India’s digital payments story is akin to none. Several factors have transformed India’s payments ecosystem. These include improvements in payments infrastructure, disruptions in information and communications technology, a responsive regulatory framework, a conducive policy environment, and a greater focus on customer-centricity. Besides, the increased adoption of smartphones, greater access to the internet, and people’s growing comfort with using technology and their improved financial capabilities have also aided this growth.

This report is an abridged version of the detailed whitepaper, “How digital payments drive financial inclusion in India.”It charts the evolution of digital payments in India and looks at the different barriers and triggers for providers and users in the ecosystem. It focuses on how various stakeholders can work together to empower users and drive the adoption of digital payments among the LMI segments.

In our previous blog, we focused on the Target segment-Technology-People-Process (2T2P) approach that postal banks can use to enhance their offerings to low and moderate-income customers. With the changing financial inclusion landscape, it becomes essential for postal banks to meet the needs of their customers. Our framework highlights major areas a postal bank can focus on to keep up with the changing financial services landscape.

In the following section, we focus on some successful practices that postal banks have followed across different countries under the 2T2P approach and the impact of these developments on customers, such as Ramesh, Ali, Dizola, and others worldwide.

1. Target segments: Postal banks that cater to the changing needs of the customers

Customer segmentation and profiling focusing on different use cases can be critical for postal banks as they serve a large set of customers through their network. Customized products for different customer segments based on their financial behavior will be vital to improving customer experience.

Some postal banks, including Al-Barid Bank in Morocco and Tunisian Post in Tunisia, have been leading the way and targeting a specific set of customers through their network:

Focus on low-and-moderate-income groups:

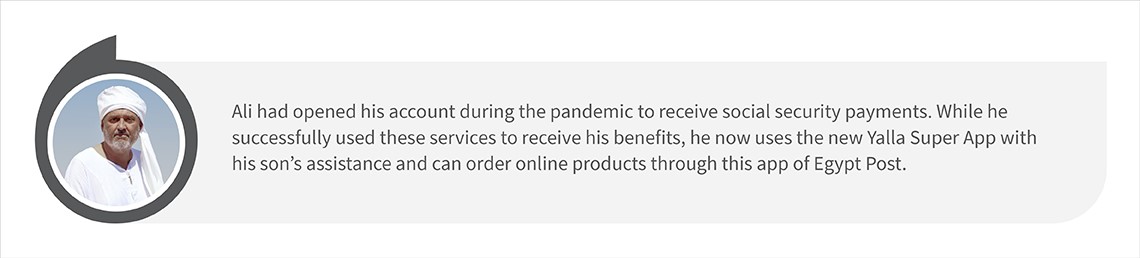

In some countries, post offices receive banking licenses to offer limited products and services. This allows them to compete with regular banks or supplement them for specific customer segments. In 2010, a subsidiary of Morocco’s post office received a limited banking license, and it floated Al-Barid Bank to serve low-income consumers. Since its inception, Al-Barid Bank has opened 400,000 to 500,000 bank accounts every year and improved access to banking for those in remote areas of the country. Similarly, Egypt Post has supported customers like Ali through their banking services.

Improving customer stickiness to the platform:

The Tunisian postal bank, La Poste Tunisienne’s mobile banking services for virtual accounts increased retention among young customers, who usually switch to other banks once they start earning. Once La Poste Tunisienne extended mobile payment services to virtual accounts and started offering additional benefits, it became popular among young customers. Adem, an engineer from Ariana, opened his account at La Poste Tunisienne in 2019 and uses the platform digitally to make mobile payments due to the ease of performing transactions.

Tunisian Post has also been focusing on advanced use cases and is exploring this through big data and blockchain to expand the reach of digital financial services. Recently, it launched a new payment infrastructure with the Swiss tech platform, Monetas. The new digital payment infrastructure enables e-Dinar users to make instant, secure peer-to-peer mobile transfers, pay online and offline merchants, pay their utility bills, send remittances, and manage official government identification documents. Tunisian Post now seeks new use cases to expand digital financial services to its customers.

These postal banks are exploring newer use cases and keeping stickiness at the forefront for their loyal customer base. With this strategic focus, they have to potential to expand digital financial services to the unserved and underserved.

2. Technology: Unique scalable solutions using emerging tech

Postal digital transformation is difficult to achieve by simply layering technology over legacy systems. It requires building a modular tech infrastructure and an easy-to-use interface that target segments whom we met in the first blog – like Ramesh, Ali, and Dizola finds intuitive and convenient. Several postal banks have been implementing innovative solutions at the front end to provide a better user experience and at the back end to build scalable infrastructure.

SmartCard solution introduced by NamPost Savings Bank in Namibia:

Namibia post offers banking services to its customers through its “SmartCard.” Whenever customers open their account with NamPost Savings Bank, the financial services arm of Namibia’s post, they get a smart card. The biometric card helps customers withdraw money in post offices and ATMs, transfer money to an account or another card, and pay in retail shops across countries via Point of Sale devices.

