Income plummets in Bangladesh as a result of Covid-19 – Stuart Rutherford’s Hrishipara diaries reveal, in graphic detail, the daunting scale of the challenges facing the poor worldwide. “Anxiety prevails, as shown in the end-March version of the monthly survey we take of our diarists’ thoughts about the month just past, and their hopes for the month to come. The fear, overwhelmingly, is of loss of income. Much of what needs to be done by policymakers is already understood. This blog testifies to, rather than reveals, those needs. What is described here suggests than from the diarists’ point of view the top priorities are relief measures to ensure food and income security and to prevent distress sales of assets. Financial services need to be unlocked, above all to release savings in MFI accounts. And the high level of anxiety means people need, somehow, to be reassured.

The DFS ecosystem in Bangladesh

The digital financial services (DFS) landscape of Bangladesh evolved multifold in 2019. This can be traced to the efforts of the government, the banking regulator, and policymakers in Bangladesh. As of December 2019, the country had 971,000 MFS agents who, on average, conducted 7.33 million daily transactions worth USD 156 million. Bangladesh has a total of11,320 agent banking outlets that serve 5.26 million customers. At present, 16 companies offer mobile financial services and 21 banks offer agent banking services. In addition, nearly 92% of the population now live within 5km of a financial sector access point.

TIGHTENED MONITORING: In 2019, two providers had to close their mobile financial services (MFS) operations-IFIC and Exim Bank. The providers did not have a substantial market share and were on the verge of being instructed to surrender their MFS licenses by the regulator due to their long-term dormancy in the market as MFS players. This move propagated a clear message-the regulator has tightened its grip on MFS and every player is expected to perform.

THE LAUNCH OF EKYC: Bangladesh Bank (BB), with approval from the Election Commission, initiated a pilot on e-KYC in September, 2019 with 15 commercial banks and two MFS providers. The list of participating commercial banks included state-owned commercial banks and agent banking providers, while bKash and Rocket were the two MFS players. The ICT Division of the government launched a gateway for easier and faster verification of national identity cards (NIDs). The “Porichoy” portal, which is connected to the Election Commission (EC) database, enables public and private organizations to provide services by verifying the NID cards of their customers. Electronic Know Your Customer or e-KYC mechanism, is a convenient process for the customers and helps reduce cost and time during enrollments.

INCREASED MFS TRANSACTION LIMITS: Bangladesh Bank raised the transaction ceiling for MFS in May, 2019. This had been a consistent demand from various industry players and policymakers. The increased limits affected multiple payment services that the MFS providers offered, such as inward remittances, e-commerce payments, business payments for micro and small enterprises, and payroll disbursements across the country.

PSP LICENCE AND E-MONEY GUIDELINES: BB issued guidelines for e-money service (EMS) in February, 2019 to highlight the transaction limits for e-wallets and to identify who can issue e-money. In July, the central bank increased the limit of transactions for e-wallets and clarified that only providers with a payment service provider (PSP) license can offer e-wallet services. At present, Bangladesh Bank has licensed iPay and Dmoney as payment service providers. This was a proactive move from the regulator to clearly state that FinTechs can operate in Bangladesh with a PSP license. Further, with the increased transaction limits, it sought to gain the acceptance of customers to FinTech services.

A major reason behind the success of various initiatives by the Bangladesh Bank is its support for the notion that innovations around use-cases are needed to drive transaction volumes and values. Guidelines such as widening the transaction limits and allowing non-bank entities to offer ATM services are critical to foster innovation and boost competition in the industry.

The future outlook for 2020

One aspect that we wished to include in our developments is the commitment of the regulator to drive the agenda for the financial inclusion of women. Bangladesh Bank has supported taking women agents on board and has made toolkits available for the industry players to develop financial products for women. The toolkit was a result of MSC’s study commissioned by IFC. BB also incentivizes banks to support the provision of credit to women entrepreneurs. Further, DFS providers target women workers in readymade garment factories with tailor-made products such as different cash-in and cash-out charges. Though these innovations drive gender inclusion in a way, we are yet to see these extended to the larger women population. MSC believes bridging the gender divide will be a top priority for Bangladesh Bank in 2020.

We also believe that the regulator will need to encourage agent banking service providers. Agent banking in Bangladesh has had organic growth until now. The country had 5.26 million agent banking customers, as of December 2019. The agent banking setup is complex and these agents have to invest around BDT 150,000-200,000 (~USD 2000) to start an agent banking outlet. However, we believe the providers may have been conservative in their outreach strategy. In countries such as India and Kenya, banks have been able to penetrate even the most distant areas through agents.

