Agent banking provides an alternative to ensure access to financial services in remote areas. It was introduced by RBI in India back in 2006 with an idea to provide low-cost access to basic financial services in rural areas to ensure better financial inclusion in the country. Having more than .7 million Business Correspondents (BCs) in the country has helped people realize the cash benefits provided to them during COVID 19 crisis. Indian government transferred USD 7 billion supporting more than 200 million households in the country.

Blog

Responses to the financial impacts of COVID-19 through social cash transfers and digital payment infrastructure

Countries with well-developed digital payments infrastructure and shock-responsive social cash transfer systems have been able to respond rapidly to the negative impacts of the COVID-19 crisis. A faster response can lessen the financial impact on the poor. This means that beneficiaries do not have to resort to negative coping mechanisms, such as selling productive assets—such as livestock or tools—which may undermine their ability to earn a living and recover financially in the long term.

Using digital delivery mechanisms instead of delivering physical cash or food parcels is an advantage as it supports social distancing, thus reducing the risk of spreading the disease. These early responses to the economic impacts of COVID-19 also provide a guide for other national governments, demonstrating several measures to support a governmental response—both “quick-fixes” and long-term investments.

World Bank Group President David R. Malpass said that the challenges that stem from COVID-19 represent “an unprecedented crisis, with devastating health, economic, and social effects felt around the world.” He stated, “If we do not move quickly to strengthen systems and resilience, the development gains of recent years can easily be lost.” He added that while the pandemic’s effects are global, “this crisis will likely hit the poorest and most vulnerable countries – and people – the hardest.”

