In the previous blog of this series, we discussed the changing nature of the financial services industry. We talked about how digital disruption has had an impact on traditional financial institutions. In this blog, we discuss how the incumbents can bring about a digital transformation to utilize the disruptive power of technology and innovation.

Traditional financial institutions need to undergo digital transformation urgently. This need is urgent because a significant number of these incumbent financial institutions face an existential crisis. Incumbent financial service providers (FSPs) need to acknowledge digital disruption, overcome institutional complacency, and embrace digital transformation if they wish to remain relevant in the rapid evolution of the financial sector.

Picture this: a typical East African traditional bank takes a month to process a working capital loan for an enterprise. On the other hand, an enterprise finance-focused FinTech disburses a customized solution to the enterprise within 24 hours in the form of an invoice discounting product, a factoring product, and an investment finance solution, among others.

Or this: In Kenya, businesses use more than a third of digital credits. This proportion is set to increase significantly as providers nurture and grow their higher value customers with good credit records, and as digitally-transformed incumbents such as Equity Bank extend their lending. These loans are processed and delivered in a matter of seconds. This is likely to leave analog incumbents serving just the lower value, harder-to-reach rural customers, and struggling to break even.

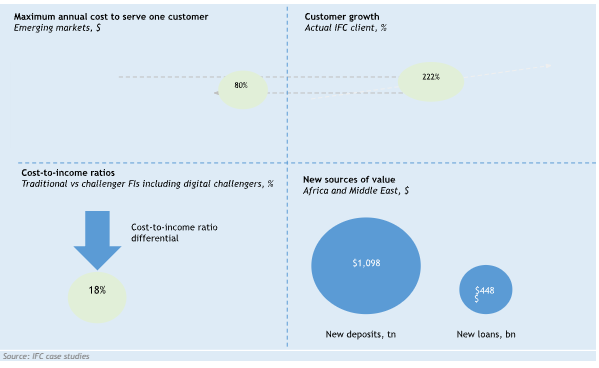

There is still a significant confusion around the business case of digital transformation. Most financial institutions think that digital transformation is a cost. It is important to realize that digital transformation is an investment to future-proof the institution. The International Finance Corporation (IFC) identifies the impact of digital transformation as 1) a reduction in the cost per customer, 2) customer growth, 3) cost-to-income differentials, and 4) new sources of value.

Digital transformation requires a strategic focus on user-centric design, alternative data analytics, personalized experience, robust technologies, and fully automated processes. Against this backdrop, a significant number of FSPs are underprepared and ill-equipped to make use of digital financial services to retain their market share.

From an institutional perspective, financial institutions need to have a clear strategy that defines their digital vision and mission. Most financial institutions end up believing that being digital means offering products through the digital channel. However, they fail to understand that being digital implies offering the right combination of: 1) digital solutions or tools, 2) digital delivery, 3) riding on digital technology, and 4) providing seamless user experience.

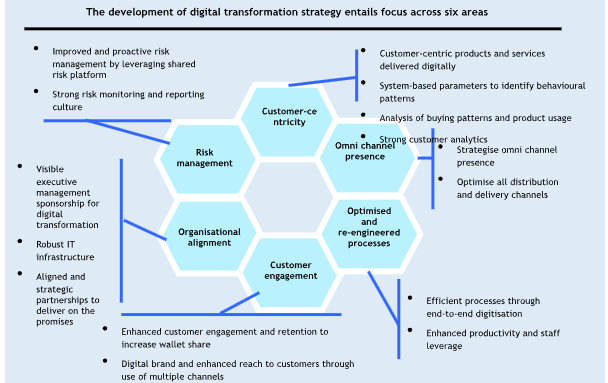

An institution’s digital transformation strategy is anchored on the use of technology to: 1) enhance its business model, 2) expand its scope to offer financial services to other segments than those it traditionally served, 3) increase its scale and outreach, 4) enhance efficiencies of operations, and 5) manage risks effectively. The key pillars of digital transformation strategy design include six areas:

