Availability of quality and affordable paid care is essential to reduce the burden of caregiving on women

The last elections in a few States sparked a new political and social debate by promising salaries for women’s household work. Some courts also awarded compensation to families of homemakers. Although isolated, these events accentuate a widening fault-line — the lack of a policy framework that acknowledges the contribution of caregiving to the country’s economy.

Whether childcare, caring for the elderly or doing domestic work, caregiving is the invisible engine that has silently fuelled the economy. The work that makes all other work possible.

Indian women disproportionately shoulder the burden of unpaid care work, spending more than five hours per day on it as compared to only 1.37 hours by men. This disproportionate burden is an issue of equality — and economic growth.

Considering unpaid care work as a quintessentially feminine activity, is one of the key reasons behind women’s falling participation in paid work in India, currently at 16.1 per cent.

Institutionalising equity in caregiving has become urgent. Systemic measures like workplaces more actively supporting men’s roles as fathers and caregivers and men sharing a more significant burden of caregiving at home are essential. Similarly, the ubiquitous availability of quality and affordable paid care is essential to reduce the burden of caregiving on women.

Quality and affordable care is required at both ends of life in all societies. However, the provisioning of care in India remains a frayed patchwork of state, market, and familial care. As a result, women end up being the primary caregivers. The US recently unveiled the American Families Plan that classified “care” as essential infrastructure, marking a major shift in perception.

Most people cannot work unless they are confident that their child or elderly parent in need of care is being looked after. A single caregiver who provides safe and quality care might provide all other family members a chance to earn money, creating a multiplier effect. However, India cannot rely on women to do the bulk of unpaid care work and keep pushing them out of the workforce. Anyone who has ever looked for reliable paid care for their family knows that finding such care in India remains an arduous task. The demand far outstrips supply.

Example for early childhood care, most households where both parents work have to rely on family-based circles of support. The few who can afford help, opt for home-based untrained nannies. The constraints are severe for low-income households. Poverty necessitates both parents to work, and they cannot afford market substitutes for their unpaid labour.

Govt support inadequate

Central and State government programmes remain inadequate in catering to the growing demand for early childhood care. Studies estimate that given the rapid shift toward nuclear families, the demand for childcare could be as high as five million facilities in cities alone.

Similarly, with India’s rising life expectancy, the demand for long-term elderly care, preventive and supportive care services has continued to rise.

The government has played a crucial role in facilitating innovation and market development for critical sectors. Encouraging innovation in the care sector will be critical to turning the unfair burden of unpaid work into an economic opportunity.

The WEF estimates 40 per cent of emerging job opportunities will be located in the care sector, given the global shift in demographics, changing social norms that have led to greater social acceptance of paid care, and the uptick in demand for trained caregivers.

Studies show that rich countries with a higher tax base have larger paid care sectors. However, some middle-income countries also have paid care sectors that make up more than 15 per cent of their employed population. Deliberate creation of policy and care infrastructure by governments can go a long way in providing universal affordable and quality care.

First step in this journey should start with better enforcement of existing government provisions.

Second step would be to experiment with different types of decentralised provisioning, understanding the pros and cons of different models of care, and subsidising care for certain groups as essential. Some models of care could include encouraging childcare entrepreneurs, co-locating childcare and elderly care programmes, cooperative- and community-based models for low-income households, vouchers, and care credits.

Three solutions

Market development and innovation to encourage the growth of a paid care sector offers three solutions.

First, paid care workers provide professional skills that differ from the knowledge and skills of family caregivers. They include certified early childhood care and geriatric care professionals.

Second, availability of quality and affordable care creates choices for families, particularly women, to share some of the labor of care with paid workers and make a choice to enter the paid workforce.

Third, it creates more employment opportunities for women represented disproportionately in the care sector. It also encourages change in social norms by de-stigmatising men in caregiving roles at home and as care work professionals.

India is poised for creating a policy framework that allows the government to explore, experiment and take risks on behalf of the public to create an ecosystem for a robust “paid care” sector. But first, we need a paradigm shift in how we treat, value, and invest in care work.

Mustika (name changed) has been the sole breadwinner of her family ever since her husband, a former factory laborer, was laid off due to the COVID-19 pandemic. She works as a nonpermanent teacher in a junior secondary school. She also takes on side hustles as a grocery reseller and a domestic helper, providing ironing services to several households.

Mustika is an active member of “Doa Bunda,” a women’s cooperative under the Pemberdayaan Perempuan Kepala Keluarga—The Female-headed Family Empowerment Foundation (PEKKA). As part of the cooperative, she commits to saving money every month consistently. She has been paying off her low-interest rate (~1%) business loan from PEKKA. Mustika reloads her e-wallet regularly to buy products in bulk on e-commerce platforms. She believes that she gets a better price on these platforms, especially using cashback promotions from the e-wallet provider.

