Auditing SHG balance sheets is vital for detecting errors, sloppy disclosure practices and fraud. It is the only way a bank can assure itself of a SHG’s capacity to repay in future. It is the only way members can assure themselves that their savings are really all present and accounted for.

Bridge2Capital: Instant supplier credit in three clicks

This blog post is part of a series that covers promising fintechs making a difference to underserved communities and supported by the Financial Inclusion Lab accelerator program. MSC is a partner to the FI Lab, which is a part of CIIE’s Bharat Inclusion Initiative.

|

Yash is a readymade women’s wear shop owner at Krishna Market, Chandigarh, clocking daily sales ranging from INR 10,000 (USD 145) to INR 12,000 (USD 175). Every week, he buys his stock from regular suppliers in Delhi and Ludhiana and also picks a few pieces from other retailers. His average supplier invoice is between INR 30,000 (USD 436) to INR 40,000 (USD 580) – which he pays through a combination of cash and bank transfer, including for the balance amount, after two to three weeks. However, he is still often unable to buy enough stock due to insufficient capital.

This has an adverse impact on his business as his sales are seasonal and managing stocks as per the season is challenging. Is there a better solution for Yash?

Small business owners like Yash do not get adequate support from existing providers like banks and micro finance institutions (MFIs) so, they have to rely on informal financial service providers. A new digital credit platform can address their short-term working capital needs. Read further to find how.

Capital in need is capital indeed

During their Basix years (from 2010 through 2015), both Mohammed Riaz and Nishant Singh partnered to set up various distribution channels for the Indian government. Their experience of dealing with small merchants and microfinance institutions made them realize the acute need for liquidity for mom-and-pop stores, also known as kirana stores, to support the burgeoning consumption-led demand. The founders saw a business opportunity to offer bill discounting to small-town merchants. Further, major changes in the Indian financial landscape such as demonetization, digital India campaign and introduction of Goods and Service Tax (GST) bolstered the idea. That’s when Riaz and Singh put their vision of helping millions of small businesses to practice and thus, Bridge2Capital was born.

Bridge2Capital’s mission is to solve the core problem of small merchants: access to capital to grow their business.

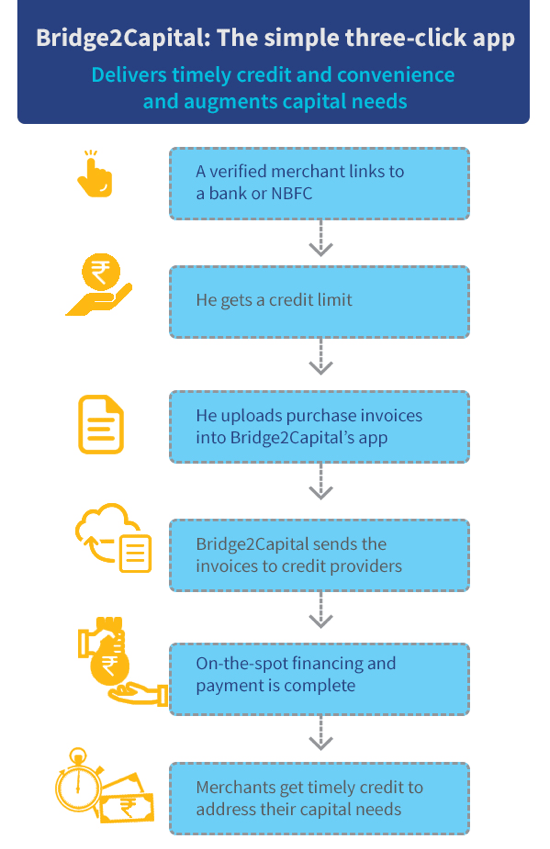

Bridge2Capital facilitates small merchants to avail credit limit through a mobile application-based paperless interface. Within five minutes, a verified merchant can be linked to a formal credit provider, such as a bank or an NBFC, and get a credit limit. Once linked, the merchants can start uploading their purchase invoices into Bridge2Capital’s app without leaving their premises. The infographic below describes the entire process flow of the app in detail. The merchants are then required to repay the amount that Bridge2Capital has paid to their respective suppliers on their behalf, in four weekly instalments within a month.

