The COVID-19 pandemic has brought upon us the responsibility to create awareness, influence precautionary behavior, and drive safety of the weak and the vulnerable segment. These books can be customized to meet the needs of country-specific guidelines, institutions, and customers. Feel free to spread them around and join us in fighting back. #staysafe

The work has been commissioned by MetLife Foundation.

The COVID-19 pandemic has brought upon us the responsibility to create awareness, influence precautionary behavior, and drive safety of the weak and the vulnerable. MSC has developed a series of collaterals in the form of conversational comics that can help microfinance institutions (MFIs) inform their frontline staff members on workplace safety, safe cash handling, customer etiquette, and personal safety measures. These books can be customized to meet the needs of country-specific guidelines, institutions, and customers. Feel free to spread them around and join us in fighting back. #staysafe

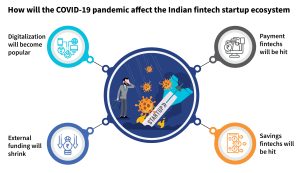

Around the world, the COVID-19 pandemic has changed the way we think about life and work. India remains in lockdown as field operations have been shut down and work-from-home is implemented across the board. Much of the fintech startup ecosystem will have to wait and watch to see how the situation unfolds after the official lockdown is over.

However, some early trends signal what is in store:

Digitalization wave

We will see digitalization happening across the board, from processes, to how employees interact with each other, to how the banks, fintechs, and other players reach their customers. Let us look at a few examples:

Functioning of microfinance institutions (MFIs) and non-banking financial institutions (NBFCs): MFIs and NBFCs have traditionally been driven by physical methods of cash collection, physical verification and onboarding of new customers. With the new normal of curtailed physical interactions, these institutions will seek ways to transform their physical and manual processes into automated and digital ones. They will look toward fintechs, especially start-ups, as they can support the MFIs and NBFCs in making this change with lower costs and quicker turnaround.

Agricultural practices: The COVID-19 pandemic will affect the incomes and modes of payments of farmers. In India, agricultural practices are largely labor-intensive and manual. This applies to tilling, plowing, sowing, and harvesting. Farmers also need to physically visit lenders—private money-lenders in most cases—and must get cash to revisit and repay their loans. The farmers, especially small landholders who have feature phones and even smartphones generally use them to consume entertainment content. We anticipate a big change coming here. Due to the restrictions imposed because of the pandemic, many lenders will embrace the idea of digital payments and farmers will thus be aligned to do so as well. In the coming months, digital payment collections should see large-scale adoption in rural areas through methods, such as UPI, IMPS, and auto-debit facilities, such as NACH.

E-commerce and its effect on payment fintechs

A major bulk of revenue for fintechs that work in payments comes from transactions in the e-commerce industry. E-commerce platforms like Flipkart and Amazon India sell a mix of non-essential and essential items. Because of the COVID-19 pandemic, these online retailers have recently stopped selling non-essential items in the short to mid-term, or between a few weeks and a few months. Since the essential items that are now sold on these platforms have low margins, the private digital payment companies or payment fintechs in India will see their revenues shrink. This will be because their margins ride on the volumes and values of transactions. With essential services being sold more frequently, despite higher volumes being sold, the effect on the margins on these low-priced goods will have a more drastic impact on their revenues.

Hit on short-term savings

With the uncertainty around the availability of food and essential items in the market, many people will switch from savings to keeping money (cash or digital) readily available to spend at short notice. This behavior will lead to a decrease in the usage of short-term savings instruments for the near future.

Survival or not

As private investors get jittery over making any new investments, they are trying to first selectively invest any available money to protect companies in their portfolios in this hour of crisis. Hence, fintechs with weak business models that rely heavily upon investor money will fizzle but the ones with solid though smaller revenue models, especially the bootstrapped ones will have a good chance to come to the fore, provided they have or can build their runways for the next 6-12 months at least.

What can be done to help the fintech ecosystem?

In these times when the future of business is uncertain and survival of fintechs—especially startup fintechs—is doubtful, the government can play a pivotal role in supporting them. How? For instance, the central and state governments can give tax breaks, tax holidays, or other incentives to the banks and financial institutions who utilize the technology strengths of fintech startups in digitalizing their processes—especially in the priority lending sector. As discussed earlier, many NBFCs and MFIs still have either manual processes or rely on archaic technologies. They have never prioritized upgrading to more automated software systems. Yet now is the perfect time to help them do it as they look at ways to grow their businesses with a minimal workforce.