Mustika lives far away from the city. So she prefers to use a branchless banking (Laku Pandai) agent for banking services, including money transfers, cash withdrawal, and social assistance benefits. In this way, she saves both time and money spent commuting to the faraway bank branch.

Women’s cooperatives are vulnerable to being left behind in the rapidly evolving digital economy

Data from the Ministry of Cooperative and Small Medium Enterprise (SME) in 2021 revealed 13,212 active women’s cooperatives in Indonesia. But, these are only 9% of the total active cooperatives across 34 provinces. Considering this limited representation, can women’s cooperatives achieve the four strategies the President of Indonesia set forth? These strategies include:

Modernization of cooperatives

Emergence of new entrepreneurs

Integration of MSMEs to global value chain

Scaling up of MSMEs

Among the strategies, “modernization of cooperatives” poses the most significant challenge to women’s cooperatives, especially in rural areas. Rural women’s cooperatives have limited access to information, resources, and digital tools. Typically, they are small-scale, semiformal, and are often left behind amid the charge toward digitalization.

The Minister of Cooperation and SME, Teten Masduki, mentioned that only 0.73% of all cooperatives are connected with the digital ecosystem. Women’s cooperatives play a critical role in the economic empowerment of rural women by helping them accumulate assets under their name through savings and providing small-scale finance. Seeing them left out of the movement is disheartening.

Moreover, modernization should go beyond digitizing the operational system of cooperatives. It should also encompass the development of digital banking products and services to meet the needs of cooperative members.

Women’s cooperatives can potentially be a great partner for banks to extend digital financial services to the last mile, especially to low-income women

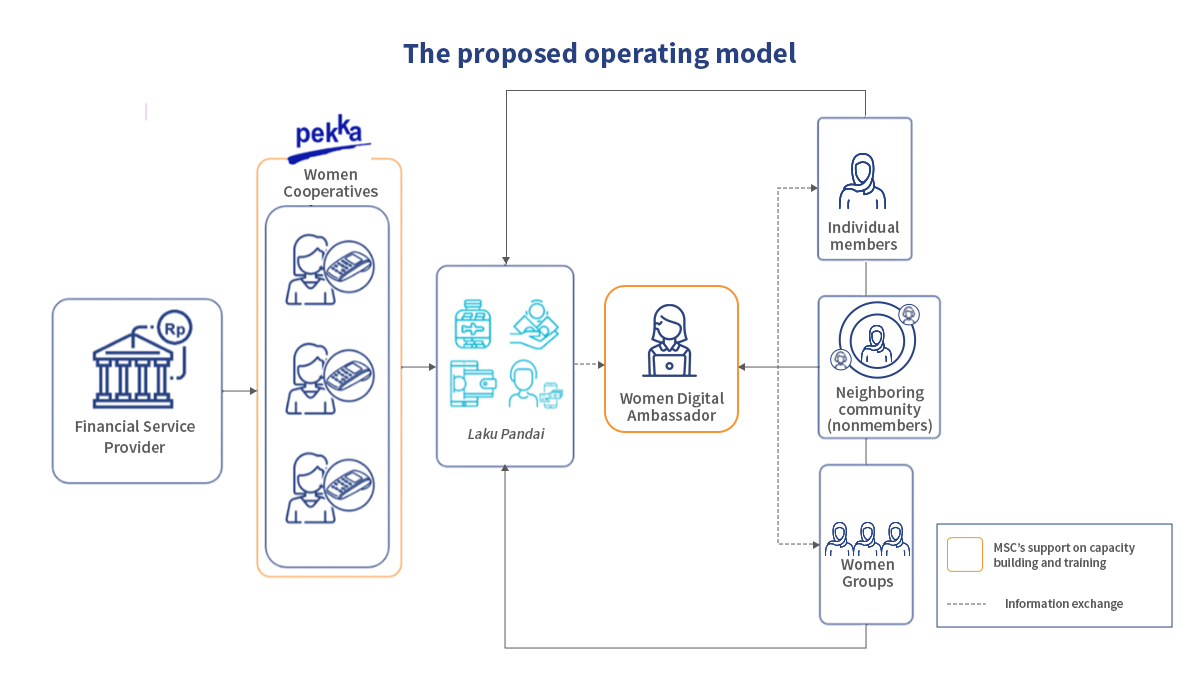

MSC and PEKKA Foundation have collaborated to enhance low-income women’s quality, uptake, and usage of digital financial services in rural areas. PEKKA runs a network of women’s cooperatives in 20 Indonesian provinces.