Partnership with mobile operator networks (MNOs) to improve technological capabilities:

Partnership to digitize traditional financial products:

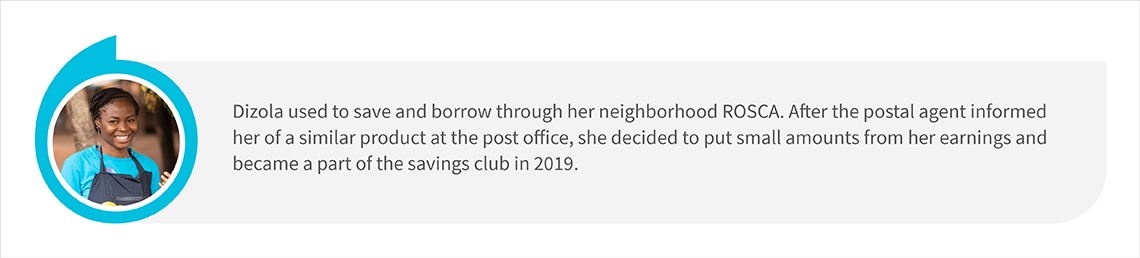

Benin Post partnered with the FinTech e-Savings club to digitize and formalize rotating savings and credit associations (ROSCAs). The postal agents collected monthly savings from customers at the convenience of their doorsteps. Further, they were also responsible for sending timely reminders to reduce the delinquency rate among customers. Once the amount collected is deposited in the post office, the customers receive a confirmation message.

The digital revolution has allowed these postal banks to use emerging technology, build innovative solutions, and provide different financial products through FinTech partners. The introduction of customized financial services through the network of postal banks can potentially disrupt and scale them—and extend their reach to the last mile.

3. Process: Building efficient processes and operational models to deliver relevant products to specific segments

Service providers can offer several services at low cost through digital and non-digital channels, thanks to the expanding internet and smartphone user base across the markets. Postal banks can build “phygital” models and processes, that combine technology with human assistance, to deliver efficiently to their target segments.

An agile approach to adopt innovations in the market and serve customers adequately:

Elta Hellenic Post, commonly known as ELTA, is Greece’s national postal service. Doorstep delivery of social security payments through bank checks was one of ELTA’s essential tasks, besides other postal services. However, when a law was introduced to outlaw the physical delivery of G2P payments during the COVID pandemic, ELTA was quick enough to respond to this change. ELTA introduced giro accounts to serve beneficiaries. Beneficiaries approach the postal delivery staff to open giro accounts to access their social security payments at home. This helped ELTA retain its customer base and adopt a robust system to deliver no-contact payments.

Co-branding approach and effective processes to deliver financial products:

In the UK, many private-sector banks have partnered with postal banks to offer co-branded basic financial products, such as customer savings accounts and current accounts for merchants. The partnership also enables banking agents to use post offices as a physical touchpoint to help customers conduct transactions, such as deposits and withdrawals. Several banks in high-income countries show similar trends to maintain their presence in rural areas. In Spain, Slovenia, and the Czech Republic, post office employees execute customer transactions on behalf of several private sector banks. In effect, these post offices act as agents for banks.

4. People: Capacity-building of the agent network and staff within the organization

Traditionally, the role of a postal agent is limited to mail delivery services, and they are not well acquainted with digital interfaces. The transition from being a mail carrier to financial inclusion enabler requires training. Further, postal banks also need strategic leadership at the top to drive innovation in service and processes to maintain a sustainable business model over time.

Training and capacity building through creative tutorials:

India Post Payments Bank introduced creative video modules for its network of 189,000 agents. These modules are constantly updated and available in regional languages across India for postal bank agents to understand the content without any challenges. This includes engaging comic strips that have generated higher awareness among agents of IPPB to serve customers effectively.

Leadership from both banking and startup experience can help drive innovation and growth:

Some post offices focus on building a solid leadership team to drive innovation. The leadership of Anas Alami, former Director General of Poste Maroc, laid the foundation of financial inclusion for the Morocco Postal Bank. The in-house experts’ knowledge base helped the bank minimize expenditure on hiring external consultants. Further, the experience of the senior management team comprising different age groups and diverse backgrounds helped Morocco Postal Bank to make well-informed strategic decisions.

The future is now, and postal banks can use their competitive advantage to make the most of the opportunity

Several postal banks, such as those in Japan, India, and Morocco, have adapted to their country’s cultural nuances, customer needs, and technological developments. Most importantly, they use the postal networks’ widespread presence to provide financial services, specifically in pockets that lack traditional banking outlets for customers, such as Dizola and Ramesh.

Postal banking played a crucial role in increasing financial inclusion globally and was a game changer during COVID-19 for beneficiaries like Ali receiving social security payments. They enabled multiple use cases across P2P and G2P payments during those difficult times. Thus, if postal banks can build their model around local requirements, they are here to stay, sustain, and thrive.

