The National Social Assistance Programme (NSAP) is a Centrally Sponsored Scheme (CSS) of the Government of India. Started in August, 1995, NSAP provides pension payments to more than 33 million elderly people, widows, and persons with disabilities from households below the poverty line. The GoI initiated the digitization of pension payments to plug leakages and streamline payments in 2014 under the National e-Governance Initiative 2006. This blog identifies last-mile challenges associated with the delivery of pension payments due to digitization.

Blog

PMAY-G: Transforming the rural housing program in India (Part II)

In the this series, we discussed the evolution of rural housing programs in India and the most recent incarnation, Pradhan Mantri Awaas Yojana- Gramin (PMAY-G). We also assessed the scheme’s performance to date and suggested improvements to its design, implementation, and monitoring when compared to its predecessor, Indira Awaas Yojana (IAY). This blog discusses the existing challenges PMAY-G faces, both on the demand and supply sides as revealed by our primary and secondary research, and recommends measures to enhance its overall effectiveness.

Challenges to PMAY-G

- Supply-side challenges

The MSC team’s interactions with stakeholders including those at the block[1] and the gram panchayat[2]levels, as well as a review of existing literature, revealed several supply-side obstacles as discussed in detail below.

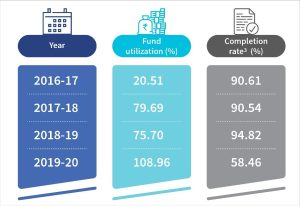

- Inadequate release and utilization of funds: The Government of India (GoI) and state governments have made profile announcements of generous allocation of funds. However, a limited proportion of the announced funds have actually been released for the program. The GoI released 58.56% (INR 272.98 billion or USD 3.9 billion[3]) of the allocated PMAY-G funds; while state governments released only 5.7% of this allocation for the fiscal year 2019-20, which translates to INR 15.63 billion or USD 220 million.

The over-allocation of funds coupled with insufficient release hurts the government’s ability to complete the targets established for the year within that same year. Although the overall target achievement under the scheme in the initial three years is more than 90%, this is primarily because of the accounting method used (see footnote 3). The actual physical progress during the respective years has remained slow—as can be seen from the rate of completion in 2019-20.

The over-allocation of funds coupled with insufficient release hurts the government’s ability to complete the targets established for the year within that same year. Although the overall target achievement under the scheme in the initial three years is more than 90%, this is primarily because of the accounting method used (see footnote 3). The actual physical progress during the respective years has remained slow—as can be seen from the rate of completion in 2019-20. - Convergence with other schemes: For convergence with the Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) and Swacch Bharat Mission-Gramin (SBM-G), the AwaasSoft captures beneficiary-specific information, which includes the job card number for MGNREGS and the SBM-G number during the beneficiary registration process. This has led to better convergence with these schemes. The scheme guidelines do not specify the requisite steps for convergence with other schemes. As a result, many beneficiaries cannot avail of the convergence benefits,[4] such as electricity connections, gas connections, and piped drinking water.

- Minimal scheme awareness: Awareness regarding the guidelines, benefits, and conditionality of the scheme is minimal among supply-side stakeholders at the village level including the gram panchayat and the Panchayat [5] Furthermore, due to complex scheme guidelines, some banking institutions lack clarity on their role in the provision of housing credit facilities to PMAY-G beneficiaries. As a result, scheme details are not communicated properly to beneficiaries.

2) Demand-side challenges

Focus group discussions and in-depth interviews with PMAY-G beneficiaries, coupled with a review of the existing literature revealed challenges that demand-side stakeholders, namely, beneficiaries face. We discuss this in detail below.

- Fund insufficiency: The quantum of assistance provided under the scheme, that is, INR 120,000 (USD 1,720), was determined in 2016 upon the scheme’s inception. The scheme design does not account for inflation in material and labor costs over the years.[6] Beneficiaries felt that home design and quality as specified by the scheme guidelines are not attainable at current market prices of material and labor. This results in compromises in construction quality and additional expenditures for beneficiaries.

