This report assesses pressing challenges that affect Mozambican mobile money agents: poor liquidity management, low working capital, and network issues. These challenges threaten the agents’ business and thus reverse the already realized gains in financial inclusion in the country.

The insights from this report will inform agent network ecosystem players in Mozambique to create sustainable strategies to maintain and expand agent networks.

Sunita, a domestic worker from Delhi, receives her monthly income through India’s United Payments Interface (UPI). She has a smartphone and a functional bank account and is well-versed in how financial technology works. However, Sunita is worried about not having enough savings for a medical emergency or old age.

India has experienced the deepening of financial inclusion through an increase in access and usage. However, a study of financial well-being to understand true inclusion is important. The US Consumer Financial Protection Bureau has defined financial well-being as the freedom to meet current financial obligations and adequate savings to manage short-term emergency needs and long-term future needs. The Global Findex 2021 describes well-being as a person’s financial resilience to deal with unexpected financial events, stress generated by common financial issues, and confidence in using financial resources.

Trends in financial well-being

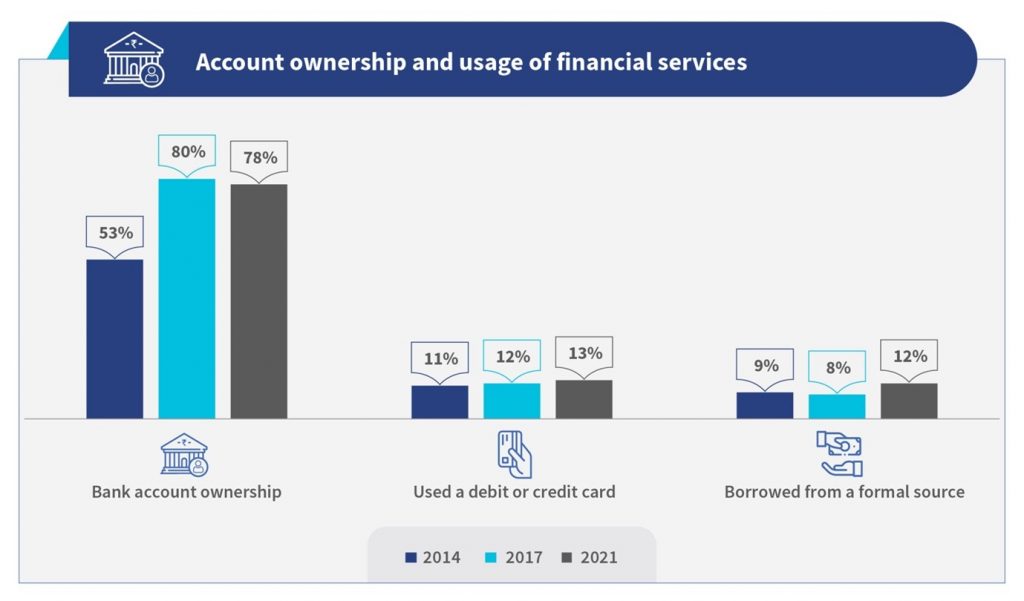

India has shown improvements in bank account ownership and usage of formal financial instruments from 2014 to 2021, as shown in Figure 1. Bank account ownership has jumped by around 50% from 2014 to 2021.

However, the data on financial well-being from India reflects high financial vulnerability. We used the Global Findex database 2021 data that included variables on individuals’ financial well-being in 2021 to gather insights in India.

Insight 1: People struggle to arrange emergency funds

In a survey, nearly 60% of the respondents in the higher-income group failed to meet their monthly expenses due to higher unexpected medical expenses during the COVID-19 pandemic and loan repayments. In the lower income group, 33% fell into a debt trap due to inadequate financial safety net, highlighting the importance of people being able to access and build an emergency fund.

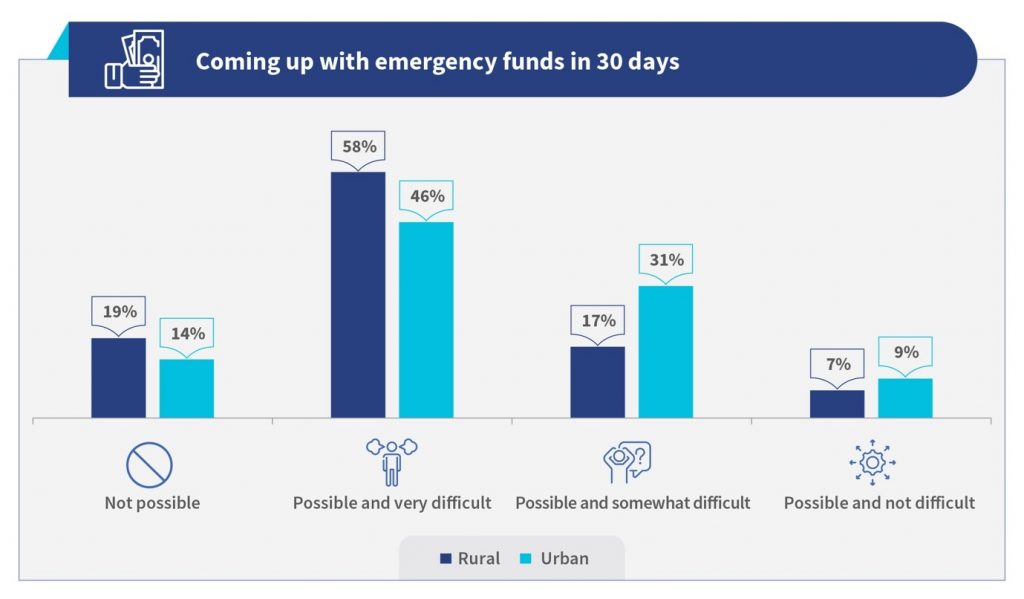

Figure 2: Source: Global Findex Database 2021

The data shown in Figure 2 captures a similar reality: most people lack a sufficient cushion for unforeseen expenses and find it “not possible” or “possible and very difficult.” Only less than 10% of the respondents across rural and urban areas were in a comfortable position to arrange emergency funds.

