To build upon the digitization of the Public Distribution System (PDS) and with a focus on beneficiary-centric reforms, the government launched a new scheme – Integrated Management of PDS (IM-PDS), also known as One Nation One Ration Card (ONORC) or portability, in April 2018. Recently, the Finance Minister announced that the scheme will be rolled out by March 2021.

Under ONORC, PDS beneficiaries can lift their entitled food grains from any fair price shop (FPS) across the country with their existing ration cards. ONORC builds on the reforms under end-to-end computerization of PDS to digitize beneficiary database and supply chain mechanisms, among others.

While ONORC remains a work in progress, several states have implemented intrastate portability (within the state). The adoption of portability in a state is primarily dependent on their readiness and progress under end-to-end computerization of PDS. However, national portability will need integration of existing PDS portals of states/UTs with the central PDS portal. This means that all the states participating in interstate portability (between states) must have basic digital readiness.

Readiness for all-India portability under PDS?

As of January 2020, the Aadhaar details of about 83% of the beneficiaries have been seeded with their ration card details in the digital database across India. Moreover, only 89% of the total FPS across India, have been automated with the installation of an e-PoS device. Under digitized PDS, beneficiaries are provided with food grains only after their biometric authentication through Aadhaar on the e-PoS devices at the FPS. In the absence of a digital database and automated FPS, the beneficiaries will be unable to access portability.

Moreover, before moving to interstate portability, it is also intended that the states implement intrastate portability. As of January 2020, the intrastate portability has been either partially or fully implemented only in 18 out of 36 states/UTs in India.

In April 2020, over 11 million transactions were carried out under intrastate portability whereas, only 351 transactions were through interstate portability. The differential use of intrastate and interstate portability by beneficiaries can be attributed to a low level of awareness on interstate portability facility amongst beneficiaries as well as FPS dealers, as assessed by a pilot study conducted by MicroSave Consulting in September 2019. Intrastate portability provides beneficiaries the convenience to access food grains at FPS of their choice.

Simultaneously, FPS dealers are able to earn an extra commission for an increase in the number of ration card holders uplifting food grains from their shop. While the FPS dealers receiving a lower turnout of beneficiaries, earn a lesser amount of commission. Under portability, the FPS dealers are also met with unpredictable demand, which could possibly lead to a shortage of food grains as well.

Additionally, on the operational front, most of the states follow different timelines and processes for the allocation and distribution of food grain stocks to FPS, this could act as a hindrance in the process of reconciliation and allocation of stocks.

The way forward

It is evident that beneficiaries have utilized intrastate portability more than the interstate. However, a shift towards a national rollout of ‘One Nation One Ration Card’ will need a lot of work across participating states and at the center, for which the government will have to ensure the following:

Fix strict timelines for the digitization of PDS and Aadhaar seeding of the PDS database.

Adopt the best practices from states which have effectively automated their PDS and draft guidelines on fixing the timelines for the uptake of food grains by beneficiaries, stock reconciliation, and on FPS dealers request for extra food grain stocks.

The government should explore ways to compensate the FPS dealers through a model with a fixed and a variable component for their commission.

Respective state governments should assess the data on intrastate portability transactions and optimize the locations of FPS.

Awareness regarding interstate portability and its operational details should be effectively communicated to beneficiaries through SMS, posters at FPS, and imparting of information through FPS dealers.

While adopting the above measures with regards to portability, it should further be implemented in a phased manner across India prioritizing states with a high migrant population.

The blog was first published on Zee Business on 23rd of May, 2020

Dhanshree is a 24-year-old entrepreneur from rural Maharashtra, India. She has a postgraduate degree and has been running a candle-making business for the past three years. Besides making candles, which is a seasonal business, she also provides tailoring and photo editing services to her customers. On a typical day, Dhanshree shifts between her various businesses as she completes orders and studies for her upcoming government job examinations. Despite all these responsibilities, she is also expected to complete her household work.

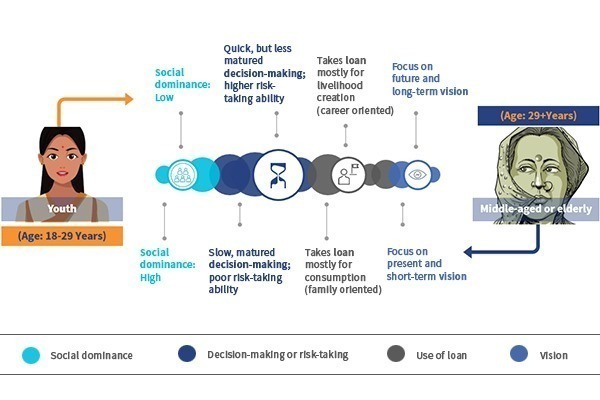

While most of us struggle to find time to do one job properly, this young woman from the Indian hinterland manages multiple roles efficiently. A recent study by MSC (MicroSave Consulting) sheds light on how someone like Dhanshree accomplishes this. The study spanned October, 2019 and January, 2020 and involved more than 200 female members from multiple self-help-groups based in Maharashtra, Rajasthan, and Uttar Pradesh. When compared to older members of self-help groups (SHGs) aged above 29 years, Dhansheree and her younger peers, who fall into the 18 to 29-year age group, are:

The Internet plays an immense role in Dhanshree’s life. Her active use of the Internet and social media facilitates her ability to multitask. She uses WhatsApp to sell and market her designs and tailoring skills while using a “Google My Business Account” to connect with intermediaries 200 kilometers away to sell candles during festival seasons. She also works with different online tools to edit photos and even subscribes to free lectures on YouTube to prepare for her government job exams. With effective access to information, she saves time, supplements her family income, and is on the path to achieving her life’s dreams.