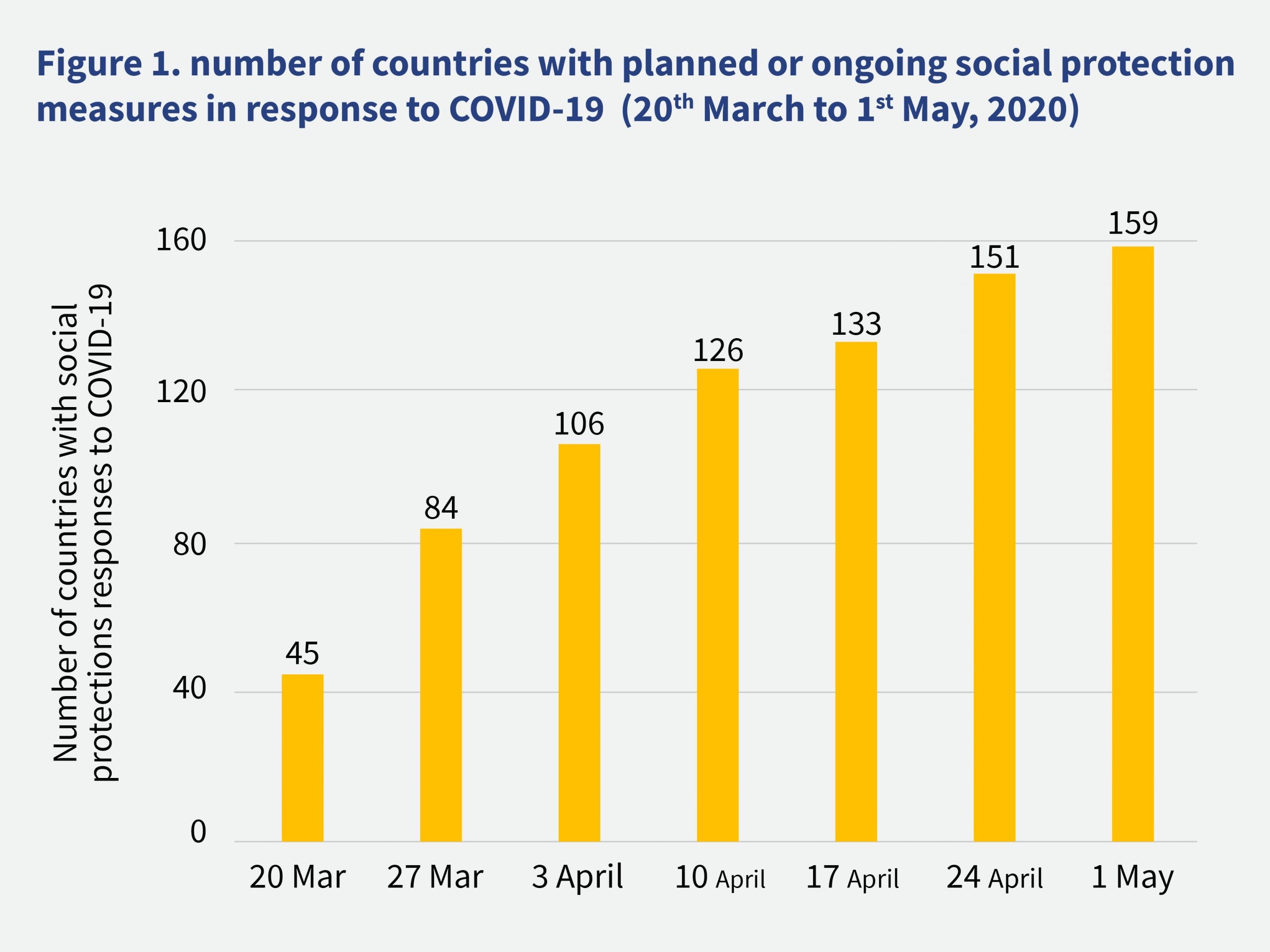

As of 1st May 2020, 159 countries have planned, introduced, or adapted 752 social protection and jobs measures in response to the pandemic. The increasing number of countries responding with social protection measures has been striking—growing from 45 countries as at 20th March to 151 countries by 24th April. Initial estimates of the investment going into social protection response to COVID-19 are at over half-trillion US dollars (USD 567 billion).

Among classes of interventions, social assistance or non-contributory transfers are the most widely used, accounting for 60% of the global response (455 measures), followed by actions in social insurance (27%), and supply-side labor market programs (13%). Within social assistance, cash transfer programs (54%) remain the most widely used intervention by governments.

Social protection measures graphic representation

This article reviews responses in three regions: (1) Latin America—where some of the first responses were initiated (2) Asia—home to some of the largest programs, and (3) Sub Saharan Africa—where governments with limited resources are coming up with innovative solutions to the crisis.

Across Latin America, several extensive and rapid responses have come up to mitigate the crisis. Many of these responses target informal workers and are built on existing payments infrastructure. In high-income Chile, the government made payments worth USD 15 under the “Bono COVID-19” initiative directly to the bank accounts of 2 million vulnerable people—predominately informal workers—in April. These payments were made possible by the national ID-linked basic bank account “Cuenta Rut”.

In upper-middle-income Colombia, the 2.6 million beneficiaries of the Familias en Acción program will each receive an extra payment worth USD 98. The government of Colombia has also launched a new cash transfer program, “solidarity income”, which provides a single payment of USD 108 each to at least 3 million informal workers and their families. The program ensures payments through bank accounts for the half of identified households who have them, and through electronic payments via mobile phones for others.

In upper-middle-income Peru, the government has been making a payment of USD 108 to each of the 2.7 million homes classified as poverty-stricken. Authorities in Peru have previously delivered G2P payments to accounts. However, under their COVID-19 response, they have increased the set of financial service providers to include private banks and mobile money providers to increase accessibility for beneficiaries.3

In Brazil, the government is adding 1 million households to its Bolsa Familia program. The Government of Brazil has also established a new three-month emergency cash transfer program of USD 115 each per month (or 60% of the minimum wage) for informal workers. The beneficiaries under the new program will be identified through Cadastro Unico, the country’s social registry.

Meanwhile, in middle-income Argentina, in April the government-approved payment of USD 151 each for informal workers, who make up 35% of the nation’s economy. In lower middle-income El Salvador, the government has announced a new cash transfer to support 1.5 million households in the informal economy with a USD 300 payment to each. The government targeted households with low electricity usage, such that any household with monthly consumption of 0-250 kilowatts per hour received the transfers.

In India, the government has sought to mitigate some of the negative impacts on poor households through a rapid response using existing programs. On 24th March, the government started its lockdown; 10 days later, through a new three-month cash transfer program, the government paid USD 6.50 into 204 million accounts of female beneficiaries of the existing financial inclusion program “PMJDY”.8 The government paid USD 13 each to 35 million beneficiaries under the National Social Assistance Program (NSAP) for the elderly, widows, and the disabled who receive social pensions.

In Indonesia, the flagship CCT program, PKH, will temporarily increase the benefit level by approximately 25% for three months and expand the program from 9.2 million to 10 million beneficiaries, or 15% of the population, starting in April. The authorities have brought payments forward and will disburse them monthly instead of quarterly.7

In Pakistan, the government launched its four-month “Ehsaas Emergency Cash Program” for 10 million families. The program will identify 3 million affected households through the national socio-economic database—while the eligibility threshold will be relaxed upwards. An SMS campaign will be launched to inform low-income families about the program.

