In this paper, we want to look more closely at OTC model, with the help of data from The Helix Institute, InterMedia and the GSMA, which provide an analytical perspective on the pros and cons of the OTC model. This will allow us to propose some recommendations on how to manage OTC going forward.

Blog

Eko In India

Eko is a Business Correspondent (India’s term for banking agent) serving the State Bank of India (SBI), ICICI Bank and Yes Bank. The Reserve Bank of India (RBI) only allows banks to have exclusive agents. Therefore, while Eko now has partnerships with multiple banks, each agent outlet may only offer services for a single bank. This means that Eko is effectively running multiple agent networks in tandem and therefore providing a third-party specialist model for banks. To read through the case study, please click here.

Debunking the Myth of OTC

Walking through the markets of Senegal and Pakistan, you will easily hear ‘Warimako!’, and ‘Easypaisa kara lo!’ These phrases have morphed into a catch-all for mobile money transfers—transactions that are typically done using Over the Counter (OTC) methodology.

Walking through the markets of Senegal and Pakistan, you will easily hear ‘Warimako!’, and ‘Easypaisa kara lo!’ These phrases have morphed into a catch-all for mobile money transfers—transactions that are typically done using Over the Counter (OTC) methodology.

OTC transactions are one of the most contentious issues in digital financial services (DFS). Some argue that OTC can decrease provider profitability, stymie product evolution, and can lead to unregistered transactions increasing the risk to terrorism financing and money laundering. Those in favour argue that OTC methodology lowers a provider’s barrier to entry and rapidly builds transaction volumes, as customers embrace this easy-to-use methodology. Further, they argue that OTC helps to increase both the awareness and comfort-level of DFS to a population that may not easily adopt the mobile wallet.

In The Helix’s upcoming paper, ‘OTC: A Digital Stepping Stone, or a Dead End Path?’, we first define OTC to anchor future discussions on this important topic, present five key concerns that often cloud our judgement around OTC, and argue that certain types of OTC should actually be embraced and propose ideas to move the industry forward given the data presented. In this blog, we demystify on one of the five concerns by analysing evidence from ANA research countries: OTC can prevent product evolution.

What Do We Mean By OTC?

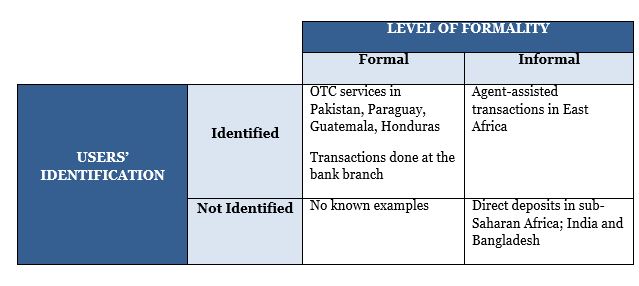

We define an OTC transaction as “a transaction that the agent conducts on behalf of a customer from either the customer’s or agent’s mobile money account.” This definition includes both transactions conducted by an agent from his/her own account on behalf of a customer, as is the case in Pakistan. The definition also includes agent-assisted transactions that are popular in sub-Saharan Africa, where many users already have mobile money accounts but are assisted by the agent to make their transactions.

In fact, in Uganda (2013) where 30% of agents offer agent-assisted transactions, 57% of registered users actually prefer these kinds of transfers over using their own handset. Such agent-assisted transactions happen usually because either the users lack the literacy to do it themselves or aren’t tech-savvy enough to make the transaction.

Our definition further distinguishes between “formal” methods approved by the provider and the regulator versus “informal” methods—prevalent in Bangladesh and India, which are frowned upon by regulators and disliked by providers to differing degrees (Table 1).

Table 1. Typologies of OTC Transaction and its prevalence

Bursting the Bubble: OTC Stymies Product Evolution

One of the biggest arguments against employing OTC is that it limits product innovation as the wallet is a better means to offer sophisticated products because it can generate more revenue for the provider and more value for the client.

While the argument resonates, it’s mostly unproven as almost no provider has introduced and scaled a new product that required wallet use, especially in the first five years of a DFS deployment to date. This includes sophisticated financial products like M-Shwari, KCB M-PESA Account, Lipa Na M-PESA and M-Ledger that require an existing M-PESA account. This may raise a question about whether an alternative approach is letting customers build familiarity with mobile money through OTC first, whilst encouraging them to register for mobile money accounts when there are more compelling use cases for mobile money accounts.

For those worried about not being able to collect data on customer’s use patterns and preferences, OTC does not preclude providers from collecting data, as long as providers are able to identify the user and the recipient (formal and identified quadrant in Table 1).

Moreover, in 2015 GSMA reported that airtime top-ups, bill payments and person-to-person (P2P) transfers globally account for 96% of transaction volumes and 87% of values. Paradoxically, OTC allows for all three of these transaction types, as long as the transactions are made at the agent.

Nevertheless, we have witnessed product evolution using the OTC methodology in ANA countries. Senegal, for example, boasts a pioneering cross-border remittance model where customers can use both OTC and the wallet. By the second half of 2014, the value of cross-border remittances on Orange Money accounted for almost a quarter of all remittances reported by the World Bank between Ivory Coast, Mali and Senegal. Further, Easypaisa Pakistan introduced Easypay Online in 2015, utilising both the wallet and OTC.

