We have seen in a number of countries how, when they work well, branchless banking and especially mobile money systems can reach millions of people. But beyond the headline numbers on customers reached, the record of such systems as a vehicle for financial inclusion is still mixed: we can hardly talk about a globally-proven solution.

Let me draw some stylized facts from the international experience:

Branchless banking systems have only tended to work at large scale. There does not appear to be an easy, gradual incremental path for providers wishing to deploy branchless banking solutions. There seems to be a chasm between the large numbers of institutions that have run sub-scale pilots and the much smaller set that have succeeded in establishing commercially sustainable branchless banking operations. As a result, there are very few examples of smaller entities –whether banks, mobile operators, microfinance institutions, or other third parties— successfully incorporating branchless banking solutions in a sustainable, impactful way.

The space is still dominated by mobile operators. Few banks in the world seem to have made sizable bets to develop agent networks, and most of those who have built agent networks have tended to see them as an add-on for specific services (e.g. utility bill or credit collections, social welfare payouts) or for specific segments (e.g. poor, rural people) rather than as an extension of their core business. Non-financial companies with a retail or distribution background have been reticent to jump into space. Therefore, space has been left largely to mobile operators, who have an easier time conceiving of a transactional, high-volume, low-touch approach.

Customers tend to use branchless banking systems relatively infrequently, and only for a limited range of applications. The median active user is likely to make a transaction only once or twice a month – typically a remote person-to-person or bill payment, and some mobile airtime purchases. It is not common to see branchless banking being a “stepping stone” or “gateway” into the use of a fuller range of financial services. In fact, where mobile money has flourished, it is far more common to see the opposite: fully-banked people adopting mobile money as “liquidity extension” to their banking service.

Branchless banking is not fundamentally reducing people´s reliance on cash. Most mobile money transactions start and end in cash. We may refer to it as a mobile or electronic transaction, but most customers would understand it as a cash-to-cash money transfer, akin to what Western Union has always done. The payment may be electronified, and as a result, the distance that cash needs to move is much reduced. But the underlying money is not electronified since the value is largely held in cash before and after the transaction. Branchless banking systems have generally failed to position the store-of-value function of customer accounts among the previously un- or under-banked, and the result is that the majority of accounts are actually or practically empty.

Branchless banking systems tend to exhibit relatively low levels of service innovation. Branchless banking –and in particular mobile money— systems are about exposing financial service platform functionalities directly to the customer by digital means. But this has not brought on the kind of constant innovation that has been the hallmark of internet business models. Of course, the need to work on basic phones has hampered the ability to innovate, but the fact remains that most branchless banking providers have brought on new services or optimized their user interfaces not more frequently than annually, if at all.

There are of course counterexamples to each point, but they are few. Zoona in Zambia is a small, independent organization growing a purely mobile-based money system incrementally by exploiting specific niche opportunities. The much larger bKash in Bangladesh operates largely as an independent entity, even though it is backed by BRAC Bank which is part of one of the most influential organizations in the country. Equity Bank in Kenya is making a big push into the mobile space with its acquisition of a mobile virtual network operator (MVNO) license.

The above factors are all inter-related, like distinct symptoms of a broader malaise. The pattern of starting and ending in cash most transactions in cash raises costs and presents a brutal business challenge of having to ensure sufficient density of liquid agents in each locality served. Higher transaction costs make the system less compelling for lower customer-value-adding transactions, such as savings or face-to-face merchant payments, which on the other hand, offer the highest potential pool of transactions. In the face of low usage levels per customer and the inherent network effects of payment businesses, the economics can only work for those able to aggregate the largest number of customers, and in particular mobile operators with a mass-market transactional business model. Other big players such as banks may not see a positive business case, or if they do, may fear that the new branchless banking activity may cannibalize their core business or be margin dilutive. As a result, few players in each market enter the business, and when they do they tend to underinvest in IT platforms, staffing and marketing spend. With such shoestring resources, they become easily overwhelmed by day-to-day operational issues and do not devote much attention to the service roadmap. With lack of effective competition, innovation falters.

Let´s not concede that branchless banking must push the unbanked into the arms of the larger banks and telcos in the country. Now that we have a good decade of experience with mobile financial services, it behooves us to look back on the trajectory and see what course-corrections can be made to spur more competition and innovation for the benefit of the world´s poor. This should start with regulation, which needs to shift from being merely enabling to being pro-competitive, as I argue in this paper.

Until this month RBI maintained the view that only licensed commercial banks can offer cash-out services. As a result, a number of banks and non-banks formed partnerships. In fact, the RBI’s view hasn’t changed. The RBI has simply decided to regulate non-banks offering business correspondent services too, as differentiated, Payments Banks (PB).