The pitch: Offering on-the-spot funding for small merchants

By enabling small business owners to avail credit limit from financial institutions through an intuitive mobile app, Bridge2Capital offers several more benefits:

Makes access to capital easier, which helps small merchants do more business and increase income

Provides better business possibilities and encourages livelihood opportunities closer to the community

Impacts the behavioral aspect of small merchants by transforming their business dealings from relationship-based to rule-based

Inculcates discipline in finances to allow merchants to manage their businesses better in a sustainable manner

The evolution: Introducing a novel platform to avail credit

The Centre for Innovation Incubation and Entrepreneurship (CIIE), along with MicroSave Consulting (MSC), conducted clinics, a boot camp, and diagnostic sessions. Subject matter experts from digital credit and marketing departments guided the startup during the sessions. It helped Bridge2Capital gain better understanding of the Indian financial ecosystem and build sound business strategies to complement it. Further, MSC also supported the Bridge2Capital team to streamline its field operations model. Thus, the team was able to craft the app’s business approach and troubleshoot business, product, and technology bottlenecks such as:

- Gaining the trust of end-consumers: The merchants still adhere to traditional business models and manually driven systems and processes. Since the Bridge2Capital business proposition is new, small merchants are wary of adopting it. Further, it required the merchants to switch from a cash-dependent business which they were habituated to, to the new age digital mode. The lack of infrastructure or technology was a valid concern but belief in the existing familiar processes was the biggest obstacle.MSC conducted a behavioral research study of small merchants focused on the key barriers that prevented the merchants from adopting the Bridge2Capital app.

- Familiarizing them with organized financial lending: Due to prevalent relaxed norms of informal lenders, the merchants had grown to feel that they could utilize the funds for whatever they want, even for personal consumption. The behavioral research study conducted by MSC helped Bridge2Capital better understand merchants’ financial behavior in managing their businesses.

With Bridge2Capital, Yash is able to check and procure stock from multiple suppliers without much trouble. His suppliers now offer him a 5% additional discount as they receive on-the-spot digital payments. With added convenience and discounts, Yash’s business is growing. With a boost in customers and income, he credits Bridge2capital for his better business.

Capitalizing on the future

The business model of Bridge2Capital has been evolving to achieve the best fit with market requirements and financial viability. It has successfully completed beta testing of its technology, with glitch-free and positive ratings of its mobile application by existing customers.

Within the overall market size of over 50 million small merchants pan India, Bridge2Capital intends to reach out to 2 million merchants across 1,500 towns and cities[1]. Today it supports 20 transactions every 30 minutes.Their dream is to support one transaction request a minute.

In a bid to use higher capacity, the company will explore models to achieve a higher conversion of merchants with optimal distribution costs. It aims to create a self-sustaining model that breaks-even at the distribution level – by enhancing user experience on the front end while creating seamless workflows at the backend.

Bridge2Capital will also focus on training and optimizing its field team. The company has chosen its way-forward revenue model and is aligning its teams and systems accordingly.

Post the FI lab support, Bridge2Capital has divided MSC’s recommendations into short-term and long-term actions and has been working towards implementing them to strengthen their business.

In the near future, Bridge2Capital seeks to ensure near-real-time disbursements, real-time reconciliation, and efficient collection processes to safeguard and deliver the “wow” factor to its customers.

[1] As per Bridge2capital’s analyses

Follow #TechForAll and #BuildingForBharat to stay updated on fintech start-ups driven to bridge the social, financial and economic inclusion gap.

Kaarva: A micro salary advance for a micro expense

This blog post is part of a series that covers promising fintechs making a difference to underserved communities and supported by the Financial Inclusion Lab accelerator program. MSC is a partner to the FI Lab, which is a part of CIIE’s Bharat Inclusion Initiative.

| Ram drives an Ola cab from 8am to 8pm across Bengaluru and makes about INR 50,000 each month. After spending on fuel, car maintenance, and the usual family expenses he barely manages to save any money. To add to that there are those medical expenses that come up every few months and Ram inevitably starts looking for a little money to tide these over. Banks and MFIs cannot give Ram one-off micro-loans at a short notice or at an interest rate that he can afford. Friends and family are not always a dependable option. What can be done to solve Ram’s dilemma? |

Hardworking Indians like Ram need easy, early access to their salary. Kaarva’s interest-free finance solution does exactly this for them.

