MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

In this podcast, Mandira Sharma and Jeanne Ng’ang’a from MSC discuss trends in Kenya's electric motorcycles (e-mobility) sector. They cover challenges hindering e-mobility adoption, the crucial role of local manufacturing, and available financing options for individuals and businesses transitioning to e-mobility.

“I wanted to buy two sewing machines for my tailoring business and reached out to my nearest bank branch for a loan. The bank officials gave me a list of documents I must submit to initiate the loan process. However, I did not understand the listed documents and where to obtain them. I tried to contact bank officials but did not receive adequate support. I am unsure what to do next,” sighs Pragna, a 32-year-old woman entrepreneur from Hyderabad, India who runs a tailoring business.

Fig 1: Pragna’s desire versus the current ordeal

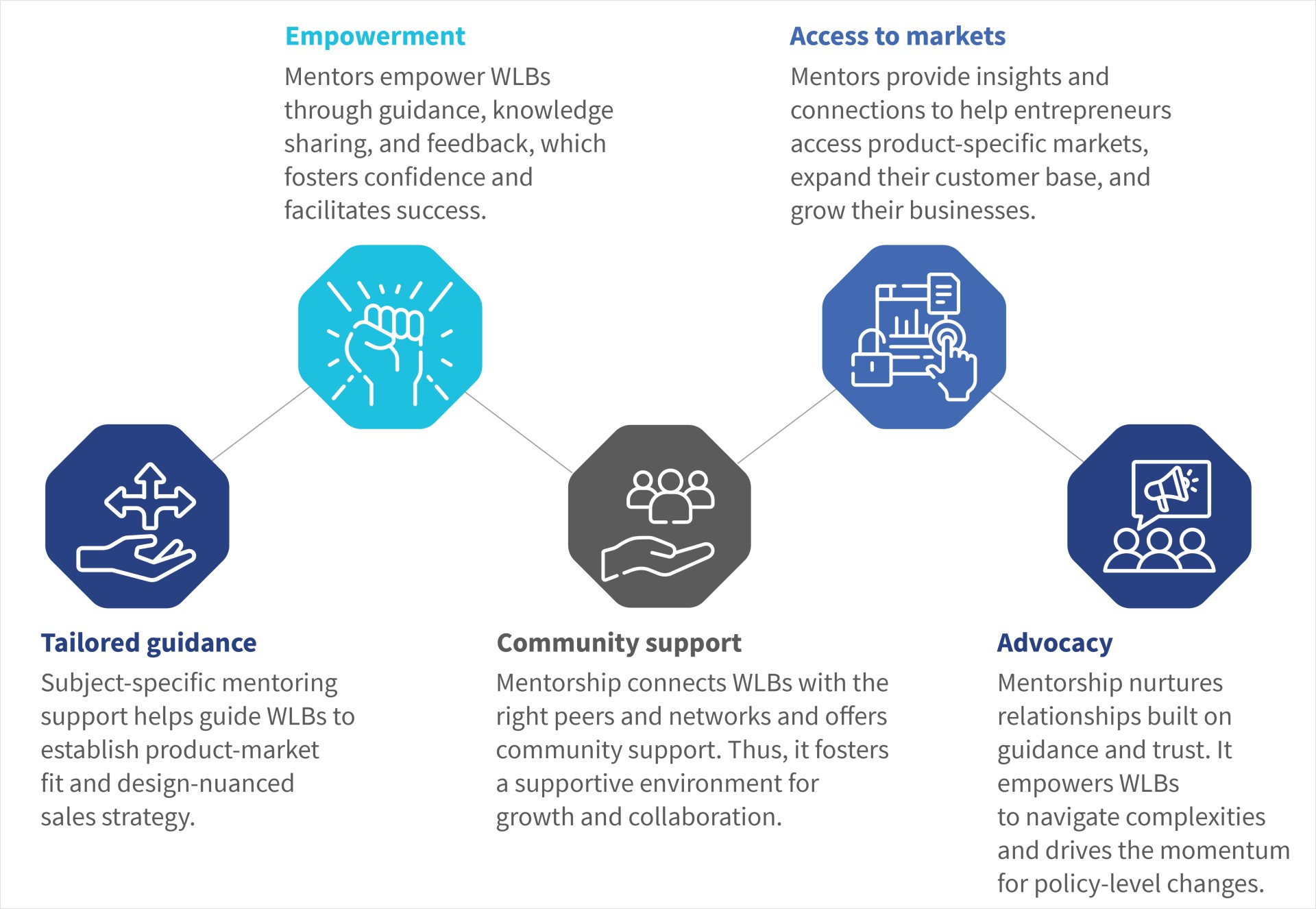

Pragna’s story is not an isolated case. It highlights the importance of mentorship support for the 8 million women-led businesses (WLBs) in India, which can help them overcome such challenges. Mentorship support implies access to professional industry networks, hyperlocal peers, and experienced mentors for handholding and guidance. MSC’s recent study reveals that mentorship support is crucial for WLBs’ growth. A study by the Reserve Bank Innovation Hub suggests that WLBs that receive mentorship support show a higher level of business acumen and willingness to seek external funding.

(Source: Qualitative interviews with 150 WLBs in India and MSC’s analysis on the importance of mentorship support for WLBs)

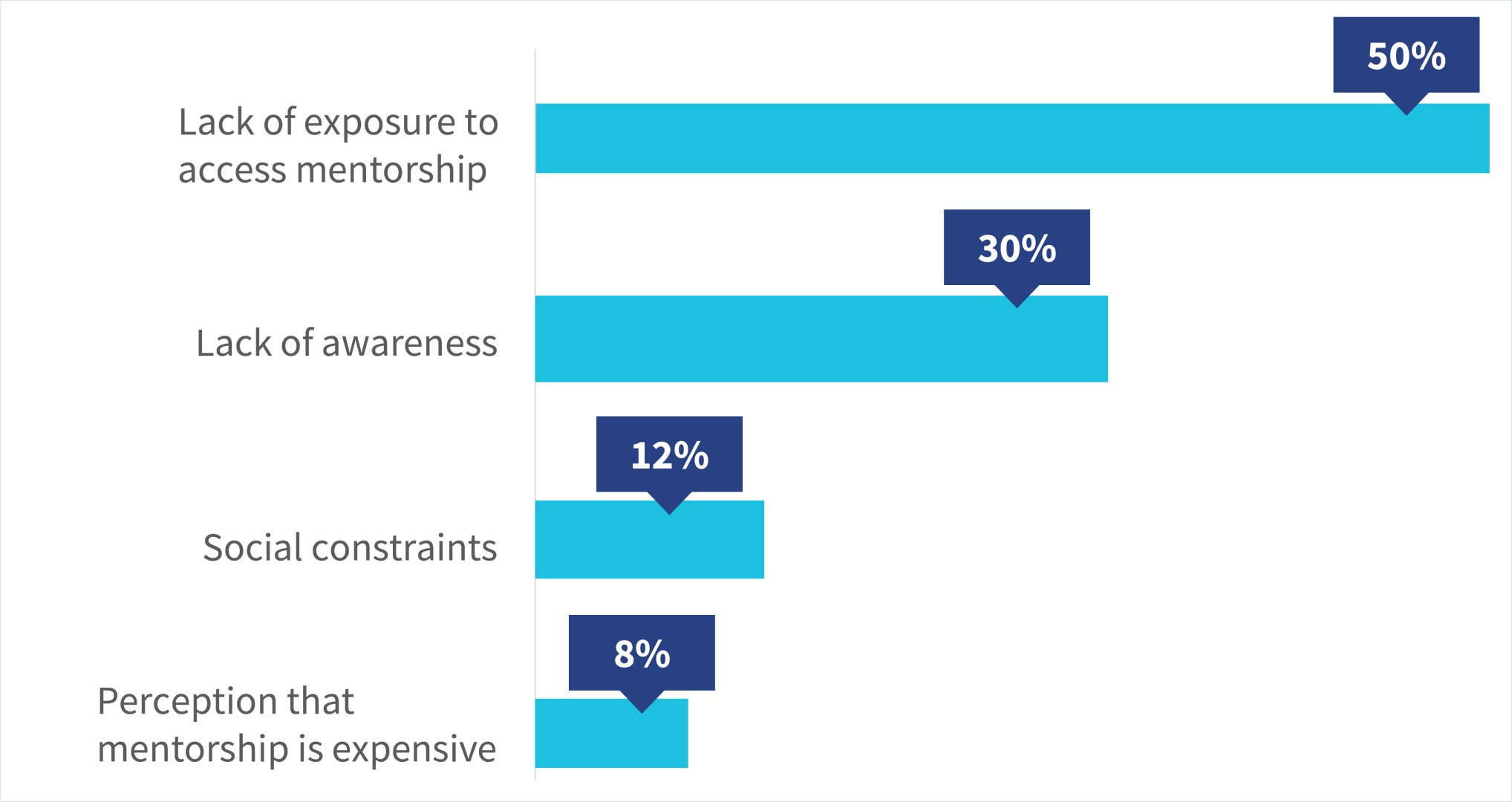

Further, a recent study by MSC and the Women Entrepreneurship Platform (WEP) found that a mere ~25% of surveyed women entrepreneurs have access to entrepreneurial mentorship and 64% are unaware of any mentorship programs for entrepreneurs. The concept of mentorship support for business growth remains nascent for women entrepreneurs, especially for those from Tier III and smaller geographies.

