The G20 Ministerial Conference on Women’s Empowerment (MCWE) was held from 24th to 25th August, 2022 in Bali as part of the G20 Presidency of Indonesia. It is a crucial precursor to the 17th G20 Heads of State and Government Summit, scheduled for November, 2022 in Bali. The Summit will be the pinnacle of the G20 process and the intense work carried out within the ministerial meetings, working groups, and engagement groups throughout the year.

MSC (MicroSave Consulting) supported the MCWE 2022 by leading the gender recommendations on the digital economy. We worked with many stakeholders, including the W20 working group and the Ministry of Women Empowerment and Child Protection in Indonesia, to create recommendations on accelerating women’s participation in the digital economy and the future of work.

Indonesia’s Minister of Women Empowerment and Child Protection I Gusti Ayu Bintang Darmawati, delivered the welcome note on the first day of the conference. She hoped MCWE would serve as a valuable platform to share global ideas, future trends, and best practices on gender equality and women’s empowerment.

The conference covered three main topics: the care economy post-COVID-19, closing the digital gender gap, and women’s entrepreneurship. Leading the discussion on the second main topic, Graham N. Wright, Group Managing Director of MSC, spoke on “Bridging the gender digital divide: from intention to action, learning from best practices.” Graham shared insights on how women are less likely to own a smartphone than men, while 264 million women worldwide are unlikely to use mobile internet. Meanwhile, the digital exclusion of women can cost an estimated USD 1 trillion in GDP loss and a USD 24 billion missed in tax revenues annually, as per a study of 32 low and lower-middle income countries (LLMICs) by the Alliance for Affordable Internet (A4AI) in 2021.

In the second session of the conference, participants discussed the digital gender gap. The session included ministerial statements from India, South Africa, South Korea, Argentina, Saudi Arabia, and Russia.

On the conference’s second day, Indonesia’s Minister of Women Empowerment and Child Protection presented the meeting’s summary notes and policy recommendations to the G20 leaders.

The Ministry of Women Empowerment and Child Protection developed and presented six policy notes on education, employment, the digital economy, environment and climate change, energy transition, and health. The policy notes submitted by the MSC-led digital economy working group distill key recommendations to G20 ministers to bridge the digital gender gaps. The recommendations suggested to:

Increase the number of women-owned MSMEs in the digital economy;

Reduce the gender digital divide and upskill the capacity of women and girls to access digital platforms;

Increase public and private investment to promote a transformative digital economy;

Guarantee safe access and use of digital technologies;

Eliminate gender bias in AI and other emerging digital technologies.

Bhupen, a 23-year-old from Tripura, is a full-time owner and chef at a small eatery in New Delhi. He has earned a reputation as one of the best chefs in the area for budget Chinese takeaways. Bhupen’s job keeps him busy since the cafe is located near a popular corporate office. This leaves him with few opportunities to visit his family back in Tripura.

An overview of the scenario in Bhupen’s household

During the second wave of COVID-19 in 2021, the offices around Bhupen’s cafe were closed, and his business came to a grinding halt. The crippled economy forced Bhupen to shut shop and move back to Tripura.

Bhupen found himself in a completely different world back in his home state. He realized this when he heard that his father, Bipin, braved the risk of infection and queued up at the local post office to pay his monthly recurring deposit (RD). Bhupen was shocked. After all, Bipin was not a novice smartphone user—he used it to access social media platforms, such as Facebook and Instagram.

For Bhupen, saving monthly deposits is as easy as opening an app and typing the security PIN. Bipin should not have to stand in queue for something that seemed relatively trivial in Bhupen’s world. Despite the gloomy environment of the second wave, Bhupen decided to make the most of his time at home. He prioritized teaching his family a few basic digital use-cases. However, Bhupen could not find a way to make the post-office RD payments in any of the popular payment apps he used.

It did not take long for Bhupen to find a solution. When travel restrictions prevented Bipin from reaching the post office, an opportunity presented itself.

