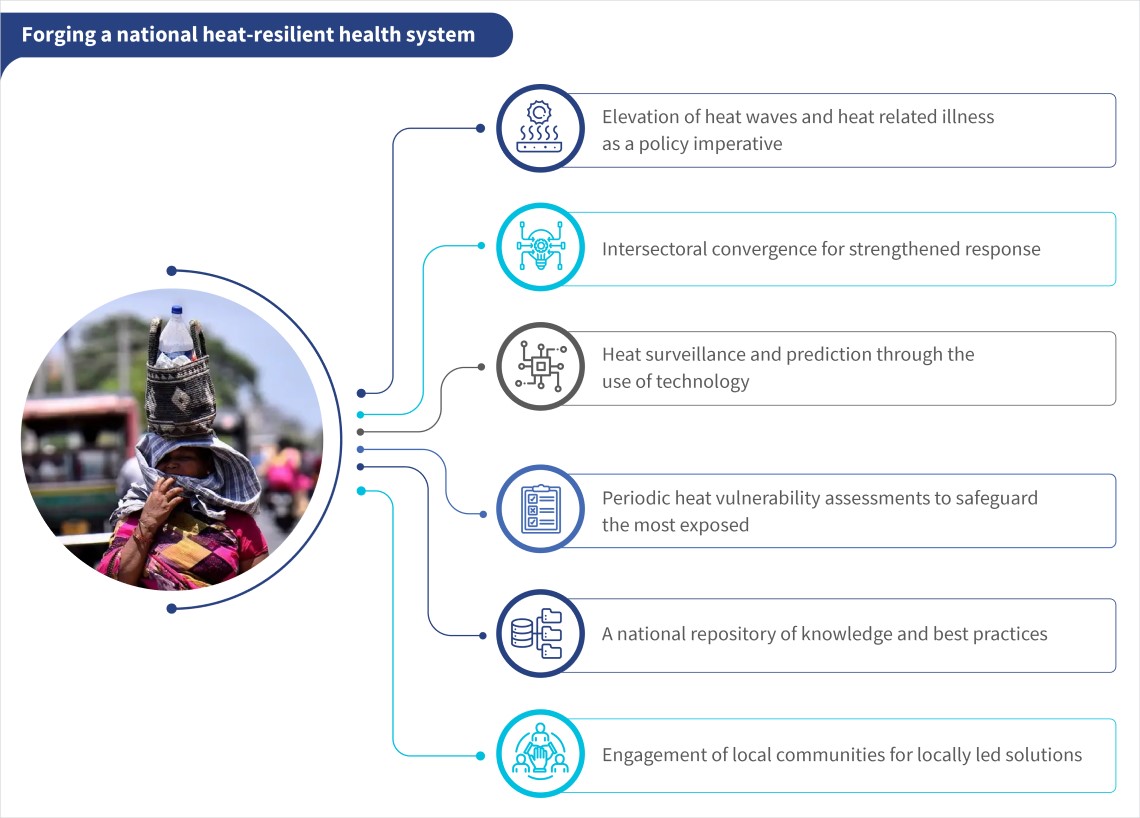

India has made notable strides in creating plans and policies to respond to the impacts of extreme heat, such as Heat Action Plans for cities, such as Delhi and states, the national Cooling Action Plan, and efforts to strengthen health systems to decrease heat-related mortality and morbidity. However, MSMEs and their workers require targeted support to increase awareness of the impacts of extreme heat and meet their financing needs to invest in sustainable cooling solutions. Workers who have high exposure to extreme heat and MSMEs that employ workers living in informal settlements, such as construction, need urgent support to reduce worker mortality and morbidity.

Figure 1: There is a lack of locally tailored and relevant support for MSMEs to respond to the impacts of extreme heat

MSC’s study on the effects of extreme heat on MSMEs and workers in Delhi NCR underscores the urgent need for comprehensive and targeted interventions to build their resilience against the escalating threat of extreme heat. These include the development of local programs that target MSMEs with the most at-risk workers, improve infrastructure, enhance access to financial products and services, and strengthen access to public services. By addressing these challenges, India can protect its workforce better, sustain economic growth, and ensure a more resilient future in the face of climate change.