Likewise, in Thailand, the government initially announced a new three-month cash transfer that pays USD 153 monthly to each of the 3 million workers who are not covered by the Social Security Fund. A week later, it increased the coverage to 9 million, although 21.7 million have applied for support. The total program cost is USD 4 billion.7 Thailand’s recent reforms allow payments to be sent to bank accounts through its fully interoperable PromptPay system. The country’s digital payments ecosystem also reduces the need to cash out. Additionally, Thailand has the advantage of a digital ID system that uniquely identifies recipients, which allows the government to determine eligibility and deposit directly to the account the beneficiary has linked to their ID.3

In Sub-Saharan Africa, underdeveloped payments infrastructure, national ID systems, and safety net systems have hampered responses. Yet the continent still provides interesting insights on how to target low-income families most affected by the crisis.

In Burkina Faso, the government announced a new USD 10 million cash transfer program for informal workers—fruit and vegetable sellers—with a special focus on women. In Ethiopia, the government expanded and adjusted its existing Urban Productive Safety Net Programme – beneficiaries will receive an advance payment for three months while on leave from their public works obligations.

Lower middle-income Kenya has a well-developed social safety net—the Inua Jamii program, which supports 1 million people, allocating them USD 19 per month each. The National Treasury appropriated an additional USD 100 million for the program in response to COVID-19. In Malawi, as part of the government’s National COVID-19 Preparedness and Response Plan, the government has proposed measures to accelerate payment of Social Cash Transfer Program (SCTP) benefits in April. It would fast-track SCTP payments with a four-month payment that covers the period up to June. The Government is also proposing to provide top-ups to SCTP beneficiaries and to increase SCTP coverage in rural areas (as of June) and urban areas from April-June.

The South African Social Security Agency (SASSA) started providing early payments of social grants to older persons and persons with disabilities from 31st March, and grant amounts have been increased effective 1st April. On 31st March, the Government of Zimbabwe announced that USD 550,000 per month would be set aside for the next three months for an emergency cash transfer program to reach 1 million vulnerable households.

African countries have made efforts to encourage the use of digital payments to support social distancing and hence cut the risk of transmission. The Western Africa Central Bank (BCEAO) has taken several steps to promote the use of electronic payments. BCEAO is a central bank that serves eight west African countries—Benin, Burkina Faso, Guinea-Bissau, Ivory Coast, Mali, Niger, Senegal, and Togo. The steps include providing flexible measures to open a mobile money wallet and making transfers person-to-person electronic money transactions free.7

In Ghana, commencing all mobile money transfers of GHS 100 and below became free of charge from service providers from 20th March 2020 for the next three months. Kenya introduced fee waivers on person-to-person mobile money transactions on M-PESA on 17th March for three months for transactions under USD 10. This followed a directive from Kenya’s President, Uhuru Kenyatta, “to explore ways of deepening mobile-money usage to reduce the risk of spreading the virus through physical handling of cash”.

Governments have launched new initiatives and used existing social cash transfers to meet the needs of low-income families affected by the economic consequences of the COVID-19 crisis. The changes to existing cash transfers have included increasing transfer values (Indonesia, South Africa, Ethiopia), providing additional one-off payments (Colombia, India), increasing the number of beneficiaries (Brazil), changing payment terms—making payments in advance, and increasing the frequency of payments (Ethiopia, Malawi, South Africa). Countries that have national ID linked to bank accounts, such as Chile, India, and Thailand, support rapid disbursement. Allowing a greater number of financial service providers to disburse payments may increase accessibility for beneficiaries and support social distancing (Peru).

The response to the COVID-19 crisis may accelerate the digitization of payments. There are some basic regulatory changes that central banks can make in support of the digital payment ecosystem. For example – allow non-bank e-money providers to provide cash-out services and fast-track, new entrants, by issuing licenses to mobile network operators, among others.

Floods and drought in 2019, a locust invasion in 2020, and now COVID-19: How do these incidents, particularly COVID-19 affect the food supply chain in the Horn of Africa?

Fifty-five-year-old Joshua is a smallholder horticultural farmer from Kiambu County, Kenya. He has endured the vicious cycle of droughts and floods all his life, most recently in 2019. He recently survived the desert locust infestation and his tomatoes are blossoming. Like many other smallholder farmers, Joshua has relied on people who live and work in Nairobi for a stable market for his farm produce. The directives to stay at home and maintain social distance, and the resultant job losses have had a great impact on the purchasing power and patterns of urban and suburban dwellers. This, in turn, has affected the ability of producers like Joshua to access a large and stable market. He now has to hawk his tomatoes by the roadside on the rack of his car. His post-harvest losses have escalated significantly. He can only access the market for a few hours in the day, and can barely make enough to feed his family.