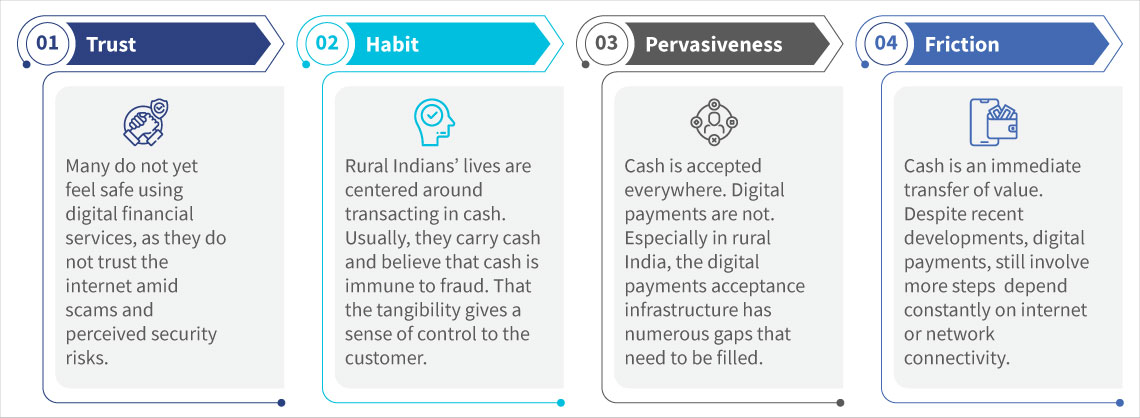

Before proceeding with Bhupen’s story, let us give you some context. In India, it is easy to assume that people must be willing to welcome convenient mobile-based platforms, such as Unified Payments Interface (UPI), or third-party apps like Paytm, or Google Pay, which offer integrated services. This was not true in Bipin’s case.

While he knew of the possibility of paying bills and monthly deposits from the comfort of his smartphone, he was risk-averse, did not trust digital financial transactions and lacked operational knowledge of such platforms. As a result, Bipin labeled himself as digitally illiterate. Such hesitation is common among low- and moderate-income (LMI) customers. We can break down the struggles of this customer segment into four key challenges.

Figure 1: Rural India’s challenges in adopting digital payments

An average smartphone user’s journey to digital payments

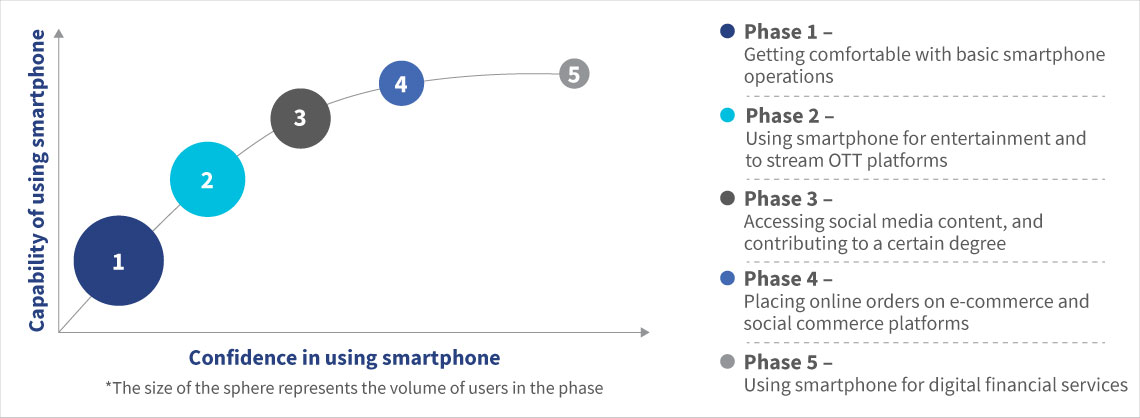

The rate of smartphone penetration in India has increased exponentially. It currently stands at 54% and will reach 96% by 2040. However, smartphone penetration in itself may not translate to an increase in digital payments and digital banking.

If we want every smartphone-equipped Indian to use digital payments, firstly, we need to understand an average smartphone user’s journey. Digital readiness is a continuum, which, when plotted across the axes of capability and confidence in using a smartphone, results in five phases as depicted in the graph below. MSC has seen these five phases replicated across Asia and Africa.

Figure 2: Path of the digitally ready to digital payments

In phase 1, all users try to get comfortable with basic operations, such as placing calls, exchanging SMSs, installing applications, using WhatsApp, using the camera, and navigating the user interface. Millennial and Gen-Z smartphone users, such as Bhupen, can navigate their smartphones easily. Hence, they quickly transition to phases 2 and 3.