The pilot project will cover four districts in four provinces: Tangerang, Karawang, Pekalongan City, and Bantul. We are working to integrate the cooperative and Laku Pandai agents to provide financial products and services on a digital platform. The platform will serve the existing member base across the women’s cooperative offices during the pilot phase, and from the result, it will be expanded to other locations under the cooperative’s network.

Cooperatives that were once limited to offering basic loan and saving services can now provide their members the full suite of a bank’s financial services. They can now offer money transfer, cash withdrawal, bill payment, disbursement of cash social assistance, and People Business Credit (KUR) applications. Also, transaction fees charged by the agent are a potential source of income for the cooperatives. It can turn into residual income or Sisa Hasil Usaha (SHU) at the year-end.

The integration of Laku Pandai and cooperative

MSC’s study on female banking agents in India found that female agents create a reassuring environment for women and men to make transactions. It also noted that the acceptance and success of female agents depend significantly on social perceptions, which play a more influential role for them than their male counterparts. For instance, our research shows that most customers generally perceive male agents to be faster, more knowledgeable, updated about product features, and less prone to commit errors in the DFS business.

Although the findings reflected India’s perceptions, social norms, and culture, MSC found similar phenomena while undertaking need assessment in the pilot project locations of Indonesia. Women need another group of empowered women of higher capacity and broader insights—“influencers”—to help them adopt digital finances.

For this reason, Women Digital Ambassadors (WDAs) are recruited from the cooperative members. These ambassadors consist of women small business owners who will be equipped with knowledge and tools through training from MSC on digital entrepreneurship, selling through social commerce, and digital finances. These small entrepreneurs are selected because they have actively accessed multiple banking products and services. They are commonly known as the “early adaptor, trailblazers, and movers” in digital finances.

These woman ambassadors will mentor the members of cooperatives to access the digital financial services and products offered through Laku Pandai agents. The weekly meetings of cooperative groups provide an excellent forum to exchange information and knowledge.

Women Digital Ambassador (WDAs) can become the torchbearers to accelerate women’s financial inclusion

Women’s cooperatives integrated with Laku Pandai services and supported by the WDAs are expected to give deeper, broader, and measurable impacts on collective initiatives that engage women in the digital economy, especially in rural areas.

Through these initiatives, MSC expects to support the vision of financial inclusion for Indonesian women outlined in the National Strategy of Financial Inclusion—Women (SNKI-P). SNKI-P intends to achieve 90% financial inclusion by 2024. The initiatives need support from financial service providers, including bank and nonbank institutions, to upskill Laku Pandai agents in operation and customer services to create quality agents.

However, financial inclusion is not the endgame. Instead, it is a vehicle to accomplish objectives like gender equality, women’s economic empowerment, leadership, and poverty alleviation.

Over the next few months, MSC and PEKKA will develop a training module for WDAs and an operating model for the new “cooperative Laku Pandai agents.” MSC has also partnered with financial service providers to ensure that these banking agents receive sufficient support to succeed. Tune in as we publish more updates.

Women in low-income communities may choose a channel based on the most economical choice that suits their life best, given their acute burden of unpaid care work and time poverty. It is critical to decode gendered aspects that lead women to choose their selected channel to help build their financial resilience.

MSC’s DEBIT framework helps us understand which channel the individual chooses and why. Comparing the DEBIT scores helps us identify actions that stakeholders like governments and financial service providers can undertake to help women have a wider range of channels to choose from.

Financial inclusion for women in India still has a long way to go. While more women appear to be financially included, the use of these accounts remains limited across the country, especially among low- and moderate-income (LMI) women. Women’s ownership of bank accounts has improved over the years. The increase is primarily due to the PMJDY mission, which was crucial to reducing the gender gap in bank account ownership—from 19.8% in 2014 to 6.4% in 2017. Findex 2017 reported that 77% of Indian women owned a bank account against 43% in 2014 and 26% in 2011. Yet it also shows that the estimated gender gap in account ownership and usage remains significant.

Women face relatively higher barriers to using financial services at the bank or agent point due to their limited mobility and adverse gender-based norms. Although pivotal to accelerating the usage of bank accounts, digital financial services continues to be under-utilized, especially among women in India.

Key drivers of the gender gap

Women’s low utilization of bank accounts mainly stems from operational factors and limitations placed by social-cultural norms. On the supply side, a lack of focus on women’s needs and financial behavior remains a crucial driver to their low utilization of financial services. Banking products and services do not recognize that women and men have different financial behaviors deeply influenced by gendered social norms. For example, women prioritize privacy and savings. They have horizontal social networks, smaller economic geographies preferring to transact closer to home due to less free time available, and constraints on safe mobility. They also have varied lifecycle needs as they experience more transitions like marriage, maternity, and childbirth.

