MSC conducted a deep-dive analysis of the digital credit users in India, Indonesia, and Kenya to assess the impact of digital credit on their financial health. The analysis presents the insights from the assessment and recommends actionable interventions at the level of providers, regulators, and policymakers to enhance the financial health of digital credit users.

This report was launched at the Global Fintech Fest in Mumbai, India on 21st September, 2022.

Ramesh, a daily-wage worker from Bihar, India, can send money easily to his family with the help of postal workers. Ali, a retired military officer from Aswan, Egypt, no longer has to queue outside any government offices to receive his social security payments. He can withdraw money easily from any Egypt Post ATM or POS-enabled post office with zero charges. Dizola, a micro-entrepreneur from Allada village, Benin, can conduct digital transactions through his postal account, even on his feature phone.

What common thread binds the lives of these people? The answer is the role the respective postal networks in their countries play to spearhead safe, affordable, and convenient customer transactions.

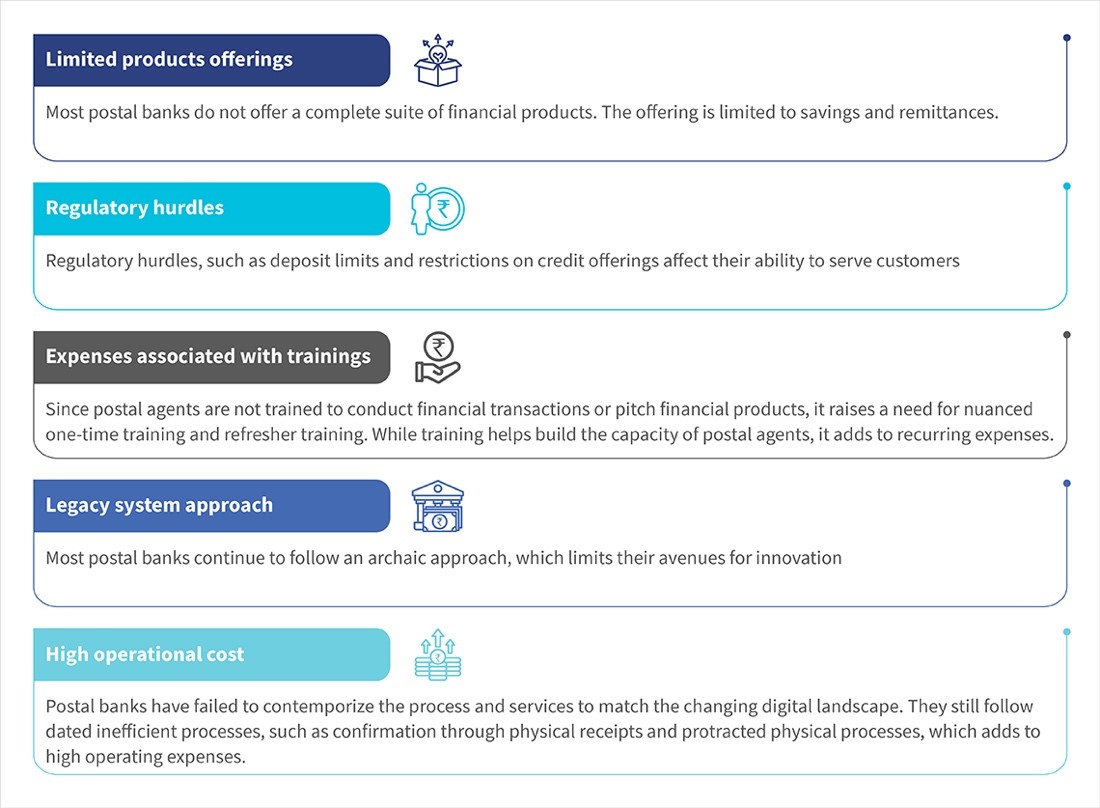

Predominant supply-side challenges faced by postal banks across the globe

Demand-side constraints including limited literacy, lack of formal documents, and lack of awareness about the formal financial channels, further exacerbate the situation. As a result, financial institutions, including postal banks, struggle to cater to LMI customers. Postal banks must now transform themselves to cater to their existing and potential customer segments against the backdrop of the changing financial service ecosystem and evolving needs of customers like Ramesh, Dizola, and Ali. The graphic below spells out some demand-side challenges:

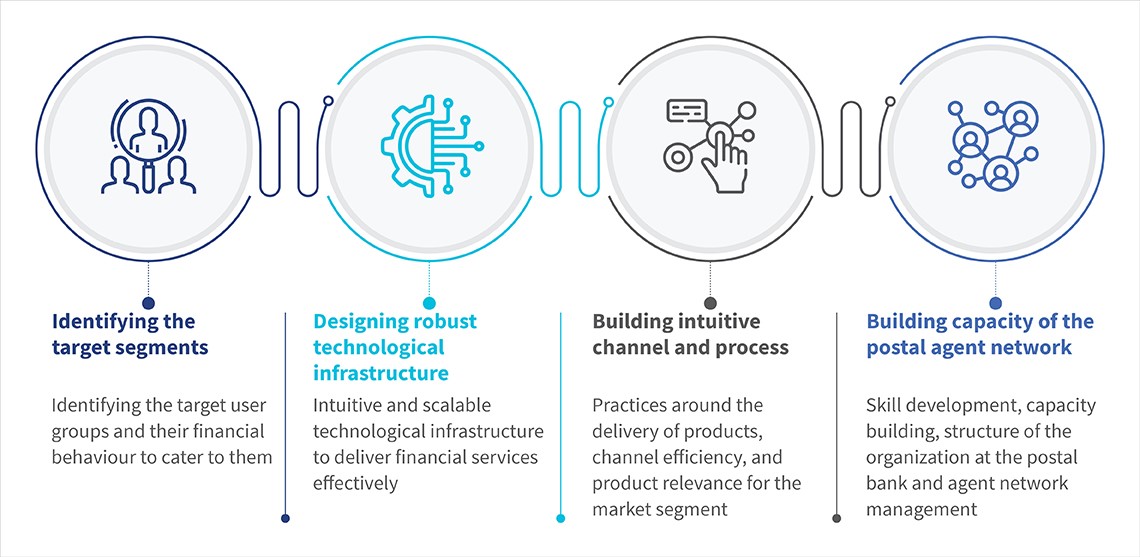

We have used the 2T2P: Target segment-Technology-People-Process approach to assess and suggest how postal banks can optimize their business operations, serve the target customer segments, and transform digitally to survive and thrive in the diverse ecosystem of financial services.

1. Target segments: Identify the right user base for the services

The customer comes first. Over the years, we have seen a major shift in customer behavior and expectations. This change has compelled financial institutions, including postal banks, to redefine their priorities to meet evolving customer needs. The postal banks must first understand the target segments to provide them value.

Profile customers: Capturing the customer lifecycle with data on financial behavior can help postal banks offer customized products, predict the need for different products, use their channels efficiently, and unlock new opportunities in the space.

Focus on advanced use cases: Emerging technologies can potentially offer advanced use cases for digital financial services. The emergence of big data has enabled different approaches to credit scoring, allowed providers to cross-sell and upsell products and services, and enabled the addition of new use cases. Postal banks are well-suited to use their existing database to provide financial services to underserved populations.

2. Technology: Achieving scale through intuitive tech infrastructure

Technological progress is transforming the financial services ecosystem globally, which can help postal banks build an efficient business model over time. Postal banks worldwide struggle with legacy systems and the inability to innovate fast. Postal digital transformation cannot take place by simply layering technology over legacy systems. It requires the creation of modular tech infrastructure and an easy-to-use interface that target segments will find intuitive and convenient. Once such upgrades are implemented, postal banks can scale and use data to advance their customers’ digital finance journey.

Build an intuitive frontend interface for customers: A user-centric platform is essential to facilitate usage and enhance customer experience. Since LMI customer segments have limited digital literacy, postal banks must build intuitive and easy-to-use solutions in regional languages with voice-assisted modes. These users have not experienced financial services on smartphones. The frontend customer interface must therefore be intuitive, with ample handholding to boost customer confidence and trust in digital transactions.

Develop a scalable infrastructure at the backend: Postal banks must use technology to implement new services and diversify into new business models to scale their services. Their core architecture must include digital innovation, e-commerce, data collection, API development, and digital identity. This inclusion will enable postal banks to propose new services, increase efficiency using technology, drive innovation and agility, and improve resilience and scalability.

Ecosystem enablement—API-driven open architecture approach: Postal banks can build strategic partnerships with emerging FinTechs and other institutions to provide products on demand through open APIs. This will help customers access multiple solutions through postal banks. It becomes a win-win solution for FinTechs and postal banks, which they can use to build competitive advantages and drive financial inclusion.

3. Process: Building efficient processes and operational models to deliver relevant products to specific segments

Customers prefer a bank that understands their needs, offers suitable products, maintains transparency, offers simple and streamlined processes, and is approachable. With an expanding internet and smartphone user base across markets, postal banks can offer many services at low costs efficiently through digital and non-digital channels. However, postal banks need to combine an all-digital experience with a human touch to cater to people at the bottom of the pyramid.