Segmenting Agents To Register Customers

In Uganda, Zambia and Senegal, we recommend providers segment their agent network so that the more dynamic, educated agents serve as a sales agent that sell products to the mass market and instruct on the usage of wallet based products, given the slow uptake of some wallet services and the preference of agent-assisted transactions. The optimal time then to register users might be on the launch of a wallet-based product that requires agent promotion.

While some argue that agents would not want to encourage customers to migrate from OTC to the wallet, given the high revenue they earn from OTC, agents in both Pakistan and Senegal show that only 26% and 40% of agents respectively (surveyed) felt this way. In fact, 74% in Pakistan are willing to conduct customer registrations for m-wallets, and in Senegal, agents note that they would open a wallet but either they aren’t really knowledgeable of these services, or their customers aren’t aware enough to sign up for a wallet. Therefore, given the right incentives, agents may be more willing to help with registrations than commonly thought, and often provide the trusted advice needed to help sell new services to the mass market.

A possible approach to product evolution is letting customers build familiarity with mobile money through OTC, gather data on these customers and build a user-friendly product with a compelling use case on the m-wallet. This then allows customers to choose to migrate over to the m-wallet when this compelling use case is offered to them—such as a credit product.

This is the first blog in a series on the merits and shortcomings of OTC, addressing the five concerns often raised about OTC, using ANA data where possible. Our hope is that this framework will enable the industry to anchor their discussions on OTC.

Offline Payment Acceptance: A Puzzle and an Opportunity

As Indians, we love cash, which is fungible and provides instant gratification – allowing us to buy anything across the country. Cash speaks one language, does not discriminate, and provides a seamless experience!

RBI estimates that 96% of all the retail transactions in the country are conducted using cash, leaving only about 4% payments on cash-less/digital channels. The situation in rural areas is even more pathetic, with less than half a per cent of payments being cash-less, and cash is the undisputed king. Cash is costly for the government to keep in circulation: the cost of printing, storing, safekeeping and transporting, all adds up. In the year July 2014 to June 2015, RBI incurred Rs. 3,760 crore (USD 578 million) on security printing alone. All the banking entities and RBI spend close to Rs. 21,000 crore (USD 3.2 billion) per annum to keep paper money in circulation according to a recent study on cost of cash.

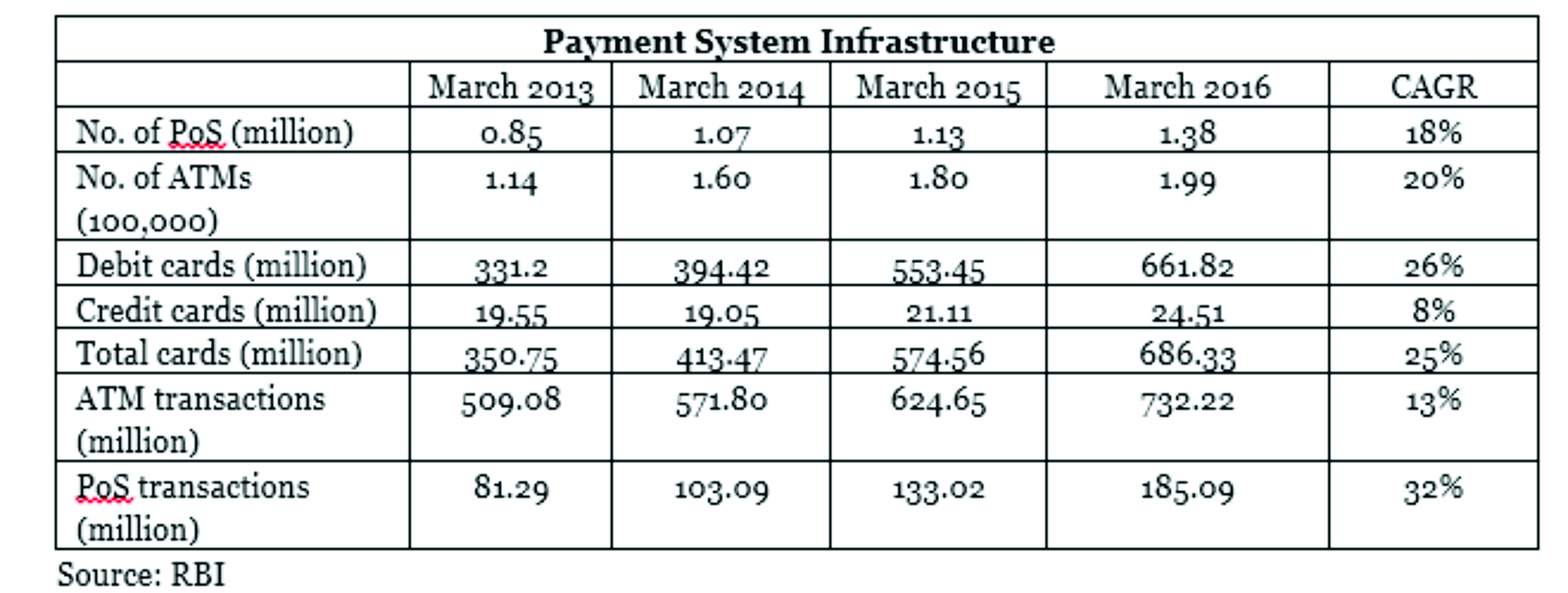

Cash is costly even for individuals, and despite the growth of ATMs (please see table below), the study estimates that the residents of Delhi spend 6 million hours and Rs. 9.1 crore (US $1.4 million) to obtain cash. Hyderabad spends 1.7 million hours and Rs 3.2 crore (US $0.5 million) to do the same – about twice as high as Delhi when calculated on a per capita basis.