The promise of DFS in addressing the gender gap

DFS can help women overcome these barriers by offering solutions that they can access remotely, safely, and cost-effectively. Such solutions could be designed to enhance privacy and women’s control over their money. It could address women’s time poverty and mobility constraints by allowing them to transact at their preferred time and location. The solutions could also help them cope better with emergencies by making it easier for women to send and collect funds from different sources. Effective digital savings tools could help women with managing risk better and enhancing their financial asset base. A digital footprint of women’s transactions can also help make their creditworthiness more visible to banks and financial service providers.

Suffice to say, DFS could be a strong catalyst for women’s economic empowerment.

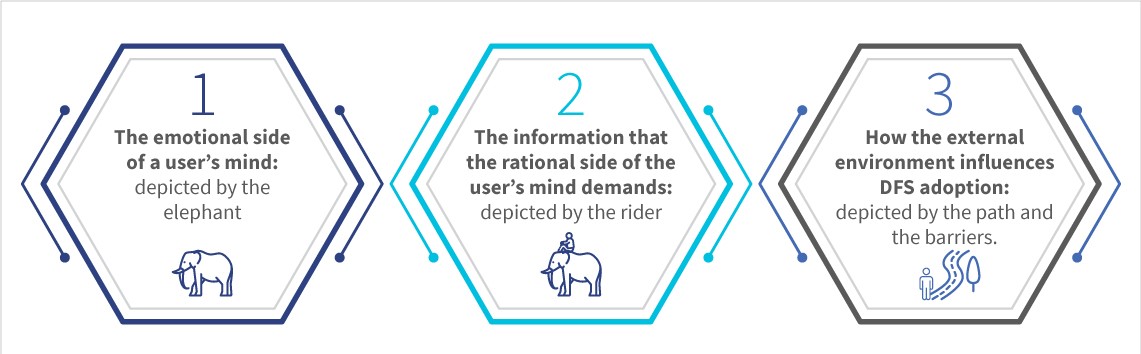

Inspired by the “Elephant, Path, Rider” framework by psychologist Jonathan Haidt, an examination of the journey of using DFS for the first time by men and women shows the interplay of the emotional and the rational mind for each step within the journey. The customized framework highlights three essential contributors to changing a user’s perspective to DFS and their interaction with it. These are:

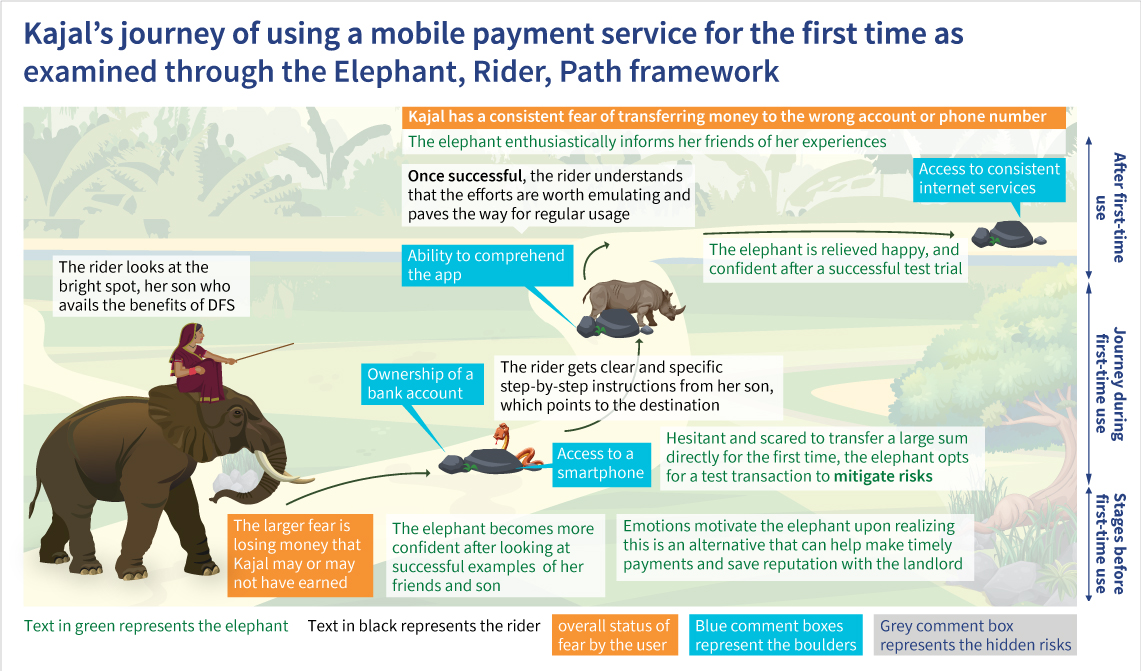

The below is a snapshot of Kajal’s (a volunteer at Odisha Livelihoods Mission) journey of using a mobile payment service for the first time. Despite a positive experience, she hesitates to use DFS the next time due to her risk-averse nature and the limited availability of customer service to help with any errors she may make.