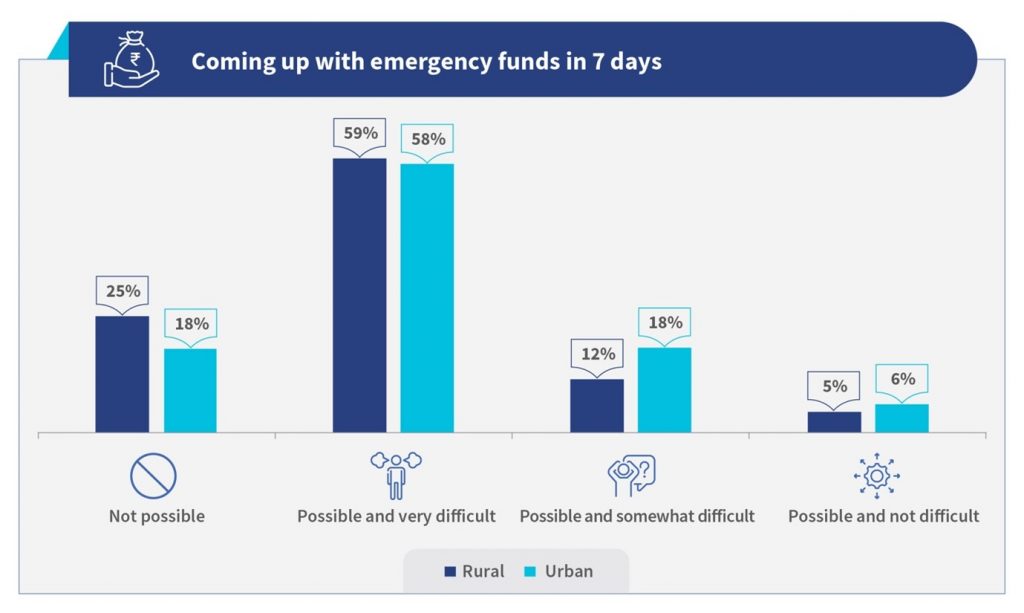

The situation was more acute when asked to manage funds within a week. See Figure 3. More than 80% of respondents found managing funds “not possible” or “possible and very difficult” to manage.

Figure 3: Source: Global Findex Database 2021

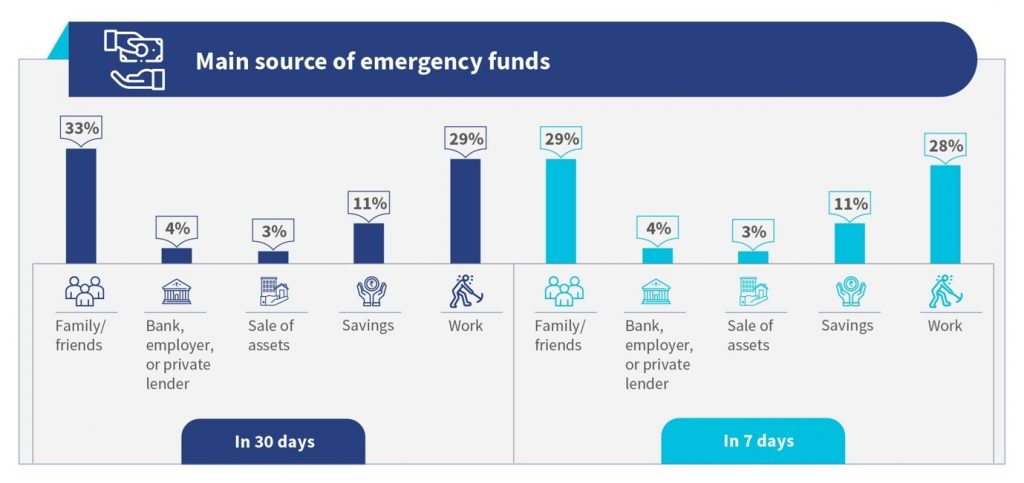

This data also highlights a deepened financial insecurity within social networks as most individuals rely on their family, friends, or employer to finance their emergency needs. Only 11% responded that they would access savings to meet emergency needs, as shown in Figure 4.

Figure 4: Source: Global Findex Database 2021

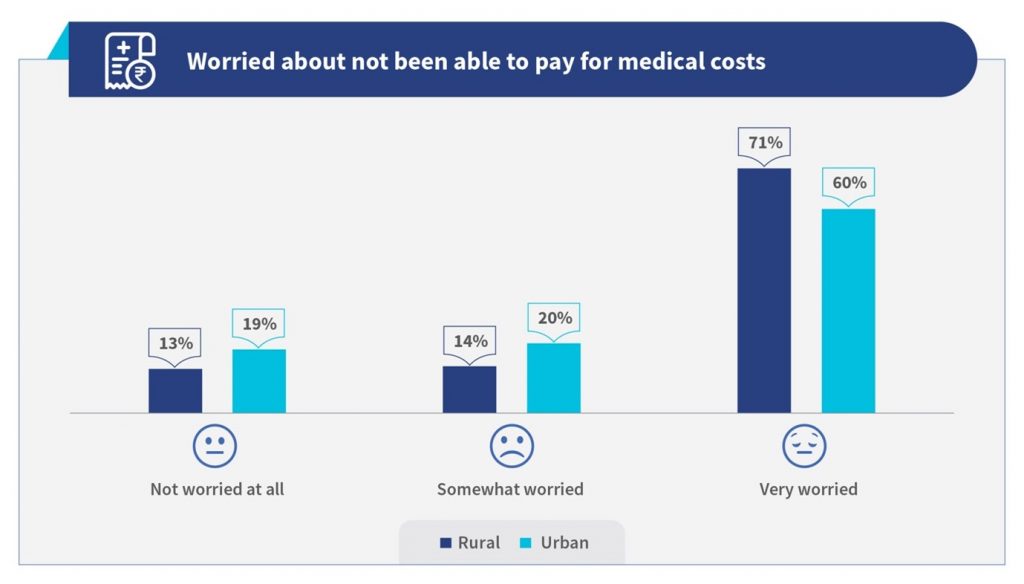

Insight 2: Medical illness remains the major cause of worry among Indians

Most Indians are one medical bill away from poverty. According to a study by the Public Health Foundation of India, about 55 million Indians were pushed into poverty in a year due to patient-care costs.

