The World Bank Institute highlights that behavioural change with regard to financial capability is a non-linear process and requires more than receiving compelling information. For an evolving channel like DFS, which has several models of service delivery, this brings its own set of challenges. For DFS to be used to its full potential, it is important that both customers and agents have functional knowledge of the channel.

Therefore, under MicroSave’s study for the Omidyar Network on customer protection, risk and financial capability in India, financial capability of the customers was assessed on the basis of:

Functional knowledge to transact on their own

Awareness about terms and conditions and product features

Ability to protect personal account information

Awareness and ability to access recourse

Financial capability of the agents was assessed on the basis of:

Functional knowledge about terms and conditions and product features for proper facilitation

Functional knowledge about recourse mechanisms to help the customers as well as to resolve problems they face

Monitoring and training support so that agent is able to serve the clients well

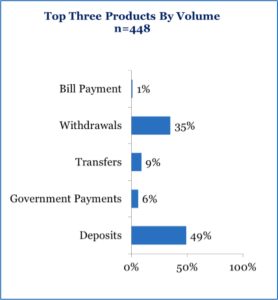

As indicated in a previous blog “Customer Protection in Indian Digital Financial Services (Part 2: Transparency and Privacy)”, almost 2/3rd of customers do not fully understand the product terms and conditions and pricing. Furthermore, knowledge about other products among agents is also low, and so they offer only a few products. The graph indicates the top three products offered by agents by volume.

Furthermore, field observations show that there is a growing trend amongst customers to carry out over the counter (OTC) transactions. These people are not covered in the study, but form a significant proportion of transaction volume. Since they conduct OTC transactions, it is fair to assume that they too have very limited knowledge of the terms and conditions of service.

Functional awareness among agents to facilitate transactions appears high. However, this does not represent the complete picture as they only have knowledge about a few products. MicroSave’s ANA India Survey highlights that only 59% of agents received training. Of those trained, 61% agents have undergone a refresher training. 36% of these have received refresher training only once.

In the MicroSave study for the Omidyar Network 96% of agents said that they knew about the product features of top three products on offer through their agency; 77% of agents said that they do not have any difficulty in handling the devices/technology; and only 68% of all active agents reported having received documents describing terms and conditions of service.

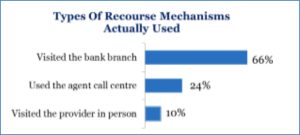

79% of the agents know about recourse options. However, of the agents who faced issues, only 24% actually used any kind of recourse option. Though agents were aware of multiple recourse options, the method actually used to resolve issues was much more traditional in nature ― agents preferred to sort out issues face to face at the branch.

This indicates that even though there is awareness about recourse options among agents, they are not used much. Moreover, the dependence on agents on going to the bank branch or provider for recourse suggests that call centres are either absent or not functioning adequately. This also raises a question on the ability of agents to resolve customer level issues if they do not have functional knowledge of recourse.

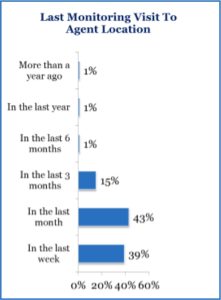

However, when asked what is discussed during monitoring visits, the answer was ambiguous both in terms of agenda and problem resolution.

A separate baseline assessment study conducted by MicroSave, for Bank Mitrs (agents) under the PMJDY scheme also highlights the fact that monitoring visits lack an agenda in terms of what needs to be checked, and often does not resolve any problems/issues that the agent/customer may be facing. At best, during monitoring visits, the bank staff checks the notebook of agents in which transaction records are maintained. There are almost no checks/interactions with customers during monitoring visits. This is primarily to avoid questions on unresolved issues like – When will they get their passbook? When will the ATM card be issued? Will they be able to access credit? etc.

Financial capability in terms of product knowledge and recourse is limited amongst agents and very limited amongst DFS customers in India. Furthermore, there is little sign that the sporadic agent monitoring visits are being used to address this problem. Providers and banks should view this as a big opportunity to both improve levels of trust in DFS and the range/uptake of products and services by the mass market. But, to achieve this, concerted efforts will be required to enhance the financial capability of both the agents and the customers they serve.