Role of specialized incubators to improve access to mentorship support

Overall, India has approximately 763 incubators and accelerators. However, most of them cater to the startup segment. Few incubation centers offer nuanced support to WLBs. In this blog, we delve into the role of one such incubator, WE Hub, which spearheads WLBs’ growth in India through mentorship support.

WE Hub is India’s first state-led incubation center in Telangana state that supports WLBs. The one-stop entity provides WLBs with entrepreneurship support across their business lifecycle. This includes access to capital, market linkages, training and capacity building, and networking opportunities. Mentorship and guidance across all these focus areas form the backbone of WE Hub’s work. Let us go back to Pragna’s case to understand this better.

Fig 4: Role of WE Hub across the entrepreneurial needs of Pragna

The WE Hub way: The use of peer groups to bridge the mentorship gap among WLBs

In the above image, we observed how guidance and mentorship play a key role in entrepreneurship. WE Hub’s method has been to provide “mentorship with the help of the community.” MSC designed a range of support areas to foster community engagement for WE Hub’s WLBs under the flagship project “ Women-led Business (WLB) program,” funded by the MetLife Foundation. These initiatives seek to create a network of mutual mentorship and empower women to support each other’s business growth collaboratively.

Community groups to lean in:

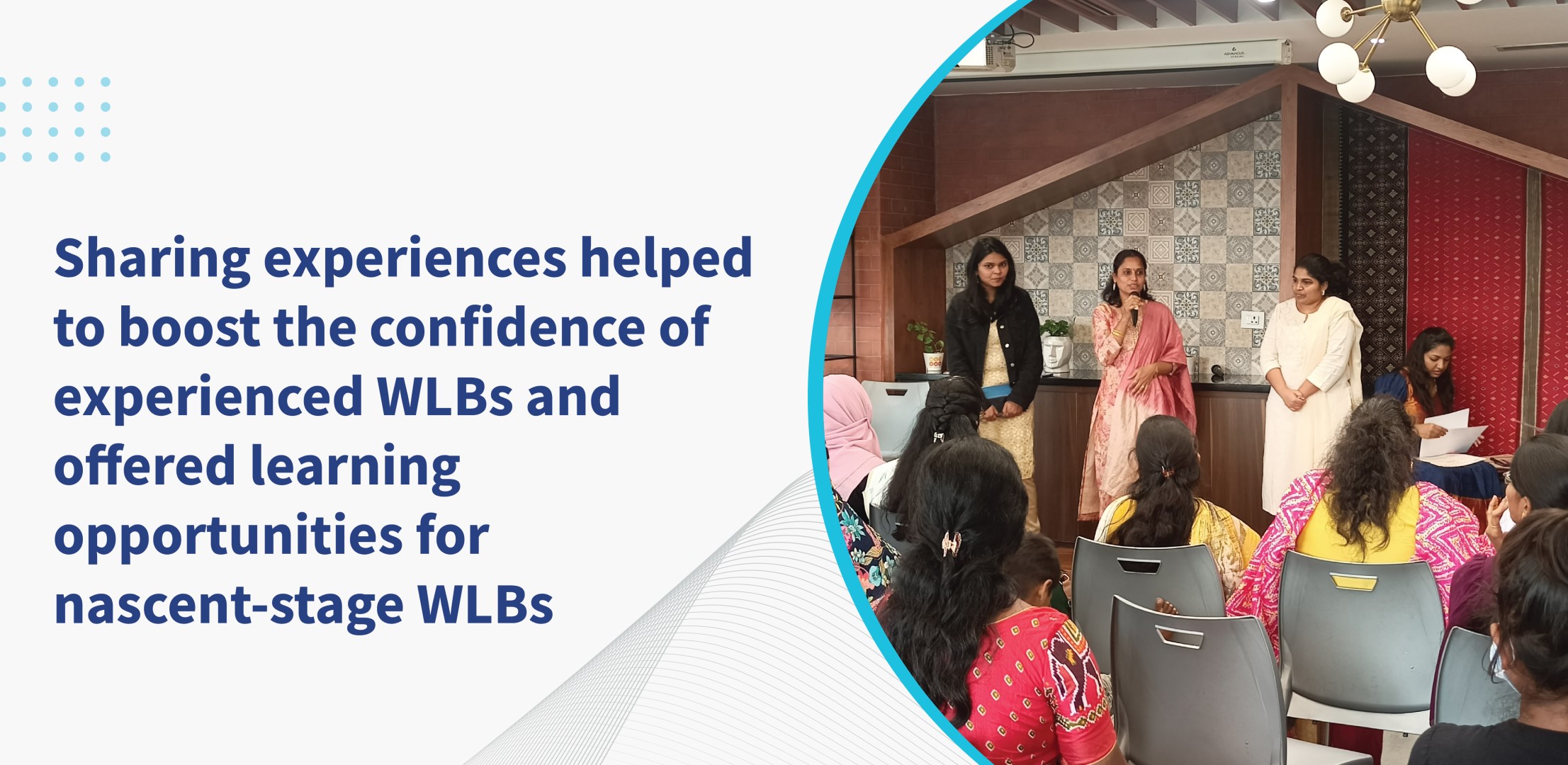

WE Hub regularly conducts in-person discussions with WLBs in similar businesses. However, those meetups primarily catered to training sessions or discussed physical marketing (fairs) events. MSC mobilized WLBs to come together and discuss the challenges around their business’s management with WLB’s support. The group was a good mix of mature and nascent business-stage WLBs.

Interactions with the peer community encouraged women to share their challenges freely and seek guidance from other WLBs. The suggestions from successful WLB entrepreneurs encouraged peer WLBs to continue to put effort into their businesses.

During our group interactions with WLBs, we observed that established WLBs had much to share about their journey. Most nascent stage WLBs were all ears to understand and learn more from each other. We asked ourselves, “Can we formalize and digitize this so that more WLBs can learn from each other?”