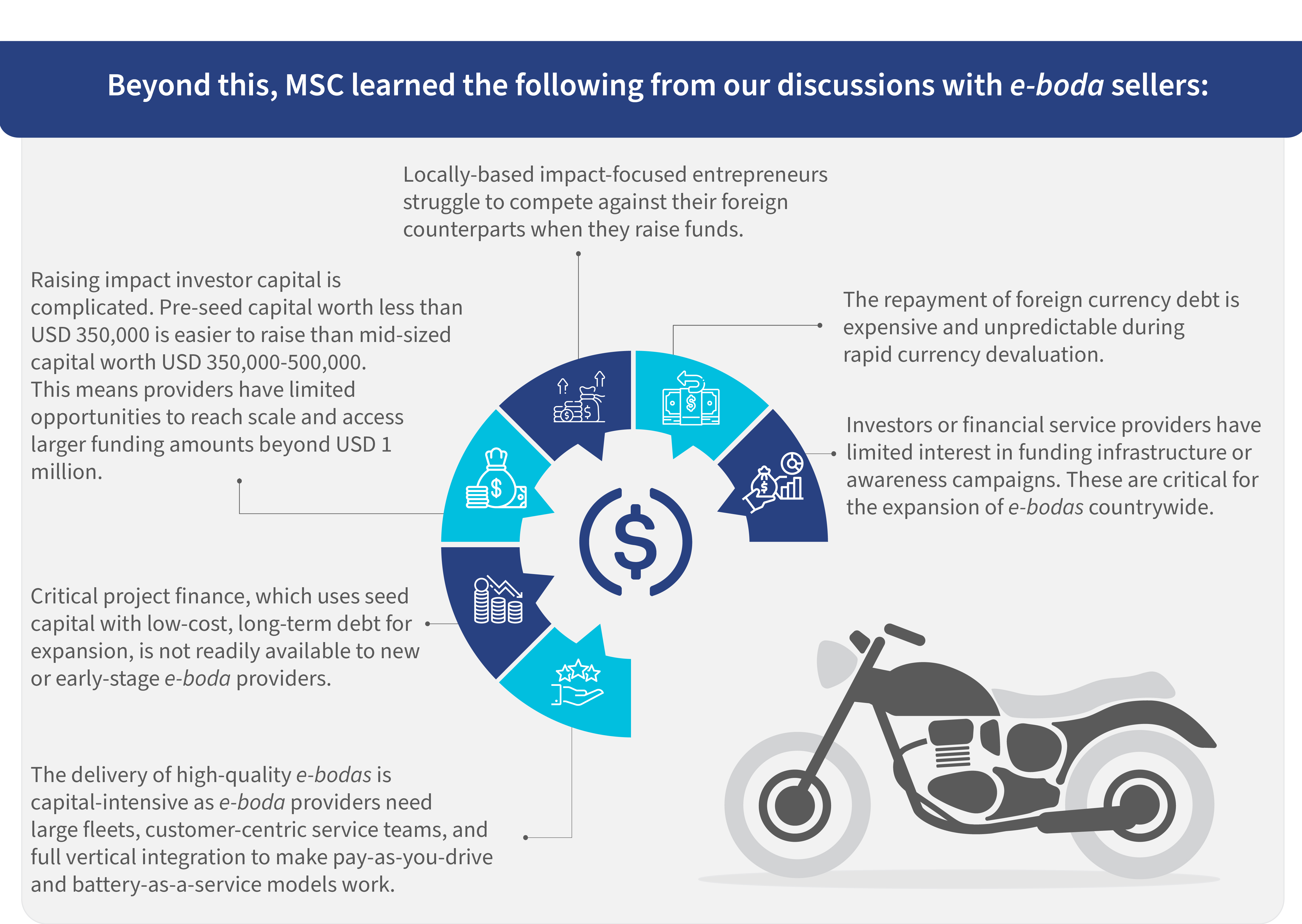

Martin and Joseph are nano-entrepreneurs in Nairobi. They are actively engaged in the transport sector. Martin ferries individuals and cargo on his boda for a living. A local financial institution finances his boda, which runs on a traditional internal combustion engine. He decided against an e-boda (electric motorcycle) due to his counterparts’ negative experiences with the first-generation e-bodas. His business was brisk until 2020, when COVID-19 shutdowns led to reduced demand for nano-entrepreneurs.

Martin and Joseph are nano-entrepreneurs in Nairobi. They are actively engaged in the transport sector. Martin ferries individuals and cargo on his boda for a living. A local financial institution finances his boda, which runs on a traditional internal combustion engine. He decided against an e-boda (electric motorcycle) due to his counterparts’ negative experiences with the first-generation e-bodas. His business was brisk until 2020, when COVID-19 shutdowns led to reduced demand for nano-entrepreneurs.