Khusbhoo Maheshwari had just graduated from Harvard Business School and Agam Goyal from IIT-Mumbai when they met through an alumni network. They soon discovered that they shared a passion to solve the financial problems of tech-savvy, low-and-middle income (LMI), employed youth.

Recent studies1 estimate that there are 121 million emerging Indian households who can be categorized as low to middle income. They will need INR 218 trillion (USD 335 billion) in credit by 2025. Kaarva’s own research shows that 30 million of these Indians make less than INR 20000 per month (USD 3,600 each year) and need INR 1000 to INR 5000 (USD 15-70) in ‘sachet’ credit from time to time. The problem is real and deep for India’s LMI segment – young people often use up their salary early in the month and then run out of money to pay bills before the next salary comes through. Available alternatives, such as pay-day loans threaten the financial well-being of this segment. Kaarva was born to break the 30-day salary cycle and in effect make salaries available on demand.

Kaarva – the hindi translation for caravan – is a name befitting a company that aims to be a fellow traveler in the financial journey of Indians in the low-income segment.

The pitch: Your salary. Your right.

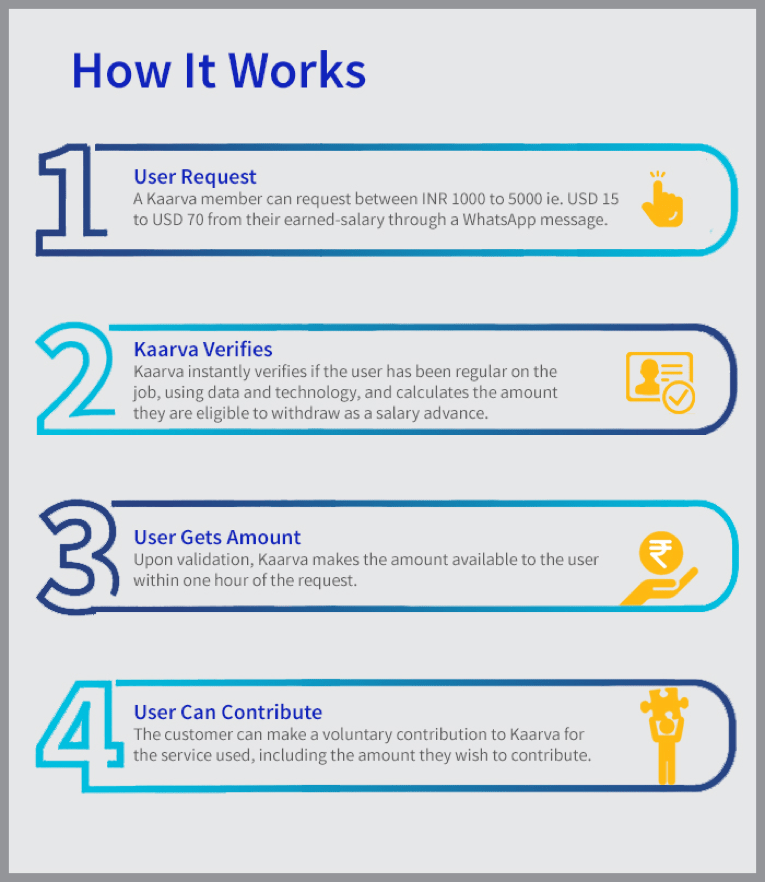

Our Ola driver Ram has a job that pays a regular salary and a bank account in which it gets deposited. He can raise a request for an advance salary with Kaarva and instantly receive that in his bank account – no fees or hidden charges. What’s more, Kaarva will not prescribe an interest rate or a fee for the loan but will allow Ram to choose the contribution he wishes to voluntarily make to support the service.