Digitizing the community interactions with human touch

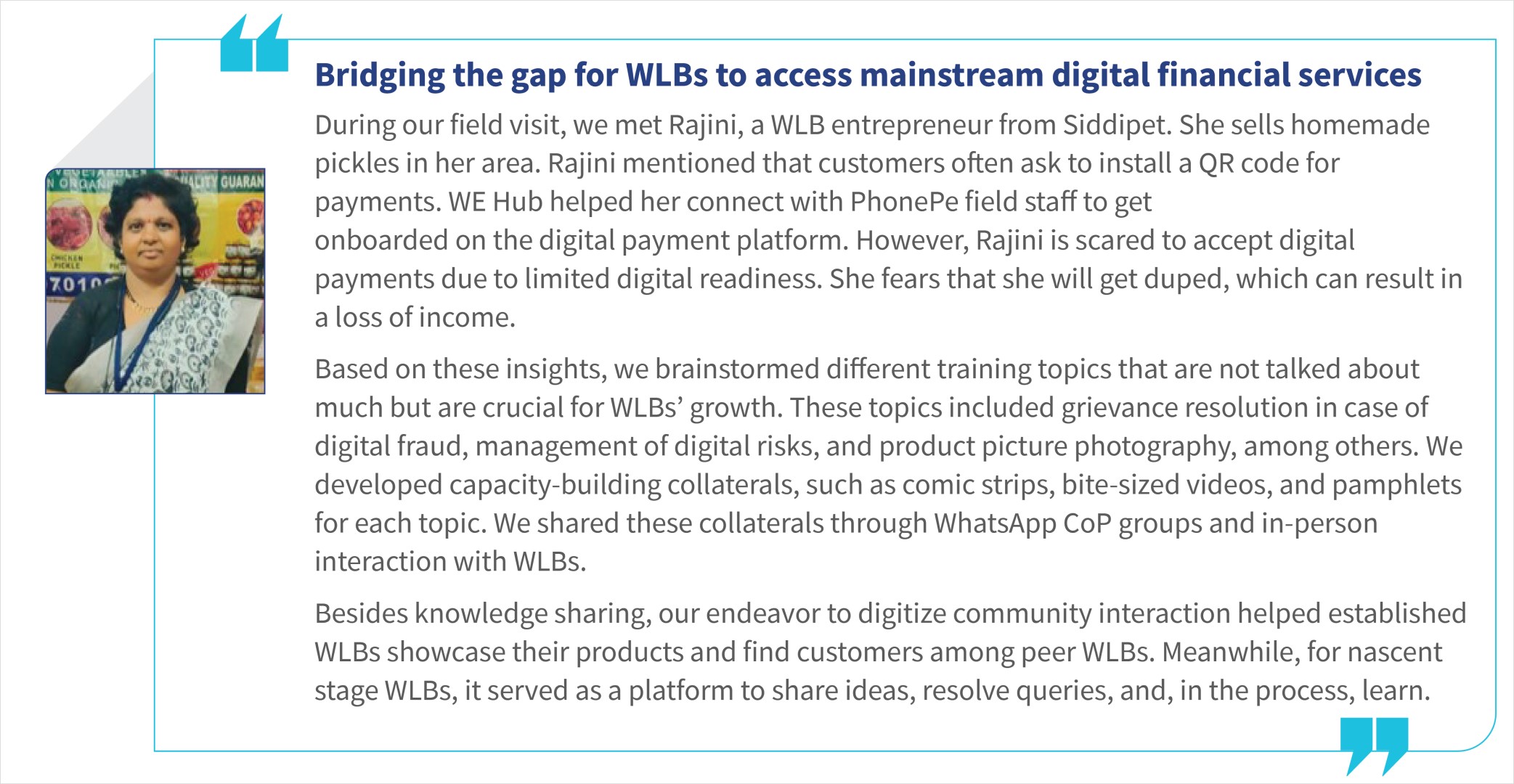

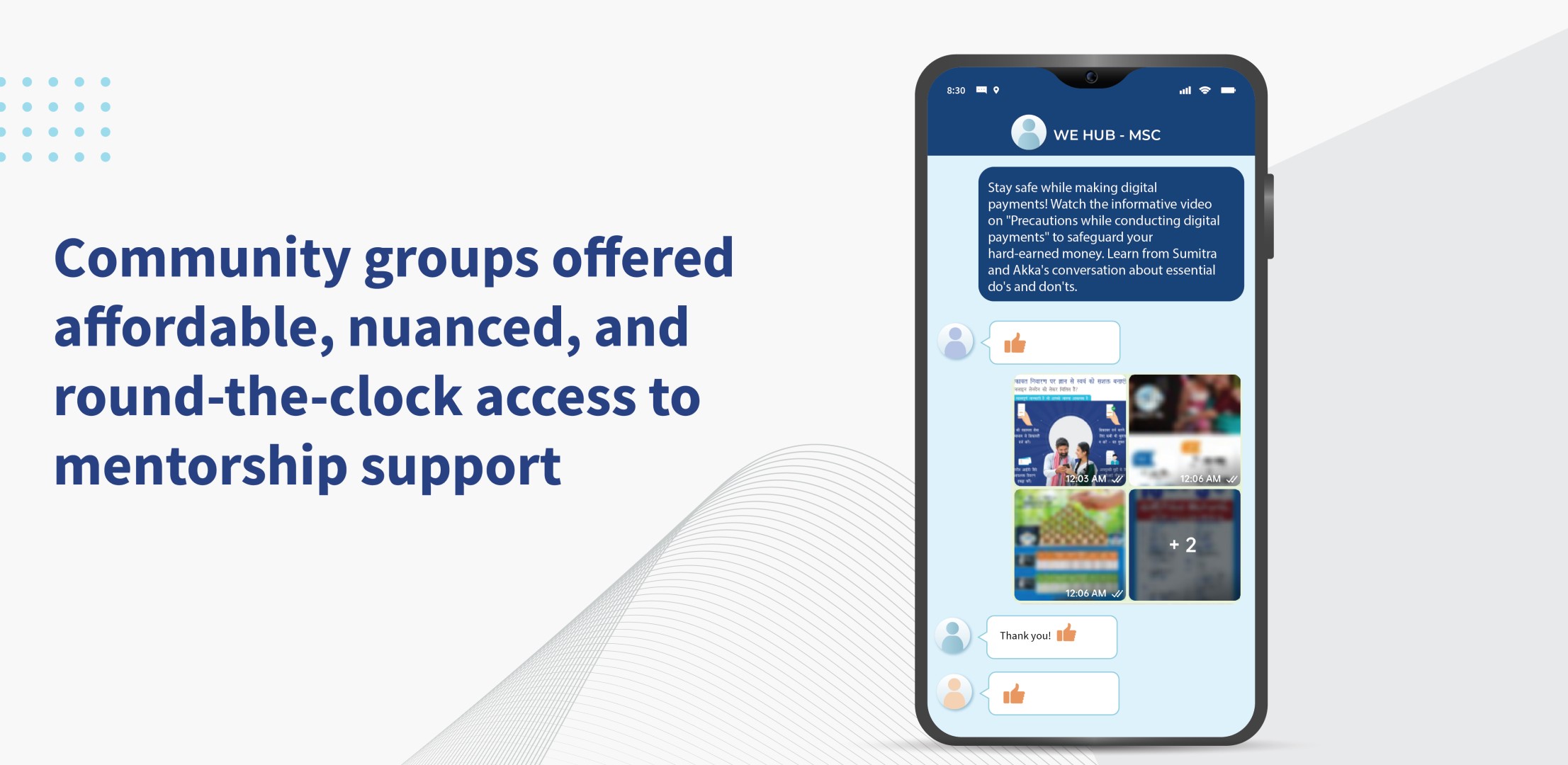

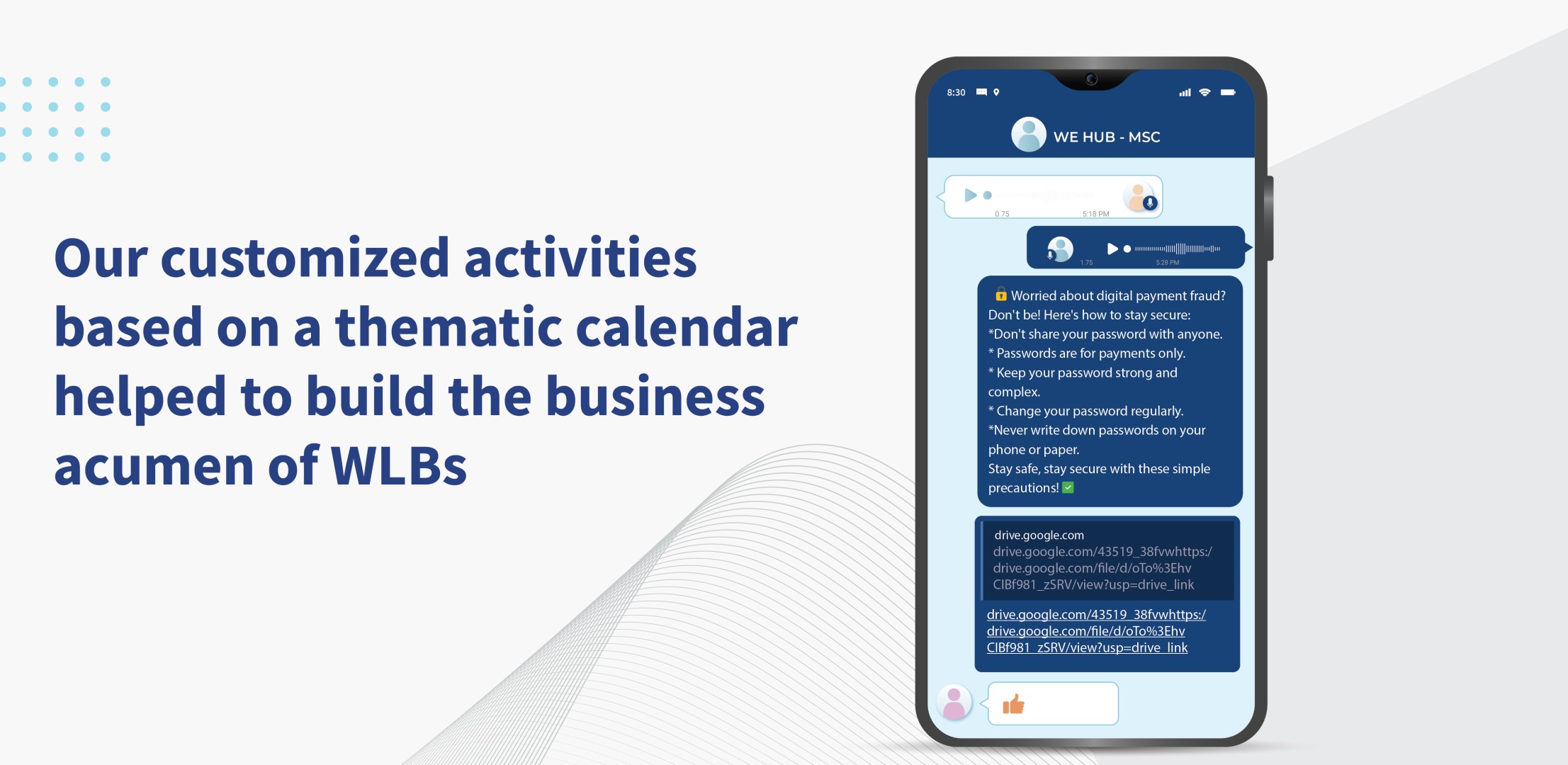

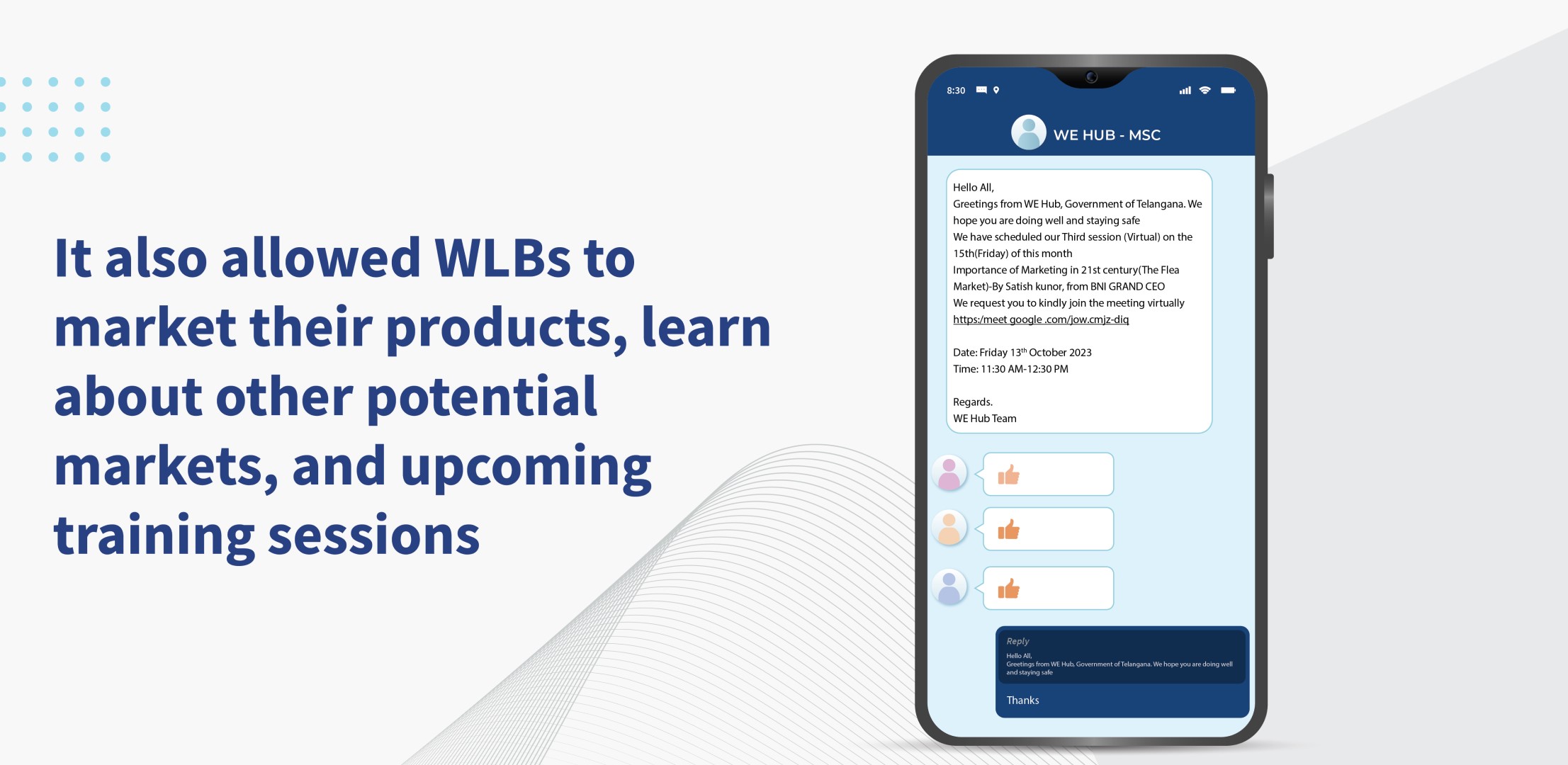

Most WLBs already used WhatsApp for communication. MSC used WLBs’ familiarity with WhatsApp for peer learning. We developed video collaterals that covered insurance, digital payments, business registration, marketing, and business management. We shared these videos with the WLBs in the learning groups we created on WhatsApp. This made the information easily accessible for WLBs.

MSC also identified other digital platforms to engage with these women, such as Google Meet, and used them to conduct group interactions. This was especially helpful for WLBs who could not participate in knowledge-sharing gatherings due to household responsibilities and long commutes. MSC included a good mix of in-person and digital learning sessions to ensure inclusivity, encourage peer learning, and forge the foundation for collaboration.

These initiatives helped WLBs engage meaningfully and learn the best business practices from each other. Ground-level insights determined most of MSC’s interventions and made them relevant and valuable for WLBs.

Use of technology for better engagement:

Our experience with WLBs suggests that they struggle to find relevant information related to business queries in simple and regional languages.

MSC used the WLB WhatsApp groups to integrate into the Sangini Konnect platform as part of the WE Hub project. Sangini Konnect is an artificial intelligence (AI) chatbot that allows WLBs to ask business-related queries and get detailed responses in the form of videos. All of this is in WLBs’ preferred regional language.

How did community-based interventions help WLBs?

WE Hub and MSC’s collaborative efforts to use the community for mentorship positively impacted 5,470 WLBs in Telangana. It encouraged 4,062 WLBs to try digital payments for business and learn about crucial financial resilience products, such as insurance. Community-based mentorship is scalable and affordable and helps WLBs navigate sociocultural norms. Studies suggest that WLBs can unlock India’s goal of becoming a USD 5 trillion economy. The lack of mentorship support is not limited to Telangana’s WLBs but also extends to India and the Global South markets.