In phase 2, users adapt to their smartphones for entertainment without incurring any significant additional cognitive load. This is when they start surfing video-streaming platforms, such as YouTube, web-based over-the-top (OTT) entertainment platforms, and music applications.

In phase 3, users gain more confidence as they sign up on social media platforms, such as Facebook and Instagram, where they consume digital content and contribute to it in various degrees. Most users usually limit their smartphone usage up to this phase. They do not feel comfortable moving beyond this usage level, as they have a higher perceived risk of fraud and fear making unintentional mistakes that would put their money at risk.

A comparatively smaller portion of users climbs to phase 4, where users can place online orders on e-commerce and social commerce platforms, such as Amazon, Flipkart, and Meesho. While users in this phase can operate their smartphones, they lack the confidence to make digital payments. Hence, while they may place the orders online, many opt for cash-on-delivery. Most netizens in rural India hold back from making digital payments.

A tiny proportion of users like Bhupen manage to advance to phase 5. Factors, such as social proof, age, assistance from a trusted network, and convenience often propel this journey. This stage is characterized by users first making digital payments wherever possible, followed by advanced digital financial service (DFS) use-cases, such as opting for digital credit, digital savings, and digital insurance through a smartphone.

Bhupen ignites a digital revolution at home

Now, let us get back to Bhupen.

Figure 3: Level of smartphone usage by Bhupen and his father

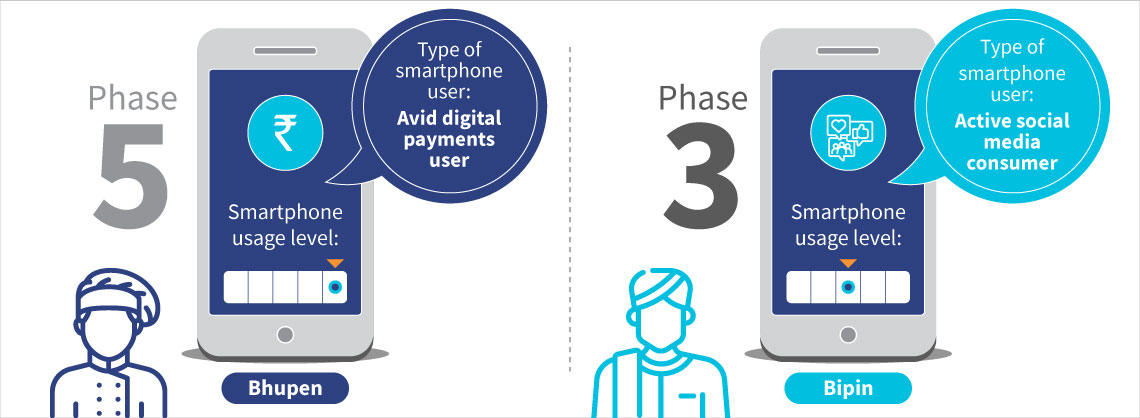

Bhupen knew of his father’s digital readiness. Hence, he was optimistic that he would be able to nudge Bipin to use digital payments for his RD deposits.

Unable to find a way to pay digitally through the payment apps, Bhupen approached Rakesh, the local Grameen Dak Sevak (postperson) and family friend. Rakesh suggested Bipin to open an India Post Payments Bank (IPPB) savings account, which offers digital payment options for popular post office small savings schemes. Rakesh offered doorstep banking services through which Bipin could pay in an assisted mode.

Rakesh used his handheld device to authenticate Bipin’s biometrics and opened a savings account for him. In a few minutes, he completed the electronic KYC without any papers, on-boarded Bipin, and linked the RD to his savings account. With Rakesh’s help, Bipin could now make Aadhaar-enabled payments from his IPPB savings account to the connected RD account through the Aadhaar-enabled Payments System (AePS). The ease of the process, the empathetic Grameen Dak Sevak, and the assisted onboarding mode won Bipin over. Bipin was on his way to phase 5.

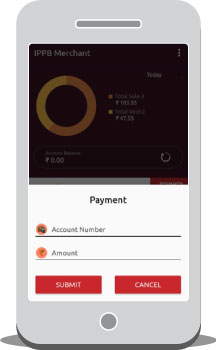

Figure 4: RD collection screen on the IPPB agent application

Was this all that the digital payments ecosystem had to offer to Bipin?