We have all seen, with mounting horror, the health and economic impacts of the Covid-19 crisis as they have unfolded globally over the past months. Unlike any crisis before, we face a challenge in that traditional humanitarian responses may not work. This crisis is unique in affecting large parts of the world at the same time, and responders who would usually be organizing ground-based efforts to specific locations and populations are themselves in lockdown, and often stunned by the scope and scale of the needs to be addressed.

We are having to work out, in a very short amount of time, how we offer humanitarian relief and solutions to these problems, and how we do this from a distance. Most are turning to digital platforms such as DFS (digital financial services) as the answer. Many donor organizations are immediately looking to replicate reactions from elsewhere in the world by organizing massive G2P (government-to-person) payment programs to alleviate missing incomes and are looking to use DFS and mobile money to execute them.

At MSC and Caribou Data we wanted to see how we could contribute to making these programs more successful, and we asked ourselves how we can, also from a distance, use our experience and platforms to understand what the situation for mobile money and banking agents is on the ground in Kenya. We wanted to understand how they’re coping with lockdowns and curfews, social distancing and hygiene, and reduced hours of bank opening. We wanted to understand how cash flow was changing, whether liquidity was becoming an issue, and what the experience of being at the very physical frontline of a digital banking system felt like for an agent in these troubled times.

After a brief discussion, we dove directly into a research sprint, using near-live data from the Caribou Data platform and MSC’s extensive contacts within agent networks to attempt a seven day research process to understand what’s going on within these agent networks. We drew quant data from over 1,000 users in a demographically representative panel to see what real cash flows were over time, and we spoke to 20 agents, one super agent and five bank agent supervisors with a simple structured questionnaire to get a sense of the experiential issues of being on the frontline of money distribution.

Our full findings are below in this report, but in summary our findings show that:

DFS wallet balances are volatile, with an initial cash-out spike evolving into a pattern of reduced overall transaction volume but increases in transaction size, with the net effect of a halving of average wallet balances since the crisis started.

Agent commissions have halved, putting pressure on their own livelihoods, and increased transaction sizes are making liquidity balancing harder and harder.

Hygiene advice is poorly communicated to agents, if at all. Without clear advice, guidance and protective equipment, agents are at risk to themselves and their customers.

We recommend that the central role of agents as frontline workers in this crisis be recognized and supported, particularly as they will be crucial to managing cash out and liquidity as DFS social payment schemes are rolled out across large numbers of the population

Further detailed research on DFS agents’ experiences in the Covid-19 crisis is available from MSC here. We plan to investigate more areas for future research, such deep dives into gender, urban/rural differences and other countries such Ghana, South Africa and Bangladesh. We welcome other organizations support and ideas for future research topics – contact us at covid19@cariboudigital.net

In the wake of the COVID-19 pandemic, the global economy will be impacted by USD 1 to 4 trillion, depending on the agency you want to believe. What underlies the statistics? What is the impact on agriculture and microenterprises?

Preliminary qualitative research on the impact of India’s lockdown provides important indicators on what is to come. For most people in India, lockdown means home confinement. Exceptions include government officials and a few services deemed “essential”. All public transport—road, rail, and air remains suspended, while private transport is heavily regulated.

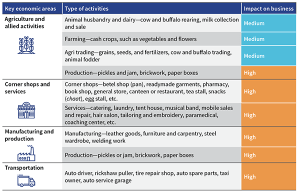

In this article, we have grouped microenterprises into four major categories.

Agriculture and allied activities

Corner shops and services

Manufacturing and production

Transport

At a high level, this is where they are, and the position will change—you bet!)

Impat of COVID-19 on business

Read on for a more nuanced and detailed understanding of agriculture and allied sectors and the corner stores and services sector.

We have split agriculture and allied sectors into three subsectors:

Animal husbandry and dairy: Farmers in this sector rear cows and buffalos to collect and sell milk. They form a significant part of the portfolio of microfinance institutions (MFIs) and banks, and have both an urban and rural presence. These farmers rarely sell milk directly to consumers. An intermediary or milk collection agents collect the milk on behalf of large dairies, such as Parag or Amul. In the case of intermediaries, they sell milk in the market and retain a margin. The farmers are paid less, but the payment is regular.