Figure 5: Source: Global Findex Database 2021

The Findex 2021 data shows that the most worrying financial issue for individuals is the inability to meet medical expenses. About 71% of respondents in rural and 60% in urban areas were “very worried” about lacking sufficient money to pay for medical expenses, see Figure 5. Moreover, even though health insurance coverage has increased over the years, it remains far from satisfactory. As per the National Family Health Survey (NFHS)-5, about 41% of households in India have at least one member insured. The fear of the inability to pay for medical illness varies with age and education level. About 72% of the people with primary or less education reported being “very worried” about the medical costs compared to just 53% who were educated at least up to the secondary level. About 70% of older people were also more worried about medical costs compared to 57% of the younger population, as per the Findex 2021 data.

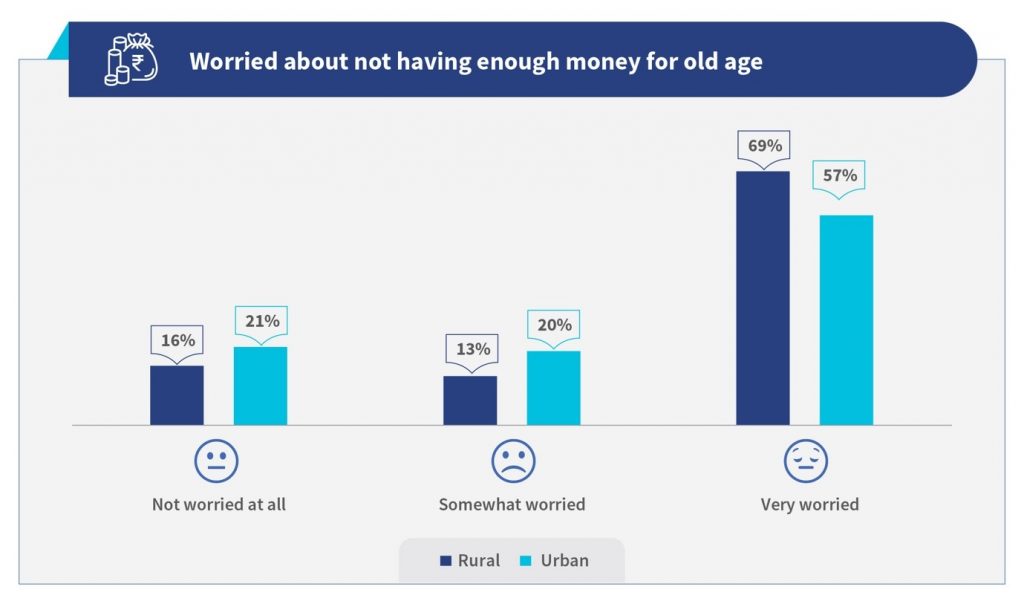

Insight 3: An increasing number of people are worried about not having enough for old age

The Findex database also measured another dimension of financial well-being—the perceived financial security for old age. Nearly 70% were “very worried” about insufficient savings to meet old-age needs, see Figure 6. The fears are corroborated by a UN report, which states that 52% of respondents think the current social security net for the elderly is insufficient in India. An August, 2017, report of RBI’s committee on household finance paints a similar picture that only 23% of Indians were saving or planning to save for retirement.

Figure 6: Source: Global Findex Database 2021

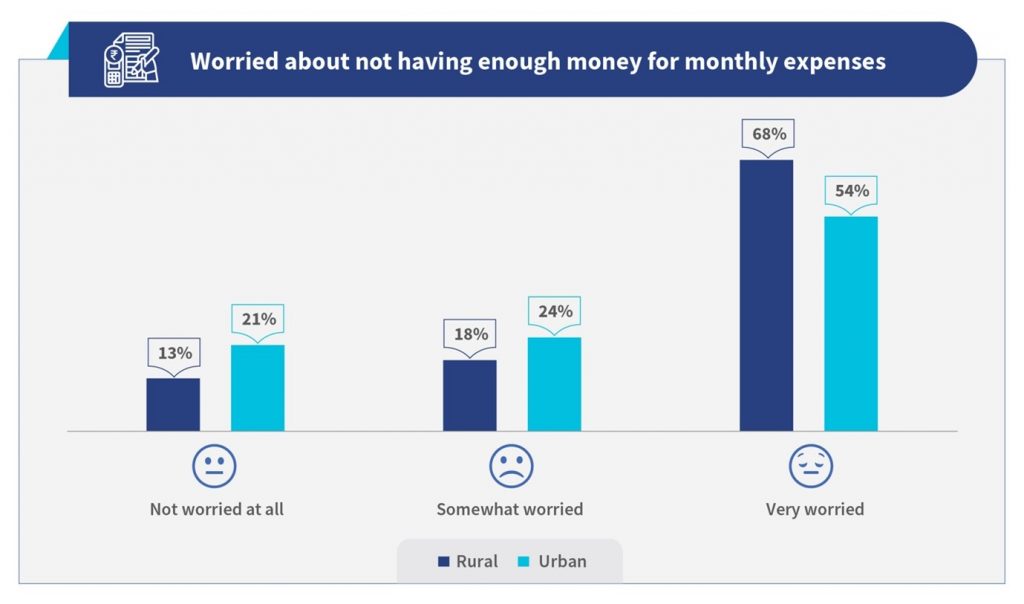

Insight 4: People are worried about not having enough for education or monthly expenses

The Findex data estimates that the majority of the people in rural (68%) and urban (54%) are “very worried” about not having enough funds for monthly expenses.

Further, about 59% of the people in rural areas and 44% in urban areas reported being worried about not having enough to pay for education (Findex, 2021).