Another area, or rather, organisation that will demand the focus of Bangladesh Bank in 2020 is Nagad, the digital financial service of Bangladesh Post Office (BPO).The MFS service has already picked a significant market share by registering more than 10 million wallets and 130,000 agents across the country within the first nine months of its commercial operation. BB may want to work with BPO to ensure that the MFS players and Nagad remain competitive within a level playing field of market operations.

Finally, the initiative of Bangladesh Bank that allows non-bank entities to set up “White Label ATMs (WLAs)”and point-of-sale (POS) terminals is worth mentioning. As per the World Bank data from 2017, with 8.07 ATMs per 100,000 people, Bangladesh ranked the lowest in terms of the density of ATMs against the size of the adult population. This is in contrast to China, India, and Pakistan with 81.45, 22.07, and 10.44 ATMs per 100,000 people, respectively. These entities will operate under the payment system operator (PSO) license, as of September, 2019. At present, only three PSOs are operational in Bangladesh, as per a report from Bangladesh Bank. We believe this move will encourage the participation of the private sector in the financial services market.

Given that around 50 percent of its population remain unbanked, Bangladesh will need to take policy decisions to push the service providers further in 2020. MSC believes that the key focus areas for Bangladesh Bank shall be to push for technological disruption, expand its work in e-KYC, tailor the design of products and services for women, and utilize the potential of agent banking.

The blog was also published on The Financial Express on 13th of March, 2020

Same problems, same inequalities: Women in the digital gig economy

“Gig work provides the flexibility I need but not the money I deserve…”

The world is increasingly going digital and technology that could only be imagined a decade ago is now a reality. Innovation has had a significant impact in encouraging women’s participation in the delivery of services enabled by technology platforms. This has given rise to the gig economy—an ecosystem that facilitates workers who are either employed or unemployed to earn income through part-time jobs, referred to as “gigs”.

The digital gig economy in Africa has quickly gained prominence over time, and continues to enhance opportunities for youth and women. Research ICT Africa estimates that by the end of 2018, there were 277 unique digital platforms in Africa alone serving close to 5 million gig workers. Some digital platforms operate internationally, such as Airbnb, Uber, Jumia, which serve multiple markets. Others are more localized and target their own markets, such as Sendy and Lynk in Kenya, goDropping in Ghana, and Gokada in Nigeria, among others.

Gender dynamics in the gig economy

Some of MSC’s recent research work in Kenya indicates increasing participation of women, especially in the blue-collar digital gig economy. Emerging platforms are enabling women to take up gig work and use their time more effectively. The flexibility of gig work enables women to offer services they are skilled at and schedule their work according to their availability. However, we observed that women were more involved in traditionally female-oriented jobs, such as hair-dressing, beauty, and housekeeping. Women take on these roles because of their familiarity in that line of work, their risk-averse nature, as well as the dictates of societal norms. Men in the gig economy are more involved in jobs such as delivery, construction, driving, and home repairs.

A behavioral analysis of gig workers reveals significant differences between the motivations for women becoming gig workers as opposed to men.

This nature arguably—and inequitably—predisposes men to navigate gig work on digital platforms in a more lucrative manner. We have examined some of the reasons for the gender gap and would like to propose some measures to overcome the discrepancy.

Women face unique challenges when they use digital gig platforms to source work and market their products and services. In many emerging economies, ownership of digital devices that enable access to gig platforms has historically been uneven between men and women. Gig platforms in Kenya, such as Littlecab, a ride-hailing service or Sendy, an errands company, demand 24-hour availability to offer services. Women’s availability on digital gig platforms that require physical presence is restricted due to domestic demands. The number of hours that workers log on most platforms informs their ratings. This, in turn, affects their presumed relative level of capability negatively. Consequently, women get less gigs on platforms that assign job opportunities based on user ratings, which are influenced by platform experience.

Female gig workers and customers alike also face increased security risks in gig work that require their physical presence. For example, female customers express higher security concerns when hailing taxis on digital platforms. Female workers report instances of sexual harassment and thus are less willing to serve male customers, especially at odd hours of the day. In an interview with a female worker who offers beauty and wellness services, she indicated that “unwarranted demands” from men had driven her to avoid work requests from male customers.

As in the workplace, women on these platforms struggle to earn equitably. Women are observed to be more flexible in pricing and are more susceptible to being underpaid on gig platforms—including white-collar gig work. This sometimes goes to the extent of not covering the costs they incur to deliver the services. Consequently, women gig workers who charge prices commensurate with men for their services often get less business on digital platforms. A system where women charge less than their male counterparts leads to a devaluation of the services they offer.

