Smart data collection and geospatial analysis have the potential to allow providers to optimize the distribution of agent networks. This report notes that in the areas studied 52% of the rural population lives more than five kilometers from their nearest agent or bank branch. Through geospatial-modeling exercises, we identified 52 alternate service delivery points that, if acting as agents, could bring all the villages within a two-kilometer radius of a financial service point. The report also discusses agent segmentation to ensure agent viability and reduce agent churn. Introducing segmentation in the geospatial model resulted in the optimization of the agent network with fewer agents required to serve the target population.

Report on findings from the impact evaluation of Program Keluarga Harapan (PKH)

MSC as part of its MoU with the Ministry of Social Affairs conducted an impact evaluation and operations assessment of the PKH conditional cash transfer program. PKH is one of the largest social assistance programs of the government of Indonesia and has been operational since 2007.

The objective of this study was to give a snapshot of the implementation of the program and to evaluate the outcomes of key health-seeking and education indicators of beneficiaries. MSC adopted a modified Regression Discontinuity Design to measure the outcomes in the absence of baseline evaluation data.

The primary data was collected in 15 provinces across 60 sub-districts. The sample consisted of 1467 beneficiaries of PKH, who formed the treatment group and 1437 non-beneficiaries of PKH, who formed the control group of the study.

Please see Operations assessment and impact evaluation of Program Keluarga Harapan (PKH)

Boot camp experiences for start-ups: Cheaper by the dozen

Ang Lee’s Academy award winner Life of Pi shows the protagonist Pi Patel’s magical journey on a lifeboat where he attempts to discover himself. The excitement of Pi Patel’s adventures was not unlike the exhilaration that start-up promoters felt at a boot camp conducted for the second cohort of BII’s FI Lab, at the IIM Ahmedabad campus. The atmosphere of the four-day boot camp could be summed up in two words — enthusiastic and intense. The boot camp brought in a confluence of ideas from multiple start-ups, was packed with elements that gave start-ups moments of self-discovery and prodded—at least many of them—to get back to the drawing board.

Most of the nine start-ups in this cohort were different from the ones in cohort 1. The start-ups in this cohort had tested their product market fit with customers who had paid for their products and services. Some participating start-ups who had graduated from the first cohort were willing to tweak and change their solutions as long as they could find an answer to the rhetoric, “show me the money”, as heard in the film Jerry Maguire. With their product and pricing in place and having completed market-testing, the teams wanted to validate it further, and scale-up to the next level. Various boot camp sessions were designed to help the start-ups introspect and redefine their growth and acceleration needs.

Begin by understanding the customer: Low and middle income (LMI) segments

Great companies do not just offer products—they solve problems that matter. For the start-ups, the first step to doing that was to understand who they are speaking to. Now while the definition of an LMI segment looks simple on paper, several factors are “unknown” and demand deeper insight.

The session on understanding the financial lives of LMIs helped participants to know the segment better, identify characteristics, and create meaningful solutions to problems. They worked on market selection, market size, and salient features. At times, these in-depth activities brought them back to the drawing board. Eventually, they were able to comprehend the nuances of a large market and the prudence needed to pick a precise segment.

Find the value proposition of the offering: Build a brand around the buyer

Customers select solutions based on affordability, accessibility, awareness, and acceptability. Hence, identifying the right customer segments and fixing the right value proposition is a critical challenge.

The boot camp included sessions on value creation for the customers, helping the start-ups ponder on building a “brand”. Customer Perceived Value Advantage (CPVA) was introduced as a concept to explain that the success of an offering largely depends on how customers believe it can satisfy their wants and needs. When a company develops its brand and markets its products, the customers determine how to interpret and react to marketing messages.

In the exercise on customer centricity, the start-ups were asked to draw their customer journey maps and see where their respective customers fit. These maps helped start-ups stand in the shoes of their customers, and experience their own offerings as a customer would. They could see clearly when, where and how interventions were needed so as to retain customers across stages. There were conclusive insights such as “a brand is a representation of what the customer is looking for” and “start-ups have to sell a solution and not a product”.

The start-ups understood that they needed to think like a customer while designing customer strategies. They realized that customer goals and company goals were different. With an enhanced understanding of customer awareness, consideration, decision, delivery, and loyalty, this was an eye-opener for start-ups that earlier struggled to detail out their CPVA.