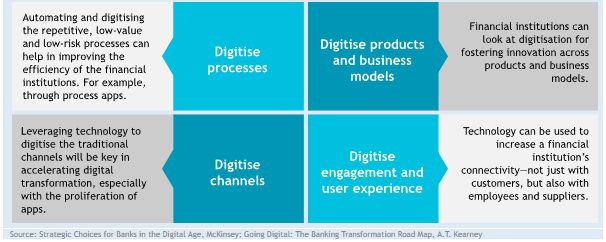

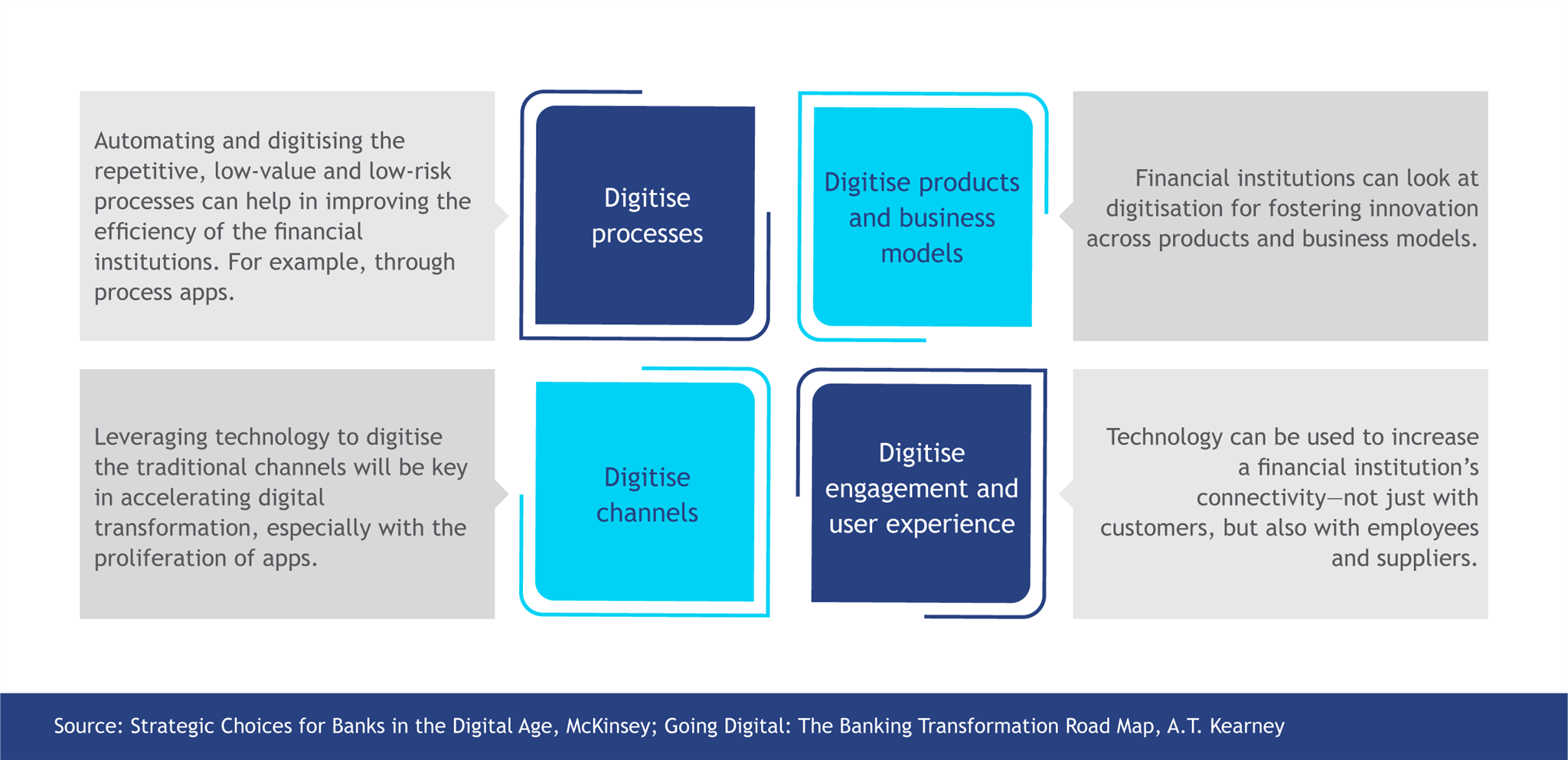

There is no formula on the steps to follow. However, to transform digitally, a financial institution may define an appropriate plan choosing from the four steps as illustrated below.

In the next blog, we explain these steps in detail along with the requirements for a digital transformation.

In the previous blog, we discussed the “why” – a business case for digital transformation. In this blog, we look at the “how” – the detailed steps for digital transformation.