Build a “phygital” operational model and processes to deliver relevant products and services to the last mile: Most postal banks have a significant physical presence that they can use to serve customers better. Depending on the existing bank structure, postal banks can gradually move to a digital-led operational model where their postal agents serve customers using digital devices. Many postal banks can take a phase-wise approach to roll out the services and move gradually from an assisted model to a self-service mode. This way, they can still keep features like doorstep delivery that add to the convenience of the customer segment, and take digital financial services to vulnerable segments, such as pensioners and rural women.

Use the trust in the post’s brand and network to add new financial and non-financial services: Most customers trust their postal banks. Postal banks can use this implicit trust to add new value-added services based on the lifestyle needs of customers, who otherwise largely remain unserved and underserved by incumbents in the ecosystem. They also offer a really important opportunity for G2P (government-to-people) payments, as postal banks typically have significant outreach into the vulnerable and remote communities targeted by G2P programs.

4. People: Developing capacities of the agent network and staff within the organization

Postal banks reach and serve customers at scale through their vast distribution network. Evolving customer expectations and technology make it essential for postal banks to recognize the emerging needs of their customers and build a skilled workforce that caters to their specific target segments. A major struggle for postal banks is achieving a sustainable business model while developing their network capacity.

Build capacities and skill sets of postal agents to deliver digital financial services: Traditionally, the role of a postal agent is limited to mail delivery services, and they are not accustomed to using digital devices for operations. Transitioning from a mail carrier to a financial inclusion enabler requires nuanced training. If postal agents wish to develop their skills, they must receive training at regular intervals with hands-on experience. They can then serve customers better.

Acquire strategic leadership and enhance the existing team’s skills with a focus on innovation with better product design and delivery: Postal banks need leadership teams that understand tech-based solutions of FinTechs and know about the operations of traditional banks. A combination of the two will help them select the right partners to drive innovation in postal banking and expand their business. They can then sustain their digital finance ambitions with a clear vision, strategy, and roadmap in-house.

Conclusion:

Research suggests that households and businesses with access to formal financial services can respond better to financial shocks. Postal banks, alongside other financial institutions, continue to make efforts to reach the 24% of people worldwide who still lack a bank account. The assisted banking approach, and technology-based solutions offered by postal banks, coupled with their vast network, show a high potential to serve millions of underserved customers like Ramesh, Ali, and Dizola.

The following blog in this series captures lessons from postal banks spread across our 2T2P model, which highlights how some postal banks can serve the excluded.

IPPB’s customer base grew from 23.6 million to 43.1 million in 2020/21.

“Dakiya daak laya, dakiya bank laaya” (“The postal worker brings us letters, they also bring us the bank”), sings Anupama, daughter of IPPB end-user Anuj, who sits chatting with a customer who wants to open a bank account. In a few moments, Anuj creates a new bank account—adding to one among the 30-odd accounts the postal bank opens each minute across India’s borders.

Forty-year-old Anuj lives in Kakori village in the Indian state of Uttar Pradesh, where he works for the Department of Posts (DoP) as a Grameen Dak Sevak (GDS) or Dakiya—a term of endearment for postal workers across large parts of the country. Anuj recently took up the responsibilities of a IPPB banking correspondent (IPPB BC), to his family’s delight. As aBC for IPPB, Anuj joins the ranks of thousands of GDS who contribute to IPPB’s rapid expansion at the last mile, fortifying the digital revolution brewing in India’s hinterlands.

Anuj joined the DoP after completing his senior secondary education. His compassionate nature soon helped him build a strong connection with the villagers. Besides delivering mail, at their request, Anuj often reads letters to older adults who await messages from their children who live in distant cities.

He also played another important role. All GDSs also help people open savings accounts with the post office, invest in long-term savings products, such as Sukanya Samriddhi Yojana (SSY) or Public Provident Fund (PPF), and thus introduce them to formal banking services.

Anuj often thought about how to reduce the inconvenience of Direct Benefit Transfer (DBT) beneficiaries when they had to travel long distances to withdraw cash. He believed assisted financial transactions at the customers’ doorstep or near it could help reduce the financial vulnerability of the elderly and the poor in his village. Anuj saw his dream come true when the India Post Payments Bank (IPPB) was created in 2018. IPPB offered him, along with other 189,000 GDSs across the country, a chance to join the Indian digital revolution by becoming IPPB banking correspondent.

Grameen dak sevaks hold the baton of inclusive banking

According to its FY 20-21 annual report, IPPB’s customer base grew by 83% that year, from 23.6 million to 43.1 million. To put this in perspective, IPPB opened an account almost every two seconds.

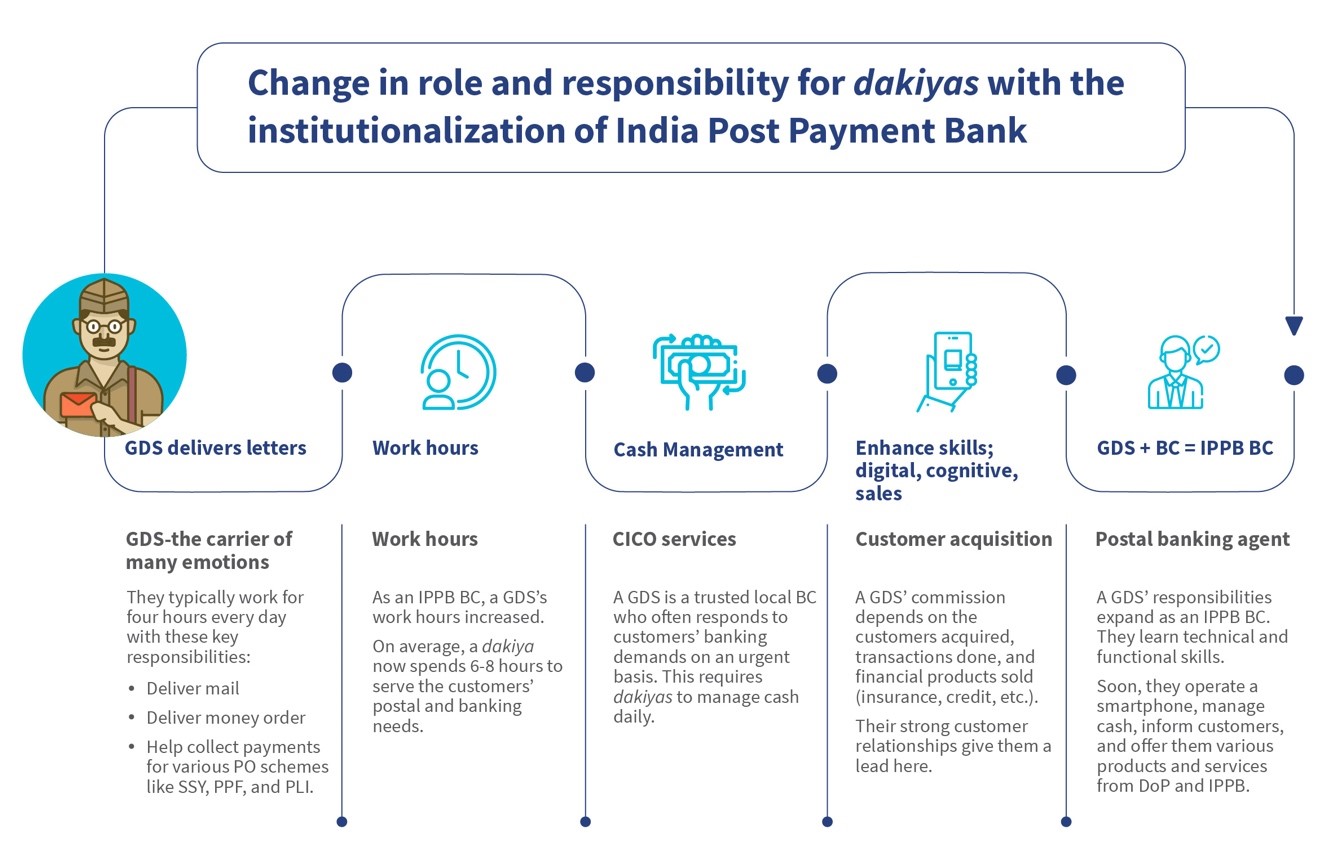

With the exponential growth of banking services and continued growing demand, GDSs have become critical to the delivery of inclusive banking in rural India. A GDS has multiple functions and has to learn new functional and technical skills to provide safe and secure digital banking services. This is easier said than done.

A Grameen DakSevak’s life as IPPB banking correspondent

When IPPB was institutionalized, many GDS sensed an opportunity and took up the role of banking correspondent to earn an extra income. Meanwhile, others found it challenging. While their job profile expanded, their responsibilities increased as well.

If a GDS chooses to work as an IPPB BC, they must gain technical knowledge of banking products, build cognitive skills to understand technology interfaces and devices, and develop business acumen to drive sales. Further, they attend classroom-based training by IPPB to qualify as banking correspondents. GDSs also attend external training mandated by the UIDAI to become eligible to offer Aadhaar-based, high-revenue products, such as the Child Enrolment Lite Client (CELC).

The enhanced role of the GDSs as IPPB BCs benefits them in multiple ways, including social recognition and additional income. For women, female banking agents further provide a safe space for banking. GDSs’ relationships with people in their neighborhood create a trusted path to onboard new customers onto digital banking. The graphic below highlights how a GDS can benefit from the role as an IPPB BC.

