Savings groups play a critical role in bringing access to financial services in rural areas where formal financial services are largely limited.

The onset of COVID-19 and the health and safety requirements to practice social distancing has limited the functioning of savings groups. Most members have been unable to meet to deposit savings, pay their monthly loan repayments, and discuss other group-related matters.

In this video, we present the challenges that savings groups face due to the COVID-19 pandemic and how the digitization of these savings groups operations benefits both the group members and the associated financial service providers.

Thirty-year-old Hope could barely contain her excitement. The homemaker from a remote district in Zambia had just heard the news that her savings group was being linked with a bank. She chose to join a savings group in her village as she knew the importance of financial services. Although she had a bank account, she preferred the savings group. This was because the bank branch was located 40 kilometers away and Hope felt that using the bank’s services was not worth the hassle of traveling the distance.

With her savings group being linked to a bank, Hope could now access door-step formal savings and credit services both for her group and herself. Her excitement though was short-lived, as her savings group halted operations once the government-mandated restrictions came into effect after the COVID-19 outbreak. This hindered access to savings and credit services for Hope and other members.

Hope’s situation is not unique. Many people like her across the world share a similar fate, as savings groups pause operations due to the restrictions and lockdowns enforced to contain the spread of the virus. Savings groups comprise self-selected individuals, especially from low- and moderate-income backgrounds, who pool money and on-lend within the group based on mutually agreed terms. Such groups play a pivotal role in bringing access to financial services in rural and remote areas where formal financial services are largely limited. The world today has about 750,000 savings groups with more than 15 million members across 73 countries.

Savings group mechanisms provide a safety net for vulnerable families by providing informal savings and credit services. Financial institutions have started to link savings groups after considering the opportunities to offer a broad range of financial and non-financial services to both groups and individual members. In this blog, we assess the impact of COVID-19 on savings groups linked to financial institutions and how financial institutions may adapt to help savings groups overcome the challenges and build resilience.

COVID-19 has caused an economic crisis and a global disruption of supply chains. MSC conducted a study recently to assess how the low and middle-income segments have been coping with COVID-19 in Kenya. It revealed that more than three-quarters of the respondents have either stopped earning or are earning less as a result of COVID-19. Most respondents confirmed that their savings are being depleted as their revenue sources have dried up.

As part of government measures to contain the spread of coronavirus, people are advised to observe social distancing and avoid social gatherings. Before COVID-19, the savings groups used to gather regularly as a group to meet, interact, and carry out financial transactions, such as savings, borrowing, and loan repayments. They would use these meetings to enhance skills and capacities and discuss social issues and problems. Social distancing guidelines and the fear of contracting COVID-19 have made it difficult for the savings groups in most countries to conduct meetings. Meanwhile, group members have shifted their expenditure priorities toward more urgent household needs, such as food. They have therefore been missing on savings or loan repayments. Moreover, the lack of meetings results in inadequate peer pressure to sustain these transactions.

The situation is equally bad for the savings groups linked to financial institutions. In the absence of group meetings, financial institutions have seen a fall in savings collection and delays in loan repayments. Besides, the members who have a need and the ability to repay credit have found it difficult to access loans. Without meetings or a digital platform, members who have saved thus far find it difficult to withdraw their savings to meet their needs—just when they need them most.

Uncertainties persist around the availability and effectiveness of the COVID-19 vaccine. No one knows if the virus will mutate, which could make the vaccine ineffective. If the prevailing situation continues, then many savings DiSustaining savings groupsgroups might dissolve altogether. This would significantly reduce access to finance for members through both informal and formal channels. How then should savings groups cope with the “new normal”, overcome the economic shocks, and build resilience against similar future pandemics? And what immediate interventions can financial institutions implement to support the savings groups sustainably?

The digitization of financial services for savings group is one answer to such questions that can provide a critical lever for business continuity, convenience, and access to financial services. Below we highlight key recommendations for financial institutions to support savings groups to overcome the economic shocks and build resilience against similar future pandemics.