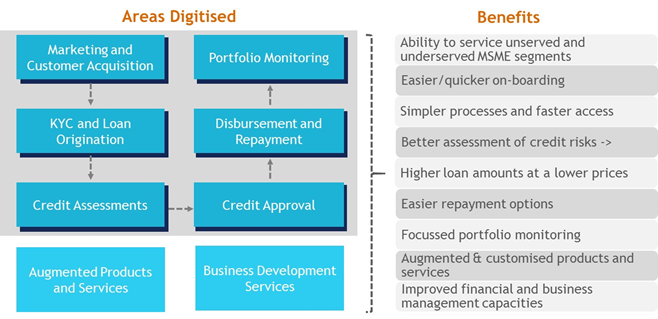

Digitise processes

Digital processes are quicker, more efficient and cheaper than manual processes. A digital transformation of processes reduces the cost and friction points of delivering service. It provides the data needed to supply a better service offering to end-users and, increasingly, to businesses. Improvements in efficiency made possible by digitisation can also help reduce the cost of sale for most products, thus providing opportunities for more competitive pricing.

The digitally-enabled processes improve:

Marketing and onboarding through lead generation and e-KYC;

Credit-scoring models through integration with the MIS, Credit Reference Bureau (CRB) checks, alternative data analytics, financial analysis, and loan utilisation checks;

Turnaround time for loan disbursement, loan collections, and delinquency management;

Internal controls and risk management through risk mapping, control breach alerts, and authentication;

Client relationship management through client engagement and retention, targeted customer service, complaints and redressal, account opening, information, personal financial management, and financial education;

Workflow management through documentation and filing, responsibility sharing, e-approvals, schedules and reminders, and data and information flows.

This case shows how digitisation can speed up and simplify back-end processes. It also has an important role as a design feature. From pre-populated fields on forms to automating how data is captured or how loans are processed, digitisation can fundamentally reshape the design of a customer’s experience to enhance efficiency, productivity, and profitability.

Digitise products and business models

Any product innovation involves utilising technology and partnerships to introduce specialised products and services. The digitisation of products requires developing solutions that resonate with customers through addressing pain-points rather than digitising use-cases. There are significant opportunities for product-level innovation as the existing products are not adequate; so, clients are forced to take up semi-formal and informal products. They seek to derive additional value from their financial service providers (FSPs), and in many cases, are willing to pay.

Financial institutions may benefit from utilising existing digital data trails and ecosystem players to deliver new products and services to clients. This brings in opportunities to enhance the capabilities of clients as a way of innovative services bundled with the products offered. The digitisation of products clubbed with an analysis of behavioural patterns may lead to hyper-customisation of products to meet the specific needs of clients.

Digitise channels

The digitisation of channels involves using technology platforms to improve customer acquisition and user experience while transacting. The emergence of digital platforms and alternative channels has profoundly changed the way customers do their banking. Only a few customers are willing to step into a bank branch. The more access points they have, the better the user experience.