Different personas of GDS and their distinct needs

Several factors determine how easily a GDS can adapt to the postal agent’s role. These factors may be intrinsic, such as social recognition and empathy, or extrinsic, such as technical skills and support from the DoP.

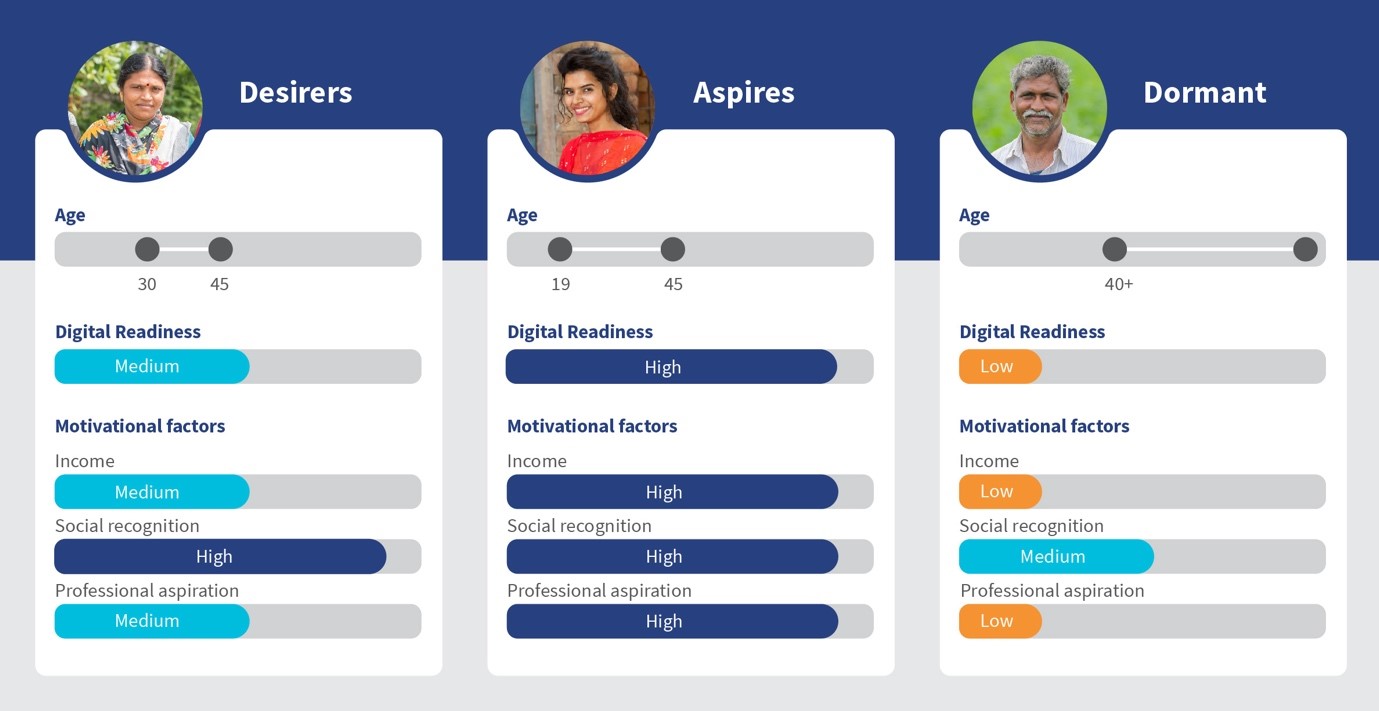

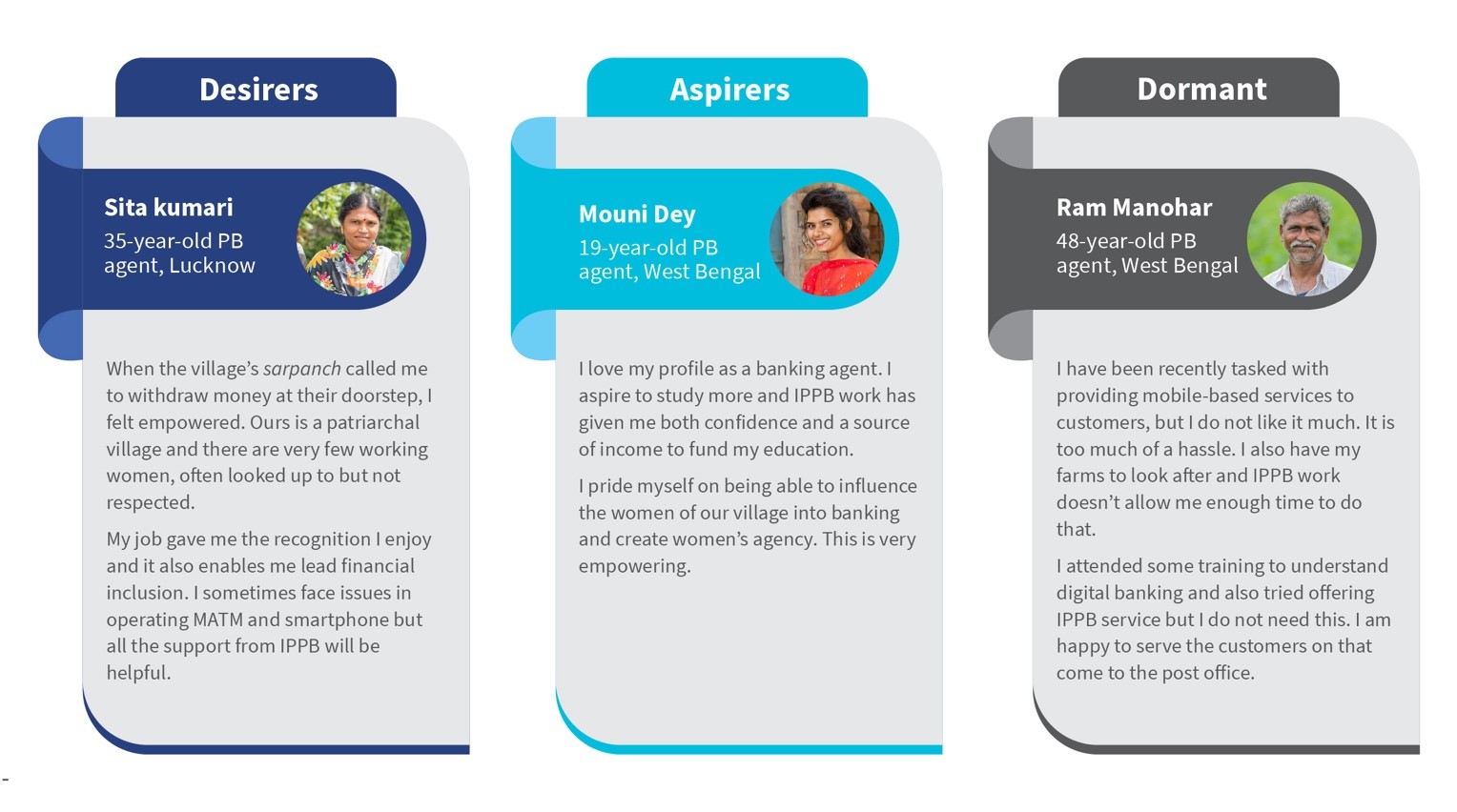

We explore three dakiya personas—desirers, aspirers, and dormants, to understand how this expansion of their role into an IPPB banking correspondent has affected them and their feelings about their role as BCs.

Desirers feel the IPPB banking correspondent opportunity empowers them: Desirers form a long-term relationship with IPPB. They are typically 30-45-year-old men and women from low- and middle-income (LMI) households. They have limited technical abilities and cognitive skills. Social recognition and enhanced income motivate them to work as agents. They struggle to operate micro-ATM devices, retain financial product information, or manage liquidity.

Yet the desirers’ spirit to work as change agents allows them to succeed. A true inspiration, these IPPB BCs have adapted to their enhanced role from postal deliveries to leading financial inclusion gracefully. IPPB and the DoP have launched successful initiatives to support the GDS with their enhanced role and responsibility:

The DoP and IPPB launcheddak karmayogi, an e-learning platform for GDSs to enhance their product knowledge and hence their commission income through higher sales. This will also enhance IPPB’s revenue—a win-win situation for all.

With support from MSC, IPPB launched bite-sized refresher training modules delivered digitally to the GDS. These modules act as ready reckoners for them.

Aspirers see the IPPB banking correspondent opportunity as a catalyst to their professional aspirations: Typically, Aspirers are highly motivated individuals like Anuj, who work as banking correspondents. They are extroverted younger people who like helping others. Moreover, they draw motivation from their ability to offer banking services to customers in their region. Many young GDSs also became postal bank agents to enhance their financial knowledge and supplement their skill set to become eligible for higher-level jobs. Further, high-incentive products, such as CELC, insurance, and bill payments motivate them to perform better and increase their income.

IPPB needs a mix of aspirers and desirers to build a strong foundation of on-field BCs and make the payments bank profitable.