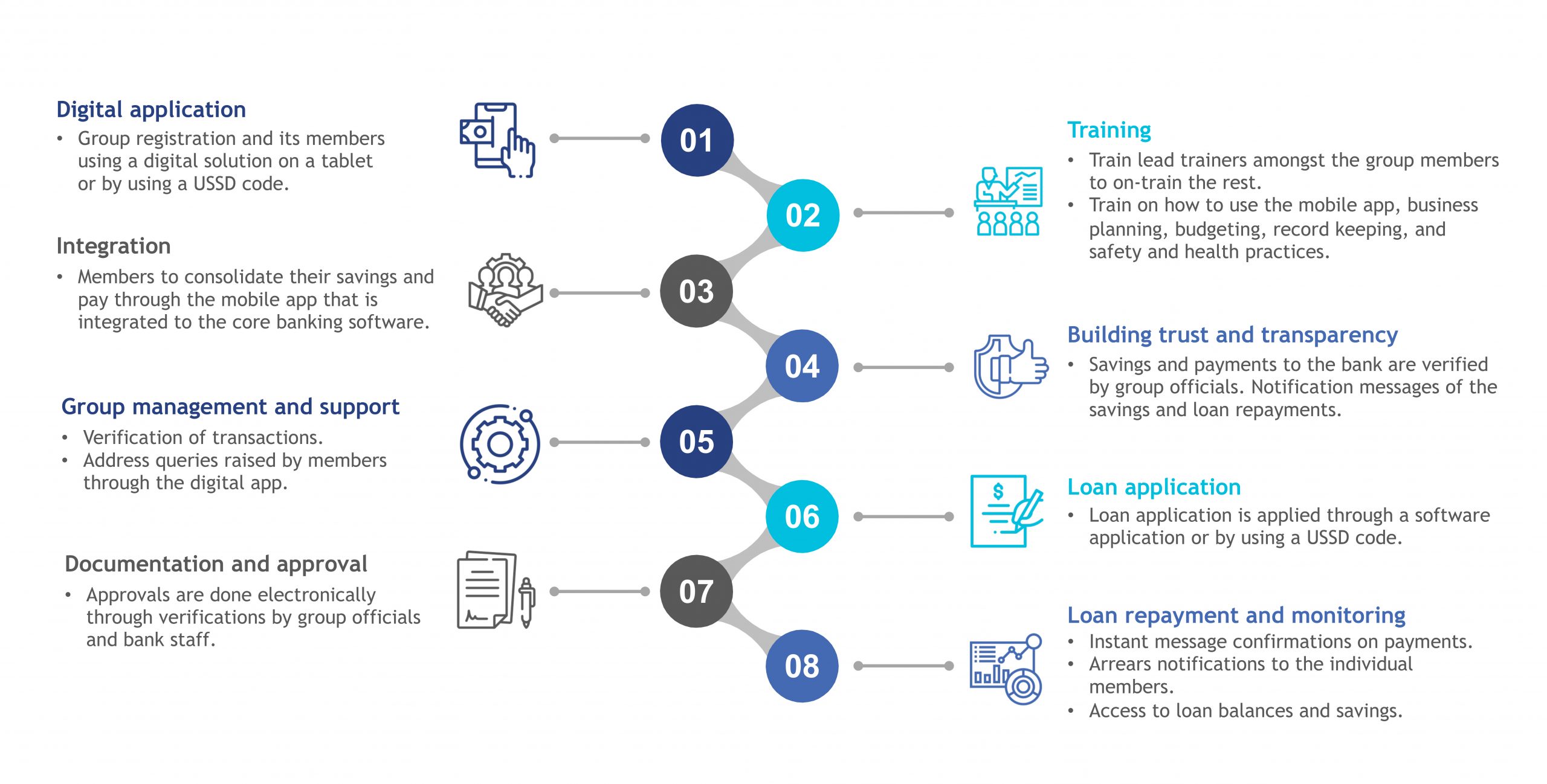

Financial institutions may revive savings group operation through digitization to include group formation, registration, training, loan processing, loan repayment, and monitoring. Figure 1 below demonstrates the steps to follow.

