“Irregular availability of water is going to be the biggest hazard in future. In case of increased water supply, the piedmont zone and river lowlands are threatened by erosion and sedimentation while in case of decreased water supply, the upland surface is endangered by salinization, desertification, and drying-up of aquifers. Decline in food production will be the major problem.” – H. Saini Climate Change and its Future Impact on the Indo-Gangetic Plain (IGP), Environmental Science, 2008

“By 2050, variability in growing conditions due to climate change is projected to lower crop yields by 10 to 40 percent and total crop failure will become more common.” – Julie Mollins, Landscape, 2018

Buxar district lies on the south bank of the Ganges River between Varanasi and Patna. Droughts and unseasonal rainfall are critical risks to agricultural productivity in the district. And these risks are growing … rapidly. We cannot see these variations in weather as anything but the impact of climate change. If these are the early signs, the implications for the Gangetic Plain in the coming decades are deeply worrying.

“The weather is so variable—we do not know what to do. When we expect rain, we get none; and then suddenly, we get so much rain that all our crops are washed away. This is getting worse, and we are left helpless. We can no longer afford the fertilizer and pesticides we need in the seasons after a bad harvest. We are forced to purchase these in credit.” – Rice and wheat farmer in Buxar.

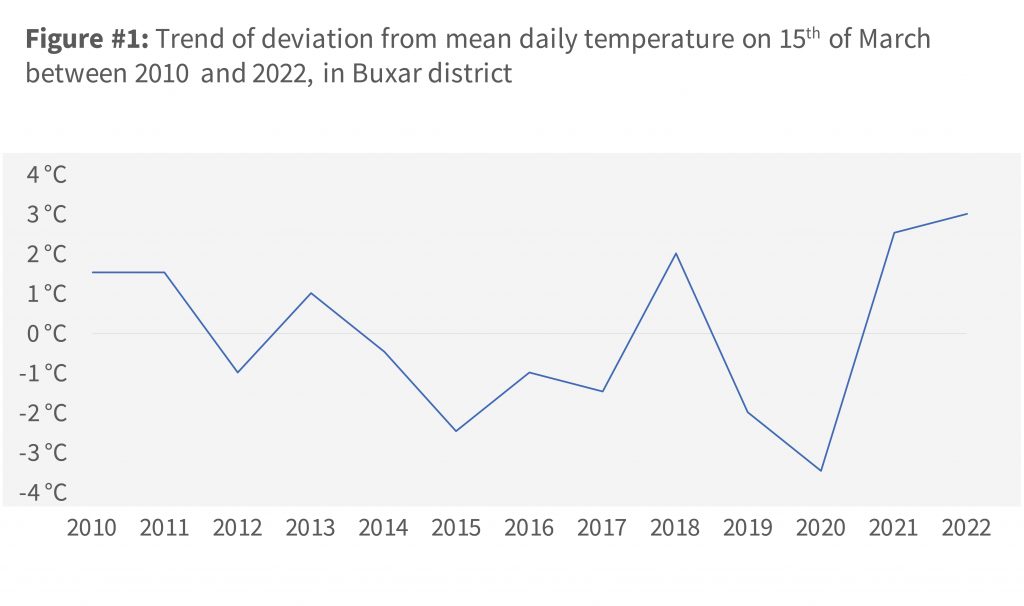

The spring temperature in the district is becoming warmer, and the variations are becoming larger.

- The daily mean temperature in the spring season (see Figure 1) has experienced a positive deviation in six of the past 13 years.

- In the past two years, the positive deviation in the mean daily has been higher than previously observed positive deviations.

- In the past two years, the district has faced intense heat waves in March, resulting in shriveled the growing wheat and thus, reduced harvest yields.

Furthermore, rainfall has become irregular in the past two decades.

- Between 1989 and 2018, the June rainfall in Buxar was highly variable (coefficient of variation = 92.4%).

- In the same period, the July-October monsoon rainfall in Buxar was also highly variable (coefficient of variation = 30.4%).