There are a variety of barriers to ‘cash-less’ and one of the most important one is the acceptance of electronic money by merchants. In a country where we have more than 20 million merchant establishments and close to 690 million cards, only 6-7% of the merchants (1.38 million) have infrastructure to accept electronic payments. Providing (mainly debit) cards, largely addresses the demand-side issues – so the mass distribution of RuPay debit cards with Jan Dhan accounts could play a very important role. With a healthy CAGR of ~20% for both PoS and ATM infrastructure, usage is spurred by transactions at PoS (though from a lower base than ATM transactions).

On the supply side, the current process has been fairly tedious and controlled by some of the entities.

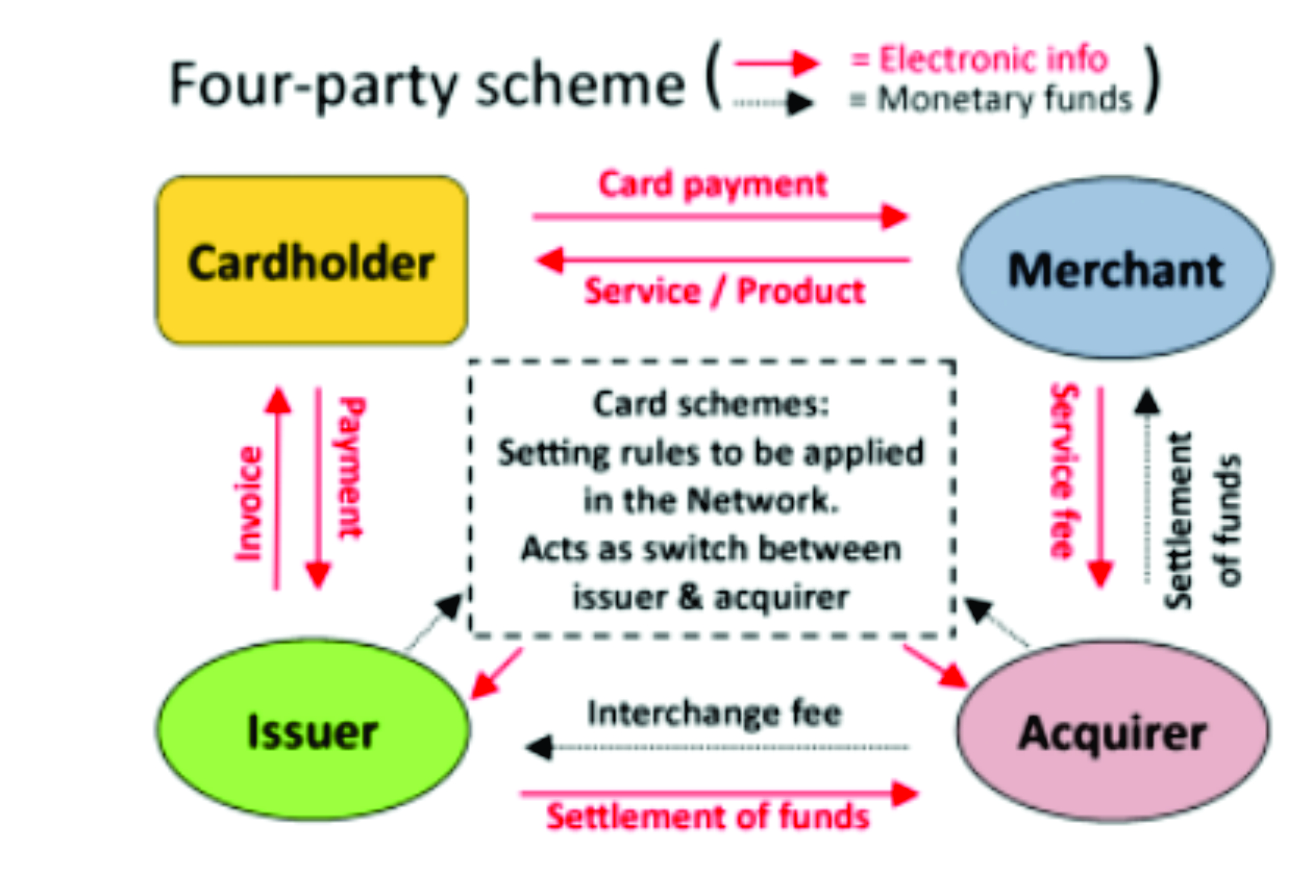

As depicted in the diagram, transactions require a customer or card-holder and a merchant, with card acceptance infrastructure, who provides goods and services in return. However, at the back end, the card used by the customer has to be issued by an ‘issuer’ (typically a bank) and the merchant is to be acquired by some entity which could be an aggregator, payment service provider, or bank. The card-holder is charged for goods purchased and the merchant is paid for goods sold through their respective acquirers. At the back end, a card association (like Master, Visa and RuPay) licenses card-issuers and provides settlement services. This provides convenience to the customer as he/she is not required to carry cash, while the PoS terminal ensures adequate safeguards.