Figure 1. Steps in digitizing the operations of savings groups

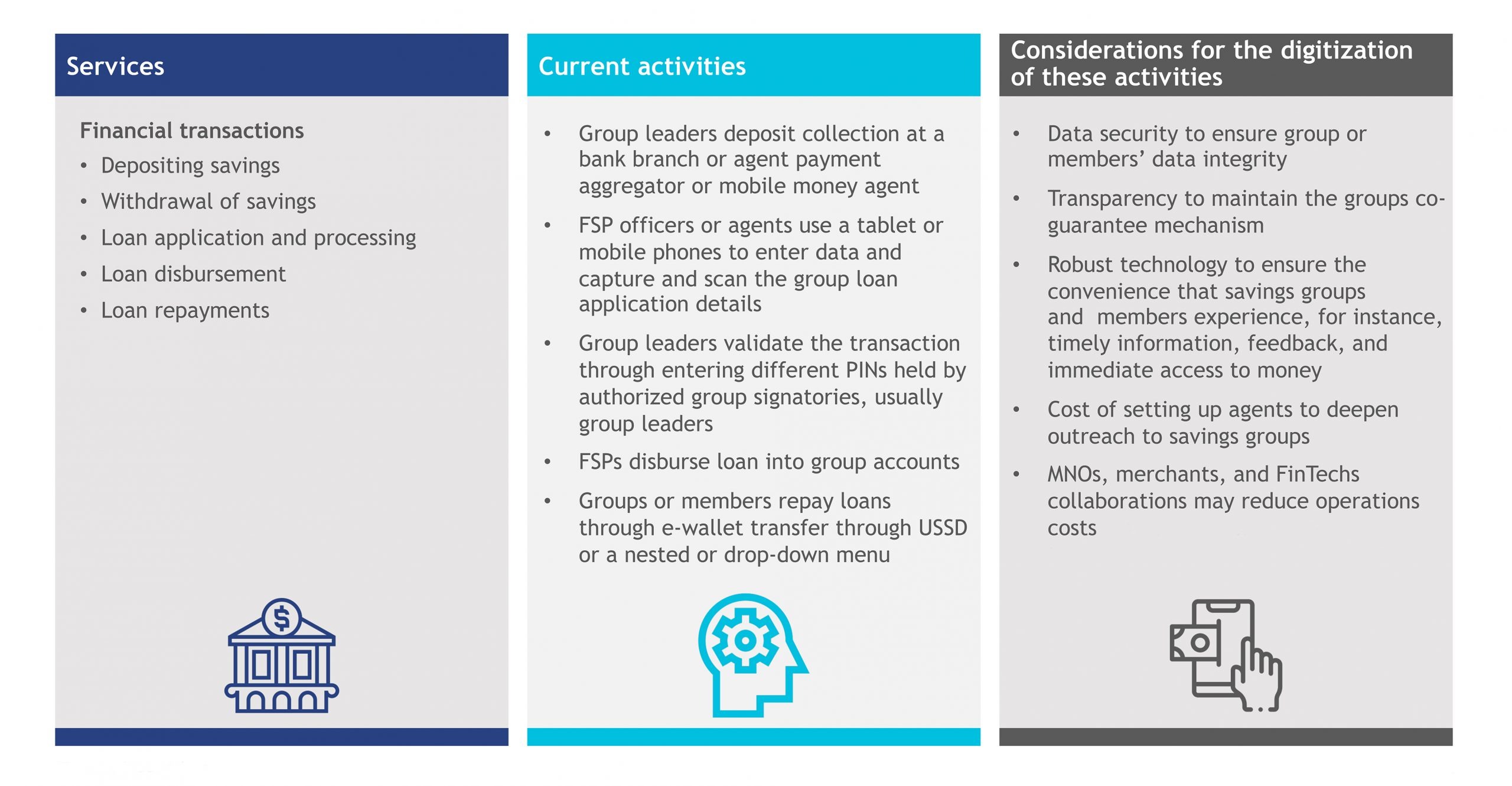

We also note that while digitizing, financial institutions should focus on financial transactions to promote trust, transparency, convenience, and efficiency. Below is an illustration of the current activities by SGs with financial institutions and the considerations for digitization.