Khushboo believes that “Fees are inherently transactional. They give power to the person who sets it and demands compliance from the people who pay it. All companies should ask themselves—if you let your customers choose the price, would they continue to pay you?” –

The process: Radically quick turnarounds with simple technology

All Ram has to do is to download Kaarva’s mobile application. On the chat, he provides his last three income statements, his photo ID card, and a written undertaking that he will replay the salary advance amount the next time he receives his salary. If approved, he will get the money in an hour.

Kaarva is the perfect solution for employers who wish to provide a better financial future for employees.

The evolution: Overcoming roadblocks with support from the Financial Inclusion Lab

Kaarva competed with over 200 applicants to be selected in the first cohort of the Financial Inclusion Lab where boot camps, diagnostic sessions, and clinics helped them think through their business, product, and technology bottlenecks and build sound business strategies for success.

- Getting to the right customers

LMI groups in India vary across regions, industries and age groups. There is no set pattern or ‘one-size-fits-all’ formula for success. MicroSave Consulting (MSC) helped Kaarva address its biggest pain-point: identifying the right target customer segment, understanding their needs based on occupation, industry, age, and geography. Kaarva now knows that aggregated cab drivers are the best potential customers for it in the next 6-18 months.

- Scaling up at low cost and reshaping customer perception

After nearly a year of operations, Kaarva has on-boarded over 1000 customers. They now need to build a low-risk model to appeal to both, employees and employers, in order to expand. Publishing the app in vernacular languages will help scale up product adoption to millions, at a low cost. Kaarva will also need to shake off the skeptics’ perception of being ‘too good to be true’, owing to its ‘pay what you like’ model.

The future looks bright and fair for all.

“Kaarva is on a mission to help millions of hard-working Indians attain their financial goals. We believe in creating a future where money works for all.” – Agam G

Kaarva aims to make money smarter and work better for people. It means building a society where people work together to support products that help them. After all, it is not people who cannot keep up with bills and expenses; it is the existing systems that hold people down when they are at their most vulnerable. Thankfully, it does not have to stay this way.

“We can create a system built on generosity instead of greed. We can shape a future where people help each other, and companies value people over profits” – Kaarva.

Follow #TechForAll and #BuildingForBharat to stay updated on fintech start-ups driven to bridge the social, financial and economic inclusion gap.

1 https://www.linkedin.com/pulse/decoding-indias-consumer-lending-opportunity-bala-srinivasa/

munshiG: Digital assistant for grocery stores

This blog post is part of a series that covers promising fintechs making a difference to underserved communities and supported by the Financial Inclusion Lab accelerator program. MSC is a partner to the FI Lab, which is a part of CIIE’s Bharat Inclusion Initiative.

| Sanjay owns a kirana (grocery) store in the busy streets of Khar, Mumbai. With over 70 customers visiting his store daily, he struggles to track and update inventory, sales, and purchase records simultaneously, often leaving gaps. Many a time, he realises the shortage of a product, only when a customer asks for it. How can Sanjay monitor his stock to serve his customers? |

Kirana store owners like Sanjay need a solution that can integrate book-keeping, inventory and goods on credit given to the customers – while fulfilling customers’ demands every time.

India, like its global peers, is witnessing massive growth of large retail formats and e-commerce. This disruption has cast a shadow on the viability of kirana stores. Till now these stores have held their own. But the future may not be easy unless the stores transform the way they conduct business.

Busy grocers like Sanjay seek a solution to tie in their store’s back-end data, input items through voice and generate bills for customers. That’s where munshiG steps in.

A change-maker by nature

As a young boy living in a small town, Nishant often bought grocery from his regular store next door. But for a few remaining items he always had to wander around different stores in the neighbourhood. It left him wondering if a one-stop solution was ever possible. Now over the years, while smartphones and internet have transformed lives and businesses, the situation in markets back home had not changed much.

As a young boy living in a small town, Nishant often bought grocery from his regular store next door. But for a few remaining items he always had to wander around different stores in the neighbourhood. It left him wondering if a one-stop solution was ever possible. Now over the years, while smartphones and internet have transformed lives and businesses, the situation in markets back home had not changed much.

Nishant, now an engineer, wanted to finally change this. Could he create something to help shopkeepers manage their store better and more efficiently?

