Agriculture is a key space where we continue our current work. Through our efforts, we will bridge the divide between farmers and the digital revolution and help them to improve both productivity and profitability. In the technology space, our recent work involves engagement with regulators and governments to create a systematic impact and build meaningful connections through digital platforms, such as AI, FinTech, and blockchain.

We continue to employ human-centric approaches to cater to the needs of the elderly, youth, women, refugees, and the health and education sectors. In our attempt to make the world a better place, we plan to address the fundamental issues related to climate change and explore ways to support its mitigation.

We place our end-client at the center of our work and provide customer-driven solutions. We work with banks, telecommunication companies, governments, and regulators to provide high-quality products and services to the financially excluded section of society. We engage in challenging endeavors to make an impact on the mass market. Our consultants and local experts go deep into the field in our assignments across the globe. Deep insights into local markets help us provide highly contextualized solutions for every client we work with.

MSC has been involved in a series of leading-edge projects. In India, we redesigned the Prime Minister’s Jan Dhan Yojna, which is the government’s countrywide financial inclusion program. As of now, the program has 335 million accounts, more than 100 million insurance policies, and a host of digitized transfer platforms. We continue our work with the government in India with engagements in Aadhaar-based subsidy and LPG reforms.

Our recent work includes human-centric design-based solutions for the illiterate and innumerate segments across geographies. This includes financial literacy and the development of digital and online platforms to enable access to financial inclusion to millions of poor people. We saw extensive use of our signature approach to design thinking—MI4ID. Last but not least, our engagements on the acclaimed Agent Network Accelerator program continues across multiple locations around the world.

In our previous blog, we outlined the potentially catalytic role that Agent Network Management Companies (AMNCs) could play in extending the reach and quality of services for the mass market. In this blog, we provide a high-level outline of six options to support the impact of ANMCs.

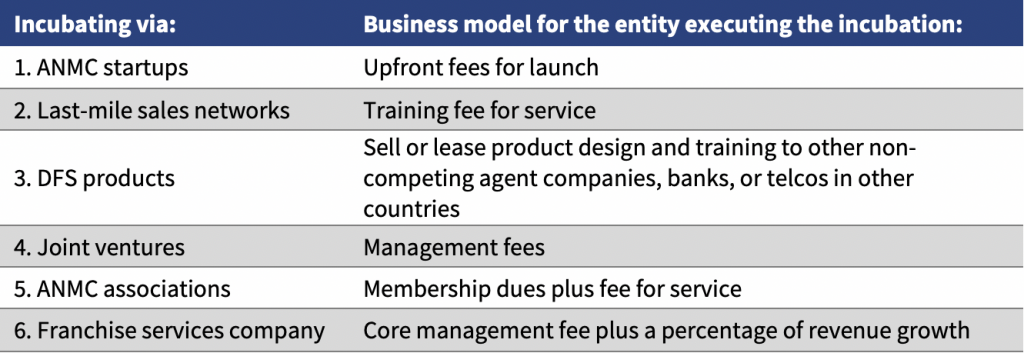

Incubate ANMCs by catalyzing startups or bolstering smaller players:

Help startups launch to introduce AMNCs in new markets that have mobile money but where telcos or banks need an outsourced way to scale for network effects. While outside support would bear upfront costs and be time-limited to get the startup up and running, local business owners would maintain the responsibility for ongoing network operating expenses. The incubating functions could include:

Recruiting long-game, socially-minded owners;

Attracting or brokering seed capital or managing a seed fund that invests in scaling networks;

Initial training of staff and assisting with surge capacity to onboard large numbers of new agents.

Why? Fragmented agents and their ANMCs lack power compared with telcos and banks and have been a missing or under-represented actor in the push for universal DFS. Telcos and banks with competing revenue lines often treat agents as costs to be minimized. This results in a neglect of agents and underinvestment in networks and thus less reliable services and slower proliferation of DFS.

Support for ANMCs with better customer education and promotion in new markets could lead to faster adoption of mobile money and a healthier ecosystem to deliver and use DFS. Tracking and demonstrating metrics of how the value-addition from and trust in agents improves the bottom line could flip the paradigm from a cost center to revenue driver and differentiator. This flip is essential to stimulate investment in innovative DFS products that agents may sell or facilitate, rather than just waiting for smartphone-only apps in the hopes of bypassing agents.