We can bring millions of WLBs into the folds of the digital finance mainstream if we tailor the learning experience around community-based mentorship to align with the Global South market’s contextual and social setting. It can digitally empower millions of women like Pragna to run their businesses and become a role models for her peer WLBs in India and beyond.

The efficacy of transfers from higher to the lower tiers of any government depends on the underlying fund disbursement system. Sample this—the Government of India, as per the budget estimates of 2024-25, plans to transfer funds worth USD 266 billion or ~7% of India’s GDP, to states. This includes devolution of states’ share, grants or loans, and releases under Centrally Sponsored Schemes (CSS). The level of sophistication of these systems have a huge bearing on the nation’s ability to spend and spend well.

On 13th July 2023, the Department of Expenditure (DoE) issued a memorandum to implement the SNA-SPARSH mechanism to ensure the “just-in-time” (JIT) release of funds allocated to the CSS through the RBI’s e-Kuber platform. It builds upon the significant gains of the Scheme Nodal Agency (SNA) system’s implementation in July 2021. This blog post highlights the journey, challenges, and innovations in CSS funding. It focuses mainly on the SNA-SPARSH model and its implications for efficient fund release and payment processing.

SNA-SPARSH’s implementation in India represents a significant milestone in the government payments ecosystem, where the holy grail is to achieve JIT payments. As the name suggests, JIT payments would eliminate the gap between the actual physical event, that is, the work for which the payment is due, and the fiscal event. In this context, the fiscal event is the outward movement of money from the consolidated funds to the end beneficiary—a citizen, a business, or other government bodies.

An implicit assumption in the government fund flow is that money will be pushed from one level to another, but SNA SPARSH inverts this assumption. It allows an agency that makes expenditures to pull funds up to the sanctioned limit when needed. With this, SNA SPARSH pushes the envelope toward smart payments, not just JIT. Operationally, the smart payment system will have two core attributes:

Efficient fund release: “pulling” funds from the treasury and passing them on directly to the beneficiary’s bank account;

Efficient payment processing: pulling funds in “real-time,” that is, just when payment for the work is due, based on rules triggered through algorithms.