- Delay in disbursement of installments: Instalment payments[7] under the scheme are linked to the level of completion of construction and are processed once a real-time verification report is submitted through the AwaasApp. Delays in physical verification of completed construction, which block-level officials and gram panchayat representatives carry out, lead to delays in disbursement of funds. Disbursements are often delayed even when timely physical verification occurs because the signatories have not signed off on the Fund Transfer Order (FTO).[8]

- Non-receipt or delay in convergence payments: Beneficiaries receive convergence payments over and above the assistance provided under the PMAY-G scheme. The convergence benefit is approximately INR 18,000 (USD 260) for MGNREGS and INR 12,000 (USD 170) for SBM-G, which, together, increases the overall assistance amount by 20%. Interaction with the beneficiaries revealed instances of delay or non-receipt of convergence payments. This renders the purpose of convergence futile, as beneficiaries do not receive benefits during the construction phase.

- Exclusion error from Socio-Economic Caste Census (SECC): PMAY-G has stringent guidelines to identify and select beneficiaries based on SECC data. However, this data was collected in 2011 and thus proved to be often out of date. Beneficiaries are often unaware of the existing guidelines or have limited information about the identification and selection processes. Beneficiaries who are excluded from the SECC database, which is a precondition for scheme eligibility, are not aware of the option to enroll manually. In general, the enrolment process remains opaque for beneficiaries.

Recommendations and way forward

Based on MSC’s research, we suggest the following enhancements at the policy and operational levels that focus primarily on scheme design and implementation:

i) Policy-level recommendations

Streamline the funding: The GoI and state governments should develop a mechanism to release funds as per budget allocations and ensure timely disbursement to beneficiaries. Delays in the release of allotted funds and disbursements to beneficiaries escalate the time and cost involved in the process of constructing a house.

The solution to this is twofold. First, the GoI and state governments should implement just-in-time funding through a treasury single account so that money is replenished for spending on a near real-time basis without creating float in the system.

Second, state governments should implement smart or automated payments by doing away with multiple signatories to the FTOs to release funds to the beneficiaries. This can be achieved by introducing automated approval of the geotagged images captured during the physical inspection of the level of completion.

- Account for inflation in the assistance amount: The GoI should account for inflation from the previous fiscal years and adjust the amount of assistance accordingly on an annual basis. The assistance amount can be revised based on the Consumer Price Index (CPI) data released by the Reserve Bank of India (RBI). The inflation-adjusted dynamic assistance amount will enable beneficiaries to maintain the desired quality of construction and finish building their houses on time.

ii) Operational recommendations

- Automate the registration of beneficiaries excluded from SECC: A manual system exists for registering beneficiaries excluded from the SECC 2011 database. Under this system, the Gram Panchayat prepares and forwards the list of eligible households to the Block Development Officer (BDO).[9] The BDO has the right to recommend inclusion based on the merit of the claim and verification, after which the name(s) is added to AwaasSoft. However, this registration process has not been communicated effectively to the beneficiaries, which renders it useless.

The GoI should make changes to the MIS and enable a mechanism for online registration of such excluded beneficiaries. Besides the online system, the GoI should also run awareness campaigns at the panchayat level to effectively communicate the registration process for those who feel they have been excluded incorrectly.

- Strengthen convergence with other schemes: The current MIS does not track convergence of PMAY-G with schemes, such as PMUY, SAUBHAGYA, and NRDWP. The lack of accountability has led to poor convergence outcomes for these schemes. The GoI should suitably modify the MIS and enable a mechanism to capture beneficiary details to facilitate convergence with such schemes during beneficiary registration—as is the case with MGNREGS and SBM-G. For example, for convergence with MGNREGS, the GoI uses the MGNREGS database, that is, the job card number. Similarly, for convergence with PMUY the GoI should use the PMUY database, that is, the gas connection, LPG subscriber ID, or application number.

- Introduce an automated module for registering for inspection: The current system of monitoring and inspection is manual and follows a top-down approach. This means that beneficiaries cannot initiate inspections of the progress of their construction. The GoI should adopt a bottom-up approach and make suitable changes to the MIS.

The system should be modified suitably by introducing a USSD-based service, toll-free number, Common Service Center-based service. This would allow beneficiaries to raise requests for completion level inspection, thereby reducing the time it takes for inspections to be carried out, and hence, disbursements.

