MSMEs are drivers of GDP and employment in all developing economies. The quicker we help them get back on their feet, the sooner we can end the economic misery that has befallen entrepreneurs and workers, especially those in the informal sector. The COVID-19 pandemic is a “grey swan” event, that is, it is a known unknown. It has no real precedent in terms of disruption at this scale, but we can find analogies in the aftermath of disasters and hazards, such as typhoons, floods, and tsunamis, to inform policy responses.

In 2018, MSC conducted a study with MSMEs in the Philippines to understand how they are affected by disasters. In the study, we assessed their coping mechanisms in the aftermath. The Philippines has historically been on the receiving end of disasters, such as typhoons and floods. MSMEs in the Philippines have had to respond to disruptions caused by these disasters, develop coping mechanisms, and work their way out of these challenges. In this blog, we will reiterate insights gathered from the study and draw parallels to identify pertinent responses for the ongoing pandemic.

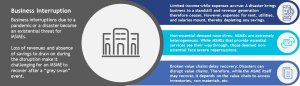

An interruption in business is the culmination of all the challenges that an MSME faces after a disaster. This interruption is heightened by disruptions in the value chain and limited access to cash. The following graphic summarizes the causes and aftermath of such a business interruption below.

GIZ – RFPI in the Philippines commissioned the MSC study, “Disaster Risk Insurance for MSMEs in the Philippines” in 2018. The insights generated led to the development of MSME-focused insurance responses by insurers in the Philippines. MSC conducted the study across three regions in the Philippines: Luzon, Visayas, and Mindanao. The sample comprised 121 MSMEs, with 66% micro, 30% small, and 4% medium enterprises across multiple lines of business.

MSME- business interruption

Source: MSC analysis

Because of such disruption, MSMEs face directly as well as indirect financial losses. Direct losses include loss of assets, such as buildings, machinery and equipment, and loss of inventory. Indirect losses, on the other hand, are due to business stoppage, value chain disruption, unavailability of raw materials, and decrease in revenue. Overall, indirect losses from a catastrophe account for more cumulative losses than direct losses suffered.

In the aftermath of disasters, MSMEs usually need a cash infusion to re-start businesses. The study identified that on average, 34% of respondents relied on formal credit, such as MFIs and pawnshops, while 33% of respondents reported self-financing losses using their savings. Only 15% of respondents took financial support from informal sources, while 18% of respondents were forced to reduce their workforce to cut down on costs.

Savings are the most readily available source of funding. However, entrepreneurs rarely demarcate their savings. Therefore, they use the same savings to meet the needs of their household and business. As a result, we found these resources only helped MSMEs bridge an eight to 10-day business interruption period. Cost-cutting was also an option, but only for larger MSMEs with enough staff to downsize. Most micro-enterprises are generally family-owned or operated. Reducing their workforce is not an option. We also found that after a disaster, 10%-12% of the MSMEs surveyed did not recover and shut down permanently. These were mostly microenterprises, and these businesses could not withstand a disruption of more than 60 days.

Government ministries in the Philippines have developed policy-level responses to strengthen the resilience of MSMEs. The Department of Trade and Industry (DTI) has established a financing mechanism that facilitates access to credit for MSMEs in the aftermath of a disaster. The DTI further promotes business continuity planning as part of its business finance and management education campaigns called “Mentor Me”, which target MSMEs. The DTI also supports the development of risk financing tools, such as insurance for disasters. Our study also concluded that business interruption insurance would benefit MSMEs after disasters.

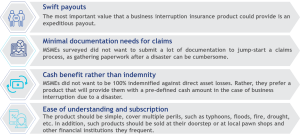

On the user front, MSMEs identified that an ideal business interruption insurance product should have the following features:

MSME identified features for business interruption insurance product

Source: MSC analysis

There are parallels for supporting MSMEs hit by COVID-19. MSC is currently undertaking a three-stage research study across eight countries in Asia and Africa to understand the nature and extent of the impact of the COVID-19 pandemic on MSMEs. The insights from the 2018 Philippines study correlate closely with initial findings from MSC’s dip-stick study of MSEs in eight countries. Some key support areas for MSMEs include:

- Make blended cash accessible, fast: It is paramount that MSMEs, especially microenterprises, have access to cash to survive this pandemic. MSMEs need a dedicated fund to meet their working capital requirements, as well as essential household and living expenses. Such a fund would offer blended loans—a mix of grants and credit. While the grants cover essential household expenses, the credit would be used to meet the needs of working capital. This is important to ensure that both businesses and families weather the storm, and MSMEs are not forced to use expensive credit for essential consumption purposes.