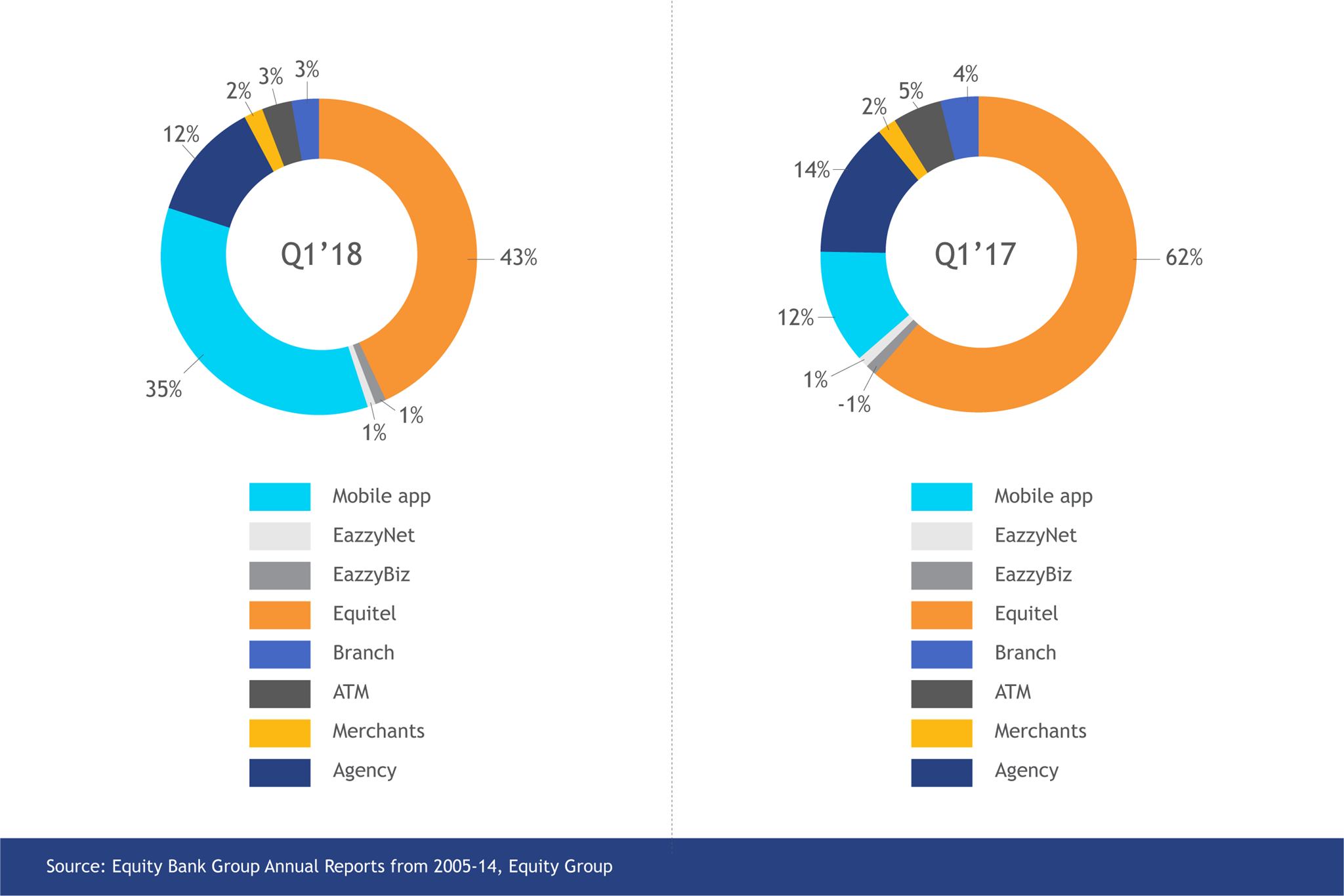

As just a single traditional channel does not resonate with the new breed of customers, there is a need to shift to an omnichannel presence where customers can interact with a myriad of distribution and delivery channels. They prefer self-service technology platforms that give them freedom, choice, and control. In 2018, the Equity Bank Kenya customers carried out 97% of their transactions outside the bank branches, as shown in the graph below.