India has been at the forefront of transforming the global digital payment landscape. The past five years have seen a massive transformation. While UPI has hit record high numbers, AePS has transformed how beneficiaries access subsidies. Merchants now conduct digital B2B payments, while FinTechs continue to evolve unique solutions to disrupt the space.

This whitepaper has been developed in partnership with the National Payments Corporation of India to showcase how digital payments continue to drive financial inclusion in India. The whitepaper shares insights on the evolution of digital payments in India and looks at the different barriers and triggers in the current state of play for providers and users in the ecosystem. It focuses on how various stakeholders can work together to empower users and drive the adoption of digital payments among the LMI segments.

MSC conducted a deep-dive analysis of the digital credit users in India, Indonesia, and Kenya to assess the impact of digital credit on their financial health. The analysis presents the insights from the assessment and recommends actionable interventions at the level of providers, regulators, and policymakers to enhance the financial health of digital credit users.

This report was launched at the Global Fintech Fest in Mumbai, India on 21st September, 2022.

Ramesh, a daily-wage worker from Bihar, India, can send money easily to his family with the help of postal workers. Ali, a retired military officer from Aswan, Egypt, no longer has to queue outside any government offices to receive his social security payments. He can withdraw money easily from any Egypt Post ATM or POS-enabled post office with zero charges. Dizola, a micro-entrepreneur from Allada village, Benin, can conduct digital transactions through his postal account, even on his feature phone.

What common thread binds the lives of these people? The answer is the role the respective postal networks in their countries play to spearhead safe, affordable, and convenient customer transactions.

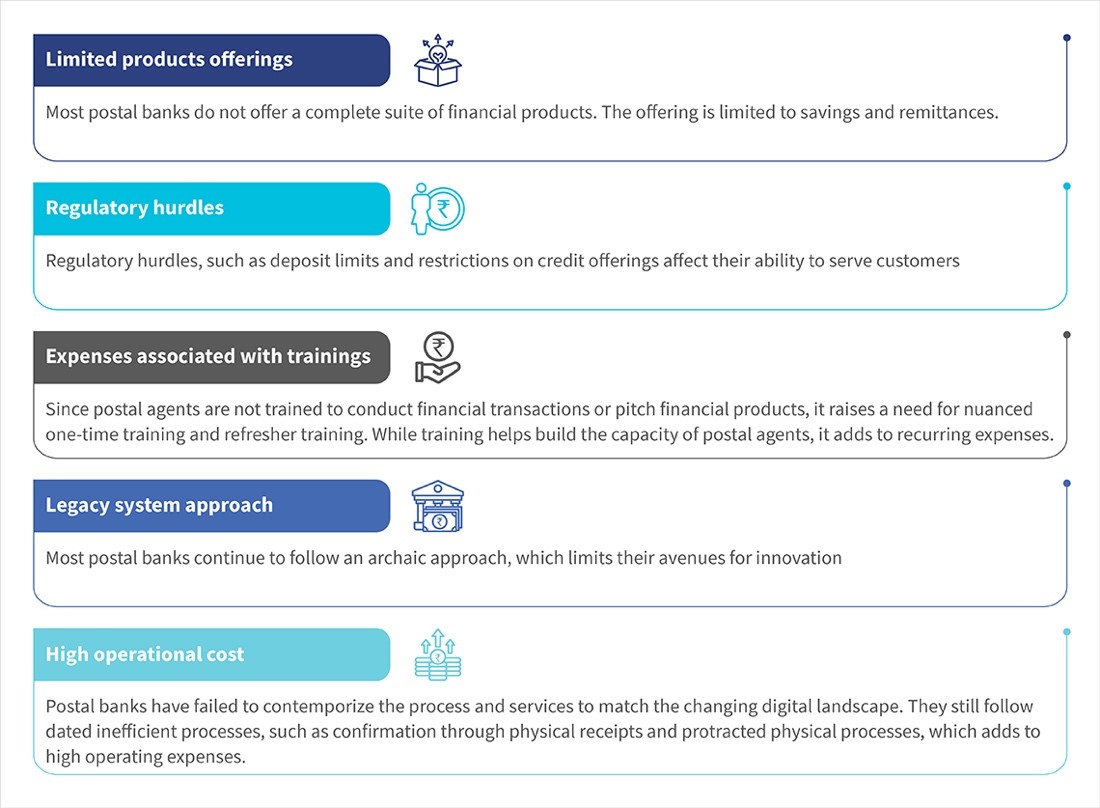

Predominant supply-side challenges faced by postal banks across the globe

Demand-side constraints including limited literacy, lack of formal documents, and lack of awareness about the formal financial channels, further exacerbate the situation. As a result, financial institutions, including postal banks, struggle to cater to LMI customers. Postal banks must now transform themselves to cater to their existing and potential customer segments against the backdrop of the changing financial service ecosystem and evolving needs of customers like Ramesh, Dizola, and Ali. The graphic below spells out some demand-side challenges:

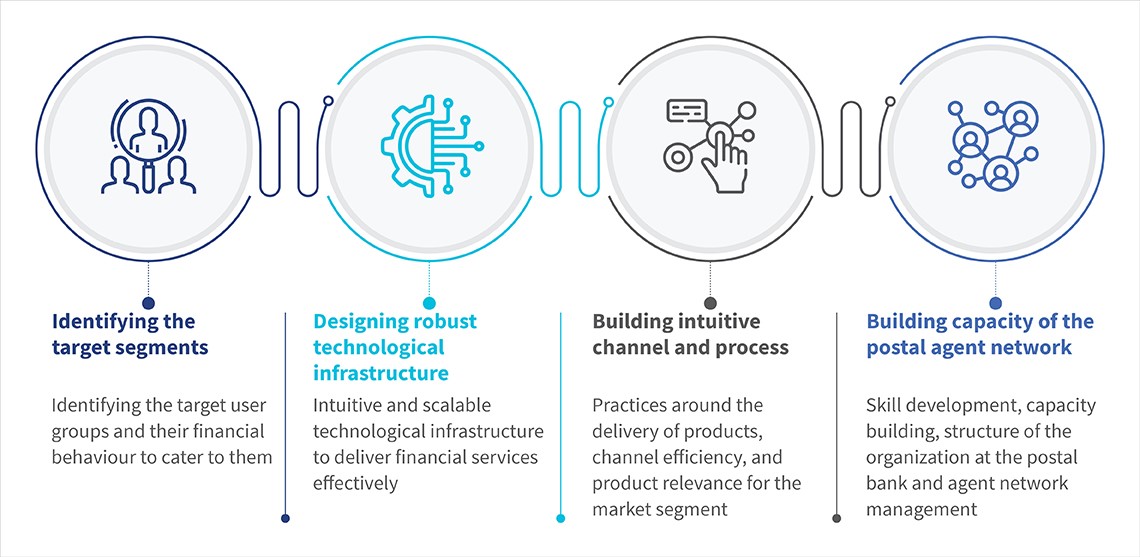

We have used the 2T2P: Target segment-Technology-People-Process approach to assess and suggest how postal banks can optimize their business operations, serve the target customer segments, and transform digitally to survive and thrive in the diverse ecosystem of financial services.

1. Target segments: Identify the right user base for the services

The customer comes first. Over the years, we have seen a major shift in customer behavior and expectations. This change has compelled financial institutions, including postal banks, to redefine their priorities to meet evolving customer needs. The postal banks must first understand the target segments to provide them value.

Profile customers: Capturing the customer lifecycle with data on financial behavior can help postal banks offer customized products, predict the need for different products, use their channels efficiently, and unlock new opportunities in the space.

Focus on advanced use cases: Emerging technologies can potentially offer advanced use cases for digital financial services. The emergence of big data has enabled different approaches to credit scoring, allowed providers to cross-sell and upsell products and services, and enabled the addition of new use cases. Postal banks are well-suited to use their existing database to provide financial services to underserved populations.

2. Technology: Achieving scale through intuitive tech infrastructure

Technological progress is transforming the financial services ecosystem globally, which can help postal banks build an efficient business model over time. Postal banks worldwide struggle with legacy systems and the inability to innovate fast. Postal digital transformation cannot take place by simply layering technology over legacy systems. It requires the creation of modular tech infrastructure and an easy-to-use interface that target segments will find intuitive and convenient. Once such upgrades are implemented, postal banks can scale and use data to advance their customers’ digital finance journey.

Build an intuitive frontend interface for customers: A user-centric platform is essential to facilitate usage and enhance customer experience. Since LMI customer segments have limited digital literacy, postal banks must build intuitive and easy-to-use solutions in regional languages with voice-assisted modes. These users have not experienced financial services on smartphones. The frontend customer interface must therefore be intuitive, with ample handholding to boost customer confidence and trust in digital transactions.

Develop a scalable infrastructure at the backend: Postal banks must use technology to implement new services and diversify into new business models to scale their services. Their core architecture must include digital innovation, e-commerce, data collection, API development, and digital identity. This inclusion will enable postal banks to propose new services, increase efficiency using technology, drive innovation and agility, and improve resilience and scalability.

Ecosystem enablement—API-driven open architecture approach: Postal banks can build strategic partnerships with emerging FinTechs and other institutions to provide products on demand through open APIs. This will help customers access multiple solutions through postal banks. It becomes a win-win solution for FinTechs and postal banks, which they can use to build competitive advantages and drive financial inclusion.

3. Process: Building efficient processes and operational models to deliver relevant products to specific segments

Customers prefer a bank that understands their needs, offers suitable products, maintains transparency, offers simple and streamlined processes, and is approachable. With an expanding internet and smartphone user base across markets, postal banks can offer many services at low costs efficiently through digital and non-digital channels. However, postal banks need to combine an all-digital experience with a human touch to cater to people at the bottom of the pyramid.