Even as they deal with these challenges, female platform workers either do not get sufficient work or drop out entirely from the digital gig platforms.

How can we encourage women to participate in the gig economy?

Stakeholders can explore different measures to address these challenges and encourage the continued participation of women. Some platform owners have been proactive in putting in place measures to resolve these issues.

To account for the intermittent availability of female workers, a system that allows workers to indicate when they are available could limit the negative implications that arise out of the level of platform experience of female workers. This way, the platform would not automatically discriminate women on ratings when they are not available.

Some platform owners provide an option for users and workers to choose whom they would like to receive services from or serve. For example, Bolt, a taxi-hailing app in several countries in Africa, allows female customers to choose female drivers and vice versa. AnNisa is a women-focused taxi-hailing platform that is run by women and serves women exclusively.

Some platform owners have implemented standard pricing for specific services to ensure the workers get adequate pay for their work. Platform owners could also put in place algorithms that encourage uniform pricing and let users simply choose a gig worker based on their respective ratings. Alternatively, gig platforms should explore measures through which customers can provide quality of service reviews that are used to rate workers on the platform. Higher ratings should allow workers to justify higher pricing, rather than ascribe to standard platform pricing.

Women’s empowerment through increased participation in the gig economy

Participation of women in the digital gig economy not only enhances employment opportunities and provides a source of income; it also helps to create a digital footprint of their work, and financial records in several instances. This, in turn, provides necessary data that financial institutions could use to design the right products and services to enhance women’s financial management and risk mitigation. When women are financially independent, it enhances their decision-making power, which boosts women’s economic empowerment.

We have a way to go to harness the gig economy for good.

MSC conducts a successful event on enhancing women’s economic empowerment through financial health with NITI Aayog and the Bill & Melinda Gates Foundation

MSC concluded a workshop in Delhi on 4th March, 2020 in collaboration with NITI Aayog and the Bill & Melinda Gates Foundation. The workshop, titled “Enhancing women’s economic empowerment through financial health—Insights from NITI Aayog’s transformation of aspirational districts” saw participation from financial inclusion experts, policymakers, and regulators across industries. The participants deliberated on policy and product recommendations that the government and financial services industry can adopt as it works towards greater financial health of women.

The event started with the keynote from Ms. Sarah Willis of the MetLife Foundation, where she spoke on setting the context on women’s financial health. This was followed by the inaugural address by Ms. Archana Vyas of THE Bill and Melinda Gates Foundation, India, and the keynote address by Ms. Alka Upadhyaya, Additional Secretary at the Ministry of Rural Development.

A panel of experts also discussed issues around women’s financial health for impactful women’s economic empowerment. The panelists included Mr. Anjani Singh of the Bill & Melinda Gates Foundation, Humaira Islam of Shakti Foundation Bangladesh, Ms. Jayshree Vyas of SEWA Bank, Ms. Manisha Sinha of India Post, and Ms. Varnali Deka, District Collector, Goalpara. The media across the country picked up various insights from the event conducted. Click through the links below to read a few mentions in the media.

Online

Event: Pradhan Mantri Ujjwala Yojana Achievements and implications on gender and the SDGs, and the way forward

About the event

The workshop will reflect on the achievements of PMUY over the past few years and highlight key lessons from the scheme with respect to policy design, targeting, coordination, implementation, and monitoring. It will also explore the impact of PMUY on gender, environment, and the health status of women and poor households. The workshop will commence with a keynote address from Shri. Dharmendra Pradhan, the Hon’ble Minister of Petroleum and Natural Gas. It will bring together various policymakers, senior officials of oil marketing companies (OMCs), sector experts, policy analysts, LPG dealers, and beneficiaries of the PMUY scheme.

For further information please see the event agenda. To register write to us at director@microsave.net.

Background

Pradhan Mantri Ujjwala Yojana (PMUY) was launched in May, 2016 with an objective to provide clean cooking fuel to poor households through LPG connections. PMUY set an ambitious target to reach 8 crore poor households by March, 2020. The scheme, however, reached this milestone seven months ahead of its schedule.

PMUY is a grand success story that has accelerated India’s progress in attaining the sustainable development goals—SDG 3: Good Health and well-being, SDG 5: Gender equality, and SDG 7: Affordable and clean energy. Ujjwala has replaced polluting firewood with clean fuel and provides new LPG connections in the name of adult women from poor households. This is a study in the empowerment of women and in providing a healthy indoor environment.