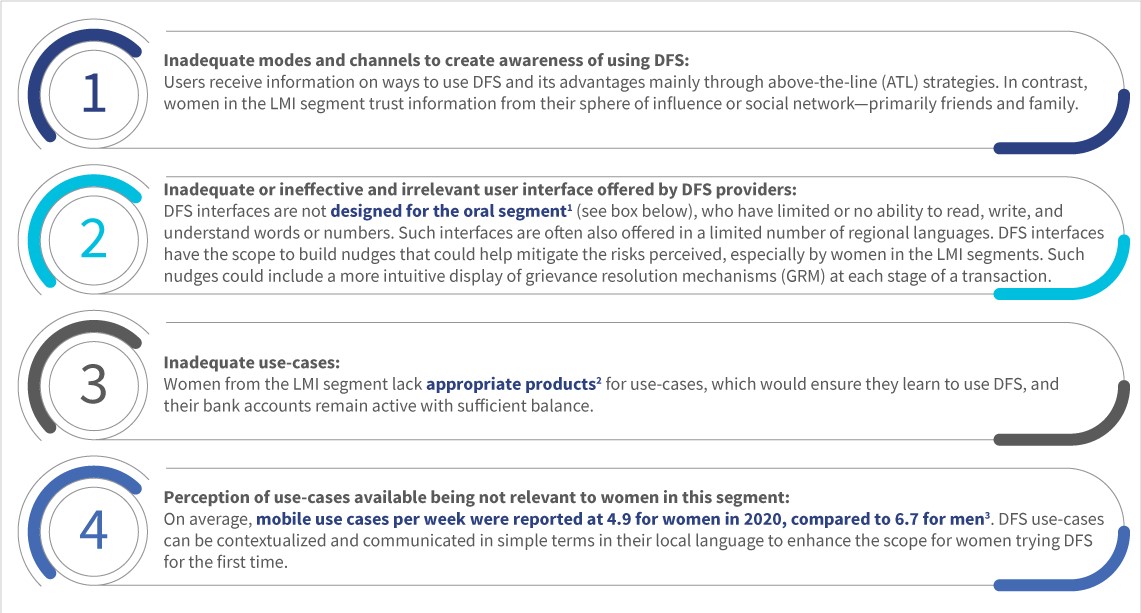

This examination has helped identify the following critical factors that contribute to limiting the uptake of DFS, especially among women:

The government’s response

Government departments have undertaken several initiatives to enhance the use of financial services, including DFS. These initiatives include efforts undertaken by the Department of Financial Services, the Ministry of Rural Development, and NITI Aayog. They focus on enhancing access to financial services among women and ensuring account ownership at the last mile.

While these government initiatives are laudable, the complex range of physical, social, and psychological barriers mean that they are unlikely to be adequate, even if they achieve scale. If India intends to achieve real digital financial inclusion for all, it will need to expand the financial services space for millions of low-income women.

Expanding the financial services space would require creating convenient access, valuable use-cases, exposure, and trust-building—first through assisted access to DFS. Female BC agents at the last mile could be a critical channel to encourage exposure, build trust, and ensure a positive first experience of DFS for women users. These local agents are an integral part of the community and enjoy women’s trust. Ultimately, these agents could provide women with the skills, confidence, and trust to use digital tools to conduct self-initiated transactions—especially if they can get their hands on intuitive user interfaces.

The Jakarta Post first published this blog on 8th March, 2022.

Working from home: A choice for some but a circumstance for another

Work from home (WFH) has become associated with the pandemic for those who have the luxury to choose to work from home. Yet not everyone can have this option and still have sustainable income, decent working space, and secured social protection each month. “Other” work-from-home workers have been working from home much before the pandemic but under different working circumstances.

These others are home-based workers. According to the ILO/MAMPU project report, home-based workers (HBWs) are those “who are self-employed and/or subcontracted piece-rate workers (putting-out system), and most of them are women.” In Indonesia, the law on MSMEs also accommodates the concept of home-based workers, categorizing them as an informal sector.

The Implementation Guideline to Home Industry Development, published by the Indonesian Ministry of Women’s Empowerment and Child Protection (MoWECP), classifies home-based workers as a cottage industry. A cottage industry is a production system within which products are produced by creating additional value from raw materials, carried out in individual homes and not in a particular location (factory).

Yet these home-based workers, whether in the putting-out system, self-employed, or part of the cottage industry, remain vulnerable to shocks. The Indonesian Labor Law is yet to define HBWs. Indonesia has yet to ratify the ILO Convention No. 177 on homeworkers. In the absence of a law, HBWs remain predominantly informal workers. Informal workers lack formal contracts, stable income, high wages, health cover, workers’ insurance, and adequate working conditions. The absence of a law increases their vulnerability to unemployment, exploitation, and poverty.