As of now, even though the consumption of milk has reduced (remember, the sweet shops and restaurants are largely closed!), the intermediary has been buying all the milk, selling a part of it and converting the rest into ghee (clarified butter). However, since the clarified butter cannot be sold at the pace at which it is being produced, the intermediary will not be able to pay the farmers for long— their cash flows are being affected. Hence, the dairy farmers will see a greater impact in the days to come—only so much milk can be converted into ghee and milk powder!

Indian poor farmer

Implication: As a first step, the government should prevail on large dairies, especially those in the cooperative sector to continue buying milk from the market, convert it into ghee or milk powder and keep paying the farmers. The rural economy will be severely impacted otherwise.

Crop farmers: Most farmers in India or around 70% own less than one hectare of land, which is below the subsistence level. Such farmers depend on MFIs for credit— this also includes landless farmers who rent land every season and cultivate. As of now, vegetable farmers are not impacted, and indeed are seeing an upside as prices of some vegetables, such as potatoes, have risen amid fear of scarcity. Farmers who cultivate staples are still on the edge—they are either harvesting their crops or have harvested their crops and are waiting to sell the produce.

Somewhat apprehensive, they are still hopeful that the administration will arrange to sell their produce in the market and they will realize a good price. In contrast, farmers engaged in flower cultivation are badly impacted. The demand for flowers has plummeted as temples and places of worship have shut down alongside flower retailers.

Implication: Mandis, which are wholesale grain, fruit, and vegetable markets, have to remain functional and farmers have to be provided transport for their produce. Farmers, especially those with mature crops should be allowed to harvest and get their grains to the market. The availability of farm labor is an issue, but the farmers will likely sweat it out in the field, with their family, to harvest standing crops. If the state can facilitate the journey from the farm to the market, we might see the current rural stress reduce somewhat. Otherwise, not only will the farmer be unable to repay debts, the next crop cycle will be impacted. Also, food grain prices will increase if the produce does not make its way to the markets.

Agri trading: This includes trading of grains, animals—cow and buffalos, seeds, fertilizers, and fodder shops. Seeds, fertilizer and fodder shops see moderate to low impact. In any case, it is early days for the demand for seeds and fertilizers. However, trade in animals has been affected seriously because the movement of goods is restricted.

Implication: The government will need to allow movement of agri essentials—seeds and fertilizer to keep the supply chains moving—both to provide inputs to farmers and to maintain food supplies. Although state governments have been vigilant in this aspect, the economic equation of demand and supply remains at play, and food grain prices have started to increase. In an atmosphere of hoarding induced by fear, it will be a herculean task to maintain normal food prices. Let us hope a good harvest can control price escalation.

Corner shops: Petty businesses, largely street shops and vendors play a critical role in the local economy. Except for those selling essential goods such as groceries, vegetables, and medicines, all other businesses are severely impacted as they are under forced lockdown. Those in the grocery business may be making a little extra money—or at least someone in the value chain is pocketing the extra cash that consumers are being made to shell out as prices begin to increase. On the brighter side, this segment of corner shops will be the first to bounce back once the lockdown ends. Though revenues may remain muted for some time, cash flows will resume as recovery gains ground and cash begins circulating in the economy.

Implication: Replenishing supplies at corner stores will call for more working capital. Will banks and MFIs have the liquidity to meet this need? A lot will depend on the relief package from the Government of India and the Reserve Bank of India. As of now, a three-month moratorium, which does not apply to NBFCs—the mainstay for these corner shops—is grossly inadequate. In case the informal economy is to survive, RBI will have to announce a six-month moratorium and include NBFCs and NBFC-MFIs as beneficiaries of the repayment holiday. How else will money flow into the informal economy?

Corner shop in India

Services: All activities under the services category are severely impacted. Either the demand for services has reduced or access remains an issue, or a combination of both continues to plague services. However, here again, recovery will be quick once the lockdown ends. MFIs and banks have moderate exposure to this segment and its loan requirements are not significant. In most cases, the person or entrepreneur is selling their skills.

Implication: These businesses may or may not need additional working capital. In case a loan is outstanding, stagger the repayments and increase the repayment period. The trickle of customers into these service outlets will build up gradually. Revenues will remain muted for some time to come. Spread the tenure of loans and—pray!