Nishant and his team developed a mobile, voice-enabled, book-keeping application for kirana stores, to deliver convenience and improve daily shopping experiences through technology. Drawing parallels from how his father’s munshiji (secretary) simplified his business, Nishant named this solution as munshiG.

The pitch: Create an era of tech-savvy kirana stores

munshiG enables shopkeepers to traverse the digital divide by giving them easy access to technology. By integrating its features into an Android application, munshiG is able to bring a low-cost solution with a technological twist. Moreover, the app can be customized as per a shopkeeper’s unique needs, which gives the app an edge.

The evolution: Making a difference to customers, storeowners and businesses

For an app like munshiG which was built to benefit a wide spectrum of kirana store owners, the way forward had several complex challenges.

Getting the voice feature of the app right: It was a challenge to detect a voice based on individual accents. Moreover, one item had varied verbiage in vernacular languages. For example, onion is called “kanda” in Mumbai and “pyaaz” in Ahmedabad.

Centre for Innovation Incubation and Entrepreneurship (CIIE), along with MicroSave Consulting (MSC), conducted boot camp and diagnostic sessions for munshiG. In the clinics, the subject matter experts guided the munshiG team in building a large repository of common terms and local word variations. With the MSC mentoring, the team improved the engine to decode maximum accents. It also addressed ineffective background noise cancellation.

Replacing shopkeeper’s existing software or switching costs: Tech-savvy shopkeepers had already invested in customised software like Bewo and Tally. They were reluctant to switch to new software because of sunk costs and limited trust in newer technologies. MSC helped munshiG to identify and recruit the right team, which would focus on familiarising the audience with the app.

Ensuring a seamless digital transaction: For small value transactions, customers were not ready to wait for payments or for the bill. Often, it led shopkeepers to skip the app for small-value transactions, particularly during rush hours. This would disrupt inventory management and bookkeeping records for the store. With support and prototype capital, munshiG could revamp its business model and leverage the right channel partners to enable swifter transactions

Started with a pilot in Udaipur, Rajasthan, munshiG decided to explore operations in Mumbai to achieve scale. With MSC’s support, munshiG could identify the target areas in Mumbai, the key attributes needed in the product and the persona of an ideal shopkeeper.

The shopping cart of the future is full

Currently, munshiG is working with 39 kirana stores in Udaipur, Rajasthan. By the end of 2019, the munshiG team aims to expand across 1200 kirana stores in 6 cities.

On the tech front, munshiG plans to upgrade the app through integration with barcode scanners and a better speech recognition engine.

As the business scales up in terms of market adoption, munshiG will leverage the unique insights generated by the kirana stores to partner with Fast Moving Consumer Goods (FMCG) companies offering them data analytics based services.

When every shopkeeper, like Sanjay, will have his own munshiG to address every customer’s needs, businesses are bound to flourish.

Follow #TechForAll and #BuildingForBharat to stay updated on fintech start-ups driven to bridge the social, financial and economic inclusion gap.

Navana Tech: Mobile tech for low-literates

This blog post is part of a series that covers promising fintechs making a difference to underserved communities and supported by the Financial Inclusion Lab accelerator program. MSC is a partner to the FI Lab, which is a part of CIIE’s Bharat Inclusion Initiative.

Bhavesh, 42, works at a kirana (grocery) store in Ahmedabad. Having dropped out of school in 5th grade, he struggles with using a mobile phone. So, on his smartphone he is able to call only those who are in his call log. He has to seek help to add or search for a contact or even to watch a YouTube video on his phone. How can Bhavesh maximise the use of his smartphone? |

Individuals like Bhavesh need a mobile interface that goes beyond their language and literacy limitations to help them make the most of their smartphones.

