MSC can play synergic role in DBT space. MSC brought significance expertise on financial inclusion and on ground experience gained from assessment of various government schemes and interventions. They helped us in making our study more strong and rich in quality.

Blog

Learning from (and about) India´s Emerging Digital Money Grid

The Government of India has embarked on a remarkable path to connect all its citizens onto a digital platform through which they can, in real-time, confirm their identity, financially transact with anyone else, and store relevant documentation in natively digital format and consent to it being shared digitally with others (for instance, to support credit applications). It presents an opportunity to close the financial inclusion divide in a country that until recently held the largest number of unbanked people in the world. This is linked to a broader e-Government agenda, which has the potential for bringing an unprecedented level of efficiency and transparency into the delivery of a whole range of public and social welfare services.

The Government of India has embarked on a remarkable path to connect all its citizens onto a digital platform through which they can, in real-time, confirm their identity, financially transact with anyone else, and store relevant documentation in natively digital format and consent to it being shared digitally with others (for instance, to support credit applications). It presents an opportunity to close the financial inclusion divide in a country that until recently held the largest number of unbanked people in the world. This is linked to a broader e-Government agenda, which has the potential for bringing an unprecedented level of efficiency and transparency into the delivery of a whole range of public and social welfare services.

What makes the Indian experience so remarkable is that it is such a fundamental departure from what had become the canonical mobile money model in developing countries: that of a powerful domestic player building the ecosystem from scratch, controlling it end-to-end, and harnessing (and fully capturing the benefits of) the consequent network effects.

The Indian authorities have been clear from the beginning that they wanted to prevent the development of a dominated market, so they have based their approach on two key concepts: promotion of interoperability at all levels of the value chain, and provision of certain technical standards and public good service elements by public entities. The ultimate intent is to create a ubiquitous, low-cost network, and that requires focusing on leveraging market-level (rather than provider-specific) scale and network effects.

It´s hard to dispute the Indian motivations, but there are some practical questions that arise:

- In such an interoperable model, where every player can potentially benefit from the actions of other players, will there be sufficient incentives for the deployment of an effective cash in/cash out network – which remains the toughest nut to crack in any digital money network?

- As entities linked to government take on the role of delivering more and more component elements of the digital financial services value chain (e.g. UIDAI, NPCI, CCA, NeGD), what is the right governance model under which they should operate, to ensure that they remain focused on the public interest and not just in promoting their own organizational agendas?

- As the central bank paves the way for much needed new institutional formats and license categories (e.g. prepaid instrument providers, white-label ATM providers, payment banks, small finance banks, etc.), the opportunities for regulatory arbitrage will increase and market access rules may come to seem increasingly arbitrary. As the competitive environment becomes complex, will the authorities be able to keep on top of market practices and ensure that the regulatory framework remains pro-competitive?

- As more of people´s data is digitized, there will inevitably be strong commercial pressures for people to share more and more data in order to be able to access advanced digital services. Beyond the usual privacy protection concerns, how can we place limits on how much data customers have to give up as the price of digital inclusion?

- A number of government initiatives are now starting to show results, just when political support is highest, but providers are often lagging behind for a lack of a clear business case. Is the market near an inflection point, and if not, how will we know when it is approaching it? What will it take for market players to take fuller advantage of the new digital finance public goods? What more can government do to push them?

We think that all digital finance professionals would do well to learn about the Indian experience, and use that to challenge their own thinking about digital financial inclusion models. With this purpose in mind, the Digital Frontiers Institute, of which I am an Executive Director with colleagues David Porteous and Gavin Krugel, has collaborated with MicroSave to create a four-week online course on the Indian journey, which we call Digital Money Grid India, and which we will offer in its first edition starting on March 27th.

The course is intended for professionals in digital money or digital financial services wanting to develop a fuller understanding of the emerging landscape for digital payments and financial inclusion in India. The intended audience includes professionals in India who expect to apply the understanding gained through the course directly in their market, as well as those outside India who want to understand and learn from the Indian model and experience

Agents Count: The True Size of Agent Networks in Leading Digital Finance Countries

This paper lays out a framework for understanding agent network size for digital financial services, drawing a distinction between agent tills and agent outlets. The paper also discusses agent activity rates.

We argue that the number of active agent outlets represents a more appropriate measure of access to finance than agent till statistics, which are usually used by regulators and the industry.

We then propose a simple methodology for calculating active agent outlets in five leading digital finance markets: Bangladesh, Kenya, Pakistan, Tanzania and Uganda. The total number of agent outlets in these countries is roughly half that of agent tills, while active agent outlets amount to just a quarter.

These findings suggest that the use of agent till statistics has led to an overestimation of global access to finance. We also compare the number of active outlets to adult population, customer and agency business data to propose industry benchmarks for the number of agents and customer-to-agent ratios that providers may target. To read through the report, please click here.

