Based on over 2200 agent interviews conducted in quarter 4 2015, the ANA Uganda report, funded by the Bill & Melinda Gates Foundation, FSDU, IFC, FSDA and the United Nations Capital Development Fund (UNCDF) highlights findings on the DFS agent landscape in Uganda covering agent profitability, transaction volumes, liquidity management and other important strategic considerations.

The research findings highlight that post the Warid-Airtel merger, the Ugandan digital finance market is split between two players. There has been a major drop in exclusivity compared to 2013, and agents now serve more providers. Agents are the most profitable among ANA East African research countries. However, the levels of agent assisted Over-The-Counter (OTC) transactions are still high for an MNO wallet market. Providers will need to develop strategies to overcome this barrier and assist customers preferring OTC in adopting wallet-based DFS products. Agents are optimistic about the business: the majority foreseeing themselves being an agent in one year’s time, yet worry about competition and unpredictable client demand. Click the download button to read the full report.

Patrick, Deputy Manager of Operations of a digital financial service provider in Zambia, was on his quarterly monitoring visit in Kafue, 60 kilometres from Lusaka, when he, yet again, encountered three new agents at different outlets in the area. High churn rates seem to be a recurring theme on his visits to different parts of Zambia, and he’s worried. He is convinced this is not good for his digital financial services (DFS) business. What can Patrick do?

The 2015 ANA Zambia Country Report highlights that three-fourths of agents in the country are operators—i.e. staff employed by owners of the mobile money business to work at their outlet. Further, qualitative research indicated that owners run multiple booths in an area. While this phenomenon indicates that owners find the mobile money business fruitful, research also finds that there is a high turnover amongst Zambian operators. This means that both service providers and owners have to train continuously and mentor a new wave of operators, only for them to leave. In turn, these operators may not be sufficiently trained, or perhaps may not be willing to invest their time and knowledge in the business. With only half of Zambians aware of the concept of mobile money, changing the ‘face’ of DFS could potentially hinder the adoption of DFS.

Operators Don’t Stick!

A large chunk of operators—90%–have been in the mobile money business for less than one year compared to 77% of owners. In fact, the operator to owner ratio of agents who have been in business for less than one year is 78:22, while for those who have been in the business for three years or longer is 48:52. This is telling that operators don’t seem to stick around for very long. Why is that?

While qualitative research can unearth operator’s motives, findings from ANA Zambia shed some light. Operators are less likely to see themselves as agents in a year from now compared to owners (55%versus 81%, respectively) as they primarily feel that the business is not profitable enough for them. This may not be very surprising given that the median monthly earning for an agent (owners only) is US $180 (PPP adjusted), which is below the national Gross National Income (GNI– US $308 PPP adjusted). This indicates that owners may not have sufficient resources to spend on salaries and in fact, operators earn much less than owners—the median salary of an operator is US$125 (PPP adjusted). As for their motivation, a little less than half of the operators indicate that their salaries are not enough to encourage them to try actively to increase the business as an agent.

How Untrained Operators Can Impact DFS Adoption

With a high percentage of operators in the market, the onus falls on both the service provider and the owner to ensure that operators are well trained on the technical aspects of delivering mobile money as well as on customer service aspects in terms of selling mobile money to customers. To do this well, training needs to take place consistently over time. While 94% of operators receive training in their first three months of service (compared to 85% of owners), more than half of them do not receive this directly from the service provider; in fact, 22% receive training from their boss or another agent (26%). This suggests that providers may not have visibility on the quality of training, how often trainings are given, and what content the training covers.

1) Converting a user—familiar with DFS brands—to regular usage of a product, and 2) Raising meaningful awareness among potential customers not familiar with DFS. It is, therefore, critical that an agent at an outlet (of which 75% are operators) are trained sufficiently, repeatedly, and of high quality, because they have the potential to motivate customers to use DFS.

ANA Zambia further found that trained agents conduct a whopping six more transactions per day than their untrained peers. Thus, the high churn amongst operators could hurt the performance of an agent and thus their income.

The Glue That Holds?