The merchant is able to service typically high-value customers, though at a cost known in payment parlance as MDR or Merchant Discount Rate. The overall cost is borne by the merchant and the proceeds are shared by the acquirer and the card-issuer as per terms of contract between them. If there are enough customers carrying cards, merchants have shown a willingness to be acquired and pay MDR to the acquirer. In the past, when carded transactions were in their infancy, many merchants insisted on 2% more (almost equal to MDR) when customers paid with cards. This practice has largely been curbed – at least in urban areas. However, some merchants like petrol filling stations, gold merchants, etc. still clearly display and charge extra for using cards. This leads us to believe that the other merchants either pay from their margins or have already factored the MDR into their costing. In the absence of credit risk, RBI capped MDR at 1% in June 2012 for debit cards. India is primarily a debit card market with close to 658 million debit cards outstanding (as of February 2016) compared to only 24.13 million credit cards. Over the last three years, both debit and credit card transactions have been growing rapidly; however, growth in the debit card segment has been higher.

Merchant-acquiring is an integral part of card-payment transaction processing. Acquirers enable merchants to accept card payments by acting as a link between merchants, issuers, and payment networks to provide authorisation, clearing and settlement, dispute management, and information services to merchants. The merchant-acquiring industry is dominated by a few large players across the globe, with the top 10 acquirers in the world handling nearly 50% of the global card transaction volume. In India, many banks have forayed into the merchant-acquisition process – with limited success, as it takes a fair amount of time and documentation to acquire merchants. The cost includes terminal infrastructure, which is in the range of US$ 150-200 and is generally paid for by the acquirer. The acquirer needs to be convinced that this expenditure is justified and more and more customers will indeed use the PoS terminal.

Currently, the cost of acquisition for the acquirer is high as a result of the device, paperwork, and the time involved; the cost to merchants is also high, given the operational costs of the card-acceptance machines and the MDR. To top it all, many customers typically carry cash and seem to be more comfortable in dealing with cash. For some people, it also helps that cash does not leave behind a trail in the way electronic money does, and hence allows the unscrupulous to evade taxation. With a growing number of debit cards issued, the focus of the government and of regulators is to grow the digital financial services ecosystem.

This requires a complete change in mindset in the way transactions are perceived and orchestrated. The 24×7 Immediate Payment Systems (IMPS) and Unified Payments Interface (UPI), managed by National Payments Corporation of India, which allow account-to-account (A2A) interoperability through a virtual or global (like Aadhaar) address, offer new opportunities. One option would be to effect P2P payments to any offline merchant (service provider), using UPI, an option that is now feasible since most households have a bank accounts and a mobile phone. This option allows a customer to easily pay (push) the amount to the merchant’s account using virtual address on UPI without requiring to share any sensitive details like account number, bank, etc. Alternatively, the merchant can collect (pull) the payment by sending a request using UPI, and the customer can then authorise this request for payment. This will not require any intermediation by any of the typical actors highlighted in the four-party diagram above. However, unlike a typical card transaction, it does not address dispute settlement between the transacting parties.

Furthermore, with IMPS and UPI in place, merchant Aadhaar and bank account details can be used to on-board all merchants en masse. It can be done leveraging the Lead Bank Scheme and service area approach for inclusive banking that makes the branches responsible for development of specific area, covering 15-25 geographically contiguous villages. Bank branches can easily identify merchants in their service area and on-board them. This would address the problem of lack of dispute settlement between the card-holder and merchant: banks would play the role of acquirers, whereas NPCI would act as card network service provider.

Another possibility to promote digital retail payment could be self-registration by merchants using Aadhaar as unique identifier through aggregators/intermediaries. These intermediaries can be new age financial technology companies (including Payment Banks), providing seamless processes at a very low cost, as compared to current MDR

These ideas may seem radical, but could be the future, given that incremental growth in PoS acceptance infrastructure is unlikely to lead to a cash-lite (let alone cash-less) India. To get to a level of large-scale acceptance infrastructure using IMPS and UPI, customer protection and dispute redressal mechanisms will require sharp focus and hard work.

That said for digital value transactions of US$ 10-50, these issues are really not that important. Most of these low-value transactions are conducted with both parties physically present; just as with a cash transaction. There is no intermediation between customer and merchant, and disputes, if any, are resolved on the spot.

If we look at the benefit to various stakeholders, these far outweigh the risk at this point of time. The merchant is not required to handle cash and pay MDR. Customers create a digital transaction history and can rely on their account for payments. The economy as a whole gets a boost from the lower cost of cash and possibly reduced costs of goods and services, as well as better tax compliance and a host of other benefits. Surely these benefits are worthy of radical, but low risk, change in procedures around merchant acquisition and offline payments?

Can Payments Banks Survive?

The news that three of the provisional licensees,Cholamandalam Distribution Services, Dilip Shanghvi and Tech Mahindra, have decided not to seek a full Payments Bank license, has caused much debate. The reasons for their withdrawal are varied – and not all necessarily based on the challenges posed by the underlying business model. Despite this, the media is abuzz with discussions on just how Payments Banks can achieve profitability given the restrictions imposed on their business model by the Reserve Bank of India (RBI).