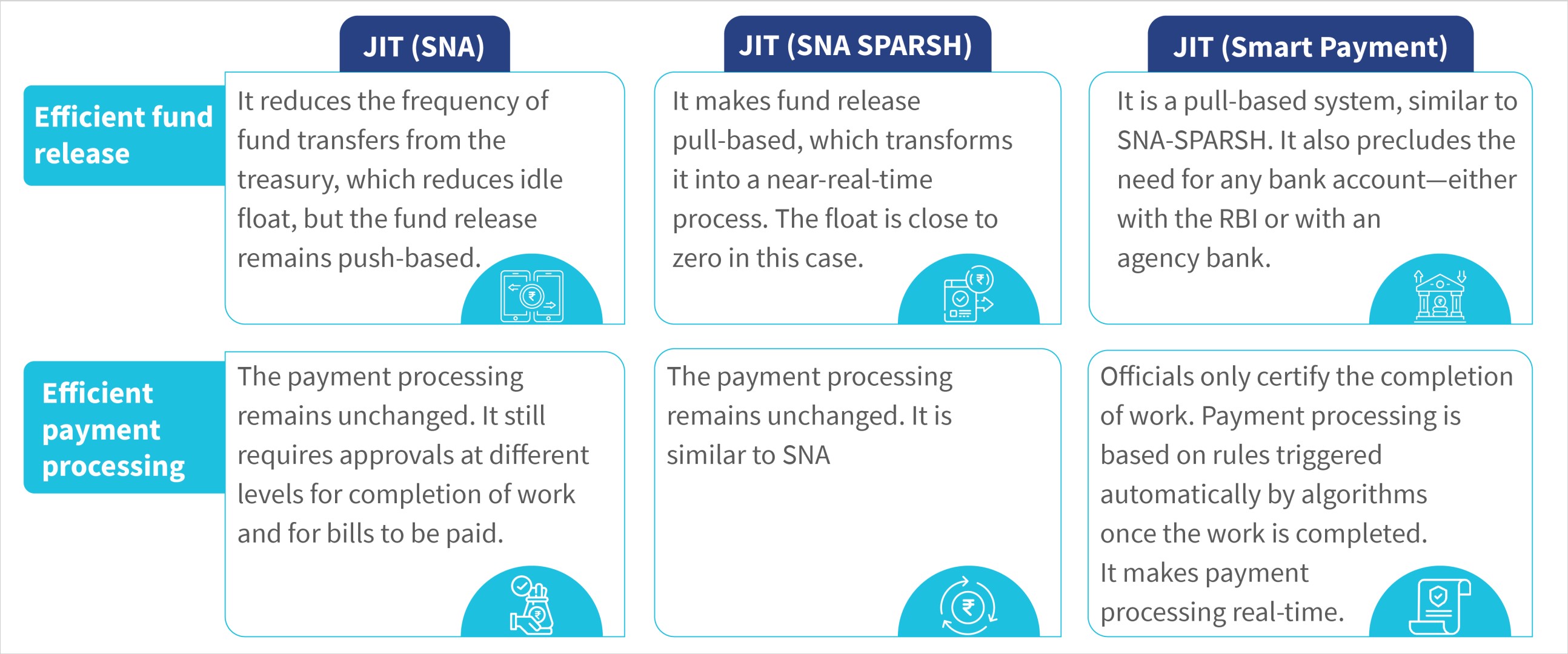

The table below compares the three evolving versions of JIT on these two attributes.

At the root of this ambition for JIT payments is to enhance the state’s capacity to make expenditures effective and efficient. While the budgetary allocations to social sectors by the governments have slowly increased, available evidence suggests budgets remain unspent. Even with spent budgets, the achievement of outcomes remains low.

CSS accounts for a substantial portion of the central government’s budget, as per the interim budget for FY’25, at INR 5.02 lakh crores (~USD 60 billion), CSSs’ share is about 51% of the total transfers committed by the central government to the states. Thus, the deployment of JIT for CSS can potentially bring significant gains to optimize fund utilization and improve outcomes in the public sector.

A brief history of (just in) time

Over any given year, the CSS would be funded via a cascading fund transfer mechanism. Since the money moved from one agency to another, it led to funds in government bank accounts that sat idle for months or years before they needed to be spent.

The SNA was introduced to consolidate banking arrangements, reduce float, and enhance transparency in fund utilization. It has successfully integrated treasury systems across states and union territories, significantly reduced the number of government accounts, and provided real-time insights into fund releases and expenditures. It tackled challenges, such as unspent balances, cash shortages in some implementing agencies, and inefficient fund release strategies.

The quarterly release of funds and contingent additional releases based on utilization have helped reduce float and prevent the accumulation of unspent balances. India’s Finance Minister highlighted estimated annual savings of USD 1.2 billion from the SNA reforms. The SNA model successfully consolidated funds, improved transparency, and addressed various challenges in the fund release process.

SPARSH—the “pull” to complete the fund release

Under the SNA, the funds are still being “pushed,” albeit with fewer intermediate halts, in shorter bursts, and with a good view of where they are at any given time. The gap between the fiscal and physical events has also been reduced but not eliminated.

However, SPARSH marks a transition from a credit push (a-priori release of funds to various implementing agencies) to a debit pull-based fund transfer system in which a debit to the central pool is triggered only when implementing agencies issue payment instructions on the system. By design, SNA-SPARSH can “pull” funds in real time to the end beneficiary’s account, which takes it closer to a smart payment system. These design features are:

Integrated framework of PFMS, the state’s treasury or financial management system and the RBI’s e-Kuber platform that enables seamless flow of information across three systems;

Ability to onboard CSS, SNA, and implementing agencies on the platform—the last two via IFMS;

Creation of CSS-wise sanction orders for each state at the beginning of a financial year.

Under SPARSH, the eventual release of funds into the beneficiary’s bank account is triggered once the SNA or implementing agency generates the payment files. However, clarity is absent in the time gap between the generation of payment files and the physical event—the moment the work or the payment milestone is achieved in the field. When we revisit the holy grail of just-in-time payments, we find pulling of funds is not in “real time.” This does not qualify it as a just-in-time system since challenges in payment processing persist at the program implementation level.

Cometh the hour, cometh the smart payments

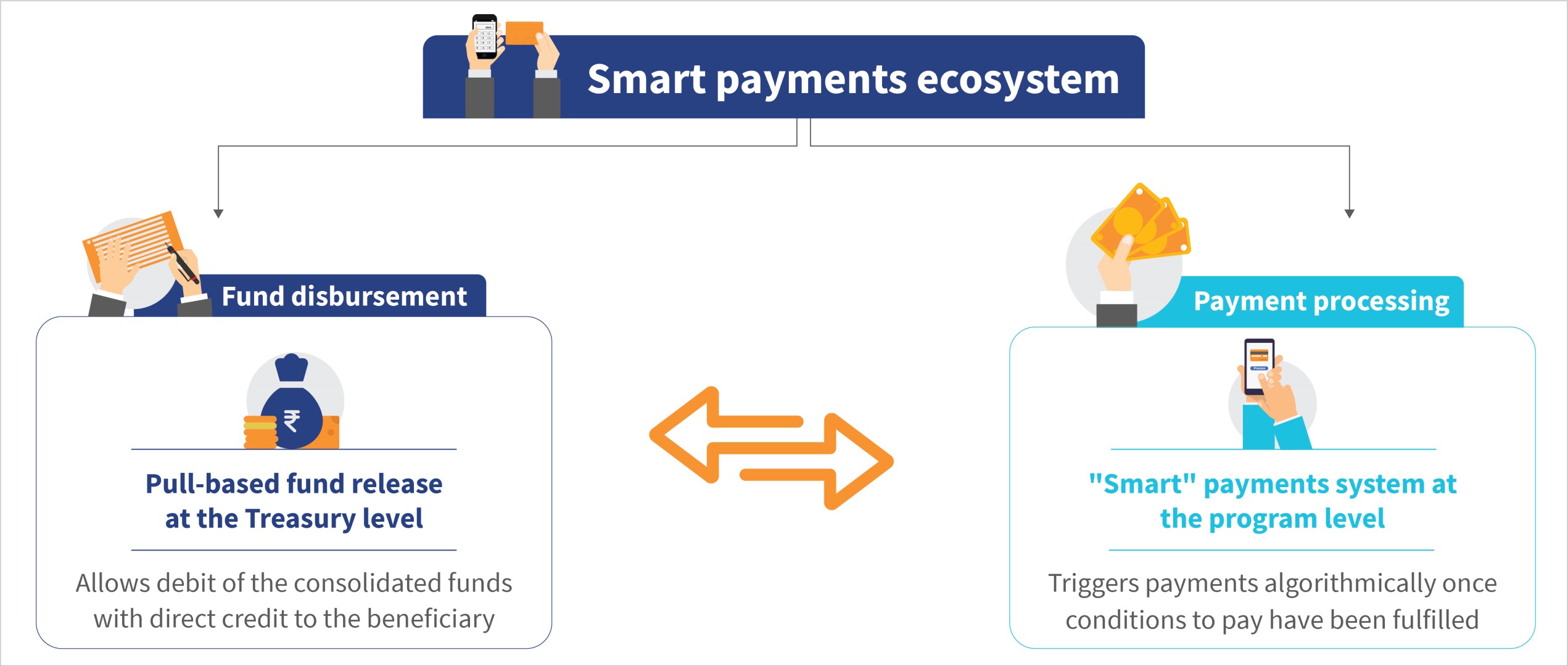

What is needed in this context is a payments processing system that can process payments, that is, generate payment orders automatically upon fulfillment of payment conditions for payees, such as vendors and citizens. Further, it should “talk” to the IFMS system to permit “straight-through processing” of invoices without manual intervention. In other words, we recommend a system that generates the payment files that SNA or implementing agencies can feed into the state IFMS.