To dive deeper read our demand side diagnostic study of LPG refills and watch these videos on PMUY: challenges and road ahead, PMUY: benefits unfolded and PMUY: Building smiles and changing lives.

MSC conducts a successful workshop on the achievements of Pradhan Mantri Ujjwala Yojana (PMUY)

New Delhi, 06th March, 2020: MSC (MicroSave Consulting) organized a workshop on the achievements of Pradhan Mantri Ujjwala Yojana (PMUY). Shri. Dharmendra Pradhan, the Minister of Petroleum and Natural Gas, attended the workshop along with several beneficiaries of the Ujjwala program, delegates from oil and gas supplier agencies, health professionals, regulators, and policymakers.

The Pradhan Mantri Ujjwala Yojana (PMUY) was launched in May, 2016 to provide clean cooking fuel through LPG connections to women in rural households. The program has benefitted 97.4% of the beneficiary households in the last five years. PMUY set a target to reach 8 crore households by 31 March, 2020 but the government has managed to achieve this objective seven months before the deadline.

While congratulating all women beneficiaries of PMUY on this achievement, Shri. Dharmendra Pradhan said, “I consider myself fortunate to be a part of this initiative and would like to thank the 8 crore women who believed in us and trusted us. I would urge all women beneficiaries to use LPG cylinders for cooking purposes and refrain from using polluting fuels to reduce exposure to harmful smoke and maintain a healthy lifestyle. Smoke can also cause irreversible damage to the fetus, which has a high social and financial cost to the family and society.”

Speaking at the session, Graham Wright, the Group Managing Director of MSC said: “PMUY has made an extraordinary achievement by reaching 80 million households that now have access to significant forms of cooking.” He added: “PMUY has differentiated itself from other DBT programs through precise targeting, faster implementation, and redistribution of savings that involved the elimination of duplicates and the “Give it Up” campaign. These integrated efforts have led to an estimated savings of USD 9 billion to the exchequer. As a result, many other countries are learning from and adopting PMUY’s model of LPG subsidy.”

The discussions at the workshop’s first panel on the “Key Lessons and perspectives from PMUY” highlighted that approximately 15-20% of the beneficiaries do not use LPG at all despite having a connection. This is due to multiple barriers, such as affordability, accessibility, and behavioral issues.

The second panel of the workshop was focused on the impact of PMUY on the environment and the health outcomes of women. The panel had senior representatives from the Centre for Catalyzing Change, the Institute of Economic Growth, Government Medical College and Hospital of Chandigarh, Jhpiego, and the Clinton Health Access Initiative (CHAI). The panelists mentioned how PMUY has helped cut the greenhouse gas emissions through the reduction of smoke generated by polluting fuels. The event was extensively covered by the print media as well as online news agencies.

To explore the media coverage in detail, please take a look at the links given below:

Trust Busters! A dozen reasons why your potential customers do not trust your agents (particularly in rural areas)

Only about 22% of direct benefit transfer recipients in Krishna District from the state of Andhra Pradesh (AP) in India had ever used an agent for cash out. Most withdraw their benefits at bank branches. This trend is disturbing for two main reasons. Firstly, Krishna District is believed to have the most advanced digital ecosystem of all 732 districts in India. Secondly, AP is recognized as the leading state in using technology to improve the delivery of public services, programs, and subsidies.

Only about 22% of direct benefit transfer recipients in Krishna District from the state of Andhra Pradesh (AP) in India had ever used an agent for cash out. Most withdraw their benefits at bank branches. This trend is disturbing for two main reasons. Firstly, Krishna District is believed to have the most advanced digital ecosystem of all 732 districts in India. Secondly, AP is recognized as the leading state in using technology to improve the delivery of public services, programs, and subsidies.

So why do people not use agents? In part, for rural people at least, because agents they are not available in or near their villages. But also for a range of reasons around their trust in those agents. Indeed, for many consumers, the kirana (grocery) store is not a desirable agent. This is because storekeepers are often key influencers of village gossip or are at its epicenter. Thus, a storekeeper who acts as the local agent presents a risk of loss of confidentiality within the community. Moreover, many households borrow from the store in times of need, so a storekeeper who is an agent creates a very real risk that the money they cash out may be commandeered to pay off debts.

Furthermore, many rural people travel each week, or every two weeks, to local market towns to perform tasks and conduct a variety of transactions. Therefore, they can go to the bank or to another agent in the market town frequently, with limited marginal costs. This option, however, overlooks two key factors in favor of continuing work to extend the “agent frontier” to establish agents closer to remote rural villages.