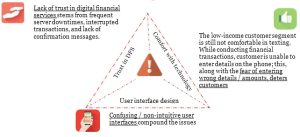

Qualitative research done as a part of MicroSave’s study for the Omidyar Network on customer production, risk and financial capability in India shows that customers’ perceptions of banking or financial transactions are still focused on brick and mortar based services. DFS providers have not done enough to change the customer’s perception and gain trust. The customer’s perception of risk of digital systems and technology can be further broken down into three broad issues.

1. Lack of trust in digital financial services arises from three key drivers:

a. Frequent server downtime: Many issues are clubbed here – including: bank server downtime; provider’s network downtime; failure or overload of the middleware linking the bank system to the provider’s system; and internet or GSMA outage. In addition, on occasions, the agent’s unwillingness (or inability due to lack of liquidity) to service the customer is covered by the agent with an assertion that “the system is down”.

b. Interrupted transactions: Often, while transacting, agents/customers face the problem of interrupted transactions. This can happen due to various technology challenges and often results in incomplete transactions.

c. Lack of confirmation messages: Lack of a confirmation message, or receipt, or any form of physical evidence of the transaction, causes anxiety amongst many customers.

2. The low-income customer segment is still not comfortable in texting for two reasons:

a. Unable to enter details: In the case of mobile delivery channel, many old and middle-aged customers are unable to type details on the phone.

b. Fear of entering wrong details: Customers do not want to conduct transactions (themselves) because they are afraid that they might enter wrong details, and thus lose money.

Customers’ low level of comfort with technology is exacerbated by often clunky user interfaces (see below) and often leads to agent-assisted transactions. Assisted transactions significantly increase the level of risk for the customer as they have to share their account details with the agent. Further, it also harms the service provider in the following ways:

• Increased risk of fraud and hence reputational risk

• Agents start behaving like middlemen, limiting the providers’ communication with clients; exposing the provider to the risk of customer poaching (if the agent is not satisfied with the service/commission given by a provider, he shifts to a different provider and also shifts the customers along with him), and limiting opportunities to cross-sell.

3. Confusing/non-intuitive user interfaces compound the issues

a. User interfaces are often confusing to the customer. The USSD interface is often too deeply layered or embedded for the customers to get to the right option. This forces the customer into risky behaviours like:

• Sharing PIN with the agent

• Leaving cash with the agent (especially when the system is down or alleged to be down)

• Leaving phones with agents to complete a transaction

b. Transaction data security relates to the privacy of customers’ account/PIN details while conducting transactions at agent locations. Poor transaction data security increases customers’ vulnerability to external frauds. Confusing interfaces and low comfort level with technology add further to poor transaction data security, as the customer is forced to share personal account details.

Two other issues further erode customers’ trust in digital finance in India:

1. Lack of liquidity at the agent is a multi-fold issue. For the customer, it means that their funds are inaccessible and service is denied. A customer who has been refused service by an agent is less likely to transact again at that agent location. Furthermore, loss of business reduces profitability and demotivates the agent, so he starts maintaining minimum (or less) liquidity – thus setting in motion a downward spiral.

2. The perception that funds held digitally are not safe. This stems from rumours which spread in the market from time to time. For example, in 2014, in response to government policy, agents were given a target of 100% withdrawal of government payments to receive their commission from the agent network managers. So, (unsurprisingly) agents communicated that customers must withdraw all their direct benefits immediately or the government would take back the amount left in the account.

These issues are very similar to the ones we found in Bangladesh, Uganda and (to a lesser extent) the Philippines (see graph below).

There are, however, important consequences of these issues and risks for DFS uptake and usage. Fears and perceptions suppress uptake and tarnish the reputation of DFS and its providers. Non users are often very aware of these issues. In the words of one customer, “We keep hearing mobile money users complain about unstable network, delayed service, missing money and many other negative comments about mobile money. Why then should we register for these services?”

