Today’s blog focuses on liquidity management. It uses recent insights from MicroSave Consulting’s (MSC) field study of DFS agent networks in the Democratic Republic of Congo (DRC), which in turn stem from interviews with over 50 agents.

Our research in the DRC showed that a significant number of agents have been using informal rebalancing methods due to inadequate access to liquidity—both cash and electronic. This behavior poses risks to the client, agent, and DFS providers alike. Insufficient initial capital investment in DFS by the agent has been fueling the practice of informal rebalancing, complicated further by the dollarization of the economy. Moreover, a scarcity of rebalancing points due to the lack of financial infrastructure in the DRC has been compounding the practice.

Why is liquidity so important in the DFS business?

Liquidity refers to the adequate availability of cash and electronic value. A DFS agent requires both to serve customers effectively at their shop or counter. An agent’s lack of liquidity will cause them to turn away customers, which, in return, (a) causes dissatisfaction; (b) erodes trust in DFS; (c) limits the agents’ ability to earn commissions and be profitable; and (d) influences brand perception negatively.

Although liquidity management is a risky and costly part of the DFS business, providers and agents must prioritize it if they are to flourish. DFS industry practitioners agree that liquidity management is critical for success, and yet challenging to “get right”—particularly in areas that lack basic banking infrastructure, roads, and security. Such market characteristics are common across most of the DRC except for a handful of major cities, where the infrastructure remains basic. According to the research conducted by CGAP, the primary cost of the mobile money business for retail agents is liquidity management, which consumes 20-30% of the total expenses for this business line. Solving liquidity issues takes a conscious effort, as it will not resolve itself on its own.

Findings from agent interviews in DRC

1. MNO DFS agents are generally not investing enough capital in the DFS business, which affects both their profitability and sustainability.

MNOs in the DRC are not consistently imposing minimum initial capital requirements on agents when starting out in the DFS business. Agents reported starting their DFS business with as little as 10 USD. This is problematic, as an agent will not be capable of serving customers who wish to deposit or withdraw funds at their agent outlet. As such, neither the agent nor the provider will earn any commissions and would have to turn customers away, causing dissatisfaction.

In contrast, banks and MFIs in DRC impose a minimum capital requirement of 500 USD on their agents in accordance with Structure 29 issued by The Central Bank of Congo (BCC). As a result, they are better prepared to serve clients. However, the downside is that this large amount of starting capital represents a significant barrier to entry to this occupation.

“You have to have a lot of money in the account and [have it] all the time because it will strengthen the trust of the customers who know that there is always cash. [The] customer will even advertise by encouraging his entourage to return to the agent who has the capital permanently.” Agent in Kasaï

2. Liquidity capacity is diminished because agents must maintain electronic float and physical liquidity in both USD and CDF (Congolese francs)

Another complication plagues the DRC and other dollarized economies, namely Zimbabwe, Liberia, and Somaliland. It is the need for agents to manage liquidity in two currencies—US dollars and Congolese francs. Agents must stock both currencies based on customer demand, and risk losing out as exchange rates fluctuate.

DFS providers in the DRC require that each agent holds multiple currencies (USD and CDF) in digital accounts and in cash to offer DFS services. However, the setup of the digital accounts prohibits the direct exchange or transfer of e-float from one currency account to another. This presents a unique operational and rebalancing challenge for agents.

Conflicts of interest often arise between an agent and a customer when the transaction involves currency exchange. Each party wishes to see their preferred rate applied, yet ultimately the agent is generally compelled to accept the client’s preferred rate because they do not wish to lose the client or decline the transaction. This has been affecting agent profitability and customer experience and satisfaction negatively.

“The exchange rate USD to Congolese francs is unstable. The price at which dollars are sold and bought differs. Some customers expect high rates from us when we serve them. This impacts my profitability, but I am obliged to serve my clients.” —Agent in Kongo Central

3. Many agents admitted to using informal methods to manage cash or electronic liquidity to avoid turning away customers—some of their liquidity workarounds may lead to fraud issues.

The formal rebalancing channel for DFS agents in DRC is through “super agents”, who are known locally as “cash partners”. Agents must travel to a local bank, MFI branch, or MNO commercial outlet to rebalance the electronic float or obtain physical cash. Many agents reported difficulties or unwillingness to do so—given that there are only 0.14 bank branches per 1,000 km2 in the DRC. Moreover, due to security concerns, carrying large amounts of cash is risky.