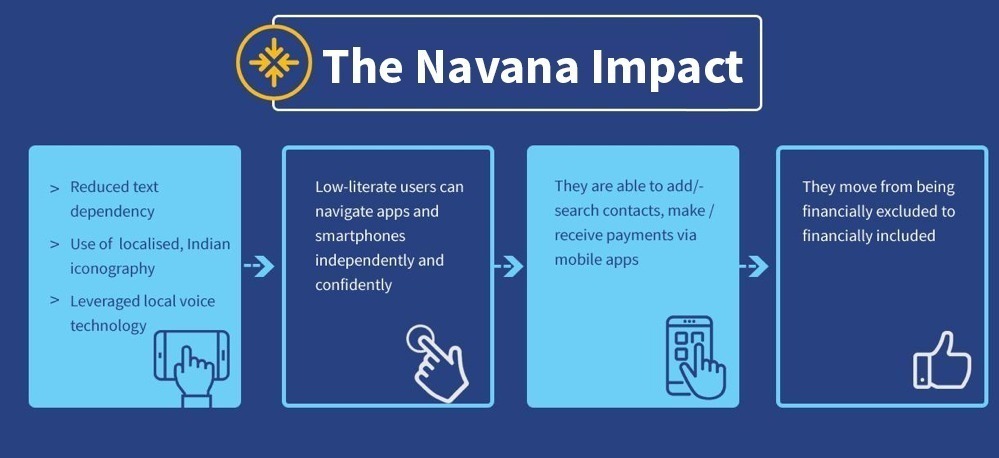

A study concluded that 775 million[1] illiterate people worldwide struggle to use text-heavy smartphones. Hence, while mobile applications have found broad usage across developing countries, usability remains a major hurdle for populations with the illiterate or low literate population. Hence, literacy levels remain a key barrier to providing access to information through technology. Navana Tech offers intuitive, text-free, voice-assisted, and image-based software development kit (SDK) that help bridge the digital divide between the literate and low-literates.

Not going by the word

When brothers and Cornell University graduates Raoul and Jai Nanavati started building products for the Indian markets, they faced a fundamental problem in the design. For example, the icon of a shopping cart could not be identified by a user who has never seen a physical shopping cart. The complex interfaces confused users in India, especially those in Tier 2 and 3 cities, dissuading them from accessing the same digital services as their literate counterparts.

Through Navana Tech, the duo developed a solution that addressed the limitations and litOS was born. At Cornell, they were one of the four student teams picked out of 45 to win a startup investment award of USD 80,000.

Through Navana Tech, the duo developed a solution that addressed the limitations and litOS was born. At Cornell, they were one of the four student teams picked out of 45 to win a startup investment award of USD 80,000.

A pitch: Beating the literacy barrier

Navana Tech offers research-driven design standards and developer tools to assist businesses to build intuitive mobile user-interfaces. It brings localized iconography, contextual voice assistance in nine Indian languages, and plug-and-play user flows. The Navana Tech Voice Dialer feature allows users to add or search for a contact by saying the name instead of typing it.

The evolution: Making the low-literates independent in mobile usage

Boot camps, diagnostic sessions, and clinics conducted by Centre for Innovation Incubation and Entrepreneurship (CIIE) and MicroSave Consulting (MSC) proved to be beneficial for Navana Tech. The experts advised Navana Tech to pivot their product offering from an operating system to a set of mobile applications based on SaaS model. The team also helped the company overcome challenges like:

Identifying the right user segment: The categories of mobile users in India are quite disparate in terms of literacy, access to mobile devices, and mobile literacy. It is hard to classify these categories to identify one common customer segment to target. Also, due to a lack of resources, Navana Tech struggled to conduct extensive testing on its product, and was unable to identify the product challenges faced by different user segments.

MSC helped test Navana Tech’s voice dialer application across geographies and customer segments including factory workers, Micro Finance Institution (MFI) customers, truck drivers, and shopkeepers. MSC helped Navana Tech understand the needs and abilities of different user segments while using mobile applications. The research insights helped Navana Tech to refine their offerings and target customers effectively. Eventually, it enabled the team to build a better and more user-friendly app.

- Designing an intuitive interface: The potential target segments varied based on mobile usage and literacy. So, it was challenging for Navana Tech to design an intuitive interface for an illiterate or low literate population; that closely replicated their familiar experience of an Android phone.

With MSC’s guidance, Navana Tech narrowed down the intuitive process of adding and searching for a contact. MSC also helped the firm build relevant iconography and relatable visual cues.