Successful Agent Networks

There is no universal definition of a ‘successful’ agent network. Agent networks are a means to an end: providers use them to advance the objectives of their digital financial services (DFS) deployments. There are many different types of deployments, with many different objectives – from upselling mobile network operator’s (MNO) customers on DFS, to decongesting bank branches or building a brand profile. But there is a best-fit agent network for any given deployment. Starting with a clear value proposition and a well-informed understanding of the competition, a DFS provider can build an agent network that drives forward their objectives; objectives that have the right agents in the right places with the right support to build and serve a loyal customer base. In short, there are many types of success. This paper sets out The Helix Institute of Digital Finance system for analysing success in this complex context: a flexible approach allowing agent network managers and researchers alike to measure six dimensions of agent network success, and to categorise agent networks so that we can make fair comparisons between similar deployments. To read through the report, please click here.

Accelerating Financial Inclusion in South-East Asia with Digital Finance

Digital finance presents a potentially transformational opportunity to advance financial inclusion. In this report commissioned by the Asian Development Bank, the role that digital finance can play in accelerating financial inclusion, focusing on four Southeast Asian markets – Indonesia, the Philippines, Cambodia, and Myanmar is discussed.

From OTC to Mobile Accounts: Easypaisa’s Journey

In 2009, Pakistan spearheaded the over the counter (OTC) transaction revolution. But in the summer of 2017, the digital financial services (DFS) landscape may experience a watershed moment. In June 2016, the State Bank of Pakistan (SBP) announced that as of July 2017, all branchless banking players offering OTC transactions will be required to use biometric verification to send and receive funds. Currently, customers transacting using OTC only need a copy of their Computerised National Identity Card (CNIC) to send and receive payments. This regulation will have major implications for DFS providers in terms of their investments and system developments, as well as the need to educate customers and agents.

In 2009, Pakistan spearheaded the over the counter (OTC) transaction revolution. But in the summer of 2017, the digital financial services (DFS) landscape may experience a watershed moment. In June 2016, the State Bank of Pakistan (SBP) announced that as of July 2017, all branchless banking players offering OTC transactions will be required to use biometric verification to send and receive funds. Currently, customers transacting using OTC only need a copy of their Computerised National Identity Card (CNIC) to send and receive payments. This regulation will have major implications for DFS providers in terms of their investments and system developments, as well as the need to educate customers and agents.

While leading players like Easypaisa, a mobile money service from Telenor Pakistan and Tameer Micro Finance Bank, have focused on converting their OTC customers to mobile account holders for the last two years, the proposed regulation puts pressure on them to migrate the majority of their 16.2 million OTC customers to the mobile account. This is not an easy task. Nevertheless, in this blog we focus on the strategies that have helped Easypaisa gain impressive numbers in mobile accounts, often overshadowed by OTC usage, and provide lessons to Pakistani DFS providers hoping to do the same.

OTC Growth Rate Is Actually Decreasing

The global annualised growth rate for the number of unregistered mobile money users who transacted using OTC was 22% in 2015, compared to 33% in 2014 and 102% in 2013. In South Asia, the 19% growth (year-on-year) of OTC in 2015 was surpassed by the 47% growth in registered mobile accounts. Easypaisa experienced 194% growth in mobile accounts versus 35% growth in OTC customers during this time period.In fact, the ratio of mobile account to OTC transactions has been increasing every quarter since 2014 for Easypaisa, as demonstrated by Table 1, reaching 77% in Q4 2015. This decrease in the OTC growth rate is also reflected in the country at large — mobile accounts grew by 183% between Q4 2014 and Q4 2015. By December 2015, Easypaisa had 9.8 million registered mobile accounts—64% of the total mobile accounts in Pakistan.

Part of this growth is due to the nation’s successful GSM biometric verification drive, where all the telecoms together successfully authenticated 68.7 million SIMs within 90 days in 2015. Easypaisa leveraged this verification drive by enabling its biometrically verified GSM customers to also simultaneously open mobile accounts, thus increasing their registration rate.

Additionally, the decrease in the OTC growth rate may be attributed to an increase in number of DFS players in the market, who rather than investing in new agents, utilized the country’s existing agents and offer similar OTC products—such as Person-to-Person (P2P) transfers and utility bill payments—on the same channel. As a result, this has granted agents a much greater influence over customers on which provider they should transact with. This power dynamic has put a lot of pressure on providers to offer competitive commissions—known as the infamous commission’s war—to their agents in order to have them specifically sell their services and lure new customers to their network.

Are Mobile Accounts Being Used?