Incubate last-mile sales networks to augment their offerings as providers of a range of digital services:

Help any base-of-the-pyramid sales network to introduce or diversify products with mobile money or DFS. This would be like equipping the sales agents or outlets of FMCG companies, or merchant networks like M-Kopo, or itinerant sales agents like Living Goods to offer airtime scratch cards, cash-in-cash-out (CICO) services, or eventually DFS products. The same could be attempted when the super-platforms develop fulfillment distributors to bring e-commerce. For this path ANMC functions would include:

Training sales forces on product details, processes, and pitch to convert any frontline salesperson into a DFS provider;

Training-Of-Trainer (ToT) for normal refresher training courses on products.

Why? Leveraging existing face-to-face networks can spur efficient growth of outreach as well as diversify revenue streams either to decrease agent churn or improve the liquidity for CICO service agents, or both. Some countries might only be able to achieve network effects by building mobile money or DFS on existing distribution systems.

Incubate DFS products by incorporating R&D specialists within the daily operations of an owned network:

Help develop and test more diversely supportive DFS products by running an R&D arm embedded within the operations of an ANMC to learn and experiment continuously with real-time data on product usage. Product development specialists, researchers, and other institutions seeking pro-poor DFS diversification could recognize and leverage the differences in the capabilities and sophistication of agent networks in different geographies in order to cross-fertilize ideas and capabilities from leading markets into those that lag. The embedding of R&D could be structured as a sponsored collaboration, outsourcing or subcontract, or a joint venture.

Why? With access to real-time data to iterate prototypes, pro-poor practitioners can focus on designing demand-side, client-centric products without the same telco or bank supply-side constraints that lead to “orphan products” from providers. Without creating their own operational footprint, embedded R&D or consulting providers also benefit from building their knowledge base from gleaning frontline experience or wisdom.

Incubate joint ventures through brokers that form and run shared agent networks:

Help create joint ventures to run shared agent networks (or “Android of agents” as proposed in Helix’s Agent Network Accelerator’s closeout). With an ANMC in place to manage agent operations on behalf of multiple clients, a brokering entity could perform functions that include:

Recruiting partners according to carefully defined standards;

Broker coopetition partnerships and facilitate negotiations that are fair to the whole group;

Navigate the product mix and equal training and promotions;

Form the legal entity and house a dedicated Director within an external Agent Network Incubator.

Why? These attempts could appear more attractive while initiating rural expansion where a sole provider might avoid trying to build their own network alone. Some markets ripe for shared networks (like Uganda) would benefit from socially-minded hubs to initiate coalition building and to protect the trust of more vulnerable partners from being torn apart by predatory negotiations from the most powerful partner. In contrast, the markets that lack the critical mass for network effects, or without a widespread agent network, could ramp up mobile money adoption by one convener—building out shared agents from the start. For example, see Nigeria’s Shared Agent Network Expansion Facility (SANEF). Joint ventures will be more effective than bilateral partnerships for all players to maintain ownership and continue to feel control and in effect protect their respective brands while ensuring the balance between parties continues to work for all as the market evolves.

Without an initiating business actor in the ecosystem who may spur action that instills a “fear of missing out”, it can take a long time for incumbent providers to overcome their hindrances simultaneously. Markets can take a long time to mature to coopetition, as is seen in the limited or tardy sharing of ATM networks or telecom masts.

Incubate ANMC associations to tackle shared problems and proliferate the increased value-add brought by their industry:

Help convene regional or global associations of ANMCs to tackle shared issues and demonstrate their unique value-add collectively. Introductory steps could begin with informal workshops in key markets and then assembling an industry conference (per region). The functions could include:

Research;

Advocacy;

Shared best practices;

Professionalization and delivery of staff training courses over e-learning platforms;

Coalition building or partnership brokering.

Why? Currently, each ANMC is learning on its own and alone holds little influence or power to demonstrate the revenue-generating value addition of investments made in the technology or human capital of agent networks. Staff churn remains a pernicious problem that would benefit from industry-wide talent development. Similar to telco and bank associations, ANMCs could also serve as the focal point of the industry for the social good achieved or a structured channel to direct socially supportive resources.