Business correspondents (BC) were the first set of non-bank players allowed to partner banks in the pursuit of deepening financial services and furthering the cause of financial inclusion. The issuance of BC guidelines back in early 2006 spawned a host of experiments where BCs appointed by banks, collect deposits and provide specified services on behalf of banks. Eight years on, beyond enrollment statistics, the BC model hasn’t resulted in very meaningful outcomes. Sadder still, hardly any BCs have succeeded at scale. In this context, scale refers to parameters such as:

a) being a sustainable, profitable business model

b) serving a significant percentage of transacting (active) accounts

c) garnering savings deposits that are material to sponsor banks

d) customer accounts with satisfactory average balances, and finally

e) a modest percentage of customers to whom the bank could extend credit

The first large-scale attempt at cracking the non-bank vs bank impasse was through the joint venture between SBI-Airtel / Airtel-SBI (depending on which side of the fence you sit). At the time of its announcement, there was much hope and excitement. Unfortunately, that engagement soured, very uncannily imitating a Bollywood first family scion’s engagement breaking, just a few years before.

The other non-bank players (like ALW, Eko, Fino, Itz-Cash, Oxigen and Suvidha, to name a few) nurtured their unequal relationships trying to take financial inclusion and domestic remittances where only the post office had been before. Cajoled by the RBI (much like an elder asking children upset over a tiff to hold hands) the telcos stitched reluctant partnerships with banks. Airtel / ICICI Bank, HDFC / Vodafone, Airtel / Axis Bank, Axis Bank / Idea, ICICI Bank / Tata Teleservices entered into BC arrangements through 2011-12. Several of the larger players obtained Prepaid Payment Instruments (PPI) Issuer licenses. Even so, the bugbear of cash-outs did not go away. Until the issuance of the PB draft guidelines.

Telcos will still likely consider the PB guidelines only a small win. However, it would seem that should the telcos go ahead and obtain PB licenses, there appears to be no compelling reason for them to want to hold on to their banking relationships; particularly now that they are allowed to hold deposits, deploy surplus beyond CRR / SLR for income-generation and cash-out depositors. However, given that over a quarter of telco revenues comes from postpaid (read credit), telcos may have reason to feel that they’ve drawn the short straw, with the PB guidelines preventing them from offering credit. At 4% postpaid subscribers, the number of people to whom telcos offer credit is nearing 40 million.

Meanwhile, by towing the banking partner’s line and learning from them, several of the business correspondents have built good institutional capacity for financial products and services delivery. The value of this is frequently underestimated by telcos. If they can infuse the necessary capital requirements or become subsidiary Payment Banks (SBI has a significant shareholding in ALW, and ICICI Bank in FINO), they could potentially succeed.

Recently an RBI circular allowed NBFCs to become BCs. Microfinance institutions (MFIs) are NBFCs who already possess superior structural last mile capabilities than banks. MFIs are present in areas with thin formal financial service provider penetration and arguably have better, more mature processes to handle credit as well as complex financial products. They have a viable business model. Bandhan has even obtained one of the two new banking licenses RBI issued. Selling credit to the poor isn’t quite at the difficulty level of asking them for deposits (ice and Eskimos come to mind). However, having established trust through a couple of lending-repayment cycles must put MFIs in a better position to collect deposits. It seems to make a lot of sense for MFIs to bid to become business correspondents of banks. In the event of a fully interoperable environment, the MFI network of branches and roving agents (with superior training) could result in a very interesting product and transaction possibilities.

That leaves retail as the other interested potential participants. For big-box retail like the Future Group, Reliance Retail, even Shopper’s Stop, becoming a Payments Bank could bring very interesting cash management efficiencies as well as improve loyalty play. It might even become a great revenue stream as an ATM alternative, given that they handle so much cash. For the e-Commerce players, many of whom including, eBay (PayPal’s PaisaPay), Flipkart (PayZippy), Mobikwik, PayTM already have large customer bases and an existing wallet play, this could be just the ticket. They will need to weave cash-out partnerships to turn their shoppers into savers and who knows, electronic-money lovers in time.

The Indian Railways, which runs the largest e-Commerce portal by transactions in the country (IRCTC) doesn’t issue a wallet. It is anybody’s guess whether they might jump into the PB fray with their own wallet. There is some precedence of product innovation by IRCTC in the form of SBI-IRCTC-Visa credit cards.

Finally, banks aren’t just going to roll over and play dead while all the aforementioned participants replace them as the sole option for payments and savings. Having been pilloried for underachieving on so many financial inclusion and innovation counts, this is a great opportunity for them to prove their critics wrong. I wouldn’t write them off just yet.

Mobile money providers in Uganda are well aware of the Over The Counter (OTC) trap and its implications, but their response to it will be the subject of another, later blog. This blog examines why OTC matters – enormously – to all stakeholders in digital financial services (DFS).

As highlighted by Pawan Bakshi, in “Beware the OTC Trap”, OTC can be used by providers to achieve scale at the beginning of the life cycle of their DFS agency roll-outs. However, the effects can be severely debilitating if the provider hits scale relying on a high proportion of OTC transactions.

In response to this discussion, I conducted a small survey in Wandegeya, a suburban market in Kampala, located within 5 km from the city center with nearly 120 mobile money agents. I asked 23 agents drawn across all the mobile network operators (MNOs) on their thoughts about OTC and found out some interesting results:

50-55% of cash-in transactions effected by agents are OTC – the amount is directly debited from the agent’s till and credited to the receiver’s wallet.