When integrated with a pull-based fund transfer system like SPARSH, such a “smart” payments system creates a “smart payments ecosystem” that meets both the conditions of pull-based fund disbursement and the real-time processing of payments. The figure below shows this in detail. SPARSH’s pull-based fund transfer functionalities can be further improved by using a virtual treasury single account (VTSA), which would also eliminate the need to park funds it in any bank account—either with the RBI or an agency bank.

One such smart payments ecosystem is currently being implemented in Odisha. The Government of Odisha launched the MUKTA (MUkhyamantri Karma Tatpar Abhiyan) program to tackle job vulnerability that resulted from the COVID-19 pandemic. MUKTA encountered challenges, such as delays in claim settlement of wage-seekers and SHGs, idle parking of project funds, and ineffective project management.

MSC designed the “smart payments ecosystem” based on our work with the state’s Finance Department since early 2020. We designed a VTSA-based JIT funding system and a smart payments system, “MUKTASoft,” for the Housing & Urban Development Department.

The solution has enabled the transition from a “push-based” to a “pull-based” fund transfer system for beneficiaries, including wage-seekers, SHGs, and material vendors. Under it, the implementing agencies (urban local bodies in the case of MUKTA), pull funds from the state’s consolidated fund directly into the end beneficiary’s bank account in real time when a payment milestone is completed. The solution also incorporates autonomous rule-based processing of payments, which significantly streamlines the process and reduces the burden on officials.

The solution is being piloted in 23 of Odisha’s 149 Urban Local Bodies, and early results are encouraging. It has eliminated the float and reduced payment delays by 57% to the beneficiaries—wage seekers and SHGs. The smart payments system can potentially save the Exchequer as much as USD 50 million for a state like Odisha.

The way ahead

The journey toward an effective and efficient government payments ecosystem in India has seen significant progress with the SNA-SPARSH model. While challenges persist, ongoing experiments and successful pilots demonstrate the potential for transformative changes in how government funds are released and payments are processed. The Department of Expenditure can plan one more reform on SNA-SPARSH to make payment processing based on rules triggered automatically through algorithms upon completion of work certified by the executing agency. It would make payment processing real-time. The vision of JIT payments may soon become a reality to pave the way for improved governance and better outcomes.

Our previous blog discussed agent networks’ remarkable growth in Indonesia. The agent network became more diverse between 2017 and 2023, which allowed multiple business models and provider practices to thrive. Despite its growth, longstanding challenges persisted, while new challenges emerged because of the networks’ increased scale. We discuss some such challenges below:

Lack of account opening services in agent outlets: Only 3% of bank agents offered bank account enrollment services—a decrease from the already low 28% in 2017. Inefficient e-KYC processes make the account opening or signing up process resource-intensive at the agent level. The process is manual, requires physical documents to be sent to bank branches, and takes one to two weeks to be completed.

Agents face liquidity management challenges: More than 60% of agents face barriers due to the unpredictable demand in DFS. The lack of working capital credit for agents exacerbates this problem. This is similar to the situation in 2017, when 63% of agents reported their struggle to manage liquidity.

Agents face increased incidents of fraud and robbery: Between 2017 and 2023, fraud against agents in Indonesia increased sevenfold in rural areas and tenfold in urban areas. 65% of agents are wary that their customers are most likely to commit fraud against them. This is a substantial cause of concern.

Provider compliance and risk mitigation measures remain inadequate: Provider compliance at agent outlets needs improvement. Only 14% of agents display tariffs, and only 42% display their agent IDs.

Providers struggle to train their agents adequately: Both banks and nonbanks struggle to provide refresher training. In 2023, only 19% of bank agents and 7% of nonbank agents received refresher training. Agents hesitate to sell new products without refresher training because they fear that they will make mistakes.

Providers have reduced support staff visits: 51% of agents reported that support staff visits have become less frequent as service providers rely on digital platforms for grievance resolution and communication. However, agents prefer in-person support staff visits to manage technical challenges.

Indonesia’s agent network has been instrumental in the extension of financial services to areas beyond Java Island and the urban regions. The amendments made by OJK and Bank Indonesia to Laku Pandai and e-money regulations in 2022 were forward-looking and aligned with global best practices. Regulators, service providers, and development partners must now collaborate to address challenges, foster innovation, and strengthen agent networks. Here are our recommendations to achieve this goal:

Recommendations for policymakers and regulators:

Promote e-KYC infrastructure’s use to increase products and services available through the agent network

Indonesia has a substantial unbanked population. It also has recently improved its e-KYC infrastructure, which includes digital ID and face recognition services. Agents can bridge the gap in account access by facilitating account openings. Yet regulators and policymakers need to promote the application of agent-assisted e-KYC processes to accelerate account opening and mitigate additional costs to make this happen. These additional costs include expenses for biometric devices to prevent hindrances to adoption.

Standardize training to improve agents’ capability with complex financial products

As agent networks expand, the provision of adequate training becomes challenging. This is especially important, given the introduction of complex financial products and rising digital fraud. Regulators should standardize training modules to maintain consistent service quality, particularly for full-service banking agents. They should also oversee these modules through regular audits to ensure compliance and effectiveness.

Encourage transparency in the agent outlet to improve consumer trust

Regulators must prioritize customer protection and transparency, as most agents fail to display official tariff sheets or agent IDs. They must disclose transaction fees, product information, and grievance resolution mechanisms to ensure transparent services.

Develop a supply-side database on DFS agents

The supply-side data on agents remains insufficient, especially on nonbank agents. Regulators must publish a regular and comprehensive database of agents. It will help assess the progress of financial inclusion and serve as a critical input for evidence-based policymaking. The database should include gender-disaggregated data for bank and nonbank agents beyond agent numbers and locations.

Recommendations for service providers:

Use e-KYC services to expand product offerings to customers

Service providers should use advancements in the e-KYC infrastructure to deliver more comprehensive products and services through agents. This will enhance the agent network’s sustainability and extend financial services to marginalized communities, which will help integrate them into the formal financial system.

Deploy third-party agent network managers to oversee agent operations

As the agent network expands in Indonesia, service providers face challenges when they seek to recruit, monitor, and train agents. They also struggle to provide support on liquidity management. Service providers should use recent regulatory changes to engage third-party agent network managers to provide comprehensive agent support services.

Offer affordable and predictable lending products to help agents manage liquidity

Service providers can offer credit to DFS agents due to the digital nature of their business, which simplifies credit assessment as it provides clear digital trails. Per MSC’s research, lending to DFS agents in Indonesia is a USD 139–250 million opportunity, which is set to grow to USD 245–490 million by 2027. Service providers can innovate internally or collaborate with lending institutions to offer credit solutions that include working capital credit and loans for their CICO-adjacent businesses.

Build internal systems and agents’ capability to detect fraud and build awareness to mitigate them

Wider adoption of DFS coincides with increased risk of fraud, both for agents and by agents. Service providers should help improve their agents’ ability to spot fraud. Service providers should also use digital media and refresher training to alert their agents about newer types of fraud and make them aware of such frauds to ensure safety.

Recommendations for development agencies:

Work with service providers to catalyze and derisk innovations on new use cases for products or services available at the agent point

Despite the growth in transactions, most transactions at agent points are limited to cash-in, cash-out, top ups, and bill payments. Additionally, 80% of money transfer transactions occur over the counter. The full potential of agent networks will be realized when more individuals can conduct digital transactions independently and eventually access other financial products and services.

Development agencies can help advance new use cases that improve DFS use. This involves the promotion of research, development of proof of concepts, and initiation of pilots to test new products and services. Development agencies can also improve agent networks’ operational efficiency if they share the risks and costs associated with the development of these new products.

Provide knowledge support to facilitate the transition from enhanced access to improved usage of financial services

Findings from the ANA 2023 research emphasize a need to shift policy focus from enhanced access to improved usage and quality of financial services. Development agencies can help improve agent networks’ regulatory and supervisory capability through research support, capacity-building support, and facilitation of exposure to international best practices. This knowledge support should extend to private sector stakeholders that intend to test innovative approaches to develop and manage their agent networks.

All stakeholders must work together to tackle the challenges and maximize the opportunities in Indonesia’s changing agent network. Meeting Indonesia’s financial inclusion targets demands efficient coordination among policymakers, service providers, and development agencies. This collective endeavor will empower agents, speed up financial access, and drive the sustainable expansion of Indonesia’s agent network.