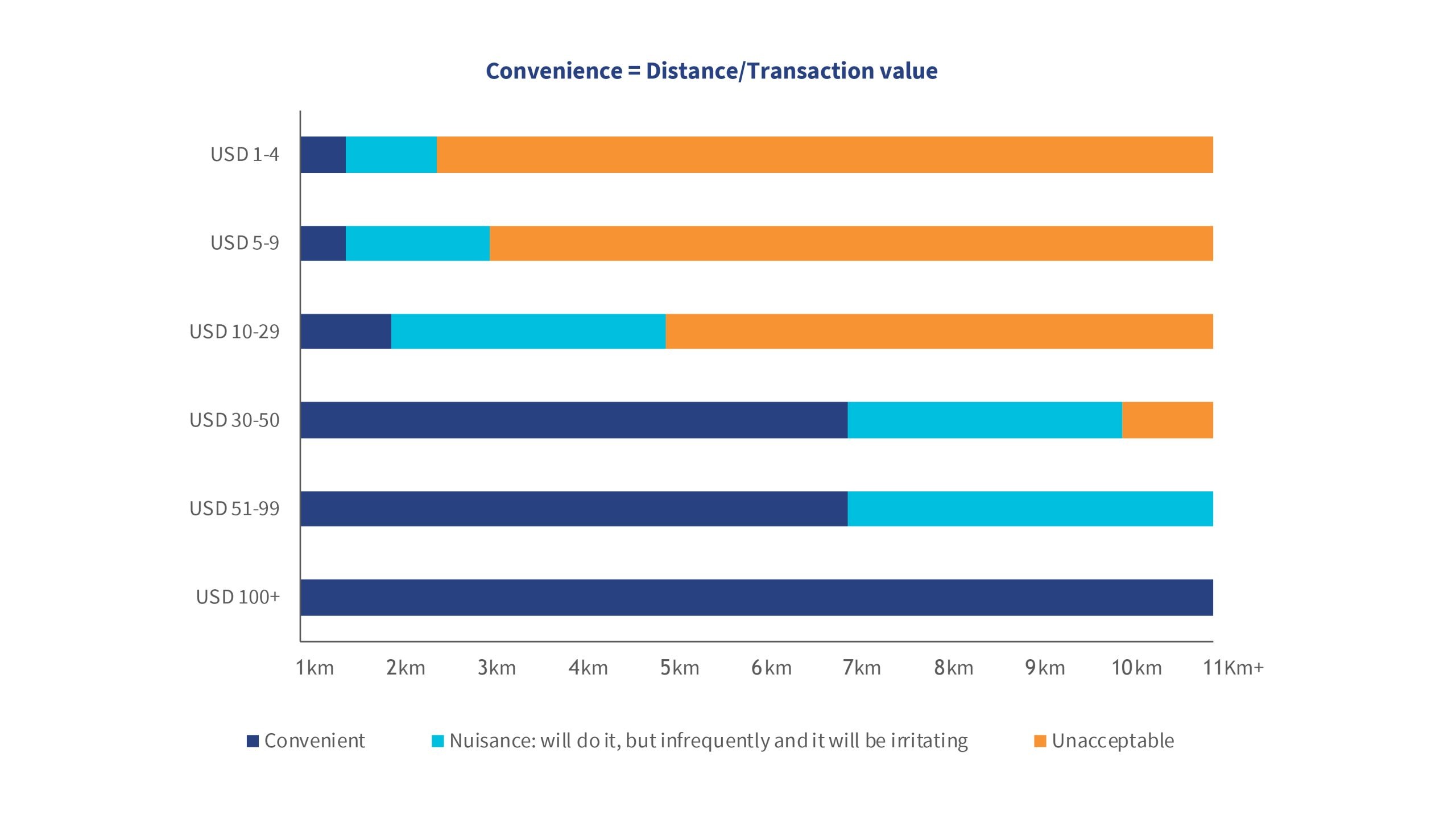

The first factor is gender—in many countries, only men travel to the market town. Yet, women want and need to conduct many of their financial affairs in confidence, often without the knowledge of their husbands. Access to agents within the locality will enable women to conduct financial transactions on their own. The second factor is small transactions, particularly savings, which can be encouraged by having agent points nearby. As IFC has already pointed out, the larger the transaction, the further people are willing to travel to conduct it (see figure below). Therefore, if we wish to help people save by putting aside small amounts outside the house, and thus away from the temptations of “frivolous spending”, or from the predations of marauding relatives, they will need an agent nearby.