Mohammad Islam runs a small grocery shop in Dhaka. Like many, he was aware of the COVID-19 crisis unfolding in China. Yet he could never anticipate the pandemic would hit him and his business so fast, and so hard. Since the Bangladesh government announced a national lockdown, Mohammad Islam has seen his revenues decline by 20%. Thankfully, his business falls in the “essential services” category. He is allowed to open his shop albeit for limited hours. However, his stock levels have been depleting and supplies remain unpredictable. He thinks small traders like him, particularly those whose businesses are shut completely, will suffer the most. These businesses are also least likely to receive support from anyone, including the government. “The government plans packages for large businesses and the poor—nobody thinks about us”, ruminates another small trader in Nagerhat, Bangladesh.

Policy measures will be needed to minimize the impact on micro and small enterprises (MSEs) like those managed by Mohammad Islam. This case is symptomatic of the position of MSEs across low- and middle-income countries. These businesses are more vulnerable because they have limited cash reserves. And of course, business cash flows are fungible with household cash flows and vice-versa. They have rents to pay, typically make a significant proportion of sales on credit, and rarely use formal financial products.

Since the pandemic, the realization of sales proceeds on credit has crashed even as revenue continues on a rapid, downward trajectory. This will have an impact on the survival of MSEs in the short to medium term. Such businesses are un-registered, which makes it even more difficult for policymakers to target them effectively for support.

In this context, MSC kick-started a three-stage research exercise across eight countries in Asia and Africa to understand the nature and extent of the impact of the COVID-19 pandemic on micro and small enterprises. The research will gather evidence to inform policymakers to devise short–term, medium-term, and long-term support for such micro and small enterprises. The research will also inform MSE-focused financial institutions and their investors on remodeling business strategies to address the evolving needs of such enterprises better.

The early evidence from our research provides important insights that policy makers and other key stakeholders should consider as we prepare for recovery and rebuilding.

Most micro and small entrepreneurs believe that it will take at least another three months to normalize businesses, once the pandemic has been contained. Businesses that had purchased inventory immediately before the lockdown are the most affected.

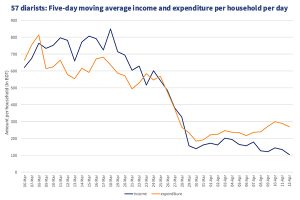

Data from 57 of Stuart Rutherford’s financial diarists, all of whom are from low- and middle-income households, in Hrishipara in Bangladesh, highlights a sharp decline in income and expenses immediately after the national lockdown. The Hrishipara Financial Diaries provide invaluable granular details on the lives of the poor and the impact of COVID-19. They show that income per household per day has currently dropped to BDT 100 (USD 1.18). Their expenditure has consistently been larger than income during the period, suggesting that household reserves are being eroded steadily.

This decline in economic activity and erosion of savings at the household level is likely to reduce demand, which will further have an impact on micro and small businesses that serve these low- and middle-income households.

Household Income and Expenditure graph

The story is similar in Indonesia, where the availability of credit from suppliers has started to dwindle, affecting the liquidity position of micro and small enterprises. “Before the Corona pandemic, my wholesalers allowed me to buy goods on credit. The pandemic has resulted in scarcity, and the wholesaler has stopped extending credit for products that are in high demand, such as vitamins, paracetamol, antibiotics, and flu medicine”, said a small pharmacy owner in urban Jakarta. He went on to add that wholesalers accept nothing but cash payment for these products. Restrictions have also been placed on the volume that can be stocked to avoid hoarding. “For other products that are not so much in demand, the wholesaler is still willing to give credit for one month”, he says.

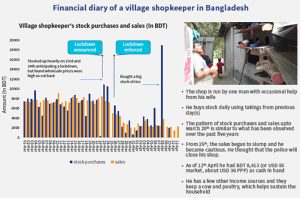

Financial Diary of a village shopkeeper in Bangladesh

While credit from wholesalers is drying up, MSEs are finding it difficult to realize cash from credit sales that they have made to their long-standing customers. “I give items on credit to many of my repeat customers—most of whom are daily wage earners. These customers used to pay me in cash on a weekly or monthly basis. However, because of the lock-down, people are not allowed to move freely and the amount owed to me is mounting. I am now worried whether I will ever realize my dues,” rued a small retail trader of tobacco and bakery products in India. Despite the challenges, some grocery retailers in India feel obliged to provide credit to their existing customer base, further adding to their liquidity crunch.