A WIEGO 2021 Statistical Brief outlines that COVID-19 exacerbated the already-existing multiple vulnerabilities of HBWs. For those who do not use ICTs in their work, HBWs suffer the greatest loss of work and income. In Indonesia, despite the challenges, women in informal work have proven to be resilient, even though they are paid lower than men. A Jakarta Post article also mentioned that informal female workers, such as women HBWs, are expected to also take on the primary child-rearing responsibilities and housework, besides earning low wages.

Sense and workability: A facilitator’s remark on women home-based workers

In many social development programs, heroes in the field contribute to the success of a program. One such hero in this context is Zaenab Hafiezh. Zaenab is a local facilitator who supports the MoWECP’s program on women’s economic empowerment for female home-based workers in Rembang Regency (Central Java Province).

Zaenab, also an HBW, applied to be a facilitator in 2016 for MoWECP’s women home-based workers program in Rembang. The MoWECP was set to support the program for only two years, after which it would continue from the local regent office. While many of her fellow facilitators resumed their role, Zaenab was among the ones that continued her critical role as facilitator to several women HBWs in the neighborhood.

As a fellow HBW, Zaenab understands her peers’ situation, challenges, and needs in navigating livelihood strategies and securing basic everyday essentials. Zaenab facilitates women HBWs who are self-employed and in the putting-out system. Her task is to support the mobility level and empowerment of those she facilitates, according to the “implementing guideline on home-based workers” published by MoWECP.

This program was part of the ministry’s effort to achieve the 3ENDs, namely: (1) ending violence against women and children, (2) ending human trafficking, and (3) ending economic inequality between men and women.

To Zaenab, the 3ENDs goals reflect real concerns she learned from several experiences of her fellow HBWs. She also believes this women’s home-based economic empowerment program by MoWECP is a tactical approach to reducing violence, trafficking, and economic inequality in her hometown. Zaenab’s facilitation journey, though, was not smooth. She faced risks from husbands who rejected the program and blocked their wives from participating. Yet she saw other instances where this program could help survivors exit domestic violence situations. From her observation, women HBWs experience economic struggles alongside domestic violence. The burden does not stop there. Some of these women are the primary breadwinners for their families and struggle to make ends meet while caring for children and household chores.

Based on the lessons from Zaenab’s facilitation, the workability of women HBWs depends on the fulfillment of four critical needs. These are:

Assistance in strengthening leadership and confidence as women home-based workers, to enhance eligibility and mobility;

Support in capacity building on product development and marketing to increase the value of their work;

Facilitating a safe space to include men in the conversation, especially husbands of women HBWs, who are also vital to support their wives;

Commitment in policy and budgeting to recognizing and protecting home-based workers as acknowledged workers.

Zaenab notes that if the above needs are supported, the pathway to increasing female home-based workers’ mobility level, quality of employment, and economic empowerment is achievable and will help achieve the 3ENDs objectives.

The MoWECP stated that:

1. Strengthening women’s leadership and economic empowerment is part of its mandate under the gender mainstreaming unit and as part of their home-based workers’ programs. It has initiated a series of awareness campaign activities as part of this endeavor. This includes socialization on themes related to gender equality, gender-equality-based entrepreneurship, eliminating violence against women and children, and reproductive health.

The MoWECP also notes the importance of including men in conversation and awareness programs on women’s economic empowerment. It has already included partners to develop and execute more tailored programs as needed.

2. The MoWECP has also connected with some sub-national governments to promote local homeworkers’ products in local markets, through local and national crafts councils, and to affiliated companies and private sectors. The mentorship program will also serve as a platform to enhance product development and marketing capacity.

3. MoWECP supports the endeavor of several local governments that made local commitments through development planning and budget. It has also mandated its agencies on-site to be the activity focal point to support local initiatives.

Yet MoWECP realizes that it too will need collaborative support from allies to achieve the needs of women home-based workers comprehensively.

Friends, allies, and comrades

So, who are these allies of women home-based workers in Indonesia who can fulfill the said needs? Moreover, how can more players support their empowerment pathway?

The MoWECP has been a friend, ally, and comrade to women home-based workers by initiating the women’s home-based economic empowerment program since 2016. MoWECP has organized a pilot program in 21 regencies and cities. It is now is in the progress of replicating these efforts to other regencies and cities. The program’s success stories, such as those led by Zaenab, have become references of best practices to other sub-national governments to have the same commitment in strengthening women home-based workers in their area.