There is strong evidence that poor customer service/protection is reducing not just uptake but also usage of DFS services. Many registered customers lapse into inactivity when they find it impossible (due to system downtime or absent/illiquid agents) or too scary (due to the risks of sending money to the wrong number or losing/compromising their PIN) to make transactions. Others choose to self-protect by using OTC services in preference to registering or keeping money in their m-wallets. These all limit the use of digital financial services. This was a repeated theme across the studies and reflects the findings of InterMedia’s work in eight leading markets across the globe. MicroSave’s recent work for UNCDF’s MM4P on the customer journey highlighted that, “Moving people from knowledge to trial, and from trial to regular usage, will require providers to address issues that erode trust: system instability, poor customer service; and improve access which is limited by current KYC requirements”.

System downtime and sending money to the wrong number, in particular, seem to damage the reputation of DFS service providers. Ironically, these technological issues can be addressed by providers themselves. Similarly, agent liquidity and overcharging can and should be addressed through effective monitoring by providers and their agent network managers. The future of DFS in India is in the hands the very people that provide these services.

Pradhan Mantri Jan Dhan Yojana (PMJDY) is now the world’s most successful financial inclusion scheme. This blog highlights the supply-side findings (specifically focused on Bank Mitrs (BMs) or bank agents) of the final round of MicroSave’s PMJDY assessment (Wave III) conducted in December 2015.

The BM network is the backbone of PMJDY scheme. The network of agents act as the arteries and veins of the Indian financial system that delivers technology-enabled financial services, at affordable cost, to otherwise inaccessible corners of India. The success or failure of the PMJDY scheme depends on the vibrancy of a network of more than 125,000 BMs spread across India. A typical BM is considered functional if he is available at the designated sub-service area location, equipped to serve transaction requests/queries of customers, earning a (sustainable) profit from operations, and has robust back-end support from link bank branches. This blog discusses these critical functional parameters of the BM network.

Are BMs available/accessible/transaction-ready?

Yes! PMJDY Wave III highlighted significant availability of BMs, i.e., BMs who are present at the stated location or could be traced to a nearby location. While 97% of the BMs were available, only 3% could not be traced, as they were neither present at their kiosk, nor could be contacted over the phone. Even the local residents could not identify/provide information about the latter. The survey highlights that 79% of the BMs are “transaction-ready”, i.e. BMs equipped to handle customers’ account opening/ withdrawal/deposit requests. BMs’ availability and their transaction-readiness has positively impacted customers’ trust of the PMJDY scheme. BMs were of the opinion that PMJDY scheme has led to greater women’s participation in financial inclusion. One BM from Jind district of Haryana says, “Many women save INR 50–500 (US$ 0.75–7.5) without their husbands knowing about it.” Our findings indicate that out of every three PMJDY customers opening a bank account for the first time, one is a woman. A BM from Bhadrak district of Odisha said “900 accounts out of 1,540 are of females. If it is convenient, we collect deposits from their houses.”

Does income from business match BM’s expectation?

No! There is a huge expectation mismatch between what a BM expects to earn (INR 13,000 (US$ 197) monthly) and what he actually earns (average monthly revenue/income is INR 4,692 (US$ 71)). At current income level, BMs are earning an average income of INR 188/day[1] (US$ 2.8), which is less than the income of an average MGNREGA worker, who earns INR 206 per dayday[2] (US$ 3). A BM from Ghazipur district of U.P. noted, “Our income is lesser than MGNREGA wages. I have received INR 3,500 (US$ 53) in the last 18 months. Can I sustain my family on this income?” BM profitability ranges between a monthly loss of INR 350 (US$ 5.3) to a monthly profit of INR 2,500 (US$ 37.7) depending on the type of commission model and investment made in the infrastructure.

BMs claim that the amount received as commission is not sufficient to cover operational costs, such as travel to link branches, stationery, rent, and connectivity. The fact is corroborated by MicroSave analysis, which reveals that an average BM incurs a monthly operational cost in the range of INR 2,600-3,300 (US$ 39-50). Additionally, BMs have no clarity on the commission structure. BMs receive a lump sum amount in their account, without any break-up to explain the commission paid to the agent. This leaves them unsure of the relationship between monthly transactions performed to the commission earned, and unable to keep track of their monthly earnings from the business. A few BMs also report not having received any commission for the last three to six months. The irregularity and low commission payment has direct impact on service to PMJDY customers due to increased BM dormancy/churn, and low level of investment (liquidity).