It’s not uncommon for DFS markets—such as Tanzania and Kenya—to have a high percentage of operators, and it need not be a negative trademark. An owner managing multiple outlets is a good sign of trust and optimism in the service and also enables owners to manage their liquidity better between their outlets.

So how can Zambian providers translate this optimism and trust to newly joined operators? Some quick wins could be:

Creating a compact training program for new operators

Developing a training of trainer model for owners

Setting operator recruitment criterion for owners

Testing different monetary and non-monetary incentives for operators who perform well

Nonetheless, it is necessary for providers to conduct a deep dive exercise to understand this phenomenon fully. In Zambia’s nascent market and indeed impressive comeback to DFS, providers will want to ensure their agents plant themselves deep into Zambian communities and reap trust to seed the demand of potential Zambians customers.

The provision of banking services is very vital for the long-term sustainable development of any country. In India, it has been a constant endeavor of the regulators and the policymakers to achieve financial inclusion with the objective extending financial services to the large hitherto un-served population of the country to unlock its growth potential. Our policy makers have been more keen on achieving inclusive growth by making financial services available to the masses (mainly the last mile).

RBI made a policy announcement on Financial Inclusion by Extension of Banking Services in January, 2006, allowing banking services through agents, known as Business Facilitators and Business Correspondents (BC). This was expected to accelerate the journey towards financial inclusion through digital channels to hitherto excluded segments. In September 2013, Reserve Bank of India (RBI)also set up the Committee on Comprehensive Financial Services for Small Businesses and Low Income Households, chaired by Dr. Nachiket Mor, with a task of framing a clear and detailed vision for financial inclusion and financial deepening in India. Key recommendations of this included measures for improving the viability of the BC model.

Towards achieving this august objective of financial inclusion, there have been sustained efforts by the Government of India and RBI over the past few years. Some of the initiatives undertaken by the Government and RBI are: Expansion of bank branch and ATM network in the country, increased focus on opening bank branches in rural areas, expansion of BC network, Direct Benefit Transfer (DBT) to beneficiary accounts, providing RuPay card, Pradhan Mantri Jan-Dhan Yojana (PMJDY) which includes aspects of credit and insurance and more recently the differentiated banking licenses to payment banks and small finance banks.

However, despite being operational for almost a decade, India’s BC model has been relatively unsuccessful in achieving the goal of effective financial inclusion.

This Policy Note explores some ideas and thoughts which can help the policy makers and regulators to achieve their vision of complete financial inclusion. This Note presents a few compelling out-of-the-box ideas in terms of having ubiquitous agent points, employing white label business correspondents, accepting eKYC documents, harmonising KYC documents, bringing in better liquidity management processes and coming up with effective agent training methods etc.

Of the remaining eight provisional Payments Bank licensees, four involve mobile network operators (MNOs): Airtel, Idea, Vodafone, and Reliance Jio.

This is not surprising, since successful Payments Banks will require a large footprint to serve a massive customer base, as it will be a volume game. MNOs’ existing customer base and extensive agent networks provide an important springboard to achieve and service the volumes required to break even.

MNOs have several significant advantages as Payments Banks:

They have established multi-layer distribution networks, with many thousands (in India’s case 1.5 million!) of retailers selling airtime and providing extensive urban and rural coverage.

The MNO business model is based on usage (those high volumes of small value transactions), and, therefore, more aligned to the willingness and ability of the poor masses to pay in small sums; unlike the traditional bankers’ business model that is based on float. SBI’s collaboration with Reliance Jio was, in this sense, visionary – Jio can leverage the SBI brand and ability to lend, while managing the voluminous transactions on behalf of the bank.

Mobile pre-paid platforms that manage high volumes of low-value electronic recharge are very synergistic with the needs of digital financial services. These platforms also allow the ability to offer highly customised and relevant products (supplemented with capabilities for fine segmentation and analysis of usage trends).

MNOs have high levels of brand awareness amongst poor and rural customers that can be leveraged well for cross-selling financial services. MNOs also invest regularly and extensively in marketing and promotions to create channel and consumer awareness.