Since its inception, PMAY-G has achieved scale, which earlier housing programs had failed to accomplish. Many believe that having a home brings pride to a household, mitigates uncertainties, and frees up time for people to pursue economic activities resulting in economic and social independence. Although PMAY-G continues to help millions of Indians realize their dream of owning a home and receive other necessities, several hurdles remain before all homeless rural Indians can build a house they call their own.

[1] Based on the administrative structure, a block is a district subdivision consisting of a cluster of villages for the purpose of the Rural Development department and Panchayati raj institutions.

[2] Gram panchayats are formalized, local self-governance systems in India at the village level, which has a Sarpanch as its elected head.

[3] USD 1 = INR 70

[4] Convergence benefits include MGNREGS for labor, SBM-G for toilets, PMUY for cooking gas connections, Saubhagya for electricity connections, and NRDWP for drinking water.

[5] The Secretary of the panchayat is a non-elected representative appointed by the state government to oversee panchayat activities.

[6] Trends in prices of material and cost indices in building construction.

[7] Payments under the scheme are made in instalments (a minimum of three). Payments are linked to the level of completed construction, that is, foundation, plinth, windowsill, lintel, roof-cast, and are subject to verification.

[8] The FTO ensures leakage-proof payments and is generated against a sanctioned number of houses.

[9] The Block Development Officer is in charge of the block. The officer oversees that approved plans or programs are implemented efficiently.

PMAY-G: Transforming the rural housing program in India (Part I)

This is the first part of a two-part series blog on rural housing programs in India

Majuli in the northeastern Indian state of Assam is the biggest river island in the world. Flanked by the mighty river Brahmaputra, the low-lying island is prone to flooding. The annual onslaught of floods destroys everything—from houses to paddy fields, disrupting the lives of poor villagers. In response, the government introduced “Chang Ghar” houses—structurally sound buildings raised on stilts. They have a big room, a central kitchen, and an attached toilet.