The news that three of the provisional licensees,Cholamandalam Distribution Services, Dilip Shanghvi and Tech Mahindra, have decided not to seek a full Payments Bank license, has caused much debate. The reasons for their withdrawal are varied – and not all necessarily based on the challenges posed by the underlying business model. Despite this, the media is abuzz with discussions on just how Payments Banks can achieve profitability given the restrictions imposed on their business model by the Reserve Bank of India (RBI).

It is clear that developing a successful model will depend on the nature of the licensee’s core business. MNOs will build on their existing client base and agent networks, and use the Payments Bank services both to reduce churn, as well as to make money on savings balances and transaction data to inform third party lenders’ decisions. India Post will do the same, but can easily add physical distribution and payment collection to their model. Consortia like the State Bank of India and Jio have a wider range of options and opportunities to build on the bank’s brand and core business. Paytm has already made it clear that they will be looking to derive value from leveraging their massive client base and encouraging a cashless ecosystem rather than from CASA (current account and savings account) operations.

Irrespective of the diversified business models, all will depend on Payments Bank using technology and agent networks to reduce costs, and offering diversified services to serve the mass market. MicroSave has already calculated the type of savings that a full-fledged bank (even with legacy technology) might make at the aggregated level, concluding that the annual average cost of saving a customer through the branches (around Rs.400-500 or circa $8) could be slashed to Rs. 65-125 (circa $2).

In 2012 we were able to look at this on a detailed, disaggregated basis. Conducting sophisticated activity-based costing we were able to look at the relative costs of conducting different transactions through branches and through business correspondent (BC) agents. As can be seen from the graphs, most but not all costs decreased. It is important to note in this case that the agents were conducting traditional BC (cash in/out) transactions as well as business facilitator (BF) type transactions (selling to and referring potential loanees as well as fixed depositors (FDs), collecting loans and recovery of loans that had been written-off). Indeed, this combined BC/BF role may well be essential for agents to break even given the extremely low commissions paid to agents in India for cash in/out transactions.

While some of the cost savings come from credit operations, from which Payments Banks are barred, it is clear that their agents could, and indeed probably must, play an important role in making and recovering loans made by their lending partners – and be remunerated for doing so.

There are two core challenges facing Payments Banks seeking to implement effective business models: 1. optimising their distribution networks, and 2. creating real value for their customers.

In order to optimise agent networks, Payments Banks will need to rethink the current, often unstable, models currently used in India. To date, as the 2015 Agent Network Accelerator survey of The Helix Institute of Digital Finance highlighted, too many agents are both dedicated (financial services agency is their only business) and exclusive (they offer services on behalf of only one provider). Both of these impede agent profitability. Payment Banks seem set to replicate and extend this model, and establish agents trying to survive by offering financial services for one provider alone. This risks adding to the fragmentation and duplication across India and to further reduce the ability of agents to make enough money to continue in the business.

Success will lie in recruiting agents for whom financial services is but one part of their business, who offer services on behalf of a range of providers and who are well-trained and monitored to ensure that they offer high quality, dependable services that are trusted by their clients. A study by The Helix Institute and Harvard Business School noted, “We find that the presence of a tariff sheet increases demand by over 12% and the ability to answer a difficult question about mobile money policy increases demand by over 10%. We also find that highly knowledgeable agents reaped even greater rewards for their expertise in the face of competition.”

To create real value for their customers, Payments Banks will need to move beyond traditional financial services. In addition to better understanding the needs, perceptions, aspirations and behavioural biases of their target clientele, Payments Banks will need to package and present their services in ways that align with the mental models of the mass market.

Poor people’s need for appropriate products mean that they need a range of products (just as you and I do) to reflect their life cycle. They also need disciplined systems that break down their accumulation of lump sums into small manageable amounts (saving up, through or down).

The products used to accumulate lump sums should ideally be differentiated and ear-marked for specific needs, in the same way that poor people often earmark specific income streams for specific uses to help with their mental accounting. For example: savings for a bicycle, to buy some land and for old age are very different in terms of the time horizons and instalment amounts.

But within this framework, as Ignacio Mas and Vartika Shukla highlighted in their blog Making Digital Money More Relevant, More Often -Part 1, different market segments have different needs, aspirations and biases. “At the highest level, the mass market has a few typical characteristics: a large percentage of people do not have a regular fixed income; most do not have a defined (predictable) income flow. Because of the uncertainty which comes along with a variable income, people employ various methods to manage and organise their money. We can broadly classify people into the following three segments:

People in the ‘Survive’ category have unpredictable or uneven income. They are more concerned about meeting day-to-day needs. Their money matters usually have a very short time horizon since their objective is to ensure stability of income. They are constantly searching for liquidity and have to plan for what to do with money every time they receive it.

In the ‘Live’ segment, people have moved beyond daily survival and are looking at satisfying wants. The focus of financial behaviour shifts from fulfilling necessities to meeting aspirations and planned expenses. Income, even though much less uncertain may still be variable. They need to manage their available liquidity in order to meet their aspirations and are planning for these using monthly budgets.

The ‘Comfort’ segment consists largely of people with regular income. They seek to have more convenience in their lives and are building assets, particularly for their next generation. They do occasional financial planning to ensure that resources are directed to asset acquisition in order to keep their legacy secure.” These segments require different services, think about/manage their money in very different ways, and thus offer a wide range of opportunities for Payment Banks. Indeed, the success of Sahara and Life Insurance Corporation of India provide a small glimpse of the business opportunities offered by rural India – and they are servicing very specific needs.