Telecommunications is a well regulated service industry, similar to banking. Thus, mobile retailers acquiring new subscribers are well equipped to handle the Reserve Bank of India’s regulatory and compliance requirements of Payments Banks, as well as KYC norms and service activation processes.

Telecommunications is also an investment-intensive and long gestation business. Thus, mobile operators have the capability to source funds, and make large investments with long-time horizons for returns.

MNOs work through extensive partnerships, aggregating third-party products seamlessly into their offerings – essential for the success of digital financial services.

As we concluded in a 2013 blog, Can India Achieve Financial Inclusion without the Mobile Network Operators? “MNO-led systems therefore have a hugely important role to play to create the market – to build people’s confidence in digital financial services and local agent-based systems – and thus lay the foundation for digital financial inclusion.”

When MicroSave examined the business case for MNOs as Payments Banks several additional opportunities and issues emerged. We used MicroSave’s extensive market research on the low-income segments, plus public domain documentation of MNOs in India and elsewhere, to develop detailed projections on the likely opportunities, revenues, and costs. This allowed us to build up a detailed model to examine the business case.

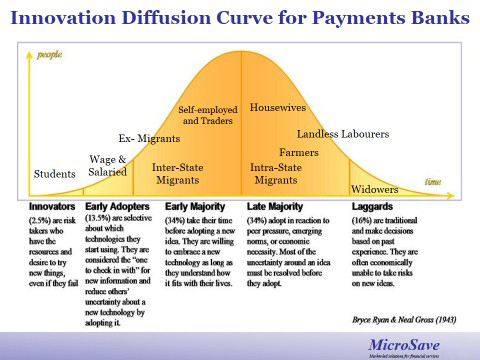

First, we examined the likely adoption patterns of key market segments (see diagram below).

On the basis of this, we mapped products for each of these segments that encompassed:

Savings and goal-based saving

Commitment/time deposits

Current accounts

B2B payments

DBT and other G2P payments

Utility and other bill payments

Airtime top-ups

Premium payments (for insurance product)

Short-distance remittances

Long-distance remittances

International remittances

Overdrafts against savings balances

Credit products: working capital, term loan and bill discounting

Credit score based loans

We then assessed the likely transactions, balances and other revenue sources from each of these by segment in order to build up a clear picture of the contribution of each and, thus, where MNOs should focus their efforts (see diagram below). Intra-state migrants, self-employed and traders, wage and salaried segment, and farmers are expected to yield the most revenue, but some of the initial work would be focused on students and inter-state migrants to drive adoption of these larger market segments. Thus, a carefully sequenced marketing campaign will be essential, and those MNOs already servicing the inter-state remittances market will have an important competitive advantage.

On the basis of our analysis, we expect around 90–95% of revenue to come from transactions, and only 5–10% from float. Of the 95%, the largest revenue source is likely to be remittances, transactions on basic savings accounts and shared interest on loans offered, backed by credit-scoring customers’ “digital footprints” (each around 20%). Other revenue sources will include G2P/direct benefit transfer payments and utility payments (around 10%). Airtime top-up is only expected to yield around 5–7% of the bank’s revenue, but would, of course, result in substantial savings for the MNO, in terms of both distribution costs and reduced customer churn.

We then examined the operational imperatives for an MNO to build a successful Payments Bank, including the IT, branding and marketing, call centre and core employee spend, as well as the costs of agent selection, on-boarding, training, monitoring and, of course, commisions. Perhaps unsurprisingly, agent commissions and distribution operational expenses were the largest costs (in the range of 40–45% and 16–20%, respectively), followed by sales and marketing and HR costs (around 10% each).

On this basis, we built a comprehensive financial modelling of the potential for a relatively modest-sized MNO to achieve financial break-even (without factoring in the value of the expected reduced customer churn). We found that, with conservative estimates, a mid-sized MNO should break even in year 5, with an ARPU of around Rs.700–800 per customer. Importantly, the Earnings Before Interest, Taxes, Depreciation and Amortisation (EBITDA) margin grows rapidly from year 5 and is estimated to be 30–35% by year 8. We estimate the total payback period will be around 8 years, and that the internal rate of return will be 12–15% in the first 10 years.