Dhanshree is not alone. Like her, many young and driven women from various self-help-groups are motivated to work tirelessly toward their goals and make life better for themselves, their families, and their communities.

What makes these young female members different from others?

An optimistic outlook and a desire to seek out new opportunities set these women apart from the rest. These young members are more enthusiastic about exploring new opportunities and have access to digital technologies that expose them to multiple sources of information.

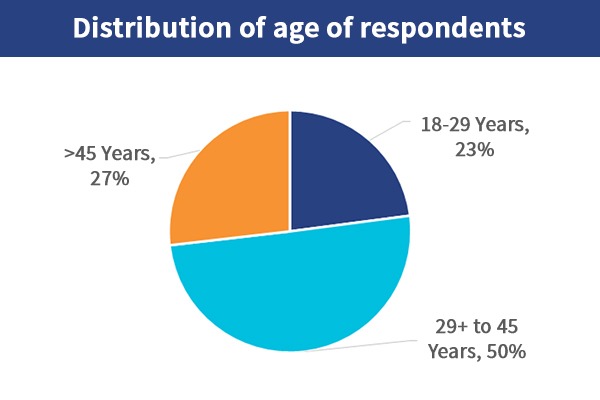

MSC obtained responses to a qualitative survey from female self-help group members representing different age groups including young (18 to 29 years old), middle age (29+ to 45 years old), and old age (45+ years old).

The respondents from the middle-aged category expressed a limited desire to take calculated risks, start enterprises, or pursue livelihood opportunities owing to their existing responsibilities to grow their families and care for children and the elderly.

Respondents from the old-age category were least motivated to grow personally by taking calculated risks. They took part in SHGs mostly to socialize and engage in networking.

Hence, young female SHG members represent the promise within the SHG movement. They are ready and eager to utilize the group and work hard to improve their standard of living.

The thought process of young SHG members differs from their elders; they are more enthusiastic about exploring new opportunities

Profile assessment: Young vs. middle-aged vs. elderly

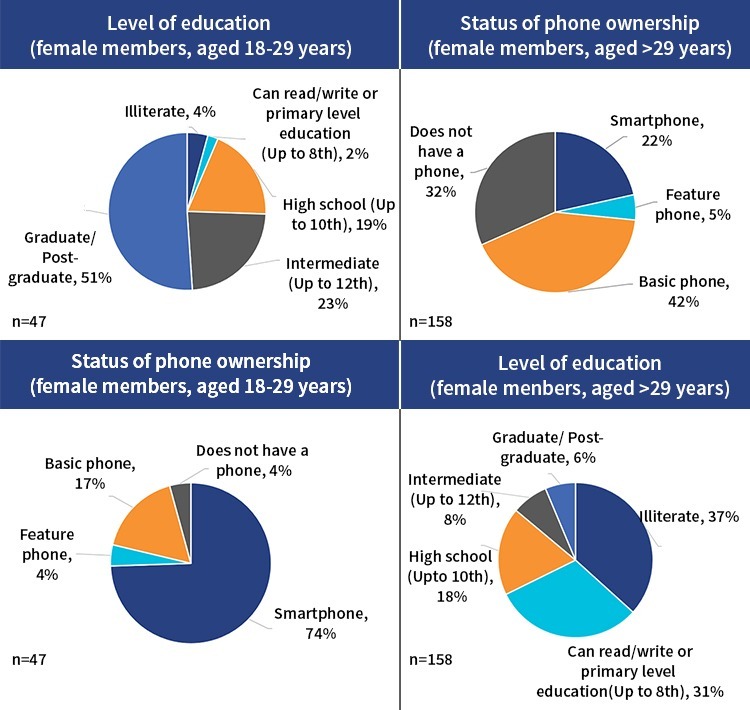

The profile assessment of young female SHG members in our study shows that they are well ahead of the middle-aged and older members in terms of digital literacy, awareness of formal financial mechanisms, as well as access and usage of savings mechanisms. The following infographic illustrates this in detail.

Why do female youth SHG members struggle to make a mark?

Former UN Secretary-General and Nobel Peace Prize laureate Kofi Annan once said, “Any society that does not succeed in tapping into the energy and creativity of its youth will be left behind.” With 27% or more than 110 million women in rural India falling into the age group of 15 to 29 years, SHGs in India present an opportunity for them to channel their energy and vision.

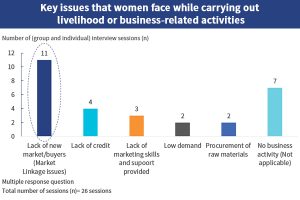

We often see that more than ever before, young rural female SHG members are more engaged in social, financial, and civic issues that affect their communities. During our research, we found that, for the most part, young female SHG members took care of all book-keeping activities and bank-related work for the group. However, when it comes to self-growth, these young members find it difficult to seize opportunities to lead livelihood activities due to a range of complex socioeconomic issues. Our interactions with many of these young female members suggest that in their start-up activities, many lack proper access to markets and human resources, are unable to promote their products, and subsequently face low product demand.

Key considerations for young female SHG members include:

New avenues of earning:

When asked, around half (49%) of young female members showed an interest in new avenues of earning that go beyond opening up a grocery shop or starting a small trading business. Instead, these women sought help to establish group-owned enterprises in their local communities. “There may be hundreds of different ways in which we can generate income by working in our locality. We want to know which business opportunities we can explore in our village. We are not equipped with the knowledge and information needed before selecting and starting a business venture,” said a 27-year-old SHG member from a village near Agra, Uttar Pradesh.