“I would rather die of COVID-19 out here rather than be at home in quarantine and watch my family die of hunger”, he says. Yet why would feeding a household force someone to disregard their health and risk of spreading the virus? Joshua’s desperation has become a common refrain for most low- and medium-income segments as they go on with their daily hustle in total disregard of government health directives. COVID-19 has demonstrated the reality that, without a daily wage, most families in the low- and middle-income segments are a meal away from starvation.

In this blog, we analyze the impact of COVID-19 across the agriculture sector in Kenya using a value chain approach. The analysis focuses on the current situation and looks at the medium-term reaction and impact of the COVID-19 pandemic.

The wheel of misfortune that has hit the agricultural sector in the horn of Africa

Africa’s annual food import bill has been rising each year from USD 35 billion in 2017 to an estimated USD 110 billion by 2025. Increasing food imports highlight the inability of the continent to produce and feed her population adequately—a situation amplified by recent disasters.

In 2019, about 45 million people suffered the drought across Eastern Africa, Southern Africa, and the Horn of Africa. However, heavy rains experienced later in the year had given the prospect for a reduced humanitarian crisis at the start of the year 2020. Then, towards the end of December 2019, the first swarm of the desert locust was seen on its way to the horn of Africa. Unfortunately, in Kenya, this coincided with the harvest period during the short rain season, leading to massive loss of farmers’ output. And the locusts seem set to return with a vengeance in 2020.

The pandemic impact (COVID-19)

The shock of COVID-19 may well be more severe than the financial crisis of 2007–08. Most countries have limited movement or imposed total lockdown in a bid to contain and combat the disease. In Kenya, for example, the government has announced a raft of policies to mitigate the pandemic. These include cessation of movement into and out of the capital city, dusk-to-dawn curfew, social distancing, among others. Just like other smallholder farmers, Joshua remains coy over the future of his farming business, as the measures have affected the entire value chain. The farmers are worried about the impact of tighter government measures down the line with the uncertainty surrounding the pandemic.

Impact of COVID-19 on the agriculture value chain

Four months after the outbreak, the pandemic has reduced productivity, curtailed social interactions, and forced us to adjust styles of working. Yet labor-intensive sectors like agriculture have suffered the greatest impact

Agri-input supply and advisory services: The current pandemic has disrupted the input and advisory supply to a limited extent. The situation will not change soon as most of these services and inputs are produced in anticipation of the onset of the season. The seasonal nature of agriculture production provides the manufacturers and suppliers adequate time to manage stock smoothly. Input supplies, however, may be affected marginally in the short to medium term, should the situation prolong. Most of the inorganic fertilizer, chemicals, and other inputs are sourced from abroad. Closed borders and suspension of the main forms of shipment—air and water—will have an impact on the supply of the situation that persists in the long-term.

The face-to-face extension services have been discouraged to minimize the risk of virus transmission. As a result, most providers have turned to alternative means of delivery. Across Africa, ownership of mobile devices has increased. This has provided a pandemic-resistant pathway for the delivery of e-agriculture advisory services to farmers. Janet, a small-scale farmer in Thika, Kenya had her seeds and fertilizer delivered to her homestead a week ago by an appointed distributor. She ordered and paid the inputs by dialing a USSD service. She also accesses to agronomic tips from Ujuzi Kilimo, a technology platform, either through SMS or USSD. She is one among the many smallholder farmers across Africa, who number around 33 million as per the latest Digitalization of African Agriculture report. Estimates indicate that about 13% of all sub-Saharan African smallholders and pastoralists are registered for digital agricultural services, such as good agricultural practices, weather updates, and market linkages.

The face-to-face extension services have been discouraged to minimize the risk of virus transmission. As a result, most providers have turned to alternative means of delivery. Across Africa, ownership of mobile devices has increased. This has provided a pandemic-resistant pathway for the delivery of e-agriculture advisory services to farmers. Janet, a small-scale farmer in Thika, Kenya had her seeds and fertilizer delivered to her homestead a week ago by an appointed distributor. She ordered and paid the inputs by dialing a USSD service. She also accesses to agronomic tips from Ujuzi Kilimo, a technology platform, either through SMS or USSD. She is one among the many smallholder farmers across Africa, who number around 33 million as per the latest Digitalization of African Agriculture report. Estimates indicate that about 13% of all sub-Saharan African smallholders and pastoralists are registered for digital agricultural services, such as good agricultural practices, weather updates, and market linkages.