Figure 7: Source: Global Findex Database 2021

Shifting focus toward financial well-being

Poor financial well-being has far-reaching consequences that affect the wallet and an individual’s physical and mental health. Further research is needed on individuals’ financial behavior and personality traits to measure financial inclusion through financial well-being and build effective strategies that do not solely focus on access or usage. This will build a story where Sunita and the many like her belonging to the LMI segment have the ability to absorb shocks, and are investing enough to meet emergencies and their financial goals.

The COVID-19 pandemic has spurred financial inclusion by increasing digital payments and expanding formal financial services. The Global Findex Database 2021 provides data on the growth in access to digital financial services and their use during the pandemic. The average rate of account ownership in developing economies increased from 63% to 71%. In the low- and middle-income (LMI) economies, excluding China, more than 40% of adults made in-store or online merchant payments using a card, phone, or the internet for the first time since the pandemic.

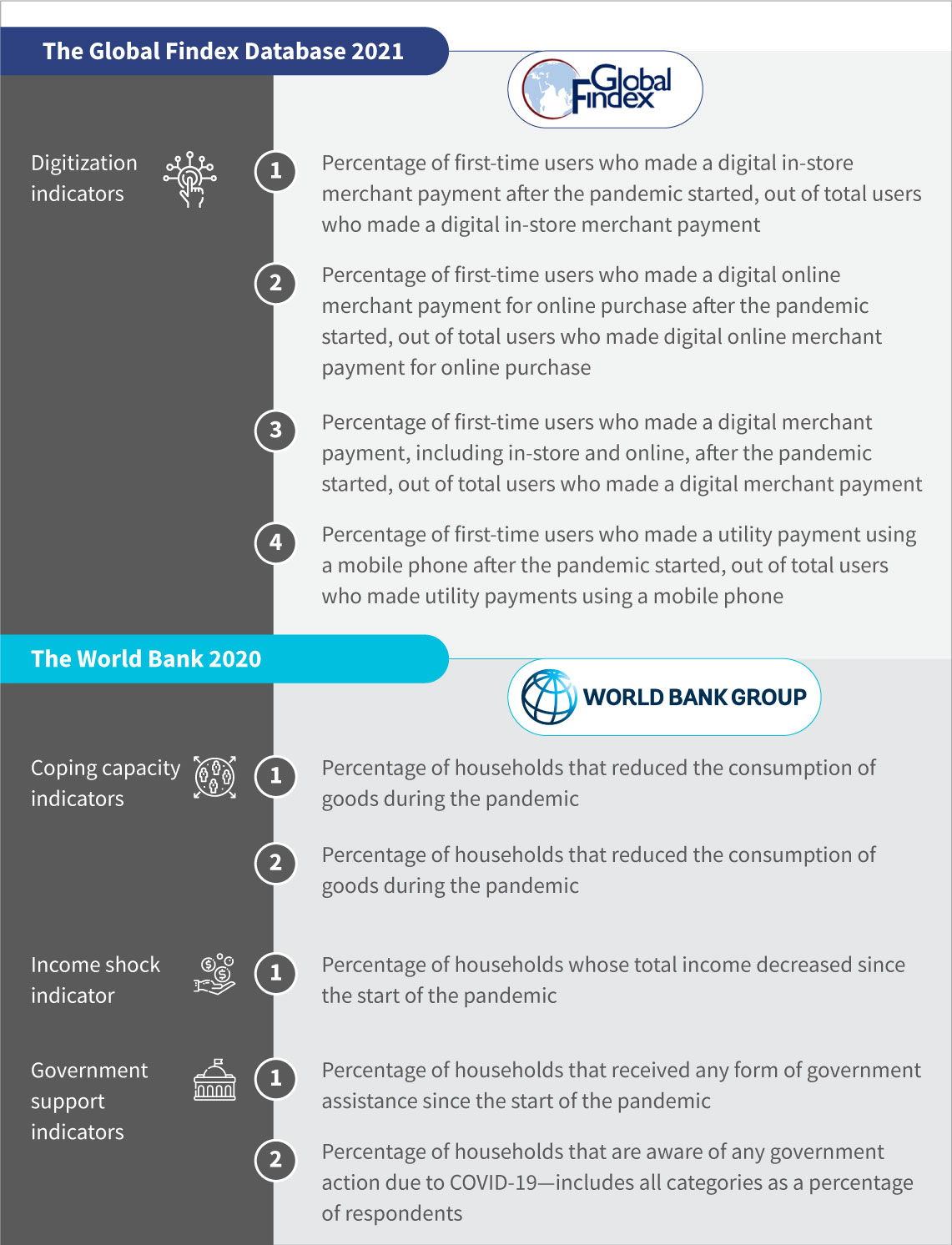

The increase in scope and intent of digital payments among LMI groups and MSMEs is also evident from MSC’s studies, where we examined the impact of COVID-19. Building on this work, we sought to understand correlations between the adoption of digital payments by an economy and its financial resilience to cope with the pandemic. We used The global Findex Database 2021 and the World Bank 2020 data to investigate.

The Global Findex Database 2021 data has indicators on first-time users of digital payments, including in-store or online merchant payments and utility payments during the pandemic. We used indicators related to income, coping capacity, and awareness of government policy from the World Bank dataset. After an exploratory data analysis of both datasets, we finalized four indicators corresponding to financial resilience and the adoption of digital payments from each dataset for this purpose.