Better “access to markets” for women:

Significant improvements in “access to markets” are needed for SHG members to be able to access livelihood opportunities and create sustainable development. Many young SHG members who have started businesses have faced problems and economic losses due to poor access to markets. “Access to finance is not a problem for me but access to markets is. How can I sell and deliver my handmade products in far off places? Why do I have to depend on my brother to sell these items? He can easily roam around day and night on his motorbike but I cannot. It is difficult for young women—we have some limitations,” rued a young SHG member who is running a business selling handmade paper envelopes.

The structure of the market and its networks—relations between producers, market intermediaries, and consumers

Producers’ skills, information, and organization—an understanding of markets, prices, and trading protocols

Availability of resources (the need for “woman-power”):

Demands within local communities dictate which products and services small businesses offer. These small businesses generally focus on a small geographical area and utilize local resources, such as raw materials, local talent, and labor.

Many young female SHG members encounter challenges while procuring resources from their local markets. The most significant of these is human resources, namely, the availability of like-minded women who are ready to join start-up businesses. Due to a dearth of human resources, many businesses fail to achieve sustainability. This scarcity is largely attributable to behavioral biases that restrict women from pursuing livelihood opportunities.

Two young, like-minded SHG members recalled how they managed to earn a good income by setting up a small snack stall for a month during a festive season through a small investment and collaboration. “We need more women members who must be ready to work with us. All of us can contribute some money at the start to establish a food business. We all are good at something and I believe that if we come together, we can do wonders,” said one of the partners.

Training and development:

Although most of young female SHG members are digitally literate and financially aware, they lack specific digital finance skills and capabilities essential to run a business. Most find it difficult to decide which business opportunities to pursue. While they understand that the decision to launch a livelihood activity should be market-driven, they struggle to gauge which business has the potential and what the required level of expertise and scale should be.

These members require training in the areas of assessing local demand to identify enterprise opportunities, financial planning and risk management, resource planning, and marketing skills—branding and design elements.

Let us help young women to lead and succeed

The development of young women through SHGs could address unemployment rates directly among rural women. The National Statistical Office (NSO), which conducts India’s Periodic Labor Force Survey, found that the unemployment rate among rural female youth (aged 15-29) was 13.6% during 2017-18. If both state and central governments want to close this unemployment gap, SHGs offer a ready medium through which this can be accomplished. Besides, these young female members of SHGs can further help the central government to achieve its vision of making India self-reliant.

Thus, we note that young female SHG members demand more from the SHG model. They seek to utilize the model for not only financial services but also for livelihood development. We have learnt that creating scalable and successful SHG models involves focusing on the younger SHG members. As young members are the future of SHGs, the development community must empower these women. It is important to remember the words of Kofi Annan, “From creating start-ups to igniting revolutions, young people have been toppling the old structures and processes that govern our world. Just imagine what solutions might be found if young people are given the space and encouragement to participate and lead.” SHGs would be well suited to follow this advice.

[1]Micro Solutions for Macro Crisis: Sustaining small and marginal farmers in Andhra Pradesh. A report by the Centre for Sustainable Agriculture, Hyderabad, India.

How much time will it take to normalize MFI operations? The answer has INR 2,000 billion (~USD 26 billion) riding on it. We could compare the COVID-19 crisis with the Indian government’s banknote demonetization exercise of 2016 when currency notes of higher value ceased to be legal tender. Demonetization disrupted significant parts of the Indian economy for three months and the recovery process was protracted and difficult.

Demonetization had the most adverse impact on daily wage laborers and artisans, who were almost entirely without work for two months. The income of rickshaw, auto, and taxi drivers also declined significantly, as they depended on cash payments for their income. Sellers who offer essential products, such as grocery, dairy, and medicines continued to receive constant inflows, though sale volumes decreased. In contrast, the income of sellers of non-essential products, such as cosmetics and restaurants shrunk by more than half.

Amid the uncertainty, salaried employees decreased their consumption of discretionary items, while households focused on thrift and restricted their purchases to essential items. Yet in many ways, the impact of demonetization on the agricultural sector was lower, as seen now with the COVID-19 crisis. Most farmers were able to sell their produce at prevailing rates despite concerns that their income might diminish in the future as homegrown seeds were used for sowing instead of buying seeds from the market.

This pattern is similar in many respects to the way in the COVID-19 crisis has been affecting India’s economy – see MSC’s analyses on “Food security: How are agriculture and the corner shops faring amid India’s lockdown?” and “Micro and small enterprises: Will the pandemic put an end to their business?”. Yet there are important differences. Demonetization was a time-limited and relatively short-term event, whereas a great uncertainty surrounds how long, how hard, and how often the COVID-19 crisis lockdowns continue. This uncertainty makes predictions difficult, so we write this blog in the spirit of optimism that the crisis and lockdown will also be time-limited to around three months.

We have examined three aspects of MFIs to analyze the impact of COVID-19:

Cash flow in the near to medium term;

Sustainability;

Staff psychology and management.

The cash flow for MFIs

The situation now

Repayments are the largest cash inflow for MFIs, followed by borrowings from financial institutions and fees from the off-book loan portfolio. The largest cash outflow is loan disbursement, followed by repayment to lenders and off-book portfolio, payment of salary and wages to employees, rent, utilities, and statutory dues, such as tax and contributions towards social security.