In MSC CPD Indonesia’s discussion with the Economic Assistant Deputy of MoWECP, Eni Widiyanti, she mentioned that MoWECP is committed to improving the conditions of women home-based workers. This commitment is also strengthened by connecting with like-minded organizations like MSC CPD Indonesia.

MSC CPD Indonesia also works on economic and financial inclusion, supporting MoWECP to strengthen women’s economic empowerment through economic inclusion and digital financial inclusion. MSC applies a gender-centrality framework to ensure its work on women’s economic and financial empowerment is inclusive and gender-responsive.

Other friends, allies, and comrades are the coalitions of civil society organizations, such as the Indonesian Homeworkers Network, the Indonesian Social Observer Foundation, and Homenet Indonesia. They have voiced and influenced the national and sub-national legislation on protecting home-based workers in Indonesia. The Ministerial Regulation on the Protection of Home-based Workers is not yet legislated. Yet at the sub-national level, local leaders have developed local regulations and policies that champion the narrative for an equal and inclusive working system for home-based workers. To name a few, local CSOs like TURC, Yasanti, and BITRA have been making progress on this advocacy in Java and Sumatra provinces.

CSOs play a significant role in connecting and networking on the issue with other strategic actors and organizations, which are potential allies in this campaign. Some conversations have also included local employment agencies, women’s empowerment agencies, and local development agencies.

MSC CPD Indonesia is also a friend, an ally, and a comrade to women home-based workers. MSC CPD Indonesia is currently developing a partnership with MoWECP to strengthen women’s economic empowerment through economic and digital financial inclusion.

Homework on home-based workers

The Rembang Regency experience led by Zaenab revealed the ecosystem of work for women home-based workers, which remains challenging. Yet these challenges can gradually be overcome with coordination, collaboration, and most of all, commitment to the recognition and protection of home-based workers. Zaenab’s experience also indicates that capacity building on gender equality and social inclusion on HBW should not be limited to the HBW. Instead, it should expand to all relevant stakeholders and key figures in the ecosystem. These stakeholders include men in the family, local and national government officials, private companies, service providers, and public institutions. Almost all have a weak understanding of the issues that women HBWs face. Strengthened coordination and collaboration can support the recognition of HBWs as workers and speed up processes to advocate policies and regulations on their protection.

Recognizing the profiles and gaps of women HBW can be enhanced by improving national and sub-national gender equality and social inclusion disaggregated data on HBWs. Such recognition will ensure they are not invisible in data. It will also ensure informed and comprehensive decision-making based on the reality and needs of (women) HBWs can fill the void on policies and development toward a decent, recognizable, and sustainable working condition for them.

Supporting the ongoing work of local CSOs and advocacy for the empowerment and protection of home-based workers is also vital. These CSOs can be partners and tandems of decision-makers and providers to assist in mainstreaming a comprehensive design and implementation of empowerment programs and policy development for and on home-based workers.

And last but not least is the inclusion of those not included in prior conversations and decision-making processes. Making room for HBWs, facilitators, companies, and service providers in the campaign and awareness dialogue and program designs on HBWs would ensure balance, meet the needs, and reinforce equity to improve their lives.

Finance Minister Nirmala Sitharaman, in her budget speech 2022, mentioned some significant reforms towards government procurement that have happened over the past few months. These are welcome developments in a landscape marked by State’s weak budget execution capacities. However, there needs to be a stronger push towards adopting public finance management reforms to enable the government to manage its finances better.

Take for instance the nearly Rs 2000 crore of idle funds recently unearthed by the special task force set up by the Tamil Nadu government. State Finance Minister Dr. Palanivel Thiaga Rajan called it a “trailer” with the whole picture across thousands of bank accounts yet to be seen.

The issue of unspent funds or ‘idle float’ lying in government accounts is, of course, not a new revelation. Last September, the Comptroller and Auditor General (CAG) of India highlighted a whopping Rs.4.72 lakh crore remaining unspent in FY19, citing poor budget formulation as a leading cause. Former CAG Rajiv Mehrishi had also pointed to the problem of unsatisfactory monitoring of allocated budgets and suggested an “end-to-end enterprise-based IT system” to improve expenditure tracing.

Idle float is a symptom of inefficient use of public funds. The funds stuck in the bank accounts of various government agencies as float add to the public debt. This is ironical for a low middle income country like India, since government cannot meet it expenditure commitments from its own funds and has to borrow additional funds adding to the fiscal deficits and the challenges that come in its wake. Downstream macro-effects include lower credit availability for the private sector and eventually, slower economic growth.

It also has a huge opportunity cost in the form of scarcity for those Implementing agencies (IAs) that have spent their allocations and need funds urgently. These IAs then struggle with mounting arrears and unpaid dues to contractors. This even as funds are available aplenty with other IAs and programs. This paradox of simultaneous plenty and scarcity manifests on the ground as poor service delivery to citizens.

