According to the ILO, the decline in employment in the second quarter of 2020 is likely to be far worse than initial estimates had indicated. The first month of crisis points to a decline in earnings of informal workers of 60% globally. The anticipated impact in Africa is higher at 81%. The growth in African economies has been dropping sharply, especially in the West African Economic and Monetary Union (UEMOA), a dynamic area of the region. External demand has declined fast, supply chains are under strain, while domestic production continues to slow. The fight against unemployment promises to be long and difficult.

In West Africa, the impact will be even greater in those places where informal employment accounts for 92.4% of the overall employment across all sectors. This is due to confinement measures or because informal employees work in the sectors that the pandemic has hit the hardest, or due to a combination of both. As we know, crises have a more negative impact on the most vulnerable, and COVID-19 will not be an exception. Young people and especially women who already face the global challenge of underemployment count among the most at risk in this global health crisis. The financial, economic, and social repercussions of the pandemic are unprecedented.

At this point, we face several questions worth exploring. How are youth coping? How can we engage young people in the management of the crisis and recovery after the pandemic? While they will need short-term financial support, different levels of impact alongside a long-term strategy should be considered.

The COVID-19 pandemic has had an impact on almost every aspect of Africa’s economic and trade landscape and reshaped the prospects of growth across the continent. Youth who were in the process of being employed have seen their hopes dashed “This crisis is going to stretch my period of inactivity and unemployment. I do now for how long my chances of entering the professional life are postponed,” laments Dirk-Emmanuel, a young graduate. Youth are also most likely to lose their jobs first as they are less experienced—many internships or fixed-term contracts will not be renewed.

Moreover, young people who have opened their businesses will find it difficult to survive the crisis. They lack the financial resources and experience, particularly of crisis management, to tide them over. Policymakers will need to develop, test, and deploy programs designed specifically to create employment opportunities for youth.

Young people are already reacting to the virus through innovation for social impact

Despite the most damaging consequences of the current health and economic crisis, some positive developments have emerged. Indeed, if anything, the situation has revealed the resilient nature of youth. Many young workers and entrepreneurs have chosen to see the proverbial glass half full and to position themselves as agents of change. The confinement has not hindered their imagination.

Enterprising youth have already developed several applications, such as AntiCoro, created by the association of 10 Ivorian startups and SOS-COVID of the Cameroonian startup House Innovation. The features of these apps include the ability to self-diagnose in light of the symptoms presented, to follow the evolution of the disease around the world, and to learn about the precautions users can take to protect themselves. Some apps allow users to request geolocation assistance and provide mapping of infected areas. Others help users identify supply points for necessities, e-learning, or telecommuting solutions.

Several young tailors whose business has slowed to a crawl have repositioned to stitch the masks that are now mandated in public places in Senegal and Côte d’Ivoire. They were able to find buyers and broaden their distribution points to include a range of companies, pharmacies, bakeries, caterers, and even associations that redistribute them to the most vulnerable individuals.

For example, the startup Dakar Masks was born out of a collaboration between Senegalese entrepreneurs and craftsmen who decided to make fabric masks as per the standards defined by the CHU de Grenoble. The startup developed a test to ensure their effectiveness. “We spark a lighter flame in front of each mask, and then we blow. If the flame does not go out, it shows that the air does not pass through the fabric. The virus is therefore unlikely to get embedded in the tissue,” explains Demba Guèye, the founder of Dakar Masks. Customers can place their orders for masks through a WhatsApp number and the company delivers them home to address social distancing.

The Senegalese brand Lesly Mac Fashion designer has also taken this opportunity to pivot its business. “I anticipated the demand for the masks because I knew there would be a spike, just like what is happening now. Our mask creation business allows us to keep our staff and pay fixed expenses,” explains Charlene Lesley, founder of the brand.

Two young Senegalese entrepreneurs Ibrahima Ndiaye and Ousmane Diop created and implemented automatic handwashing stations, named Kayy Rakhassou, which means, “come and wash your hands”. The device offers soap and water and works with solar energy, which makes its use completely autonomous and sustainable. It also has paper tissues and a bin. The two entrepreneurs hope that their next steps will be to increase their production volume through partnerships with companies, governments, and municipalities.

Oumar Basse is the co-founder of Yobante Express, a marketplace that connects delivery drivers to local businesses to optimize last-mile delivery in developing countries. He had to adapt to the new need quickly to deliver while strictly respecting the need for social distancing. “We have also implemented #yesfood (food delivery) and #region (delivery in all regions) in close collaboration with the Ministry of Trade and DER (General Delegation for Rapid Entrepreneurship of Youth and Women). We bring concrete solutions to the problem related to the distribution of bread with the “Diaym Mbourou” device”, Omar notes.

Such applications, masks, hand washing stations, and home delivery services are all innovations that came into being by adapting existing businesses or by creating new services. These can generate critical revenue streams and contribute to the survival of many businesses while enhancing the welfare of the population.