Incubate a franchise services company that spreads expertise and investments for ANMC owners to not have to each learn best practices alone:

Help to eventually create a franchise services company—perhaps spun out by the Association. Once enough ANMCs have grown strong enough globally, they could professionalize in the same ways as other labor-intensive hotel or restaurant chains, and distinguish the owner from the specialist operator. They could provide functions that are typical of franchises:

Systems—standard procedures, manuals, and software or apps;

Shared backend services, such as liquidity management or cloud systems;

Training courses;

Brand, with standards enforcement;

Combined marketing;

Business consultation.

Why? Beyond all the value that these functions are better provided more centrally, franchising ownership structure is an efficient way to scale a large footprint that nurtures successful business. It differentiates operating expenses from the upfront ownership investment provided by the franchisees.

Each of these six incubation paths originates from ideas already at work in other industries of the global marketplace and so has a corresponding business model. Therefore, any social or philanthropic infusion involves a way to propel each method sustainably.

Social sector practitioners or donors want agent networks—whether owned by the telco, bank or independently as ANMCs—to run in a manner that delivers real value to the base of the pyramid (BoP). This will require patient capital, client-centric strategies, innovative HCD-based products, and a combination with complementary services to develop more comprehensive solutions that meet the daily needs of the BoP. Investing in ANMC approaches could help convince many providers to adapt their business strategies, or as a coopetition actor, to raise the bar on how to serve the needs of BoP through profitable business practices. None of these ANMC approaches are incompatible with also pursuing telco, bank, super platform or FinTech strategies. They could actually be flip sides of the same coin as the Catalyst Fund discovered a key success factor of inclusive FinTechs involved deploying a mix of “tech + touch for new interactions to reach & and keep customers“. Rather than every Fintech having to create their own field force, might FinTechs (or any specialized e-marketplace or tech platform company needing to deploy gig “digital translators” to help customers transition into the digital economy) stay lean by relying on a developed industry of ANMCs as face-to-face specialists?

Accion Venture Lab’s report “The Tech Touch Balance” advises “design an intuitive customer journey that maintains established relationships, trust, and cost-effective, scalable operations, yet still balances digital and human engagement”. As has been done with many call centers, insurance brokers, or BPOs (Business Process Outsourcing), in what ways could FinTechs outsource the handling of different stages of their customers’ journey where customers prefer human touch? Customers have demonstrated a preference for human touch when learning more about a product and its benefits, enrolling, and trying to resolve complaints. ANMCs could offer another “leg of the stool” that focuses on optimizing the various human touch prerequisites for digital finance usage still seen even by the research in digitally prolific markets of Kenya (see Pesatransact’s range of services through app + agents on page 14) or India. This special attention could prove a necessary tool in the efforts to close the gender gap in DFS.

Nonetheless, an ANMC-based strategy does face limitations. Some are as following:

Outside India, there are not that many large ANMCs to support.

Operations of a large human network are inherently difficult given the requirements to manage recruitment, onboarding, training, and churn.

Margins are very thin, requiring efficient operations and making investment opportunities less attractive.

Investors entering this market must have long-term horizons and patient capital.

Many telcos at the moment prefer to control agent management in-house.

Much larger telcos and banks would maintain much stronger negotiating positions.

Some fundamental questions remain:

Are there willing business partners, and is there market demand for such ANMC services?

Would a mix of philanthropic funding and patient capital investors commit to a long-term vision of next-generation DFS agents amidst the inevitable learning curve and setbacks?

How can the unit economics work out to manage to break even and business sustainability for these pro-poor ANMCs?

While benefiting from what a developed industry of ANMCs could provide different institutions, here are some practical steps each could take to complement their own work.

Philanthropic funders can add the above paths to social impact by deploying the same technical assistance, challenge funds, and grants to ANMCs that they use to incentivize banks and telcos to tackle financial inclusion.

Telcos can start by hiring ANMCs for their rural expansion strategies to penetrate harder to reach areas. As that alternative of outsourcing proves to not threaten their control, they could increase their reliance on ANMCs in established markets as a way of offloading cumbersome system hassles or lack of internal capacity. Then telcos could turn to ANMCs to better segment and support agents and promote and deliver more complex products and value-added services (VAS) to customers.