These, and other issues related to the digital divide, make the work of MSC, BCG, and CGAP on expanding the rural frontier critical. Creative, country-specific solutions will be essential to enable profitable agents beyond the current frontier. Such solutions include:

- Differentiated agents and enhanced commissions for processing G2P payments in India;

- Alignment of regulations, particularly on who is permitted to be an agent and what products they are allowed to offer, as well as commissions for processing G2P payments in Indonesia;

- Broadening the range of products offered by mobile money agents across Africa;

- Enhancing the number, role, profile, and support for female agents across South Asia and parts of Africa;

- Leveraging technology to achieve efficiencies in “Distribution 2.0”; and thus ultimately

- Re-imagining the last mile of agent networks.

MSC conducted its initial analysis of consumer protection issues in India in 2016 as the BC agent model was rolling out at scale. We found that many people trusted the agents—not least of all because they were dependent on agents to conduct “agent-assisted” transactions. This seems to be changing. In our extensive fieldwork across India, we are increasingly hearing a dozen issues that are eroding trust in agents.

And the problem is not confined to India…

We drew similar conclusions of our analysis of the operations and impact assessment of the PKH conditional cash transfer system in Indonesia. We found that only 18% of beneficiaries used agents to withdraw their funds. In part, this was because agents are simply not present in many rural areas, so beneficiaries have to go to the nearest ATM. Yet even in areas where agents are present, many lack the liquidity to provide the big cash pay-outs as beneficiaries withdraw the entire PKH payment in one go.

As a result, even PKH facilitators and banks discourage agents as cash-out points. Moreover, agents charge informal fees to make cash payouts. The median fee charged is IDR 10,000 (USD 0.73) per disbursement, which makes ATMs more cost-effective.

Once again, consumers have lost trust in the agents’ ability to meet their needs in a transparent and honest manner.