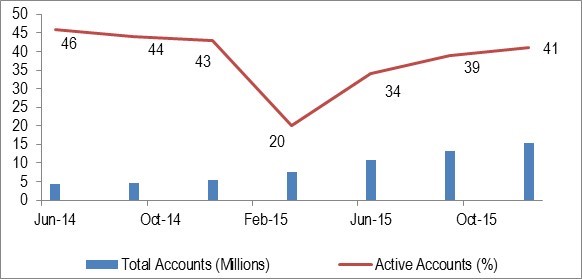

Mobile account usage is a more useful indicator of the successful conversion of OTC customers to mobile accounts. Easypaisa has aggressively pushed new products and offered pricing incentives, among other approaches in an effort to increase usage of mobile accounts. For instance, Easypaisa dropped its P2P fees for mobile account holders in September 2014. Following this change, the number of P2P transactions increased from 15,000 that month to a peak of 783,000 P2P transactions in May 2016. As demonstrated in Figure 1, Pakistan witnessed a remarkable growth in both registered and active mobile accounts in 2015, whilst concurrently offering OTC transactions. As of December 2015, Easypaisa had 26% of Pakistan’s total active accounts and expects this percentage to increase.

Figure 1. Mobile Money Accounts versus Active Accounts (Pakistan)

Source: State Bank of Pakistan, Branchless Banking Newsletters

Mobile Account Strategies: What’s Worked

One of the driving factors for Easypaisa achieving mobile account growth was the team’s commitment to this goal. Indeed, both Easypaisa and Jazzcash—Easypaisa’s competitor — committed to working together to end the OTC commission war that was decreasing both providers’ profit margins. They took this bold action to focus instead on mobile accounts, as they understood that this is where the lion’s share of opportunities in DFS lies.

Some of the successful strategies taken by Easypaisa are as follows:

- Pricing. With the prevalence of OTC transactions, Easypaisa recognised that a pricing incentive could lure customers to mobile accounts. Easypaisa then waived all cash deposit, cash withdrawal, and P2P transfer fees. While this strategy does not result in profits, it enables registered customers to get accustomed to their mobile account, while making them more likely to sign up and employ other use cases on the wallet.

- Offer compelling use cases to your target customers. First and foremost, Easypaisa had to understand their customers’ financial journey, recognising that not all segments have the same financial needs and patterns. Easypaisa conducted market research to understand customers’ needs, preferences, desires, aspirations, as well as attitudes to financial services. With this research, Easypaisa has come up with three unique customer segments and have started rolling out a diverse product suite targeted to them. These use cases aim to solve real financial pain points, and also influence customers of the value of storing money on their mobile account. These products vary from retail payments, online payments, lending, saving, and insurance products, to ATM/debit cards.

- ATL and BTL marketing campaigns. Easypaisa’s OTC marketing campaigns proved effective as ‘Easypaisa kara lo’ [‘conduct an Easypaisa’] became a euphemism for money transfers. In 2015, Easypaisa changed their strategy and started focusing on educating customers — particularly middle-income customers as they see this segment as early adopters — on the value of a mobile account, beyond money transfers to include bill and merchant payments, as demonstrated by their TV advertisements.

- An Easypaisa account is actually SIM agnostic (telco operator agnostic). A customer can have a SIM card from any service provider in Pakistan and still utilise Easypaisa’s mobile account services. This move was especially important as 60% of OTC customers do not carry Telenor SIMs, and in this approach, Easypaisa is the first DFS provider to offer their services to any telecom customer.

- The introduction of the Easypaisa Mobile App. The rapid adoption of smartphones in Pakistan — currently at 11% ownership with an ambitious projection of 40 million by the end of the year– convinced the Easypaisa team to start offering newer, more user friendly channel in addition to USSD. Easypaisa’s team developed a faster and intuitive smart phone application where users can register their mobile account. Easypaisa understands that while smartphone penetration is increasing, there is a large customer segment that relies on feature phones that they will need to target and address according to their needs.

- Interoperability with the financial ecosystem. All Pakistani banks are connected to the 1-Link switch, and in addition to facilitating ATM transactions, the Inter-Bank Funds Transfer (IBFT) services offered by the 1-Link service, allows Easypaisa mobile account users to move funds from any bank to their mobile account and vice versa. This interoperability also facilitates fund transfers between different DFS mobile accounts today.

What Does the Future Hold?

Easypaisa has always maintained that rolling out OTC transactions first was the right thing to do and they would undoubtedly do it all over again. Usage matters, and as discussed in our previous blog, OTC does not prevent product evolution and usage of mobile accounts, but can enable customers to build familiarity with DFS services through OTC first, whilst encouraging them to register for mobile accounts when there are more compelling use cases.

Easypaisa believes OTC will be around for a while given low literacy levels in Pakistan (58%), and the trust and influence an agent garners with customers, amongst other factors. While Easypaisa recognises that not all of their OTC customers will migrate to the mobile account, it takes just a few account-based transactions to influence customers. Easypaisa faces this challenge with unwavering courage. They have faith that the future of mobile accounts is in the payment space—a hugely untapped market among 180 million Pakistanis of whom only 7% are banked and rely on cash to conduct their transactions.

Omar was part of the core Mobile Financial Services team at Telenor that designed and deployed the OTC and e-Wallet businesses for Easypaisa, which was launched in 2009 as the first Mobile Money service in Pakistan. He has been involved in developing and managing the distribution channels for Easypaisa and is currently the head of Strategy and Payments.