Courtesy: Dilbert by Scott Adams

Win the markets: Using right marketing strategy and pricing as weapons

The boot camp session on marketing strategies and communication (marcom) helped start-ups that were using social media for marketing. These sessions covered marketing strategies, while focusing on the importance of having repeat customers – and how this was an important goal of having the right marcom.

Products pricing: Pricing is crucial as it represents the start-up’s assessment of the value that customers see in their offering and are willing to pay for it. For start-ups that ride on aggregators, right pricing with the right channel partners is essential for rapid growth. Most start-ups had already priced their products, yet were seeking the sweet spot. Some start-ups had also experienced the decoy effect, where consumers change preferences between two options when presented with a third option that is asymmetrically dominated. For start-ups that ride on aggregators, getting the pricing right with the channel partners was a key aspect. Finding the right type of channel partners are essential for rapid growth.

Go-to-market (GTM) strategies: In this cohort, some start-ups had no GTMs, and others needed sharpening. A few start-ups had demonstrated the working of their business model with a robust GTM strategy. The boot camp discussed the “blue ocean strategy”[1]which referred to the simultaneous pursuit of differentiation and low cost to open up a new market space and create new demand. The boot camp shared how start-ups can create and capture uncontested market spaces—called “blue oceans”, making the competition irrelevant. These specific sessions opened new possible strategies to enter unknown waters.

The boot camp concluded with entrepreneurs intending to make a difference in the lives of the underserved. They all echoed what Will Smith says in the iconic film, The Pursuit of Happyness, “if you want something, go get it. Period”.

This FI Lab will be helping the start-ups with all that they need to go and get it!

[1] Introduced by W. Chan Kim and Renée Mauborgne in their best-selling book of the same name

Boot camp image credit – Centre for Innovation Incubation and Entrepreneurship (CIIE), IIM Ahmedabad

Operations assessment and impact evaluation of Program Keluarga Harapan (PKH)

MSC as part of its MoU with the Ministry of Social Affairs conducted an impact evaluation and operations assessment of the PKH conditional cash transfer program. PKH is one of the largest social assistance programs of the government of Indonesia and has been operational since 2007.

The objective of this study was to give a snapshot of the implementation of the program and to evaluate the outcomes of key health-seeking and education indicators of beneficiaries. MSC adopted a modified Regression Discontinuity Design to measure the outcomes in the absence of baseline evaluation data.

The primary data was collected in 15 provinces across 60 sub-districts. The sample consisted of 1467 beneficiaries of PKH, who formed the treatment group and 1437 non-beneficiaries of PKH, who formed the control group of the study.

Please read Report on findings from the impact evaluation of Program Keluarga Harapan (PKH)

Jai Kisan: Farmer’s gateway to quality financial services

This blog post is part of a series that covers promising fintechs making a difference to underserved communities and supported by the Financial Inclusion Lab accelerator program. MSC is a partner to the FI Lab, which is a part of CIIE’s Bharat Inclusion Initiative.

| Just hours away from booming urban setups, an average agricultural household in India makes a mere INR 6426 (around USD 100) per month: shockingly inadequate but surprisingly common. According to agricultural census of 2015-16, as many as 126 million, or 86% of Indian farmers are small and marginal landholders with a land size of under two hectare. Farmers, especially the smaller ones, lack access to affordable and timely credit, preventing them from enhancing their income – keeping them trapped in a vicious cycle. Could there be a way out? |

Today, smallholder farmers are the lowest priority for financial lenders and other service providers in the agriculture sector. The need of the hour is to fill the gap by enabling financing to such farmers at a lower cost.

Smallholder farmers regularly face issues of expensive and untimely financing, high-cost and low-quality agri-inputs, legacy or obsolete harvesting techniques, and an opaque supply chain. This leads to a sub-optimal realization of produce, making them a rare business entity that buys at retail prices and sells at wholesale prices—inverting the fundamental economic model, and leading to consistent net losses. While the Indian government has undertaken several initiatives to improve access to credit, the same could not reach to a majority of smallholder farmers.