For agents, rebalancing through the official channel is time-consuming and risky. It also proves costly for agents in terms of the opportunity cost of shutting up their shop to travel to a bank branch. It is unsurprising that agents have been turning to unofficial methods to manage their liquidity. These methods comprise borrowing money from fellow agents or trusted acquaintances in their proximity and holding on to a client’s physical cash but waiting until a later time to add the electronic value into the client’s account. While these informal methods may help an agent to avoid turning away customers in the short run, they certainly bear more risk—for the client, agent, and provider.

“If I am stuck, I call my friends who send me liquidity. [For] example, if a customer comes to make a deposit of 500.000 CDF and I do not have 500.000 CDF in electronic money, I call a friend who is an agent who sends me virtual currency to serve the customer, and I settle with him at the end of the day.” Agent in Kivu

Agents in urban areas of the DRC reported fewer problems with liquidity management due to the greater access to bank branches (or other rebalancing points). Yet, they still reported that this activity was time-consuming, costly, and sometimes dangerous for them. The e-money providers (Vodacom, Orange, and Airtel) have partnered with banks and other financial institutions. As a result, their agents are able to obtain physical or digital liquidity from bank branches throughout the country. The agency banking providers (Finca and Equity Bank) require their own branches in the various regions to help their agency bankers manage their liquidity.

What next for liquidity management practices in DRC?

There is certainly room for Congolese DFS providers to support their agents better to manage their liquidity. Indeed, many are already looking at implementing new, official procedures and methods. These include implementing master agent models or partnering with new types of “cash-rich” institutions, that is, not just the banks, which could also act as liquidity providers. It is evident that partnerships will be required if the accessibility and availability of rebalancing points are to be improved.

Liquidity management partnerships and innovations from across the globe

As the DFS industry over the world matures, we see providers implementing new and innovative methods to help their agents manage their liquidity effectively. In the following section, we take a quick look at some innovative liquidity management practices that involve partnerships between DFS provider and one or more external entities. These new liquidity management practices are listed in order of relevance to the DRC market, where smartphone penetration remains minimal, which means that more advanced app-based solutions are currently less relevant.

Identifying cash-rich businesses that can also act as liquidity providers

Alongside the banks that traditionally supply liquidity, finding businesses that can provide liquidity would increase the number and also possibly the proximity of official rebalancing points for agents.

Direct delivery of cash or e-money to the agent

Several DFS providers globally are now developing “float runners” systems. In some cases, the DFS provider offers this service directly, and in other cases, they have partnered with external entities. In Uganda, Airtel Money partnered with 53 float runner entities, known locally as “aggregators”, who buy float from a super-agent or the official liquidity provider and deliver it to individual Airtel Money agents. Airtel defines a specific territory for each of its aggregators. One of the float runner companies, Blacknight, covers about 800 agents in different regions—mainly rural areas.

Adding functionality to the agent account to facilitate dual currency management while ensuring commission structures encourage transactions of both currencies

The highly successful mobile money provider, Telecom Zaad, from Somaliland has been using a dual currency platform for some time. It recently also added currency conversion functionality to its wallet service, allowing customers to convert Somaliland shillings to US dollars quickly.

Credit advances for agents

Airtel Uganda, in partnership with JUMO, uses alternative credit scoring methods to provide a digital micro-credit product to its agents—Wewole. Similar initiatives have also found use in the Philippines and Fiji.