Loan repayments are a consistent and reliable source of cash inflow. In India, this has ground to a complete halt from 25th March 2020, because of a national lockdown. Lending institutions are also on a wait and watch mode – fresh loans are unlikely in the prevailing situation. On the other hand, MFIs still need to maintain scheduled cash outflows for salary and wages, payment of rent and utilities, payment of loan installments to lenders, and for payments toward off-book portfolio—particularly securitization and direct assignment. Though the Reserve bank of India (RBI), the country’s apex bank, has announced a moratorium on all term loans, banks were divided on whether NBFCs and NBFC-MFIs are eligible for a moratorium.

This seems to have been settled for now, with State Bank of India, the largest lender, agreeing to extend a moratorium. Hence, MFIs that struggled in the first month have received a breather. However, the struggle is unlikely to end, especially for small and mid-sized MFIs and the overall impact will vary. The smaller players face major challenges, while large MFIs, with well-capitalized books, may weather the storm marginally better.

The probable situation when the lockdown is lifted

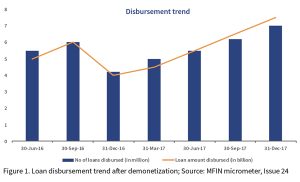

Over the years, MFIs have proven their resilience. During demonetization, repayment rates recovered from 50% to 80% within a month and settled at upward of 90% within three months. With this as a reference point, we can hope that repayment rates to MFIs will bounce back in the range of 90% within 3-4 months. This may rise further over a time horizon of, say, six months. Slowing down fresh loan disbursements will be an obvious strategy for MFIs, particularly in the first few months, which should allow them some space to manage cash flows.

Sustainability

Almost without exception, all MFIs revived after the three months of chaos following demonetization. MFI commentators think that it will take 12 to 18months for a full rebound, depending on the extent of the problems post the initial lockdown. Moves towards normalization will only be possible after the lockdown ends and field staff can move unhindered again. Yet given the nature of the virus, there is a real risk of second spikes and possibly repeated and localized lockdowns. These have the potential to disrupt the recovery further.

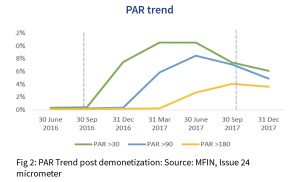

Portfolio at risk (PAR) will shoot up initially. It will gradually decline over 2-3 quarters once full-fledged operations resume. During demonetization, it took two quarters for PAR (>90 days) to start its downward journey. Fig.2 presents the PAR trends during and after demonetization.

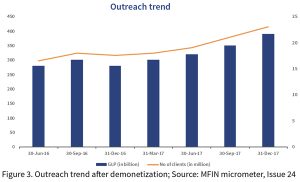

Under the present lockdown, the intensity of the problem may be in line with the challenges that demonetization had presented in 2016. Post demonetization, MFIs had to write-off5%-10% of the book. However, the increased demand for credit had compensated for losses (see Fig. 3). Post demonetization, the demand for credit shot up as customers needed the liquidity to re-establish their business.

We may expect a similar outcome this time around. Of course, clients will need additional time to repay their current loans. The moratorium may have to be extended and installments staggered. However, most of the credit outstanding will flow back. MFIs in India have some experience of dealing with stresses in customer liquidity, which should come in handy in managing the current situation.

Staff psychology and its management

Operations staff, particularly branch managers and field staff, will play a pivotal role in managing the field once the lockdown lifts. The post-lockdown period will present additional challenges. The fear of infection from the coronavirus will play on the minds of field staff. MFIs will have to address this psychological fear upfront and offer a safety net in the form of insurance cover or support, or both, in the event of hospitalization. Plenty of rumors will fly around, both at the level of clients and among field staff. MFIs must over-communicate – or rumors will fill the void. Three areas where MFIs will have to focus on include:

Movement in the operational area

This may be the biggest challenge for staff when they will begin moving in their respective operational areas. In India, the government has divided districts into green, orange, and red zones based on the prevalence of COVID cases. Movement will continue to be restricted in red zones. Moreover, the situation is dynamic and a green area can slip into orange or red. We are not yet out of the woods.

Dealing with customers

MFI staff will have to deal with customers who have now been traumatized by the loss of income. A few may have faced medical emergencies during this period. Understanding customer psychology and dealing with them appropriately will be key. Here, the senior staff will have to handhold field staff and keep channels of communication open. Branch staff will be able to draw from the experience of senior staff at the head office and zonal or regional offices. Feedback or information from the field should be turned into advisories quickly for wider dissemination across the organization.

Furthermore, MFI staff have a critical role to play as communicators on hygiene and role models for their clients. A pandemic of misinformation has already permeated the villages—MFI staff are uniquely positioned as respected opinion leaders to counter these dangerous and damaging rumors, half-truths, and lies. Both clients and staff are at significant risk of infection as they collect and count cash—indeed group meetings could become the dreaded “super-spreader” vectors for the virus.

Therefore, MFI staff need to model and demonstrate best practices in to protect themselves and educate their clients. To help with these issues, MSC has developed two comic books to inform and educate both clients and staff – MFI client awareness and MFI employee training. These are free to download and available in English, Hindi, and Bengali at the time of writing.

Besides, as the pandemic runs its course, the government will want and need to communicate additional information to help the country recover and return, cautiously, to a new normal. MFI staff can and should play a critical role in these communication efforts.

Dealing with external entities

MFIs deal with poor and vulnerable clients. Political leaders at the lower levels find MFI clients to be easy pickings as they try to create a following in local communities—particularly with promises of loan waivers. Over the years, MFIs have learned to deal with this problem better but it is unlikely to go away completely. The lockdown and the consequent economic stress will make clients vulnerable to overtures from such external interest groups. MFI associations will have to play a critical role in dealing with such challenges.