Banks and MFIs can outsource or subcontract the basic CICO service component of agency banking and then expand their reach through ANMCs that develop sales agents to promote and cross-sell digital financial products and services on their behalf.

FinTechs can develop and iterate their technology in conjunction with ANMCs to deliver the customer-preferred “touch” portion of the experience rather than each building their own human channel to market.

NGOs are experienced in mobilizing volunteers to reach masses, especially where it is harder for markets to reach. So they can look for ways to partner with ANMCs to deliver complementary value, such as health insurance via community health workers or agriculture finance via extension workers or partnering co-ops. Moreover, they can help with pro-poor product development or integration of DFS with NGO social services to meet practical needs.

Social enterprises while targeting BoP markets can consider diversifying their “basket” offering with digital financial products to diversify revenue streams for their sales force.

To fulfill the promise of diversified DFS meeting tailored needs, everyone in the ecosystem would benefit from a reliable industry of expert ANMCs that focus on maximizing value through face-to-face networks.

Government of Indonesia, as part of its long term plan to digitise all G2P programs, transformed the existing in-kind food subsidy program, called Rastra or Beras Sejahtera, to a direct transfer of the subsidy amount to the bank account of the beneficiary. The initial rollout was started back in 2017 in 44 cities/regencies and expanded to 118 cities/regencies across multiple provinces/islands in Indonesia. The Ministry of Social Affairs of Indonesia (MoSA) intends to target a total of 15.6 million beneficiaries in 2019. MicroSave Consulting as per the request from MoSA, initiated a study to evaluate BPNT operations implementation. This evaluation is a follow up to the evaluation that MSC did for BPNT in 2017. Using a mixed method approach by interviewing 2,398 beneficiaries and 779 e-warongs/agents in 93 regencies/cities in Indonesia, the study reports key issues in the operations, feedback and satisfaction of the beneficiaries and e-warongs to the program implementation, including some policy recommendations to MoSA for future implementation.

In addition, the study also analyses the role of digitizing G2P programs on financial inclusion and key barriers for low income beneficiaries to enter the digital economy.

“I am going to stop. I did it with [supplier x], I told his representatives not to come here anymore. I work with my own money and I am free to stop whenever I want,” exclaims Mr. Mataba, a non-exclusive agent who operates in the Kongo Central region in the Democratic Republic of Congo (DRC). He started his business as an agent six years ago, first with Airtel Money and then with other electronic money operators.

Like others, Mr. Mataba had been motivated by the lure of commissions but over time, he saw profits decline. He continues, “If the providers improve their services, I will continue and ask my friends who are agents to continue too. Otherwise, we will stop and they will lose customers as happened with the transfer agencies “Ami fidèle” and others…”

Mr. Matamba knows that many people in his region work as agents, and has been concerned about their working conditions. He formed an agent association, and as president, he brings agents’ complaints to the attention of the suppliers’ representatives. Yet he believes that he has not yet been heard, and has decided to stop working with one supplier and is in the process of moving away from the others.

In the DRC, the digital financial service market has been booming. Mobile money operators mainly dominate it—although recently, financial institutions have started to develop their offers. One such institution is FINCA RDC, which was a pioneer in this field.

MicroSave Consulting (MSC) conducted a qualitative study in the Kinshasa, Central Kongo, Katanga, Kasaï, and Kivu regions. The team met stakeholders of the distribution chain from the five major suppliers, comprising division managers, sector managers, super-agents, and agents. MSC focused its research on understanding the behaviors, perceptions, and attitudes of agents, based on our MI4ID approach.

The study identified a wide range of agent profiles and approach models. Indeed, agents have a central role in the service distribution chain. Not only are agents the points of contact for customers, but they also represent a major expense for providers, costing 40 to 80% of the revenue generated by the activity. Providers must, therefore, approach the development and operation of agent networks with a clear strategy to ensure sufficiently rigorous operational control. It is paramount for a provider to build and maintain an optimal relationship with its agents.