“Rains have become very irregular. When the rains start, we sow paddy. If we have a long dry period afterwards, the entire crop dries up due to insufficient water availability. We have to replant again. This phenomenon is becoming more frequent.” – Rice farmer from Buxar

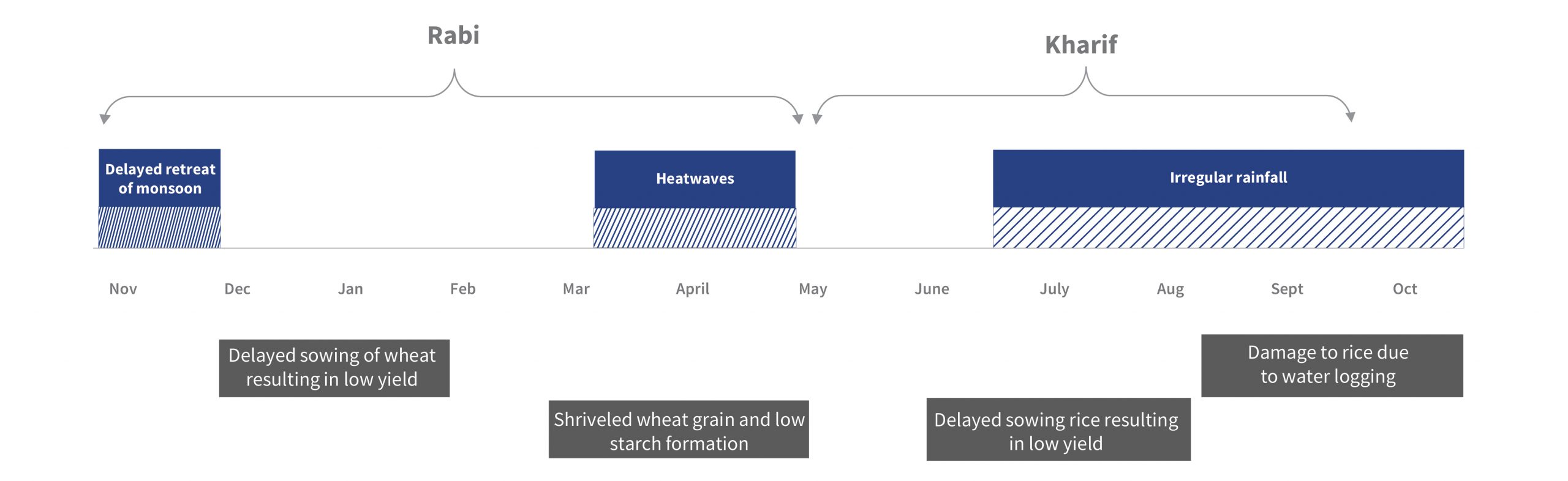

Figure 2 highlights how these slow-onset climate-change stresses affect farmers and their productivity over the year.