For a complete overview of the recent findings, you can view the full Agent Network Accelerator (ANA) Research – 2023 report here.

Meet Neha and Sarita, rural women based in Alwar, Rajasthan. Neha is a confident business correspondent (BC) agent who uses her smartphone effortlessly for many things, such as e-commerce. In contrast, her neighbor Sarita uses a shared household smartphone her husband owns, which she hesitates to use for e-commerce. Then, one day, Sarita’s fate changed when she tapped into her community and reached Neha, who inspired her to master e-commerce platforms.

This blog charts a journey from uncertainty to confidence through a community of practice (CoP) in the era of the digital divide.

(Learn more about MSC’s work on CoP). In this internet age, e-commerce enables entrepreneurs to access larger markets and diversify their income streams. It also helps users, especially women, reduce their dependency on traditional and often less accessible market channels. Thus, it increases their economic independence.

Community of practices: A step closer to bridge the gender divide

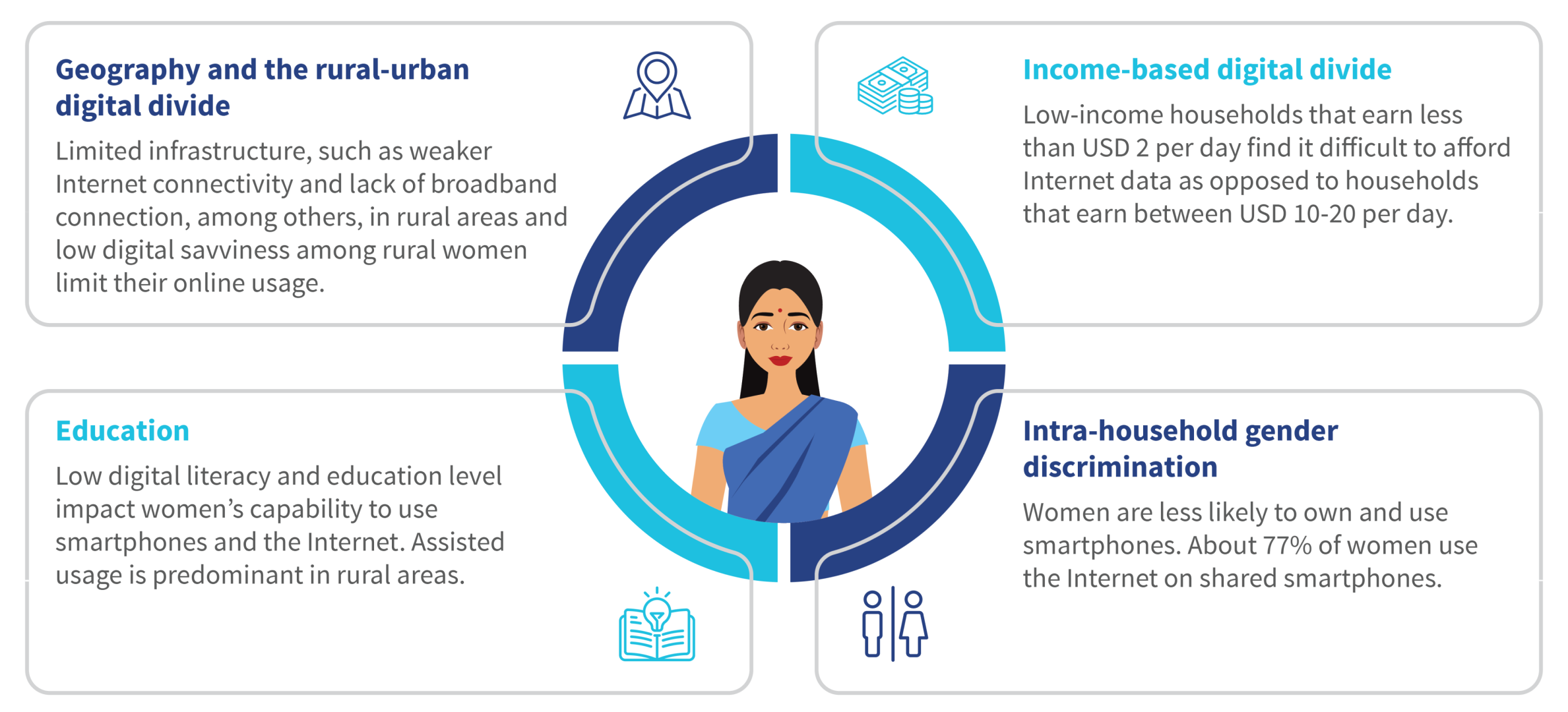

As per the Findex data 2021, about 80 million customers aged above 18 years made their first digital merchant payment during the COVID-19 pandemic. Almost 95% of all Indian districts have access to e-commerce platforms. Yet, disparities persist between the urban and rural areas. As per GSMA’s “The State of Mobile Internet Connectivity 2023” report, 10% of Indian smartphone users do not use the Internet, while 37% of the rural population is unaware of the Internet, and 15% do not know how to use it on a mobile phone.

Gender inequalities continue to plague the digital world. Women lack regular access to technology and digital products. As per GSMA’s “Mobile Gender Gap Report 2023,” women are 40% less likely to own a smartphone and use mobile Internet than men. Women’s usage of smartphones and the Internet in India for digital payments is 17% less than that of men, as per the Global Findex Database 2021. Their digital proficiency with smartphones and the Internet is limited to calling, short message service (SMS), and social media, such as WhatsApp and YouTube.

Figure 1: Four key factors that contribute to the digital divide

We can significantly enhance women’s proficiency in e-commerce if we actively build their capacities. While this is easier said than done, MSC’s ground-level work with Frontier Markets provides a ray of hope as it builds and sustains a localized community of practice (CoP).

Driving women’s participation through CoP: Offline and online channels

A CoP is a “collaborative network where individuals bond over a shared interest or field and engage in collective learning and expertise development.” A CoP can play a key role to drive initiatives on the ground through peer-to-peer (P2P) learning and encourage more women to use e-commerce on the demand side as customers and the supply side as entrepreneurs. For instance, a field visit with Frontier Markets in Rajasthan revealed that women were eager to develop their capacities, diversify their income, and strengthen their financial resilience through e-commerce.

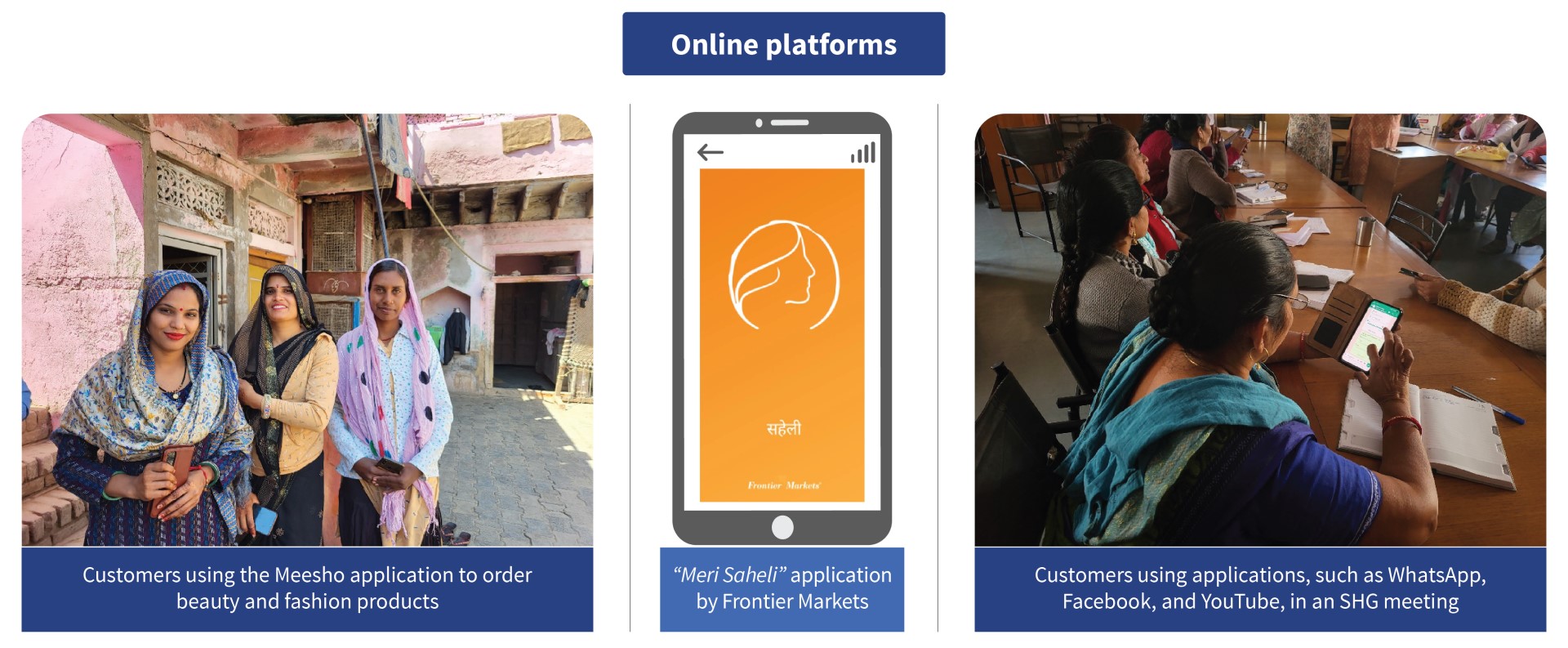

Stakeholders can build CoP initiatives through both offline and online channels. Offline channels include SHGs, while online channels include platforms, such as WhatsApp, Facebook (Meta), YouTube, Meesho, and Frontier Markets’ “Meri Saheli” application. CoPs can empower rural women to use the Internet and smartphones for e-commerce.