Build a “phygital” operational model and processes to deliver relevant products and services to the last mile: Most postal banks have a significant physical presence that they can use to serve customers better. Depending on the existing bank structure, postal banks can gradually move to a digital-led operational model where their postal agents serve customers using digital devices. Many postal banks can take a phase-wise approach to roll out the services and move gradually from an assisted model to a self-service mode. This way, they can still keep features like doorstep delivery that add to the convenience of the customer segment, and take digital financial services to vulnerable segments, such as pensioners and rural women.

Use the trust in the post’s brand and network to add new financial and non-financial services: Most customers trust their postal banks. Postal banks can use this implicit trust to add new value-added services based on the lifestyle needs of customers, who otherwise largely remain unserved and underserved by incumbents in the ecosystem. They also offer a really important opportunity for G2P (government-to-people) payments, as postal banks typically have significant outreach into the vulnerable and remote communities targeted by G2P programs.

4. People: Developing capacities of the agent network and staff within the organization

Postal banks reach and serve customers at scale through their vast distribution network. Evolving customer expectations and technology make it essential for postal banks to recognize the emerging needs of their customers and build a skilled workforce that caters to their specific target segments. A major struggle for postal banks is achieving a sustainable business model while developing their network capacity.

Build capacities and skill sets of postal agents to deliver digital financial services: Traditionally, the role of a postal agent is limited to mail delivery services, and they are not accustomed to using digital devices for operations. Transitioning from a mail carrier to a financial inclusion enabler requires nuanced training. If postal agents wish to develop their skills, they must receive training at regular intervals with hands-on experience. They can then serve customers better.

Acquire strategic leadership and enhance the existing team’s skills with a focus on innovation with better product design and delivery: Postal banks need leadership teams that understand tech-based solutions of FinTechs and know about the operations of traditional banks. A combination of the two will help them select the right partners to drive innovation in postal banking and expand their business. They can then sustain their digital finance ambitions with a clear vision, strategy, and roadmap in-house.

Conclusion:

Research suggests that households and businesses with access to formal financial services can respond better to financial shocks. Postal banks, alongside other financial institutions, continue to make efforts to reach the 24% of people worldwide who still lack a bank account. The assisted banking approach, and technology-based solutions offered by postal banks, coupled with their vast network, show a high potential to serve millions of underserved customers like Ramesh, Ali, and Dizola.

The following blog in this series captures lessons from postal banks spread across our 2T2P model, which highlights how some postal banks can serve the excluded.

IPPB’s customer base grew from 23.6 million to 43.1 million in 2020/21.

“Dakiya daak laya, dakiya bank laaya” (“The postal worker brings us letters, they also bring us the bank”), sings Anupama, daughter of IPPB end-user Anuj, who sits chatting with a customer who wants to open a bank account. In a few moments, Anuj creates a new bank account—adding to one among the 30-odd accounts the postal bank opens each minute across India’s borders.