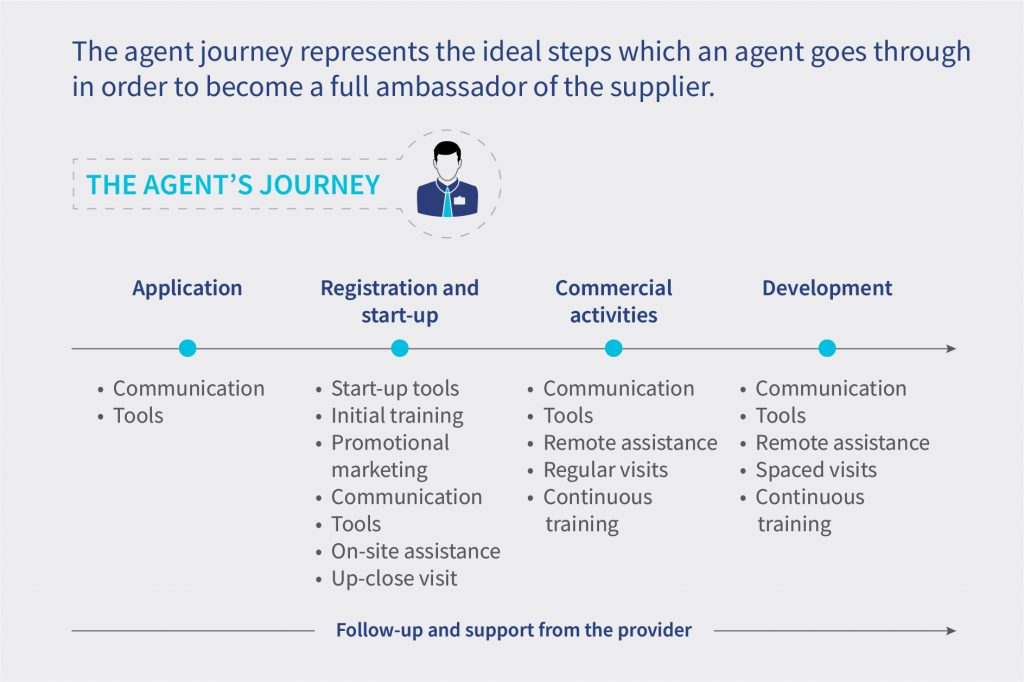

Using MI4ID approach allows to map the agents journey from the awareness stage to the development of the business stage, in order to understand what are the enablers and barriers to their success. The agent journey represents the ideal stages through which an agent evolves to become a full-fledged ambassador for the providers supplier. The support provided at each stage by the provider creates and boosts the agent’s loyalty. Agent path modeling makes it possible to capture and communicate an agent’s experience during a particular action or event.

An analysis of agents’ careers in the DRC has revealed key lessons that providers can use to improve their commercial relationship with agents and make them more accountable. The final objective is to guarantee a good level of service quality and reliability to clients.

1. From becoming acquainted with the function of agents to the application

Building knowledge and understanding the agent’s profession

From one prospective agent to another, the experiences of obtaining the right information concerning the role of an agent are different depending on the contact person. Family and close acquaintances who are already in the business play an important role in attracting the interest of a potential agent. They have a prescriptive role and are critical to winning the potential agent’s trust, especially with regard to the services of electronic money operators: access to the profession is perceived to be easy. No minimum level of education is required and it is possible to start an agency business with low investment in terms of equipment and location, and with low working capital in the form of liquidity.

The result is a strong demand from prospective agents that suppliers cannot meet, and the development of a market for the sale of SIM cards. Providers would do well to pay attention to how information is communicated to prospective agents and the channels used, given that the experiences of agents in the field are highly varied.

The purpose: Integrating the agent’s role

To reassure hesitant prospective agents, it is important that the provider’s sales representatives meet the prospective agent to confirm that the candidate matches the required agent profile. A prospective agent may have an existing relationship with the provider either as a credit customer, that is, as an agent for financial institutions or as an airtime credit reseller. For such prospective agents, the opportunity of becoming an agent through a rigorous selection process gives them a sense of importance and is crucial in establishing a sound relationship.

Obviously, the main source of motivation for prospective agents is the commission earned, and this usually means obtaining a regular but not necessarily high income. For non-dedicated agents, the possibility of stimulating the growth of the main activity is an important factor. When potential agents receive better and more realistic information from providers, they can get a sense of the working conditions and benefits expected through this activity more accurately.