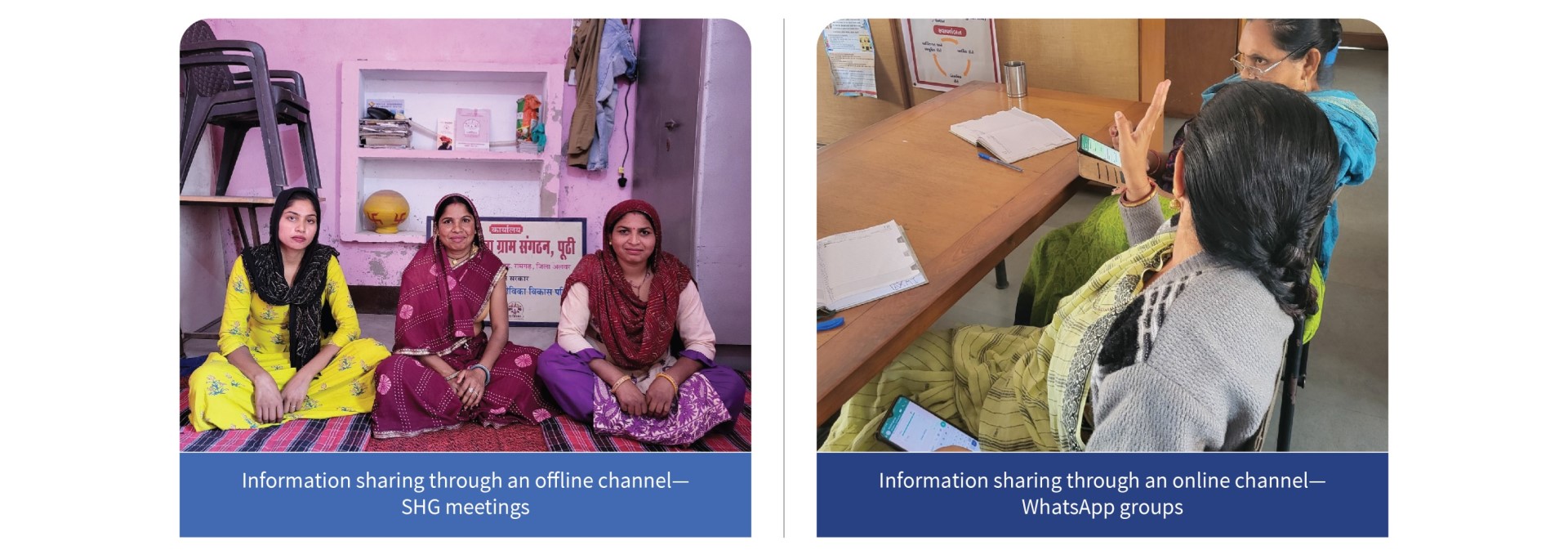

Figure 2: Rural customers as they share information through offline and online channels

Offline channel: SHGs (self-help groups)

Several women entrepreneurs are part of SHGs. They come together and discuss group members’ financial needs, aspirations, and challenges, share expertise around their primary occupations, and organize skill-building activities to support each other. This creates a collaborative environment where women learn and grow. These existing institutions, therefore, serve as launch pads for the women entrepreneurs to build localized CoPs, upskill, and scale their businesses. These women also share their success stories and help other women in their community use technology to benefit their businesses.

For instance, during MSC’s fieldwork with Frontier Markets in Rajasthan, we observed that female BC agents actively promote digital transactions on e-commerce platforms and at BC agent points.

Figure 3: Key highlights of the SHG offline channel

Additionally, SHGs provide a platform for financially and digitally proficient women to build their peers’ capacities and offer guidance. For example, Frontier Markets has a strong network of Sahelis in rural Uttar Pradesh and Rajasthan, which builds rural women’s capacities to place orders on e-commerce platforms and conduct person-to-person (P2P) and person-to-merchant (P2M) digital payments. These women entrepreneurs’ efforts catalyze the businesses of other women entrepreneurs through technology-driven tools and platforms.

The use of community spaces for offline channels

Although CoPs are a stepping stone where women entrepreneurs share lessons with each other, social constraints deter women from gathering in common places. However, women can overcome social constraints and engage in SHG activities when they generate income for the household, provide access to financial services in the community closer to home, and build their identity. Community gatherings in the panchayat office, the primary health center, and schools, among others, can emerge as a channel through which women teach each other how to use e-commerce platforms and conduct digital payments.

Online channels: A potent option to drive CoP

CoP thrives on knowledge sharing and peer learning. Besides SHGs, where women share information in person, digital platforms also provide women with a channel to share information and learn from each other.

Many rural women often use digital applications, such as WhatsApp, YouTube, SMS, and phone calls. A few also use e-commerce or social commerce platforms, such as Amazon, Flipkart, Meesho, and the “Meri Saheli” platform, to buy products independently or with Saheli’s assistance. These self-initiated and assisted transactions clearly demonstrate the use of technology and the key role technology plays to grow their business and build awareness in their community. The following section outlines some platforms we see in action on the ground.

Virtual groups, channels, and chatbots on WhatsApp encourage knowledge sharing and absorption. Geography-specific WhatsApp groups and channels at the SHG or CLF (cluster level federation) level create a platform for women who want to learn how to conduct digital payments and buy and sell products on e-commerce to exchange information regularly. For instance, Frontier Markets encourages engagement among Sahelis and rural women through WhatsApp groups, where they learn about digital payments and advanced agricultural inputs, such as climate-resilient seeds, liquid fertilizers, and animal nutrition.

Figure 4: Frontier Markets used these three features of WhatsApp to share information with women

Platforms, such as Facebook, Meta, and YouTube, equip rural women with diverse skills, such as digital payments, vocational education, and farming. This strengthens their employability and income-generating potential. Moreover, platforms, such as Meesho and the “Meri Saheli” application, enable rural women to access essential household products conveniently. Through these platforms, rural women gain familiarity with digital payment modes, such as UPI (Unified Payments Interface) and QR (quick response) code-based systems (PhonePe, Paytm, and Google Pay). This streamlines their experience to conduct digital financial transactions and build their digital footprints.

Figure 5: Rural customers using online platforms

The way ahead

CoP initiatives through offline and online channels can help rural women like Sarita develop their financial and digital proficiency and bridge the digital divide. Tapping into the local leadership’s potential and skill sets of financially and digitally proficient women can develop rural women’s capacity to use e-commerce. With an active CoP and willing service provider, many women like Sarita can access larger markets, diversify their income streams, become economically empowered, and enhance their financial and digital literacy.

Indonesia’s agent network landscape is dynamic. It witnessed significant changes in recent years, which include a proliferation of service providers and the emergence of various business models. Moreover, external factors, such as COVID-19 and regulatory and policy changes, have shaped the network’s growth. The Agent Network Accelerator (ANA) 2023 research is the biggest-of-its-kind survey of DFS agents in Indonesia that delves into some of these changes. This crucial benchmark compares the agent network’s growth in 2023 with the ANA research in 2017 and features participation from 2,644 agents countrywide. Read on as we track these changes and examine their implications for agent sustainability in the “State of the agent network, Indonesia 2023” report.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

WE Hub regularly conducts in-person discussions with WLBs in similar businesses. However, those meetups primarily catered to training sessions or discussed physical marketing (fairs) events. MSC mobilized WLBs to come together and discuss the challenges around their business’s management with WLB’s support. The group was a good mix of mature and nascent business-stage WLBs.

WE Hub regularly conducts in-person discussions with WLBs in similar businesses. However, those meetups primarily catered to training sessions or discussed physical marketing (fairs) events. MSC mobilized WLBs to come together and discuss the challenges around their business’s management with WLB’s support. The group was a good mix of mature and nascent business-stage WLBs.