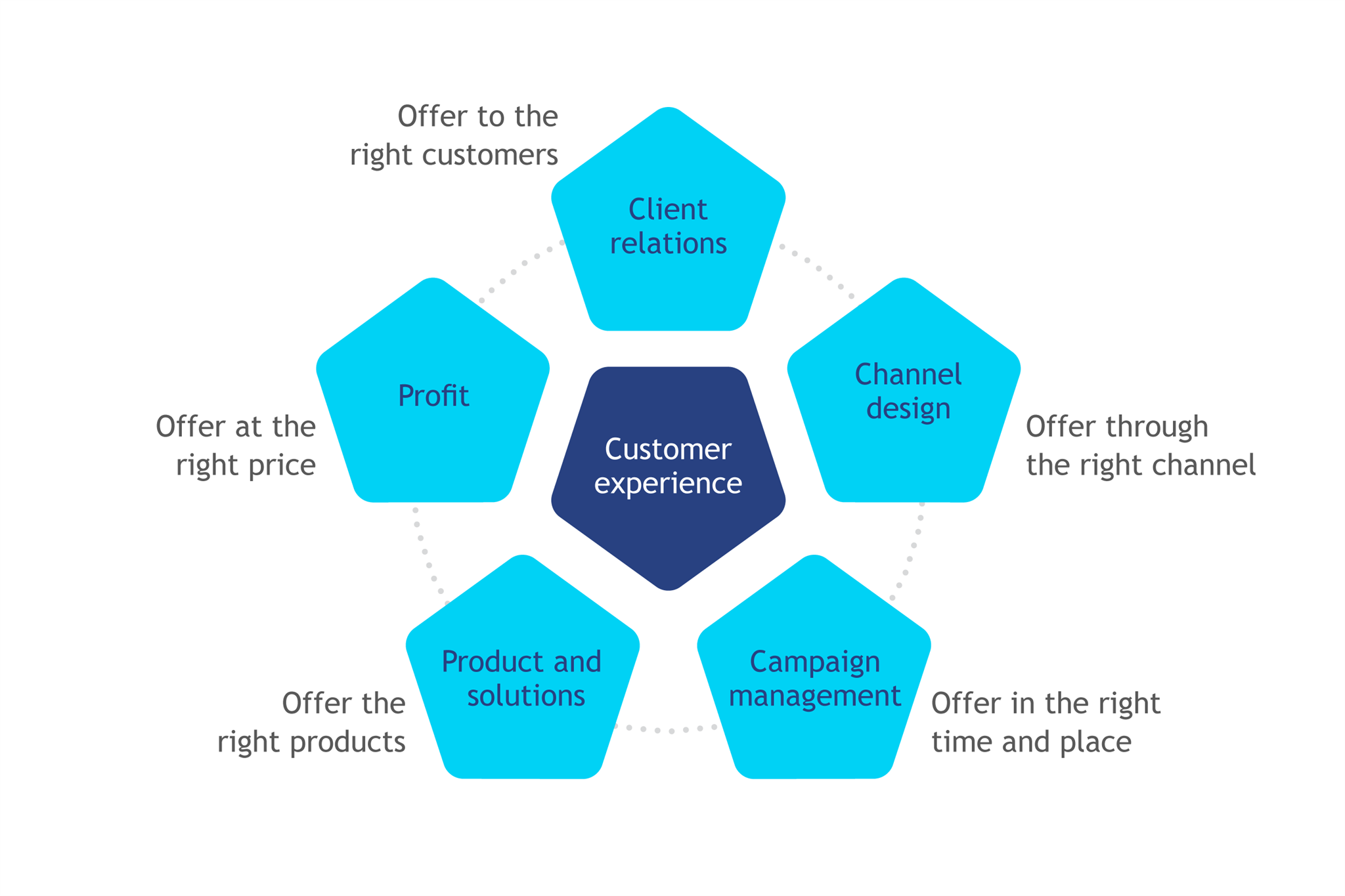

Digitise engagement and user experience

An effective digital transformation delivers a great customer experience that includes the following:

A great user experience involves solutions and the manner of their delivery that mimic the behaviours and attitudes of users. The provision of services is clear, obvious and intuitive for the end-users. To build a customer-centric solution, focus on user experience, assess the users’ bottlenecks, incorporate the customer journey approach, embed the progressive learning curve of the users, implement design thinking, and personalise the user experience.

In addition, addressing people dynamics among the staff is fundamental if the financial institution has to make technology work. This can be done by forging inclusive digital teams within the institutions. A mindset transformation to “think digital” will take shape when combined with skills, structure, incentives, and performance management. This involves creating a competency centre that drives the whole institution to talk and walk the digital transformation agenda. Transforming institutions will equip the executive management with an expertise in technology, championing the initiatives. Meanwhile, change management will clearly paint the new digital reality to the employees and secure their buy-in. This will include managing their expectations of how they spend their time and how they work alongside the new technologies along with some clarity on what technology competencies they need to develop.

Conclusion

In most cases, digitisation has an impact on the traditional financial services business model radically. Institutions that make large-scale investments required to transform digitally benefit from: 1) enhanced competitive advantage through new products, better service and competitive pricing, 2) increased revenue from new products, distinctive digital sales and using data to cross-sell, 3) lower operational costs from automation or digitisation and transaction migration, and 4) increased outreach and improved portfolio quality.

As we close the discussion, we will also like to dispel five myths about digital transformation.

Digital transformation solves all organisational problems: Digital transformation is not a silver bullet. It helps in enhancing the efficacy of processes and systems. However, it may not be a solution to operational challenges and issues faced by an organisation. If existing products, processes, systems and models did not work previously, just digitising them will not solve these problems.

Digital transformation is “cool”. Every other organisation is transforming; so we should also do so: Do not transform an organisation just because every other institution is doing so and it is “trendy” to transform. Unless there is a clearly defined business case, digital transformation is not worthwhile.

Every process, product, system, and business model needs to be digitised: It is important to remember that not everything can be and should be digitised. Every business has subtle nuances that are inherent to the business model and requires human intervention. Indeed, there is a growing body of evidence highlighting the importance of blending human touch with technology to serve the mass market effectively.

Technology for digital transformation should be disruptive and cutting-edge: As an organisation transforms, it is important to decide on the technology not based on how disruptive it is, but based on how useful and effective it is to the organisation.

Digital transformation yields results immediately: Realising the benefits of digital transformation takes time. It is an expensive, time-consuming, inexact and painful process. Transforming organisations need to recognise that cultural shifts and change require proactive management.

To make digital transformation work for your institution and for your end-customer, a clear strategy of starting with one option or combining many options to achieve scale and improve reach to the underserved populations is a must. The end goal is for a financial institution to meet the need while leveraging technology. Indeed, winter is coming. So, are financial institutions prepared for the digital onslaught?

Digital small and medium enterprise (SME) lending offers enormous potential to revolutionise access to credit for small businesses, which form the backbone of so many economies across the globe. With the digitisation of processes, SME businesses can be on-boarded, assessed, and receive a loan within 48 hours. Furthermore, since SME businesses leave much deeper digital footprints than most individuals who take personal consumer loans, this data can indeed to facilitate informed lending decisions. SME loans are typically large enough to allow some form of direct involvement of a loan officer with the borrower, which significantly enhances the chances of the loan being repaid.