Production: COVID-19 has primarily affected the capital cities and major towns across Africa. In rural Africa, far fewer cases have been reported at the time of writing. With smallholder farmers largely driving production, the first harvesting season is likely to see minimal disruption to production. However, as the disease spreads and governments impose tighter measures, production may be affected, especially that of cash crops, vegetables, and cereals. The disruptions extend to microfinance and informal savings groups, which form a critical source of finance for rural farmers. COVID-19 has forced the microfinance sector to put a hold on all disbursements. This means most rural people, including farmers, have no access to funding.

In turn, this will lead to constrained investment in the sector. In the next couple of months, we expect that production will slump, the food market will be disrupted, and food crises will follow. Smallholder farmers in rural areas are especially vulnerable to the pandemic as they are less likely to have access to healthcare facilities with oxygen and ventilators. This is compounded by the fact that any added financial shocks from hospital admission or funeral costs for rural households can be devastating.

Transportation of food in Kenya

Transportation of food in Kenya

Transportation: Most governments have recognized food delivery as an essential service. However, geographic restrictions (both within countries and across borders), and curfews have had a great impact on the movement of agricultural produce. Some truckers have already suspended their services due to a fear of contracting and spreading the virus, coupled with the constrained demand in retail markets due to the reduced purchasing power of customers and the closure of restaurants and hotels.

A businessperson from Kilifi country, Mr. Wachira, has returned to his ancestral home in Central Kenya. He owns several trucks that transport fresh produce from Mpeketoni, in Lamu County in the coastal region of Kenya. These trucks supply to major markets across the counties of Mombasa, Kilifi, Kwale, and Lamu itself. His clients typically include tourist hotels along the coastal region, major retail traders, and convenience stores. The COVID-19 situation saw most of his clients cancel orders as the hotels remained deserted. His truckers also requested him for unplanned leave from work, days before the government announced movement restriction.

Processing: As production and transportation decreases, the processors are finding it increasingly difficult to maintain the supply chain for both raw materials and products. With the contraction in the financial markets under the full impact of the pandemic, access to credit for the processors will become difficult. The processors have also suffered in terms of workforce. Reduced working hours due to curfews and lockdowns have seen workers either declared redundant or asked to work from home. Essential processes that require physical labor have also been affected greatly.

Retail: The pandemic has had a heavy impact on the market for food. The disease has brought economic suffering and loss of jobs, which has in turn reduced purchasing power. Meanwhile, the policies adopted to mitigate the spread of the infection have also hurt the retail business. The responses to control the spread of the virus has affected enterprises, such as the hotels and restaurants, value addition industries, and transport that would normally operate 24 hours a day. Some have closed entirely while others have been operating under restricted timings due to the curfews.

The situation may worsen if the spread of the pandemic continues. As the spread reaches the rural producers, most retailers have lost operating capital and have both fewer customers and fewer suppliers of the products. Interestingly, partnerships between e-commerce players and convenience stores have seen a spike, as demand increases for home delivery of goods to customers during lockdowns. This may become the modus operandi until the situation normalizes. This leaves us with the question—will it be a permanent trend, as the customers taste digital approaches?

African man in forest

Call to action

The earlier sections depict Kenya’s situation under COVID-19. However, these issues pervade all countries in the Horn of Africa. In this regard, we see the importance of governments across the region to consider the following:

- Monitor the impact of COVID-19 over the crop seasons that spans March 2020 to December 2020: As community transmission of the virus grows from major towns to rural areas, there will be a need to ascertain the exact impact on the sector by end of current cropping cycle. This is going to provide relevant data for the players in the agriculture ecosystem to plan strategies for the sector to bounce back.

- Accelerate the role of digitization: Agri-digitization initiatives in the continent have increased in the past two years. However, most are at the infancy or pilot stage. The creation of accelerator programs that target agritechs in Africa will help curb the over-reliance on human resources in food production and distribution. Cash transfers and transfers of other government benefits have seen great success, offering lessons that the agricultural sector across Africa could borrow and integrate.

- Re-imagined and innovative agriculture finance strategies: Most formal financial service providers consider agriculture finance as too risky. However, the critical role of the sector for economies in Africa, especially in times of disaster, is now evident. There is, therefore, a need to apply an ecosystem-oriented approach to address this. Credit-guarantee programs and hedge financing are some of the initiatives required to help the sector bounce back after the pandemic. In March, the Central Bank of Kenya announced measures to mitigate the adverse effects of the coronavirus pandemic on the banking sector. However, the microfinance sector, which the central bank does not regulate, awaits similar support measures. Meanwhile, agriculture sub-sector finance will also require a special focus.