Here is the list of indicators we used in our analysis:

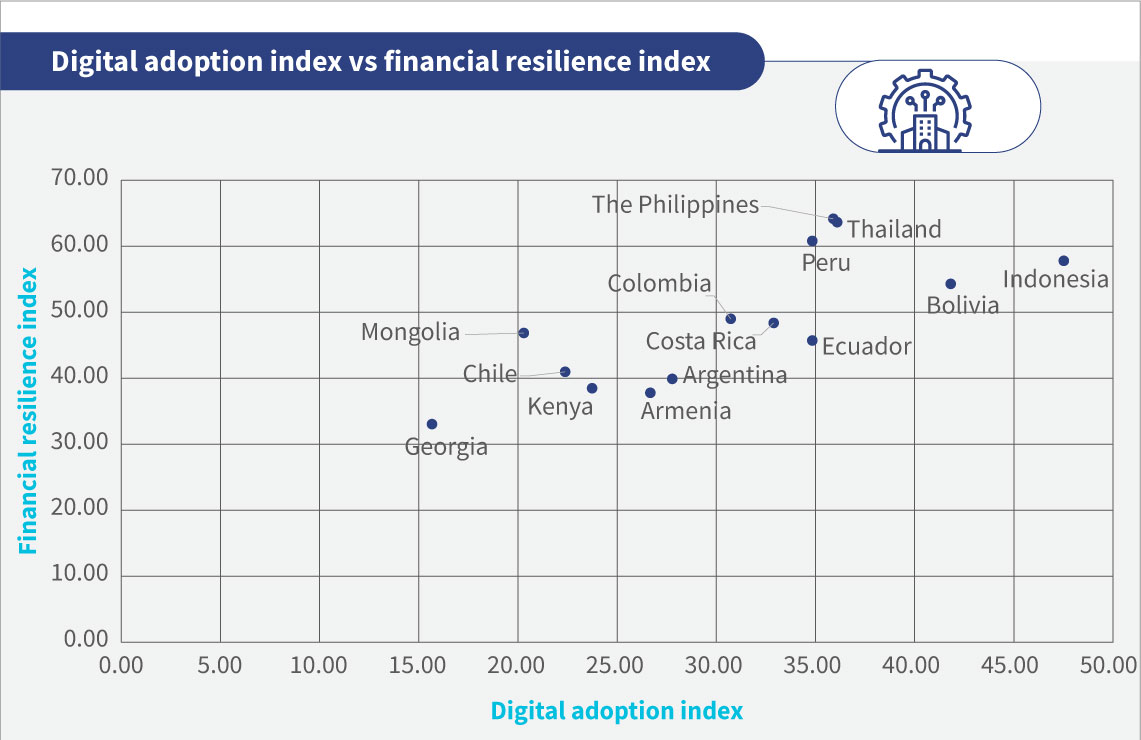

Data were missing for many indicators in most countries. We selected only those countries for which the complete data was available, or only one indicator value was missing. We created a Digital Adoption Index using Findex data and a Financial Resilience Index using the World Bank data for 14 countries across different regions.

The Index is inspired by the method Mandira Sarma used in ICRIER’s working paper on the Index of Financial Inclusion. We used the simple weighted average method to create indices.

The graph given below shows the relation between the two indices:

The scatter plot shows a strong positive correlation of 0.73 between the indices, implying that countries with high digital adoption at the start of the pandemic also showed higher financial resilience.

Increased financial resilience could have emerged from governments using digital channels to transfer benefits directly to beneficiaries’ accounts. Beneficiaries could use this amount digitally whenever and wherever they needed it. For example, people in cities could send money to their relatives in the villages. Digital payments sped up the transfer of money in the challenging times of the pandemic.

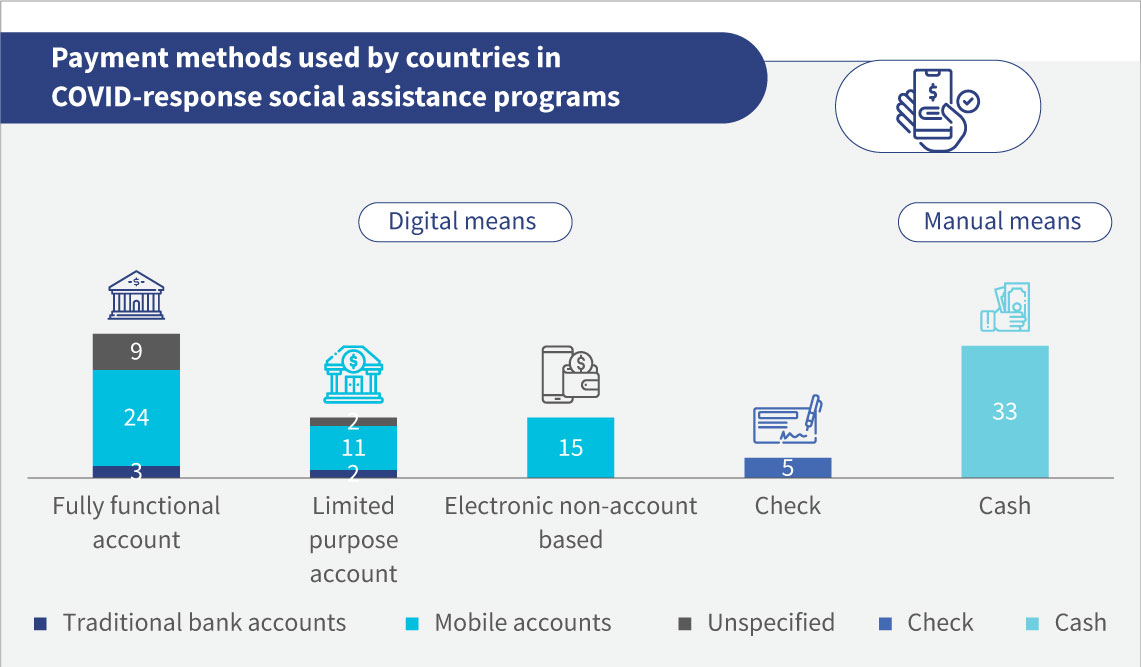

A World Bank tally of policy responses to the pandemic in 2021 found that at least 58 governments in developing countries used digital payments to deliver COVID-19 relief. Of these, 36 countries made payments into fully functional accounts, and only 33 governments used manual modes to deliver COVID-19 relief.

Payment methods used in COVID-response social assistance programs across a subset of 58 low- and middle-income countries (Source: The impact of COVID-19 on financial inclusion, a report by the World Bank and Global Partnership for Financial Inclusion (GPFI))

According to data from the World Bank, 84 countries reported changes to their social protection systems in response to the pandemic. Of these, 58 countries scaled up cash transfer programs. In many developing countries, the scale of these payments was unparalleled. For instance, new programs covered one-third of the population in Argentina, Pakistan, and Peru, and more than 70% of households received emergency transfers in the Philippines.