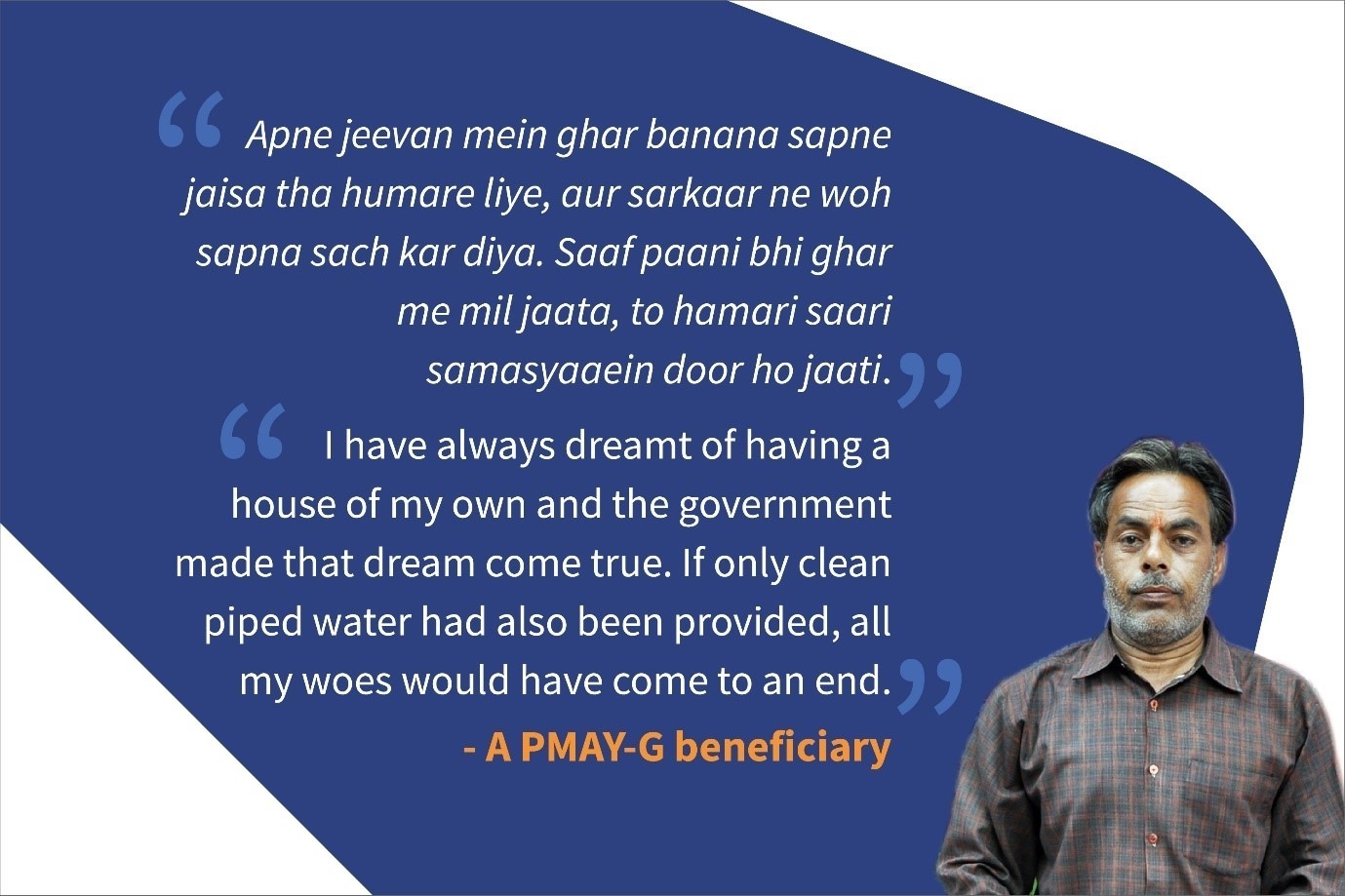

“This is sheer magic and I now have a pukka[1] house for myself with a toilet, running water, and also a gas connection,” exclaimed one villager after she received her house through the Pradhan Mantri Awaas Yojana – Grameen (PMAY-G) scheme. Many others in her village had a similar experience. PMAY-G is the central government’s program that provides affordable housing for eligible poor beneficiaries.

To understand how PMAY-G came into existence and how it has performed so far, we must look at the genesis of the rural housing programs in India.

Introduction and evolution of rural housing programs in India

After India became independent in August 1947, the young nation faced a huge housing crisis due to large-scale migration, which left many without houses or shelter. During the 1950s, the Government of India (GoI) began providing housing to rehabilitate refugees of the partition. By 1960, around half a million homes were provided across northern India.

From 1957 to 1996, the GoI implemented several rural housing schemes. In 1957, the GoI introduced the Village Housing Program (VHP), under which individuals and cooperatives availed housing loans of up to INR 5,000 (USD 70[2]). The GoI then introduced House Sites-cum-Construction Assistance Scheme (HSCAS) in 1969, under which it constructed 67,000 houses over the next 10 years.

The GoI further advanced its rural housing agenda through employment programs, such as the National Rural Employment Program (NREP, 1980) and the Rural Landless Employment Guarantee Program (RLEGP-1983). Houses were constructed under these programs for Scheduled Castes/Scheduled Tribes (SCs/STs)[3] and rescued bonded laborers.[4] Indira Awaas Yojana (IAY) was the first major attempt by the GoI to respond to the shortage in rural housing in the country by providing lump-sum monetary assistance for construction.

- Indira Awaas Yojana

The GoI launched IAY in June, 1985 as a sub-scheme under RLEGP for the construction of houses for SC, ST, and rescued bonded laborers. In January, 1996, IAY became an independent scheme and coverage was extended to Below Poverty Line (BPL)[5] households as well. Since its inception, assistance under IAY has been used to construct 36 million homes, which represents 89% of the annual target set by the GoI.[6] Although this completion rate is quite respectable, the GoI faced several challenges in the design, implementation, and monitoring of the IAY scheme. The following section outlines these challenges:[7]

- Targeting: Under the scheme, authorization to select beneficiaries from the target segment rested with gram panchayats.[8] Providing greater autonomy to local village bodies without proper monitoring resulted in the inclusion of ineligible beneficiaries. There were instances of multiple benefits being provided to the same family. The scheme did not meet the criteria regarding the allotment of 60% of the funds for the construction of houses to SC/ST and 40% to non-SC/ST below poverty line (BPL) households. Out of the houses sanctioned during 2008-09 to 2012-13, only 55% were allotted to SC/ST households.