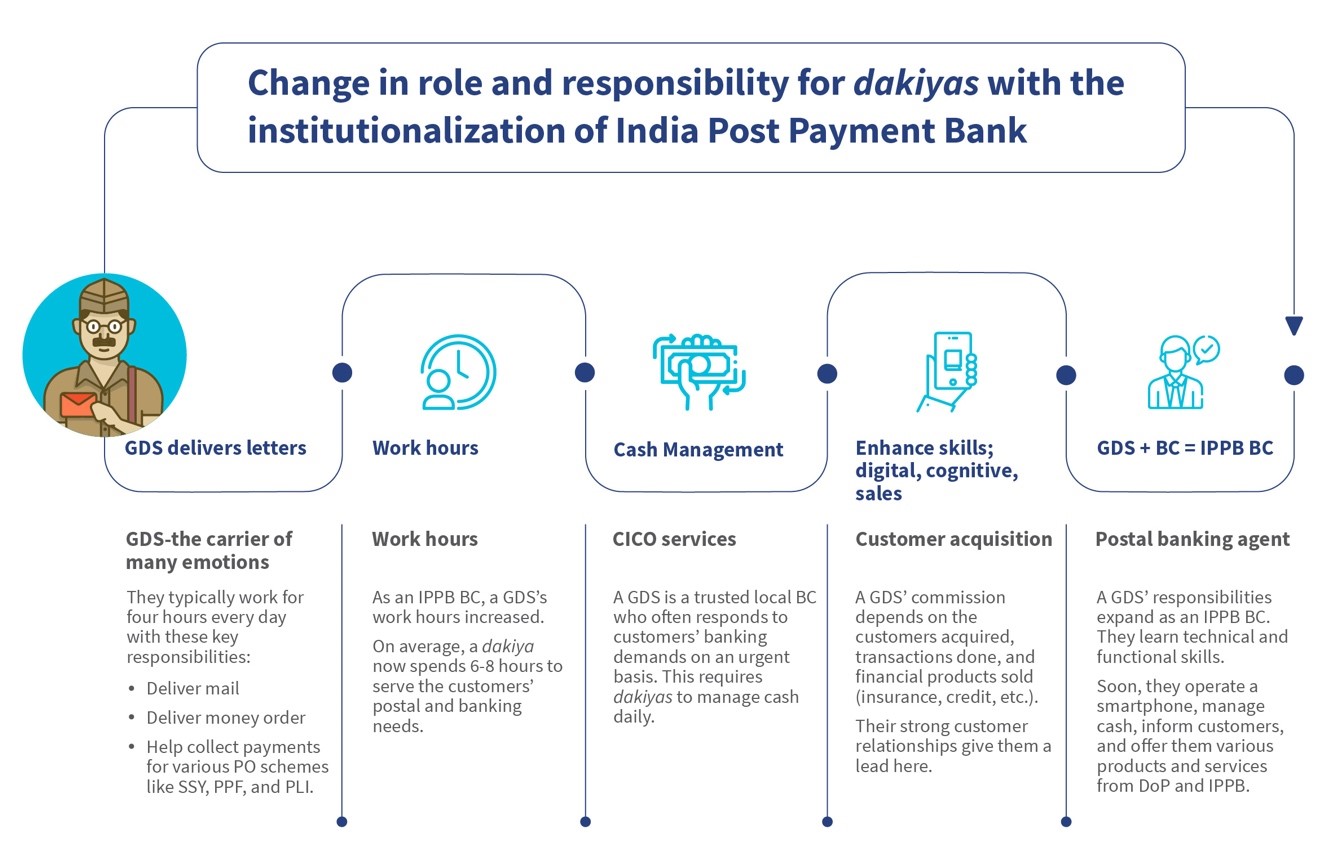

Forty-year-old Anuj lives in Kakori village in the Indian state of Uttar Pradesh, where he works for the Department of Posts (DoP) as a Grameen Dak Sevak (GDS) or Dakiya—a term of endearment for postal workers across large parts of the country. Anuj recently took up the responsibilities of a IPPB banking correspondent (IPPB BC), to his family’s delight. As aBC for IPPB, Anuj joins the ranks of thousands of GDS who contribute to IPPB’s rapid expansion at the last mile, fortifying the digital revolution brewing in India’s hinterlands.

Anuj joined the DoP after completing his senior secondary education. His compassionate nature soon helped him build a strong connection with the villagers. Besides delivering mail, at their request, Anuj often reads letters to older adults who await messages from their children who live in distant cities.

He also played another important role. All GDSs also help people open savings accounts with the post office, invest in long-term savings products, such as Sukanya Samriddhi Yojana (SSY) or Public Provident Fund (PPF), and thus introduce them to formal banking services.

Anuj often thought about how to reduce the inconvenience of Direct Benefit Transfer (DBT) beneficiaries when they had to travel long distances to withdraw cash. He believed assisted financial transactions at the customers’ doorstep or near it could help reduce the financial vulnerability of the elderly and the poor in his village. Anuj saw his dream come true when the India Post Payments Bank (IPPB) was created in 2018. IPPB offered him, along with other 189,000 GDSs across the country, a chance to join the Indian digital revolution by becoming IPPB banking correspondent.

Grameen dak sevaks hold the baton of inclusive banking

According to its FY 20-21 annual report, IPPB’s customer base grew by 83% that year, from 23.6 million to 43.1 million. To put this in perspective, IPPB opened an account almost every two seconds.

With the exponential growth of banking services and continued growing demand, GDSs have become critical to the delivery of inclusive banking in rural India. A GDS has multiple functions and has to learn new functional and technical skills to provide safe and secure digital banking services. This is easier said than done.

A Grameen DakSevak’s life as IPPB banking correspondent

When IPPB was institutionalized, many GDS sensed an opportunity and took up the role of banking correspondent to earn an extra income. Meanwhile, others found it challenging. While their job profile expanded, their responsibilities increased as well.

If a GDS chooses to work as an IPPB BC, they must gain technical knowledge of banking products, build cognitive skills to understand technology interfaces and devices, and develop business acumen to drive sales. Further, they attend classroom-based training by IPPB to qualify as banking correspondents. GDSs also attend external training mandated by the UIDAI to become eligible to offer Aadhaar-based, high-revenue products, such as the Child Enrolment Lite Client (CELC).

The enhanced role of the GDSs as IPPB BCs benefits them in multiple ways, including social recognition and additional income. For women, female banking agents further provide a safe space for banking. GDSs’ relationships with people in their neighborhood create a trusted path to onboard new customers onto digital banking. The graphic below highlights how a GDS can benefit from the role as an IPPB BC.

Different personas of GDS and their distinct needs

Several factors determine how easily a GDS can adapt to the postal agent’s role. These factors may be intrinsic, such as social recognition and empathy, or extrinsic, such as technical skills and support from the DoP.