Figure 2

Figure 2

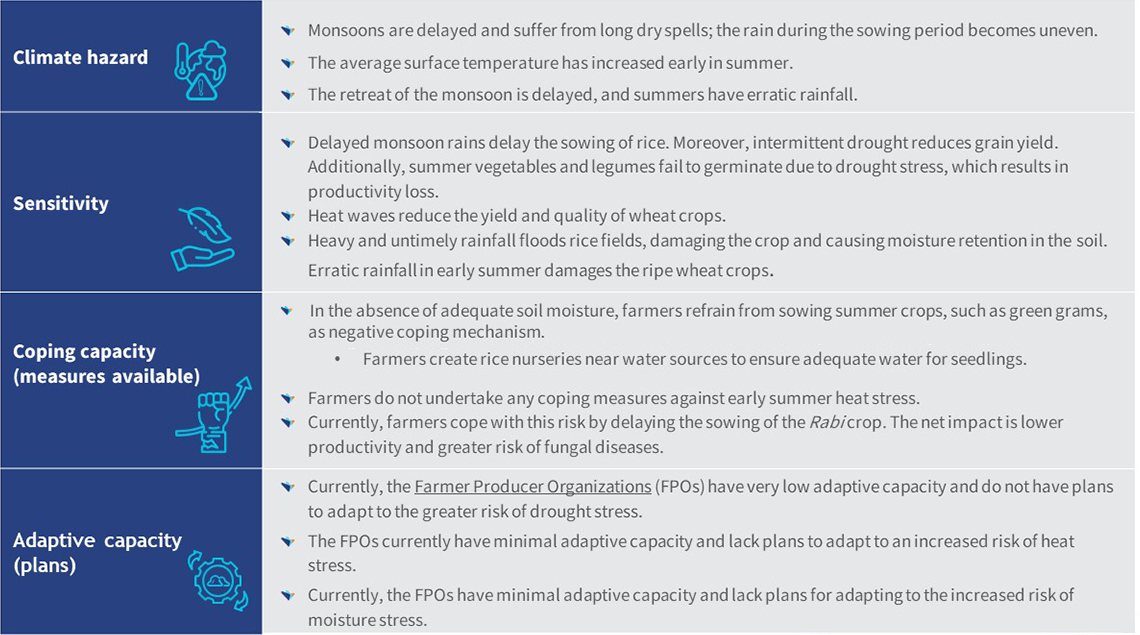

Table 1 below highlights the impact of these significant shifts in climate in Buxar. Similar impacts are likely to be replicated across much of the Indo-Gangetic plains, home to 900 million people or one-eighth of the world’s population.

Table 1: Impacts of climate hazards

Table 1: Impacts of climate hazards

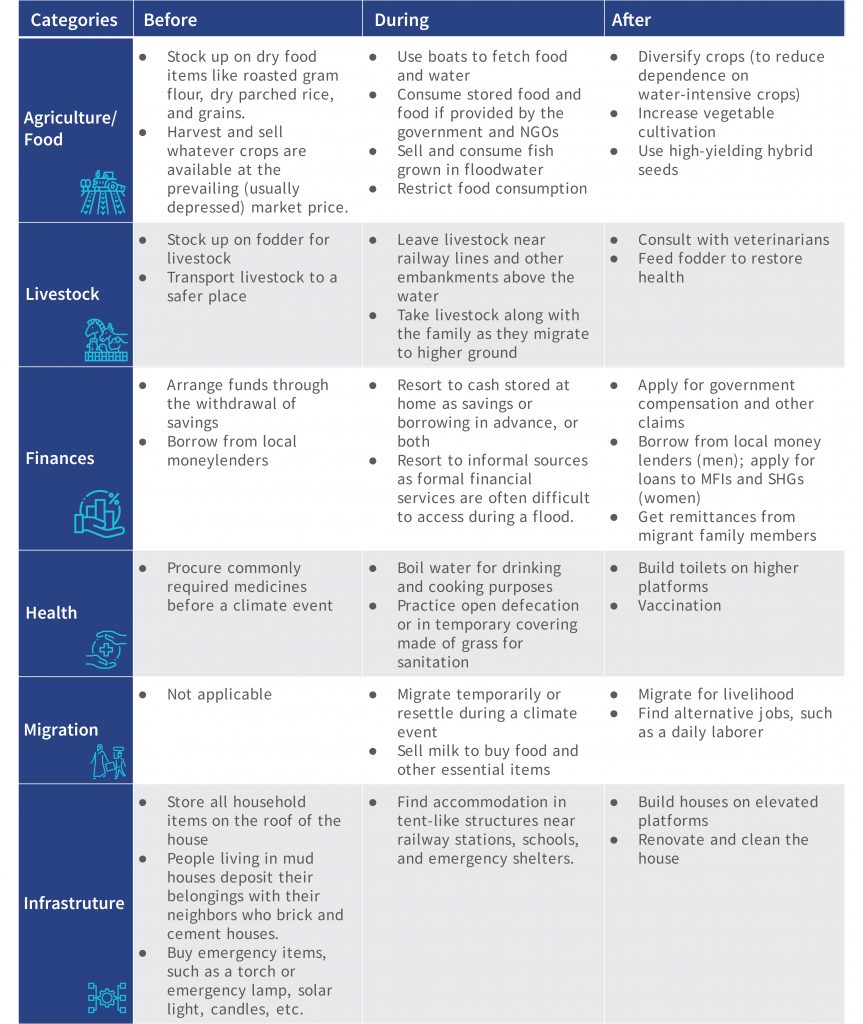

In Buxar, farmers are struggling to cope with the changing conditions and adapt to them (see Table 2 below). Yet, significant annual variation in rainfall and temperature further erodes farmers’ adaptive capacities (see Figure 1 above). In some cases, farmers’ coping mechanisms risk maladaptation. For example, if farmers are compelled to delay sowing of the Rabi season crop, they risk reducing the yield, and the crop becomes prone to fungal disease.

“The only solution we have to the rainfall variability is to delay the sowing of crops. We are not aware of any other solutions to this situation.” – Rice and wheat farmer from Buxar

Farmer Producers Organizations (FPOs) are yet to spearhead collective action to build resilience to climate change impacts, but they could be the key to a more effective response.