The agents charge customers an extra, unofficial amount for OTC despite receiving a commission from the providers. This means that the agent is earning twice (from the customer and the MNO).

The agents prefer OTC because of its added revenue to their business.

The agents are aware that they are cheating the customer; I would also imagine most customers are also aware of the extra, unofficial fee, but still go ahead with the transaction.

The agents admit that the practice of OTC is common across all of Uganda’s agent networks.

The Uganda agent network accelerator (ANA) survey, conducted in mid-2013, highlighted that on average an agent in Uganda makes 30 transactions daily (this could now have increased with the passage of time and further maturation of the market). Today Uganda has an approximate total of 45,000 active (on a 30-day basis) agents. This means that we have approximately 1.35 million transactions each day at mobile money agents, using the findings from the national survey.

From the 23 agents transaction records (gathered from agent transaction books), they register close to 52% as cash in a transaction (so approximately 700,000 transactions daily countrywide) and 50% of these cash in transactions are OTC (350,000 transactions daily countrywide).

The median cash in the transaction in Uganda lies between UgSh60,000 – 125,000 (US$23-49), for which the provider pays the agent UgSh440 ($0.17). Providers pay these commissions even though, of course, they derive no revenue from most of the transactions, in the hope that the cash in will generate revenue from person to person (P2P) transactions made by the customer. However, OTC allows a customer to make a direct deposit to another (who in most cases immediately withdraws it) and thus the provider only makes income on the cash withdrawal and foregoes the P2P. Yet it is the P2P where the providers make most of their profit since the costs of effecting the P2P are negligible, whereas much of the commission charged for withdrawals are paid to the agents providing the service. See Ignacio Mas’ outstanding Pricing of Mobile Money for a discussion on this.

The charge for P2P transfers for these median transfers of UgSh60,000 – 125,000 (US$23-49)is UgSh4,400 (US$1.72), and with the direct debit nature of OTC into the receiver’s account, this is not realized by the provider. This forms a very significant opportunity cost for the provider.

To assess approximately how big a loss the providers are incurring by permitting OTC, I looked at the 100 transactions from the 23 agents I interviewed and found the mean direct cost to the provider from payment of commission for cash-in to the agent of US$0.16; and the mean opportunity cost of loss revenue from P2P transfer of US$1.57. Multiplying this by the 350,000 OTC transactions each day gives a daily loss (direct and opportunity cost) of US$605,500; which converts to over US$221 million per annum.

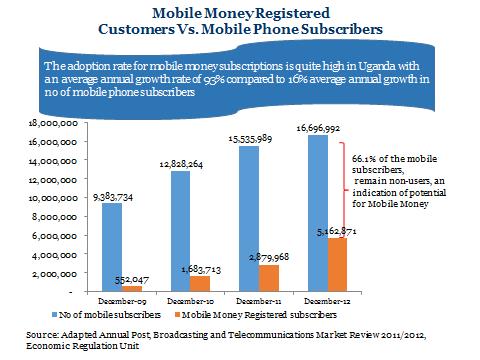

So what is the impact of OTC on the growth rate of mobile money in Uganda? According to the 2013 Uganda communications commission (UCC) report, the use of mobile money is doubling each year but is this the true potential growth rate? Uganda is estimated to have 17 million mobile phone subscribers, yet there are only 5.2 million active (on a 30-day basis) mobile money users. This is despite the fact that over 9 million users are already registered with at least one provider for mobile money.

So how is OTC stifling active subscriber growth in Uganda’s DFS space?

1. Customers do not need to register for DFS: The customer enters into a comfort zone where he can send money without necessarily registering or activating his SIM card with any MNO for mobile money. Incidentally, OTC is also prevalent for cash outs too, as long as the customer has the withdrawal codes from the wallet from which the money is to be taken, as in the case of one of the leading providers. Many such customers will not be easily convinced to subscribe their mobile numbers to mobile money – particularly with the growing levels of fraud in Uganda.

2. Agents have limited motivation to register customers and earn more from unregistered customers: Through OTC, agents are earning double revenue: from the provider (in cash-in transaction commissions) and from the customer (in unofficial fees). They prefer to have more customers conducting OTC transactions. Registering and converting customers into active mobile money users also takes time, and therefore less interesting for agents.

So what next for DFS providers in Uganda?

In Beware The OTC Trap: Is There A Way Out? Pawan argued that addressing the OTC trap requires a mindset paradigm shift. Providers need to conduct a deep dive analysis into and to develop an understanding of, the implications of OTC transactions especially for scaling both volume and value of transactions. This paradigm shift must start with the providers accepting that OTC can be greatly minimized (indeed, in Kenya, M-PESA has almost eliminated it as the ANA survey for Kenya shows). But the journey towards zero OTC environment starts with providers and requires collective action and effort. In Uganda, my discussions indicate that some MNOs some believe OTC transactions are impossible to eliminate, while others believe the elimination of OTC is possible.