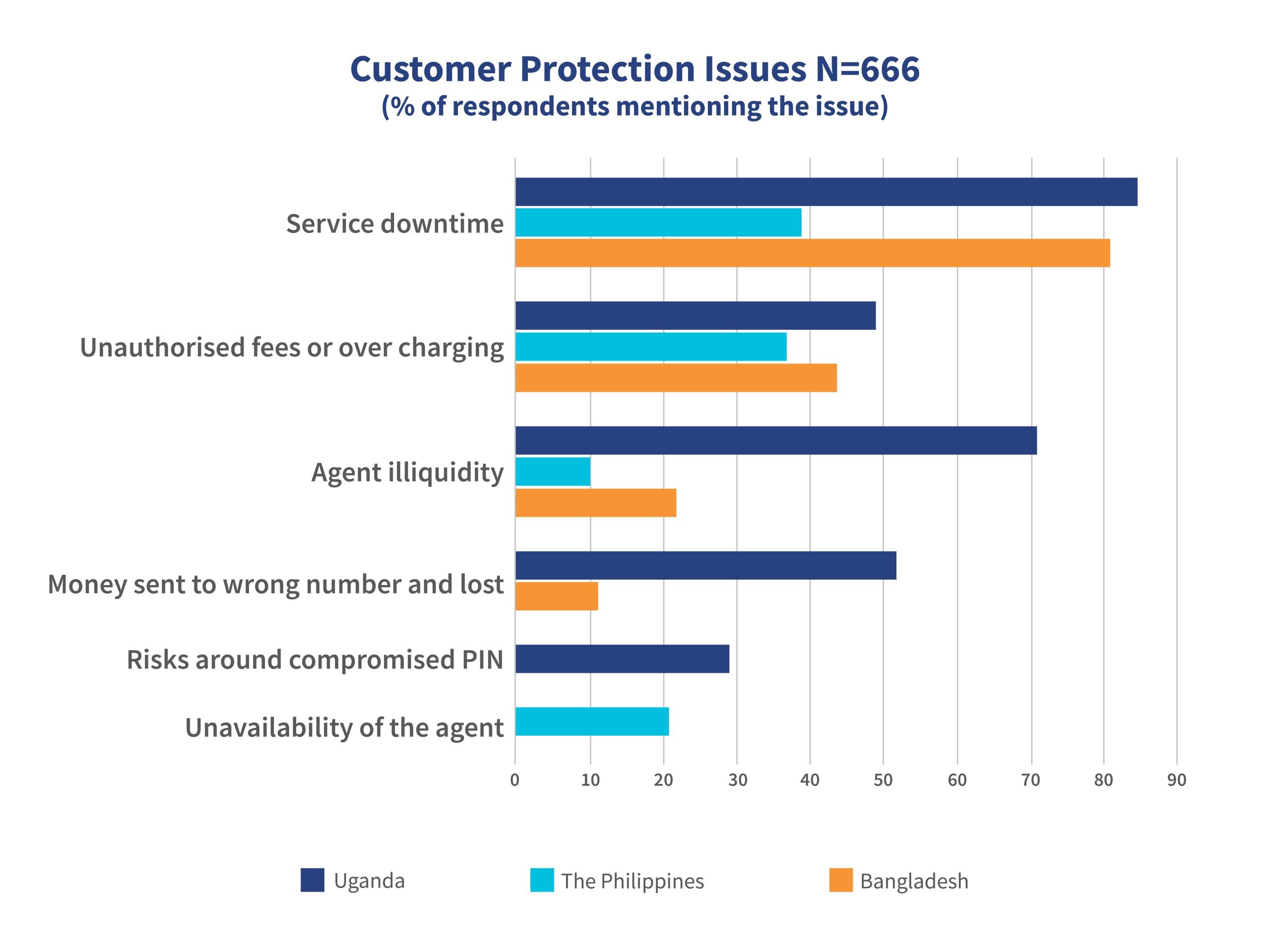

We picked up similar issues in our study on customer service for CGAP back in 2015, when we identified three key issues that were eroding the trust of customers in three different, but relatively mature markets. These issues were 1. Service or network downtime; 2. Unauthorized fees charged by agents; and 3. Agent illiquidity.

It was clear from the analysis that many registered customers relapse into inactivity when they find it either impossible or too intimidating to make transactions. Customers cannot transact during system downtime, or in the case of absent or illiquid agents, and feel intimidated by the risks of sending money to a wrong number, or losing or compromising their PIN. Other customers choose to protect themselves by using over-the-counter (OTC) services in preference to registering or keeping money in their mobile money wallets. All these limit the use and potential of digital financial services.

Furthermore, given the importance of word of mouth, which MSC estimates drives around 60% of decision-making on the adoption of financial services, bad experiences spread quickly in rural communities—amplifying the erosion of trust. In the words of one customer, “We keep hearing mobile money users complaining about unstable network, delayed service, missing money, and many other negative comments about mobile money. Why then should we register for these services?”

This lack of trust represents a real and expensive problem for providers. The GSMA 2018 State of the Industry Report notes, “34.5% of the world’s registered accounts are now active [90 days]”. Or, put another way, only one in three of digital financial services accounts opened are used to conduct more than one transaction in three months. Given the cost of customer acquisition, one cannot help but think that investments to improve trust in digital financial services would make economic sense.