Access to small amounts of credit with a few keystrokes can be immensely important and valuable for people facing short-term cash-flow problems or emergencies. This is why digital consumer credit meets an important demand – as the enormous uptake of such products in East Africa has demonstrated. Yet it does carry considerable risks for consumers and the industry as a whole. This blog focuses on digital consumer credit.

Consumer credit has a startling array of similarities to old-style microcredit – and seems set to have to re-learn the same lessons all over again.

Microcredit

Digital consumer credit

Insufficient or no emphasis on savings

Savings services are only available in a limited number of institutions

Savings services, if available, typically only find use in the assessment of credit risk or loan size. Ironically, many providers offer a good range of savings services as part of their digital credit offering, but these are rarely promoted.

Loan amounts are too small to be useful

Most initial loans fall into this category – and so are often used for “non-productive” purposes like settling expensive debts, buying medicine, or sending children to school. Yet thereafter, the subsequent size of loans is typically adequate to finance a very small enterprise.

Most loans offered are too small for enterprise. They are at best suited for basic daily trading activities under which people buy goods at the wholesale market in the morning and sell them during the day. Many such loans are too small to be useful even for health and education expenses. There is increasing evidence that individuals may use such loans for gambling.

Borrowing from multiple sources to get a useful sum

As a result of the small size of loans – this “patching” of loans behaviour is common.

Reliance on repayment behaviour to assess credit risk

Two key risk management systems of microcredit comprise group guarantee and repayment history. Based on these, the institutions offer larger follow-on loans to borrowers.

All consumer credit providers depend above all on credit history, including those based on smartphone apps – see How Smart are Smartphone Lending Apps in Kenya? These providers manage risk by initially lending minuscule amounts and then slowly increasing loan sizes based on the borrowers’ repayment behaviour.

High drop-outs in initial loans

Default on the first loan cycle is not as high because of group guarantee but drop-out after the first loan is common. This is because borrowers discover that the weekly instalments associated with microcredit are stressful.

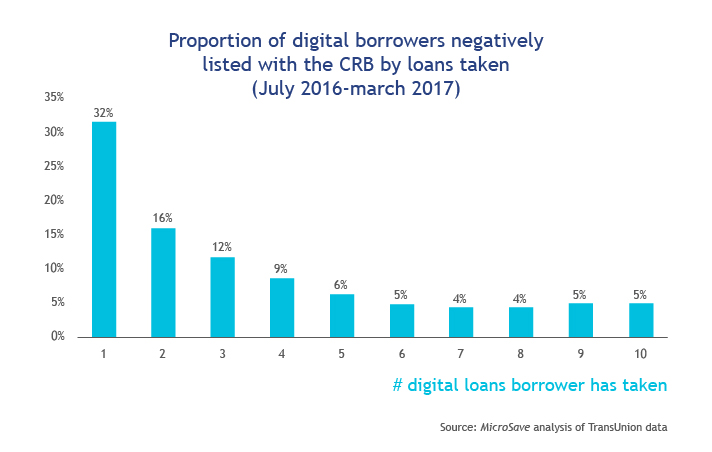

MicroSave analysis has shown that 32% of first loan cycle and 16% second loan cycle borrowers default – small wonder that the interest rates are so high to cover this risk! These defaulting borrowers are then excluded from accessing another loan. In Kenya, for instance, more than 10% of the adult population are now negatively listed on the credit reference bureau.

One loan used to settle another

This is increasingly common in oversaturated markets but particularly problematic when markets move rapidly from a total lack of credit to very easy access to credit. For example, in the case of Andhra Pradesh in India.

Most efficient microcredit institutions keep their PARs below 5%.

Our analysis shows that digital consumer credit providers lose around 50% (yes, fifty per cent) of the money they lend. Yet they write these loans off quickly to report low NPL/ PAR rates.

Furthermore, this is not the first time that we have seen consumer lenders try to address the low-income market. In the late 1990s, several domestic and foreign consumer lending companies entered the Bolivian microfinance industry. At the time, it was perhaps the best served and one of the best-performing markets in the world. The highly efficient MFI sector in Bolivia had achieved close to 50% penetration.

Consumer lenders in the country rapidly gained market share by offering quick disbursement loans to salaried employees, as well as to anyone who had earned a good credit score based on their previous or existing relationship with an MFI. The ensuing competition resulted in multiple borrowing, over-indebtedness, and ultimately created a crisis that included a debtors’ revolt. The crisis forced the industry to reschedule or write off massive amounts of debt.