No … Bhupen was convinced his father could move to a self-service payment mode. After all, readiness to use self-service platforms, such as mobile apps, is more likely to lead to repeat use and graduation to more digital use-cases.

After the second wave of the pandemic receded, Bhupen returned to New Delhi as business resumed. One day, as he was about to pay his electricity bills, he started worrying about his parents back home. Bhupen called his father and was in for a pleasant surprise when Bipin revealed that he has had figured out how to pay household bills through the IPPB mobile app. With Rakesh’s support, Bipin downloaded and started using the IPPB mobile banking app. Hence, Bipin paid last month’s RD, electricity bill, direct-to-home (DTH) television bill, and gas bill through the app. Bipin was truly on his way to phase 5 now.

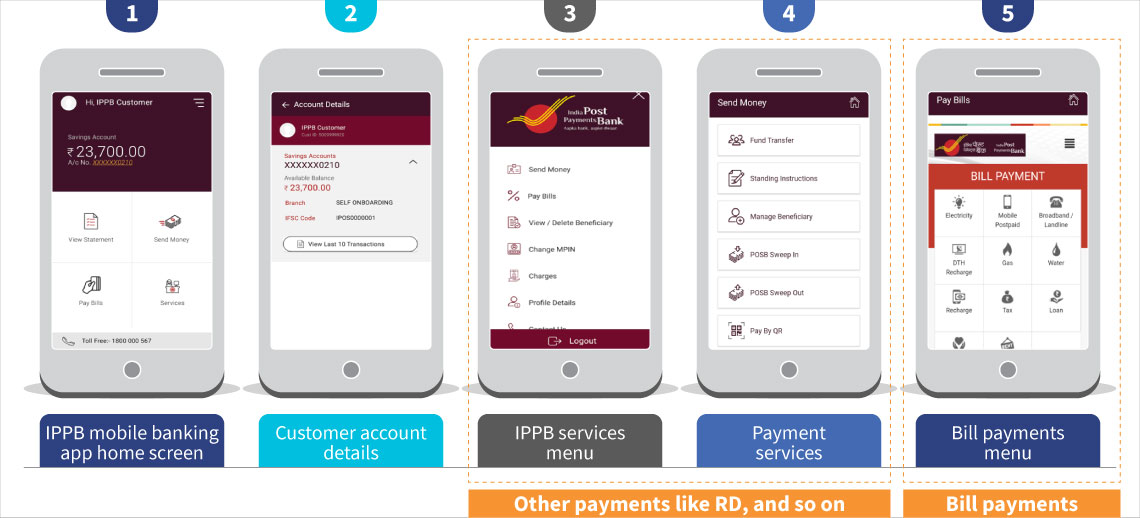

Figure 5: IPPB mobile banking application – services menu

Fast forward to the present date, Bipin pays most of his bills and makes deposits digitally through the IPPB mobile banking app from the comfort of his home. This would not have been possible if Bhupen had not initiated a digital revolution at his home and a helpful postal agent had not handheld his father onto mobile banking. Millennials like Bhupen, ably supported by financial institutions like IPPB, play a crucial role in onboarding middle-aged and senior users onto the digital payments ecosystem.

Watch this short video below to see how IPPB has enabled young Indians like Bhupen to become “mobile-first” and helped them onboard their households onto digital platforms.

The Bill & Melinda Gates Foundation commissioned MSC to conduct an action research program to enhance the quality and usage of digital financial services among female traders in open-air and cross-border markets in Kenya. We analyzed 6,000+ transactions in the research and we bring forth findings from these financial diaries research in Kenya in this report.

In our report, we will further unpack the financial life of women-led MSMEs and asses the constraints they grapple with in open-air and cross-border markets. The research also uncovers in-depth knowledge on the opportunity to serve this segment with quality digital financial services to accelerate financial inclusion.

Faith is a married woman with three children. She runs a microenterprise in an open-air market in rural Namanga, Kenya, and sells dairy products. Her business enables her to earn a living, averaging around USD 18 daily. Faith often faces liquidity crunches, especially during the lean season in January when earnings drop to less than USD 12 per day. This income is barely enough to feed her family and keep her business a float.