- Governments, MSME associations, and financial institutions must come together to administer the cash assistance identified above: To establish blended funds, grants should come from governments or international donor agencies that seek to assist the MSME sector. Local and international financial institutions should provide credit to these funds. These funds must be overseen by associations and chambers run by representatives of the MSMEs to ensure that the money is directed to the target sectors and segments. While registered, tax-paying MSMEs should have the first claim to relief. A portion of this can also be earmarked for informal MSMEs, which includes most micro and small enterprises. In the past, a lack of official recognition has made it challenging for MSMEs to access funds from state-run programs. One way to address this issue could be to allow unregistered MSMEs to self-certify to access the relief funds. In the long term, countries could introduce a low touch and paperlite registration for all microenterprises to allow them to qualify for support in the event of a disaster.

- Make assistance accessible to all businesses and value chains: In the pandemic, MSMEs that deal in non-essential items, such as cloth shops and small manufacturing entities have been hit much harder. Available assistance must be accessible to all MSMEs that need it. Value chains, both local and part of the wider network, have also been hampered severely and must be eligible to draw on assistance. Therefore, support to backend service providers like cargo transporters and storage facilities is an important piece of the puzzle to get the value chain back up and running quickly.

At the policy level, long-term resilience of MSMEs must be at the core of all measures to limit fall-outs from such shocks in the future:

- MSMEs must develop business continuity plans. Government agencies that promote MSMEs and support agencies should take the lead in helping MSMEs develop better risk management capacities. They should encourage MSMEs to:

- Develop rainy-day reserves to tide them over during business interruptions. This can be undertaken through the promotion of savings products for MSMEs with favorable interest rates. These promotions can be incentivized. One possible idea could be that future government relief would be defined multiple of the value of such savings.

- Have contingency plans in place to respond to business interruptions. These plans could take the shape of well-defined cost-cutting measures, as well as diversification strategies.

- A comprehensive multi-risk business interruption insurance product would help MSMEs become self-reliant and resilient in the face of hazards like disasters and pandemics, as well as other risks, such as fires and theft. Insurers and market facilitators should consider bundling business interruption insurance with business development loans. It is also crucial that such products are designed with user needs and context in mind. The characteristics of such insurance products should include quick claims assessment and automatic payouts based on directives issued by the government, as with some crop insurances. These products should ensure payouts are made immediately into the bank accounts of MSMEs after the government declares a disaster or a pandemic.

- Given the vulnerability of MSMEs to disasters and pandemics, there should be more reliance on digital access to financial services. For example, in our Philippines MSME study, none of the MSMEs interviewed reported using digital financial service platforms other than Internet banking services. Whether for credit or insurance, greater access to digital finance will create disaster- and pandemic-resistant pathways and provide speed and transparency. An example of this is in India where the government has made use of the JAM trinity (Jan Dhan bank accounts, Aadhaar ID cards, and Mobile payments infrastructure) to process 403 million transactions by 140 million of the low- and middle-income segment to access cash relief against the COVID-19 crisis.

Confronted with “grey swan” events, such as a disaster or pandemic, MSMEs face long business interruptions. The immediate response in such situations must be swift and blended. In the long-term, policymakers should focus on helping MSMEs devise business continuity and risk management plans by promoting risk reserves and business interruption insurance solutions. MSMEs must also adopt digital financial services because, as the current COVID-19 pandemic has shown, digital access remains largely functional when all other avenues have shut down. For now, however, we must focus on getting cash into the hands of MSMEs, and fast.

Reference note:

On March 11, 2020, the World Health Organization (WHO) declared COVID-19 a global health pandemic. Life as we once knew it has been suspended suddenly. Among those who have been hit the hardest are micro, small, and medium enterprises (MSMEs).

As per the IFC, an enterprise qualifies as a micro, small or medium if it meets two out of three criteria of the IFC MSME definition (employees, assets, and sales), or if an outstanding loan on its books falls within the relevant MSME loan size proxy

criteria of the IFC MSME definition

criteria of the IFC MSME definition

Platform economy across the globe

Platform economy across the globe