Dormant are influenced by status-quo bias and need strong social proofing to adapt to the role of IPPB banking correspondent: The dormant is often a GDS who does not depend much on the role as a BC for their livelihood. They are typically 40+ year adults from relatively higher income backgrounds. Dormant has low motivation to work as banking correspondents and do not actively support digital banking services. They do, however, have great relationships in the village, and are influencers to many in their neighborhood. Initiatives that build social proof, such as recognition ceremonies, can motivate skeptics to spread banking information among their groups.

Looking ahead

The Indian postal system expects a lot from its GDSs, and many GDSs often struggle to offer financial services. Yet they have risen to the challenges and are now eager to help underserved customers in India’s towns and villages – and fulfill their aspirations by doing so. We need to enable and empower them to reach millions more who seek financial services in an environment they trust and consider safe.

Rafiqul, the son of a betel nut farmer in Kushtia, Bangladesh, had dreams beyond his village. In 2008, a newspaper reported an essay writing competition organized by NASA for children from low-income families in developing countries. The prize was a trip to space! Rafiqul submitted an essay and, to everyone’s surprise, won the first prize. He became a role model for other children in his village and countrywide.

Rafiqul’s story is part of the book The Government of Chronic Poverty: From the politics of exclusion to the politics of citizenship?, edited by Sam Hickey, in the chapter titled “School Exclusion as Social Exclusion: The Practices and Effects of a Conditional Cash Transfer Programme for the Poor in Bangladesh,” a scholarly paper by Naomi Hussain. His story captures and furthers the widespread belief in the possibilities that education can offer in Bangladesh. Many Asian and African countries share faith in the transformative power of education as it promises social mobility, material wellbeing, social inclusion, and status.

Bangladesh has many such Rafiquls. The Primary Education Stipend Programme (PESP) supports their aspirations by providing BDT 150 (USD 1.58) from the Government to their mothers. The benefit is conditional on maintaining 85% monthly school attendance and achieving at least 50% grades in the annual exams. The program started in 2001 to increase attendance and enrolment rates by reducing the dropout rates of primary school students. The stipend is transferred directly to the beneficiaries’ mobile banking accounts since 2017 instead of the earlier payment system in cash.

MicroSave Consulting (MSC) and the Centre for Global Development (CGD) conducted a mixed method research to gain insights into the PESP program and ascertain its effectiveness in achieving its objectives. The survey interviewed mothers who received the beneficiary stipend. Sixty-two percent of the interviewed mothers lived in rural areas. Only 17% of the interviewed mothers completed high school, and 34% of them, one-third, only finished primary school. More than half of these mothers were from poor economic households and worked as daily wage or agriculture laborers.

Mothers prefer digital payments to cash

More than 95% of beneficiaries preferred the new system of digital payments over cash payments. The most common reasons for choosing digital payments included how closely the agent is located for convenient cash-out, as cited by 81% of respondents, more monetary control, cited by 21%, and easy withdrawal, cited by 27%. More than half of the respondents mentioned they do not have to forgo a day’s wage to visit the school to receive the benefit in cash.

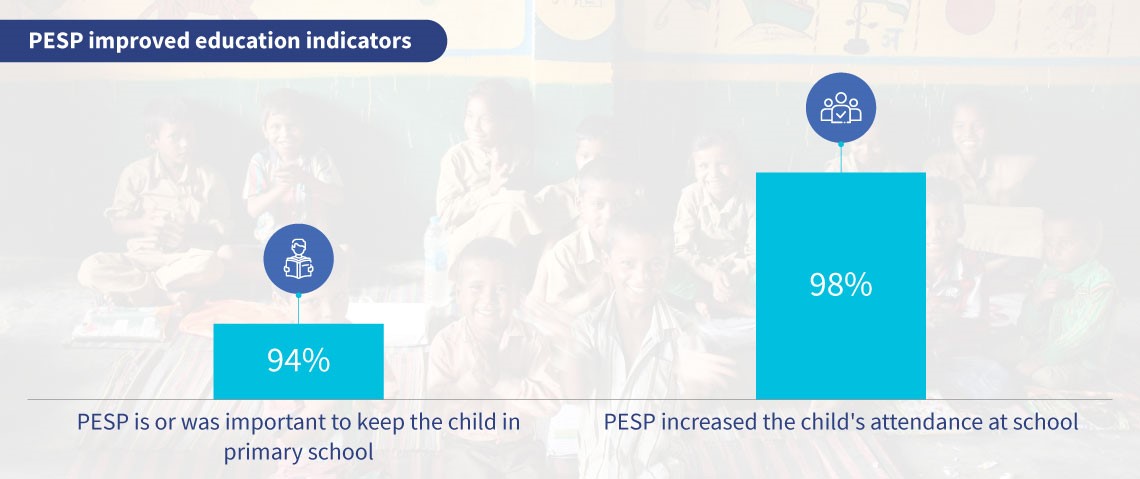

PESP and education indicators

One of the program’s main focuses was to improve education indicators, such as school attendance, enrolment ratios, and retention among primary school children. As per a World Bank report, enrolments in primary schools in Bangladesh increased from 80% to 98% between 2000-2015. Thanks to various other policy interventions, the enrolment rate has seen a consistent rise.

The gross enrolment rate considers all students, including underage and repetitions, which can go beyond 100%. Thus, the gross primary school enrolment rate in the PESP schools across different locations was estimated to be between 89% and 140%, whereas it was much lower for secondary schools and ranged only from 21% to 77% (Ahmad and Sharmeen, 2004). However, an increase in enrolment does not guarantee high retention or learning outcomes.

The requirement for more than 85% attendance to be eligible for PESP payments addresses the issues of retention and learning. These two hypotheses were tested in the field. Most mothers believe that PESP is essential to keep their children in school, with 98% reporting an increase in attendance and ensuring the children complete primary school.

Ninety-eight percent of mothers reported ensuring their children completed primary school, and none reported children dropping out for employment or vocational training. Another study by IFPRI estimated the dropout rates at 8.5% for PESP schools compared to 14% for non-PESP schools. The statistics reflect PESP’s effectiveness in improving attendance rates and reducing dropout ratios among the beneficiaries.

Additionally, PESP requires students to achieve specific grades to avail the benefits. The conditionality meant that about 89% of the parents invested in their children’s educational needs by hiring a private tutor, and 50% saved the stipend for the children’s future educational needs. From our qualitative evidence, we found that mothers used the transfer amount to buy new school supplies, such as uniforms, books, and stationery. Notably, 73% of mothers mentioned that PESP helped increase their role in the decision-making about their children’s education needs.

Several studies have drawn insights from PESPs in different geographies, highlighting how conditional cash transfers improve education outcomes. Similar studies on Progresa in Mexico and Program Keluarga Harapan (PKH) in Indonesia also found that CCTs help increase enrolment and attendance and reduce student dropout rates.

The Progresa program in Mexico facilitates short-term benefits, including increased attendance rates, reduced dropout rates, and enhanced grade progression of the beneficiaries. For children between 6-14 years, average education attainment levels increased by 0.7 years, and students attending school in their junior years increased by 21%. The long-term benefits are increased employment incomes and more geographical and social mobility.

The Government of Indonesia introduced the PKH program in 2007. The program helped increase enrolment by 4% among primary schoolchildren and 10.5% among secondary schoolchildren. Another study found that PKH delivered significant gains in the results of school-level examinations.

The PESP program, in common with other CCT programs, has increased attendance and enrolment ratios among the target group through conditional cash transfers. The transfer has also increased the amounts families spend on school supplies. Further analysis can help assess whether these improved ratios also translated into long-term outcomes, such as better economic prospects in the labor market and living standards. And more importantly the dreams of Rafiqul and others like him, could turn into reality.