The future is mobile-literate

Navana Tech believes that smartphone penetration, mobile data usage, and online banking will redefine the fintech landscape in India. Various discussions during acceleration, helped Navana to identify the importance of partnership to reach users on a large scale. Today, the team works closely with its partners like Ujjivan Small Finance Bank (SFB) to re-design the Ujjivan mobile app for low-literate users. Navana Tech is also in the process of on-boarding two more partners in 2019.

In the future, Navana Tech aspires to impact the lives of millions of low-literate customers like Bhavesh. The aim is to customize products for the underserved segment and increase their access to digital solutions. Accordingly, Navana Tech believes that its business can reduce the digital divide while still achieving a sustainable revenue model and business growth.

[1] Indrani Medhi Thies, User Interface Design for Low-literate and Novice Users: Past, Present and Future, Now Publishers Inc., 2015

Follow #TechForAll and #BuildingForBharat to stay updated on fintech start-ups driven to bridge the social, financial and economic inclusion gap.

SureClaim: Assurance of insurance claims

This blog post is part of a series that covers promising fintechs making a difference to underserved communities and supported by the Financial Inclusion Lab accelerator program. MSC is a partner to the FI Lab, which is a part of CIIE’s Bharat Inclusion Initiative.

| There is a huge gap between the premium collected and claims reimbursed in India. Indians are likely to spend an estimated INR 300,000 crore (USD 42 billion) in 2021 towards treatment expenditures, with the low and middle income (LMI) segments incurring a significant part of the expenses. How can these customers leverage their insurance policies to the maximum? |

There is a pressing need to orient many, like 32 million Employee State Insurance (ESI) beneficiaries, and assist them in filing and claiming the entitled reimbursement claims.

A few years ago, Anuj Jindal faced serious challenges while filing insurance claims for a family member. The troubled times made him wonder how other customers might be coping with similar issues. The numbers backed his doubts: as per FY 2016-17 data, under the ESI Scheme, the central government collected a premium of INR 14,000 crore (USD 2 billion) and paid around INR 6,000 crore (USD 857 million) to its beneficiaries. This gap between insurance premium collected and paid is a whopping 57%.

At the country level, insurance can help maintain healthy financial lives during adverse times, especially in the LMI segment. But the low penetration of insurance and the complex reimbursement process acts against the philosophy of hedging unknown risks. Together, these form an important barrier to onboard new customers.

Today millions of people in the LMI segment, including those under the ESI Scheme, need support in filing their reimbursement claims. SureClaim is here to fill the gap.

The pitch: Offering right insurance benefits to the right people

SureClaim is co-founded by Anuj Jindal who looks after business development and Varun Kansal who manages operations. Their experience of working at Practo, Qikwell, and other companies provided them an understanding of the vital nuances of the insurance domain. Kshitiz Gupta, a technology expert with multiple stints at renowned firms like Expedia, Adobe, and Walmart, has completed the trio.

SureClaim is co-founded by Anuj Jindal who looks after business development and Varun Kansal who manages operations. Their experience of working at Practo, Qikwell, and other companies provided them an understanding of the vital nuances of the insurance domain. Kshitiz Gupta, a technology expert with multiple stints at renowned firms like Expedia, Adobe, and Walmart, has completed the trio.