Indian MFIs have weathered many challenges in the past. The Andhra Pradesh microfinance crisis of 2010 and the demonetization in 2016 disrupted operations. However, in both cases, MFIs bounced back and emerged stronger. The lockdown enforced to control the spread of coronavirus in 2020has been the most severe crisis to hit the sector. Hopefully, with some deft financial and people management, MFIs will once again emerge resilient and ready to provide valuable credit services to their millions of clients across the cities, villages, and far-flung frontiers of the country.

Technology has the potential to increase employment rates amongst youth, especially in informal work. In 2019, a report on Gig Economy estimated the size of the gig economy (access to work online) in Kenya at USD 109 million, employing over 36,000 workers. The report further states that based on the current investment the gig economy is witnessing, the sector is projected to grow by 32% in the next five years, to a value of USD 345 million and will employ over 93,000 workers. The informal sector in Kenya has consistently represented over 80% of the workforce. The use of technology provides a significant opportunity to offer jobs and employment to the informal sector.

The current COVID-19 pandemic has just outlined how vulnerable job and social security is for gig workers. CGAP reports that most workers on platforms, offering artisanal and personal services, are seeing up to 90% reduction of business for them. Most have had to dig into their savings, if any, to take care of their living expenses. Those without savings are finding it hard to cope with the lockdowns. Gig work also does not fall within the customary contractual structures and grievance mechanisms provided by traditional formal employment. Insurance, as an example, has traditionally targeted the formal sector. There are very few insurance companies that offer adequate and accessible products to gig workers. The nature of gig work makes offering insurance products to the gig workers much more difficult. Gig work varies significantly based on the technical platform, type of work, and risk exposure. Online gig workers are, in particular, more complicated to insure due to the on-demand and unpredictable nature of gig work.

Several gig platforms such as Lynk based in Kenya provide professional services through matching customers to a pool of blue-collar workers. Lynk has a focus on generating employment opportunities for youth and is on track to achieve this with over 60% of its workers in the youth category. A large portion of their workforce, however, have inadequate access to insurance. Through support from the Mastercard Foundation, MSC supported the development and delivery of microinsurance products to serve gig workers. In our previous blog, we defined the platform economy and explored the challenges faced by gig workers. Poor and irregular pay, unstructured contracts or lack thereof, and unpredictable cash flows are some of the leading reasons that make gig workers a segment that is an ill fit for traditional insurance companies.

Mutiso, a carpenter who lacked health assistance when he needed

Mutiso is a twenty-eight-year-old carpenter, who runs a furniture workshop on one of the busy roadsides in Nairobi. He joined Lynk as a pro, three years ago, upon recommendation from a friend. As his regular business had issues of seasonality, he envisaged that these gigs on the platform would lead him to regular customers and smoothen his cash flow.

Mutiso has been very careful with his work that involves dangerous tools to cut, shape, and build furniture. He rarely had an accident at work. However, two years ago, as he was sawing a large trunk of wood to make a table, he moved the log too fast, and the saw got to his hand. He cut half-way through his forearm. This injury put him out of work for six months. He had no source of income during the period and no health insurance. It cost him over KES 200,000 (USD 2,000) just for the hospital bill, and he had to rely on friends and family to be able to pay for his treatment.

How can we create microinsurance product concepts for gig workers and platforms?

Behavioral research and human-centered design can be applied to develop product concepts that are adequate, accessible, and meet the needs of the gig workers. Our research shows that most gig workers have no access to formal insurance, although they recognize and experience several risks. Also, our assessment shows that most traditional products provided by insurance companies are not adequate to serve the unique needs of the gig workers’ segment.

The core use cases of insurance for young gig worker included the following:

Developing microinsurance product concepts for gig workers

Based on our research, key insights to develop microinsurance product concepts for gig workers include:

The flexibility of the worker’s gigs: Gig workers would like to be able to afford a cover before they commence their gigs. Thus, the product should have an on-demand cover that the gig workers may pay for when carrying out gigs.

Incorporate the use of technology: Considering the tech-savvy nature of the youth gig workers and need for an efficient experience, providers must digitize and embed technology at each stage of service. Thus, the core processes such as enrollment, premium payment, and claim settlement should be digitized.

Affordable and dynamic pricing: Differential pricing and payment models could make it easier for the gig worker to afford the premiums. To reduce the cost of access to insurance, a liability sharing model where both the gig platform and the gig workers contribute towards the premium payment. The flexibility of gigs demands a dynamic pricing model where the gig workers may split and pay premium across the predicted number of gigs.

Developing a microinsurance model that works for gig workers

Based on our research, an insurance provider is piloting an umbrella personal accident product for the gig economy, to include the following attributes:

On-demand access: Together with the platform, the provider has assessed the overall platform’s insurance needs to develop and deliver an umbrella Personal Accident (PA) cover for all the gig workers associated with the platform. The cover is applicable during the working period and protects gig workers against all the risks associated with the gigs. The provider is offering work injury benefits to all the gig workers in line with existing labor regulations.

Pooled and agnostic: The pooled insurance product covers a specific and pre-determined number of workers at any given point of time. The number depends on the history of active daily workers on the platform but does not prescribe the specific individuals. This approach acknowledges that from the pool of the gig workers, not all of them will work on the same day or at the same time, and it is certain that not all workers are at risk every day. If only 400 out of 1,000 workers are active every day, the platform pre-pays insurance for only the daily active workers. Consequently, the premium paid per worker is significantly reduced.