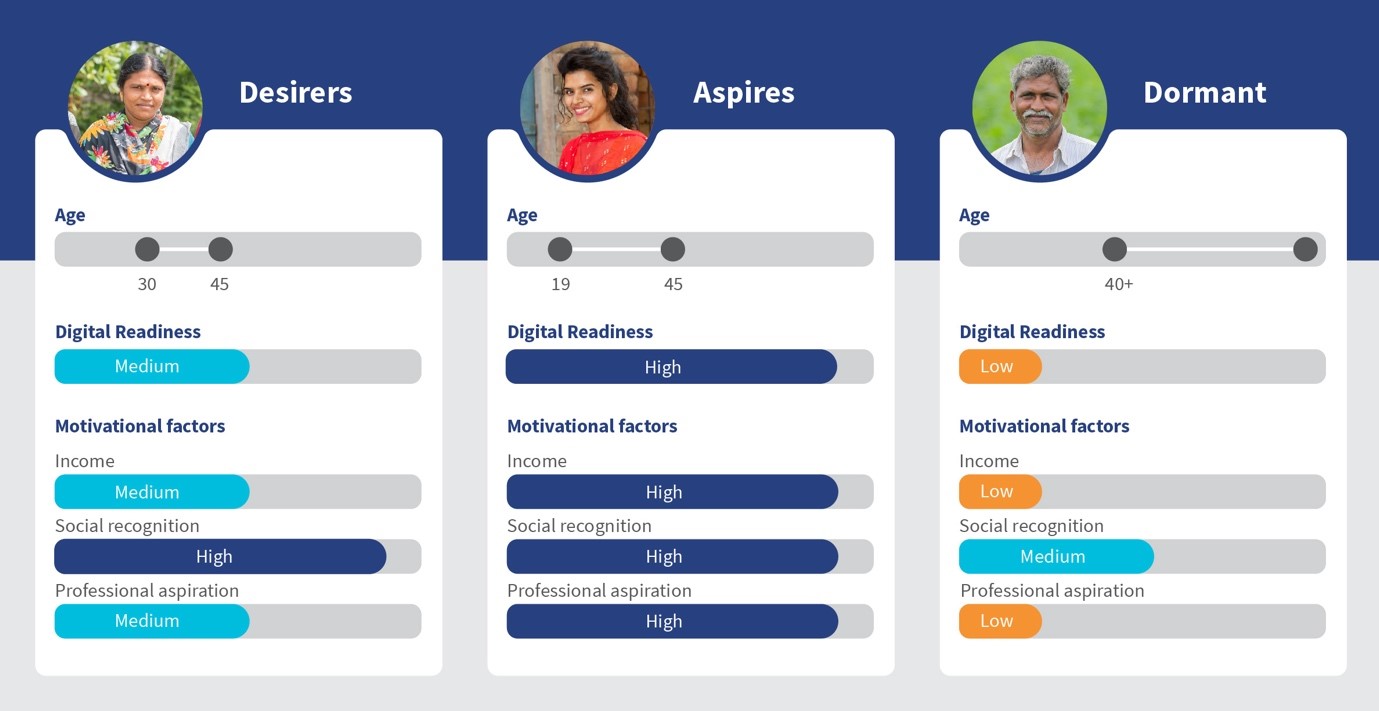

We explore three dakiya personas—desirers, aspirers, and dormants, to understand how this expansion of their role into an IPPB banking correspondent has affected them and their feelings about their role as BCs.