Financial institutions could develop customer-centric financial products beyond the “vanilla” savings and credit offerings. The new product suite may include insurance, on-tap credit, insurance, and pension, among other services. The savings groups should be built using approaches, such as MI4ID, which uses behavioral economics and user-centric design techniques.

Such products will ensure the continuity of savings groups , spur linkages with financial institutions, and help members to meet their needs for financial services during a pandemic and afterward.

Stakeholders must recognize that most rural areas where savings groups are largely based have limited scope to adopt digital technologies. These regions suffer from poor internet connectivity that affects most FinTech services, which need 3G or better connectivity to function properly. People in these rural regions also have limited access to and have to struggle with inadequate infrastructure such as access to electricity and a high prevalence of .

Taking these dynamics into consideration, financial institutions can explore different approaches to training and capacity-building for saving groups:

Financial institutions can use mobile phones to connect with savings groups. For instance, they could undertake virtual capacity-building initiatives, such as ePaathshala by MSC[1], especially on digital financial services to replace the that is currently in use. These institutions may carefully select (those with access to device and ), train (using a training-of-trainers’ approach), and incentivize lead trainers who would in turn train the rest of the members as they transition. The digital training materials should be translated into local dialects for ease of understanding.Sustaining savings groups

Financial institutions may partner with civil society organizations to train the members and the local communities on safety and health precautions. Informative comics-based narratives can augment this training among the members.

Financial institutions may also use agent networks to serve savings groups that find it difficult to transact. Agents usually operate from locations that are served relatively well with electricity and 3G networks. So, savings groups that lack smartphones, electricity, or 3G connectivity can transact through agents, who are often located in market towns that group members visit on a weekly or fortnightly basis

As the world continues to observe the norms of social distancing, we see that the traditional approaches to managing savings groups are no longer feasible. Group members have been unable to gather to undertake training, save, and repay loans. Better management of savings groups calls for the digitization of their operations, including group formation, registration, training, savings collection, and loan disbursement and collections. Through the use of digital means, the financial institutions around the world can provide uninterrupted financial services to countless members of savings groups, not unlike Hope.

[1]ePaathshala is a platform for skill development, capacity-building, training, and certification built on innovative digital technology

The tragedy of the COVID-19 pandemic will have long-lasting implications on the global economy. Many financial institutions need to accelerate digital innovation and transformation to remain sustainable.

Olivia Obiero and Anant Tiwari, deliver a FREE virtual training on “Digital Transformation for Financial Institutions in the backdrop of COVID-19.” where they cover the following key topics through a three-hour interactive session:

• Digital transformation, importance, and relevance amid COVID-19

• Strategic choices and options for digital transformation

• Implementation of digital transformation

As landscape and context changes, the traditional financial services industry is facing an existential crisis. Other players are displacing traditional financial institutions. There is a business case for digital transformation for financial institutions and this case study from Kenya, from Equity Bank, demonstrates how digital transformation helps financial institutions increase efficiency, serve more customers, and reap greater profits.

About four years ago, Shakti Foundation for Disadvantaged Women, our partner in Bangladesh, faced multiple cases of misappropriations related to its voluntary savings product. As a result, the senior management team of Shakti decided to withdraw it. They realized the need to strengthen internal controls before offering voluntary savings products that create unpredictable flows of cash. However, the management was unclear and apprehensive about how to offer customer-centric products while managing the associated risks.

This case study charts how Shakti Foundation responded to these challenges through the conceptualization and implementation of appropriate technological interventions. It lists the interventions Shakti undertook, the critical factors behind their success, and the impact on Shakti and its customers.

The case study was developed as part of the Digital Microfinance Project funded by the MetLife Foundation. The project supports select microfinance institutions in Bangladesh to provide digital financial services, especially for savings, to their customers

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.