Marketing and communication will be key to these efforts and must address all levels – the providers, agents, master agents and, above all, customers who need to know their rights and understand the benefits of carrying out their own transactions … as well as the fact that agents’ supplementary charges for OTC transactions are not sanctioned by the providers.

In Beware OTC Trap: Are Stakeholders Satisfied? we highlight that OTC is a double-edged sword that rarely, if ever, really meets the ultimate needs of any of the stakeholders involved.

Customers are paying additional fees and losing the opportunities and flexibility that self-initiated transactions offer them. Needless to say, agents have also burnt their fingers offering OTC transactions. It is considerably less risky for them to transact directly with a customer’s phone right in front of them.

For providers looking to limit the churn in their voice and data customers, need to enroll and activate these customers into mobile money irrespective of what stage of business life cycle mobile money is in.

Ultimately, the provider needs to ask if encouraging OTC is worth the inherent risks for short-term expediency. What is the revenue loss involved, especially if they reach scale? And how many subscribers do you forego by allowing agents to offer OTC services? And what is the reputation risk of agents charging at will for OTC transactions?

In the first blog of this series, we outlined the evolution and increasing sophistication of fraud in Uganda. The ingenuity of fraudsters is impressive. But what about the MNOs’ response?

Have the providers set up systems improvements and processes geared toward checking such frauds?

Talking to the staff of leading mobile money providers in Uganda, they concur that eliminating fraud poses a serious challenge for them and note that they continue to build internal systems that audit and check fraud. Some have now incorporated the appearance the recipient’s name on the phone’s display to confirm the right recipient before completing transactions. This both reduces the number of remittances to the incorrect number and narrows the scope for fraud using spoof SMS and requests to reverse “erroneous” transactions – see Survival of the Fittest: The Evolution of Frauds in Uganda’s Mobile Money Market (Part-I).

The MNOs say they have increased the capacity of their customer helplines for mobile money with dedicated teams that quickly respond to fraud and other complaints. They have also set up separate helplines and call center representatives to service and support agents. They also continue to improve internal processes to frustrate fraudsters, including blocking of disputed mobile money accounts and quick resolution of reported fraud cases.

In addition to these system and process improvements, MNOs talked to say they continue to spend significant sums of money on above the line (ATL) awareness campaigns to educate customers and agents on how to safeguard themselves from fraudsters.

MNOs note that they also use their agent hierarchy channels of float distribution. This is through the use of their master agents commonly referred to as “float aggregators”. MNOs have trained these master agents on fraud detection, reporting and resolution processes. The master agents (who interface with agents on a daily) pass on this knowledge to their agents during their site visits for rebalancing and support.

MNOs have also used regional mass agent meetings across Uganda. See “How MTN Uganda Communicates To Its Network Of 15,000 Agents” for a description of MTN’s approach to this. At these regional meetings, agents air their grievances and highlight areas that require attention from the provider. Typical pain points include rebalancing issues, customer care response and efficiency on issue resolution, and marketing/branding. However, fraud is one topic that always appears in these agent meetings and MNOs come well prepared with key learnings and tips to avail agents on how to safeguard themselves from fraudsters. The challenge with these agent meetings is that they are not regular with some MNOs taking more than a year to organize them … and when they do, it’s a one-day event (of approximately 8 hours). Towards the end, there is a rush to complete the day’s agenda. And who knows … the fraudsters could also be in attendance disguised as agents!

Three of the MNOs add that in 2012, the GSMA Association held workshops in Kampala to bring MNOs dealing in mobile money together for the first time. At this workshop, the participating MNOs agreed to work together on pertinent issues that concern the industry – with fraud strongly at the forefront. The MNOs have since then had a number of consultative meetings with the regulator (Bank of Uganda) to come up with collective policies to protect the industry from fraud. They are however quick to add that the regulator is also on a learning curve on mobile money operations, so decisions go back and forth before being agreed upon. These lags provide leeway for fraudsters to become even more innovative and sophisticated in at their game.

So why does fraud continue to manifest and evolve within mobile money in Uganda’s market?

If we analyze the evolution of fraud in Uganda, it is evident that fraudsters have always been ahead of measures to curb their activities, with MNOs typically having to react to fraud. This is however not surprising, given that mobile money is a new in Uganda (it is close to six years since the first deployment) – the providers (and their agents) are on a steep learning curve.

However, there are some mechanisms that MNOs might usefully consider:

1. Frequent on-site visits to agents. From the 2013 Agent Network Accelerator survey for Uganda conducted by The Helix Institute of Digital Finance, of the over 2,000 agents interviewed, only 33% reported being visited, trained and monitored by MNOs. And 46% of agents were not visited at all and are thus left to learning from their peers, or by bitter experience, about the tactics commonly used by fraudsters. If this lacuna continues, is good news for fraudsters. MNOs should consider increasing their site visits to agents with a view of training them on fraud management thus increasing agent’s awareness of the evolution and increasing the sophistication of fraud. Since agents interface with customers, given knowledge on fraud prevention, and the time involved to resolve fraud related challenges, they will pass this on to customers.