BMs’ dormancy (i.e., BMs who have abandoned their role as a BM and have stopped offering financial services) stands at 10%. At 10% dormancy level, it is estimated that a total of 12,595 BMs[4] across India. Further, an additional 2% BMs have stated that they plan to exit the business in the next two months, owing to inadequate commission, poor support from the bank or agent network manager, and lack of business potential. This may add another 2,519 BMs to the total dormant BM numbers in India and cut off approximately 2.4 million PMJDY customers from mainstream banking. In addition to this, PMJDY survey reveals that around 6% of the active BMs are not conducting any transactions and it is highly probable that they may become dormant if immediate steps are not taken to improve their business profitability.

If it’s a no-profit business, why BMs are still continuing the operations?

Surprisingly, despite challenges, most BMs continue with the business and hope that the situation will improve in future. A BM from Ferozpur, Punjab, noted: “The bank may recruit us as staff, if we continue to perform better.” The perception that work as a BC will lead to full-time job opportunity with the bank led many to join as agents. At times, we also observed banks taking undue advantage of this false expectation of BMs, by asking them to assist in their day-to-day activities.

BMs also cite reasons such as better standing in society as a result of their BM status; and also feeling accountable to the customers for whom they opened accounts/from whom they have taken savings, as reasons for continuing in the role. A BM in Bhadrak district of Odisha stated, “I get a lot of respect wherever I go”.

However, only 37% of the BMs surveyed have additional businesses/occupations (such as photocopy machines, general stores, and/or insurance agent, etc.), indicating that they are not solely dependent on the uncertain income from BM operations. This gives them an important cushion. Worldwide, the agent network surveys performed by MicroSave’s The Helix Institute are showing an increasing trend of agents to be “non-dedicated” – i.e. running the agency business alongside another core business. Even in Kenya, in 2014 64% of agents were non-dedicated – up from 54% a year earlier.

Is BM’s sustainability the only concern?

No! There are other issues as well!! A BM from Jind district in Haryana pointed out: “I have enrolled for the Rs 330 (US$ 5) insurance, but no amount has been deducted from my account. I am not aware where to approach if an accident were to happen?” The survey highlights that many BMs are unaware and untrained about the full benefits and process details, such as insurance premium deposit and claim settlement. BMs reported that they did not receive product details from link branches but, instead, gather information through advertorials in television and newspapers. They mentioned feeling helplessness in the face of customer queries, such as status of activation of an insurance policy, premium deduction, process and documentation of claim submission, etc. BMs noted that a major challenge that they face is the absence of proper documentation which should be received by a customer taking out an insurance policy. BMs reported providing the stub of the insurance form as ‘acknowledgement slip’ only if customers asked for it; otherwise, no proof/documentation was given to customers.

And, finally, what about link branch support?

A BM from Ferozpur district of Punjab noted: “We are called Bank Mitrs, but link branches don’t accept us as one”. BM business and performance improves with better quality support from link bank branch staff. On a day-to-day basis, a BM needs regular support from bank branch staff for a variety of aspects of the business, such as account approval at the back-end, resolving technical challenges, connectivity-related issues pertaining to point of sale (POS), and liquidity management. BMs with better branch support showed higher customer footfall. As one BM from Dadra & Nagar Haveli said, “If the branch manager is good, then everything is good”. Interestingly, only 63% of active BMs were satisfied with the support they got from staff at the link branch, while 18% BMs were dissatisfied.

MicroSave’s qualitative analysis reveals that, on an average, a bank branch managed 2 BMs and approximately 2,000 PMJDY customers. Assuming 10% of PMJDY customers approach the bank branch for their day-to-day non-financial /financial transaction – bank branches need an additional 34 man-hours to successfully address these additional customers. The lack of support that BMs received from branch staff can thus also be attributed to the bandwidth limitations prevalent in rural branches.