However, we noted a few exceptions to this general pattern observed across countries— particularly Bolivia and Indonesia—where the Financial Resilience Index lags in growth compared to the Digital Adoption Index.

In Indonesia, the adoption of digital payments grew during the COVID-19 pandemic. Of all the people who made digital in-store merchant payments, 47% did so for the first time after the pandemic. Similarly, 54% of all people who made digital merchant payments used digital payments for the first time after the pandemic started.

However, this did not reflect high financial resilience in Indonesia. Almost 50% of people in Indonesia reported reduced consumption of goods to cope with the pandemic. At least 10% had to sell their assets to pay for daily living expenses. A possible explanation for that could be limited use-cases in the country, as indicated in our latest study on QRIS implementation in Indonesia.

While COVID-19 prompted increased use of digital finance, all communities or consumers were not in a position to pivot rapidly toward digital financial products and services. People need connectivity, including ownership of a mobile phone, access to the internet, and digital skills to use digital financial services, which are not distributed evenly among the population. Besides, vulnerable segments tend to have limited access to these technologies.

Despite these challenges, most countries in our study showed a high correlation between resilience to the pandemic and the adoption of digital payments. Findex 2021 data suggests countries that adopted digital payments were financially resilient during the COVID-19 pandemic. However, our analysis was based on a restricted dataset due to the lack of data availability, and the results might change if we explore a richer dataset. The data shows how driving financial inclusion and digital payments can help build the resilience of nations in times of global disasters, such as the COVID-19 pandemic.

In our last blog, we featured the plight of Faith—a woman open-air and cross-border trader from Kenya. We highlighted the challenges she faces in accessing credit. We also discussed how existing solutions do not quite serve her needs.

But life was not always so hard for Faith. Before the COVID-19 pandemic, Faith was among the 45% of Kenyans living a comfortable middle-class lifestyle. She was a well-respected member of her community and the envy of her local women’s group. Her children went to good schools.

Faith owned a thriving retail business in her town that employed three full-time staff. She could comfortably service a USD 1,000 facility she had taken from Milly Finance (name changed), her local financial service provider. She would prepay her loans during good times to save on interest expenses. She was a model borrower for Milly Finance. She envisioned expanding her business and requested Milly Finance to extend her a credit line.

After the pandemic struck, the COVID-19-related restrictions dealt a fatal blow to Faith’s business. Her business was among 20% of businesses that closed permanently. Auctioneers picked off whatever they could to recover the outstanding loans. As she tried to manage the situation, she ended up depleting her savings reserves to pay her employees and keep her family afloat.

Things got so bad at the height of the pandemic that Faith had to downgrade her lifestyle. She moved to a different town. Unable to find meaningful work, Faith tried trading from an open-air market to supplement her income. She tried to borrow to make ends meet. However, risk-averse financial institutions meant little formal credit was available.

Further, formal credit providers did not lend to informal businesses like hers. Faith resorted to borrowing from an informal women’s group. As she was new to the area, she had not cultivated sufficient trust or savings to meet her needs. As a result, informal lenders became her primary source of capital despite their punitive rates.

No matter how hard she tries, Faith is yet to recover fully. Worse still, she no longer has confidence in formal financial institutions.

Like Faith, Milly Finance also struggled through the pandemic. More than 40% of Milly Finance’s portfolio deteriorated like many other financial institutions in Kenya, as many borrowers faced significant economic and financial impacts and thus could not service their loans. This situation forced Milly Finance to write off such loans.

Milly Finance also closed its local branches and now only operates from the capital city. However, it can barely survive and no longer afford to offer credit lines to micro-entrepreneurs. Instead, Milly Finance has anchored its turnaround strategy on lending to salaried up-market customers. Its dreams of digital transformation are shattered.

Even in the best times after COVID-19, Milly Finance and other financial institutions would struggle to meet the needs of micro-entrepreneurs like Faith.

According to our research, financial institutions find it difficult to cost-effectively tailor financial products for micro-entrepreneurs. Tailoring financial products for micro-entrepreneurs is difficult due to costs driven partly by the lack of scale to justify the business case.

Digital transformation for financial institutions is critical for them to remain relevant and competitive in an increasingly digital landscape. Beyond costs to implement, digitization also requires effective change management procedures and commitment from the board and senior management. If these essential components are lacking, efforts to transform the financial institution are often met with resistance and are short-lived.

Click here to watch our webinar on digital transformation for more insights.

A transition to risk-based lending and using alternate data to appraise customers would also be a game-changer. Unfortunately, these investments require upfront capital, which is not easy for Milly Finance and other financial institutions to come by in a post-pandemic and high-inflation environment.

Moreover, Kenya’s macroeconomic outlook makes it difficult for financial institutions, such as Milly Finance, to obtain wholesale credit cheaply. With a weakened shilling and reduced foreign currency reserves, lenders face high currency risk when servicing dollar-denominated debt. Locally, the situation is worse. With the 91-day T-bill rate at 9%, the government continues to borrow heavily from the domestic market to meet its development agenda due to an inability to access funds at cheaper rates internationally. This dependence on the domestic market raises lending costs and makes it harder for Milly Finance and others to extend affordable credit to micro-entrepreneurs like Faith.

Fortunately, the government is aware of the challenges that micro-entrepreneurs currently face. In partnership with the private sector, the government has rolled out new measures to lower short-term credit costs and whitelist excluded borrowers. In addition, the government has increased access to affordable, accessible, and convenient credit through the Hustler Fund to fulfill its mandate. The USD 500 million annual Hustler Fund will enable micro-entrepreneurs to access loans ranging from USD 5 to USD 500 at an interest rate of 8% per annum.

Undoubtedly, the promise of a single-digit, unsecured credit delivered digitally is attractive to Faith and others like her. Sadly, none of the government’s solutions would solve the problem for Milly Finance or similar financial institutions that face liquidity challenges.

Based on our work with financial institutions in Kenya’s financial sector, we observe that most institutions urgently need solutions that address the three pillars of credit: accessibility, affordability, and convenience.