Faith wants to rear chickens and fatten pigs since she heard from her friends that these ventures offer high margins. She believes diversification will help her overcome cyclical downturns in business and increase her earnings. Faith also dreams of transitioning from operating in open-air markets to running her business in a permanent structure—for which she would need access to formal financial services—and credit—often unavailable because she lacks collateral. The digital resources available are expensive and provide small loans that fail to meet her business needs.

Faith’s story is not unique. Many like her in the developing world run successful micro businesses but remain invisible to formal financial institutions. It is almost as if the unbanked and the banked exist in separate universes, co-existing yet unable to meet for mutual benefits.

A key question emerges at this juncture. How can financial institutions offer innovative digital financial services (DFS) that meet Faith’s needs, increase her business’ resilience, and help her attain financial goals?

Women who work in open-air and cross-border markets present an untapped opportunity

In Kenya, the near-ubiquitous “access” to financial services results from the widespread use of mobile money. Digital payments enable pundits to tick the box and declare women “financially included.” However, under the hood, a significant gender gap persists in the “usage” of formal financial services.

Women like Faith contribute significantly to the Kenyan economy. Kenya has 1.17 million women-led micro and small enterprises (wMSEs) operating from open-air markets. Of these, only 50,000 are formal enterprises (MSC, 2011; KNBS, 2017). Moreover, Kenya has a large population of women who sell goods across borders (cross-border traders). MSC’s financial diaries research shows that wMSEs need a median of KES 30,000 (USD 270) to start a business.

Projection from MSC’s financial diaries research shows that if we assume all wMSEs are eligible for affordable credit when starting their businesses, it alone would translate to KES 38 billion (USD 316 million) in new loans for financial service providers. Clearly, female traders’ ongoing needs for working capital would further expand this colossal opportunity.

Yet, most financial service providers continue on a “one-size-fits-all” approach to low-income segments. Instead, they need to show sensitivity to the needs of women like Faith. Female entrepreneurs often juggle many family responsibilities while running their businesses, which compels them to prioritize convenience. Moreover, many lack proper documentation and collateral, which makes access to formal credit even more challenging. Most women find digital payments useful. Yet digital payments do little to enhance their businesses, build financial muscle, or diversify income streams. Therefore, women-led enterprises are more likely to fail due to reduced liquidity and excess reliance on informal credit. Female entrepreneurs frequently borrow from chamas (self-help groups) and informal moneylenders who charge exorbitant interests, which often prove costlier compared to formal sources.

Demand and supply-side challenges

Financial inclusion is a prerequisite for women’s economic empowerment, development outcomes, and poverty reduction. In its current format, digital payments alone do not work for Faith and others like her. WMSEs need access to other financial services like credit, savings, and insurance. The inability of financial service providers to extend a comprehensive suite of services pushes Faith and her peers toward informal channels. Chamas are particularly attractive because they offer “easy” access to credit. Banks, on the other hand, require documentation and collateral.