The Surveys: Background, Samples and a Technical Caveat

MicroSave conducted three rounds of PMJDY assessments (Waves I, II and III) from October 2014 to December 2015, to analyse the impact of and challenges associated with PMJDY, both for beneficiaries and channel partners. MicroSaveconducted the study with funding support from the Bill & Melinda Gates Foundation (BMGF) and presented the findings to the Department of Financial Services, Ministry of Finance, Government of India.

It is important to note here that Wave III incorporated a nationally representative survey conducted with 1,627 BMs and 4,859 PMJDY account holders, in a total of 42 districts across 17 states and one Union Territory. The survey results of PMJDY Wave III are not strictly statistically comparable with PMJDY Wave I and II surveys, due to difference in sample frames. The comparisons presented in the blog are for the purpose of convenience and are indicative in nature.

[4] On an average, a BM handles 949 PMJDY customers: PMJDY Wave III findings. Therefore 12,595 dormant BMs multiplied by 949 gives us a total of approximately 12 million PMJDY customers who are not being served

In the first part of this blog, we discussed the demand-side findings of PMJDY Wave III survey conducted by MicroSave in December 2015. The blog highlights the positive impact of the PMJDY scheme on the financial behaviour of rural customers. Rural customers, including women, have enthusiastically contributed to the success of the scheme and have started to make small savings in these accounts. This blog presents the other side of the coin and highlights some of the areas where things are not working quite as well.[1]

1. Expectation mismatch because of low awareness on ‘Jan Suraksha’ scheme

Despite their success, the PMJDY schemes (PMJJBY, PMSBY, and APY) have not been able to build required trust among customers. The low trust can mostly be attributed to low scheme awareness (among customers and Bank Mitrs (BMs)) and process inefficiencies. “Customers visited my place to claim money for natural death as they were unaware that the claim can only be made for accidental cases,” said a BM in Vidisha district of MP. BMs report of difficulty in getting customers to sign up for schemes, since customers are not sure whether these schemes would continue beyond the current government, and also whether the claim would be settled successfully. A customer in Odisha raised his doubts: “I have enrolled for INR 330 [US$4.85] insurance, but no amount has been deducted from my account. Where will we go if an accident happens now?”

Miscommunication of the Overdraft.[2] (OD) facility as “free money” has been one of the motivations to open PMJDY accounts. Customers did not perceive OD to be a credit product and enthusiastically opened bank accounts to ‘receive’ INR 5,000 (US$ 73). A BM in Ghazipur district of Uttar Pradesh said: “Around 50% of the accounts have been opened with the intention of receiving ‘free money’ of INR 5,000.” BMs report that such customers do not want to take the OD when they realise that they have to repay the amount with interest.

On the other hand, banks are reluctant to provide OD to customers presumably because the perception is that these will turn into non-performing assets. BMs reported submitting OD documents to the bank branch and not receiving any information thereafter.

2. Mismatched expectations has led to account duplication and dormancy

Customer dormancy, i.e., the number of PMJDY accounts where no transactions have been conducted in the last three months, stands at 28%. The high level of customer dormancy can be attributed to reasons such as lack of customer awareness (misconception that PMJDY account is a must to avail of government benefits) and false expectation of receiving free money (overdraft) in bank accounts. Of the total customers interviewed during Wave III surveys, 67% reported that PMJDY is their first formal bank account.

However, it is important to note that 33% of the PMJDY customers reported having alternate bank accounts (other than PMJDY account) and 31% of such customers actively use their alternate account. A significant portion of overall PMJDY account dormancy can also be attributed to these customers, who open multiple accounts just to avail benefits of facilities such as OD and insurance.

3. Low pace of Aadhaar seeding and RuPay Card distribution

The rate of RuPay card distribution (47%) and Aadhaar seeding (62%) is slow. Only 33% of the PMJDY customers are “RuPay transaction-ready” (i.e., customers who carry activated RuPay cards) and only 26% of the customers have ever used their RuPay card.

