MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

The Central Bank Digital Currency and its value to the economy

byMicroSave Consulting

Our podcast features Dr. Juliet Ongwae, a consultant with MSC, and Ritika Sah, the Training Coordinator at the Helix Institute at MSC. They discuss the Central Bank Digital Currency (CBDC) and the value it adds to the economy. The podcast also explores why central banks worldwide want to launch a digital currency and the different risks associated with digital currencies.

The PM Kisan program provides all eligible farmers three equal installments of 25 USD every four months. At the time of the launch, it focused on small and marginal farmers. Later, it extended the benefits to all the farming families providing more coverage.

These cash assistance programs for farmers have similar objectives but differ in design and impact. The deck compares the three programs on the themes of enrollment, grievance redressal systems, and supply-side challenges.

This strategic insight deck explains the program’s contribution to the income and expenditure of the average farmer’s household. It also reveals PM Kisan’s differential impact on different categories of farmers.

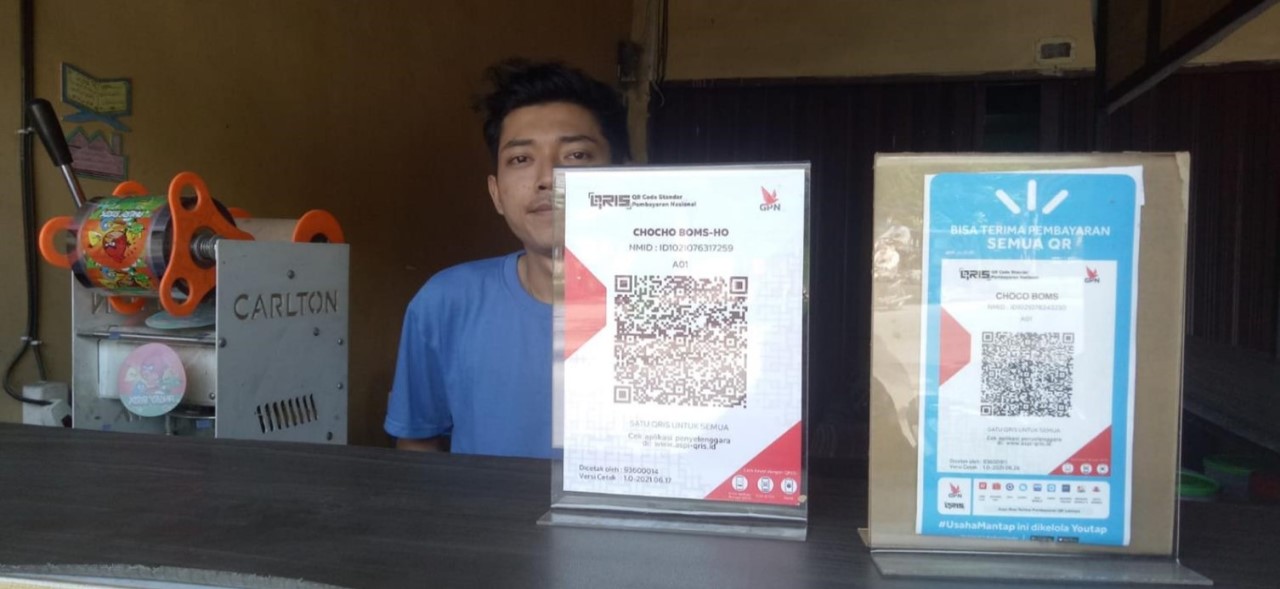

“QRIS is easy and safe to use. I do not worry about loose change or fixed amounts of cash anymore. I consider it safe to use during the pandemic because it means less exchange of physical cash with customers,” says Putri, a female food stall owner in rural Indonesia.

Putri is one of the 15 million micro-entrepreneurs in Indonesia who now has affordable access to digital payments. For many micro-merchants like Putri, who earn less than IDR 300,000,000 each year, using QRIS is their first experience using digital financial services. Earlier, offering digital payment options to customers was expensive and time-consuming for micro-merchants. Merchants had to buy expensive point-of-sale (PoS) devices, which took more than two weeks. Now, service providers can onboard merchants and provide them with the option to use QRIS on their merchant applications faster and at nearly no cost.