- Consider adequate policy and regulatory changes: Most governments in Africa have restrictive trade and taxation policies. For example, input supplies are often highly centralized. Would this be the best time to rethink the decentralization of seeds and other agricultural inputs? The taxation regime (VAT and other taxes) for agriculture trade will also require review as the sector might take a bit longer to bounce back. The Kenya Revenue Authority has directed a reduction in VAT and PAYE. Similar decisions, which would benefit the agricultural sector are expected. The ministry of agriculture is working on reforms to facilitate access to inputs, mechanization, and in discussion with other agencies to reduce trade tariffs for agriculture commodities.

Agriculture contributes over 25% of most African economies GDP, over 70% of employment, and among the top foreign exchange earner. Targeted government subsidy programs to the agriculture sector will not only help the sector to bounce back but will induce GDP growth and job creation as well in the post-COVID-19 recovery phase.

Read a similar analysis by MSC for the Asia market on:

- Food security: How are agriculture and the corner shops faring amid India’s lockdown?

- Innovations and coping strategies for food security at the time of COVID-19

How India is securing its G2P beneficiaries from COVID-19 – Lessons for other countries to create a G2P delivery platform

As of May 1, about 159 countries have planned, introduced or adapted 752 social protection measures in response to COVID-19. 244 of such measures, representing one-third (32.4%) of total COVID-related social protection programs, are cash transfer programs. This includes both pre-existing and new programs.

India was among the first few countries to announce a social protection package of USD 24 billion at the federal level. State governments have announced, and are still announcing, additional measures. To our last count, this amount is around USD 14 billion. Of the USD 24 billion package, about USD 10 billion is for cash transfer and remaining is for in-kind support, primarily food grains. Under the cash transfer package, INR 500 (USD 7) will be transferred to the bank accounts of 200 million women every month for three months. 87 million farmers will get advance payment of INR 2000 (USD 28) under a pre-existing income support program called PM-Kisan. 30 million poor senior citizen, widows and disabled will get ex-gratia of INR 1000 (USD 14) under a pre-existing pension program called National Social Assistance Program (NSAP). 80 million poor women will get advance payment of about INR 784 (USD 11) to buy LPG for household cooking for the next three months[1]. In addition, 800 million beneficiaries will get three months of food grain free of cost through an extensive network of public distribution system that already delivers food grains to these beneficiaries every month at a highly subsidized cost.

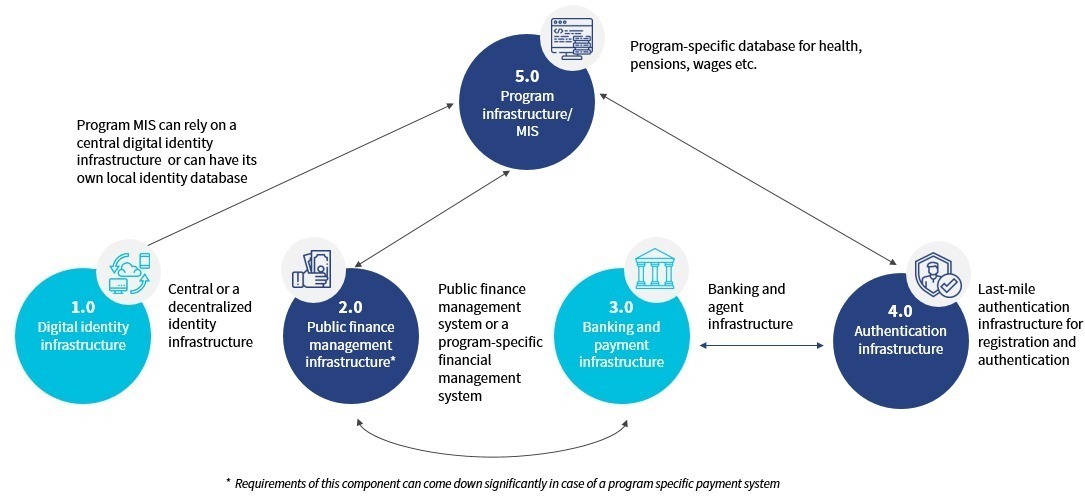

The value of Indian federal government’s social assistance package is almost half of the combined package of all middle income countries (MICs). But what is surprising is the speed at which the cash component of this package reached the beneficiaries. About 400 million G2P payment transactions were processed by the Indian federal government within of this announcement. Challenges such as payment transaction failure and onboarding new people, who are falling into poverty due to this pandemic, continue. But nonetheless this is a remarkable feat that many other countries, developing and developed, aspire to. Over the last few years there has been an increased interest among many countries to learn from India’s experience in digitizing its G2P program. The following figure illustrates various components of the ecosystem that must be considered.