PMJDY customers who have received RuPay card as well as PIN, find it difficult to activate the RuPay cards and to use it continuously. Only 24% of BMs have RuPay card-enabled devices; most customers have to visit the nearest ATMs to activate their RuPay cards and to change personal identification numbers (PINs). Since first-time activation happens at the issuing bank terminals/ATMs, PMJDY customers find it cumbersome, owing to unavailability of ATMs in the vicinity; this leads to RuPay card turning dormant. BMs report that risks (fraud/misuse of RuPay card by relatives) associated with the card also demotivates PMJDY customers from maintaining active RuPay cards.

4. Unfair charges/practices may reduce customer’s trust in PMJDY

PMJDY scheme was launched with the intent of financially including the otherwise traditionally excluded customer segments. Since these customers lack experience of transacting on formal financial channels, they are susceptible to risks such as overcharging or unfair practices by BM, bank staff and/or BCNM. A few BMs in Vidisha, MP, stated that customers were charged for all withdrawal as well as deposit transactions in their PMJDY accounts. The branch had not provided any plausible explanation for these charges, even after multiple complaints by the BM and customers. Deductions from these accounts have reduced their trust in formal financial channels.

A bank in Mahasamund, Chhattisgarh, provided PMSBY to MGNREGA account holders by debiting INR 12 from their wage payments without the customers’ prior consent. Some of these customers had already enrolled for PMSBY and lost money on the same scheme. One of the leading banks, in its attempt to tackle zero-balance accounts, deposited INR 10 in each zero-balance account, and the BM was asked to put another INR 2 from his/her commissions. This process disappointed most BMs associated with the bank.

[1]Survey results of PMJDY Wave III are not strictly speaking statistically comparable with PMJDY Wave I and II surveys, due to differences in sample frames. The comparisons presented in the blog are for the purpose of convenience and are indicative in nature.

[2] Overdraft facility is a general purpose loan to provide hassle-free credit of up to INR 5,000 to low-income group / underprivileged customers.

Pradhan Mantri Jan Dhan Yojana (PMJDY) is now the world’s most successful financial inclusion scheme. The scheme envisages universal access to banking facilities with at least one bank account for every household, in addition to access to credit, insurance, and pension facilities. As of March 15, 2016, the scheme has mobilised approximately INR 335 billion (US$ 4.9 billion) through 210 million new bank accounts ― a significant achievement, considering that the scheme was launched on August 28, 2014.

MicroSave conducted three rounds of PMJDY assessments (waves I, II and III) from October 2014 to December 2015. The key aim of the three assessments was to analyse and assess the impact of, and challenges associated with, PMJDY from the perspective of beneficiaries and channel partners (specifically Bank Mitrs (BMs) or agents). The study was conducted with support from the Bill & Melinda Gates Foundation (BMGF) and the results were shared with the Department of Financial Services, Ministry of Finance, Government of India.

This blog highlights the demand-side findings of the final round of PMJDY assessment (Wave III), conducted in December 2015. Wave III incorporated a nationally representative survey, conducted with 1,627 BMs and 4,859 PMJDY account holders, in 42 districts across 17 states and one Union Territory.

1. Acceptance of PMJDY scheme has increased

Pinki, a PMJDY customer in Khadoli village of Dadra and Nagar Haveli, summarised: “Jan means poor people and dhan means money.

Therefore, jan-dhan means wealth of the poor”. Pinki summarises the top-of-the-mind perception customers have about PMJDY scheme. PMJDY is positioned in customers’ minds as a useful government scheme that provides low-cost insurance facility and an opportunity to open a bank account for free.

PMJDY has led to universalisation of accounts and provided easily accessible banking to customers in their neighbourhood. Most PMJDY customers (78%) use BM to make their regular financial transactions. A BM in Ghazipur, Uttar Pradesh, said, “The number of bank accounts have increased from 15 to 500 in the village. Villagers have understood banking.”