Affordable, convenient, and accessible credit can become the norm for borrowers and lenders in Kenya by deploying targeted interventions on the demand and supply side. This paradigm shift has the potential to usher in a new future where informal micro-enterprises can flourish, expand, formalize, and contribute meaningfully to the country’s economy. This shift would be significant as more than 80% of Kenyans are engaged in the informal sector, which forms 98% of all business activity in the country.

Struggling financial institutions can follow a similar roadmap to regain their footing and cement their legacy in delivering credit that can unlock productive sectors of the economy.

Good causes need great designs and greater details. Funders, donors, and the general public want to know more about the social value created by projects. MSC has experience in both ends of the spectrum. We worked with donors and institutions to design better products or processes and evaluate the social value created by the products or processes for end users.

Yet, one constant aspect across these products and processes is not every user uses or acts the intended way. Acquiring this understanding made us the early advocates of customer-centered design. We found segments within the population worth studying and saw an opportunity to delve into the complexities of data to identify unique segments.

The segmentation MSC uses

MSC is among the early adopters of statistical techniques to understand the study population better. We base our recommendations on insights generated from data.

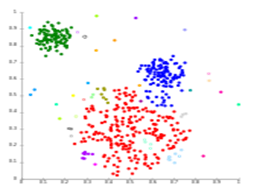

For instance, MSC conducted a study with fisherfolks to understand their financial behavior and management. The figure 1 shows three segments within the fisherfolk data, based on socio-demographic indicators, such as age, education, and income. The graph has three segments—red, green, and blue clusters—that were tested across different variables to understand their differences. Further, the graph shows groups with similar characteristics using cluster analysis.

Figure 1: Distribution of fisherfolk in three clusters

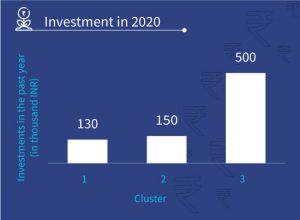

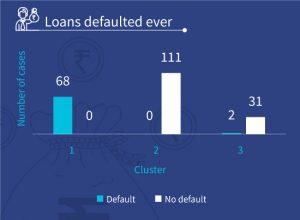

The figures 2 and 3 depict the investment made by fisherfolk in past year and number of cases of default by fisherfolk in each cluster. It shows how we used the segmentation approach to understand each segment’s investment pattern, credit behavior, and rate of defaulting on loans to develop a credit assessment framework.

Figure 2: Investments made by fisherfolk in 2020 Figure 3: Loans ever defaulted by fisherfolk

We conducted a similar exercise with the users of small finance banks (SFB) to understand the banking needs and financial behavior of different customer segments. Segmentation allowed us to design a better and more customized range of financial products for the banks’ LMI customer segment.

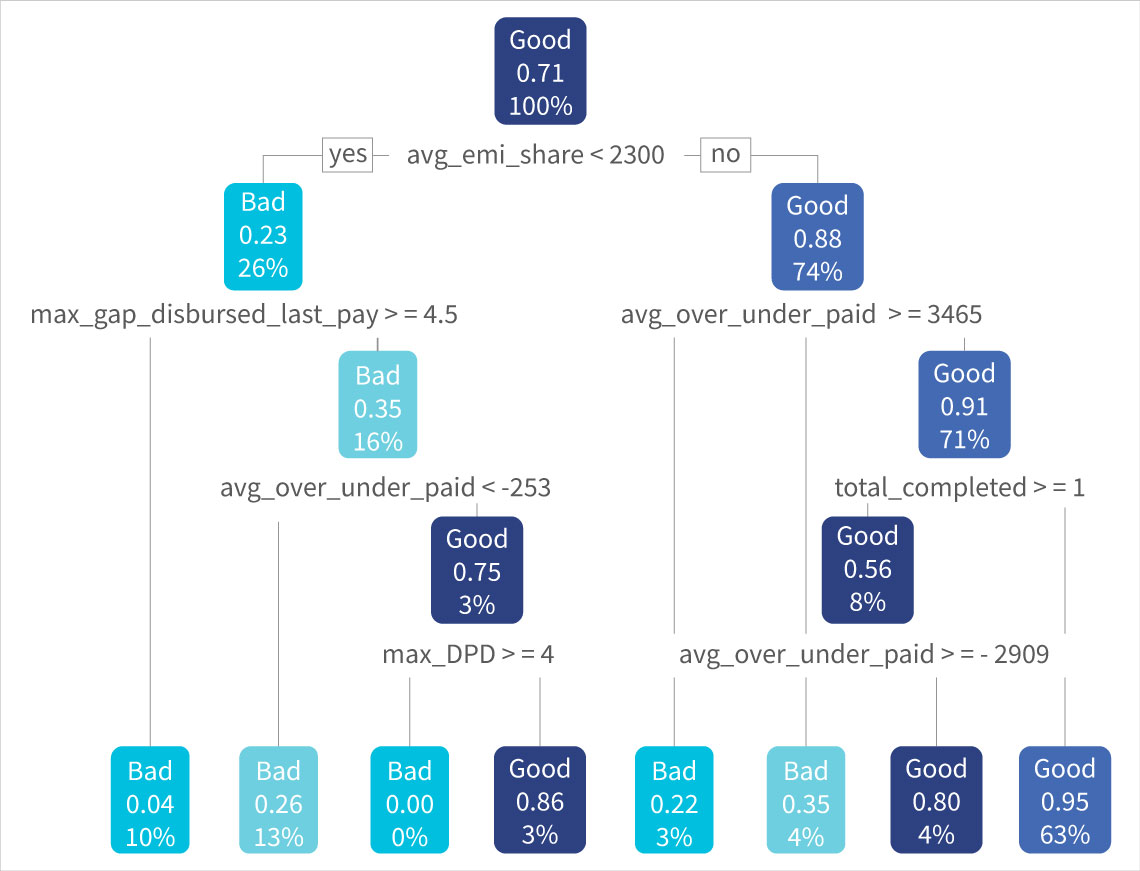

We conducted another exercise with a FinTech partner that offers digital credit to small merchants. We categorized creditworthy customers as “good” and customers with high defaults as “bad.” We followed up the segmentation exercise with predictive modeling using a decision tree approach, as shown in the figure. It helped us predict the customers’ patterns of defaulting and provide insights on indicators, such as likely geographical areas and groups of merchants with high defaults. Such analyses help businesses minimize risks greatly and adopt an agile customer approach.