2. Risk/Fraud teams within mobile money functions. MNOs in Uganda have employed staff with a banking background and fraud management experience into their mobile money departments. However, these staff is mostly concerned with checking and controlling internal system fraud. MNOs need to move beyond this and have dedicated staff who are on the lookout for trade/field fraud targeting their agents and customers. Such staff would be charged with fraud prevention KPIs, and not just with KPIs for responding to fraud cases. Such staff could be trained to think like fraudsters so that they predict the next possible tricks and tactics of fraudsters. Basis these predictions, MNOs can run agent training and agent/customer awareness drive to prepare for the next generation of fraud in the market.

3. The use of agent themselves. In 2012, Ugandan agents formed a national association that is meant to represent agents’ interests and concerns. The association currently claims to have 30,000 members. Its activities have not been wholly welcomed or accepted by all MNOs, primarily as it has been lobbying against exclusivity clauses in agents’ agreements. However, this national agents’ association could play a very important role in fraud mitigation. MNOs can leverage on this by equipping the agents’ association with fraud prevention knowledge which they also pass on to the rest of the agents countrywide through an agent to agent visits or organizing agents’ meetings.

4. Collaboration. MNOs will eventually need to continue and deepen collaboration and information sharing on the emerging frauds in the country (and ultimately elsewhere too) to better address these. With the growing prevalence of non-exclusive agents, it is reasonable to hope that collaboration not just on information but also on agent training and monitoring will follow.

The role of the Bank of Uganda (BoU).

The role of the regulator is paramount in prevention and mitigating of risks in the DFS industry. In a bid to protect clients, BOU in October 2013 introduced mobile money guidelines which spelled out the role of each player in the ecosystem in preventing and mitigation of fraud.

The guidelines require providers to meet specific criteria, including providing a risk management proposal and putting in place appropriate and tested technology systems to detect anti-money laundering (AML) and terrorist financing. The guidelines require the providers to comply with requirements on consumer protection and also stipulate that providers train their agents (including training on fraud management).

The guidelines require agents to provide some KYC credentials (at the time of recruitment) that include proof of registered business with a physical address and to have an account with a licensed bank. The agent should also register and collect appropriate KYC documents from customers and deliver these to the provider. Agents are required to sensitize customers on PIN code safety, attend to their queries and of course service their transaction needs.

The guidelines forbid the agents to carry out customer transactions when the mobile money platform is down and it does not allow them to carry out transactions on behalf of customers through over the counter (OTC).

The guidelines advise the customer to exercise due care during transactions and note that it is their responsibility to keep PIN codes safe.

Is this enough from the regulator?

BoU says it works with other regulatory bodies with regards to mobile money because the industry cannot be looked at in isolation. Other regulators such as the Uganda Communication Commission have a role to play since they regulate the MNOs who are the major players in DFS. The BoU specifically regulates licensed institutions, especially the banks that work closely with the MNOs. The BoU focuses on the effectiveness of the board of licensed institutions that provide mobile money. They also look at the policies, internal controls and IT systems of the organizations that are in charge of these accounts. They also carry out targeted inspections periodically and act on issues brought to their notice.

The BoU perceives mobile money as any another product in the banking system and has no separate or dedicated department to monitor operations of mobile money. It falls under the Directorate of Supervision for Commercial Banking, which has a Financial Innovations Sub-committee and an Agency Banking Sub-committee. This could be interpreted as suggesting that the regulator does not have the capacity to monitor and supervise mobile money activities at the agent level.

The BoU has recently issued full-page pull outs in newspapers with the intention of educating and explaining consumer rights and their bare minimum expectations from agents. This was done in English with a promise of making translations into different local languages and is an important positive step forward towards improved customer protection.

With the proliferation of mobile money services in the country, there is a strong case for BoU increasing its capacity to supervise agents as well as compliance with core banking requirements. After all, there are now nearly twice as many active mobile money accounts as traditional bank accounts. The hundreds of mobile money agents and users being defrauded each week deserve this protection. Ultimately, such supervision should increase the credibility of the industry and thus it will be in the interest of the providers too.

The Prime Minister is all set to announce a mega new programme on financial inclusion on India’s Independence Day. The Department of Financial Services, Ministry of Finance, is busy shaping the ‘Sampoorn Vittiyea Samaveshan (SVS)’ (Comprehensive Financial Inclusion) scheme in consultation with bankers. Anyone closely associated with the financial inclusion space will worry that without very careful engineering, the scheme may be found lacking. While it incorporates some of the lessons learned from the past, MicroSave worries that it may struggle to overcome many fundamental barriers that have stalled inclusion over the years, despite very many concerted efforts by the central and state governments, the RBI, banks and innumerable other agencies involved. So does this grand scheme risk having the fate that all the previous avatars1 of financial inclusion programmes ran into? Quite likely, unless the fundamental issues are understood well and appropriate solutions embedded in the scheme.