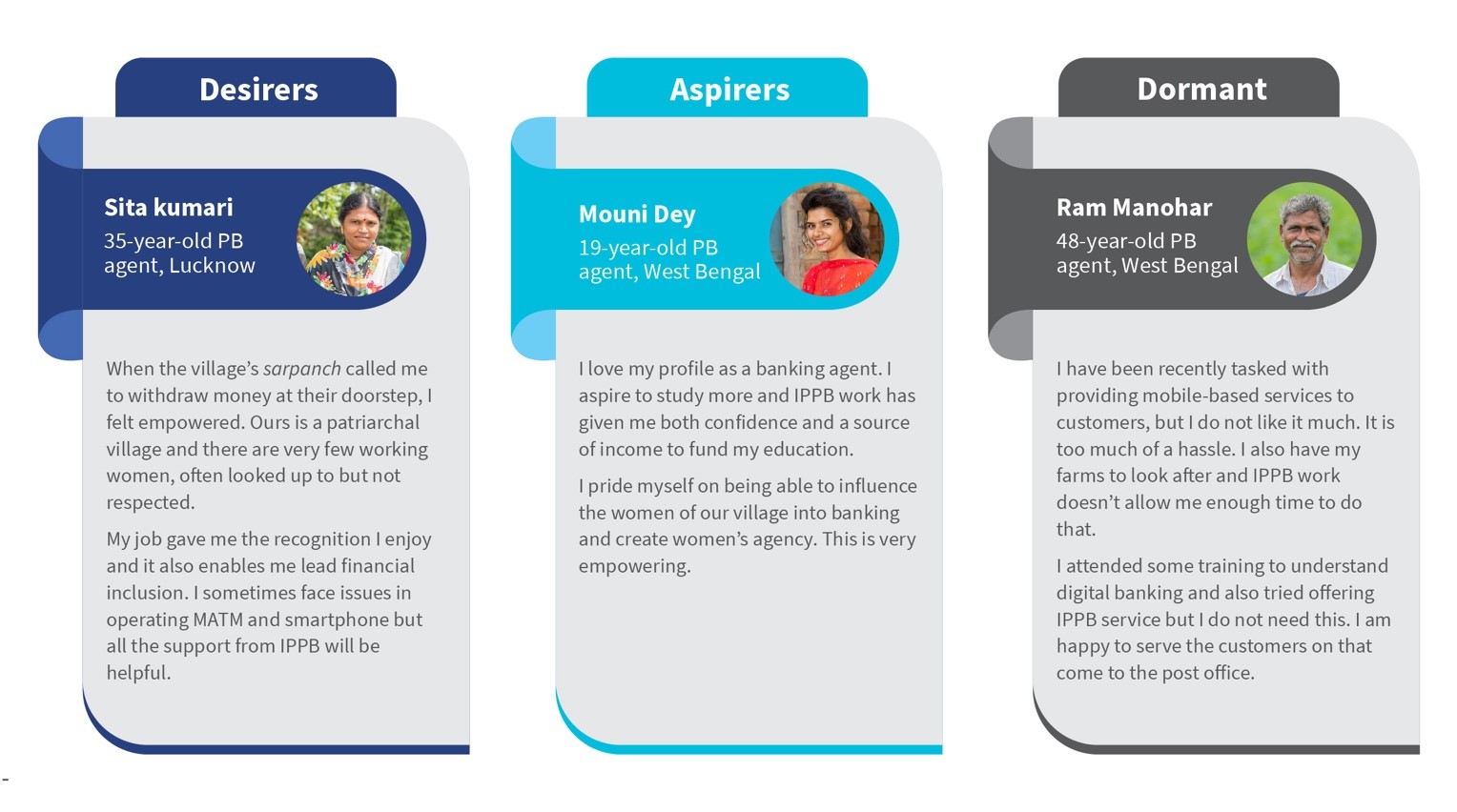

Desirers feel the IPPB banking correspondent opportunity empowers them: Desirers form a long-term relationship with IPPB. They are typically 30-45-year-old men and women from low- and middle-income (LMI) households. They have limited technical abilities and cognitive skills. Social recognition and enhanced income motivate them to work as agents. They struggle to operate micro-ATM devices, retain financial product information, or manage liquidity.

Yet the desirers’ spirit to work as change agents allows them to succeed. A true inspiration, these IPPB BCs have adapted to their enhanced role from postal deliveries to leading financial inclusion gracefully. IPPB and the DoP have launched successful initiatives to support the GDS with their enhanced role and responsibility:

The DoP and IPPB launcheddak karmayogi, an e-learning platform for GDSs to enhance their product knowledge and hence their commission income through higher sales. This will also enhance IPPB’s revenue—a win-win situation for all.

With support from MSC, IPPB launched bite-sized refresher training modules delivered digitally to the GDS. These modules act as ready reckoners for them.

Aspirers see the IPPB banking correspondent opportunity as a catalyst to their professional aspirations: Typically, Aspirers are highly motivated individuals like Anuj, who work as banking correspondents. They are extroverted younger people who like helping others. Moreover, they draw motivation from their ability to offer banking services to customers in their region. Many young GDSs also became postal bank agents to enhance their financial knowledge and supplement their skill set to become eligible for higher-level jobs. Further, high-incentive products, such as CELC, insurance, and bill payments motivate them to perform better and increase their income.

IPPB needs a mix of aspirers and desirers to build a strong foundation of on-field BCs and make the payments bank profitable.

Dormant are influenced by status-quo bias and need strong social proofing to adapt to the role of IPPB banking correspondent: The dormant is often a GDS who does not depend much on the role as a BC for their livelihood. They are typically 40+ year adults from relatively higher income backgrounds. Dormant has low motivation to work as banking correspondents and do not actively support digital banking services. They do, however, have great relationships in the village, and are influencers to many in their neighborhood. Initiatives that build social proof, such as recognition ceremonies, can motivate skeptics to spread banking information among their groups.

Looking ahead

The Indian postal system expects a lot from its GDSs, and many GDSs often struggle to offer financial services. Yet they have risen to the challenges and are now eager to help underserved customers in India’s towns and villages – and fulfill their aspirations by doing so. We need to enable and empower them to reach millions more who seek financial services in an environment they trust and consider safe.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.