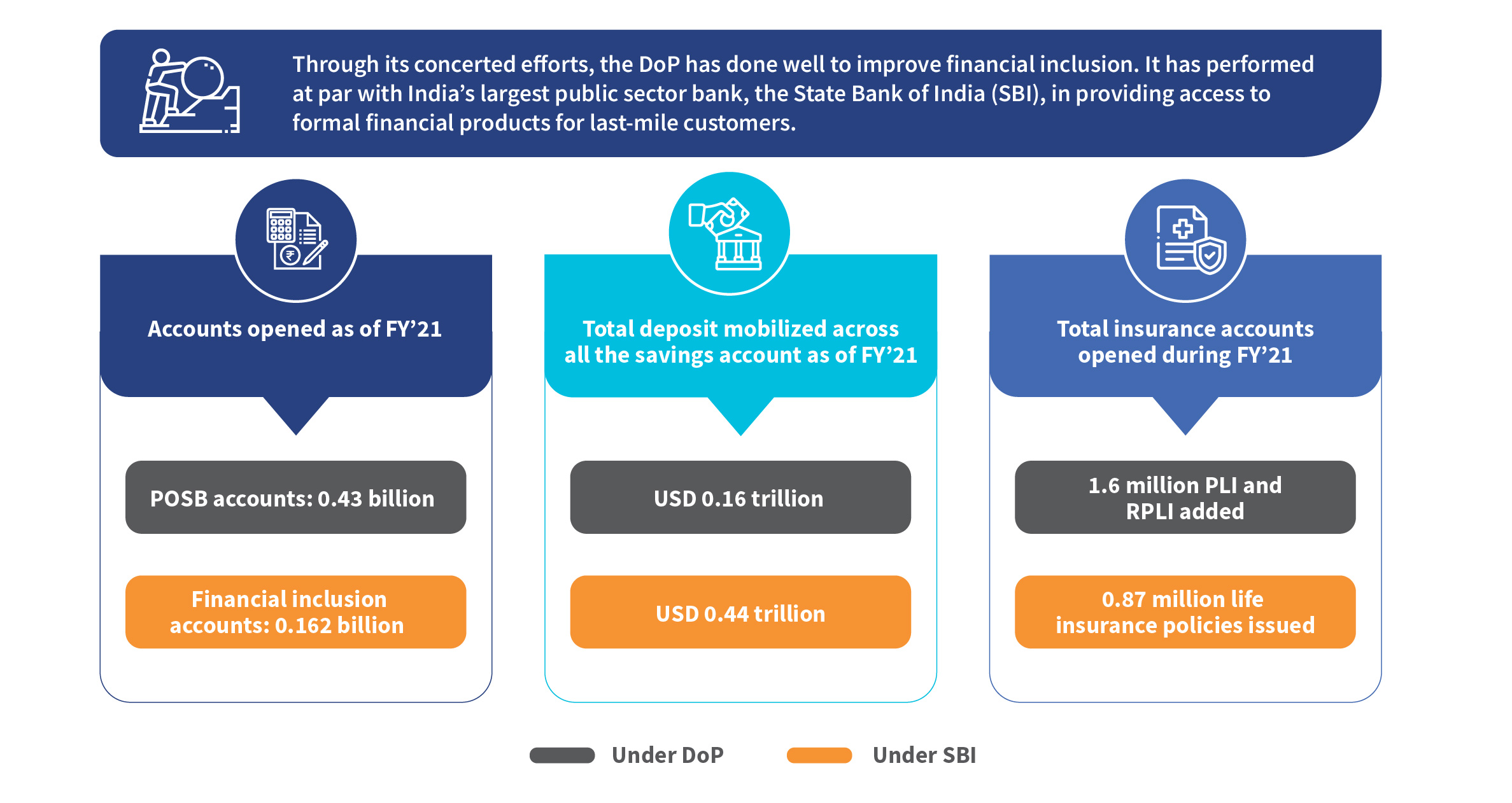

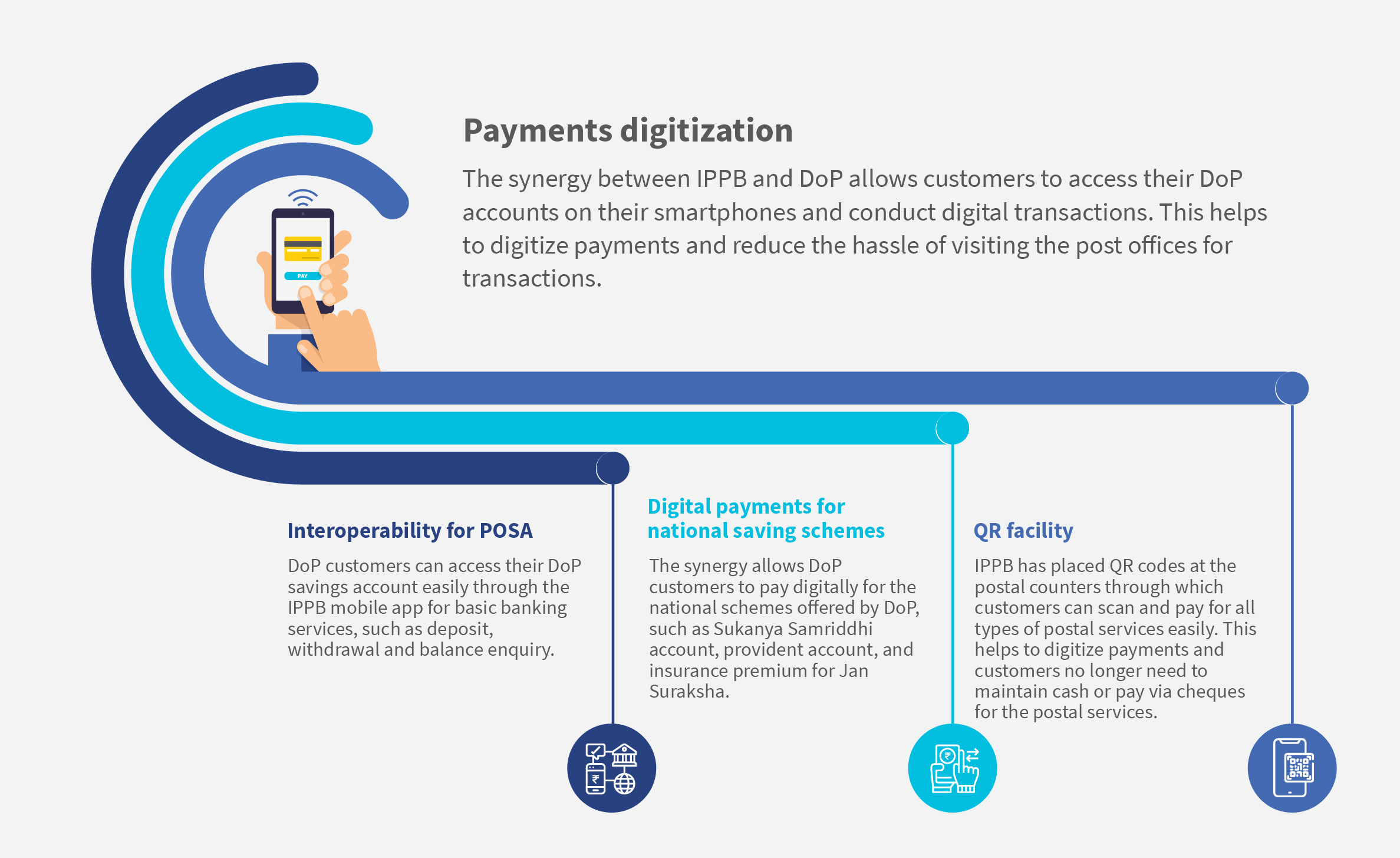

Stay-at-home mothers, pensioners, and migrant workers are some of the most vulnerable and underbanked populations across the globe, and in India. As per Findex 2021, 22% of Indians lack an account in any financial institution. Across banks, INR 267 billion (USD 336 billion) have been lying in around 90 million dormant accounts for more than 10 years, as of December 2020. Findex 2021 also reports that India has the highest share of inactive bank accounts globally at 35%. Women account owners in developing countries are, on average, 5% more likely than men to have inactive accounts. However, India leads the gender gap with a 12% difference in account inactivity. The India Post Payments Bank (IPPB) was set up in 2017 as a subsidiary of the Department of Posts (DoP) to address these challenges and provide safe, convenient, digital, and affordable banking services to last-mile customers. While millions of customers are financially included, the top two reasons why Indian adults from remote, rural areas do not use their bank accounts are the long distances from financial institutions and a lack of trust. IPPB intends to address these concerns with its last-mile presence, digital-first approach, and handholding support through its nationwide network of friendly, neighborhood GDSs.

IPPB is perfectly positioned to serve the underbanked in far-flung geographies—where other formal financial institutions have a limited presence. One of its major strengths is its vast network of 160,000-plus Gramin Dak Sevaks (GDS), who offer doorstep banking (DSB) services.

The GDS are highly trusted members of the community. They generally live among the country’s underbanked population, especially in remote and rural areas. In addition to the GDSs, IPPB offers 140,000 banking access points, out of which more than 78% are in rural India. With its unprecedented reach and high customer trust in the postal network, IPPB touches households of more than 43.1 million customers.

IPPB addresses the concerns low- and moderate-income (LMI) segments face when accessing formal financial services. These segments include the elderly, women, and the differently-abled. IPPB offers government services, such as digital life certificates (DLCs), G2P payments, Aadhaar updates, and bill payments, improving customer convenience. IPPB has brought 43.1 million customers – 90% of who are from rural areas, into the fold of formal banking services. IPPB can potentially emerge as a one-stop solution across the country with its unique offering of facilitating self-service and an assisted mode of customer onboarding and product usage.

High customer impact

Below are three typical LMI personas that IPPB supports. Besides being low-income, these personas typically remain underserved by other formal financial institutions because they are either not lucrative enough or prove too challenging to serve.