At one point, non-performing loans amounted to more than 20% for some of the lenders. The foreign consumer lenders soon exited the market, leaving it in ruins. It took years for the rest of the industry to recover. See Elizabeth Rhyne’s Crisis in Bolivian Microfinance for a great overview of this.

Microcredit is no panacea but …

For all its faults, microcredit was founded with a clear social purpose to alleviate poverty by nurturing enterprise. Although the idea that microcredit is used exclusively for enterprise is, of course, a marketing myth. Microcredit has been held to account on disclosure and transparency, primarily through MIX Market and investors. It has usually been financed, and held to some account, by donor agencies and social investors who look for financially sustainable developmental impact.

Microfinance has received support from a range of not-for-profit agencies. These agencies seek to safeguard the clients’ interests, for instance, the SMART Campaign. The agencies also seek to monitor or support the social performance of providers, for instance, the Social Performance Task Force. While there is some discussion of the efficacy of these agencies, many providers and their funders regard them to have a legitimate place in the discourse.

Even today, delinquency rates are appalling, particularly in the early loan cycles (see graph below). However, few providers seem willing to innovate or even deviate significantly from the base M-Shwari model, which rolled out more than five years ago in Kenya. Currently, providers still largely deal with credit risk by raising interest rates. So, for instance, in Uganda, the MTN/Commercial Bank of Africa MoKash product costs 9% per month. This is in contrast to the 7.5% charged for the same product (M-Shwari) in Kenya, where there is a credit reference bureau and, arguably, a better credit culture.

Providers who subscribe to the GSMA’s Code of Conduct formalise their commitment to eight principles that underpin three key areas of importance:

i. Soundness of services;

ii. Security of the mobile network and channel;

iii. Fair treatment of customers

This is an excellent step forward, but there seems little application of the third principle of “fair treatment” to customers of digital credit. These customers are subjected to aggressive push-marketing and have to wade through hard-to-access, complex terms and conditions. These factors drive high levels of delinquency and thus result in high, risk-priced interest rates.

A two-pronged approach is required to address these challenges:

Regulators often pay inadequate attention to this industry because it is of low value and thus does not present a systemic risk. However, the volume or the number of people affected by poor – and indeed often predatory – provider practices, is high. Therefore, there are some the steps they need to take:

Establish robust credit reference bureaux;

Require automated data submission systems to ensure consistency of loan or repayment data reported to credit reference bureaux;

Mandate off-shore, app-based lenders to report to credit reference bureaux;

Customise credit ratings basis amount and number of days overdue;

Institutionalise mechanisms for customers to check and correct credit history;

Provide strong guidance or enforcement on drafting and communicating clear and customer-focused terms & conditions; and

Limit or ban aggressive push marketing over SMS.

Providers

Provide clarity on terms & conditions – even for feature phone users. This has been proven to reduce delinquency by nearly a third.

Re-engineer products to include:

i. Overdrafts – to meet the needs of day-traders and those who require loans for terms shorter than a month. Currently, more than a third of borrowers repay their month-long loans within a week of taking them … but receive no interest rebate.

ii. Higher amounts, longer repayment terms and reduced interest rates that reflect good credit history built over time – so that providers stop placing the burden of the massive delinquency in the early loan cycles onto those that repay on time every time.

iii. Behavioural nudges to minimise imprudent borrowing used to finance gambling, drinking, and even pornography.

iv. Increased human touch (particularly for larger loans) – to respond to the clearly expressed need for human interaction when deciding on whether to buy a product, when there is a problem, or when customer grievances need resolution.

The potential to harness digital footprints and channels to provide rapid access to credit cannot, and should not, be denied. But it will take concerted efforts to optimise the products currently being delivered and realise the full potential of the digital revolution for consumers and providers alike.

Disclaimer – Martin Holtmann is Manager – Digital Finance and Microfinance for the IFC. The opinions expressed in this blog are his alone.

But how has this service really affected the lives of customers? This article explores the customer experience (CX) around the introduction of mobile money repayments and what this means for SAJIDA’s business going forward.

On 26th March 2012, National Payment Corporation of India (NPCI) launched Rupay – India’s own payment gateway network. ‘RuPay’ is a low-cost alternative to other payment gateways, such as MasterCard and VISA. Banks pay lower transaction processing fees as transactions are performed on the domestic payment network. This makes RuPay a viable digital payment solution for the rural, low, and middle-income segments in India. RuPay offers various benefits to its cardholders, such as cash-back on utility bills and ticket bookings, in-built accidental insurance cover, and online payments across e-commerce portals.