Through behavioral and human-centered research, a provider may understand the dynamic nature of work, risks that affect them, and practical use cases, and may design effective microinsurance product concepts for gig platforms and workers. The COVID-19 pandemic has brought to life the reality that informal workers unjustifiably get the short end of the stick concerning financial services and specifically insurance. Regardless of informal workers’ equitable and unappreciated contribution to the economy and society, our embrace of technology in the gig economy can indeed extend the benefits enjoyed by formal economy workers to the informal workers.

The abridged version of this blog was first released on NextBillion.

In 2018, MSC conducted a study with MSMEs in the Philippines to understand how they are affected by disasters. In the study, we assessed their coping mechanisms in the aftermath. The Philippines has historically been on the receiving end of disasters, such as typhoons and floods. MSMEs in the Philippines have had to respond to disruptions caused by these disasters, develop coping mechanisms, and work their way out of these challenges. In this blog, we will reiterate insights gathered from the study and draw parallels to identify pertinent responses for the ongoing pandemic.

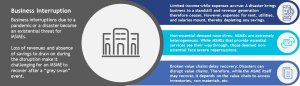

An interruption in businessis the culmination of all the challenges that an MSME faces after a disaster. This interruption is heightened by disruptions in the value chain and limited access to cash. The following graphic summarizes the causes and aftermath of such a business interruption below.

GIZ – RFPI in the Philippines commissioned the MSC study, “Disaster Risk Insurance for MSMEs in the Philippines” in 2018. The insights generated led to the development of MSME-focused insurance responses by insurers in the Philippines. MSC conducted the study across three regions in the Philippines: Luzon, Visayas, and Mindanao. The sample comprised 121 MSMEs, with 66% micro, 30% small, and 4% medium enterprises across multiple lines of business.

MSME- business interruption

Source: MSC analysis

Because of such disruption, MSMEs face directly as well as indirect financial losses. Direct losses include loss of assets, such as buildings, machinery and equipment, and loss of inventory. Indirect losses, on the other hand, are due to business stoppage, value chain disruption, unavailability of raw materials, and decrease in revenue. Overall, indirect losses from a catastrophe account for more cumulative losses than direct losses suffered.

In the aftermath of disasters, MSMEs usually need a cash infusion to re-start businesses. The study identified that on average, 34% of respondents relied on formal credit, such as MFIs and pawnshops, while 33% of respondents reported self-financing losses using their savings. Only 15% of respondents took financial support from informal sources, while 18% of respondents were forced to reduce their workforce to cut down on costs.

Savings are the most readily available source of funding. However, entrepreneurs rarely demarcate their savings. Therefore, they use the same savings to meet the needs of their household and business. As a result, we found these resources only helped MSMEs bridge an eight to 10-day business interruption period. Cost-cutting was also an option, but only for larger MSMEs with enough staff to downsize. Most micro-enterprises are generally family-owned or operated. Reducing their workforce is not an option. We also found that after a disaster, 10%-12% of the MSMEs surveyed did not recover and shut down permanently. These were mostly microenterprises, and these businesses could not withstand a disruption of more than 60 days.

Government ministries in the Philippines have developed policy-level responses to strengthen the resilience of MSMEs. The Department of Trade and Industry (DTI) has established a financing mechanism that facilitates access to credit for MSMEs in the aftermath of a disaster. The DTI further promotes business continuity planning as part of its business finance and management education campaigns called “Mentor Me”, which target MSMEs. The DTI also supports the development of risk financing tools, such as insurance for disasters. Our study also concluded that business interruption insurance would benefit MSMEs after disasters.

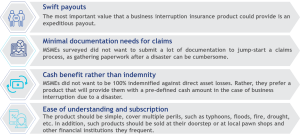

On the user front, MSMEs identified that an ideal business interruption insurance product should have the following features:

MSME identified features for business interruption insurance product

Source: MSC analysis

There are parallels for supporting MSMEs hit by COVID-19. MSC is currently undertaking a three-stage research study across eight countries in Asia and Africa to understand the nature and extent of the impact of the COVID-19 pandemic on MSMEs. The insights from the 2018 Philippines study correlate closely with initial findings from MSC’s dip-stick study of MSEs in eight countries. Some key support areas for MSMEs include:

Make blended cash accessible, fast: It is paramount that MSMEs, especially microenterprises, have access to cash to survive this pandemic. MSMEs need a dedicated fund to meet their working capital requirements, as well as essential household and living expenses. Such a fund would offer blended loans—a mix of grants and credit. While the grants cover essential household expenses, the credit would be used to meet the needs of working capital. This is important to ensure that both businesses and families weather the storm, and MSMEs are not forced to use expensive credit for essential consumption purposes.

Governments, MSME associations, and financial institutions must come together to administer the cash assistance identified above: To establish blended funds, grants should come from governments or international donor agencies that seek to assist the MSME sector. Local and international financial institutions should provide credit to these funds. These funds must be overseen by associations and chambers run by representatives of the MSMEs to ensure that the money is directed to the target sectors and segments. While registered, tax-paying MSMEs should have the first claim to relief. A portion of this can also be earmarked for informal MSMEs, which includes most micro and small enterprises. In the past, a lack of official recognition has made it challenging for MSMEs to access funds from state-run programs. One way to address this issue could be to allow unregistered MSMEs to self-certify to access the relief funds. In the long term, countries could introduce a low touch and paperlite registration for all microenterprises to allow them to qualify for support in the event of a disaster.