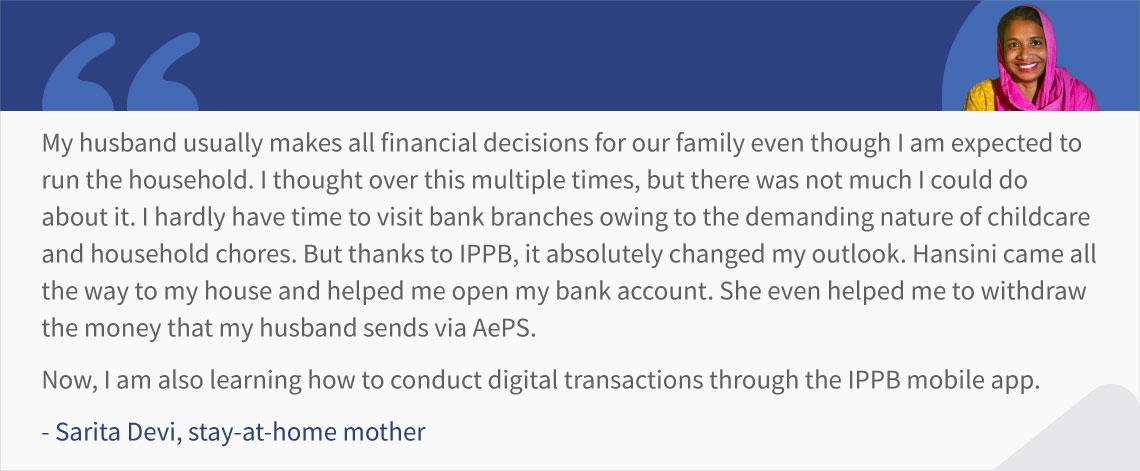

Sarita Devi, a 30 years old homemaker, stays with her in-laws in the Bhiwani district of Haryana. Her husband, Pankaj, works at a construction site in a nearby city and visits her every six months.

The couple recently had a baby girl, who keeps Sarita busy. At the beginning of every month, Pankaj sends her money to cover household expenses via India Post money order. Sarita does not have a bank account as she feels she does not need one. Moreover, the nearest bank branch is almost 15 km from her home, which makes it difficult to visit the branch.

One day, she met Hansini, a friend who works as a GDS in the Bhiwani area, who told Sarita about opening an account with IPPB. Sarita hesitated initially but decided to take the plunge since she trusts Hansini and is comfortable interacting with her. Shortly after, Sarita shared the requisite documents to open her first bank account.

Today, Sarita is confident and has learned to navigate the IPPB app to conduct transactions. She reaches out to Hansini whenever she struggles with payments.

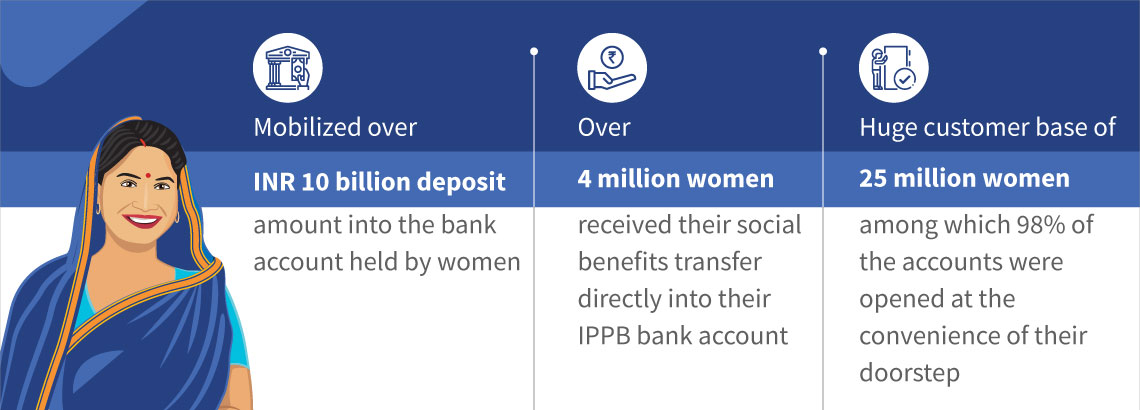

The situation is dismal for women in rural areas primarily due gendered social norms, low digital literacy, and lack of infrastructure. Further, limited exposure to technology exacerbates the situation and discourages rural women from trying digital transactions. IPPB seeks to bridge this gap through its network of 26,000 women GDSs from the local community, spread across Indian states, to offer DSB services. It makes banking convenient for millions of largely house-bound women like Sarita.

The government’s direct benefit transfer (DBT) program to female Jan Dhan account holders during the pandemic made it imperative for women to operate their accounts. While the speed and scale of the cash transfers made by the government were unprecedented, many of these women beneficiaries were first-time account users and feared being duped. IPPB supported women to withdraw their DBT payments through the Aadhaar-enabled Payments System (AePS) at the convenience of their doorstep during the COVID-19 pandemic, minimizing the risk of contracting the virus.

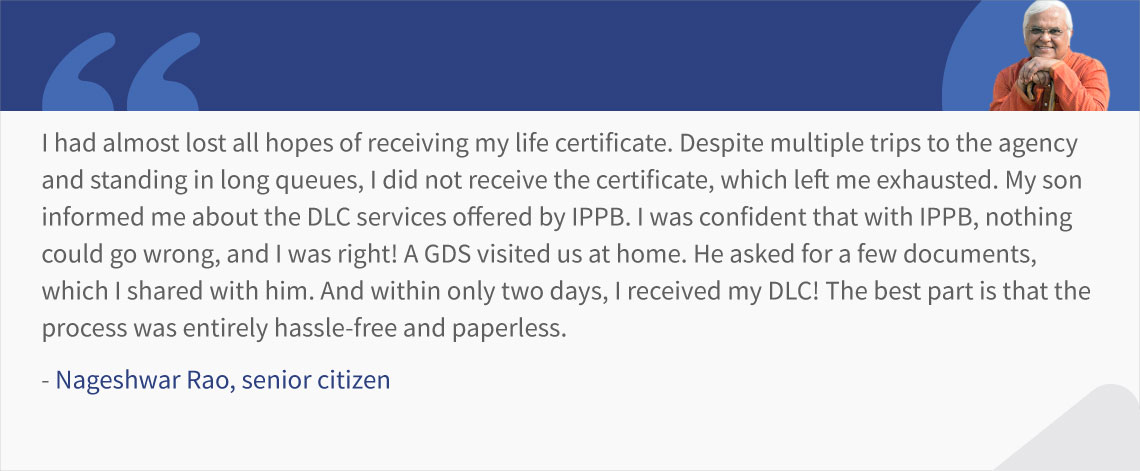

Nageshwar Rao is a 56-year-old retired teacher from Jalgaon, a city in the western Indian state of Maharashtra. A few years back, he met with an accident while returning from school that paralyzed his left leg. Nageshwar is doing better today, but needs help to walk. When Nageshwar retired, he visited his nearest pension disbursing agency for his DLC—a mandatory document for receiving a pension in India. However, he did not receive it despite several trips to the agency. His son Ranjan works at a private firm. He would accompany Nageshwar to the agency office and had to take frequent leaves, and thus lost income. One day, Ranjan visited the post office, where a GDS informed him about IPPB’s doorstep service. The next day, Ranjan requested the doorstep service—and Nageshwar received his DLC.

India is home to 6.5 million central government pensioners. Unfortunately, the challenges that Nageshwar faced are a norm not an exception. IPPB’s doorstep DLC services revolutionized the banking experience for senior citizens who remain underserved by traditional financial service providers. As of March 2021, IPPB has delivered more than 0.5 million DLCs through DSB services. Fraud and leakage from pension payments decreased by 47% after India transitioned from cash to Aadhaar-enabled payments. AePS transactions helped millions of senior citizens easily withdraw their pension and social benefit transfers during the pandemic.

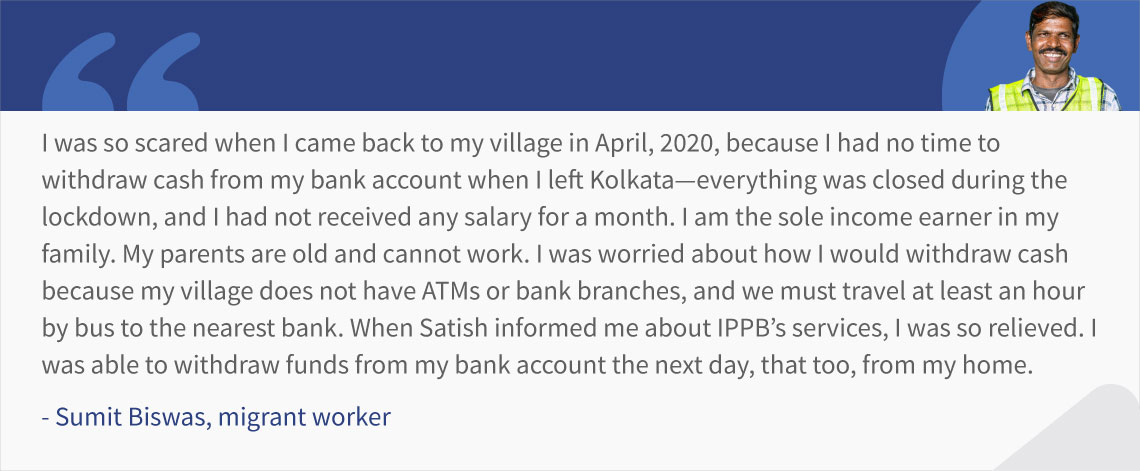

Sumit Biswas, 32, hails from the Midnapore district in the eastern Indian state of West Bengal. He migrated a hundred kilometers away to the capital city of Kolkata for a job where he worked at a construction site. He lost his job during the COVID-19 pandemic-induced lockdowns and traveled back to his village, much like the 10.6 million other migrant workers in India. Left without an income, Sumit decided to dip into his savings. However, access to the bank was a major issue as the nearest branch was more than one hour away.