So can mobile network operators make it as Payments Banks? There is clearly a long-term business case for MNOs to open and run Payments Banks. But, as many commentators (and indeed the Reserve Bank of India) have said, it is a long-term play, requiring significant investment. This is no different for a more traditional mobile money offering like M-PESA, MTN Money or hundreds of other mobile money offerings across the globe. Indeed, as GSMA has pointed out, seriousness of intent and significant investments are required to ensure that mobile money systems flourish and yield profits. Indeed, this is the key differentiator between mobile money deployments that “sprint” and those that “limp”. But as a Payments Bank, MNOs have significantly more options to derive revenue, particularly from transactions on, and to, the savings accounts they offer – if they are able to build and maintain a robust technological infrastructure to gain the trust of the mass market.

This blog was first published in EconomicTimes on 17th August, 2016.

Targeted Public Distribution System (TPDS) is the largest social security programme in the world but has been bogged down with heavy diversion and leakages. To address diversion, the government started digitisation of PDS supply chain, ensuring subsidised grain access only to the Aadhaar authenticated beneficiaries. However, the income and revenue of Fair Price Shop owners has come down drastically as one of the outcomes of digitisation. This note highlights the importance of FPS sustainability and details options to ensure its continuity. It thus becomes imperative to cross-subsidise FPS operations to ensure service availability. The note suggests two methods to ensure FPS continuity. The first method is to deliver TPDS through social organisations such as NGOs/cooperatives/Self-Help Groups. The second method is for FPSs to sell items other than only subsidised food grains, as is currently the practice. We give examples of cooperative-run FPS networks (Chhattisgarh and Madhya Pradesh) and public-private partnership model in the form of Annapurna Bhandar Yojana in Rajasthan.

KYC harmonization study was undertaken to analyze the existing Know Your Customer (KYC) practices of first-time customer on-boarding by service providers (Banks, Mobile Network Operators, Mobile Money Operators, and Pre-paid Payment Instrument issuers) with respect to the prevailing regulatory landscape.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

Patrick, Deputy Manager of Operations of a digital financial service provider in Zambia, was on his quarterly monitoring visit in Kafue, 60 kilometres from Lusaka, when he, yet again, encountered three new agents at different outlets in the area. High churn rates seem to be a recurring theme on his visits to different parts of Zambia, and he’s worried. He is convinced this is not good for his digital financial services (DFS) business. What can Patrick do?

Patrick, Deputy Manager of Operations of a digital financial service provider in Zambia, was on his quarterly monitoring visit in Kafue, 60 kilometres from Lusaka, when he, yet again, encountered three new agents at different outlets in the area. High churn rates seem to be a recurring theme on his visits to different parts of Zambia, and he’s worried. He is convinced this is not good for his digital financial services (DFS) business. What can Patrick do?

On the basis of our analysis, we expect around 90–95% of revenue to come from transactions, and only 5–10% from float. Of the 95%, the largest revenue source is likely to be remittances, transactions on basic savings accounts and shared interest on loans offered, backed by credit-scoring customers’ “digital footprints” (each around 20%). Other revenue sources will include G2P/direct benefit transfer payments and utility payments (around 10%). Airtime top-up is only expected to yield around 5–7% of the bank’s revenue, but would, of course, result in substantial savings for the MNO, in terms of both distribution costs and reduced customer churn.

On the basis of our analysis, we expect around 90–95% of revenue to come from transactions, and only 5–10% from float. Of the 95%, the largest revenue source is likely to be remittances, transactions on basic savings accounts and shared interest on loans offered, backed by credit-scoring customers’ “digital footprints” (each around 20%). Other revenue sources will include G2P/direct benefit transfer payments and utility payments (around 10%). Airtime top-up is only expected to yield around 5–7% of the bank’s revenue, but would, of course, result in substantial savings for the MNO, in terms of both distribution costs and reduced customer churn.