2. Registration and launch of activities

In DRC, agents who work for electronic money operators but lack the official documents have to complete the registration process through an information sheet, which simplifies the procedure for setting up an agent account. However, this information sheet does not explain the rights and duties of an agent. Agents are not informed or trained in detail about what is expected of them in terms of work, how to carry out this work, and what to do in case of difficulties. It is essential to establish the principles of a partnership relationship with the agents because this will inform the choices that will guide the agents’ behavior during the implementation of the activities.

A second problem that agents face stems from the shortage of a start-up kit in the form of transaction booklets and marketing material, which some agents experience. This fosters a sense of inequality between agents and a supposed lack of consideration on the part of the provider. As a result, agents incur additional expenses, and this increases their expectations about the profitability of the activities. Agents with potential may also lose interest in the activity or fail to comply with the rules.

The providers could improve the stock management policy to ensure proper distribution of marketing materials to agents. They could also improve the tools for monitoring those in charge of supporting new agents and thus ensure better management of agents from the very beginning.

Agents need training that goes beyond simply learning how to do transactions. Such training would help them understand the intricacies of their role and help them succeed in the business. Providers should support agents throughout their careers through initial and continuous training that is diversified according to the agents’ capacities and aspirations. For agents of electronic money issuers, obtaining the status of agent issuance of the agent SIM card, equipment, and activation should be systematically pegged to the successful completion of the initial training. By incorporating practical exercises into the training, the agent will be able to assimilate the tasks expected of them.

3. Business management and development

Agents face a number of obstacles that prevent them from developing their activities successfully. First, the value proposition faces a challenge from the agents’ dissatisfaction with the commissions earned. The frustrations of agents and the predominance of transactions at the counter result in additional fees to clients, a loss of interest in this activity, and diminished quality of customer service.

Secondly, the frequency of payments and delayed payments by agents erodes their confidence in the supplier. Difficulties in managing commission payments compound the inability to grow capital and lead to attrition. Lastly, a lack of incentives discourages agents from selling the services. The provider should propose an economic model and value proposition for the agent that reflects market dynamics. The rewards must be a clever mix of monetary and non-monetary incentives.

Furthermore, in terms of the management of operations, the agents have mixed perceptions about the quality of support they receive from providers. To avoid making mistakes, some agents in the DRC allow customers to write down the account number on the transaction book or on the mobile phone, which increases the risk of fraud. Then in case of an error, it takes a long time to deal with the complaint. Moreover, poorly trained agents who are not familiar with the support mechanisms have to bear the costs by reimbursing customers. Therefore, the providers should invest in more sophisticated interfaces to reduce agents’ margins of error and shorten the time required to process claims.

Another challenge is liquidity management. Agents lack the capacity or willingness to invest capital into their float, and liquidity supply mechanisms are insufficient. As a result, they use informal strategies to compensate for this shortfall. The agent is forced to keep clients waiting indefinitely for them to replenish the float. They cope by either refusing a type of transaction, by dividing a transaction between several agents, by transfer of money between agents, and by keeping the client’s money until sufficient funds are available. However, informal procurement strategies can create risks of fraud and breach of trust. To avoid the lack of liquidity, the provider must ensure a greater variety of supply distribution methods, such as fixed and mobile points, and set a satisfactory level of supply service.

Lastly, there is the problem of business development: the agent as a partner must contribute to customer development and needs support from the supplier to deal with customer complaints properly. The supplier needs to encourage agents to recruit prospective clients and manage customer relations. The management of an agent’s career seems to be an area that is lacking in the partnership relationship.

Although the Congolese agents interviewed planned to remain in the business for an indefinite period, some agents have the ambition to move up the distribution chain ladder but do not have a direct relationship with the suppliers and are neither informed nor supported to achieve their objectives. The provider should step up support to agents to foster motivation and success. In short, a study of the agents’ journeys in the DRC highlights not only the opportunities available but also the bottlenecks that curtail the agents’ progress towards success and ultimately encourage agent attrition.

For suppliers, the improvement of the relationship with agents hinges on the win-win principle, which is guided by an understanding of agents’ aspirations because the agent needs to feel included. To establish good relations, the provider must also define and implement a strategy on agent satisfaction management. This entails not only setting up a more tailor-made system of agent segmentation and management but also strengthening the quality of the network and systems to monitor communication with agents. These measures are necessary because agents are the pillar of customer relations. An investment, therefore, guarantees the growth of digital financial services.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.