Enhancing the reach of financial services to the excluded population and targeted distribution of subsidies to low-income groups have been universal problems to which few developing or underdeveloped countries have found scalable solutions. India has been on this journey tirelessly for over seven years but has made limited progress. It is evident and well recognized that subsidies need careful targeting to have a real impact. Budget 2014 and subsequent announcements indicate the government’s willingness and resolve to overhaul the systems and design suitable mechanisms to achieve this. However, it will take a well thought through approach with intensive inter-ministerial efforts to find real workable solutions that can take us beyond the failed attempts of the past. It will be vital for the government to unearth the root causes of past failures, to learn from these and thus avoid another faulty design.

An approach paper on the scheme talks of six pillars that would comprise SVS. The government needs to be congratulated on several aspects that been addressed for the better. These relate to access to services through multiple channels (business correspondents, branches and ATMs); online transactions; the promise of adequate compensation to the correspondent banking agents/CSPs; provision of a healthy mix of financial products across savings, micro-credit, micro-insurance, and pension.

While many constituents of the scheme are laudable, I highlight major gaps that need attention. The first one is finding real solutions to the last mile delivery problem. According to various research studies including several by MicroSave, less than 0.5% of the business correspondents (the agents appointed to provide banking services) on the ground are in a state of readiness to offer services and earning more than Rs. 5,000 a month (minimum compensation that is being contemplated under SVS). In this situation, who will service the 200 million odd accounts or 2 accounts per household, proposed to be opened? How will the Rs. 5,000 overdraft per account be delivered? And more importantly who will collect the repayments to prevent them from becoming bad debts? 182 million accounts have been opened in the past and RBI’s own data states more than 50% of these are dormant; while a majority of the rest are accessed less than once in a quarter (that too mainly to draw government subsidy payments and not as a full-service bank account). As has happened in the past, we worry that there will be a rush from agencies wanting to make a quick buck from opening new accounts or reactivating existing ones; and from disbursing (and pocketing) the Rs. 200 billion (at a conservative Rs. 1,000 overdraft per account) and going to Rs. 1,000 billion if the entire overdraft of Rs. 5,000 is provided. But if there is no mechanism on the ground to collect the repayments or to service the accounts, these are likely to turn dormant as soon as the overdraft is disbursed. There is a high risk that the scheme leads to massive dole out of subsidies instead of assisting targeted distribution of benefits. It is hard to comprehend how the arithmetic of using a leverage of 1:20 to set up a credit guarantee fund of Rs. 10 billion will be adequate and prevent credit defaults if the front line structures do not exist or are dysfunctional.

To address this issue, a sharp focus is required on drastically improving the last mile readiness through active business correspondents and operational ultra-small branches (USBs). This can only happen if it is market driven and commercially viable for banks and frontline agencies. It cannot be lasting if it is compliance driven, as we have seen very clearly over the last five years. The existing viability gap can be bridged in multiple ways. According to our analysis, for management and disbursal of government subsidy payments (MGNREGA, pensions, scholarships, LPG and so on) banks need to be paid 3.0%, of which at least 1.25% to 1.5% should go directly into the accounts of active BCs, to prevent pilferage by intermediaries, including corporate BCs. This can be achieved through linking performance to metrics of account activity and service standards that can be measured easily and accurately, with further monitoring by DLCCs/SLBCs/district and state administration and independent agencies. Only services with a consumer pull will eventually sustain, and in that case, it is also important that consumers pay (at least partly) for these services. Time and again MicroSave has established rural and poor consumers’ willingness to pay a reasonable fee for quality, proximate services. Remittance services provide a great example of this. Most remittance consumers actually pay more than NEFT charges (paid by mainstream account holders) as they find value in instant and safe transfer of funds. Moreover, they realize a net saving compared to informal and alternate channels.

The second major gap, also leading to high cost and viability challenges, is a near-random distribution of villages to lead banks. The current distribution does not allow any bank to have a critical mass of villages to constitute suitable structures for sustained service delivery. A cluster of adjoining villages is often allocated to multiple banks, and in turn, all of them find it impossible to achieve economies of scale or scope. The net result is bare minimum efforts for compliance and not to operate commercial banking. The village and gram panchayat allocation need to be completely re-worked in consultation with participating banks. Forward-looking banks will be very willing to swap villages to have a win-win situation.

A third aspect is a sharp focus and aggressive efforts on consumer awareness and protection measures at all levels from national to panchayat. Financial literacy and credit counseling (FLCC) centers have been in existence in every district for many years, however, their role in enhancing awareness for the under-banked and un-banked has been rather limited. A vast majority of consumers interviewed by MicroSave are completely clueless about the accounts they have opened in the past. Consumer responses range from ‘opened account to get a free photograph’ to ‘getting a smart card that is a must to draw pension subsidy’. Unless consumers are well educated about the power of the bank accounts and their rights in terms of associated overdraft, insurance and so on, only the intermediaries will take advantage of the monies flowing through. There will also be a need to be wary of consumer fraud that is starting to gain momentum amongst the newly banked illiterate population in India. Countries ahead of the curve with the extensive scale of branchless banking and mobile money such as Bangladesh, Kenya, the Philippines, and Uganda are now struggling with the aftermath of incessant growth without adequate consumer awareness, to contain the consumer and channel fraud that is now increasingly common.