Make assistance accessible to all businesses and value chains: In the pandemic, MSMEs that deal in non-essential items, such as cloth shops and small manufacturing entities have been hit much harder. Available assistance must be accessible to all MSMEs that need it. Value chains, both local and part of the wider network, have also been hampered severely and must be eligible to draw on assistance. Therefore, support to backend service providers like cargo transporters and storage facilities is an important piece of the puzzle to get the value chain back up and running quickly.

At the policy level, long-term resilience of MSMEs must be at the core of all measures to limit fall-outs from such shocks in the future:

MSMEs must develop business continuity plans. Government agencies that promote MSMEs and support agencies should take the lead in helping MSMEs develop better risk management capacities. They should encourage MSMEs to:

Develop rainy-day reserves to tide them over during business interruptions. This can be undertaken through the promotion of savings products for MSMEs with favorable interest rates. These promotions can be incentivized. One possible idea could be that future government relief would be defined multiple of the value of such savings.

Have contingency plans in place to respond to business interruptions. These plans could take the shape of well-defined cost-cutting measures, as well as diversification strategies.

A comprehensive multi-risk business interruption insurance product would help MSMEs become self-reliant and resilient in the face of hazards like disasters and pandemics, as well as other risks, such as fires and theft. Insurers and market facilitators should consider bundling business interruption insurance with business development loans. It is also crucial that such products are designed with user needs and context in mind. The characteristics of such insurance products should include quick claims assessment and automatic payouts based on directives issued by the government, as with some crop insurances. These products should ensure payouts are made immediately into the bank accounts of MSMEs after the government declares a disaster or a pandemic.

Given the vulnerability of MSMEs to disasters and pandemics, there should be more reliance on digital access to financial services. For example, in our Philippines MSME study, none of the MSMEs interviewed reported using digital financial service platforms other than Internet banking services. Whether for credit or insurance, greater access to digital finance will create disaster- and pandemic-resistant pathways and provide speed and transparency. An example of this is in India where the government has made use of the JAM trinity (Jan Dhan bank accounts, Aadhaar ID cards, and Mobile payments infrastructure) to process 403 million transactions by 140 million of the low- and middle-income segment to access cash relief against the COVID-19 crisis.

Confronted with “grey swan” events, such as a disaster or pandemic, MSMEs face long business interruptions. The immediate response in such situations must be swift and blended. In the long-term, policymakers should focus on helping MSMEs devise business continuity and risk management plans by promoting risk reserves and business interruption insurance solutions. MSMEs must also adopt digital financial services because, as the current COVID-19 pandemic has shown, digital access remains largely functional when all other avenues have shut down. For now, however, we must focus on getting cash into the hands of MSMEs, and fast.

Reference note:

On March 11, 2020, the World Health Organization (WHO) declared COVID-19 a global health pandemic. Life as we once knew it has been suspended suddenly. Among those who have been hit the hardest are micro, small, and medium enterprises (MSMEs).

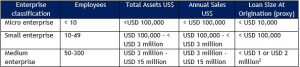

As per the IFC, an enterprise qualifies as a micro, small or medium if it meets two out of three criteria of the IFC MSME definition (employees, assets, and sales), or if an outstanding loan on its books falls within the relevant MSME loan size proxy

India announced a nationwide lockdown on 24th March, 2020 to deal with the effects of the COVID-19 pandemic. The initial days after the lockdown were disruptive for tech-based delivery platforms, as the government instructed these platforms to restrict their deliveries to essential goods and services alone. These platforms became increasingly flooded with orders as government directives restricted the movement of citizens. A rushed decision and lack of clarity on the implementation guidelines resulted in on-ground confusion, causing frustrating delays in the delivery of goods.

With customers unwilling and in many places unable to go out and shop, the opportunity for tech platforms was there for the taking. Eager not to miss out, some agile tech platforms quickly formed innovative partnerships to ensure deliveries and minimize the impact of the lockdown on their businesses. BigBasket, a grocery delivery platform, which is classified as an essential service, forged a partnership with Uber to complement its delivery fleet. Uber entered the arrangement as cabs were deemed a non-essential service, and therefore had an idle fleet available to deploy. Similarly, the grocery delivery platform Grofers hired 2,500 people to continue delivering services from affiliated industries and partner companies that had to shut down.

The effect of COVID-19 on platform-based gig work

The gig workers across tech platforms who offer rideshare, personal and home care, and delivery services have not been so lucky. Initially, the possibility of no work and therefore no income during the lockdown forced many of them to travel back to their villages. Many such workers and their families have had to walk hundreds of kilometers to do so. The ones who continued to work faced the occasional wrath of the police and local authorities.

The driver-partners of ride-share platforms Uber and Ola have been hit the worst. Even as they face mounting losses in income, they are under pressure to repay their car loan installments. Meanwhile, the need for strict hygiene and safety measures meant that food delivery continued to operate at lower than normal levels. Researchers Simiran Lalvani and Bhavani Seetharaman report from their self-administered survey of food delivery workers that the proportion of delivery partners who would earlier receive 16-20 orders per day went down from 30.9% to 7.2% post the lockdown.

Despite the usual gaps between promises and actual implementation, the measures that these platforms have put in place are steps in the right direction as they consider the health and economic security of the gig-workers. However, one may wonder why the platforms hesitated to implement such measures before the COVID-19 outbreak. Gig workers have continued to face challenges around the lack of transparency in remuneration structure and payout, absence of safety nets, and long working hours, all of which have had an impact on their health and economic security.