- Baseline assessment of housing shortage: The housing shortage assessment, which determines the gap between housing required and existing availability, is of utmost importance for the scheme to be effective. Under IAY, 14 states across the country did not undertake a housing shortage assessment, which resulted in inaccurate figures for housing requirements.

- Convergence with other schemes: The scheme envisaged convergence with existing GoI programs around sanitation, clean drinking water, electricity connections, and affordable credit so that benefits under these programs could be extended to IAY beneficiaries. Convergence with these existing schemes rested with the gram panchayats. Lack of effective monitoring resulted in poor outcomes for the convergence.

- Universal house design: Under IAY, the GoI suggested a uniform house design across all geographies. The design, however, was not suited for topographical variations in the country, which reduced the longevity of the houses. The GoI also failed to provide technical assistance for the design and construction process to beneficiaries of the scheme.

Thirty-one years after its inception, IAY was not able to completely address the shortage of housing in rural India. In 2012, the rural housing gap was estimated to be approximately 40 million based on the assessment of the Working Group on Rural Housing under the XIth plan. To address the shortcomings of IAY and expedite the provision of rural housing, the GoI revamped the scheme and relaunched it as Pradhan Mantri Awaas Yojana – Gramin (PMAY-G) in 2016.

2) Pradhan Mantri Awaas Yojana – Gramin (PMAY-G)

The Ministry of Rural Development (MoRD), a Ministry under the GoI’s purview, launched PMAY-G to provide 29.5 million pukka houses, which featured basic amenities including toilets, electricity connections, and clean drinking water. The objective of the scheme was to provide such pukka houses by 2022 to all rural houseless and those living in kutcha houses[1] and in dilapidated housing. The GoI utilized the Socio Economic Caste Census (SECC 2011) to identify and select beneficiaries.

Under PMAY-G, eligible beneficiaries receive a sum of INR 120,000 (USD 1,720)[2] in multiple installments[3] to construct a house. To provide further assistance and basic necessities to the PMAY-G beneficiaries, the scheme converges with existing government programs.

PMAY-G’s convergence with Mahatma Gandhi National Rural Employment Guarantee Scheme (MGNREGS) entitles beneficiaries to 90 person-days of work on one’s own house and payment of INR 18,000 (USD 260) for such work, while convergence with the Swacch Bharat Mission – Gramin (SBM-G) entitles beneficiaries to additional assistance worth INR 12,000 (USD 170) for toilets. Convergence with Pradhan Mantri Ujjwala Yojana (PMUY) ensures cooking gas connections, the National Rural Drinking Water Program (NRDWP) ensures clean drinking water connections, while Pradhan Mantri Sahaj Bijli Har Ghar Yojana (SAUBHAGYA) ensures electricity connections to PMAY-G beneficiaries.

Besides, beneficiaries are entitled to avail of a housing loan of up to INR 70,000 (USD 1,000) from banking institutions at a rate below the prevailing rates in the market. All monetary benefits accruing to beneficiaries are transferred to their respective Aadhaar[4]-linked bank accounts through the Public Financial Management System (PFMS).

Under PMAY-G, MoRD targeted the construction of 29.5 million houses in multiple phases. During the first phase, 10 million houses were to be constructed between 2016 and 2018, and another 19.5 million in the second phase from 2019 to 2022. PMAY-G was designed to overcome the challenges that emerged under IAY. We discuss these challenges in more detail below.

Improvements over IAY

i) Scheme design

- Robust beneficiary identification and selection: The scheme emphasizes fairness and transparency in beneficiary selection. The scheme design was built on the principle of “housing for all.” Under the revamped PMAY-G scheme, beneficiaries are identified and targeted as follows:

The eligible list of beneficiaries that has been generated is verified by gram panchayats for discrepancies. This list is referred to as the permanent waitlist. Based on annual targets, housing sanctions are made based on the final rankings of beneficiaries on the waitlist.