NPCI has established a domestic payment gateway to turn RuPay into a fully functional card. The payment gateway, ‘RuPay PaySecure’, has been promoted as a solution for various e-commerce portals in India. The gateway aims to nudge domestic consumers to make digital payments. The government provided important support to the RuPay card by bundling it with Basic Savings Bank Deposit Accounts (BSBDAs) opened under the national financial inclusion programme Pradhan Mantri Jan Dhan Yojana (PMJDY).

About 586 banks including commercial banks, regional rural banks (RRBs), and cooperative banks offer RuPay cards. A paper by JM Financial Research, 2016, titled “RuPay – Driving card penetration in India”, shows that RuPay cards had a market share of 38% or 247 million of the total 645 million debit cards in India. As of 20th June, 2018 there are 318.3 million

1Jan Dhan accounts, out of which 239.9 million account holders have received RuPay cards. Although 75% of PMJDY account holders have received RuPay cards, only 42.2% of these are active.

The key findings indicate that there are operational challenges around the process to issue and distribute RuPay cards and PINs. The challenges on both the supply and demand-sides are explained below.

Challenges on the demand-side:

Low awareness among customers:

Customers are unaware that:

They are eligible to apply for a RuPay card in the first place; this lack of awareness thus reduces penetration of RuPay cards;

The RuPay card PIN becomes invalid after 45 days4 if the card is not used within this period after initial activation;

A RuPay debit card comes with an in-built accidental cover of INR 100,000 (1424.8 USD)5 . However, to keep the insurance cover in-force, the cardholder needs to carry out at least one transaction every 45 days.6 Customers are largely unaware of this add-on benefit and the associated conditions – thus also reducing the potential use of RuPay cards.

Accessibility of card collection points:

In many cases, rural customers do not collect their RuPay cards due to the long distances they have to travel to reach the bank branch, and because of lack of acceptance infrastructure in the villages (see next point);

Those that do collect their cards find that there are no ATMs or stores with point of sales devices in the villages available to conduct transactions.

Technical know-how on usage

Illiterate customers are not comfortable with using cards themselves at an ATM. They tend to seek help from others and often share the PIN, which may lead to fraud. Hence, they are reluctant to use their card.

Challenges on the supply-side:

Non-distribution of RuPay cards or PINs by BMs:

BMs do not receive RuPay card or PINs within stipulated 7-8 working days from the bank branch to which they are linked.

BMs are unable to inform customers to collect their RuPay cards or PINs. Their phone is either switched off, not reachable or is invalid.

Bank branches discourage applications for RuPay cards

Some bank branch managers are reluctant to encourage applications for RuPay cards as they fear that cards held by illiterate customers may lead to fraud.

Delay in issue and distribution of RuPay cards or PINs by banks:

The bank’s district head office either fails to issue or dispatch the RuPay cards or PINs to the linked bank branch within 7-8 working days8. As a result, the linked bank branches and BMs are unable to provide RuPay cards or PINs to customers in time.

Most of the challenges on the supply-side are because of operational issues, and those on the demand-side are largely due to low awareness levels of customers. The following interventions may help to improve activation and use of RuPay cards:

Banks should provide a list of inactive RuPay cards to their BMs. With some training and incentives, BMs may be able to push activation and usage.

Improving access to transaction points is crucial for RuPay card activation. Banks can install at least one ATM at every bank branch. Banks can also increase the number of BMs, equipped with Aadhaar and RuPay-enabled micro ATMs, in villages and marketplaces. This could encourage customers to conduct transactions using RuPay cards.

Banks could collaborate with district authorities, urban local bodies, and NGOs to organise periodic financial literacy camps. BMs may use these camps to distribute RuPay cards and simultaneously educate cardholders on how to conduct smooth and safe transactions.

1 https://www.pmjdy.gov.in/home

2 Figure 1: Referring to “RuPay cards issued (in percentage)”

3 https://www.pmjdy.gov.in/flc/Home.aspx, status as on 7th June, 2018

4 Refer to FAQ 19, 4th bullet point

5 Conversion based on 17th August, 2018. Time – 17:30 from site www.unitconverts.net

6 NPCI circular dated on 31st March, 2015. Refer to 1st point of terms and conditions

7 A standard procedure followed by the bank, refer to FAQ; Question Number: 19.

8 A standard process conducted by banks, refer to FAQ; Question Number: 19.

UNHCR Zambia had been providing cash assistance to refugees in the Meheba Refugee settlement camp. MSC was engaged to design and test the digitization of cash payments under a project that designed and implemented the digitization of UNHCR’s cash-based interventions (CBI) in the camp. At the time of writing, UNHCR would be replicating lessons from the project in other sites.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.