80% of PMJDY customers who regularly transact, ranked Bank Mitr agents as their first preference to conduct banking transactions. The main reasons for this are: proximity of the BM location to their home and work place; quick and convenient processes; and availability of BMs beyond bank working hours.[1]

PMJDY scheme has also led to inclusion of women in the financial mainstream. For every three PMJDY customers who opened a bank account for the first time,[2] one was a female customer.“900 accounts out of 1,540 are of females. If it is convenient, we collect deposits from their houses”, said a BM in Bhadrak, Odisha

2. Saving behaviour has been induced among rural customers

There is significant shift in savings behaviour of PMJDY customers; the percentage of those who do not save has come down from 12% in Wave II to 8% in Wave III . Similarly, the number of customers who save at home has gone down (21% in Wave II to 17% in Wave III). These customers have started to use their own savings account to save (up from 77% in Wave II to 86% in Wave III). Additionally, there is a small increment in number of customer transactions per month from last wave of PMJDY survey. A total of 65% of customers transact at least once in a month at a BM location, compared to 58% in Wave II. A recent study in rural households of Karnataka highlights that PMJDY has led to significant increase in total household savings and savings in bank accounts.

“Non-skilled labourers have greatly benefited. They save out of their daily wage income” – BM, Ghazipur, U.P.

3. Product uptake is not only limited to savings

PMJDY has helped improve uptake of financial products; customers have enthusiastically enrolled for PMJDY life and accident insurance policies due to the value proposition that they offer and the low cost. These schemes are popularly known as “12 aur 330 rupaya wala bima” (i.e., insurance for INR 12 (PMSBY) and INR 330 (PMJJBY))

By paying a nominal premium of INR 12 (US$ 0.18) per person per year, PMJDY account holders can avail of an accidental insurance scheme under the Pradhan Mantri Suraksha Bima Yojana (PMSBY) with a maximum insurance cover of INR 200,000 (US$ 3,077) in case of accidental death or permanent disability. For a premium of INR 330 (US$ 5.1), a PMJDY account holder can avail life insurance cover of INR 200,000 (US$ 3,077) under the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY). Another interesting product available for Jan Dhan account holders is Atal Pension Yojana (APY), specially designed to cater to pension needs of the unorganised sector. See Jansuraksha: India’s New Tryst with Mass Insurance for more details of these schemes.

The number of customers who have either enrolled for insurance or pension scheme has increased to 56% from 43% in Wave II. A PMJDY customer from Sonitpur district of Assam said “I am fine now but that may not be the case later. INR 50 is spent on tea and snacks, so spending INR 330 for such a nice insurance facility is not a problem.” The uptake of accident insurance scheme (60%) among surveyed PMJDY customers is higher than for life insurance (49%) and pension scheme (6%).

Life insurance scheme is found to be popular among female customers, as women feel that there are less likely to be involved in accidents as compared to male members. On the other hand, pension scheme has been popular among literate and relatively higher-income customers. Low-income customers find this scheme costlier (INR 504 or US$ 7.52). They also find it burdensome to make regular monthly contribution over a long period. Further, customers who are receiving old age pension under National Social Assistance Programme (NSAP) do not want to pay for another pension scheme.

[1] Multiple responses received from customers for this question

[2] 3,273 out of a total 4,859 PMJDY customers interviewed have PMJDY as first and only account

[3] Survey results of PMJDY Wave-III are not strictly-speaking statistically comparable with PMJDY Wave-I and II surveys due to differences in sample frames. The comparisons presented in the blog are for the purpose of convenience and are indicative in nature.

Pradhan Mantri Jan Dhan Yojana (PMJDY) is now the world’s most successful financial inclusion scheme to provide access to savings accounts, credit, remittance, insurance and pensions, to the financially excluded of India. MicroSave conducted three rounds of assessments of PMJDY scheme between October 2014 and December 2015. The detailed analysis of data on Bank Mitrs (BMs) and PMJDY customers revealed bottlenecks prevalent in PMJDY scheme at both policy and operational levels. This IFN presents key policy and operational interventions that need to be addressed to improve the overall scheme effectiveness, enhance the usage of PMJDY accounts and improve the sustainability of the BM channel.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.