Ultimately, Payments Banks will want to encourage and facilitate the cashless (or at least less cash) vision articulated by the Government of India. As Paytm has already clearly articulated: cash costs! A digital, cash-lite India leveraging Payments Banks’ technological capabilities offers increased efficiency, reduced corruption and a viable business model as the marginal costs per cash-free transaction is negligible.

Open Application Programming Interfaces (API): Purpose and Possibilities

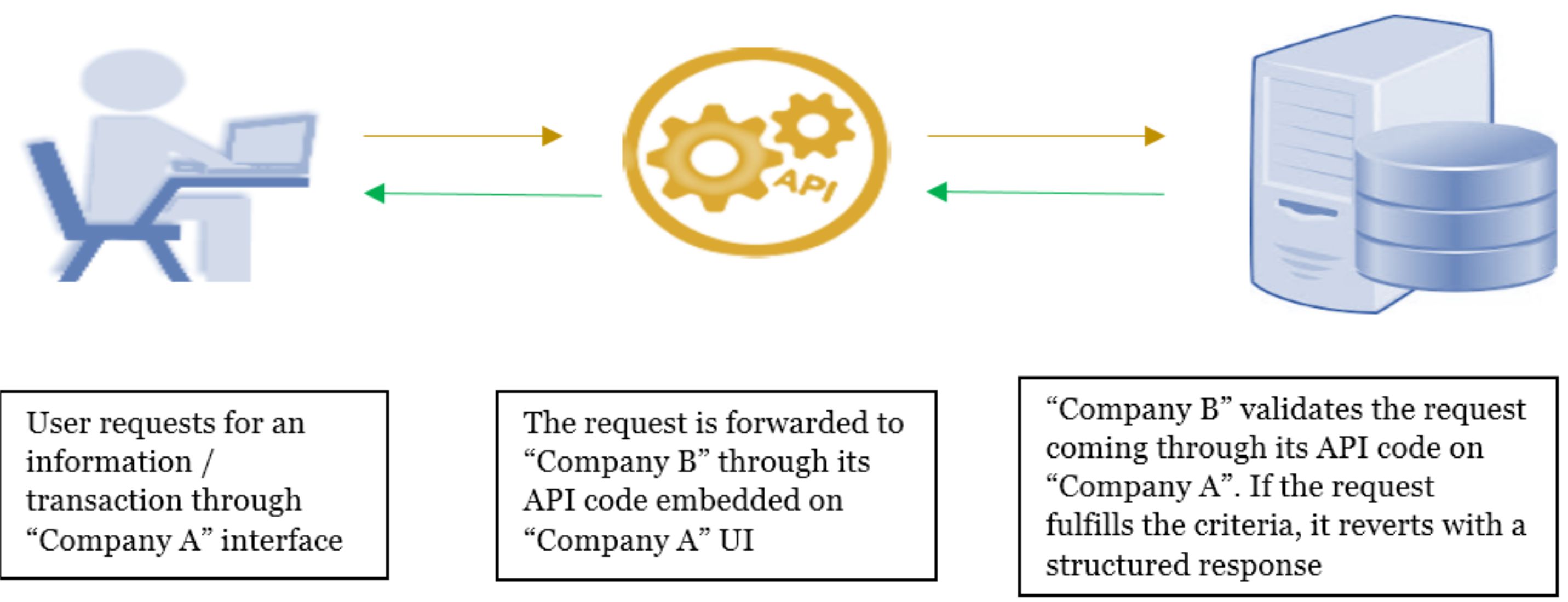

Application Programming Interface or API, a software programme, acts as a bridge between disparate applications. It performs the intended function when a set of instructions are provided through a user interface (UI). The front-end of UI is usually a website or mobile application.

The following diagram illustrates the basic architecture of any API-based business model:

Guided by the strategy of Open APIs, many companies like PayPal, Master card, Mobikwik, M-PESA, Eko, etc. have embarked on this journey for mobile money and payment services. Though a provider charges a fee for consuming APIs, it makes sense to a variety of user organisations on the basis of time-to-market and cost parameters. For many upcoming organisations, it is more feasible to use open APIs of a specialised company, in a particular service line, instead of building the same.

The second generation platform of M-PESA in Kenya allows partners to build on disbursements and services payments like automated payment receipt processing, payment disbursement, and payment reversals in case of failed transactions.

DBS, a Singapore-based bank, has announced a mobile-only bank in India. The digital bank would use open APIs to acquire, authenticate, and facilitate transactions for customers, using Aadhaar.

As part of Digital India, India Stack is a set of open APIs authorised by the government to create an identification, authentication, and transaction ecosystem across different sources. For payment solutions, National Payment Council of India (NPCI) has released its API for Unified Payment Interface (UPI).