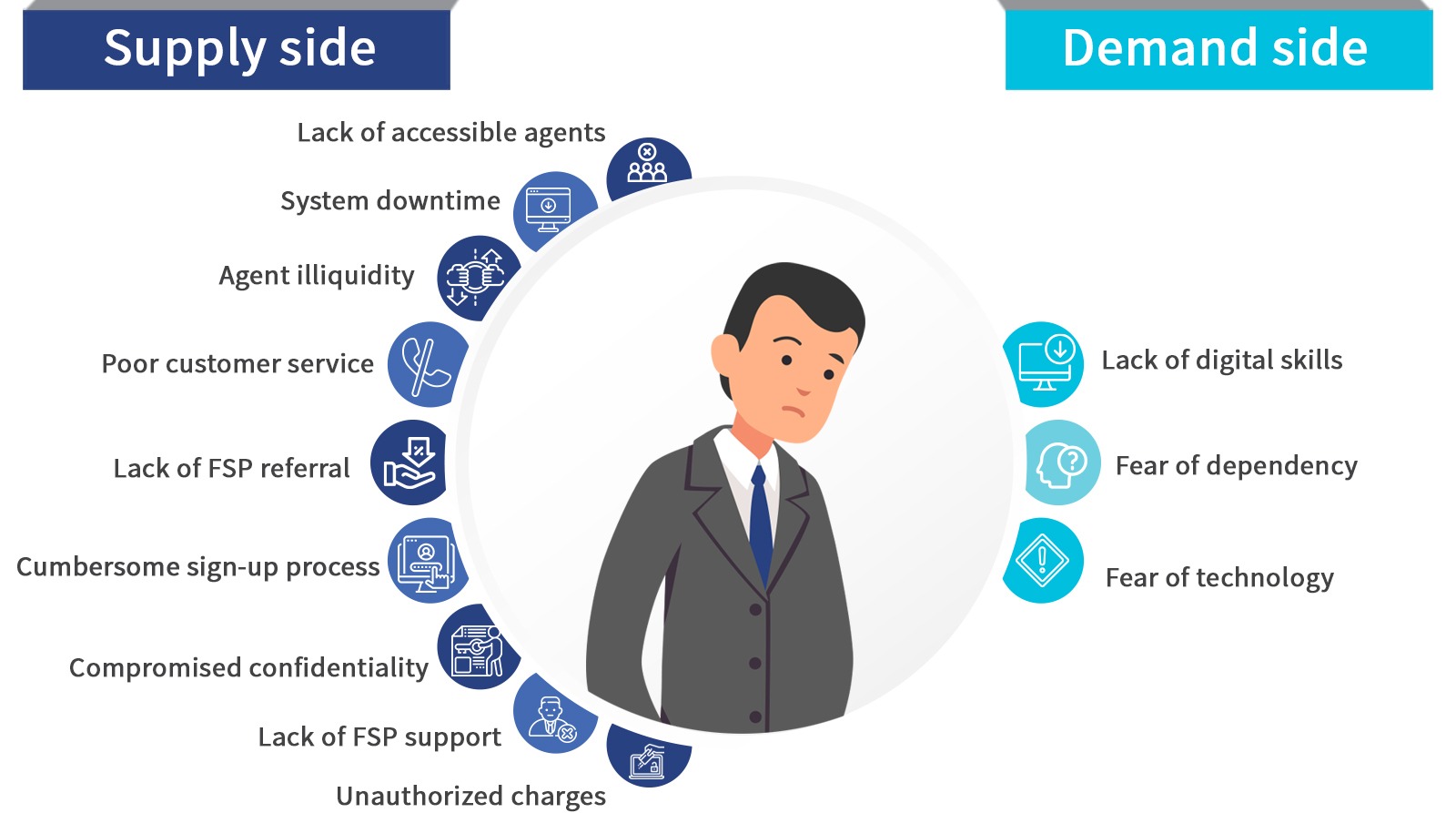

So what are the dirty dozen trust busters?

Supply side:

- Lack of accessible agents: when there are too few accessible cash-in or cash-out agents to provide credible access to basic services. In many markets this is driven by agent closures and churn, which can leave customers without access to their money. In some countries, this access is a question of opening hours, for example, in Zambia and Kenya, where most agents only work the hours and days that bank branches do. Customers in these geographies are unable to find agents to serve their transactions on weekends or after 5 pm.

- Service or system downtime: when technological issues mean that users are unable to access their funds or transact. Agents often use this as an excuse not transact when they face liquidity issues.

- Agent illiquidity: when agents lack enough e-money or cash to make cash-in or cash-out transactions. Customers find it difficult to trust an agent who is frequently unable to conduct transactions.

- Poor customer service: when agents are provided limited training and thus their ability to conduct transactions, explain products, or manage customer complaints is compromised. Poor or nonexistent agent and customer support through call centers can worsen the problem.

- Lack of referral from the FSP: when the local branch does not refer customers to agents—this is seen as a sign that they are not sanctioned or to be trusted. In some instances, where branch staff fear a loss of jobs, we have seen branches undermining agents by saying that people should carry out transactions at the branch where it safer and cheaper.

- Cumbersome sign-up process: when sign-up and know your customer (KYC) procedures are complex, convoluted, and time-consuming. Potential users, particularly those new to digital financial services, will often simply give up and not complete the registration process. When agents help with the sign-up and are apparently unable to make it quick and easy, trust is compromised.

- Compromised confidentiality: everyone, not just those who depend on agent assistance, wants confidentiality in their financial transactions. As we have seen in India and elsewhere, customers often do not consider a hyper-local agent based in the same village as desirable for exactly this reason.

- Lack of support from the financial service provider (FSP): when the FSP does not provide: 1. marketing support for the agent network to enhance its credibility and/or 2. monitoring of agents either directly, or through third party representatives commissioned to monitor and support the agent network.

- Unauthorized charges: when agents charge additional amounts for transactions, as is now common across the globe.

Demand side:

- Lack of digital skills: when potential users lack the knowledge or capability to use digital interfaces on their own. This is, unsurprisingly, more common among the oral segment for whom no intuitive interfaces have been rolled out.

- Fear of technology: when potential users lack understanding of the technology, which makes them afraid of losing funds by making the wrong keystrokes or because funds “disappear”.

- Fear of dependency: when users are dependent on agents for assistance, thus compromising confidentiality and increasing vulnerability to unauthorized charges or even fraud by agents.