The scheme clearly has the right intent and does indeed address several design issues that have marred financial inclusion efforts since 2005. What is needed is meticulous attention to cover the potential pitfalls, some of which as described above, risk completely derailing the programme.

1 Refer MicroSave focus notes, case studies, and papers at www.microsave.net

Uganda has seen an explosive growth in mobile money adoption in the last few years, growing from 550,000 active users in 2009 to 5.2 million in 2012 (active on a 30-day basis) according to the Economic Regulation Unit’s Broadcasting & Telecommunications Market Review 2011/12. Now, the rate of mobile money account ownership outstrips bank account ownership, which stood at 3.6 million bank accounts in 2013.

We have already outlined the nature of many mobile money frauds and presented a generic framework broadly based on the Kenya market to understand these and their evolution with the maturation of the mobile money market – see Fraud in Mobile Financial Services. However, the Uganda market evolved differently to the Kenyan one, with multiple players entering the market over time and, most importantly, no national ID. These factors modified the evolution and sequencing of frauds, and in this blog, I highlight the six most common agent/customer level frauds in Uganda. The blog draws on my five years of my personal experience in the mobile money business in Uganda with Warid and Airtel during which I keenly observe the evolution of the mobile money market. As Zonal and then Regional Manager, I was able to watch and discuss frauds with agents across the country – indeed responding to fraud was a key part of my work.

The approaches to fraud executed by the con-men demonstrate their thorough understanding of the mobile money system and the lacuna in the processes in place. While the regulators and MNOs were busy fixing the leaks in the systems and processes, the fraudsters also learned and evolved their modus operandi to find new ways to cheat mobile money agents and customers. Their fraud mechanisms have become more sophisticated over the years.

In Uganda, the fundamental underlying problem is the country’s weak KYC norms. Currently, anyone can obtain a SIM(s) in different names and can operate under different identities. This phenomenon is compounded by the lack of a national ID in Uganda. The registration process for a national ID just started 2 months ago. The typical identifications for KYC have been either a passport, work ID or local council ID. The latter is most common, yet easily obtained by fraudsters and in as many distinct copies as they want, typically by paying the local council leader a small sum of money (usually ranging between $ 2-3). The ease of securing a fake local council ID for SIM and mobile money KYC registration makes it difficult to trace fraudsters, Such SIM cards are registered for purposes of committing fraud and quickly thrown away after successfully achieving their purpose/objective.

So how has fraud evolved, manifested and become sophisticated in the DFS space 0f Ugandan market?

1. Fake currency

During initial years the fraudsters took advantage of the low level of awareness by customers and agents through the use of counterfeit money to defraud unsuspecting victims. Fraudsters targeted busy agents in high traffic areas who did not perform due diligence in monitoring counterfeits, and in turn, agents also passed this fake currency to unsuspecting customers. Soon, agents became vigilant and many started to use ultra-violet lighting rods to detect fake currencies, resulting in a drastic decline with this tactic.

2. Reversing “erroneous” transactions

Fraudsters then resorted to sending fake SMS messages to customers’ phones (alerting the customer of a P2P/cash in transaction on his mobile money wallet). Shortly thereafter, the fraudster would call the customer claiming to have erroneously sent money to a wrong customer number. Innocently, and before checking the balance on his mobile money wallet, the customer would make a P2P transaction to reverse the “erroneously sent money” from his account – thus losing money. This did not stop with registered customers, un-registered customers would also fall prey of the fake SMS and “send back” the erroneous money through OTC at the agent point. The fraudsters had a field day with this tactic.

In a bid to protect their customers, MNOs run above the line (ATL) campaigns and to send SMSs broadcasts to educate customers on how to differentiate between authenticated messages from mobile money payment systems and fake ones sent by fraudsters. Although this had moderate success, it called for the change of tactics from fraudsters.

3. Facilitation fees for winners of the prize draw

The next evolution saw fraudsters introducing yet another tactic, this time using the MNOs’ marketing and advertising strategies to their advantage. Between 2010 and 2012, the Ugandan telecom sector was witnessing fierce fights for supremacy in revenue, customer acquisition, and retention. There were price wars, bonuses on airtime top-up and special prizes under loyalty programmes that included motor vehicles, bikes, money, etc. Winners would be called through telephone calls asking them to pick up their prizes.

The fraudsters responded quickly by creating their own “call centers”. Posing as staff from the MNO, they would call customers informing them that they were lucky winners and should come quickly to redeem their prizes. However, the fraudsters requested the customer (their “lucky winner”) to make an initial deposit of mobile money to facilitate the process of hand over of the prize, this would range from $45 to $400 depending on the magnitude of the “prize won”. For a motor vehicle, the “facilitation fee” would increase up to $1,000. Excited customers would quickly send this “facilitation fee” to a mobile money account provided to them by the fraudsters, only to wait in vain for the prize. On checking with the MNO, customers would then realize that they had been defrauded and the mobile money number to which they had sent the “facilitation fee”, had been switched off with no trace of ownership.