Jai Kisan exists to disrupt this landscape by changing the lending ecosystem for smallholders. Jai Kisan is a fintech platform that caters exclusively to farmers by giving them access to finance, and enabling financial health in emerging rural markets.

Born from firsthand experience

Co-founders Arjun (CEO) and Adriel (COO), graduated from Texas A&M University with expertise in investing, structuring, and operations. They got early exposure to solutions, thought leaders, and professors who championed the idea of serving the consumers at the bottom of the socioeconomic pyramid. However, it is when they saw firsthand how access to financial services could enable development in rural emerging markets—and how the rise of the rural consumer is the next big opportunity-that the idea of Jai Kisan was born.

Co-founders Arjun (CEO) and Adriel (COO), graduated from Texas A&M University with expertise in investing, structuring, and operations. They got early exposure to solutions, thought leaders, and professors who championed the idea of serving the consumers at the bottom of the socioeconomic pyramid. However, it is when they saw firsthand how access to financial services could enable development in rural emerging markets—and how the rise of the rural consumer is the next big opportunity-that the idea of Jai Kisan was born.

Defeating the credit crunch through a comprehensive fintech platform exclusively for farmers

Jai Kisan is committed to breaking the current informal credit culture that stunts the economic and social growth of farmers. To begin with, it treats farmers as businesses rather than as consumers while facilitating formal credit efficiently. Jai Kisan’s FinTech platform analyzes farmers better, monitors the end use of capital, mitigates production risk, and facilitates repayment.

A unique pitch: Thriving with technology, differential lending

Jai Kisan utilizes a hyper-local credit-scoring assessment based on streams of financial and alternate data. Its credit-scoring platform assesses the risk of farmers quite accurately, enabling financing them at a lower cost. With its unique features and offerings, Jai Kisan aims to differentiate itself from the other players, through an innovative securitization solution that caters to current market needs.

Differentiators of Jai Kisan

Evolution: Unlocking ways to help Jai Kisan expand strategically and extensively

The Centre for Innovation Incubation and Entrepreneurship (CIIE) and MicroSave Consulting (MSC) conducted boot camps and diagnostic sessions to support Jai Kisan to build multiple business skills and identify present and future impediments to their business. Various experts in the field of technology, Corporate Social Responsibility (CSR), and agriculture guided the Jai Kisan team on setting up their IT infrastructure, and mentored and advised the team on improving business plans and building their competitor matrix.

The current model of Jai Kisan requires them to extensively understand the region: including the dynamics of key agriculture value chains, agro-climatic zone, the progressiveness of farmers, existing level of mechanization, and potential demand for equipment financing, before they can begin lending operations. They also need to understand other factors such as credit culture among farmers, a network of input retailers, the existing relationship between key stakeholders, processing or aggregating units, and markets, among others. It needs efficient methods to evaluate the potential of an area and make a go or no-go decision.

The MSC team supported Jai Kisan in assessing the suitability of Barwani district in Madhya Pradesh for geographical expansion of their operations. It was based on a number of factors such as farmers’ outlook towards agriculture; comfort levels in using technology, such as computers, smartphones, and feature phones; and credit behavior of farmers.

MSC also built the capacity of Jai Kisan and equipped them with an assessment template to customize and use in the future for similar assessments while venturing into new geographies.

Advance Mulching Technique MSC team with Farmers

The future is flourishing

Jai Kisan plans to scale to 100 operational channel partner locations across Maharashtra, Madhya Pradesh, Karnataka, and Rajasthan by the end of 2019. Further, it aims to invest heavily in building partnerships with credible stakeholders, including input suppliers and buyers. It intends to offer bespoke sustainable financing options across several farm mechanization solutions, enabling many smallholder farmers to reap the benefits in the future.

Follow #TechForAll and #BuildingForBharat to stay updated on fintech start-ups driven to bridge the social, financial and economic inclusion gap.

Wonderlend Hubs (WLH): Alternate route to credit history

This blog post is part of a series that covers promising fintechs making a difference to underserved communities and supported by the Financial Inclusion Lab accelerator program. MSC is a partner to the FI Lab, which is a part of CIIE’s Bharat Inclusion Initiative.