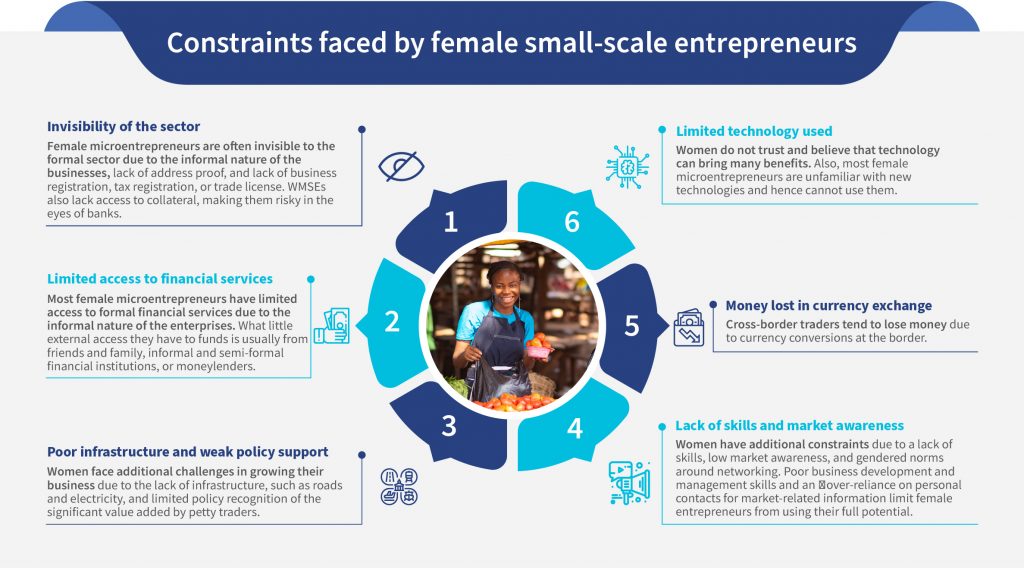

MSC conducted primary research in Kenya to understand the challenges encountered by women in open-air and cross-border trades. The study identified limitations that restrict comprehensive DFS usage by WMSEs—credit, savings, insurance, and payments.

The graphic below shows the constraints women like Faith face while accessing digital financial services.

On the supply side, challenges preclude the delivery of affordable financial services to women, which include:

Staff members of formal financial institutions have a limited understanding of the unique needs of female entrepreneurs and do not collect or analyze gender-disaggregated data. Thus, traditional banking methodologies and operations are not gender-sensitive and often lead to exclusion.

Financial institutions require formal documentation, which most WMSEs lack. The informality of WMSE business structures presents a data-related challenge for most financial institutions.

Most financial service providers have not evolved their lending methodologies to provide alternative ways of credit scoring.

In stark contrast to the experience of microfinance institutions across the globe, most traditional financial institutions believe WMSEs present high credit risk (Are women better borrowers in microfinance? A global analysis, 2020). This is mainly due to their lack of collateral and the inability of financial service providers to develop innovative solutions to lend without depending on collateral.

Financial institutions make no genuine attempt to tailor products and services to suit the needs of women like Faith. No single provider—formal or informal—meets more than one or two of her financial needs.

Currently, financial and non-financial services are insufficient to help WMSEs build and grow their business. Financial service providers need to provide customized and bundled products and services to meet the complex and diverse needs of women like Faith.

MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

Usage and quality of DFS for women in open-air markets and cross-border traders

byMicroSave Consulting

In our podcast today, Nicholas Mungai, and Thomas Murayi, financial inclusion experts at MSC, give an in-depth analysis of how digital financial services can bridge the digital divide to make formal financial formal services available to women, particularly those in open-air markets and cross-border trades.

MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

This podcast brings together MSC’s Financial Services Analysts, Nicholas Mungai and Gregory Ilukwe. They share insights on how the significant changes and milestones in Kenya’s financial services sector have shaped the sustainability of its mobile money agents. They also discuss how the future of mobile money agencies should hinge on agents offering various complimentary financial and non-financial services to ensure their sustainability.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

Bhupen, a 23-year-old from Tripura, is a full-time owner and chef at a small eatery in New Delhi. He has earned a reputation as one of the best chefs in the area for budget Chinese takeaways. Bhupen’s job keeps him busy since the cafe is located near a popular corporate office. This leaves him with few opportunities to visit his family back in Tripura

Bhupen, a 23-year-old from Tripura, is a full-time owner and chef at a small eatery in New Delhi. He has earned a reputation as one of the best chefs in the area for budget Chinese takeaways. Bhupen’s job keeps him busy since the cafe is located near a popular corporate office. This leaves him with few opportunities to visit his family back in Tripura

Figure 3: Level of smartphone usage by Bhupen and his father

Figure 3: Level of smartphone usage by Bhupen and his father

Figure 5: IPPB mobile banking application – services menu

Figure 5: IPPB mobile banking application – services menu

Faith wants to rear chickens and fatten pigs since she heard from her friends that these ventures offer high margins. She believes diversification will help her overcome cyclical downturns in business and increase her earnings. Faith also dreams of transitioning from operating in open-air markets to running her business in a permanent structure—for which she would need access to formal financial services—and credit—often unavailable because she lacks collateral. The digital resources available are expensive and provide small loans that fail to meet her business needs.

Faith wants to rear chickens and fatten pigs since she heard from her friends that these ventures offer high margins. She believes diversification will help her overcome cyclical downturns in business and increase her earnings. Faith also dreams of transitioning from operating in open-air markets to running her business in a permanent structure—for which she would need access to formal financial services—and credit—often unavailable because she lacks collateral. The digital resources available are expensive and provide small loans that fail to meet her business needs.