The local GDS, Satish, informed Sumit about IPPB’s services. Although Sumit did not have an account with IPPB, he could withdraw money from his other bank account via AePS right at his doorstep. Therefore, Sumit could access his savings from his account to fund his day-to-day expenses during the pandemic.

IPPB’s AePS service is the country’s largest interoperable DSB service provider to both IPPB and non-IPPB customers across the states. Through AePS, IPPB facilitated 25.2 million transactions worth INR 53.62 billion (USD 675 million) during the initial phase of the lockdowns in India. As it grows, IPPB contributes tremendously toward providing last-mile banking services, boosting account opening, and improving account usage. IPPB has immense potential to empower underserved segments to use financial products, such as insurance, credit, and digital credit, through third-party collaborations.

The impact

IPPB has made significant strides in enabling inclusion for those at the margins and continues to transform their banking experience. Its customer-centric approach ensures that the products align with customers’ evolving needs, while its digital-first approach provides convenience for the customers. All these features have immense potential to digitally empower millions of customers like Sarita, Sumit, and Nageshwar and support their financial inclusion journey.

Basant Raj, 38, from Khodala village in Maharashtra, works as a daily wage worker in the nearby city and is the sole breadwinner for his family of five. Basant opened his bank account four years ago but prefers to save in cash at home. He considers formal banking channels a hassle since the nearest bank branch is far off, which requires him to travel a long distance, miss a day’s wage, and incur additional expenses to commute. Basant is among 35% of the account holders whose bank account lies dormant due to reasons, such as the large distances from the financial institution and lack of trust and need.

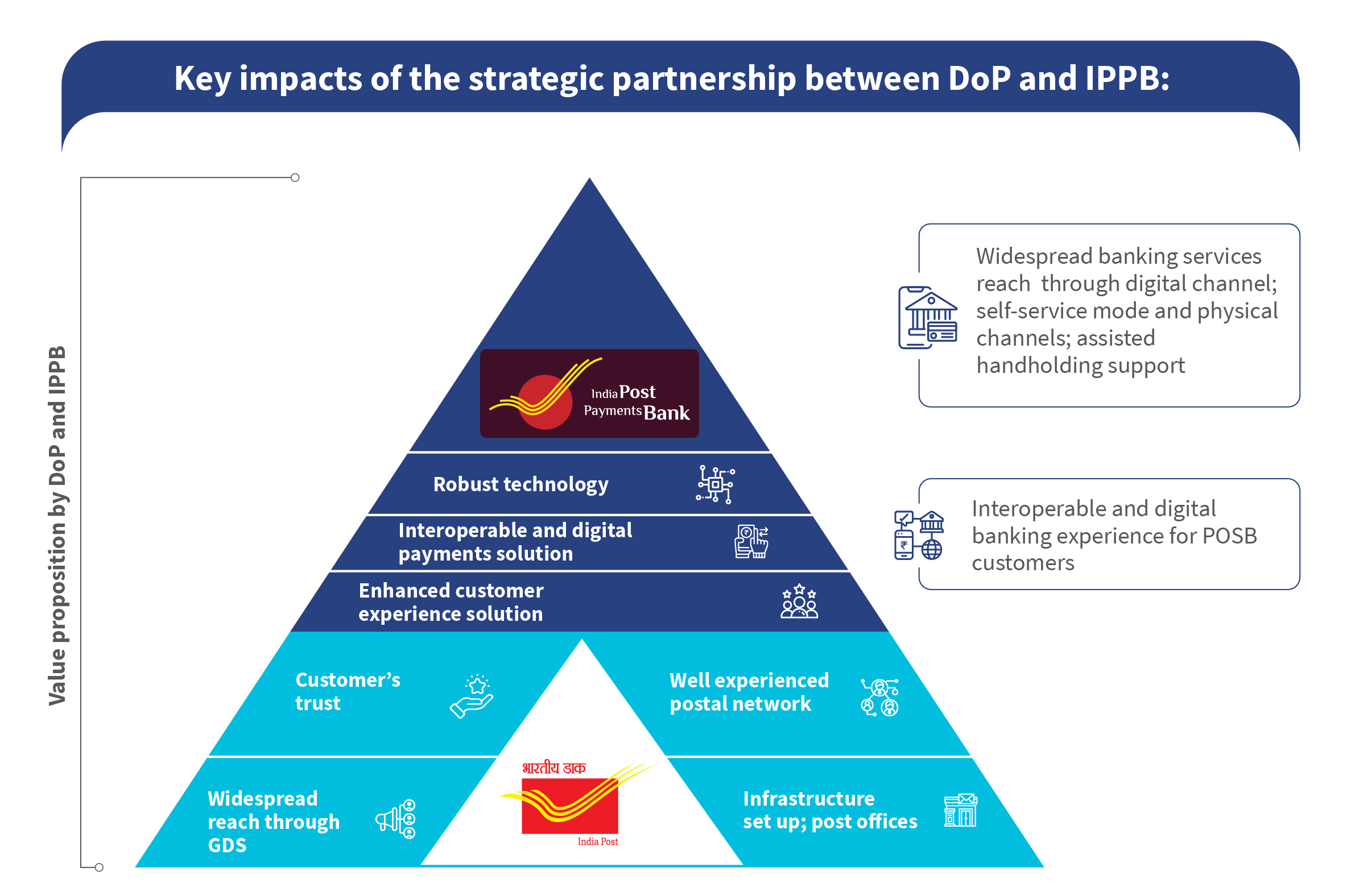

The collaboration between IPPB and the DoP created a win-win situation for both organizations through their shared vision of improving financial inclusion in India. Below is a glimpse of how this partnership has built a thriving ecosystem for each other.

Distribution and trust: The DoP was established in 1854 when letters delivered by the GDS were the only source of information that brought people closer to their loved ones. The deep-rooted trust in the postal network forms a crucial pillar of IPPB’s vast distribution network. IPPB uses DoP’s giant network of 189,000 GDS to deliver financial products and services at the convenience of the customers’ doorstep. Further, the trusted network of GDS offers handholding support to customers to bring low- and moderate-income (LMI) people into the fold of digital payments. Around 90% of IPPB’s 43.1 million customers live in rural areas.

The trust in the postal network has enabled IPPB to grow extensively. During FY 21 alone, IPPB’s customer base and their deposits grew by 83% and an impressive 169%, respectively—all at minimal additional customer acquisition cost—by using and incentivizing the existing network of GDS. The massive growth in customer acquisition is a testament to high customers trust in the partnership, which will grow over time.

Infrastructure and technology: IPPB uses post offices spread across the country to serve walk-in customers. This helps IPPB reduce capital expenditure on constructing physical touch points or branches. So far, IPPB offers banking services through more than 136,000 post offices. Out of these, around 90% are in rural areas, which has increased India’s entire rural banking network at least 2.5 times. IPPB’s banking services allow customers to digitally transact for the various small savings schemes of the Post Office Savings Bank (POSB).

Branding and product sales uptick: IPPB enjoys widespread support from the DoP’s postal network. It helped IPPB establish itself and reach 50 million customers within just three years. Out of the total 50 million account holders, around 48% are women. Thanks to the GDS network, about 98% of women opened accounts at their doorsteps. Trust in the DoP and IPPB’s technology-first approach convinced customers of different age groups to open their bank accounts with IPPB. While the DoP already had the confidence of millennials, IPPB’s doorstep banking (DSB) and handholding services encouraged other vulnerable segments, such as women and the elderly, to start using banking services. Further, the convenience that IPPB offers through its digital-first approach has motivated Gen Z to try the postal banking product suite. Overall, 41% of the IPPB account holders are 18-30 years old.

What does this collaboration mean for the customer?

This collaboration is ubiquitously associated with improved access to digital financial products for customers. The digital transformation drive initiated by the DoP and IPPB will improve process efficiency, enhance scalability, and introduce sustainability. The collaboration has improved access to basic banking products and services through doorstep services. This allowed more usage of accounts-such as cash-in, cash-out, and payments—the lack of which remains a common problem for low-value accounts.

The widespread access to affordable and convenient financial services coupled with handholding support motivates LMI customers to use formal financial channels. This in turn has immense potential to improve customers’ financial health and safeguard them against financial shocks.