Sujit, Shopkeeper, Sujit, Shopkeeper,Maharajganj Sujit, 25, runs a kirana (grocery) shop at Maharajganj. He inherited the shop from his great grandfather over seven years back, but without legal papers. With expansion on his mind, he seeks capital to purchase products in demand, renovate the shop etc. But lack of credit history and legal ownership documents make Sujit a least preferred customer at banks. Can new-age technology help Sujit? |

Small business owners like Sujit need a platform to build their credit history using alternative sources of data – such as cash flow and transactions – and finally enable them to take loans easily and on time.

Micro and Small Enterprises (MSEs) play a vital role in the Indian economy. According to a recent Confederation of Indian Industries (CII) survey, MSEs provided 13.5 to 14.9 million new jobs in the past four years – mostly to unskilled and semi-skilled people from semi-urban and rural areas. This segment is identified by irregular income, lack of credit history in formal financial institutions and lack of physical collaterals – impediments to accessing credit from formal institutions.

Wonderlend Hubs (WLH) utilizes everyday digital footprints and cash flows of an MSE owner to create a credit record. It tracks the repayment capability, business solvency, and credit needs of MSE owners, making them a credit worthy customer in the formal credit market, and facilitating hassle-free and quick credit.

Treading new roads

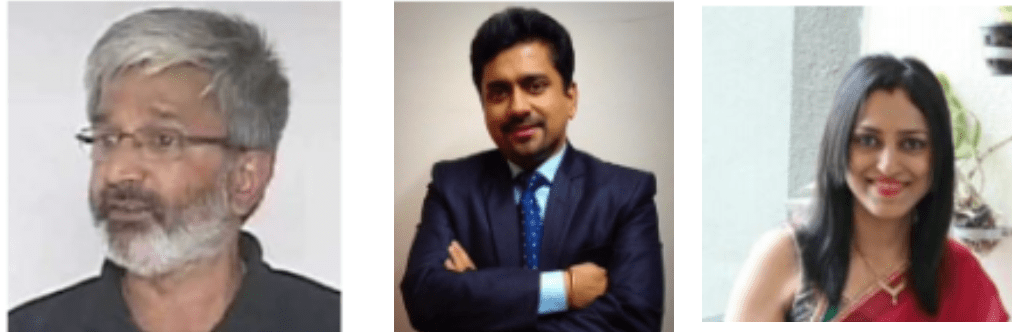

The WLH team, Ram Ramdas, Founder, Rajesh Iyer, Chief Business Officer and Anusha Jathanna, Co-founder and Head – Platform & Products goes back to Herald Logic, an earlier venture they started together. At that time, they garnered knowledge about big data, machine learning, and human innovation, and observed that credit flow was significantly hampered for a large segment of India due to lack of credit history. This gap steered the idea of WLH – a unique solution that makes finance accessible to “the next 500 million” of India from the MSE and other underserved individual segment.

Ram Ramdas, Founder Rajesh Iyer, Chief Business Officer

The pitch: Building credit history one day at a time

Today, banks find it challenging to assess potential loan customers based on non-standard data without a credit history. Collecting and analyzing relevant data-sets for a small loan ticket size for MSEs is not cost-efficient either. Underwriting and operations are not feasible, making formal credit unviable for MSEs. WLH aims to bridge the credit gap for the under-served segments across the urban, semi-urban, and rural areas of the country. WLH also intends to customize the credit product based on business needs and aspirations.

