This note examines how the Indian MFIs should respond to save their industry – denial is no longer an option. It examines how MFIs need to improve transparency of interest rates, governance and operations; as well as analysing and documenting their social performance management. It looks at the role of a credit bureau and concludes that ultimately, MFIs will have to move towards 3rd generation microfinance, probably on the mobile money platforms.

Blog

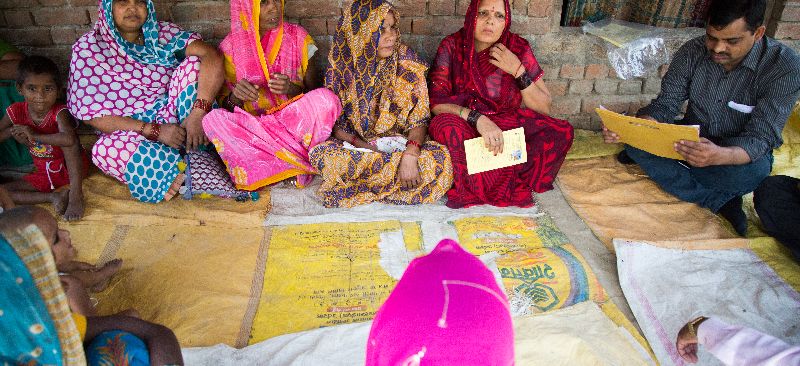

The Andhra Pradesh Crisis: What Should MFIs Do?

Clearly the microfinance, or better said “microcredit”, industry in India is undergoing a major shake-up. This note examines the nature of the shake-up and likely consequences including interest rate caps, sources of capital, equity valuations and the worst case scenario. It concludes that long-term the current turmoil in Indian microfinance may result in improved financial services for the poor – so long as they are easily accessible and not in high cost to operate areas. In the short run the options for poor people will shrink significantly – much to their detriment.

The Andhra Pradesh Crisis: Three Dress Rehearsals … and then the Full Drama

In the four years prior to the Andhra Pradesh crisis, Indian microfinance had three dress rehearsals for the final drama now unfolding. In Indian microfinance circles, these are known as the “three Ks” and each provided an important lesson and warning for the Indian microfinance industry. This note explores these and critically examines the responses of the microfinance industry.

Liquidity Management: Mobile Money

In this video, Ignacio Mas Deputy Director Bill & Melinda Gates Foundation, talks about stores acting as cash merchants and their basic need to periodically rebalance their cash and e-money holdings. He explains the basic options for doing so, including going to a bank branch.

Mobile Banking: Speed to Scale Part 2

In this video Daniel Radcliffe, Program Officer, Bill & Melinda Gates Foundation, describes how retail payment systems can reach a critical mass of customers. Daniel notes that agents need to be incentivised in order to encourage them to take up these activities.

Mobile Banking: Speed to Scale Part 1

In this video Daniel Radcliffe, Program Officer, Bill & Melinda Gates Foundation, talks about the fundamental factors that affect the growth and success of retail payment systems. He insists that remote payments add the ‘wow’ factor to mobile banking.