“FPOs can mobilize resources to provide suitable tools and infrastructure to fight variations in the climate.” – FPO member in Buxar

So what should farmers and FPOs do?

FPOs should seek to play a central role to promote and facilitate farmers’ adaptation to climate change. In the short run, FPOs could serve as knowledge and communication centers to drive better climate-resilient practices among their members and serve as conduits for credit for farmers. Farmers can use such credit support to finance farm inputs and drive the adoption of climate-resilient agricultural practices to protect against multiple shocks and stresses. In the medium and long term, FPOs will need to play a more prominent role to hire farm equipment and emerge as aggregation and cold-storage centers.

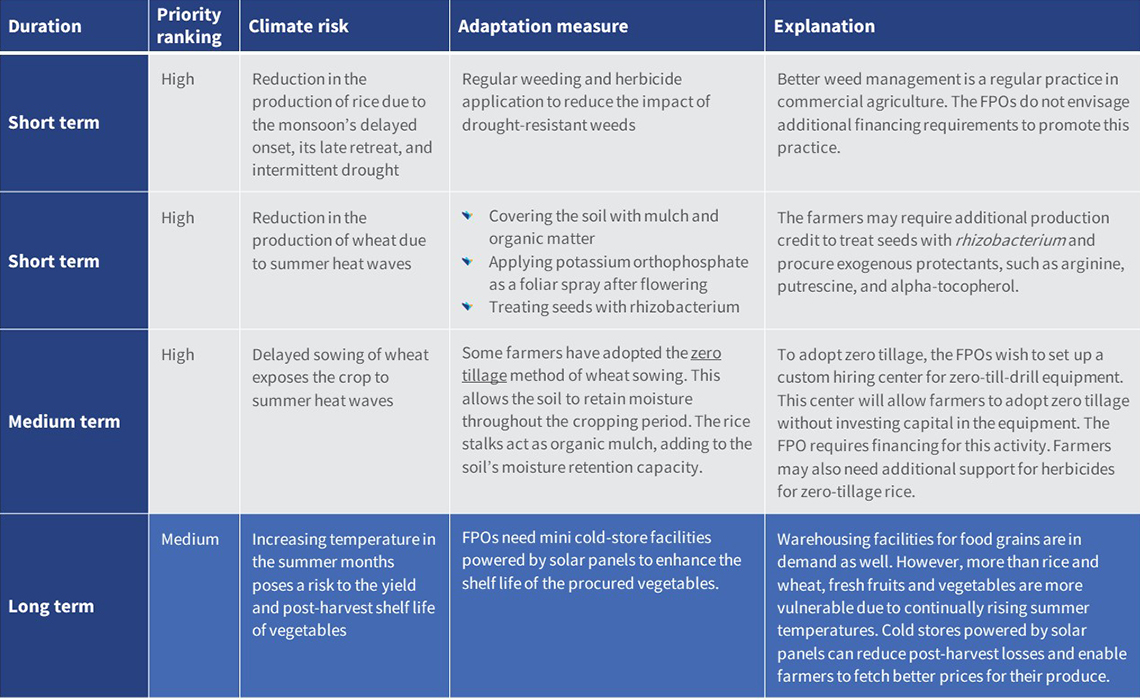

Proposed solutions to many problems arising from climate change are already available among the local scientific community, such as universities and state-owned research establishments like Krishi Vigyan Kendras (KVKs). Table 2 describes examples of the solutions recommended by these institutions.

However, farmers are yet to adopt these solutions due to the:

- Lack of awareness and technical knowhow, particularly of new techniques like zero tillage;

- Lack of access to appropriate financial services;

- Inertia or status quo bias as current practices have been used for generations;

- Mistrust of new ideas.

“These farming practices have been in our family for generations—we cannot take the risk of trying new ideas. We have heard of so many people trying new things and failing. We feel what we do is right for our farms.” – Rice farmer from Buxar

FPOs can work as a platform for information and training on these new solutions, develop new business models (such as renting out tools), and demonstrate success stories. FPOs need to be adequately incentivized to empower their members to respond to climate change.

Table 2: Responding to climate risks—solutions recommended by agricultural experts

Table 2: Responding to climate risks—solutions recommended by agricultural experts

“It is in the FPO’s own interest to support its member farmers through information, training, and access to new technologies to meet the challenge of climate change.” – Director of Ravidas Baba Farmers Producer Company Limited, Buxar.