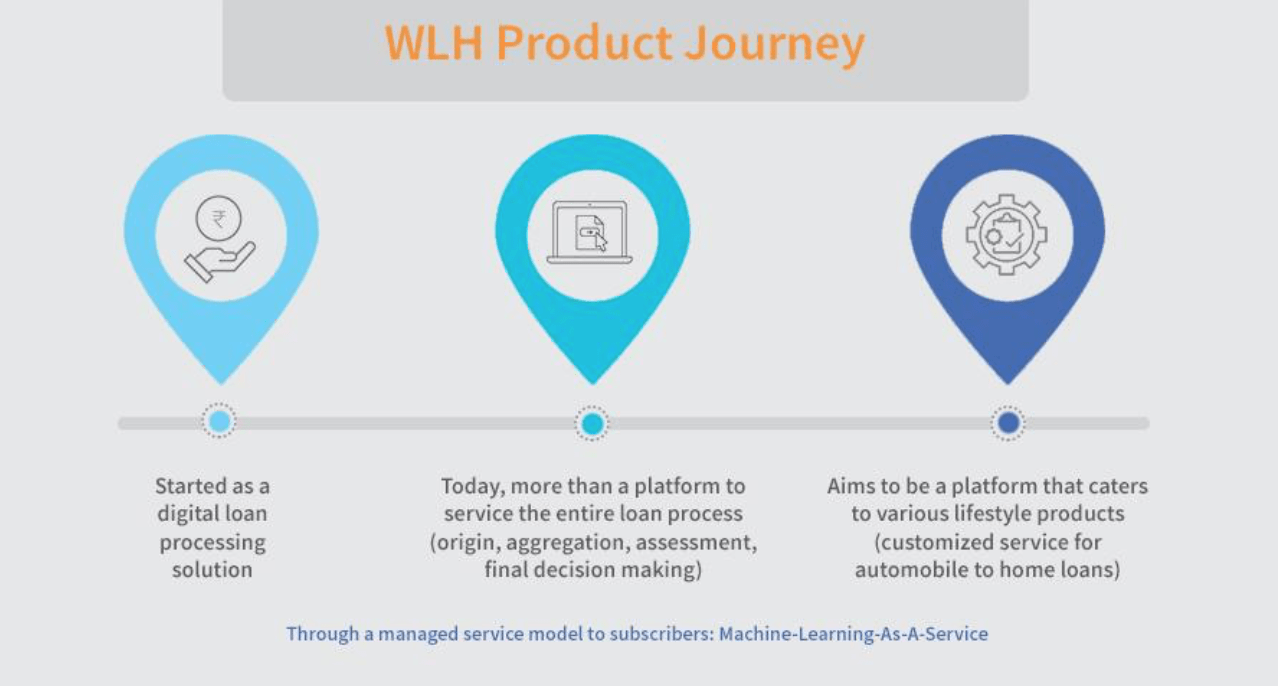

WLH product range

The evolution: Reaching out to the right target segment

Along with MicroSave Consulting (MSC), the Centre for Innovation Incubation and Entrepreneurship (CIIE) conducted boot camps, diagnostic sessions, and clinics to help the WLH team to tide-over their business, product, and technology bottlenecks and craft sound business strategies.

While WLH wanted to disrupt the credit market for the unserved and under-served segments, identifying the exact target segment was a challenge. The team needed to understand the MSE segment better, their diverse day-to-day business practices, how they sought credit and how the local financial ecosystem influenced their behavior.

These sessions, coupled with MSC’s research, helped WLH gain a better insight into the current business and credit practices, and the demand for credit among MSEs. The team could also assess a merchant’s familiarity with digital financial services, and identify enablers to promote uptake of digital products. Based on the study, WLH gauged their position in the market and how they could design a customized product to maximize business.

A future for Bharat

WLH is a business-to-business-to-consumer (B2B2C) platform aiming to provide fully configurable and scalable managed services to help the new age lenders, aggregators, independent originators, and other fintechs. It will help these institutions to identify customers who can take small ticket size loans and offer tailored credit products to them. The solutions will be available in the form of “The Bharat Credit Stack” – easy to access, easy on the wallet, and bundled API usage plans that target highly customized credit sanctioning.

WLH aspires to be a preferred “credit gateway of Bharat”, where it can use alternate sources of data to generate a credit history for people like Sujit. This will make him a creditworthy customer in the formal credit market.

Along with strategic product partners – “How India Lives” and “121 Mapping” – WLH has also developed Socio-Economic Profiler (SEP), an industry-first, alternate public data-based system. WLH leverages a bevy of conventional and new-age macro-economic data sources backed by machine learning and advanced analytics to build SEP. The SEP will provide indices and scores at pincode levels to predict delinquency. WLH has already done a successful proof of concept (POC) on the SEP and it is in the final stages of client data validation, slated for a market release shortly.

By developing India’s first alternate data credit bureau by 2020, WLH intends to process approximately 20% of the retail and small business loan volumes in India by 2025.

Follow #TechForAll and #BuildingForBharat to stay updated on fintech start-ups driven to bridge the social, financial and economic inclusion gap.