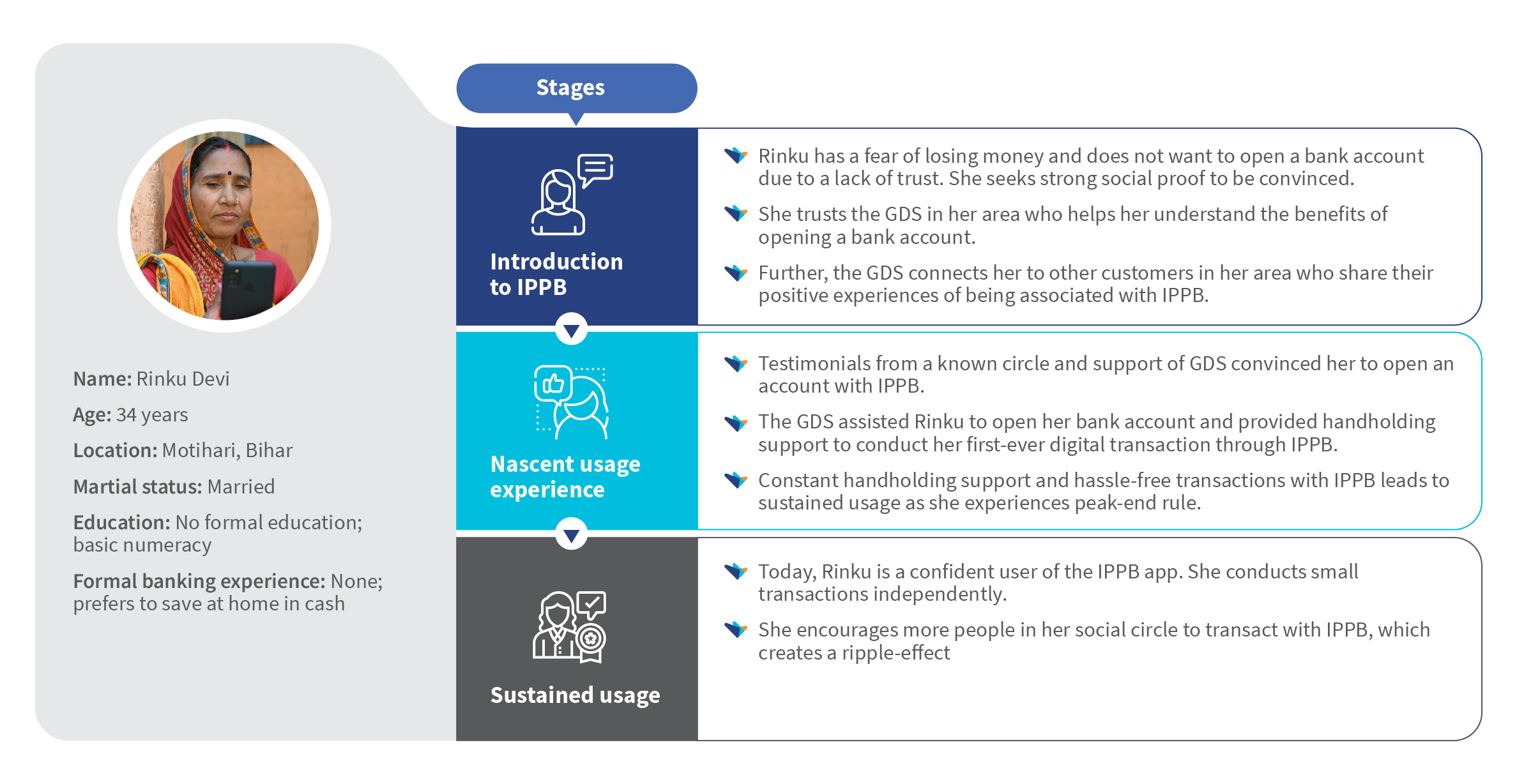

Due to limited digital and financial literacy, most rural customers feel intimidated by digital interfaces. They require strong social proof to use formal financial channels and generally exhibit status-quo bias. Despite these challenges, IPPB retains a robust, rural customer base, whom it has offered doorstep banking to help kick-start its formal financial journey. IPPB has influenced a behavioral shift among the rural segment—another feather in its cap.

Here is how the GDS put Rinku Devi—a stay-at-home mother from the Motihari village in Bihar—onto her path to financial inclusion:

The road ahead

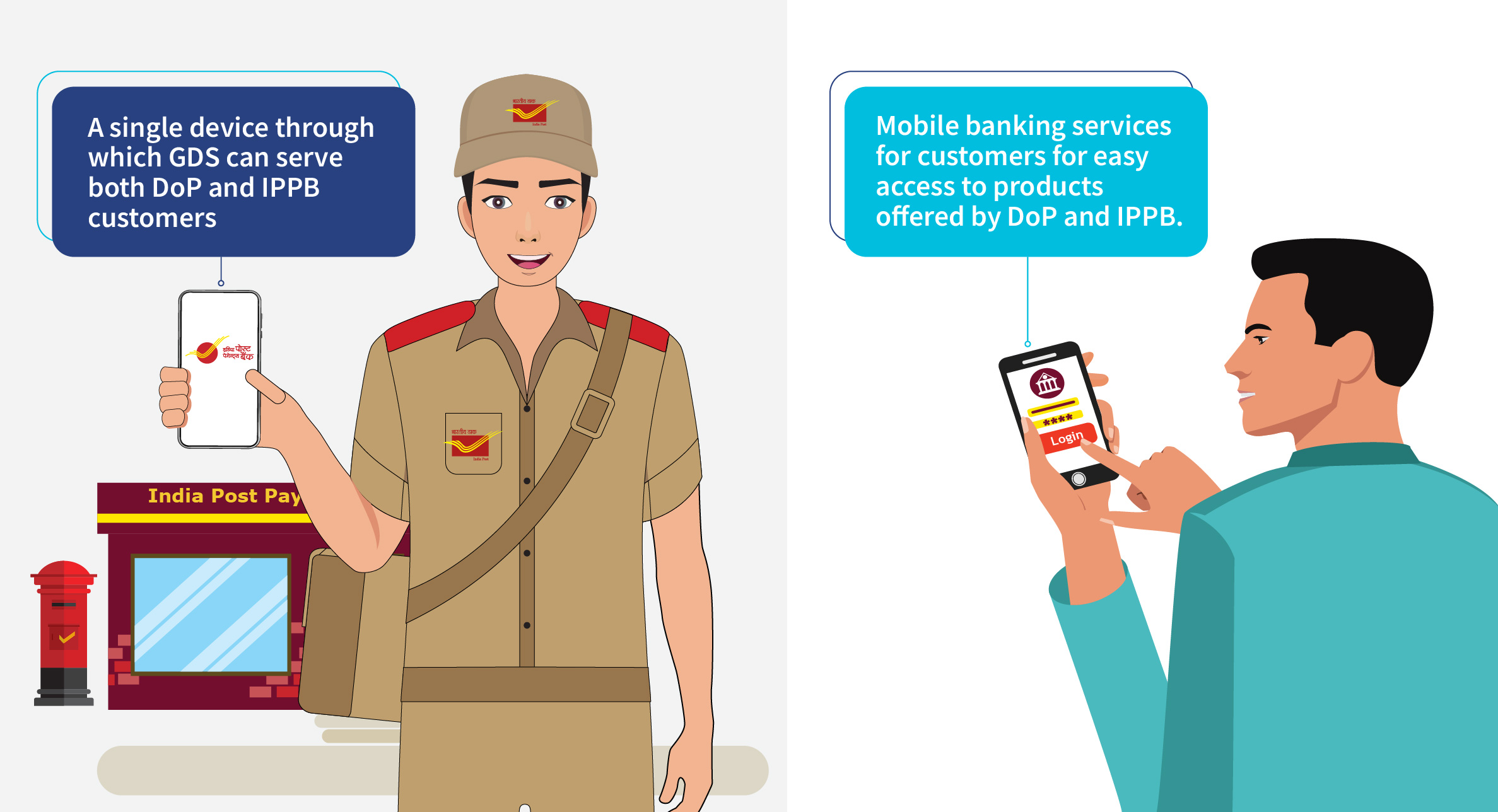

Despite the collaboration, IPPB and DoP must resolve any underlying challenges if the network is to function to its optimum capacity.

Device and workload management: The shift from being postal workers to financial inclusion enablers implied increased responsibilities for the GDS. While IPPB’s training helped in this transition, a GDS needs to manage different devices to serve customers using DoP and IPPB products, which is inconvenient. Providing a single device to the GDS to manage both IPPB and DoP operations is a possible step to streamline their workflow. Unifying IPPB and DoP at the technology and performance matrix level will further help streamline the operational and functional responsibilities of the GDS. The unison has immense potential to transform the GDS into a force to reckon with, pushing financial inclusion to the next level.

Skillset requirements: GDS is a heterogeneous group with varying levels of digital literacy. The varied skillset and tech-savviness required to manage different devices and solutions for DoP and IPPB often overwhelm them. This impacts their performance and impedes their ability to assist more customers. A combined induction and capacity-building program that intersperses DoP’s mail operations training with IPPB’s banking operations training can help gradually upskill the GDS. If mail operations and banking operations are on the same platform, the smooth user experience of using the app can reduce the cognitive load on the GDS. Furthermore, a unified performance evaluation system of the GDS would go a long way to keep them motivated. The basic tenets of the unified device include a customer-centric approach, technology-backed infrastructure, and a focus on the well-being of the postal network.

IPPB—the digital engine of inclusive growth

IPPB is on a path to revolutionizing the digital banking experience for customers through the unprecedented reach of the postal network. The innovative steps that IPPB has taken, such as DSB, distributing digital life certificates, and paperless transaction receipts, have paved the way for a digital transformation even in the country’s hinterlands. Between 2019 and 2021, IPPB processed 48 million doorstep transactions and mobilized social security payments worth USD 0.39 billion for rural customers. Extensive handholding support through the trusted GDS network paved the way for affordable and accessible financial services for millions of customers, especially women and senior citizens. These milestones signify that IPPB has immense potential to turn digital India’s dreams into reality.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.