MIS Program Infrastructure

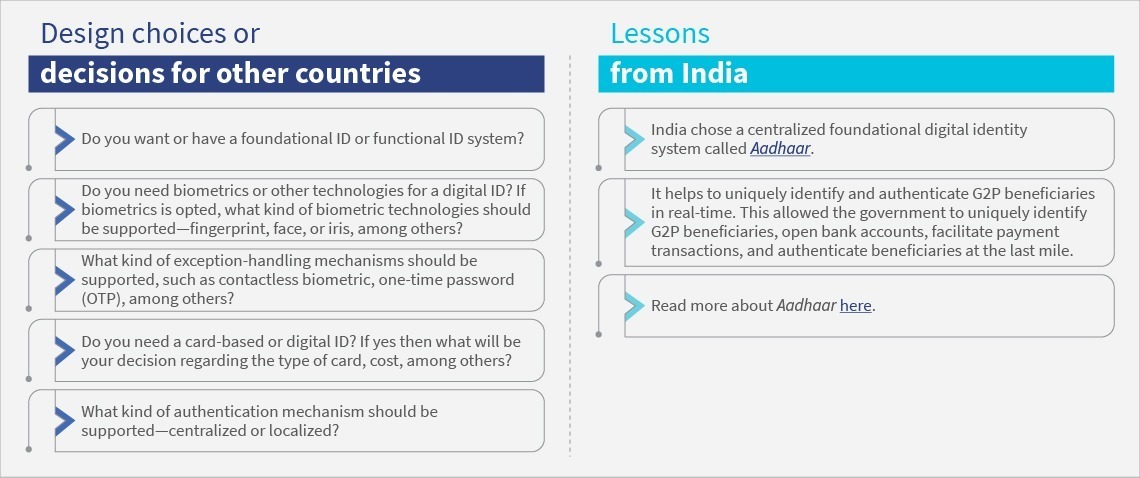

1.Digital identity and authentication infrastructure

A digital identity system can help to uniquely identify and enrol people into a G2P program. Countries have choices depending on whether they already have an existing digital identity database, are creating a new one, or can repurpose an existing database for this purpose.

A digital identity system can also serve as an authentication system that can reduce the cost of last mile authentication infrastructure and overall transaction cost.

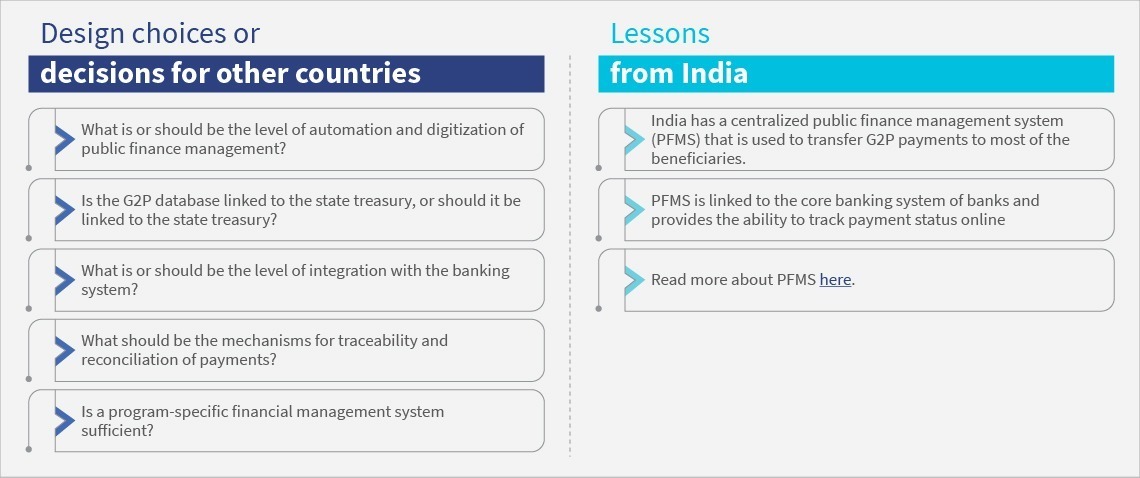

2.Public finance management infrastructure

A digital public finance management system can increase the observability, efficiency and targeting of G2P payments by several fold. However, it is difficult to create and manage. Volume and value of G2P payments will also play and important role in deciding whether one should have a centralized system to manage G2P payment or a program specific financial management system is sufficient.