Given the evidence so far, a comprehensive policy framework to support micro and small enterprises will be essential. Many governments have responded with specific measures, such as a moratorium on the repayment of existing loans by MSMEs. However, these are at best, short-term solutions. A more nuanced approach will be needed going forward. Otherwise, the survival of most MSEs will be open to question.

A policy framework to accelerate the recovery of micro and small businesses should achieve the following objectives:

Address the immediate shock in cash flow

The liquidity crunch has severely affected microenterprises, particularly those managed by low-income families. They need immediate cash assistance to manage short-term cash flows. A cash transfer spread over three to six months will help these enterprises address the immediate shock in their cash flow. The volume of such cash transfer should cover the basic monthly expenses of the household.

Support enterprises to reduce expenses

Governments may consider offering direct subsidy to micro and small businesses through a waiver of utility bills. However, such a waiver should be tier-based to prevent wastage and overuse. “Electricity and water should be available for free for up to three to six months so that we can cover our losses. This might help us a little. Otherwise this year we do not know what we will earn and what we will save,” said a manufacturer of printing machinery in India.

Take proactive measures to boost sales and augment supply

Even amid the national lockdown in several countries, businesses classified as “essential services” are allowed to function with certain restrictions. The government, particularly local authorities, should work with such enterprises to ensure they can sell their goods without any fear of forced closure of shops. Our research shows that the police response across and within several countries is variable—some allow stores to remain open, while others insist that they shut.

Also, local authorities should permit and promote enterprises that offer home delivery services to support their sales.

Policy-makers should also focus on improving supplies. The value chain that gets raw materials and goods to MSEs must function effectively. Evidence from grocery stores in our research sample from India suggests that while the supply of food grains is robust, the supply of packaged food and other non-food essentials, such as toiletries and personal hygiene products is limited. This may be because the manufacture of such products has stalled or due to the closure of state borders, which restricts the movement of goods.

Promote the adoption of digital payments and the use of social media

Many entrepreneurs, especially in India, have been taking orders over WhatsApp. Customers enter the items they want or send a picture of their hand-written shopping lists. Digital payment options like Paytm and GooglePay facilitate home delivery options. The government should promote social media and digital payments as it helps social distancing even as business can be carried out. Governments may partner with private sector players, such as digital payments firms and social media platforms to enhance both personal hygiene communication and the development of the digital ecosystem.

Increase access to credit

The moratorium on existing loans to MSMEs, where allowed, will help address immediate challenges in liquidity. Nonetheless, those businesses that are allowed to operate during the lockdown will be able to repay their existing loans. However, they will need assurance that they will get additional credit once they complete their repayments. Therefore, policymakers and financial service providers need a nuanced, rather than a blanket approach.

Digital lenders that offer working capital assistance based on cash flows may be positioned better to offer instant credit delivered remotely. Any repayment moratorium on loans to enterprises should be based on the recovery cycle and the cash flows as they build-up. Similarly, a moratorium for those entrepreneurs who take loans after the initiation of lockdown should be reconsidered, so that lenders have the confidence to advance credit to businesses that are still functioning. This will help maintain credit discipline while maintaining some business revenue and liquidity for financial institutions offering loans to such enterprises.

Financial institutions are also part of a value chain. Unless those that extend wholesale credit to MSEs, such as microfinance institutions, get similar repayment moratorium, the liquidity position of frontline financial institutions will be affected. Hence, repayments have to be reworked across the credit supply chain.

The government should also use the opportunity to boost efforts to formalize micro and small businesses to deliver some of these policy outcomes effectively. This may require confidence-building measures among the micro and small enterprises and for MSEs to realize the benefits of formalization. The question remains — what are these and how do we communicate them effectively?

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

We are having to work out, in a very short amount of time, how we offer humanitarian relief and solutions to these problems, and how we do this from a distance. Most are turning to digital platforms such as DFS (digital financial services) as the answer. Many donor organizations are immediately looking to replicate reactions from elsewhere in the world by organizing massive G2P (government-to-person) payment programs to alleviate missing incomes and are looking to use DFS and mobile money to execute them.

We are having to work out, in a very short amount of time, how we offer humanitarian relief and solutions to these problems, and how we do this from a distance. Most are turning to digital platforms such as DFS (digital financial services) as the answer. Many donor organizations are immediately looking to replicate reactions from elsewhere in the world by organizing massive G2P (government-to-person) payment programs to alleviate missing incomes and are looking to use DFS and mobile money to execute them.