- Implementation of e-governance: The implementation and monitoring of the scheme are carried out through an end-to-end e-governance model, consisting of AwaasSoft (MIS) and AwaasApp (mobile application). The AwaasSoft plays a pivotal role in key governance and operational functions and AwaasApp provides a mobile-friendly interface. The functions include target setting, beneficiary selection, beneficiary management, fund management, sanction management, and construction progress monitoring. The implementation of the e-governance solution has expedited the overall progress of home construction and facilitated more effective resource management.

- Convergence with other schemes: To foster better convergence outcomes, AwaasSoft is linked to the respective scheme databases for MGNREGS and SBM-G. It captures beneficiary details during registration that are utilized to transfer convergence benefits seamlessly into their respective bank accounts. Responsibility of convergence with other schemes, that is, PMUY, SAUBHAGYA, and NRDWP rests with the gram panchayats.

- Technical assistance: The National Technical Support Agency (NTSA), which was established under PMAY-G, monitors construction quality. Beneficiaries receive suggestions on housing design and the use of appropriate technology for home construction best suited to the local conditions through information, education, and communication activities. Beneficiaries also receive assistance with raw material procurement from locally available sources and cost and material estimates, as well as labor requirements.

ii) Scheme performance

- Physical progress of the scheme: The scheme has achieved 94.8% of its target[5] for the first three years. It has completed the construction of 9.11 million houses.

-

Effects on employment generation: Various research organizations have assessed the effectiveness of PMAY-G on generation of direct employment.[6] Research estimates from the National Institute of Public Finance and Policy (NIPFP) showed that since its inception on 1st April, 2016 up until 5th March, 2018, the scheme generated up to 298.4 million person-days of unskilled labor[7] and up to 213 million person-days of skilled labor[8].

PMAY-G benefitted from improvements to both design and performance when compared to its predecessors. Difficulties, however, remained around achieving targets and differential performance among states. The next blog in this series, “PMAYG: Transforming the rural housing program in India – Part II” will discuss the challenges PMAY-G faces and how addressing these challenges will facilitate the GoI’s objective of “Housing for All by 2022.”

[1] A kutcha house is a temporarily constructed shelter not made from cement. They are mostly made from brick and mud.

[2] PMAYG is funded by GoI and state governments in the ratio of 60:40, for the Northeastern states and two Himalayan states (Himachal Pradesh and Uttarakhand) the ratio of funding is 90:10. The scheme is financed wholly by GoI in the case of union territories.

[3] The installment payments are linked to level of construction. State governments have the autonomy to decide the number of installments.

[4] Aadhaar is a verifiable 12-digit unique identification number issued by the GoI to residents of India.

[5] Houses for which construction started in one year but completed in subsequent years are counted as achievement against the annual target set for the year in which construction was initiated; hence, this does not reflect actual physical completion of houses in that particular year.

[6] Impact of PMAY-G on Income and Employment, 2018

[7] Unskilled labor refers to workers who have no special training or experience. They comprise the workforce and have an extremely limited skill set.

[8] Skilled Laborers are workers who have acquired the necessary skills and training for a particular job (Example: plumber or electrician).

[1] A pukka house is one that can withstand normal wear and tear due to usage and natural forces including climatic conditions, with reasonable maintenance, for at least 30 years.

[2] Conversion rate USD 1 = INR 70

[3] Due to the iniquitous and hierarchal character of Indian society, SC/ST communities are considered as socially disadvantaged groups.

[4] Bonded labor is the pledge of a person’s services as security for the repayment of a debt or other obligation.

[5] Below Poverty Line is an economic benchmark set by the GoI to identify economically weaker people and households. It refers to a threshold income level; people whose income is below this threshold are considered poor or below poverty line.

[6] Rajya Sabha question on status of IAY, 2016

[7] Performance audit report: Indira Awaas Yojana, 2014

[8] Gram Panchayats are formalized local self-governance systems in India at the village level, which has a sarpanch as its elected head.