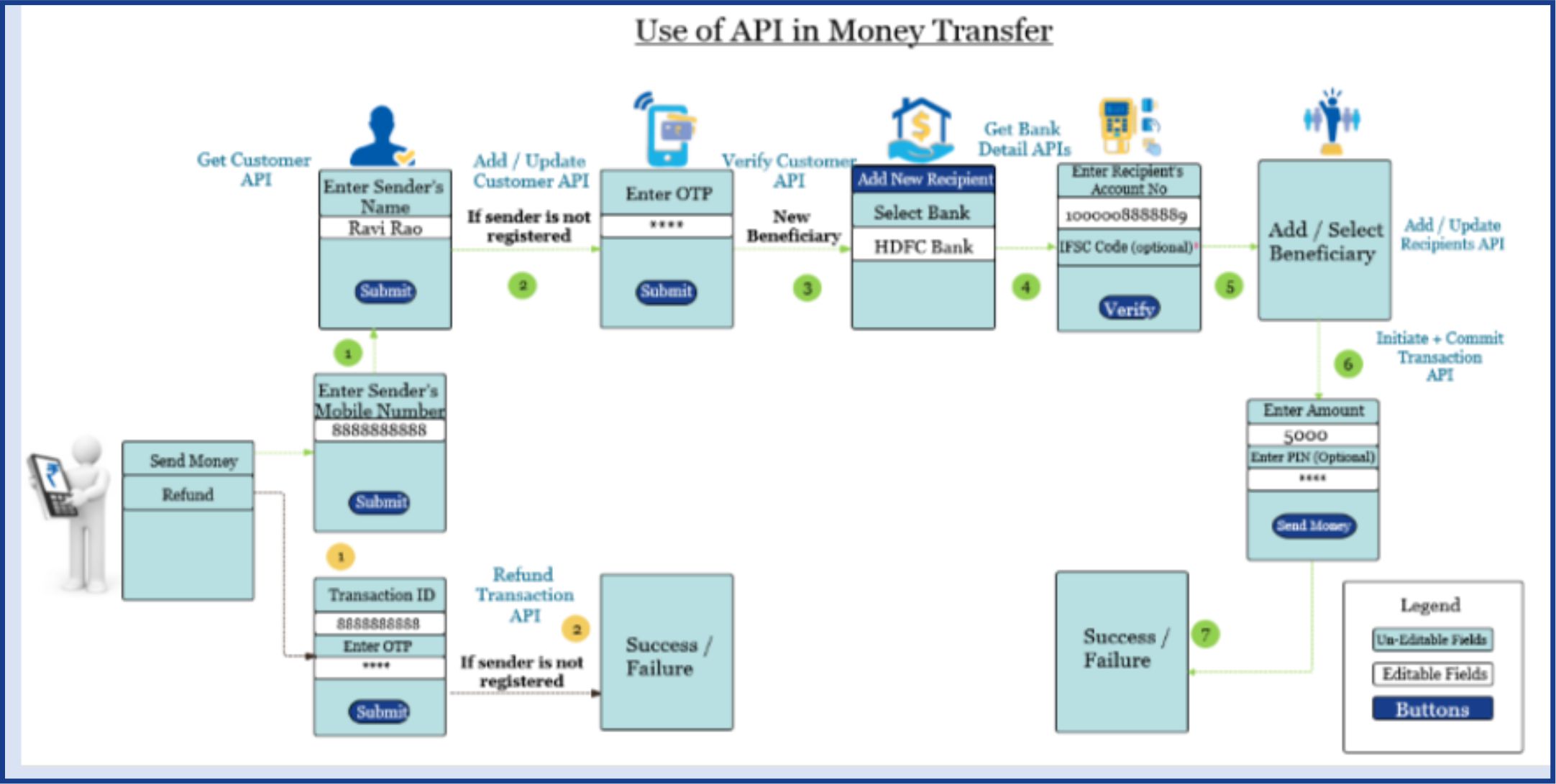

| Case Study – Eko’s Open API Platform

Eko India Financial Services is involved in the payments sector with a pre-paid instrument (PPI) licence* from RBI. Eko’s key customers include low- / middle-income customers and micro entrepreneurs earning less than Rs. 50,000 (US$ 770) per month. Eko provides technology platform for bill and merchant payments, peer-to-peer fund transfer, and agent-assisted remittancesEko provides open APIs to organisations interested in money transfer, and charges a fee for using its services and APIs. Eko’s open APIs allow partner entities to leverage Eko’s technology platform and connect with NPCI, UIDAI, banks, and aggregators, to build their own products. So far, Eko has released APIs for its domestic money transfer (DMT) business. This allows others to build their business models by consuming these APIs within the allowed boundary conditions. Besides providing superior UI/UX to their customers, partners have developed innovative payment and financial services use cases such as lending, money transfer, P2P transfers, and in-store and online payments.Open APIs have benefitted both Eko and its partners. Eko’s partners are able to scale rapidly and increase their distribution footprint. Through partners, Eko has been able to reach newer geographies. Eko is planning to expand its partner base, as well as introduce new APIs to provide more services through its ecosystem.The diagram below shows how Eko’s open API interacts with other embedded APIs to complete a money transfer transaction. |