Solutions and recommendations

Many are pessimistic about Africa’s future, even though the region offers tremendous potential. Part of the solution lies in the youth. Young people need to be consulted and engaged in the development of health, economic, and social interventions that respond to COVID-19 and its recovery. Africa needs context-specific solutions and is already demonstrating its ability to reinvent itself in response to the crisis. Now is the time for the private sector to build strong partnerships with start-ups to maximize the impact of innovative emerging solutions.

“Africans must “occupy the ground” and become key players in the continent’s development. Stakeholders, such as the private sector and academia need to be more involved in sustainable development,” says Ahunna Eziakonwa, Deputy Under-Secretary-General of the UN. The President of MTN, Rob Shuter, agrees: “The private sector has a major role to play because we can very quickly put our assets and expertise into service.”

Conclusion

The recovery after the pandemic is going to be slow, very slow. The future looks difficult but the exit from the crisis will necessarily be through cooperation and partnerships. Many young workers and entrepreneurs have seized the opportunity to reposition their businesses or jobs and adapt. They are part of the solution. The private sector needs to see young people as potential partners, build their capacities, help them innovate, and bring solutions to the world in which they wish to live.

We have an opportunity to enhance the role of digital solutions. Many training courses, and tools of all kinds, are available online for free to support this. People can utilize the many opportunities of this challenging period to innovate, build capacity, and get ready to rebound after the pandemic is over. Many positive initiatives continue to emerge, making it more necessary than ever to collaborate and coordinate. The world will be a very different place—our collective work now, together, can help shape it for good.

The Internet plays an immense role in Dhanshree’s life. Her active use of the Internet and social media facilitates her ability to multitask. She uses

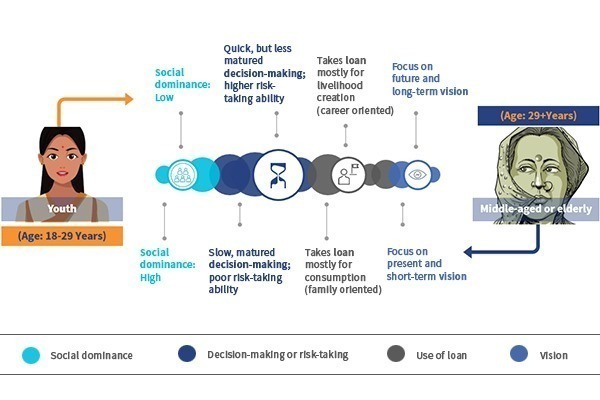

The Internet plays an immense role in Dhanshree’s life. Her active use of the Internet and social media facilitates her ability to multitask. She uses  The respondents from the middle-aged category expressed a limited desire to take calculated risks, start enterprises, or pursue livelihood opportunities owing to their existing responsibilities to grow their families and care for children and the elderly.

The respondents from the middle-aged category expressed a limited desire to take calculated risks, start enterprises, or pursue livelihood opportunities owing to their existing responsibilities to grow their families and care for children and the elderly.

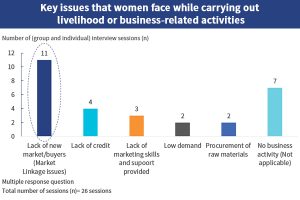

We often see that more than ever before, young rural female SHG members are more engaged in social, financial, and civic issues that affect their communities. During our research, we found that, for the most part, young female SHG members took care of all book-keeping activities and bank-related work for the group. However, when it comes to self-growth, these young members find it difficult to seize opportunities to lead livelihood activities due to a range of complex socioeconomic issues. Our interactions with many of these young female members suggest that in their start-up activities, many lack proper access to markets and human resources, are unable to promote their products, and subsequently face low product demand.

We often see that more than ever before, young rural female SHG members are more engaged in social, financial, and civic issues that affect their communities. During our research, we found that, for the most part, young female SHG members took care of all book-keeping activities and bank-related work for the group. However, when it comes to self-growth, these young members find it difficult to seize opportunities to lead livelihood activities due to a range of complex socioeconomic issues. Our interactions with many of these young female members suggest that in their start-up activities, many lack proper access to markets and human resources, are unable to promote their products, and subsequently face low product demand. Significant improvements in “access to markets” are needed for SHG members to be able to access livelihood opportunities and create sustainable development. Many young SHG members who have started businesses have faced problems and economic losses due to poor access to markets. “Access to finance is not a problem for me but access to markets is. How can I sell and deliver my handmade products in far off places? Why do I have to depend on my brother to sell these items? He can easily roam around day and night on his motorbike but I cannot. It is difficult for young women—we have some limitations,” rued a young SHG member who is running a business selling handmade paper envelopes.

Significant improvements in “access to markets” are needed for SHG members to be able to access livelihood opportunities and create sustainable development. Many young SHG members who have started businesses have faced problems and economic losses due to poor access to markets. “Access to finance is not a problem for me but access to markets is. How can I sell and deliver my handmade products in far off places? Why do I have to depend on my brother to sell these items? He can easily roam around day and night on his motorbike but I cannot. It is difficult for young women—we have some limitations,” rued a young SHG member who is running a business selling handmade paper envelopes.