These problems are not new and definitely cannot be attributed to COVID-19. These issues have been talked about for some time now. The COVID-19 pandemic and the ensuing crisis should lead to more concrete action to develop a social security program for gig workers.

Designing a social security program for gig workers for the future

Given the size of the informal workforce and their vulnerability, particularly in times of crisis, designing social security programs for gig workers who comprise an emerging subset of the informal workforce could be a good starting point.

The role of technology and the formal financial system in creating a social security net

Tech platform-based gig workers are better equipped than others are in the informal sector in terms of their access to technology and the use of formal financial services. They receive their payments in bank accounts and know how to use smartphones. However, like other informal workers, their incomes vary according to the total time worked, availability of orders on the platforms, and seasonality of demand and migration patterns. Gig workers also alternate between one or two service providers to take advantage of any differential incentives on offer.

These attributes suggest that gig workers need a model of social security distinct from the ones prevalent for formal sector workers, such as the Employment Provident Fund Organization, or the Pradhan Mantri Shram Yogi Maan-Dhan (PMSYM), which targets informal workers in general. The variability, temporary nature, and seasonality of demand for gig work require careful design of the model to ensure wider adoption.

With the advancement of technology, the sharing and portability of social security accounts across multiple platforms no longer pose as barriers. Improvements in payments technologies enable low-value transactions at low costs like the Unified Payments Interface, while a million-strong physical cash-in cash-out network can help the design of scalable social security systems for gig workers.

The role of the government

In their book In Service of the Republic, Ajay Shah and Vijay Kelkar point to the limited capacity of the Indian state and caution against expecting too much from the government. The government has diminished capacity to design and implement large-scale social security programs for gig workers. This will be truer still in the aftermath of this crisis.

Shah and Kelkar suggest that the ideal role of the government should be on the “regulatory” and “financing” aspects of the system. One of the criticisms of the several social security programs that the Indian government runs is that these are fragmented and limited in their coverage of informal workers. Therefore, the government should focus on creating a universal social security system with the participation of the private sector to include all informal workers.

The government, therefore, should frame rules to implement the program and provide a platform for dialog among stakeholders—including private sector players and labor unions. It should also determine the size and scale of the subsidy. This entails committing its contribution to social security programs to maintain a minimum social security floor and complement the contribution from individuals or employers, or both.

In conclusion, as the lockdown lifts slowly across India, the immediate focus will be to kick-start the economy and push the participation rates of the labor force up to pre-COVID-19 levels. State and national governments will continue to remain stretched from the emergency spending during the crisis. Therefore, the role of the platform economy will be crucial to provide economic opportunities for informal workers.

This crisis offers tremendous opportunities to derive valuable lessons. The absence of a well-functioning social security system has aggravated the sheer scale and impact of the crisis on the livelihoods of the bottom 40% of the population. Not only is gig work likely to be a key component of India’s economy moving forward, but it also provides unique opportunities to provide embedded social safety nets. India could, and indeed should, pioneer this.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

The Internet plays an immense role in Dhanshree’s life. Her active use of the Internet and social media facilitates her ability to multitask. She uses

The Internet plays an immense role in Dhanshree’s life. Her active use of the Internet and social media facilitates her ability to multitask. She uses  The respondents from the middle-aged category expressed a limited desire to take calculated risks, start enterprises, or pursue livelihood opportunities owing to their existing responsibilities to grow their families and care for children and the elderly.

The respondents from the middle-aged category expressed a limited desire to take calculated risks, start enterprises, or pursue livelihood opportunities owing to their existing responsibilities to grow their families and care for children and the elderly.

We often see that more than ever before, young rural female SHG members are more engaged in social, financial, and civic issues that affect their communities. During our research, we found that, for the most part, young female SHG members took care of all book-keeping activities and bank-related work for the group. However, when it comes to self-growth, these young members find it difficult to seize opportunities to lead livelihood activities due to a range of complex socioeconomic issues. Our interactions with many of these young female members suggest that in their start-up activities, many lack proper access to markets and human resources, are unable to promote their products, and subsequently face low product demand.

We often see that more than ever before, young rural female SHG members are more engaged in social, financial, and civic issues that affect their communities. During our research, we found that, for the most part, young female SHG members took care of all book-keeping activities and bank-related work for the group. However, when it comes to self-growth, these young members find it difficult to seize opportunities to lead livelihood activities due to a range of complex socioeconomic issues. Our interactions with many of these young female members suggest that in their start-up activities, many lack proper access to markets and human resources, are unable to promote their products, and subsequently face low product demand. Significant improvements in “access to markets” are needed for SHG members to be able to access livelihood opportunities and create sustainable development. Many young SHG members who have started businesses have faced problems and economic losses due to poor access to markets. “Access to finance is not a problem for me but access to markets is. How can I sell and deliver my handmade products in far off places? Why do I have to depend on my brother to sell these items? He can easily roam around day and night on his motorbike but I cannot. It is difficult for young women—we have some limitations,” rued a young SHG member who is running a business selling handmade paper envelopes.

Significant improvements in “access to markets” are needed for SHG members to be able to access livelihood opportunities and create sustainable development. Many young SHG members who have started businesses have faced problems and economic losses due to poor access to markets. “Access to finance is not a problem for me but access to markets is. How can I sell and deliver my handmade products in far off places? Why do I have to depend on my brother to sell these items? He can easily roam around day and night on his motorbike but I cannot. It is difficult for young women—we have some limitations,” rued a young SHG member who is running a business selling handmade paper envelopes.

criteria of the IFC MSME definition

criteria of the IFC MSME definition