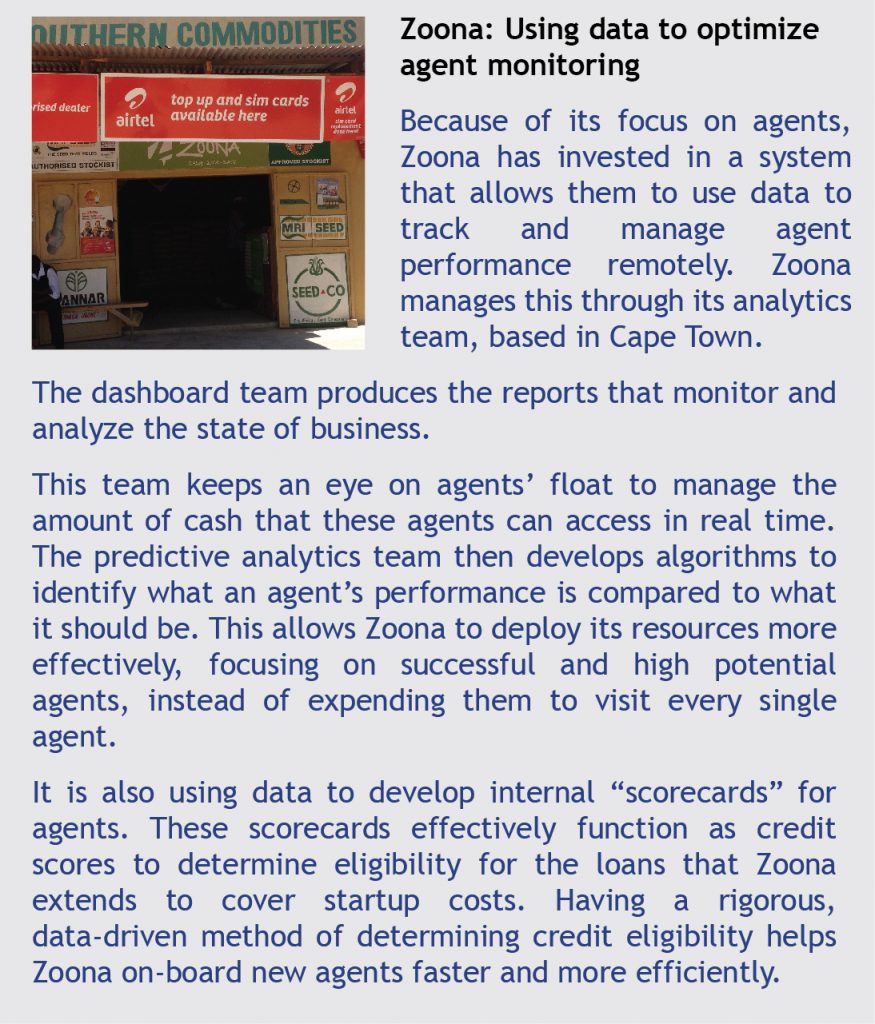

Using data analytics to help predict liquidity requirements

Predictive data analytics, using transactional data around agent locations to predict future demand for float, may improve liquidity management by providing efficient estimates of float inventory. African Mobile Money provider, Zoona, has pioneered this approach in Zambia.

Using geo-mapping to improve the visibility of rebalancing points

NovoPay in India uses advanced GIS mapping systems to match agents with nearby field officers who top up agents’ floats.

Conclusion

Poor access to liquidity—both cash and electronic—is one of the primary reasons behind the low activity of agents and customer dissatisfaction in DRC, and has been leading to a proliferation of informal, risky rebalancing methods. As a result, we call on the local DFS providers to look closely at how they can better support their agents to manage their liquidity effectively.

Trustworthy, sustainable partnership agreements will be key to improving liquidity management for agents in DRC. Some local DFS providers have already started focusing on methods 1 and 2 from the liquidity management practices. These providers have been building partnerships between banks, telecoms providers, microfinance institutions (MFIs), and other cash-rich organizations to help increase the number of formal rebalancing points for agents. They have also been looking at ways to mobilize cash liquidity so that agents themselves do not have to travel the distance to meet their rebalancing needs.

Dr. Kim highlights that agents are required to provide a range of services upon which all of mobile money depends. Yet liquidity management, marketing, customer service, complaint management, and agent assistance with transactions are rarely, if ever, factored into their formal compensation. Agent commissions should be seen as part of mobile money’s “cost of goods sold”, plus sales incentives. Agents are fundamental to any mobile money service rather than merely a channel cost to be squeezed out of existence. Despite smartphone sales growth (accompanied by data or not), in most countries, low-income customers will want and often need a trusted person to explain the nuances of aspired-to, sophisticated products, to promote the benefits, and to provide the after-sales service.

Dr. Kim highlights that agents are required to provide a range of services upon which all of mobile money depends. Yet liquidity management, marketing, customer service, complaint management, and agent assistance with transactions are rarely, if ever, factored into their formal compensation. Agent commissions should be seen as part of mobile money’s “cost of goods sold”, plus sales incentives. Agents are fundamental to any mobile money service rather than merely a channel cost to be squeezed out of existence. Despite smartphone sales growth (accompanied by data or not), in most countries, low-income customers will want and often need a trusted person to explain the nuances of aspired-to, sophisticated products, to promote the benefits, and to provide the after-sales service. It is our belief that proponents of financial inclusion need to also foster ANMCs with the same philanthropic or social-technical support that banks or telcos have received. Some options are highlighted in the next post.

It is our belief that proponents of financial inclusion need to also foster ANMCs with the same philanthropic or social-technical support that banks or telcos have received. Some options are highlighted in the next post.