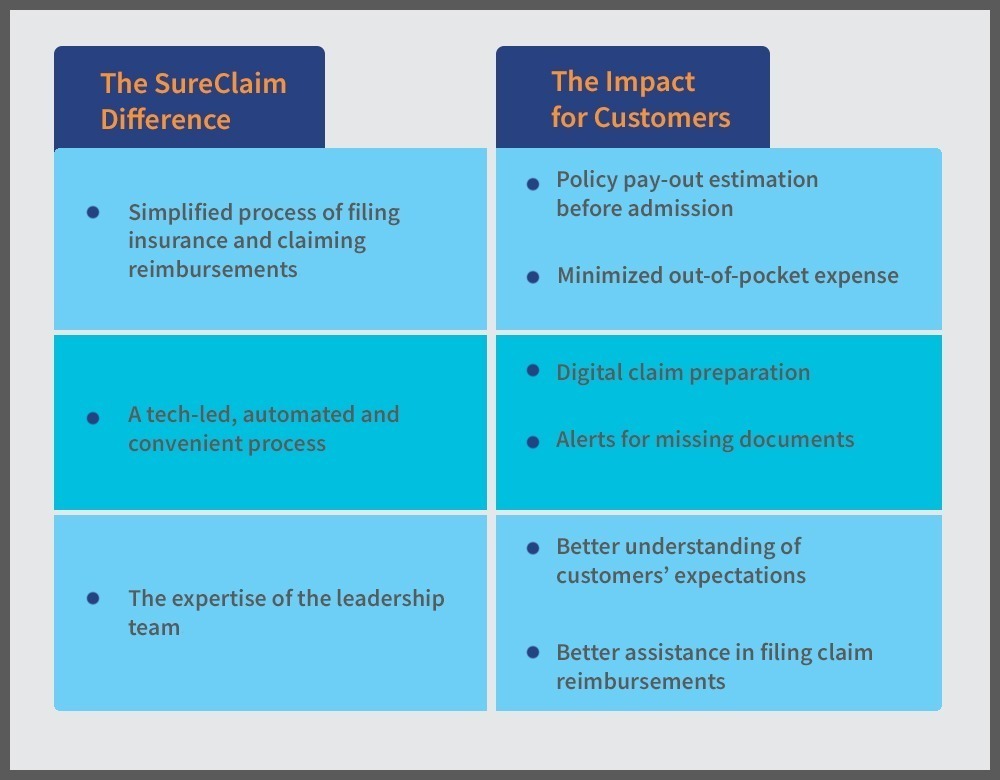

During a year-long in-depth field research, the team helped hundreds of patients in filing their claims. In doing so, the team realized that most people were willing to pay a fee, as the SureClaim service saved them precious time and effort. More importantly, the team minimized customers’ expenditure towards items that their insurance schemes covered – which customers were neither aware of nor apprised of by the insurance companies. As a result, the customers expressed a sense of gratitude towards the SureClaim team for their support.

These research findings set the stage for SureClaim. The team validated that it was solving a crucial problem by helping people claim all that they were entitled to as per their respective insurance policies. So, SureClaim aligned its staff and core processes to optimize insurance-related benefits for its customers – a unique service not offered by many market players. The team also understood exactly what the customers expected from insurance claims. It further helped SureClaim to better assist its customers in filing claim reimbursements. Today, SureClaim takes pride in understanding claims better than most other market players.

The evolution: Overcoming roadblocks in the claim reimbursement proces

The Centre for Innovation Incubation and Entrepreneurship (CIIE) and MicroSave Consulting (MSC) organized boot camps, diagnostic sessions, and clinics to advise the SureClaim team to refine its strategies and address its challenges. The team also received intensive guidance from sector experts.

For SureClaim, streamlining its processes and scaling-up was key. Under the technical assistance (TA) component of the FI lab, MSC supported SureClaim to look at their current business as well as exploring a new segment of ESI benefits.

- MSC provided insights to SureClaim to identify the different areas of intervention during orientation and claim reimbursements. SureClaim understood that they had to build a robust partner ecosystem to fill the gaps, and design a scalable technological solution for their product.

- On ESI front, MSC helped the team to understand the current processes followed by employers to orient employees on the benefits of ESI, thus refining their product. SureClaim team also found that employees lacked knowledge about ESI benefits and the claims-filing processes for medical reimbursements. This led the team to realize that employers required support to address their pain points – highlighting the need to build a customer service desk to reach a wider audience.

Together, this helped SureClaim to enhance their business offerings and craft better communication strategies for their audience.

The future of insurance. Claimed.

SureClaim aspires to add more capabilities to its online claims platform. These capabilities will enable users to search for their policy benefits using simple, everyday terms. They will also be able to predict all their expenses specific to a treatment which would be covered by their policy. SureClaim also seeks partnerships with service providers and insurance intermediaries who wish to deliver better claim reimbursement experience to their customers.

By covering gaps in the processes, SureClaim ensures that due claims are reimbursed in time with minimal troubles.

Follow #TechForAll and #BuildingForBharat to stay updated on fintech start-ups driven to bridge the social, financial and economic inclusion gap.