Issues galore, reorientation a must

How does public finance work in India? If visualized as a tree, the Centre or states are at the top and transfer funds to lower branches representing state, district, local governments and panchayats. For most Centrally Sponsored Schemes (CSS), there is a multi-layered fund release mechanism. Each step of fund flow requires documentation, usually utilization certificates (UCs), to prove previous payment tranches have been used up. When this is done, the relevant state-level department releases more funds.

A delay at one branch – say, at the district level – for any reason often hampers the smooth release of funds to the next one, i.e. the block or panchayat level. As a result, funds often get stuck for years. Furthermore, after tranches are transferred, they are often not spent within a stipulated time period either on account of work not being done on time or delays in reporting.

Importantly, the flow of information is no smoother, resulting in a lack of observability on expenditure status. In most cases, data at the primary unit of activity (e.g. teacher attendance or weight measurement of a child by an Anganwadi worker) is fed manually and gets digitized “manually” by an army of Data Entry Operators (DEOs) who enter program data in computers. This same data, often with compromised authenticity, moves from one IT system to another. This too is done through another round of manual entries, not automatically through data exchange protocols between interoperable systems.

Overall, the data that resides in the system is recorded away from the primary unit of activity, and through a series of manual processes between disconnected information systems. This leads to a gap in the reporting of physical and financial progress.

While the Public Financial Management System (PFMS), managed by the Controller General of Accounts (CGA), has certainly helped such flows become more traceable over time, the scale of the issue demands a mix of process and technology interventions.

So, what’s the solution?

There is an urgent need for these disparate systems to ‘talk to each other’. This will require an approach that integrates digital principles with public finance management (PFM) principles. These integrated ‘Digital PFM (DPFM) principles’ can transform the PFM ecosystem and improve governance and development outcomes. Two specific ones, Just-in-Time (JIT) and Single Source of Truth (SSOT), are starting points of the DPFM journey.

A JIT funding approach for centrally sponsored, central sector and state schemes will enable real-time funds transfers to the payee (contractor or individual) instead of it being parked in the bank account of implementing agencies (IAs). It would negate the need for pre-loading or funds transferred in advance.

It’s analogous to a bank issuing a credit card and defining a spending limit on that card. It authorizes an individual to spend up to a specific limit without transferring advance money into that individual’s bank account. Similarly, the Centre and state governments can define the spending limit of IAs for their respective schemes, without transferring money in advance. Money flows directly into the bank account of the contractor or beneficiary, only when the work is complete and the money is due. Modern technology allows this to work seamlessly with some tweaks in work practices. In fact, Rule 230(7) of the General Financial Rules, 2017, recommends JIT but unless it is implemented in principle and totality, the government and citizens cannot reap the technological benefits.

Similarly, pursuing an SSOT will enable aggregating scheme/program data at a single point that is accessible to a variety of public departments and agencies. This would foster higher systemic accountability and transparent reporting by individual departments and program heads. It will allow quick and, in some cases, algorithmic decisions. Such high-fidelity data is critical to the functioning of a JIT system.

Way forward

DPFM principles such as JIT and SSOT do not require an overhaul of current systems. They all have an associated technology play that just needs to be layered on current systems with tweaks in work practices. The PFMS is one part of the solution. It already tracks funds and expenditures. It can be re-factored a little, or a new module for JIT can be created to meet the requirements of real-time fund release and improve visibility.

Such enhancements will improve scheme monitoring and reduce float. If JIT can be integrated with the program MIS, it can help auto-trigger both payments from the Consolidated Fund of India or State to a department or program as well as to end beneficiaries. This would help administrators focus more keenly on service delivery than simply approving payments at respective branches. And one must not look far for inspiration. The Government of Odisha is implementing the Just-in-Time rule for various schemes such as the ‘Grant-in-Aid to Special Schools’ under Social Security & Empowerment of Persons with Disabilities Department (SSEPD) and the ‘Urban Wage Employment Scheme (MUKTA)’ under Housing and Urban Development department.

The Centre and States would do well to consider these smart solutions in their existing PFM architecture. The wins would not just be mutually beneficial; but have long-lasting positive impacts on state capacity, government savings, welfare planning, and service delivery.

This blog first appeared as an Op-ed in the Times of India, on March 9, 2022.

Financial inclusion for women in India still has a long way to go. While more women appear to be financially included, the use of these accounts remains limited across the country, especially among low- and moderate-income (LMI) women. Women’s ownership of bank accounts has improved over the years. The increase is primarily due to the

Financial inclusion for women in India still has a long way to go. While more women appear to be financially included, the use of these accounts remains limited across the country, especially among low- and moderate-income (LMI) women. Women’s ownership of bank accounts has improved over the years. The increase is primarily due to the