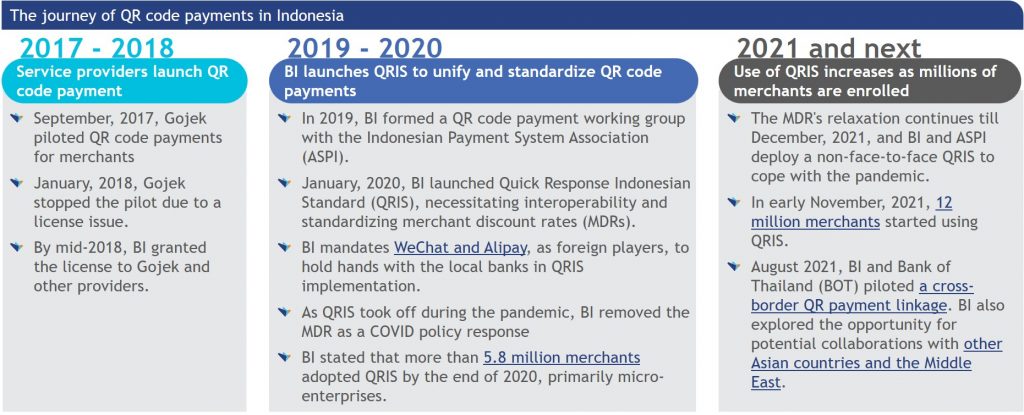

In a country where ~88% of the MSMEs still prefer cash as the primary mode of payment, the growth of QRIS has been impressive. In 2021, Indonesia recorded around 12 million QRIS transactions worth IDR 27.7 million (USD 1,840), showing a growth of 237% from the previous year. However, despite such growth, some challenges restrict the uptake and usage of QRIS.

We highlighted these challenges in our earlier blog, and validated them using insights from our most recent study to assess the implementation and usage of QRIS among micro and small merchants. The only other major challenge quoted by some merchants in using QRIS as a payment method was the limit on the transferable amount and wallet balance. However, as of 1 March, 2022, the regulation has changed, and Bank Indonesia increased the limit from IDR 5 million (USD 330) to IDR 10 million (USD 660), and then further to IDR 20 million (USD 1,320). This new limit is a reasonable amount, even for some of the larger merchants.

The evolution of QRIS and where it should head

While QRIS has evolved majorly, the focus now must shift to optimizing the usage of the platform and provide value-added services to the merchants.

As QRIS has forged a path into digitalization for many merchants, service providers and the government can use it to deliver better services and relevant support. Service providers have a unique opportunity to onboard merchants and help them gradually enhance the digitalization and resilience of their businesses. Merchants who start their digital financial journey with QRIS are ideal for upselling and cross-selling other products offered by the service providers.

Using QRIS and digital transactions to access more products

Service providers now have a record of digital transactions conducted by merchants. Based on these transactions and other socioeconomic details, providers can use alternative credit rating mechanisms to offer credit to merchants who previously lacked the required information to avail of credit traditionally. Uni offers pay later credit cards to the masses in India, specifically targeting applicants without a credit history. Uni determines the creditworthiness of applicants based on alternate credit rating techniques and its proprietary underwriting tech.

Building merchant resilience through other business development applications

Besides offering products based on QRIS and digital transaction history, service providers have the opportunity to upsell other useful products. Business management tools can help merchants keep track of their business based on transaction trends. Providers can offer such tools as an additional feature or an upgrade to the merchants. Basic analytics can be used for stock management by determining trends in sales to help growing businesses make more informed decisions. GoBiz is a super app that provides several business management tools and integrates payment and credit options for merchants.

Supporting business growth with other relevant financial products and services

Providers can tailor other products like savings and investments to merchant requirements based on their business stage and growth prospects. GoPay, a mobile wallet, has an option for its users to save with Bank Jago and invest through the app. Products developed specifically for merchants could build their business resilience and create a strong relationship with service providers who can benefit from these opportunities to cross-sell.

Onward and upward

For MSMEs to reap the benefits of being truly digitally included, stakeholders need to take collaborative action. Complete digital inclusion of MSMEs in the digital ecosystem will ensure benefits for MSMEs and profits to service providers. Regulatory oversight is required to keep fraud and data privacy issues in check so that new digital merchants are included responsibly.

Like many other micro-merchants, Putri would benefit from a small short-term loan to buy her raw materials or equipment. Micro-merchants like her would also appreciate a savings product that offers easy liquidity to tide over the weeks sales are low. Technologies like QRIS offer a great start to build merchant capabilities and support them in their digital journey. Using QRIS will develop the right skills and confidence among merchants and access to useful digital products and services will help them thrive in the digital era.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.

“QRIS is easy and safe to use. I do not worry about loose change or fixed amounts of cash anymore. I consider it safe to use during the pandemic because it means less exchange of physical cash with customers,” says Putri, a female food stall owner in rural Indonesia.

“QRIS is easy and safe to use. I do not worry about loose change or fixed amounts of cash anymore. I consider it safe to use during the pandemic because it means less exchange of physical cash with customers,” says Putri, a female food stall owner in rural Indonesia.