MNOs responded by ATL campaigns to increase awareness of their office phone numbers through which winners would be contacted. These numbers were publicized through TV, radio, newspapers and trade materials. Customer’s awareness of this fraud tactic increased and soon there was a drastic drop in its use.

4. PIN Appropriation

Fraudsters were still thinking and soon introduced a new wave of fraud targeting mobile money agents – specifically those that were busy and highly liquid. It was common practice for busy agents to initiate a transaction and then hand over his phone to the customer to punch in his number. The customer would give the phone back to the agent to complete the transaction by inserting in his PIN code.

Fraudsters took advantage of this. They would go to the agent point as normal customers wanting to conduct a transaction and followed the usual process. During this time, the fraudsters studied the buttons the agent pressed for his PIN code. After a few visits to the agent, the fraudsters could usually identify the agent’s PIN codes. The fraudster then went to the agent to transact. This time when the agent handed over his phone to the “customer”, the fraudster quickly punched in a phone number, inserted the agent’s PIN code and completed the transaction. The fraudster then started another transaction to cover his tracks and handed the phone back to the agent to complete it. The fraudster then walked away … never to come back. The agent was not aware that two transactions had taken place on his phone and had lost money ranging from $500 – $1,500.

Again MNOs had to intervene and they conducted awareness campaigns targeting agents advising them to:

Make an end to end transaction by themselves and avoid customer contact with agents’ phones

Keep the PIN codes safer and better still frequently change them to avoid anyone studying them

Check and record their balance after every transaction is completed

Record all transactions done so that a trail can be made

Call helpline as soon as the loss of money is detected

These awareness campaigns forced fraudsters to adopt more sophisticated methods that required patience and careful study of the behavior of both customer and agents.

5. SIM Replacement

Fraudsters now study behaviors of customers and agents to find out those who carelessly expose their PIN codes. The fraudsters do not need to get in contact with the customer or agent’s phone, all they need is the phone number and PIN codes of the customer or agent.

MNOs provide a four-figure PIN code when activating a mobile money account for security purposes. Yet customers and agents usually (perhaps for fear of forgetting their PIN codes), chose to have a similar 4 figure PIN code, for instance choosing to use the classic 1234 or 4444, 2222, 5555, or 1111. See Ignacio Mas’ excellent blog “My PIN is 4321” on this. This makes it easy for them to memorize the PIN at all times. They continue to use this simple PIN without changing it (even when advised by MNOs to frequently change their PIN codes), thus making the fraudster’s work easy. Once he knows these PIN codes, through guessing or observation, the fraudster gets a duplicate ID issued in his name. He then goes to a police station to report the loss of “his/her” SIM, for which he gets a police letter. He presents this police letter to the MNO’s customer care center and a replacement SIM is provided thus inactivating the original, correct SIM. As the fraudster knows the PIN code of the target customer or agent, he is able to withdraw the money using the replacement SIM.

MNOs are facing a challenge with this tactic because the police innocently provide a letter for loss of a SIM (of course fraudulently obtained), so it is their obligation to provide a replacement SIM. Interrogating the MNO’s database for information to confirm KYC information provided at the time of registration is an option. But this is often inadequate to ascertain if the customer seeking a new SIM is genuine because the fraudsters have done his homework well and are well equipped with relevant information of their target victim. The relevant information and frequently verified include the customers’ date of birth, parents name and next of kin – upon this information matching with that of the MNO’s database (for proof and authentication purposes), a replacement SIM is issued to the fraudster who goes on to defraud innocent customers.

6. Reversals

In the latest round of frauds, the fraudsters have targeted the MNOs’ processes for the reversal of money sent to wrong mobile money accounts by customers and agents. Its common practice for money sent to the wrong recipient, to be sent back to the source account (after the MNO has received the complaint and done its due diligence investigation).

Fraudsters now go to a merchant to purchase an item for which they propose to pay using mobile money. Once the fraudsters have transferred the money to effect the payments, they leave the shop with the item and then call the MNO’s customer care center and ask them to block and reverse the payment on the basis that it was a wrong transaction. The MNO (following set reversal procedures) blocks the merchant’s account or the amount in a debate, then listens to both parties. However, the merchant in many cases has no proof that he is the genuine recipient and will be asked go ahead and settle the dispute legally. Clearly, this is not an ideal solution for a busy shopkeeper, and with the prospects of repeated visits to the MNO or lawyers for a reversal, he is left with no option but to agree to the transaction.

This blog examined the evolution of customer/agent-level fraud in Uganda by examining the six most common frauds in the market. In the next blog, we will examine how the MNOs have responded to the activities of fraudsters and how they might strengthen that response.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

Remember your preferences such as language or region.