Figure 4

Frontier Markets focuses on rural e-commerce. So, we conducted a similar segmentation exercise to identify their good and bad customers based on the customers’ buying preferences. Further, the segments helped us conduct anassociation analysis, make recommendations to the firm on product bundling, and provide customized marketing suggestions to its customers.

An approach to the segmentation exercise

MSC’s segmentation exercises are typically done in four steps, each adding a layer to the analysis required.

1. Variable selection phase: In the first step, we try to understand the purpose and need of the segmentation exercise. Understanding this helps chalk out the method or process to be followed to create segments from the available dataset. For instance, if we wish to know about a product’s uptake or usage, our variables of interest will be behavioral data or anything that affects that behavior, such as socio-demographics, income, or other variables.

2. Data collection and dataset development phase: Before collecting the data, we must identify customer characteristics. Once we have identified these characteristics, we can prepare a data collection plan that details where we can find each variable and the method to collect data. After data collection is over, we validate and process it, addressing outliers where needed. The data may often require creating variables from existing variables or converting numeric data to categorical data for better analysis.

3. Segmentation phase: After preparing the data for analysis, we must choose a model using machine learning techniques to conduct the segmentation exercise. The segmentation approach requires unsupervised techniques as no response variable is measured here. For example, when we predict loan defaulters the response variable is whether a person has defaulted on a loan in the past. Here, we wanted to group people with similar credit risk. Thus, no variable can be measured to compute similarity between credit behavior in a group of people.

Cluster analysis is the most popular algorithm used for segmentation. Creating rules manually to group observations together is challenging for datasets with a large number of variables. We need an algorithm to create these rules to segregate observations into homogenous groups accurately and efficiently. The cluster definitions change when we provide new data to the algorithm, which ensures that segments always reflect the current state of the data.

4. Data interpretation and modeling phase: The last step of the analysis is to find or define the characteristics of each segment obtained. We calculate averages of all data features for each cluster and use them to prepare cluster profiles to gain insights into our different segments.

However, segmentation may not help in all the scenarios. The insights generated from data can be unreliable if the sample size is not sufficiently large. Data can also lack any natural groups even though they may be present in the population. Incorrect responses, especially to ranking or Likert scale questions, can introduce bias in the data.

However, despite its limits, segmentation remains a powerful tool to find and analyze the diverse groups in a population. It enables policymakers, donors, and implementing agencies to understand and meet the needs of specific groups more effectively. In the ever-growing data economy, using tools like segmentation to understand our audience better and develop more customized and meaningful solutions.

The following are timestamps of the meeting conducted on 4th November, 2022, on “Climate resilient agriculture, virtual breakfast club.”

We organized a discussion with a panel of experts drawn from leading agriculture startups, who focused on the following:

Hurdles for AgTechs to effectively support the climate resilience of Indian smallholder farmers

AgTechs that enable the identification and assessment of climate vulnerability

Barriers to climate resilience of Indian smallholders that technology-enabled startups can help overcome

Click on the timestamps from the webinar stream to hear specific segments.

0:06– 3:10 : Welcome note and Introduction by Partha Ghosh, Senior Manager at MSC’s climate change & sustainability practice, along with the presentation on the climate resilient agriculture, virtual breakfast club

3:13– 04:08 : Graham A.N. Wright, Founder and Group Managing Director, MSC: Welcoming the speakers and start of the session

Akbar Sher Khan: Cofounder, Impagro Farming Solutions

Rahul Prakash: Founder and CEO, Amalfarm

Vimal Panjwani: Founder and CEO, AgriVijay

10:31– 11:30 : The speakers answered the first question: What are AgTechs doing to help farmers to respond to climate change?

11:40– 15:29 : Akbar Sher Khan of Impagro Farming Solutions responds: “Lots of innovation in identification and assessment has emerged for farmers. There are many technologies like IoT devices for soil data, micro weather stations to record data on a real-time basis, and remote sensing satellites.”

15:47– 21:19 : Rahul Prakash of Amalfarm responds: “We encourage farmers to adopt climate-resilient crops to cope with uncertainties in weather.”

21:40–25:25 : Vimal Panjwani of Agrivijay responds: “75% of farmers are smallholder farmers. As AgTechs, we work on the ground and have many devices for weather forecast, which can help farmers with proper harvesting.”

25:30– 26:41 : The speakers answer the second question: How do we make AgTech services available to poor smallholder farmers?

26:48–29:19 : Vimal Panjwani of Agrivijay responds: “AgTechs face the challenge of making technology affordable and accessible for farmers.”

29:40– 33:49 : Rahul Prakash of Amalfarm responds: “An advisory must have localization as per the location… otherwise, it will fail to find adoption from farmers.”

34:23– 39:30 : Akbar Sher Khan of Impagro Farming Solutions responds: “No matter how good your tech is, it all comes down to the human side of your business.”

44:07– 44:54 : The speakers answer the third question: How can value chain players be involved in driving the adoption of nature-based solutions and carbon credits?

44:46– 48:45 : Rahul Prakash of Amalfarm responds: When a carbon farming plugin is added with the context of Indian agriculture and issues arise in the absence of farmer ownership of the land.

48:53 – 52:57 : Akbar Sher Khan of Impagro Farming Solutions responds: “The carbon credit story to farmers is a fantasy … what we say is “the next generation will reap the benefits because your farms, your soil will survive.”

53:04– 56:08 : Vimal Panjwani of Agrivijay responds: “The value proposition for a farmer is increasing their income and decreasing expenses… so you have to link with that.”

56:10– 59:26 : Conclusion and note of thanks by Partha Ghosh, Senior Manager at MSC’s climate change & sustainability practice

59:29– 59:58 : Closing note by Graham A.N. Wright, Founder and Group Managing Director of MSC

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.