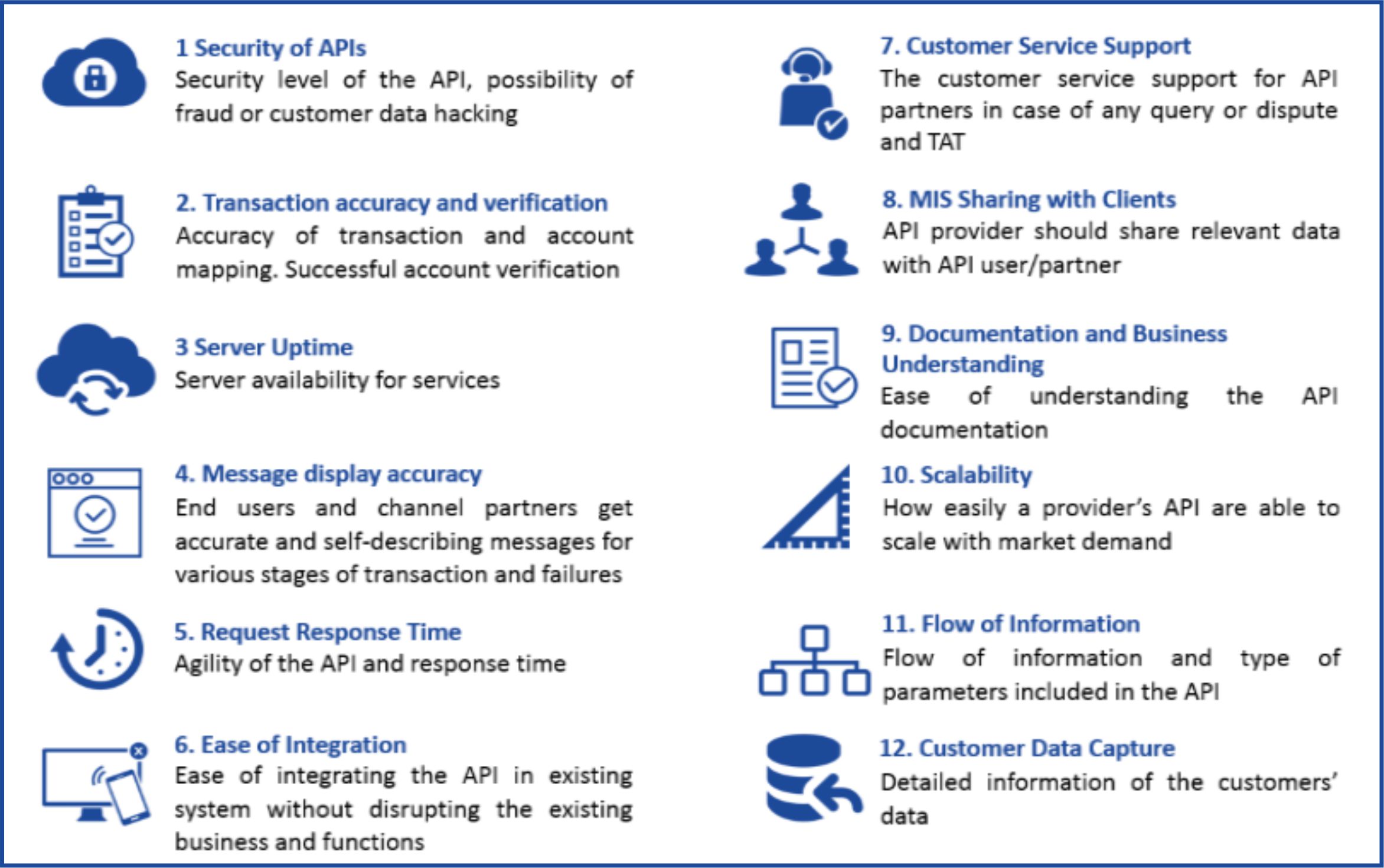

CGAP has identified comprehensive documentation, stability, easy access, and tracking as important elements for success of open API ecosystems. Based on a recent study done by MicroSave on use of APIs with a client, users evaluate the effectiveness of the APIs based on the following parameters:

Benefits of open API

Properly designed APIs provide benefits to both providers and users, along with a positive impact on customers.

a) Providers:

a) Providers:

• New revenue stream: Providers can capitalise on their existing assets, i.e. software and hardware, by providing their APIs to other companies on payment of a fee.

• Increased outreach: They can reach out to a larger customer base, through partners, without incurring high costs of distribution.

• Better utilisation: Providers can use their hardware effectively and can reap benefit of economies of scale.

• Future proofing: It is difficult to accurately predict the future. Open APIs can help providers a piece of the pie, even on unknown trends, as highlighted by CGAP based on M-PESA’s open APIs.

b) Clients (API Users):

• Time and cost reduction: A significant reduction in the time for go-to-market can be seen by riding on the existing stable platform, instead of developing the complex software. The users can not only reduce the cost of development, but also avoid sinking high one-time capital cost towards hardware.

• Scalability: Instead of worrying on scaling up of software and hardware, the clients can focus on distribution and scale quickly.

• Innovative solution: The clients have to build on the basic APIs exposed by the providers. This enables them to design and provide innovative solutions on top of the basic services provided by the API provider. Such customised solutions can provide unique services and experience to users, in line with local needs.

c) Impact on Customers:

• Convenience and experience: Properly designed and tailored services made available at the doorstep of citizens translates into convenience, and better experience. Even marginalised consumers will be able to choose providers and consume digital services according to their need.

Conclusion

Going by the global experience, a set of open, well-documented APIs provide enormous benefits to providers and clients. They also help improve customer experience.

API providers need to ensure easier integration, customer support, and scalability, while maintaining the security of financial transactions. Clients need to be sure of antecedents and capabilities of service providers as they scale up their businesses.

Today, there is tremendous amount of innovation around open APIs. The Government of India has taken early steps to fuel it through its ambitious Digital India plan. The possibilities of open APIs will only be limited by creativity, imagination, and business requirements.

Abhinav Sinha is co-founder, Eko Financial Services Pvt. Ltd