3.Banking and payment infrastructure

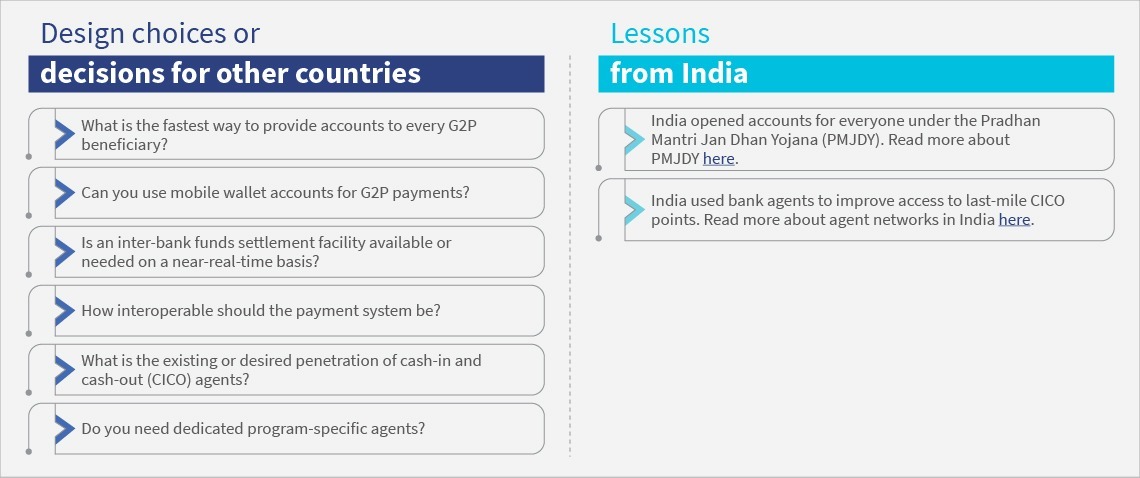

Penetration of banking and payment infrastructure is key to facilitate G2P payments. There are three key elements to this – access to bank/mobile wallet account to g2P beneficiaries, integration of backend payment system and last mile access points for transactions.

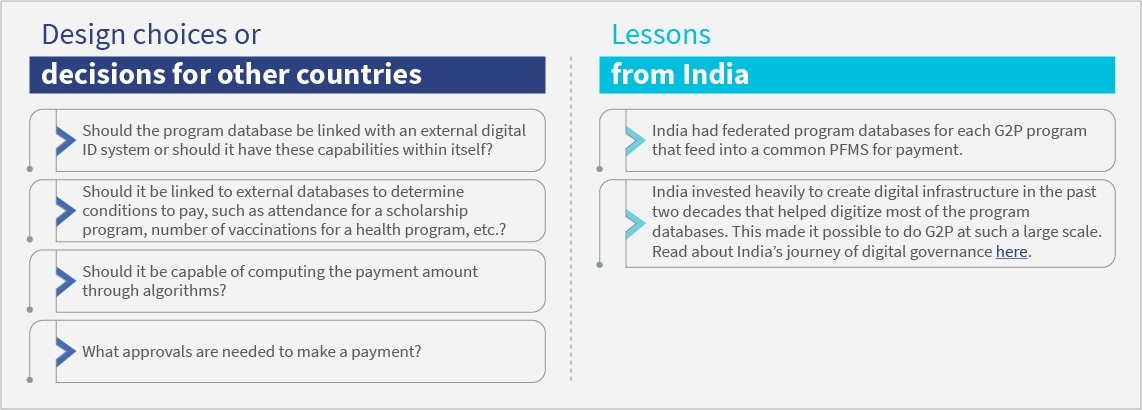

4.Program infrastructure/MIS

A digital program database is an important requirement for running a G2P program. The level of automation of this database can vary and determines the efficiency of the system. Designers of program database have many design choices depending on the requirement and budget.

Every country’s journey to create a digital system that brings in efficiency, accuracy and speed to G2P payments will be unique depending on its current situation, aspiration, budgets, legal and regulatory requirements and many other conditions. India offers valuable lessons for other countries to learn and adapt these learnings to create its own roadmap.

Digital governance Ideas and lessons from India

Efforts against digital governance or e-governance started way back in 2000’s in India. Digital governance or e-Governance is the use of information and communication technology by the government to provide the quality information and services to country’s ecosystem in an efficient, cost-effective, and convenient manner bringing transparency and accountability in government functioning. Digital governance includes services and processes in any interaction between Government-to-government (G2G), Government-to-person (G2P), and Government-to-business (G2B). The digital infrastructure created over more than a decade helped the government support the citizens by transferring USD 7 billion benefitting more than 200 million households in the country during COVID 19 crisis.

Public Financial Management System Ideas and lessons from India

Indian government manages its public finance using an application called Public Financial Management System (PFMS). It is used for payment, accounting, and reconciliation of government transactions. During the lockdown period (March 2020 till 17th April 2020), government-supported more than 200 million households by transferring cash amounting to USD 7 billion directly to their bank accounts. All these transactions were managed in PFMS.